Container As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 23.35 Billion |

| Growth Rate (2026 - 2031) | 31.10% CAGR |

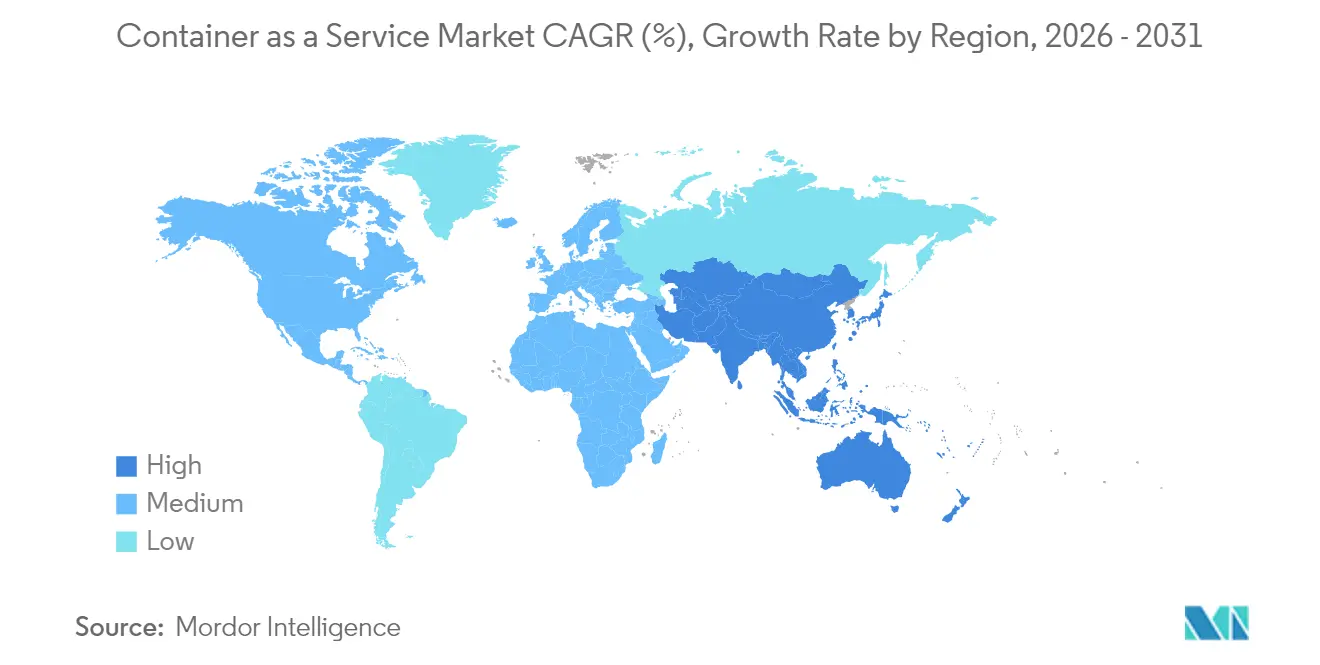

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

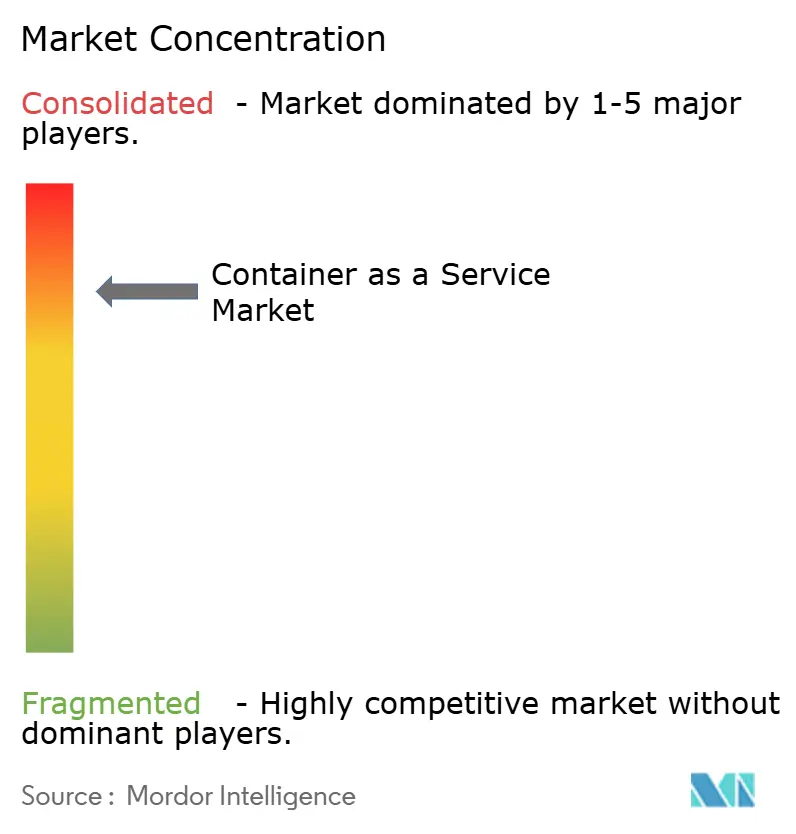

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Container As A Service Market Analysis by Mordor Intelligence

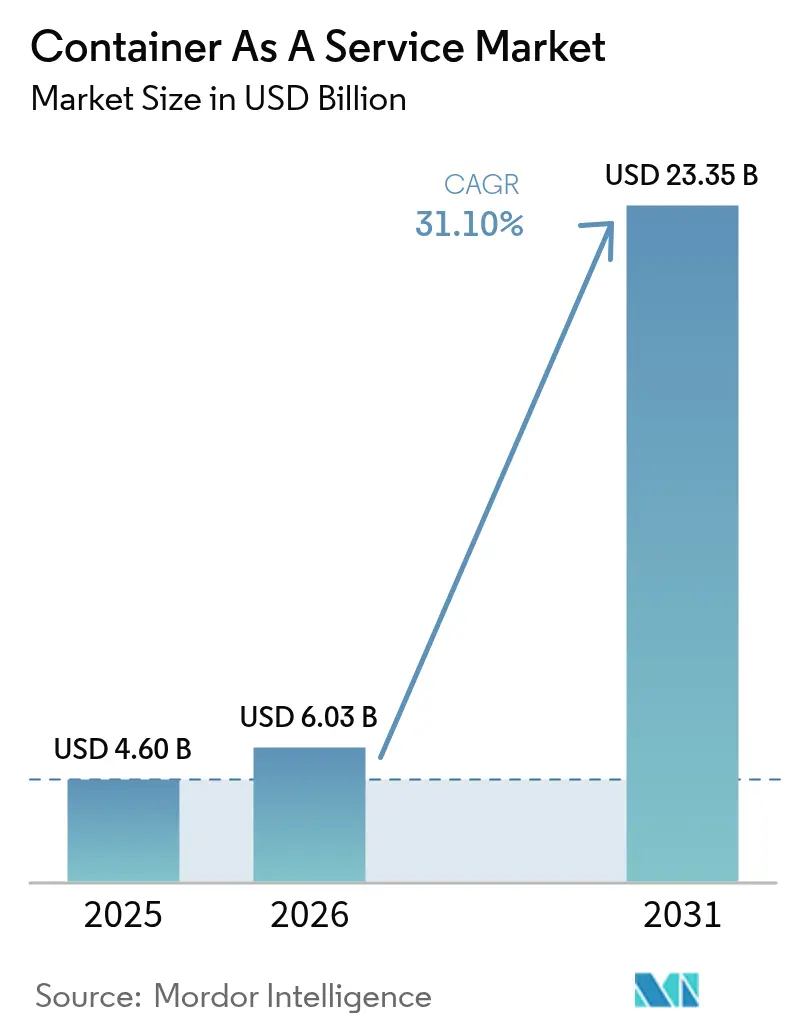

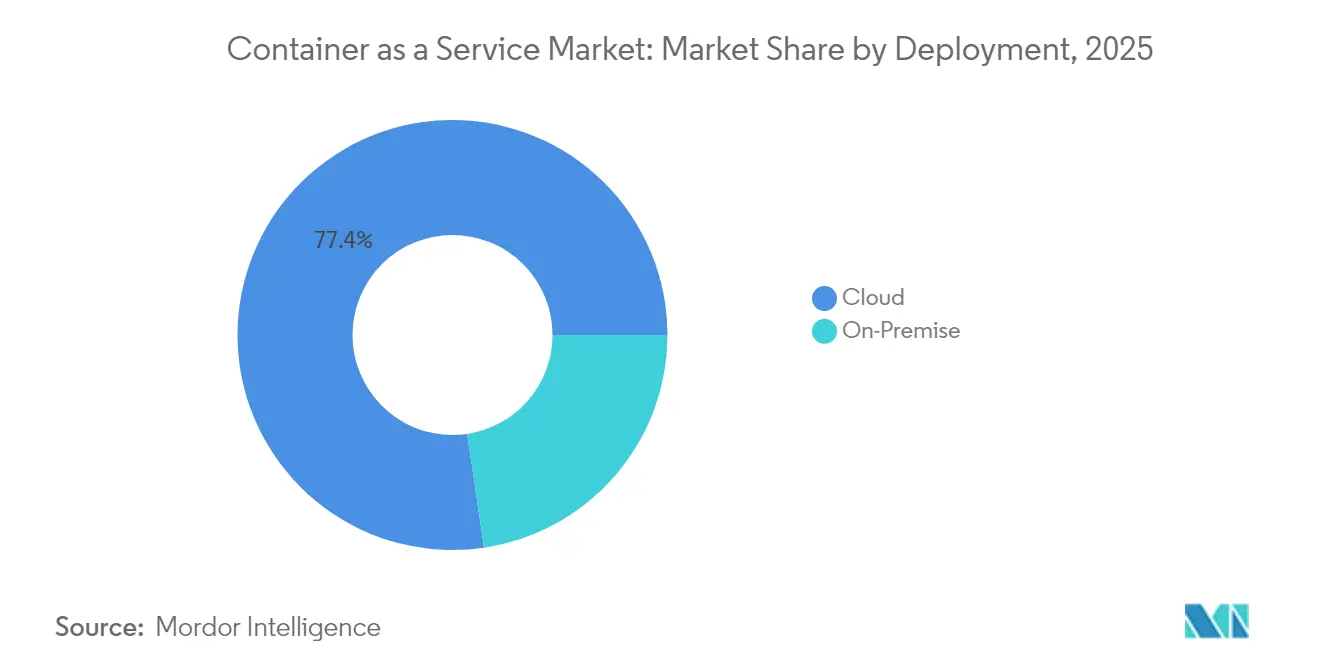

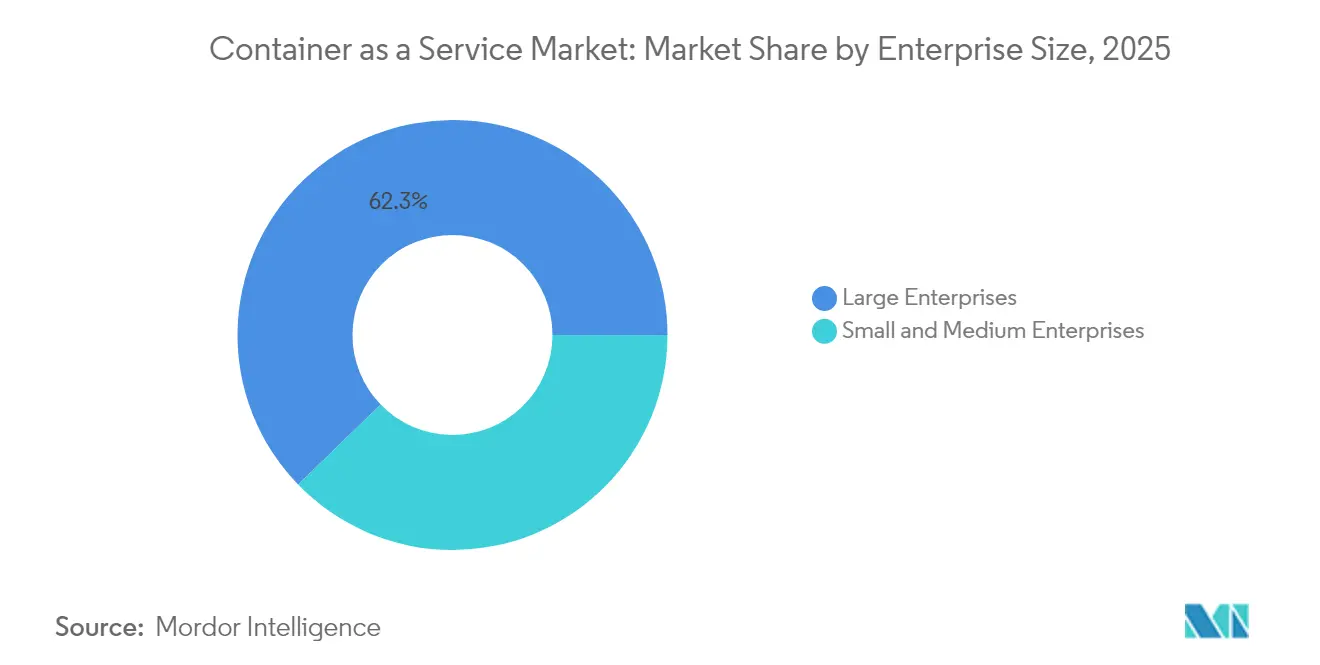

The Container-as-a-Service market size is expected to grow from USD 4.6 billion in 2025 to USD 6.03 billion in 2026 and is forecast to reach USD 23.35 billion by 2031 at 31.1% CAGR over 2026-2031. Strong demand for cloud-native agility, rising multi-cloud strategies and granular resource allocation are reshaping enterprise infrastructure decisions. Sovereign-cloud directives in Asia-Pacific and Europe, together with mandatory software bill of materials (SBOM) rules, are widening adoption beyond classic lift-and-shift migrations. Cloud deployment still represents 78% of revenue, but on-premise deployment is accelerating at a 34% CAGR as regulated industries embrace hybrid models. Managed services, which hold 54% share, are taking on security scanning and compliance automation tasks once handled internally. Small and medium enterprises now form the fastest-growing customer group, reflecting the appeal of pay-per-use billing and low entry costs. Manufacturing is the leading growth vertical, leveraging lightweight orchestration to operate AI-enabled edge workloads that support Industry 4.0 initiatives.[1]Red Hat, “Boosting Manufacturing Efficiency and Product Quality with AI/ML, Edge Computing and Kubernetes,” redhat.com

Key Report Takeaways

- By deployment, cloud held 77.35% of the Container-as-a-Service market share in 2025; on-premise is projected to expand at a 33.55% CAGR to 2031.

- By service type, managed services commanded 53.35% share of the Container-as-a-Service market size in 2025 and are set to advance at a 33.9% CAGR through 2031.

- By enterprise size, large enterprises accounted for 62.25% revenue share in 2025, while SMEs are growing fastest at a 35.85% CAGR.

- By end-user application, manufacturing captured 37.55% of Container-as-a-Service market size for new bookings in 2025 and is forecast to progress at a 37.6% CAGR between 2026-2031.

- By geography, North America led with 38.05% Container-as-a-Service market share in 2025; Asia-Pacific is expected to post the highest CAGR of 38.7% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Container As A Service Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-agnostic Kubernetes platforms avert lock-in | +8.5% | Global, stronger in North America and EU | Medium term (2-4 years) |

| Pay-per-use transparency grows SME adoption | +6.2% | Global, strong in APAC emerging markets | Short term (≤2 years) |

| DevSecOps SBOM mandates accelerate managed CaaS | +4.8% | North America and EU | Short term (≤2 years) |

| AI/ML GPU-ready clusters surge | +7.1% | Global, concentrated in tech hubs | Medium term (2-4 years) |

| 5G edge micro-DC roll-outs need lightweight CaaS | +3.9% | APAC core, spill-over to North America | Long term (≥4 years) |

| Sovereign-cloud mandates spur domestic CaaS | +2.8% | APAC and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-agnostic Kubernetes Platforms Avert Lock-in

Enterprises increasingly deploy cloud-agnostic orchestration to avoid vendor dependency and negotiate favorable pricing. Platforms that run identical clusters across providers simplify workload portability and reduce migration downtime by 77% in stateful microservices tests. Vendors such as HPE integrate virtual machines and containers within one control plane, strengthening hybrid strategies.[2]HPE Community, “The Next Wave of Virtualization Is Containerized,” community.hpe.com

Pay-per-use Transparency Grows SME Adoption

Consumption pricing eliminates capital expenditure barriers for smaller firms. AWS Fargate and EKS cost-visibility tools help SMEs deploy production clusters without dedicated DevOps teams.[3]Sedai, “Understanding AWS EKS Kubernetes Pricing and Costs,” sedai.io Automated rightsizing and spot-instance use further align expenses with fluctuating traffic, supporting the 36.7% CAGR recorded for SMEs.

DevSecOps SBOM Mandates Accelerate Managed CaaS

Regulators now require detailed component inventories, prompting firms to outsource container security. Managed platforms embed SLSA frameworks, automating provenance tracking and vulnerability scanning. CycloneDX xBOM covers cryptography and ML artifacts, demanding skills many enterprises lack.[4]Security Boulevard, “What Is the xBOM?” securityboulevard.com

AI/ML GPU-ready Clusters Surge

AI workloads intensify demand for orchestration that schedules GPUs efficiently. Research shows optimized scheduling cuts CPU overhead by 1.5% while boosting request handling by 32.4%. Manufacturing pilots on Red Hat OpenShift prove real-time analytics can improve product quality and predictive maintenance.

Restraints Impact Analysis of Container As A Service Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified K8s operators | -4.2% | Global, acute in emerging markets | Short term (≤2 years) |

| Kernel-level escape and eBPF attack vectors | -3.1% | Global, heightened in regulated industries | Medium term (2-4 years) |

| Unpredictable cloud egress fees | -2.8% | Global | Short term (≤2 years) |

| Fragmented observability licensing costs | -1.9% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified K8s Operators

The talent gap delays deployments and raises operating risk. Enterprises in emerging markets often rely on costly consultants, lengthening project timelines. Training pipelines have yet to match demand for service-mesh, GitOps and edge cluster skills.

Kernel-level Escape and eBPF Attack Vectors

Notable exploits such as CVE-2023-5528 illustrate how malicious YAML files can gain SYSTEM privileges, expanding the threat surface. Confidential-computing solutions and stricter runtime sandboxing are gaining traction in financial services to mitigate these risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Container As A Service Market Segment Analysis

By Deployment:

Hybrid Strategies Drive On-Premise AccelerationOn-premise clusters are forecast to grow at a 33.55% CAGR even though cloud maintains dominant share. This reflects compliance needs, local-processing latency advantages and a desire to modernize existing hardware rather than relocate every workload. HPE GreenLake offers consumption-based private-cloud pricing that mirrors public-cloud economics, demonstrating how suppliers adapt to hybrid demand.

Organizations usually run development and bursting workloads in the cloud while retaining latency-sensitive or regulated applications on-site. The Container-as-a-Service market supports seamless workload migration through unified control planes, allowing teams to shift containers in response to performance or sovereignty requirements. As hybrid maturity rises, placement decisions hinge on measurable cost and compliance variables rather than a default cloud-first stance.

By Service Type:

Managed Services Maintain Growth LeadershipManaged offerings hold 53.35% share and are expanding at 33.9% CAGR as enterprises offload day-two operations. Providers integrate AI-driven resource tuning and automated patching, ensuring uptime while lowering internal headcount needs. T-Mobile adopted a managed Red Hat OpenShift stack for telco cloud functions, validating the approach for mission-critical 5G workloads.

Professional services remain essential for migrations and complex integrations, but revenue is episodic. Over time, recurring managed contracts outpace project work. The Container-as-a-Service market reflects this shift as new features—SBOM automation, supply-chain security and FinOps dashboards—are bundled into subscription tiers that deliver measurable outcomes.

By Enterprise Size:

SMEs Challenge Traditional Adoption PatternsLarge enterprises currently control 62.25% revenue, but SMEs are expanding faster because pay-per-use models avoid capital lock-in. Consumption billing, serverless container options and click-through user interfaces reduce the expertise barrier. This democratizes advanced orchestration while fueling 35.85% CAGR among SMEs.

Larger organizations still drive the highest absolute spend, requiring multi-cluster governance, role-based access control and integration with complex IT workflows. Yet SME momentum shapes the product roadmap, nudging vendors toward simplified experiences instead of bespoke customization. The Container-as-a-Service industry therefore spans both streamlined entry-level plans and enterprise-grade control planes.

By End-user Application:

Manufacturing Leads Digital TransformationManufacturing recorded a 37.6% CAGR, overtaking IT and telecom as the lead growth vertical. Real-time analytics, predictive maintenance and autonomous robotics need low-latency edge processing, and containers deliver consistent deployment from factory floor to central cloud. The MHI Industry Report found 55% of manufacturers increasing technology budgets, and case studies report USD 4.2 million annual savings after AI and robotics rollouts.

Meanwhile, IT and telecom retains the largest installed base but shows slower growth as adoption matures. BFSI, retail and healthcare steadily expand, supported by confidential computing and compliance features that container platforms now embed.

Geography Analysis

North America Container As A Service Market

North America earns 38.05% of 2025 revenue, benefitting from established hyperscale ecosystems and aggressive enterprise modernization. Major providers posted double-digit cloud revenue growth in 2025, reinforcing regional dominance. Skills shortages in Kubernetes operations, however, are creating a drag that fuels demand for managed services.

APAC Container As A Service Market

Asia-Pacific is forecast to grow at 38.7% CAGR, the fastest worldwide, due to sovereign-cloud rules and state-funded AI infrastructure. India allocated USD 1.3 billion for compute capacity, including 10,000 GPUs earmarked for public-private AI clusters. China’s ecosystem, led by Alibaba Cloud, Tencent Cloud and Huawei Cloud, is expanding hybrid-cloud deployments, with Huawei Cloud Stack reporting 106% revenue growth in emerging Asia-Pacific markets.

Europe Container As A Service Market

Europe faces distinctive dynamics under the EU Data Act, effective September 2025, which mandates cloud portability and removes switching fees by 2027. Providers with genuinely cloud-agnostic architectures appear better positioned, while sovereignty clauses are likely to spur regional CaaS platforms. Germany, France and the United Kingdom lead adoption, but regulatory complexity could slow purchase cycles until certification schemes settle.

Competitive Landscape

The top three hyperscalers—AWS, Microsoft Azure and Google Cloud—collectively account for 63% of 2025 revenue, but pressure from specialist vendors and edge requirements is rising. IBM’s USD 6.4 billion purchase of HashiCorp bolsters multi-cloud automation, and its planned DataStax acquisition would extend capabilities into real-time vector databases, crucial for AI pipelines. Patent filings covering encrypted orchestration and AI-based cluster management strengthen IBM’s hybrid-cloud moat.

Edge-focused upstarts target resource-constrained environments that hyperscalers cannot serve economically. Red Hat OpenShift Virtualization provides a migration path away from VMware following Broadcom’s acquisition, while HPE GreenLake offers on-prem consumption pricing that mirrors cloud economics. Providers that document measurable cost savings, performance gains and compliance automation are gaining share as procurement teams shift from feature comparisons to business-outcome metrics.

Container As A Service Industry Leaders

Amazon Web Services, Inc.

Google LLC (Google Cloud)

Cisco Systems, Inc.

IBM Corporation

Microsoft Corporation (Microsoft Azure)

- *Disclaimer: Major Players sorted in no particular order

Container As A Service Market Companies Covered in this Report

- Amazon Web Services

- Microsoft Azure

- Google Cloud (GKE)

- IBM Corp (Red Hat OpenShift)

- Alibaba Cloud

- VMware Tanzu

- Cisco Systems

- SUSE Rancher

- Oracle Container Engine

- Hewlett Packard Enterprise (Ezmeral)

- Mirantis

- D2iQ

- Platform9 Systems

- Akamai (Linode)

- DigitalOcean

- Rackspace Technology

- Nutanix

- Canonical

- HashiCorp

- Huawei Cloud

- Tencent Cloud

- OVHCloud

Recent Industry Developments in Container As A Service Market

- May 2025: AWS reported USD 29.3 billion Q1 cloud revenue and unveiled USD 105 billion capital spending plans focused on AI infrastructure.

- March 2025: Microsoft’s Intelligent Cloud revenue reached USD 26.8 billion in Q1, with Azure unveiling extended AI workload support.

- February 2025: T-Mobile selected Red Hat OpenShift Platform Plus to underpin its nationwide telco cloud.

- January 2025: IBM closed its USD 6.4 billion HashiCorp acquisition and announced its intent to acquire DataStax, expanding its automation and data portfolio.

Container As A Service Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the Container-as-a-Service (CaaS) market as all commercially offered public, private, or hybrid cloud services that let development or IT teams package, deploy, orchestrate, scale, and retire container workloads through an API, CLI, or web console and pay either per node minute or through a managed subscription.

Scope Exclusion: Solutions that only sell container runtime libraries or proprietary DevOps stacks used solely inside a provider's own operations are excluded.

Segments Covered in This Report

- By Deployment

- Cloud

- On-Premise

- By Service Type

- Managed Services

- Professional Services

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Application

- BFSI

- Retail

- IT and Telecommunications

- Manufacturing

- Healthcare

- Government

- Others (Media, Gaming, EdTech)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with cloud architects, managed-service operators, and procurement leads across North America, Europe, and Asia-Pacific helped us validate typical node densities, average service mark-ups, and emerging edge-CaaS use cases. Short surveys of SME DevOps heads confirmed adoption inflection points and discount schedules used to tune growth assumptions.

Desk Research

We first pulled baseline utilization and pricing signals from open datasets such as the Cloud Native Computing Foundation DevStats repository, the annual Flexera "State of the Cloud" survey, Eurostat ICT cloud-adoption tables, and NIST cloud reference material, which ground the model's service definitions. Additional context on hyperscaler billing trends and enterprise shift-to-cloud ratios came from SEC 10-K filings, investor days, and earnings transcripts. To size spend at the supplier end, analysts mined import shipment data for container-optimized server SKUs using Volza, skimmed Kubernetes project dependency counts on GitHub, and reviewed regional IT contract awards on Tenders Info. Financial sanity checks for leading vendors were supported by D&B Hoovers. The sources listed are illustrative only; many further public and subscription databases informed the evidence base.

Market-Sizing & Forecasting

A top-down demand pool is built from enterprise cloud spend by region, adjusted for container workload penetration and average CaaS price per compute hour, which are then cross-checked with selective bottom-up supplier roll-ups drawn from channel checks. Key variables feeding the model include Kubernetes penetration in production clusters, microservice share of new application builds, managed node tariff curves, edge cluster shipments, and container security spend ratios. Multivariate regression, informed by primary-research consensus on workload elasticity, projects each driver to 2030, and scenario analysis stress-tests high-growth regions. Data gaps on private-cloud volumes are bridged through ratio proxies derived from CNCF membership surveys.

Data Validation & Update Cycle

Outputs pass a three-step analyst peer review, anomaly flags trigger re-contact with select respondents, and variance beyond +/-5% versus quarterly earnings references demands model reruns. Mordor analysts refresh the file annually and issue interim updates when material vendor pricing or regulatory changes surface.

How Mordor Intelligence's Container As A Service Market Size Compares to Other Published Estimates

Published figures often differ because firms mix serverless units with CaaS or freeze exchange rates months before release.

Our study aligns scope strictly to managed container hosting, applies live currency conversion, and refreshes variables every twelve months. Others may extrapolate vendor press statements without triangulating real usage hours or verifying node-price erosion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.60 B (2025) | Mordor Intelligence | - |

| USD 6.62 B (2025) | Global Consultancy A | Includes container security tools and ignores regional price variance |

| USD 5.6 B (2027) | Industry Journal B | Uses 2022 base year FX rates and projects at flat margin assumptions |

In sum, Mordor's disciplined scoping, multi-source validation, and rolling update cadence deliver a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps, ensuring confidence when planning investments in container platforms.

Key Questions Answered in the Report

What is driving the fast growth of the Container-as-a-Service market?

Rapid adoption of cloud-native architectures, sovereign-cloud mandates and pay-per-use billing models are pushing the market toward a 31.1% CAGR through 2031.

Why are on-premise deployments still expanding?

Regulated industries need data control and low-latency processing; hybrid models integrate on-prem clusters with public cloud to meet those needs without losing flexibility.

How are SBOM regulations influencing purchasing decisions?

Enterprises increasingly select managed CaaS platforms that embed automated SBOM generation and vulnerability scanning to satisfy new compliance rules.

Which region will grow fastest over the next five years?

Asia-Pacific is projected to post a 38.7% CAGR, buoyed by government digitization projects and strict data-sovereignty requirements favoring domestic providers.

What skills are in shortest supply for successful container operations?

Certified Kubernetes operators with expertise in multi-cluster management, service mesh integration and security hardening remain scarce worldwide.

How concentrated is the competitive landscape?

The market shows moderate concentration: the top three hyperscalers hold 63% share, but specialist and edge-focused vendors are steadily eroding incumbent dominance.

Page last updated on: