Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Construction Robots Market Report is Segmented by Robot Type (Demolition Robots, 3D Printing Robots, and More), Automation Level (Semi-Autonomous, and Fully Autonomous), Function (Demolition, Masonry and Bricklaying, and More), End-Use (Commercial Buildings, Residential Buildings, Public Infrastructure, and Industrial and Energy Facilities), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

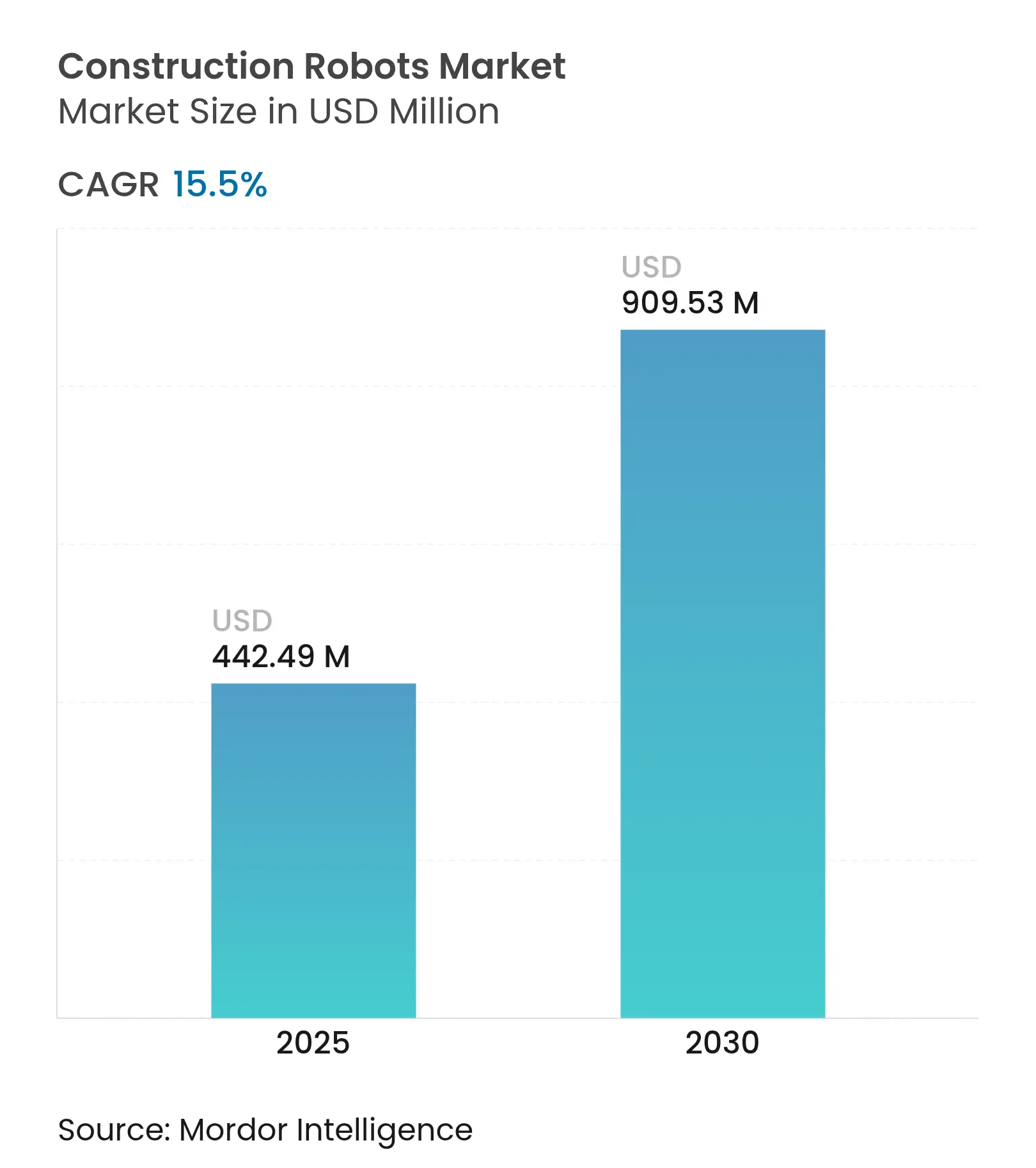

| Market Size (2025) | USD 442.49 Million |

| Market Size (2030) | USD 909.53 Million |

| Growth Rate (2025 - 2030) | 15.50 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The construction robots market size stands at USD 442.49 million in 2025 and is forecast to reach USD 909.63 million by 2030, reflecting a CAGR of 15.50% over 2025-2030. Nationwide labor shortages, stricter safety rules, and sovereign-AI mandates are pushing contractors to shift from manual methods to low-waste robotic workflows that meet carbon-reduction targets. Demolition robots continue to anchor demand as urban renewal accelerates, while 3D concrete printing systems deliver fast-tracked infrastructure, higher design flexibility, and material savings. The construction robots market is also witnessing more funding into purpose-built startups and greater participation from established industrial automation leaders, signaling manufacturing scale inflection points. Tariff-driven cost spikes and fragmented building codes, however, weigh on near-term adoption economics.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Severe skilled-labor shortages Severe skilled-labor shortages | +4.2% | Global, with acute impact in Japan, Germany, North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast :+4.2% | Geographic Relevance :Global, with acute impact in Japan, Germany, North America | Impact Timeline :Medium term (2-4 years) |

Stricter safety regulations and penalties Stricter safety regulations and penalties | +3.1% | North America and EU, expanding to APAC | Short term (≤ 2 years) | |||

Rapid adoption of 3D concrete printing Rapid adoption of 3D concrete printing | +2.8% | Global, with early gains in Netherlands, Germany, Singapore | Medium term (2-4 years) | |||

Surge in urban-redevelopment demolition projects Surge in urban-redevelopment demolition projects | +2.4% | APAC core, spill-over to North America urban centers | Long term (≥ 4 years) | |||

BIM-integrated robot-as-a-service business models BIM-integrated robot-as-a-service business models | +1.9% | North America and EU, pilot expansion to APAC | Medium term (2-4 years) | |||

Carbon-reduction mandates favouring low-waste robotics Carbon-reduction mandates favouring low-waste robotics | +1.1% | EU primary, California, New York, expanding globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Severe Skilled-Labor Shortages

Construction firms face structural workforce gaps as aging populations retire faster than new workers enter the trade. Japan’s construction labor pool fell from 6.85 million in 1997 to 4.77 million in 2024, yet nominal investment climbed to JPY 26.2 trillion (USD 175 billion) in fiscal 2024.[1]CIO Japan, “鹿島建設が挑んだ世界初の自動化施工システム『A⁴CSEL』開発秘話,” cio.com Kajima’s A4CSEL platform demonstrates how three operators remotely manage fourteen machines around-the-clock, converting labor scarcity into a productivity catalyst. Similar shortages in Germany and the United States keep the construction robots market in a long-term demand cycle as contractors treat automation as labor-insurance rather than a cost-cutting option.

Stricter Safety Regulations and Penalties

OSHA now requires risk assessments, emergency-stop systems, and operator training for onsite robots, effectively raising the compliance bar. Europe links safety with environmental criteria, so robots that cut dust and waste satisfy multiple rules simultaneously. The IEC 62443 cybersecurity standard, extended to connected construction equipment, adds a digital-safety layer that favors certified robotic platforms. Heightened penalties for violations accelerate adoption because robots consistently execute high-risk tasks without exposing workers.

Rapid Adoption of 3D Concrete Printing

ABB’s IRB 6700 robots printed Germany’s first commercial non-residential structure, proving industrial-scale viability.[2]ABB Robotics, “Transforming the Future of Construction,” abb.com Material savings matter because construction waste accounts for 25% of transported materials, so precise deposition lowers disposal fees and emissions. XtreeE in France and COBOD in the Netherlands demonstrate the on-demand production of complex elements within hours, thereby compressing project schedules. Integration with BIM enables design-for-manufacturing workflows, tightening feedback loops between virtual models and onsite execution. Regulatory code alignment remains uneven, but early adopters see faster approvals as pilot projects accumulate safety data.

Surge in Urban-Redevelopment Demolition Projects

Dense Asian megacities replace aging stock amid space constraints that restrict large equipment. Husqvarna’s DXR 310 operates in confined interiors, delivering selective removal while controlling dust. Singapore’s renewal programs and California’s seismic retrofits keep demand elevated for precise, low-vibration demolition solutions. Robots also pre-sort debris for recycling, dovetailing with circular-economy goals and lowering landfill costs. Rising land values justify higher equipment capex because faster demolition unlocks earlier revenue from redevelopment.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital and set-up costs High capital and set-up costs | -3.8% | Global, particularly acute in developing markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast :-3.8% | Geographic Relevance :Global, particularly acute in developing markets | Impact Timeline :Short term (≤ 2 years) |

Absence of harmonised building codes for robotics Absence of harmonised building codes for robotics | -2.1% | Global fragmentation, EU leading harmonization efforts | Long term (≥ 4 years) | |||

Tariff-driven cost spikes in sensors and actuators Tariff-driven cost spikes in sensors and actuators | -1.9% | North America and EU primary, global supply chain impact | Medium term (2-4 years) | |||

Cyber-security and IP-theft risks for connected robots Cyber-security and IP-theft risks for connected robots | -1.2% | Global, with acute concerns in North America and EU | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Set-Up Costs

A typical autonomous excavator retrofit can exceed USD 350,000, stretching the payback period to 5-7 years, which is longer than the conventional equipment cycle. Tariffs amplify the hurdle for OnRobot, citing a 17% component price increase after 145% China-specific levies on automation parts, while Caterpillar absorbed USD 250-350 million in Q2 2024 tariff expenses that roll downstream. Robotics-as-a-service models lower upfront outlays, but contractors must still budget for site prep, data networks, and operator retraining. Smaller firms often struggle to secure financing, accelerating consolidation toward larger builders with stronger balance sheets.

Absence of Harmonised Building Codes for Robotics

Manufacturers juggle divergent regional rules on structural integrity, safety certification, and liability, forcing costly redesigns. IEC 62443 sets a cybersecurity base, yet no global equivalent exists for robotic concrete printing or autonomous grading. The EU is moving toward unified directives, but North America and Asia maintain patchwork standards, delaying scaled rollouts. Each jurisdiction’s custom testing elongates approval timelines and drains R&D funds that could go to product enhancements.

By Robot Type: Demolition Dominance Faces 3D Disruption

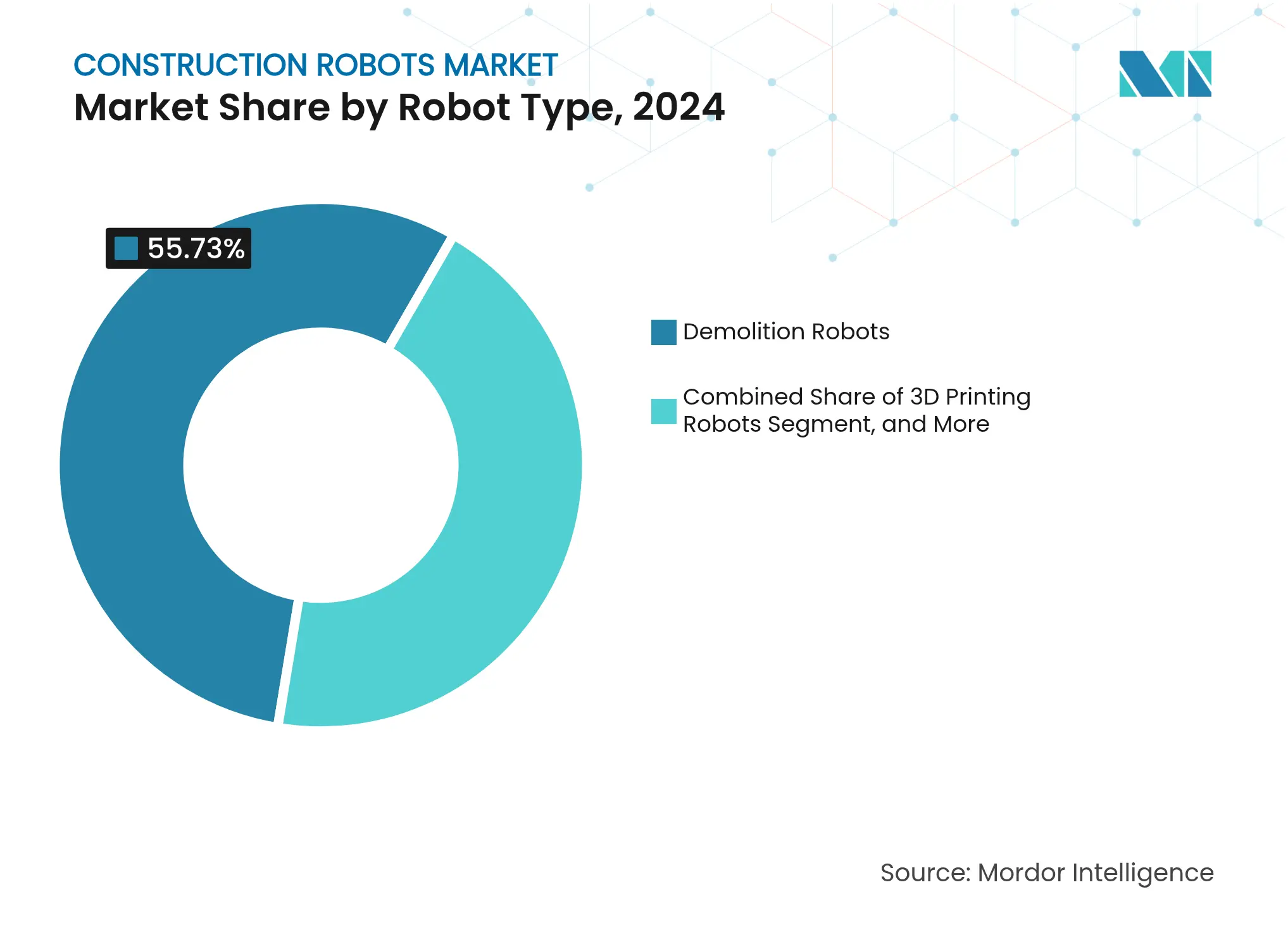

Demolition robots accounted for 55.73% of the construction robots market share in 2024, reflecting strong demand for remote-controlled units that comply with urban safety regulations. The construction robots market size for demolition is projected to expand steadily, as selective teardown in dense cities remains a critical need. Drone bricklaying systems such as BrickPilot have introduced aerial automation that places 121 bricks in 1.5 hours with millimeter accuracy, signaling an emerging challenge to ground-based robots. Vendors now embed debris-sorting modules into demolition units, enabling contractors to recycle materials on-site, which aligns with increasingly stringent waste management mandates.

3D printing robots are expected to grow at a 16.78% CAGR through 2030, driven by municipalities' demand for rapid and low-waste infrastructure delivery. Hybrid platforms are blurring categories; KUKA’s KR IONTEC, integrated into Baubot’s mobile chassis, drills tunnel segments and positions materials within a single workflow.[3]KUKA AG, “Automation for the Construction Industry,” kuka.com With AI-based perception and planning present in 69% of new machines, a single unit can seamlessly shift from material handling to selective demolition, all without any hardware modifications. These cross-functional gains suggest future segmentation will pivot from hardware tiers to application bundles.

Note: Segment shares of all individual segments available upon report purchase

By Automation Level: Autonomous Systems Gain Momentum

Semi-autonomous units held 64.83% of the construction robots market size in 2024 because regulators trust human-in-the-loop oversight. Kajima’s A4CSEL platform shows three operators steering fourteen machines across continuous shifts, proving scale economics while maintaining real-time control. However, fully autonomous systems are poised for a 17.12% CAGR, as physics-informed neural networks predict excavator-rock interactions and eliminate manual overrides. Insurance carriers increasingly price premiums on safety data, so autonomy that reduces incidents earns lower rates.

Liability rules still lag behind technology, so most builders stage autonomy in layers that default to teleoperation during complex tasks. Remote command centers centralize expert talent, widening access for smaller sites that cannot hire specialist crews onsite. As AI assurance frameworks mature, certification bodies are drafting test suites that could shorten approval times for new autonomous releases. Those shifts should gradually move shares toward higher-autonomy tiers while leaving semi-autonomous machines as a bridge for retrofit fleets.

By Function: 3D Printing Transforms Construction Workflows

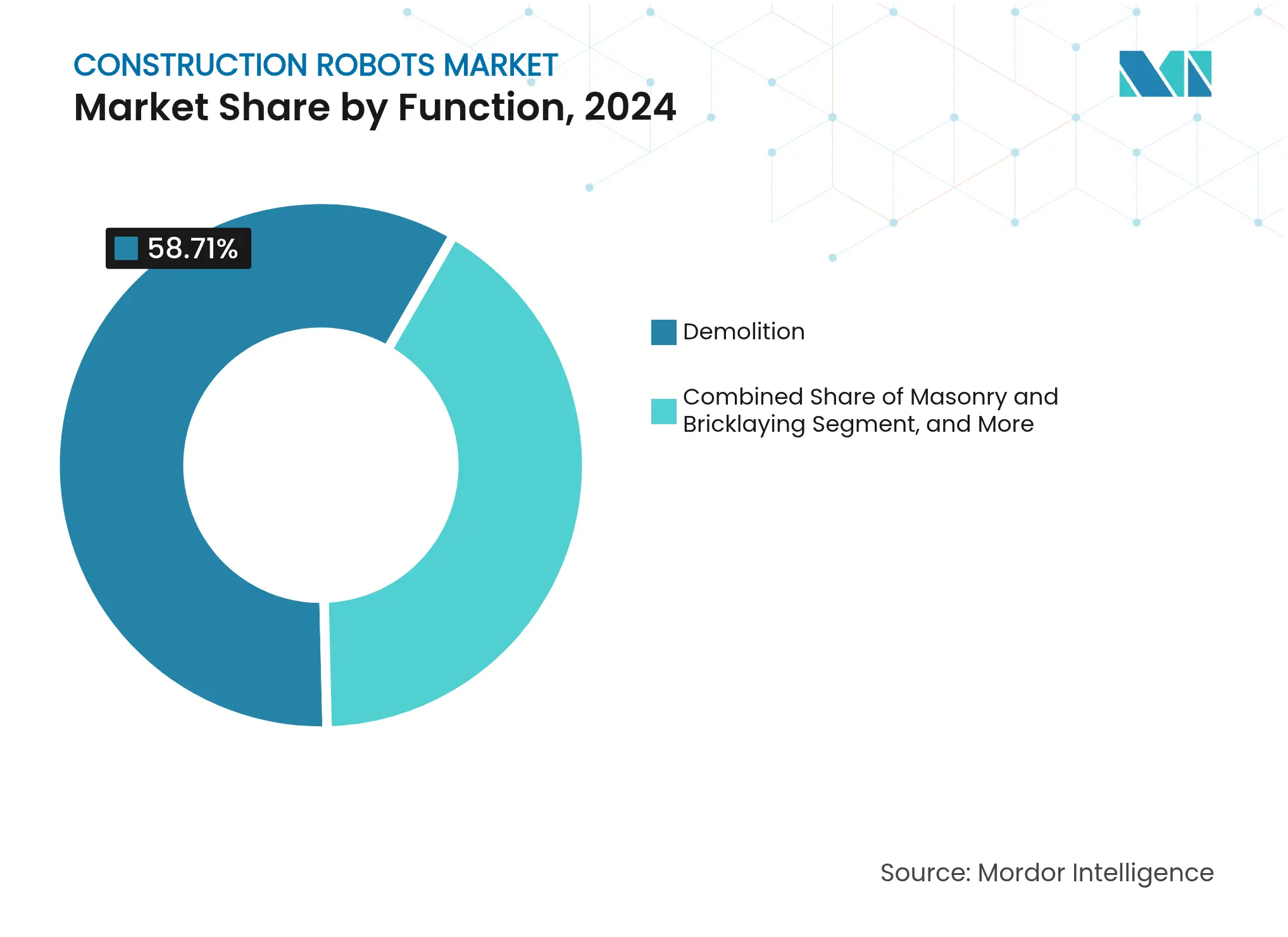

Demolition preserved 58.71% share of the construction robots market size in 2024, yet 3D concrete printing is pacing the field with a 16.88% CAGR through 2030. ABB’s IRB 6700 printer produced Germany’s first commercial non-residential structure, demonstrating 12 m height capability in a single pass. Layer-by-layer deposition reduces waste that historically accounted for 25% of hauled material, thereby easing both disposal costs and carbon footprint.

Parallel task execution defines the new workflow, printers lay walls while rebar-tying cobots reinforce adjacent segments, collapsing overall schedules. Masonry drones eliminate the need for scaffolding on curved façades, enhancing worker safety. BIM-linked sensors feed progress data to digital twins, enabling precise inventory drops when needed and reducing site congestion. As multi-material print heads mature, expect printers to handle insulation and conduit embeds in one run.

Note: Segment shares of all individual segments available upon report purchase

By End-Use: Public Infrastructure Drives Growth

Residential projects commanded 51.83% of 2024 revenue because large builders like PulteGroup scaled framing robots across Florida sites. Even so, public infrastructure displays the strongest 16.44% CAGR as governments bundle robotic criteria into highway, tunnel, and bridge bids. Longer project durations support the learning curves that automated systems require, and public owners favor predictable timelines over lowest initial cost.

Obayashi’s Singapore lab aims printable bridge girders at Southeast Asian transport corridors, showing how R&D hubs tie into regional megaprojects. Renewable-energy facilities such as offshore wind farms adopt robots for tower segment assembly where human access is limited. Commercial and industrial buildings trail in volume but pick targeted functions, facade installation and interior finishing, for robots that prove payback within current depreciation cycles.

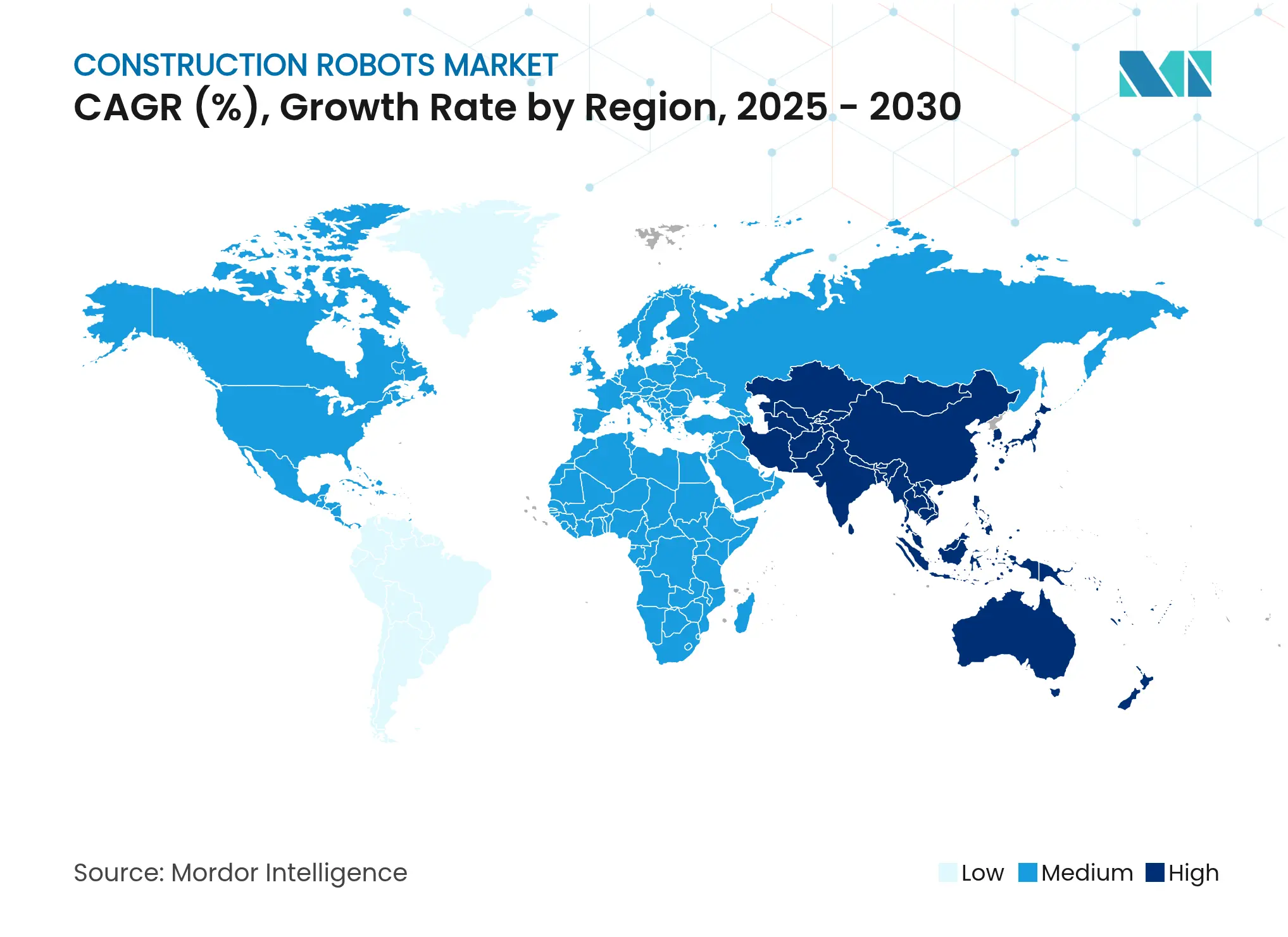

North America’s 41.70% share in 2024 reflects two decades of BIM investment, venture funding, and OSHA guidance that make job-site automation less risky. Built Robotics attracted USD 112 million, leveraging established dealer networks to retrofit earthmovers. Tariffs remain a cost headwind; component levies lifted prices 17% for key gripper suppliers, while 25% cement duties in Canada and Mexico re-sliced budgets for robot-printed concrete in 2025. Municipalities, nonetheless, increasingly award contracts that embed digital-twin deliverables, locking in robot-compatible workflows.

Asia-Pacific registers the fastest 16.23% CAGR, led by Japan’s automated megaprojects and China’s low-cost robot supply chain. Kajima’s field data show three operators steering fourteen machines across continuous shifts, setting benchmarks for productivity. Singapore’s dense urban environment fuels demand for compact demolition bots and printable high-rise components. India’s public-works boom raises volume potential but capital constraints slow smaller contractors’ uptake.

Europe aligns national codes under EU directives that pair safety and carbon metrics. France’s 2025 green-building rule limits on-site waste, nudging builders toward 3D concrete printing and dust-free robotic demolition. Germany leverages its precision-manufacturing base to integrate industrial robots into construction, exemplified by ABB’s IRB 6700 deployment for printed offices. Harmonized standards ease cross-border deployments, yet liability frameworks for autonomous gear still differ among member states, tempering rollouts.

Market Concentration

Industrial automation giants and specialized startups share a moderately fragmented arena. ABB deploys IRB 6700 units in 3D printing alliances, such as the August 2025 Cosmic Buildings partnership in Los Angeles, extending its factory lineage into site robots. KUKA co-developed a mobile tunnel robot with Baubot, showing incumbents’ readiness to customize beyond arm-only offerings. Startups such as Built Robotics and Dusty Robotics focus on earthmoving and layout, respectively, leveraging software-centric value to carve niches.

Service business models gain ground; Renovate Robotics teams with Saint-Gobain to rent roofing bots, trimming capex barriers for contractors and shifting competition toward uptime guarantees rather than one-time sales. Patent intensity remains high, with iRobot reporting 556 active U.S. patents, underscoring the entry hurdles for latecomers. Market leaders now stand out as advanced AI architectures facilitate multi-functional adaptability and smooth collaboration between humans and robots.

Capital requirements portend selective consolidation. Scale manufacturing favors deep pockets, yet niche applications leave room for agile entrants with domain-specific know-how. Overall, the construction robots market sees competition shift from pure hardware specs toward platform ecosystems integrating AI, cloud analytics, and equipment-as-a-service billing.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Construction robots are professional service robots that are a part of construction and demolition work in the construction industry. Robots considered part of the study include demolition robots, radiation handling equipment, robots with cutting tools used in the industry, concrete removal robots, hydro demolition, bricklaying robots, 3D printing robots, and exoskeleton and exoskeleton masonry robots. Heavy civil construction robot equipment, such as earthmoving, drilling, and forepoling robots, is separate from the study.

The construction robots market is segmented by type (demolition, bricklaying, and 3D printing), application (public infrastructure, commercial, and residential buildings), and geography (North America, Europe, Asia-Pacific, and the rest of the world). The market sizes and forecasts are in terms of value in USD million for all the segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.