Cone Rod Dystrophy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

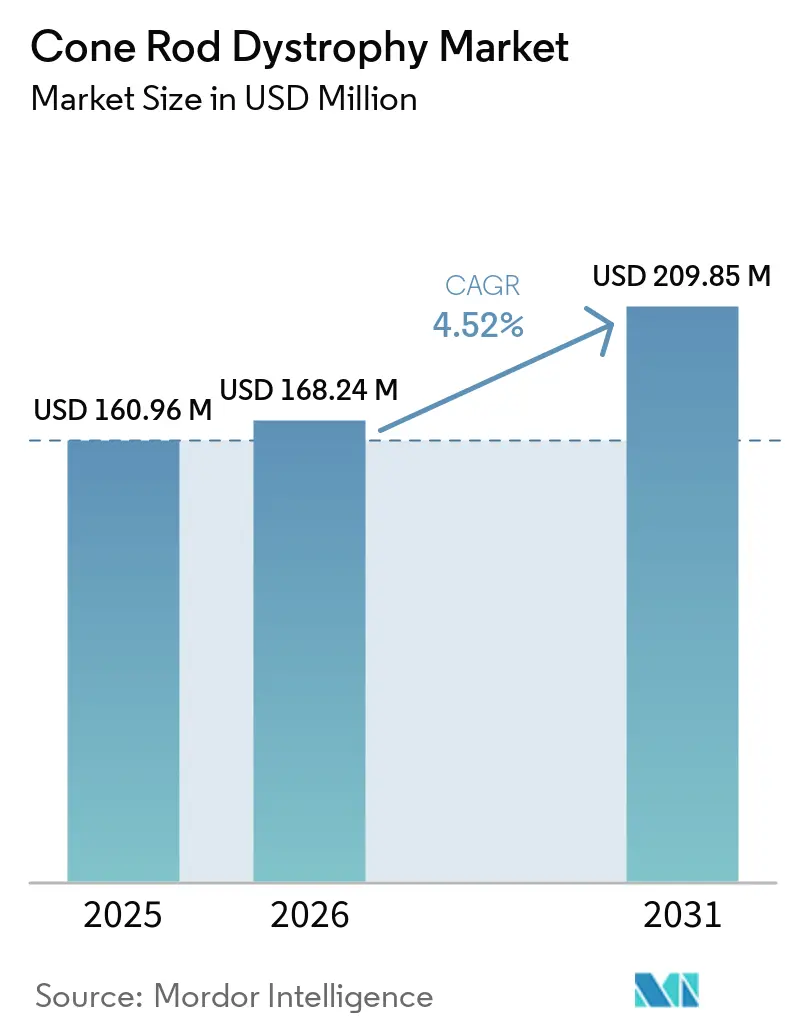

| Market Size (2026) | USD 168.24 Million |

| Market Size (2031) | USD 209.85 Million |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cone Rod Dystrophy Market Analysis by Mordor Intelligence

The Cone Rod Dystrophy Market size is expected to increase from USD 160.96 million in 2025 to USD 168.24 million in 2026 and reach USD 209.85 million by 2031, growing at a CAGR of 4.52% over 2026-2031.

The market is moving on two tracks, with gene therapy developer spending rising much faster than the supportive care base, which continues to expand at a steadier pace. Pipeline activity is unusually dense for a disease of this size because many cone rod dystrophy mutations overlap with targets already explored in adjacent retinal programs, which lowers early clinical risk for new entrants. North America leads current demand because it combines specialized ophthalmology infrastructure, inherited retinal disease research activity, and a concentration of treatment delivery centers that can support advanced retinal interventions. The main near-term constraint on the cone rod dystrophy market remains reimbursement for one-time gene therapies, since payer systems still favor chronic payment models and can slow access through narrow coverage rules and authorization delays. A second drag comes from the continued gap between validated retinal biomarkers and the clinical endpoints that regulators and payers accept as meaningful proof of benefit, which can lengthen development timelines for inherited retinal disease programs.

Key Report Takeaways

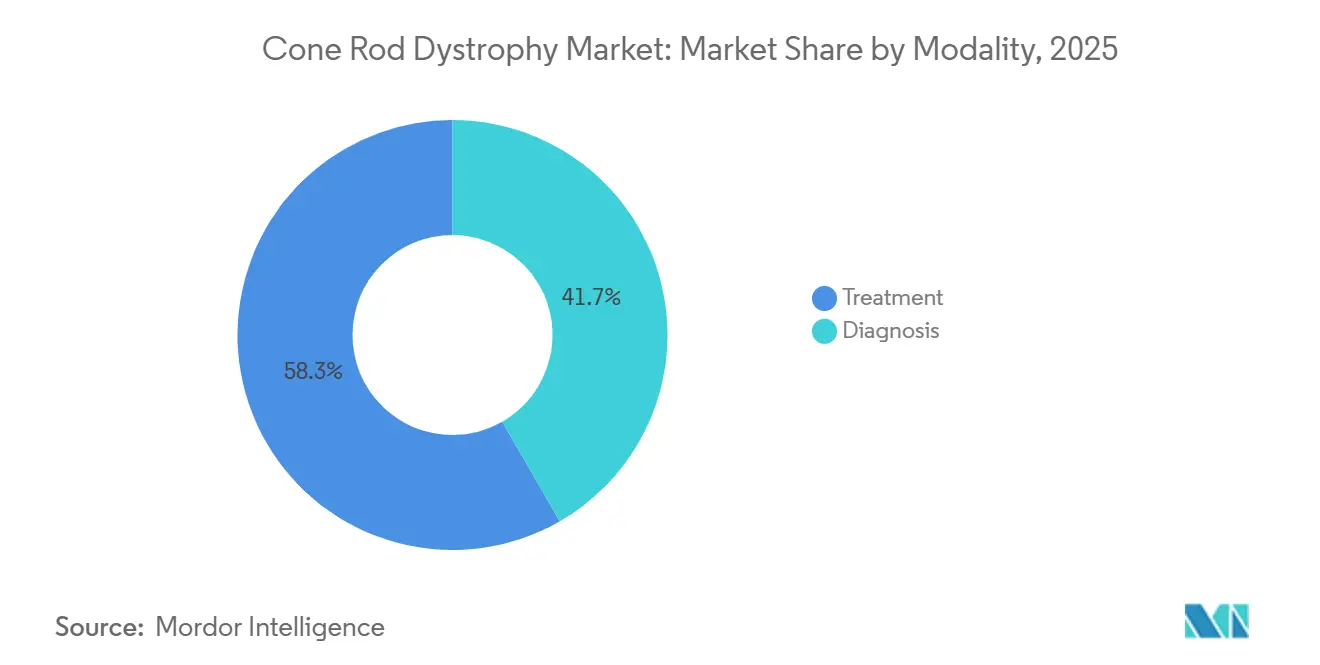

- By modality, treatment held 58.31% of the cone rod dystrophy market share in 2025, while diagnostics is forecast to grow at a 6.38% CAGR through 2031.

- By inheritance pattern, X-linked cone rod dystrophy held 40.24% share in 2025, while autosomal recessive cone rod dystrophy is projected to expand at a 6.52% CAGR through 2031.

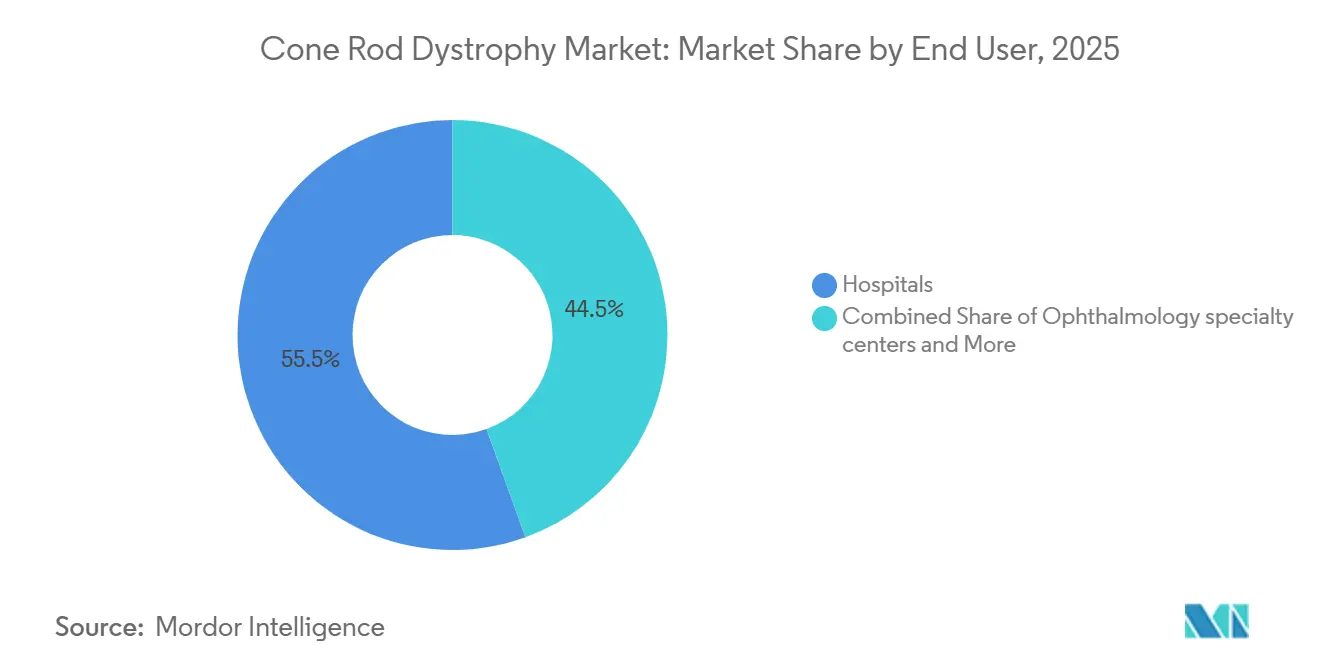

- By end user, hospitals held 55.52% share in 2025, while ophthalmology specialty centers are projected to grow at a 7.25% CAGR through 2031.

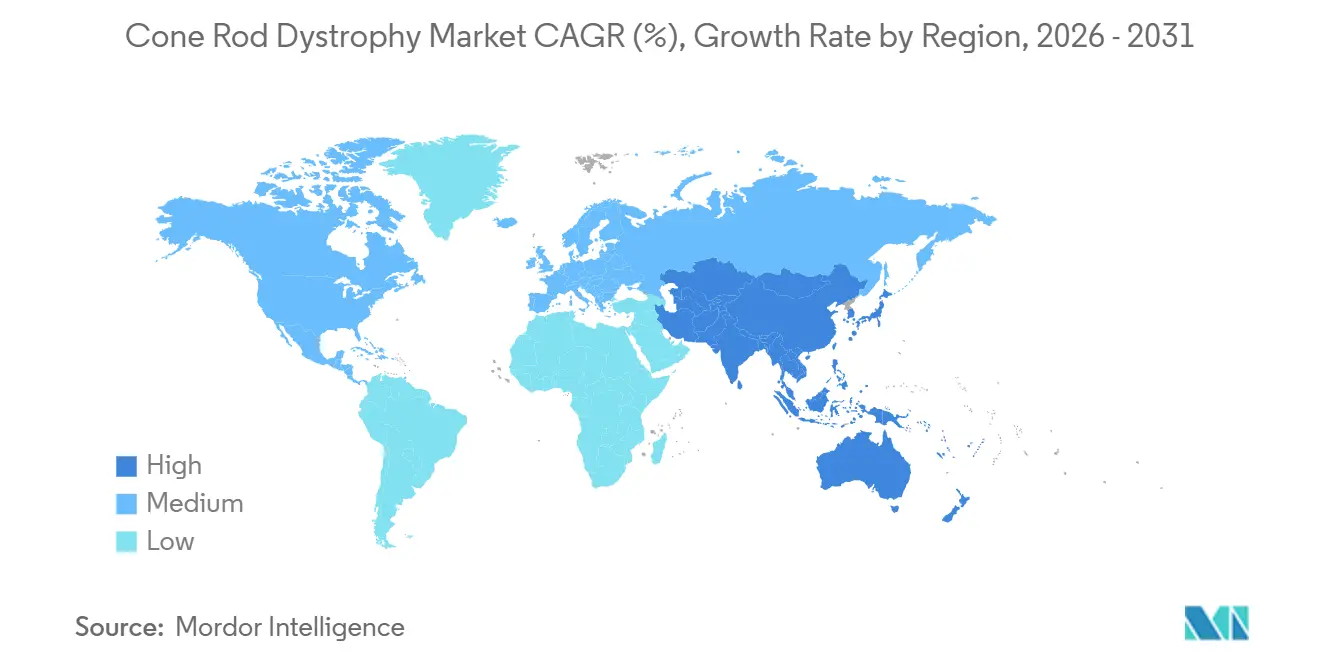

- By geography, North America held 38.24% share of the cone rod dystrophy market size in 2025, while Asia-Pacific is projected to grow at a 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cone Rod Dystrophy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gene Therapy Progress and Orphan Incentives | +1.2% | Global, with highest concentration in North America and Europe | Medium term (2-4 years) |

| Wider Molecular Diagnosis and Multimodal Retinal Imaging | +1.0% | Global, North America and EU lead, with Asia-Pacific accelerating | Short term (≤ 2 years) |

| Rising Supportive-Care and Low-Vision Technology Adoption | +0.6% | Global, APAC fastest growing | Medium term (2-4 years) |

| Genotype Prescreening and Natural-History Cohorts | +0.7% | North America and Europe, with spill-over to APAC | Medium term (2-4 years) |

| Mutation-Agnostic Retinal Therapies | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Gene Therapy Progress and Orphan Drug Incentives Are Reshaping CRD Development Economics

The market is seeing a different development path because orphan incentives have made small retinal programs easier to finance. In the United States, Orphan Drug Designation offers 7 years of market exclusivity, major fee waivers, and potential review-related value that can justify late-stage spending even with a limited patient base. Beacon Therapeutics has already secured RMAT and Fast Track designations from the FDA and PRIME status from the EMA for laru-zova, and its VISTA trial completed enrollment in June 2025[1]Beacon Therapeutics, “Beacon Therapeutics Announces Positive 12-Month Safety and Efficacy Update from Phase 2 DAWN Trial of laru-zova in Patients with X-Linked Retinitis Pigmentosa at ARVO 2026 Annual Meeting,” Beacon Therapeutics, beacontx.com. This combination lowers funding risk for companies entering the cone rod dystrophy market from nearby retinal indications. It also raises the odds that the first approved therapy will shape pricing and reimbursement expectations for the rest of the field.

Wider Molecular Diagnosis and Multimodal Retinal Imaging Are Expanding the Diagnosable Patient Pool

The cone rod dystrophy market is expanding its diagnosable pool because panel-based sequencing and better imaging now reach patients earlier in the disease course. In optimized academic settings, inherited retinal disease diagnostic yield has moved from the earlier 40% to 50% range toward 60% to 80%. That shift matters because a confirmed molecular diagnosis extends the window for gene-specific treatment decisions and genetic counseling within the cone rod dystrophy market. OCT and fundus autofluorescence have also emerged as useful progression markers in natural history work, which reduces reliance on functional measures alone. Japan still shows a diagnosis gap, with a reported 40% molecular diagnosis rate and 12 designated genetic testing facilities, which points to persistent regional access inequalities. Japan also approved the PrismGuide IRD Panel System in 2023, and the panel includes the RPGR ORF15 region that is relevant to X-linked cone rod dystrophy.

Genotype Prescreening and Natural-History Cohorts Are Enabling More Efficient CRD Trials

The market is benefiting from genotype prescreening and natural-history cohorts that now function as recruitment channels as much as research assets. These datasets shorten prescreening because investigators can identify eligible patients before a formal trial enrollment window opens. SparingVision's PHENOROD2 cohort followed 100 patients and supported microperimetry and ellipsoid zone mapping as sensitive 12-month markers for rod-cone dystrophy progression. Ascidian's STARPATH observational study offers genetic testing and retinal imaging to adults and children aged 5 and older with ABCA4 retinopathies, which helps build a ready cohort for ACDN-01 screening. Companies that control large genotyped datasets gain a durable advantage in trial design, patient stratification, and partnering across the cone rod dystrophy market.

Mutation-Agnostic Retinal Therapies Are Shifting the Addressable Market Boundary

The market is also being reshaped by mutation-agnostic therapies that can serve patients across many gene variants. SparingVision's SPVN06 uses RdCVF and RdCVFL through an AAV vector, and the PRODYGY trial completed dosing in 33 patients in February 2026. Ocugen's OCU400 is a modifier gene therapy for broad retinitis pigmentosa, and Phase 3 liMeliGhT enrollment reached 140 patients across RHO and gene-agnostic arms in March 2026. Nanoscope's MCO-010 program has received 5 EMA orphan designations across multiple retinal dystrophy categories, which points to a wider regulatory route for disease-agnostic retinal treatment. Even with this shift, patients still need a clinical diagnosis, so diagnostic providers remain central to the cone rod dystrophy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tiny Fragmented Patient Pools | -1.0% | Global | Long term (≥ 4 years) |

| One-Time Therapy Pricing and Reimbursement Uncertainty | -1.1% | North America and Europe | Medium term (2-4 years) |

| Weak Endpoint and Biomarker Standardization | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tiny Fragmented Patient Pools Constrain Trial Power and Commercial Returns

The cone rod dystrophy market remains constrained by a very small and genetically split patient population. Prevalence estimates of 1 in 30,000 to 1 in 40,000, combined with more than 30 causative genes, make the field behave like many ultra-rare markets rather than one large pool. This fragmentation raises recruitment cost because developers often need multi-country enrollment to reach statistical power in the cone rod dystrophy market. Molecular diagnosis still resolves only 50% to 75% of cases in clinical settings, so many patients cannot enter mutation-specific programs. Concentrated cohorts can exist in consanguineous populations, as shown by the 2025 Pakistani dataset where autosomal recessive inheritance represented 95.9% of solved cases, but regulators may not treat these data equally across regions.

One-Time Therapy Pricing and Reimbursement Uncertainty Depress Near-Term Uptake

The market also faces a near-term adoption ceiling because payer systems were built for repeated drug spending, not one-time gene therapy pricing. The reimbursement challenge is already visible in inherited retinal disease care, where payers often use narrow coverage rules and prior authorization delays. ASGCT reported in 2025 that coverage can be limited to pivotal-trial criteria and that accelerated-approval cell and gene therapies are often treated as experimental. A 2025 systematic review found that the economic evidence for retinal gene therapies is still too limited for many health technology assessment decisions. As long as single-administration therapies carry high upfront cost and uncertain durability assumptions, reimbursement friction will continue to weigh on the cone rod dystrophy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Diagnostic Volume Growth Outpaces the Existing Treatment Base

Diagnostics is projected to grow at a 6.38% CAGR in the cone rod dystrophy market through 2031, which makes it the fastest-growing modality segment. This rise reflects wider use of NGS panels, growing ERG capacity in ophthalmology specialty centers, and more routine use of OCT with fundus autofluorescence for monitoring. ERG remains the clinical standard because it shows cone dysfunction exceeding rod loss and helps distinguish the condition from retinitis pigmentosa. Structural measures such as ellipsoid zone width are now used alongside ERG because they offer a quantifiable view of photoreceptor integrity[2]S. Li et al., “Molecular Genetics and Clinical Characteristics of Cone-Rod Dystrophy and Retinitis Pigmentosa in a Chinese Cohort,” Scientific Reports, nature.com.

Treatment represented 58.31% of the cone rod dystrophy market share in 2025 because trial administration, retinal implant procedures, neurostimulation, and pharmacologic care still account for most spending. Retinal implants and neurostimulation form a more mature treatment pocket, while supportive care and low-vision aids are picking up as options for patients who remain genetically unresolved in the cone rod dystrophy industry. Pharmacologic and nutraceutical approaches, including visual cycle modulation and antioxidant regimens, appeal to a broad patient group because they do not depend on advanced gene therapy delivery infrastructure. This mix keeps treatment larger today, even though diagnostics is gaining faster in the cone rod dystrophy market.

By Inheritance Pattern: X-Linked Revenue Weight Reflects Pipeline Focus

X-linked disease accounted for 40.24% of the cone rod dystrophy market share in 2025, which reflects pipeline concentration more than epidemiology. Published evidence places X-linked cases at 12% to 25% of all cases depending on the population, which shows how much revenue has clustered around RPGR-linked development. Beacon Therapeutics reported positive 12-month Phase 2 DAWN data in May 2026, and the company expects VISTA pivotal topline results in the second half of 2026. This heavy clinical investment lifts revenue capture in imaging, dosing, and trial administration across the cone rod dystrophy market.

Autosomal recessive disease is projected to grow at a 6.52% CAGR through 2031 in the cone rod dystrophy market, which makes it the fastest-growing inheritance segment. That growth is tied to an expanding ABCA4-focused pipeline that spans RNA editing, dual-AAV replacement work, and visual cycle modulation. Alkeus received FDA Rare Pediatric Disease and Fast Track designations for gildeuretinol in November 2024, which reinforces commercial interest in this patient pool. Autosomal dominant disease remains the smallest segment in the cone rod dystrophy industry because it has fewer active programs, although reported GUCY2D and CRX findings show that clinical inheritance patterns can be complex in practice.

By End User: Specialty Centers Are Pulling Ahead as Delivery Points

Hospitals held 55.52% share of the cone rod dystrophy market size in 2025 because they remain the main referral points for complex inherited retinal disease workups. Their role is supported by ERG equipment concentration, genetic counseling capacity, and routine links to clinical trial networks. Ophthalmology specialty centers are projected to grow at a 7.25% CAGR through 2031, which makes them the fastest-growing end-user group in the cone rod dystrophy market. Gene therapy delivery and advanced retinal imaging are increasingly concentrated in these dedicated eye disease settings rather than in general hospital departments.

Academic and research institutes still handle a large share of diagnostic and natural history activity in the cone rod dystrophy market because many early gene therapy studies run through these sites. Their role extends beyond research, since they also supply genotyped cohorts and longitudinal imaging data that later support commercial trials. Home-based low-vision rehabilitation is emerging as a parallel channel for patients who cannot access gene therapy because of geography or reimbursement. AI-enabled assistive devices and orientation tools improve daily function without requiring a confirmed genotype, which makes this category relevant to the 30% to 40% of patients who remain genetically unresolved.

Geography Analysis

North America held 38.24% of the cone rod dystrophy market share in 2025, which made it the largest regional segment. The region benefits from a dense ophthalmology specialty network, active inherited retinal disease research support, and a concentration of treatment delivery centers that can support advanced retinal interventions. The United States also remains central to developer financing, as Opus Genetics secured up to USD 155 million in April 2026 to advance 3 more gene therapy programs, including OPGx-RDH12, into clinical testing. Canada and Mexico add smaller contributions, while the United States is likely to stay dominant through the forecast period as inherited retinal gene therapy filings move closer to commercialization.

Europe is the second-largest regional block in the cone rod dystrophy market, led by Germany, the United Kingdom, and France for diagnostics and trial participation. Beacon's laru-zova holds EMA PRIME status, which gives the program accelerated regulatory support that is similar in purpose to FDA RMAT. Europe also demonstrated first-in-human capability through the Phase 1 and Phase 2 AAV8-RLBP1 study run across Swedish and EU centers with Swedish regulatory approvals. Access still varies by country because health technology assessment timing and reimbursement pathways differ across national systems.

Asia-Pacific is projected to grow at a 6.92% CAGR through 2031 in the cone rod dystrophy market, which makes it the fastest-growing region. Japan has already established an ophthalmic gene therapy access pathway, and 1-year Phase 3 outcomes for voretigene neparvovec were published in 2025 as Asia's first Phase 3 inherited retinal gene therapy trial. Japan also opened its first optogenetics trial in February 2025 through Restore Vision and Keio University Hospital for patients with photoreceptor loss regardless of genetic cause. China is strengthening its role through cohort studies that map local mutation patterns and through published work on CRISPR applications for inherited retinal disease. South Korea, Australia, India, the Middle East and Africa, and South America contribute smaller volumes, while GCC trial funding and rare disease registries in Brazil and Argentina provide incremental support.

Competitive Landscape

The cone rod dystrophy market remains moderately fragmented, with competition spread across gene therapy developers, diagnostic laboratories, and ophthalmic drug and device companies. Companies are not yet competing head-to-head on price because no approved cone rod dystrophy-specific gene therapy is currently available. Instead, the main differentiators are asset quality, clinical data, testing breadth, turnaround time, and integration with clinical genetics programs. This structure leaves room for companies that link diagnosis with patient registry creation, since trial-ready cohorts have become valuable commercial assets.

Beacon Therapeutics, Ocugen, Opus Genetics, SparingVision, MeiraGTx, and ProQR Therapeutics are among the visible therapy developers shaping the cone rod dystrophy market. Beacon strengthened its position by completing VISTA enrollment in June 2025 and by reporting positive 12-month DAWN data in May 2026 for laru-zova. SparingVision advanced SPVN06 by completing PRODYGY dosing in February 2026, and it continues to use PHENOROD2 as a supporting observational platform. Ocugen extended its reach through a Korean regional license for OCU400 in 2025 and followed with USD 130 million in convertible notes in May 2026 to support parallel BLA plans[3]Ocugen, “Ocugen Provides Business Update with First Quarter 2026 Financial Results,” BioSpace, biospace.com. These moves show that geographic licensing and non-dilutive capital remain key tools for scaling the cone rod dystrophy market before first approvals arrive.

Diagnostic players such as Blueprint Genetics, Fulgent Genetics, Invitae, Labcorp, and PreventionGenetics compete on panel design, interpretation quality, and fit within specialist referral pathways. Accreditation and standardized variant classification remain important because physicians need confidence that test results will support counseling and trial enrollment. Emerging platforms such as RNA editing and optogenetics are widening competitive pressure because they can target patients who fall outside classic gene replacement windows. Smaller developers can still challenge larger peers in the cone rod dystrophy market when they combine focused pipelines with strong regulatory or financing milestones, as seen in Opus Genetics' RDEP engagement and long-term financing package.

Cone Rod Dystrophy Industry Leaders

SparingVision

Ascidian Therapeutics

Beacon Therapeutics

Ocugen

Labcorp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ocugen closed USD 130 million in 6.75% convertible senior notes to fund rolling BLA submissions for OCU400 (RP, targeted Q3 2026) and OCU410ST (Stargardt disease, targeted mid-2027), extending cash runway into 2028.

- May 2025: Ocugen, Inc. shared that the U.S. FDA granted Rare Pediatric Disease Designation (RPDD) to OCU410ST. This designation is for the treatment of ABCA4-associated retinopathies, which include Stargardt disease, retinitis pigmentosa 19, and cone-rod dystrophy.

Global Cone Rod Dystrophy Market Report Scope

As per the scope of the report, cone rod dystrophy is a group of inherited eye disorders characterized by progressive degeneration of the cone and rod cells in the retina. This condition typically leads to loss of vision, affecting color perception, visual acuity, and peripheral vision over time. It often begins with loss of central vision and color vision (due to cone cell degeneration), followed by loss of peripheral and night vision (due to rod cell degeneration).

The cone rod dystrophy market is segmented by modality, inheritance pattern, end user, and geography. By modality, the market is divided into diagnosis, which includes molecular diagnosis, electroretinography, and OCT and fundus autofluorescence, and treatment, which encompasses retinal implant and neurostimulation, pharmacological and nutraceutical therapy, and supportive care and low-vision aids. By inheritance pattern, the market is categorized into autosomal recessive cone rod dystrophy, autosomal dominant cone rod dystrophy, and X-linked cone rod dystrophy. By end user, the segmentation includes hospitals, ophthalmology specialty centers, academic and research institutes, and home-based low-vision rehabilitation. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Diagnosis | Molecular diagnosis |

| Electroretinography | |

| OCT and fundus autofluorescence | |

| Treatment | Retinal implant and neurostimulation |

| Pharmacological and nutraceutical therapy | |

| Supportive care and low-vision aids |

| Autosomal recessive cone rod dystrophy |

| Autosomal dominant cone rod dystrophy |

| X-linked cone rod dystrophy |

| Hospitals |

| Ophthalmology specialty centers |

| Academic and research institutes |

| Home-based low-vision rehabilitation |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Diagnosis | Molecular diagnosis |

| Electroretinography | ||

| OCT and fundus autofluorescence | ||

| Treatment | Retinal implant and neurostimulation | |

| Pharmacological and nutraceutical therapy | ||

| Supportive care and low-vision aids | ||

| By Inheritance Pattern | Autosomal recessive cone rod dystrophy | |

| Autosomal dominant cone rod dystrophy | ||

| X-linked cone rod dystrophy | ||

| By End User | Hospitals | |

| Ophthalmology specialty centers | ||

| Academic and research institutes | ||

| Home-based low-vision rehabilitation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the cone rod dystrophy market?

It is valued at USD 168.24 million in 2026 and is projected to reach USD 209.85 million by 2031 at a 4.52% CAGR.

Which region leads current demand?

North America leads with 38.24% share in 2025 because of specialized ophthalmology infrastructure, active retinal disease research, and concentrated delivery capacity.

Which area is growing fastest by care type?

Diagnostics is the fastest-growing modality at a 6.38% CAGR through 2031 as NGS testing, ERG use, OCT, and fundus autofluorescence expand in clinical practice.

Why are ophthalmology specialty centers gaining ground?

They are projected to grow at a 7.25% CAGR through 2031 because gene therapy delivery and advanced retinal imaging are shifting into dedicated eye care settings.

What is the biggest commercial hurdle for new therapies?

Reimbursement remains the main near-term hurdle because payers often apply narrow coverage criteria and prior authorization delays to high-cost one-time gene therapies.

Which genetic pattern is gaining fastest attention?

Autosomal recessive disease is growing fastest at a 6.52% CAGR through 2031, supported by ABCA4-related development in RNA editing, gene replacement, and visual cycle modulation.

Page last updated on: