Comprehensive Metabolic Panel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.42 Billion |

| Market Size (2031) | USD 18.63 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

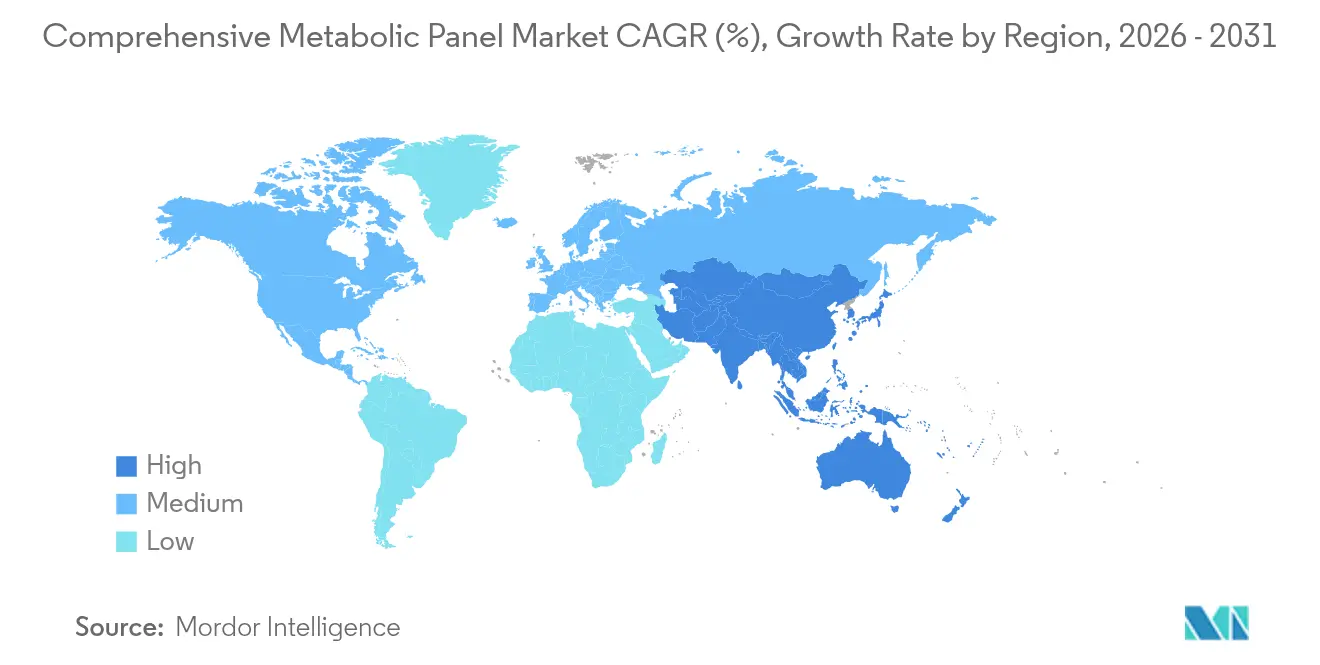

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

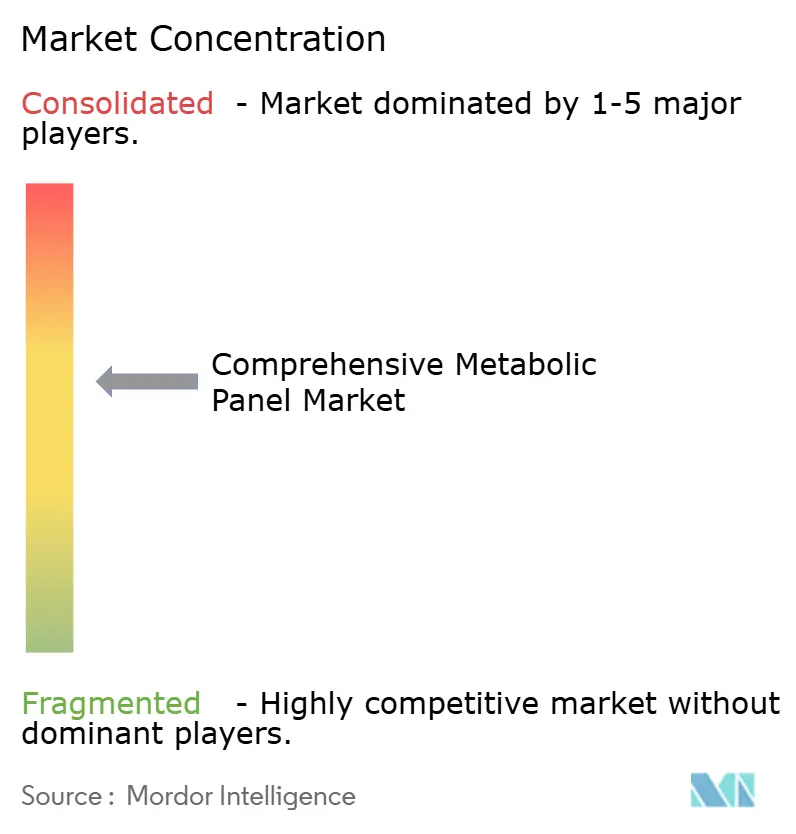

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Comprehensive Metabolic Panel Market Analysis by Mordor Intelligence

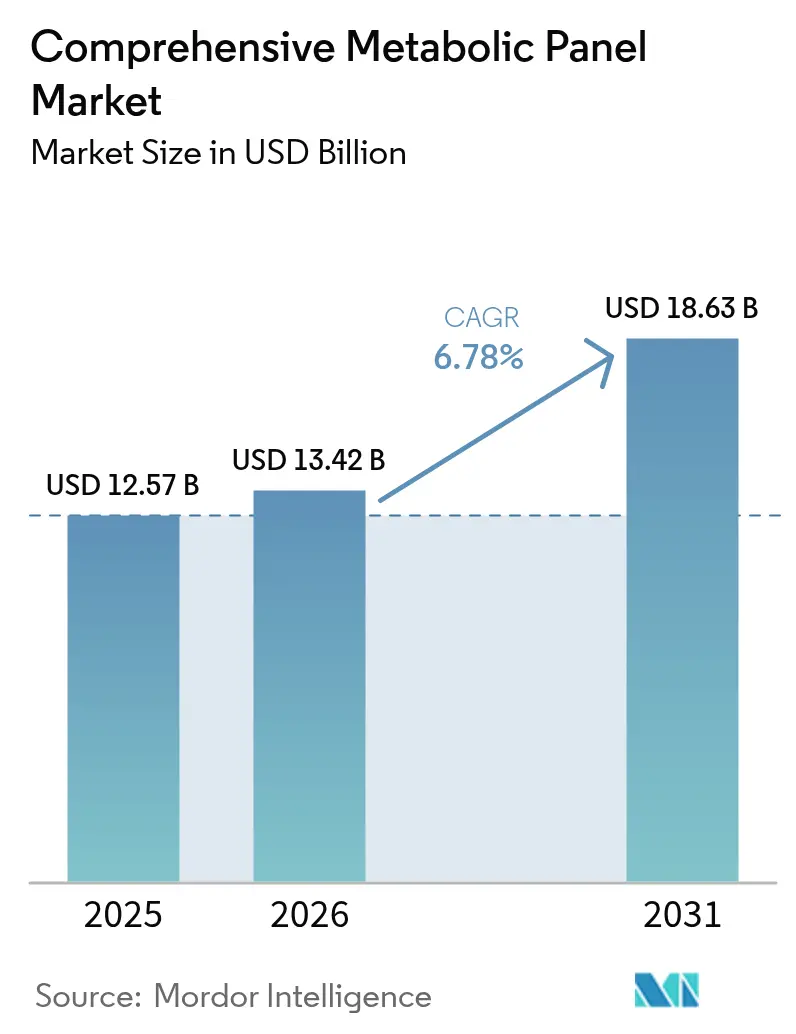

The comprehensive metabolic panel market size is expected to grow from USD 12.57 billion in 2025 to USD 13.42 billion in 2026 and is forecast to reach USD 18.63 billion by 2031 at 6.78% CAGR over 2026-2031. Emerging preventive-care policies, the widening burden of diabetes, kidney, and liver disorders, and expanding point-of-care (POC) diagnostic networks form the bedrock of sustained demand. Hospitals are automating chemistry workflows to meet the FDA’s 2024 Laboratory Developed Test (LDT) rule, while independent laboratories deploy high-throughput systems to comply with new quality-system mandates. AI-powered analytics are becoming standard add-ons, reducing manual review rates and turning routine panels into decision-support assets. POC chemistry analyzers that deliver lab-grade results in minutes now compete directly with core labs for test volumes, reshaping procurement patterns.

Key Report Takeaways

- By test type, kidney function tests led with 31.12% of comprehensive metabolic panel market share in 2025; Glucose testing is set to rise at a 9.12% CAGR to 2031.

- By disease application, kidney diseases held 32.95% of the comprehensive metabolic panel market size in 2025, while Diabetes testing records the fastest 7.92% CAGR through 2031.

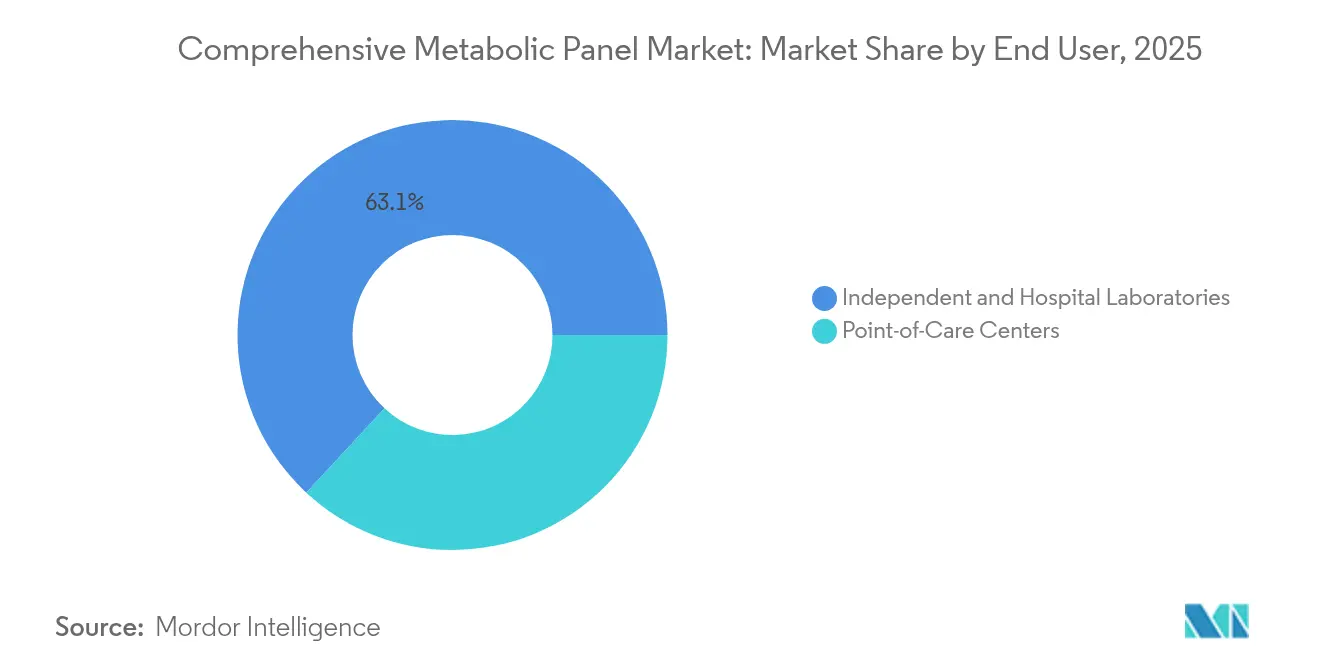

- By end user, independent & hospital laboratories dominated with 63.10% revenue share in 2025; Point-of-Care Centers post the highest 8.83% CAGR to 2031.

- By geography, North America commanded 36.45% share of the comprehensive metabolic panel market in 2025, whereas Asia-Pacific is projected to expand at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Comprehensive Metabolic Panel Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Awareness Of Preventive Health Check-Ups | +1.2% | Global, with stronger adoption in North America & EU | Medium term (2-4 years) |

| Rising Global Burden Of Chronic Kidney, Liver & Diabetes Cases | +1.8% | Global, highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Rapid Adoption Of POC Chemistry Analyzers In Ambulatory Settings | +1.1% | North America & EU leading, expanding to APAC | Short term (≤ 2 years) |

| AI-Driven Decision-Support Embedded Into CMP Workflows | +0.9% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Employer-Sponsored Wellness Panels Boosting Test Volumes | +0.7% | North America primarily, expanding to EU | Short term (≤ 2 years) |

| Home Sample-Collection Start-Ups Partnering With Labs | +0.8% | North America & EU, early adoption in urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Preventive Health Check-Ups

Rising employer-sponsored wellness initiatives are normalizing annual metabolic panels, with biometric screening programs cutting employee healthcare costs by USD 24.25 per member per month and uncovering hidden risks in 16% of participants. Governments also subsidize preventive diagnostics; Medicare expanded reimbursement for metabolic panels used in chronic-care management in 2025. Mass-media campaigns in Canada and Germany highlight silent kidney disease, nudging at-risk adults toward routine chemistry testing. Pharmacies now bundle metabolic screens with vaccination drives, widening consumer access. Together, these actions move panels from episodic to scheduled care, elevating test volumes and stabilizing reagent demand across the comprehensive metabolic panel market.

Rising Global Burden of Chronic Kidney, Liver & Diabetes Cases

Diabetes cases are projected to hit 1.31 billion by 2050, anchoring long-term demand for metabolic monitoring. Chronic kidney disease (CKD) already affects 673 million people worldwide, with type 2 diabetes the primary driver of CKD-related deaths. In China, adult diabetes prevalence reached 13.7% in 2023 and could double without intervention[1]Yu-Chang Zhou et al., “Diabetes Prevalence and Burden in China to 2050,” mmrjournal.biomedcentral.com. Such statistics compel payers to reimburse routine CMPs for early detection and risk stratification. As metabolic dysfunction-associated steatotic liver disease gains clinical recognition, liver function markers embedded in CMPs gain additional relevance. Long-term epidemiological pressure therefore injects a durable 1.8-percentage-point lift into forecast CAGR for the comprehensive metabolic panel market.

Rapid Adoption of POC Chemistry Analyzers in Ambulatory Settings

Abbott’s Piccolo Xpress runs a 31-test metabolic disk in 12 minutes, enabling urgent-care clinics to bypass core labs. Siemens Healthineers’ epoc system uploads wireless results to electronic records in under 60 seconds for emergency decisions. Adoption is fastest in ambulatory surgery centers, retail clinics, and telehealth kits, advancing decentralized care delivery while alleviating core-lab backlogs. For suppliers, this shift redistributes reagent revenue toward cartridge-based formats and elevates instrument placements among non-traditional buyers.

AI-Driven Decision-Support Embedded into CMP Workflows

Laboratories increasingly combine AI autoverification with machine-learning reflex testing to triage abnormal CMP results in real time, cutting manual review rates by 30% and invalid reports by 77%[2]Ankit Gupta et al., “Precision Partners: AI in Diagnostic Labs for Clinical Decision Support,” mlo-online.com. AI chatbots interpret reports for patients, reducing anxiety and improving understanding of abnormal values. Quest Diagnostics’ alliance with Google Cloud adds generative AI that surfaces longitudinal patterns across billions of test results, assisting physicians with earlier disease detection. Although data-privacy hurdles persist, pilot deployments across US hospital networks prove clinical and economic value, steering widespread adoption by 2027.

Restraints Impact Analysis of Comprehensive Metabolic Panel Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified clinical chemists & lab technicians | -1.4% | Global; most acute in North America & EU | Long term (≥ 4 years) |

| Stringent CLIA-88 & EU IVDR compliance costs | -0.8% | North America & EU primarily | Medium term (2-4 years) |

| Data-exchange gaps between LIS and EHR ecosystems | -0.6% | Global; varies by system maturity | Medium term (2-4 years) |

| Rising price volatility of high-grade enzyme reagents | -0.7% | Global; supply-chain dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Clinical Chemists & Lab Technicians

Nearly 46% of US clinical laboratory positions are vacant, and only 5,000 graduates enter the workforce annually against demand for 26,000. New CLIA personnel rules effective January 2025 require higher educational credentials and supervised rotations, narrowing the applicant pool. Canada and parts of Western Europe face similar deficits, driving overtime costs and lengthening turnaround times. Staffing gaps slow instrument adoption because laboratories cannot run additional shifts, subtracting an estimated 1.4-percentage-point from forecast CAGR for the comprehensive metabolic panel market.

Stringent CLIA-88 & EU IVDR Compliance Costs

The FDA’s LDT final rule mandates phased compliance with medical-device regulations, imposing design-control and premarket submission costs that can exceed USD 1 million per high-complexity assay. EU laboratories grapple with IVDR requirements for extensive documentation and periodic surveillance audits. Smaller independent laboratories must either outsource validation or consolidate, dampening capital expenditure on new CMP platforms. Compliance overhead compresses margins and may deter market entrants, reducing forecast CAGR by another 0.8 percentage-point.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Comprehensive Metabolic Panel Market Segment Analysis

By Test Type:

Glucose Testing Drives InnovationKidney Function Tests accounted for 31.12% of the comprehensive metabolic panel market in 2025, supported by CKD screening mandates in primary care. Glucose testing, however, is expanding fastest at a 9.12% CAGR as diabetes programs embed fasting glucose and HbA1c within every CMP. Proteins testing grows steadily as albumin status gains importance in surgical risk scoring, while electrolytes panels remain indispensable in critical-care triage. Liver Function Tests draw renewed attention amid rising metabolic dysfunction-associated steatotic liver disease prevalence.

Continuous glucose monitoring trends spur novel specimen-collection products that blend capillary sampling with central-lab accuracy. Labcorp’s at-home glucose risk device achieved 97% concordance with venous draws, broadening direct-to-consumer uptake. Roche’s Elecsys PRO-C3 leverages advanced biomarkers to stage liver fibrosis more precisely. AI algorithms embedded in glucose panels flag early glycemic variability, enabling personalized management plans. Collectively, these advances cement glucose testing’s leadership in new-revenue creation and enhance the comprehensive metabolic panel market size for digital-health-linked assays.

By Disease:

Diabetes Testing AcceleratesKidney-disease testing commands 32.95% of comprehensive metabolic panel market share, reflecting integrated CKD-diabetes protocols across nephrology and primary-care networks. Diabetes-specific CMPs, however, register the fastest 7.92% CAGR to 2031. The CITE study in India showed 32% CKD prevalence among type 2 diabetes patients, underscoring the interconnected pathophysiology that drives dual testing. Metabolic panels also broaden to cover liver enzymes for early detection of steatotic liver disease linked to insulin resistance. Emerging “other diseases” segments include cardiovascular-risk CMPs that integrate advanced lipid markers.

Expanded reimbursement for diabetes management in the United States now covers quarterly CMP monitoring, lifting routine test frequency. Asian health ministries adopt similar guidelines as diabetes counts climb, anchoring steady demand. Advanced panels that incorporate neurometabolic markers, such as Fujirebio’s FDA-cleared pTau 217 for Alzheimer’s, illustrate how CMP platforms diversify into adjacent disease areas. Increased disease-specific customization therefore positions the comprehensive metabolic panel industry to tap new clinical budgets beyond traditional metabolic disorders.

By End User:

Point-of-Care Centers Transform TestingIndependent & Hospital Laboratories processed 63.10% of global CMP volume in 2025, leveraging automation and Six-Sigma-grade assays that meet tighter quality targets. The comprehensive metabolic panel market size generated by Point-of-Care Centers is growing at a 8.83% CAGR, reflecting demand for immediate results in retail clinics, ambulances, and home-health chains. BD’s MiniDraw capillary-collection device equalizes fingertip accuracy with venous draws, enabling non-phlebotomists to perform tests.

Hospital labs counter decentralization by integrating rapid-turnaround modules like Siemens Healthineers’ Atellica Solution, which completes critical assays in under 10 minutes. Meanwhile, telehealth providers forge lab partnerships for home-sampling kits, illustrated by Locke Bio and imaware’s collaboration. These dual tracks of central-lab modernization and POC proliferation collectively broaden revenue channels across the comprehensive metabolic panel market.

Geography Analysis

North America Comprehensive Metabolic Panel Market

North America held 36.45% of comprehensive metabolic panel market revenue in 2025 owing to sophisticated insurance coverage and employer wellness programs that subsidize routine testing. The United States further benefitted from AI pilot deployments in major hospital networks, while Canada leveraged public-health campaigns encouraging metabolic screens during flu-shot visits. Mexico’s federal health reform accelerated POC adoption across community clinics. The 2024 FDA LDT rule added upfront compliance costs but also formed a clear approval pathway that boosts investor confidence.

Europe Comprehensive Metabolic Panel Market

Europe remains the second-largest contributor as national health systems integrate CMPs into chronic-disease management protocols. Germany, the United Kingdom, and France upgraded chemistry platforms to AI-ready configurations, while Spain and Italy piloted home-collection partnerships. The EU IVDR raised documentation requirements, nudging small labs toward strategic alliances or outsourcing. NHS England’s Long-Term Plan promotes POC chemistry in community health hubs, catalyzing decentralized testing. Eastern European countries modernize laboratories through EU cohesion funds, importing integrated chemistry-immunoassay platforms.

APAC Comprehensive Metabolic Panel Market

Asia-Pacific delivers the fastest 9.05% CAGR through 2031. China’s soaring diabetes prevalence drives nationwide CMP screening campaigns aligned with its Healthy China 2030 strategy. Japan and South Korea adopt AI-assisted autoverification to address technician shortages, while Australia links POC devices to My Health Record for real-time data aggregation. India’s diagnostics sector grows at 8-9% CAGR as private chains expand laboratory networks. Southeast Asian nations invest in containerized mobile labs for remote areas, widening access to CMP testing.

MEA and South America Comprehensive Metabolic Panel Market

The Middle East and Africa region invests in centralized mega-labs within Gulf Cooperation Council states and rolls out POC analyzers in primary-care centers. South Africa’s National Health Insurance roadmap lists CMPs among essential diagnostics, stimulating procurement. South America sees incremental growth led by Brazil and Argentina, where private insurers fund annual metabolic screens as part of chronic-disease bundles. Across all emerging regions, donor-funded programs targeting diabetes and kidney disease build foundational volume for the comprehensive metabolic panel market.

Competitive Landscape

The comprehensive metabolic panel market exhibits moderate concentration. Abbott, Roche, Siemens Healthineers, and Beckman Coulter anchor the top tier with integrated platforms that marry chemistry and immunoassay throughput. Abbott’s Alinity ci-series reaches 1,550 CMP tests per hour, and 86% of its assays meet Six-Sigma quality, slashing repeat runs. Roche moved downstream by acquiring LumiraDx’s POC portfolio for up to USD 350 million, signalling its commitment to decentralized workflows. Siemens Healthineers continues to enhance the Atellica ecosystem with AI readiness and modular expansion capability.

Strategic moves focus on AI, home sampling, and vertical integration. Quest Diagnostics’ partnership with Google Cloud embeds generative AI into data analysis pipelines. Labcorp’s acquisitions of BioReference assets broaden specialty-test menus and extend consumer-direct reach. ABB’s dual-robot Lab Table II showcases how robotics address labor shortages, running 160 samples per hour in a German dark lab.

Emerging disruptors emphasize ultra-sensitive biomarker detection and telehealth integration. Quanterix’s planned acquisition of Akoya Biosciences will create an end-to-end platform for blood- and tissue-based proteins. Start-ups such as SpinChip, soon to be purchased by bioMérieux, promise microfluidic CMP cartridges delivering results in minutes at the bedside. Competitive emphasis is shifting toward ecosystem play: vendors bundle instruments, reagents, connectivity, and AI analytics into subscription models that lower upfront costs while locking in reagent revenue.

Concurrently, Six-Sigma service models and Total Value of Ownership contracts enable suppliers to guarantee turnaround-time targets. Hospitals sign multiyear reagent rental agreements tied to performance metrics, fostering stickiness. Overall, technological differentiation, bundled service offerings, and digital-health collaborations define the evolving rivalry within the comprehensive metabolic panel market.

Comprehensive Metabolic Panel Industry Leaders

Quest Diagnostics

Laboratory Corporation of America Holdings

Sonic Healthcare Ltd.

SYNLAB Group

Eurofins Scientific

- *Disclaimer: Major Players sorted in no particular order

Comprehensive Metabolic Panel Market Companies Covered in this Report

- Quest Diagnostics

- LabCorp

- Sonic Healthcare Ltd.

- SYNLAB Group

- Eurofins

- Mayo Clinic Laboratories

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Danaher Corp. (Integrated Dx)

- ARUP Laboratories

- Charles River

- NeoGenomics Laboratories

- Genoptix

- Centogene

- Unipath Limited

- BioReference Laboratories

- Scion Lab Services

- TCG

- Medicover Diagnostics

Recent Industry Developments in Comprehensive Metabolic Panel Market

- May 2025: Fujirebio received FDA 510(k) clearance for its Lumipulse G pTau 217/β-Amyloid 1-42 Plasma Ratio test, the first FDA-cleared blood-based IVD for amyloid pathology.

- January 2025: Roche secured FDA clearance for the Tina-quant Lipoprotein (a) Gen.2 assay, enabling cardiovascular risk assessment in molar units.

Comprehensive Metabolic Panel Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the comprehensive metabolic panel (CMP) market as every laboratory-processed or point-of-care blood chemistry panel that, in one draw, quantifies fourteen core biomarkers (glucose, calcium, standard electrolytes, and routine liver-plus-kidney enzymes). We convert each billed test, whether inpatient bundle, outpatient requisition, or physician-office order, into net revenue expressed in 2024 constant US dollars.

Scope exclusion: stand-alone single-analyte assays, veterinary CMPs, and reagent-rental agreements lacking per-test revenue.

Segments Covered in This Report

- By Test Type

- Proteins

- Kidney Function Tests

- Electrolytes Panel

- Liver Function Tests

- Glucose

- Other Test Types

- By Disease

- Kidney Diseases

- Diabetes

- Liver Diseases

- Other Diseases

- By End User

- Point-of-Care Centers

- Independent & Hospital Laboratories

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts then interview pathologists, lab managers, kit distributors, and payer advisers across North America, Europe, Asia-Pacific, and Latin America. These dialogues verify price spreads, point-of-care penetration, and ordering habits, closing gaps flagged during desk work.

Desk Research

We start by extracting CMP claim volumes, fee schedules, and disease prevalence from open sources such as the WHO Global Health Observatory, US CDC, CMS, and Eurostat. Trade bodies like the Clinical Laboratory Management Association and regional IVD associations supplement this with analyzer shipment and utilization signals. Company 10-Ks, investor decks, and verified news archived in Dow Jones Factiva, together with patent analytics from Questel, help our team map price dispersion and automation uptake. The references above illustrate, not exhaust, the secondary material consulted.

Market-Sizing & Forecasting

A top-down model rebuilds national test volumes from insurance and public billing data, multiplies them by weighted average selling prices, and adjusts for payer mix. Supplier roll-ups and sampled ASP-by-volume checks act as a bottom-up sense test that tunes totals. Core drivers tracked include diabetes and chronic kidney disease prevalence, CMP orders per inpatient stay, analyzer throughput upgrades, reimbursement resets, and typical lab operating costs. Multivariate regression combined with scenario analysis projects these levers through 2030.

Data Validation & Update Cycle

Outputs run through variance scans, peer review, and senior sign-off. We refresh every twelve months and issue interim updates whenever material regulatory or reimbursement shifts arise, ensuring clients receive the latest view.

How Mordor Intelligence's Comprehensive Metabolic Panel Market Size Compares to Other Published Estimates

Published numbers diverge because research houses apply differing test lists, price curves, and refresh intervals. By disclosing every variable and recalibrating them annually, Mordor Intelligence limits drift and enhances comparability.

Key gap drivers versus other publishers include whether bundled chemistry groups are counted, the steepness of price-erosion curves, and treatment of uninsured self-pay volumes. Some models stay frozen for years; our analysts revisit inputs each cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.57 B | Mordor Intelligence | - |

| USD 14.02 B | Global Consultancy A | Counts lipid and HbA1c panels; uses static tariff pricing |

| USD 15.78 B | Industry Journal B | Converts analyzer sales into revenue; minimal discount adjustment |

These contrasts show how unvetted scope creep or optimistic pricing can move totals by billions, while Mordor's disciplined variable selection and yearly field checks give decision-makers a balanced, transparent baseline.

Key Questions Answered in the Report

What is the current size of the comprehensive metabolic panel market?

The market stands at USD 13.42 billion in 2026 and is projected to grow to USD 18.63 billion by 2031 at a 6.78% CAGR.

Which test type is growing fastest within comprehensive metabolic panels?

Glucose testing posts the highest 9.12% CAGR through 2031, driven by the global diabetes surge and advances in home-based sampling.

Why are point-of-care centers important for market growth?

POC centers deliver lab-quality CMP results in minutes, supporting immediate clinical decisions and registering a 8.83% CAGR—the fastest among end users.

How does the new FDA LDT rule affect laboratories?

The rule introduces medical-device-grade design controls, reporting, and premarket reviews, raising compliance costs but clarifying approval pathways for CMP assays.

Which region shows the highest growth potential?

Asia-Pacific is forecast to expand at a 9.05% CAGR, supported by expanding healthcare access and rising chronic disease prevalence.

Page last updated on: