Colombia Plastic Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

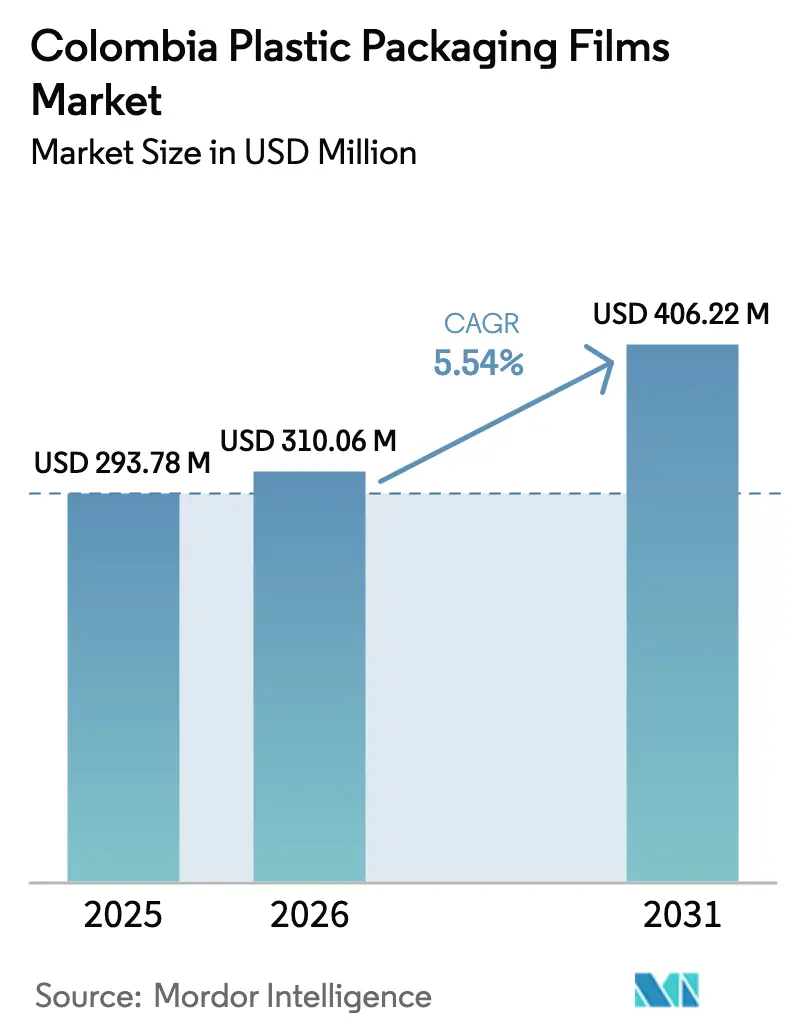

| Base Year Market Size (2025) | USD 293.78 Million |

| Market Size (2026) | USD 310.06 Million |

| Market Size (2031) | USD 406.22 Million |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

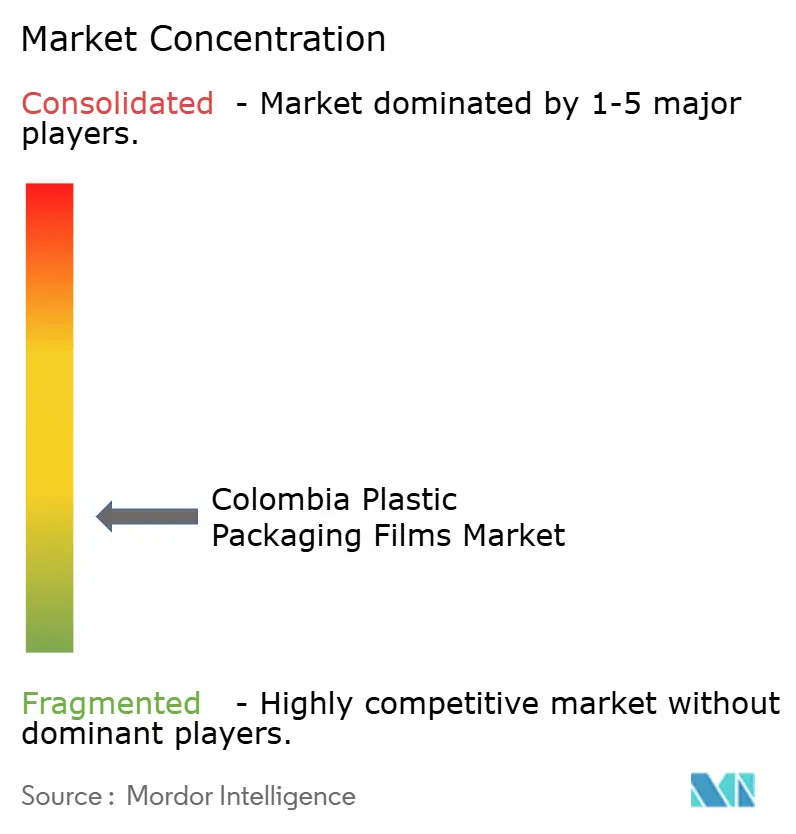

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Plastic Packaging Films Market Analysis by Mordor Intelligence

The Colombia plastic packaging films market size in 2026 is estimated at USD 310.06 million, growing from 2025 value of USD 293.78 million with 2031 projections showing USD 406.22 million, growing at 5.54% CAGR over 2026-2031. Bioplastics investments, regulatory pressure to phase out single-use plastics, and strong demand from export-oriented food processors continue to expand revenue streams. Producers have accelerated the launch of recyclable mono-material structures that cut carbon footprints by more than 50% while safeguarding oxygen and moisture barriers. Colombia’s export-focused coffee, cocoa, and processed-food industries specify multilayer films that meet international shelf-life mandates, while urban retailers favor lightweight packs that reduce logistics costs. Healthcare converters are also upgrading to medical-grade PET films with post-consumer recycled (PCR) content to comply with stricter sterilization rules.

Key Report Takeaways

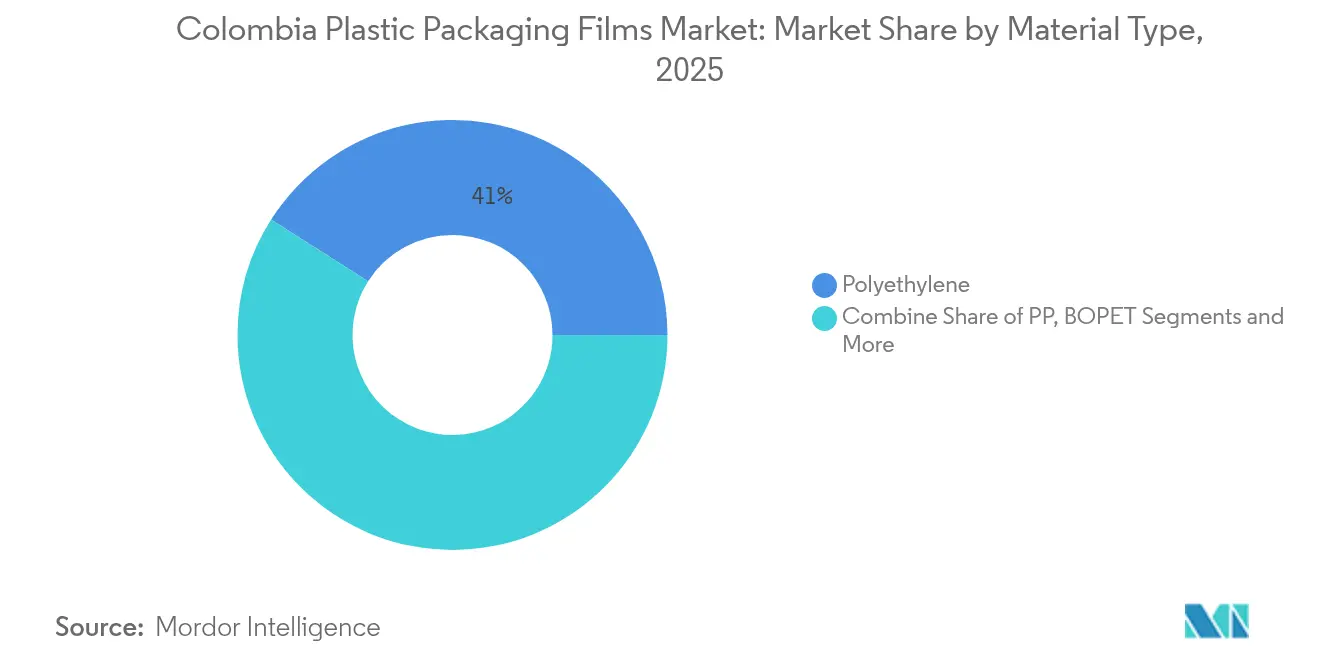

- By material type, polyethylene held 40.98% of the Colombia plastic packaging films market share in 2025; bioplastics are projected to grow at a 9.22% CAGR through 2031.

- By end-use industry, the food segment led with 56.42% of revenue in 2025; healthcare packaging is poised to expand at a 7.55% CAGR to 2031.

- By film functionality, low-barrier mono-material films commanded 61.67% of the Colombia plastic packaging films market size in 2025, while high-barrier multilayer films are set to rise at a 6.58% CAGR.

- By packaging format, wraps and overwraps accounted for 45.12% of sales in 2025; pouches are forecast to record a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Colombia Plastic Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for lightweight flexible packs in urban retail | +1.2% | National, concentrated in Bogotá, Medellín, Cali | Short term (≤ 2 years) |

| Rapid expansion of Colombia's processed-food exports | +1.8% | National, with export hubs in Cartagena, Buenaventura | Medium term (2-4 years) |

| Cost advantages of films over rigid formats for SMEs | +0.9% | National, particularly affecting regional manufacturers | Short term (≤ 2 years) |

| Growth of e-commerce requiring durable secondary packaging | +0.7% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Bogotá zero-waste public-procurement mandates | +0.3% | Bogotá metropolitan area, potential national expansion | Long term (≥ 4 years) |

| Coffee-capsule film uptake by specialty roasters | +0.4% | Coffee-growing regions, urban specialty markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for lightweight flexible packs in urban retail

Supermarkets in Bogotá, Medellín, and Cali are replacing rigid containers with pouches and flow wraps to reclaim shelf space as average retail rents climbed 15% during 2024. [1]Departamento Nacional de Planeación, “La industria redujo su producción real en 2023,” dnp.gov.co Brand owners achieve weight reductions of up to 40% per stock-keeping unit and cut logistics emissions, which aligns with Law 2232 targets. Inflation of 5.1% in March 2025 further intensifies the hunt for lower-cost packs, driving small snack and personal-care brands to switch to stand-up pouches that improve price-point competitiveness.

Rapid expansion of Colombia’s processed-food exports

Coffee output rose 8.1% year on year in 2024, and overall agricultural GDP advanced 2.5%, fuelling demand for high-barrier laminates that secure flavor and aroma during trans-Pacific shipments. [2]Corficol, “Perspectivas de crecimiento y precios del sector agropecuario para 2024,” corfi.comFood processors targeting North American and European markets now specify multilayer films with EVOH and aluminum oxide barriers to meet shelf-life guarantees. Falling farm input prices—down 7.5% in 2024—free capital for packaging upgrades, and customs data shows steady gains in export tonnage to the United States, Ecuador, and Chile.

Cost advantages of films over rigid formats for SMEs

Flexible rolls require 40-60% less resin than comparable rigid packs, slash warehouse footprints, and ship flat, which resonates with small enterprises navigating thin margins. Polyethylene zippers and laser-scored tear lines allow SMEs to launch premium-looking packs without costly injection-mold tooling, supporting the Colombia plastic packaging films market’s resilience among regional manufacturers.

Growth of e-commerce requiring durable secondary packaging

Digital platforms extend beyond the major three cities into mid-tier markets, demanding co-extruded mailer films with puncture resistance and tamper-evident seals. Retailers specify moisture-guard properties to cover deliveries that transit from humid coastal warehouses to cooler Andean altitudes, reinforcing steady volume gains for high-strength polyethylene collation shrink films.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ley 2232 escalating single-use-plastic tax | -1.4% | National implementation, stricter in major cities | Short term (≤ 2 years) |

| Resin-price volatility tied to Brent crude | -0.8% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Local shortage of post-consumer PCR feedstock | -0.6% | National, more acute in interior regions | Medium term (2-4 years) |

| Rise of cellulose-based compostable wraps | -0.3% | Urban markets, premium segments initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ley 2232 escalating single-use-plastic tax

Effective July 2024, Law 2232 levies an annually rising tax on specific single-use items and sets mandatory collection and recycling quotas. Producers must fund take-back schemes or face penalties, which raises compliance costs, particularly for firms lacking dedicated environmental teams. [3]Olga Sanmartín, “¿Cómo impactará la prohibición de plásticos en Colombia?,” cambiocolombia.com

Resin-price volatility tied to Brent crude

Polyethylene and polypropylene prices can swing 15-20% within a quarter, squeezing margins for converters that import most feedstocks and operate under a peso that tends to track oil price cycles. Larger multinationals hedge purchases, but small converters often absorb cost spikes or lose volume when passing increases to customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bioplastics innovation accelerates

Polyethylene retained a 40.98% share of the Colombia plastic packaging films market in 2025 thanks to established converter networks and broad suitability for food wraps and mailers. Yet the bioplastics sub-segment is growing at a 9.22% CAGR because law-driven demand for compostable or bio-based packs is redirecting capital toward cassava-starch and sugar-cane formulations. Natpacking’s 100% cassava-based bag line illustrates how local feedstocks shorten supply chains and appeal to brands seeking a Colombian provenance story. Polypropylene remains essential for microwaveable snack and hot-fill sauces that require higher heat tolerance. BOPET uptake centers on premium coffee and confectionery exports. Polystyrene and PVC lag because they trigger higher recycling fees under municipal waste regulations.

As converters reformulate toward PCR blends, several plants now co-extrude 30-50% recycled content without sacrificing seal strength. Multilayer barrier baselines continue to lean on polyethylene matrices with EVOH or metallization layers, but mono-material innovation is narrowing performance gaps. The Colombia plastic packaging films market size for bioplastics is projected to achieve USD 57.9 million by 2031, reflecting this shift. Continuous R&D investment ensures that bio-based films meet migration limits for direct food contact while offering comparable puncture resistance.

By End-use Industry: Healthcare expansion outpaces food growth

Food applications generated 56.42% of 2025 revenue, supported by rising consumption of processed snacks, bakery goods, and fresh produce. The Colombia plastic packaging films market size within healthcare, however, is accelerating at a 7.55% CAGR, underpinned by local pharmaceutical batch expansions and tighter sterilization codes. Evertis’ Evercare PET films with 50% PCR content now satisfy gamma-irradiation compatibility, enabling clinics to meet infection-control protocols while progressing toward circular-economy goals.

Home-care and personal-care categories benefit from refill pouch trends that cut plastic use by up to 70% per refill cycle and align with retailer waste-reduction pledges. Industrial users, automotive, electronics, and fertilizers, continue to require heavy-duty liners and films, but growth trails the overall average as producers optimize packaging weight.

By Film Functionality: Barrier technology advances

Low-barrier mono-material constructions captured 61.67% of 2025 demand due to easy recyclability and low cost. High-barrier multilayer grades are projected to expand 6.58% per year through 2031 as food exporters and drug makers lengthen distribution cycles. Metallized BOPP and AlOx-coated PET open three-to-five-year shelf-life windows for dehydrated coffee capsules and powdered chocolate mixes. Meanwhile, brand owners invest in EVOH-rich mono-material PE films that retain recycle-stream compatibility while reducing oxygen transmission rates to under 0.4 cc/m²/day.

R&D teams are also examining antimicrobial additives that curb bacterial growth on medical drapes and meat wraps. Active scavenger films targeting moisture and ethylene are in pilot testing with Colombian banana and avocado shippers looking to cut post-harvest losses.

By Packaging Format: Pouches surge on convenience trends

Wraps and overwraps commanded 45.12% of revenue in 2025, mainly bread bags, produce sheets, and shrink bundles. Pouches are forecast to grow at a 9.05% CAGR as consumers gravitate toward resealable, lightweight options that maximize pantry space. Coffee roasters have adopted aluminum-free high-barrier pouches with degassing valves, enabling an export-ready presentation that fits capsule machines. FLtècnics’ AutoSplicer Pro roll-splicing technology trimmed waste and boosted pouch-line uptime by 10%, underscoring capital spending that sustains format shifts.

Bulk bags and multiwall liners remain significant in fertilizers and pet-food channels but show slower velocity. Vacuum shrink and stretch hoods hold stable demand in beverage multipacks despite the rise of corrugated alternatives, as film keeps unit cost lower for domestic bottlers.

Geography Analysis

The Colombia plastic packaging films market is clustered in Bogotá, Medellín, and Cali, which together draw around 60% of national consumption. Bogotá accounts for the largest slice thanks to dense retail chains and government procurement that now mandates recycled or recyclable packs. The return of Label Summit Latin America to the capital in 2024 attracted 750 delegates, underscoring the city’s status as a packaging innovation hub.

Coastal corridors anchored by Cartagena and Buenaventura handle a high share of export-grade films. Their port logistics favor quick containerization of coffee, tropical fruits, and processed foods bound for the United States and Europe. Humid Caribbean climates necessitate moisture-barrier enhancements, creating opportunities for metallized and AlOx coatings. Inland coffee belts near Medellín demand specialty laminates for roast-and-ground bags as well as oxygen-barrier capsule lidding.

Secondary cities such as Bucaramanga, Pereira, and Pasto now register elevated e-commerce parcel flows that rely on durable mailer films. Yet recycling systems remain less developed outside major hubs, and PCR feedstock shortages curb local closed-loop ambitions. Film suppliers that establish collection partnerships in these regions can secure input streams and earn tax credits under Law 2232.

Competitive Landscape

Global majors Amcor, Sealed Air, and Mondi share the stage with local names Distripacking Colombia SAS, Plafilm SA, and Empaques Transparentes SA. Compliance costs tied to recycled-content quotas are spurring gradual consolidation as scale advantages matter more. ExxonMobil’s technical partnership with Plastilene on PCR-rich collation shrink film exemplifies how resin suppliers back converter innovation to secure downstream demand.

R&D pipelines now center on mono-material solutions, digital printing for SKU agility, and bio-based resins. Amcor pledged to source mechanically recycled polyethylene from NOVA Chemicals’ new Indiana facility, aligning supply to reach its 30% recycled-content target by 2030. [4]Amcor, “Amcor and NOVA Chemicals announce agreement to source mechanically recycled polyethylene,” amcor.comMondi expanded extrusion capacity in Europe, providing barrier PE grades adaptable to Latin American climate profiles.

Local converters such as Flexo Spring invest in 8-color flexographic presses to service regional brands with short-run graphics, while smaller firms pivot to niche offerings like compostable syringe overwraps. Bio-specialists Natpacking and start-ups experimenting with sugar-cane PLA blends may carve market share in premium retail. Success now hinges less on cost leadership and more on rapid regulatory compliance, PCR sourcing, and application engineering.

Colombia Plastic Packaging Films Industry Leaders

Taghleef Industries

Distripacking Colombia SAS

Plafilm SA

Amcor Plc

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ExxonMobil and Winpack launched stretch films containing 50% PCR and simultaneously partnered with Plastilene on shrink films for the Colombia plastic packaging films market.

- March 2025: Línea Adhesiva expanded its Bogotá plant with a Nilpeter FB-17 press to diversify laminated-film offerings and raise throughput for regional food customers.

- January 2025: Amcor signed a memorandum of understanding with NOVA Chemicals to secure mechanically recycled polyethylene, supporting a target of 30% recycled content in Colombia-made films by 2030.

- June 2024: Amcor unveiled Colombia’s first designed-to-be-recycled high-barrier sachet for powdered chocolate, cutting the pack’s carbon footprint by 53% and water consumption by 84% during recycling.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines Colombia's plastic-packaging-films market as the annual demand for newly extruded or converted polymer films, principally PE, PP (BOPP & CPP), PET, PVC, EVOH, and emerging bio-based grades, sold to brand owners, co-packers, and industrial users for wrapping, lidding, pouches, sachets, and lamination. Values mirror ex-factory prices of finished rolls and exclude rigid formats, shrink sleeves, labels, and any value of the packed goods.

Scope exclusion: thermoformed trays, blister sheets, agricultural mulch, and stretch-wrap used strictly for palletization are outside this study.

Segmentation Overview

- By Material Type

- Polypropylene (PP)

- Polyethylene (PE)

- Polyethylene-terephthalate (BOPET)

- Polystyrene (OPS)

- Polyvinyl-chloride (PVC)

- Bioplastics

- Other Material Types

- By End-use Industry

- Food

- Candy and Confectionery

- Frozen Foods

- Fresh Produce

- Dairy Products

- Dry Foods

- Meat, Poultry and Seafood

- Pet Food

- Other Food Products

- Healthcare

- Personal Care and Home Care

- Industrial Packaging

- Other End-use Industry

- Food

- By Film Functionality

- Low-Barrier Mono-material Films

- Medium-Barrier Metallised Films

- High-Barrier Multilayer Films

- Specialty Active and Antimicrobial Films

- By Packaging Format

- Wraps and Overwraps

- Bags and Linings

- Pouches (stand-up, spouted)

- Other Packging Format

Detailed Research Methodology and Data Validation

Primary Research

Conversations with converters, FMCG procurement managers, and logistics specialists across Bogotá, Medellín, and Barranquilla helped us validate average selling prices, gauge pouch-penetration shifts in meat exports, and stress-test resin-cost pass-through assumptions. Insights from sustainability officers clarified likely substitution rates once single-use bans tighten.

Desk Research

Our analysts started with Colombian trade statistics from DANE customs, resin import data via Volza, and packaging output series from ANDI. Industry position papers from Acoplasticos, government gazettes outlining Ley 2232 phases, and peer-reviewed studies on barrier-film recycling supplied policy and technical baselines. Company 10-Ks, local IPO filings, and news archives accessed through Dow Jones Factiva rounded out corporate intelligence. The sources cited are illustrative; many additional publications fed the desk stage.

Market-Sizing & Forecasting

We anchored 2024 volume using import plus domestic extrusion tonnage, then layered a top-down application pool check that ties film intensity to packaged-food output, e-commerce parcel counts, and hospital admission data. Supplier roll-ups and sampled ASP × kilogram benchmarks supplied a selective bottom-up cross-check before totals were reconciled. Key variables like chicken-meat consumption trends, Brent-linked PE price curves, and retail-pouch share feed a multivariate regression that projects demand to 2030. Scenario cushions adjust for resin volatility greater than 15% and for accelerated bio-film uptake.

Data Validation & Update Cycle

Models run through variance flags versus historic trade flows and ANDI production indices. Senior reviewers challenge anomalies, and we re-contact at least three market participants when deviations exceed two standard deviations. Reports refresh every twelve months, with mid-cycle tweaks when material events, such as a new 40 kt BOPP line, occur.

Why Mordor's Colombia Plastic Packaging Films Baseline Commands Reliability

Published estimates differ because firms select divergent product scopes, price points, and refresh rhythms. Some fold in rigid sheets or count retail mark-ups, while others model Latin America averages and apportion to Colombia.

Key gap drivers include: 1) Mordor's focus on converted film rolls only, 2) our mixed top-down and bottom-up cross-walk, 3) annual field interviews that catch swift swings in pouch adoption, and 4) constant-currency adjustment using Banco de la República averages, which contrasts with peers' mid-year FX lifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 293.8 M (2025) | Mordor Intelligence | - |

| USD 250 M (2023) | Regional Consultancy A | Includes semi-rigid barrier sheets and applies uniform LATAM growth proxies without Colombia-specific trade checks |

| USD 890 M (2023) | Industry Journal B | Values computed at retail-pack level and embeds shrink-wrap and labels, inflating base significantly |

In sum, by limiting the scope to true flexible films, triangulating volumes with customs and plant audits, and updating models on a strict yearly cadence, Mordor Intelligence delivers a balanced baseline that decision-makers can trace back to clear, repeatable variables.

Key Questions Answered in the Report

What is the current value of the Colombia plastic packaging films market?

The market is valued at USD 310.06 million in 2026 and is projected to reach USD 406.22 million by 2031.

Which material leads the market today?

Polyethylene leads with a 40.98% share, though bioplastics are expanding fastest at a 9.22% CAGR.

Why are pouches gaining popularity?

Pouches provide resealability, lightweight logistics advantages, and strong retail shelf appeal, helping them grow at a 9.05% CAGR through 2031.

How does Law 2232 impact manufacturers?

The law imposes escalating taxes on single-use plastics and mandates collection quotas, increasing compliance costs and spurring investment in recyclable or bio-based films.

Which end-use segment is forecast to grow most rapidly?

Healthcare packaging is set to grow at a 7.55% CAGR as stricter sterilization standards boost demand for medical-grade PET and PE films.

Page last updated on: