Food Cold Chain Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

| Market Size (2025) | USD 70.55 Billion |

| Market Size (2030) | USD 121.77 Billion |

| Growth Rate (2025 - 2030) | 11.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Cold Chain Market Analysis by Mordor Intelligence

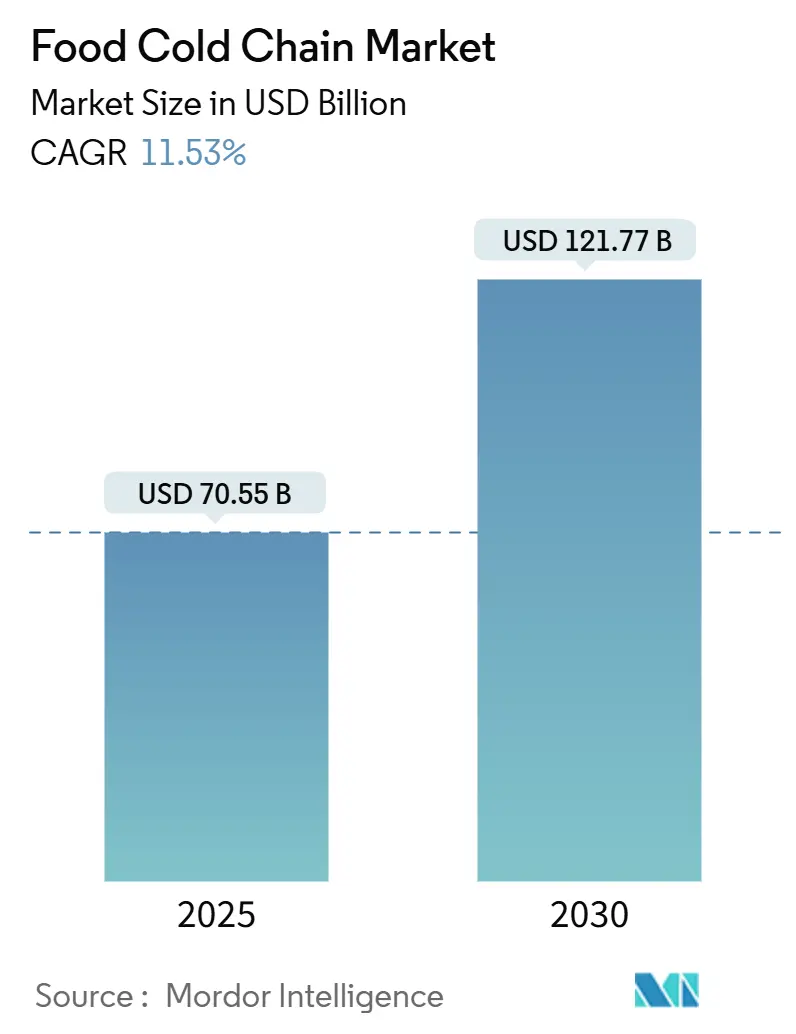

The global Food Cold Chain Market reached USD 70.55 billion in 2025 and is projected to expand to USD 121.77 billion by 2030, representing a robust compound annual growth rate (CAGR) of 11.53% during the forecast period. This acceleration reflects the convergence of stringent food safety regulations, technological disruptions in temperature monitoring, and the explosive growth of ready-to-eat convenience foods that demand uncompromised cold chain integrity from farm to fork. The market expansion is further supported by rising consumer awareness about food safety, growing international trade of perishable goods, and the rapid development of organized retail sectors across emerging economies.

Regulatory momentum is reshaping market dynamics as the FDA's Food Safety Modernization Act (FSMA) 204 mandates comprehensive traceability for foods on the Food Traceability List by January 2026, compelling operators to invest heavily in digital monitoring infrastructure [1]U.S. Food and Drug Administration, " Food Safety Modernization Act (FSMA)," fda.gov. This regulation specifically impacts high-risk foods such as fresh produce, dairy products, and seafood, requiring companies to maintain records of critical tracking events throughout the supply chain. The implementation of these requirements is driving the adoption of advanced tracking technologies, IoT sensors, and blockchain solutions across the food cold chain industry.

Key Report Takeaways

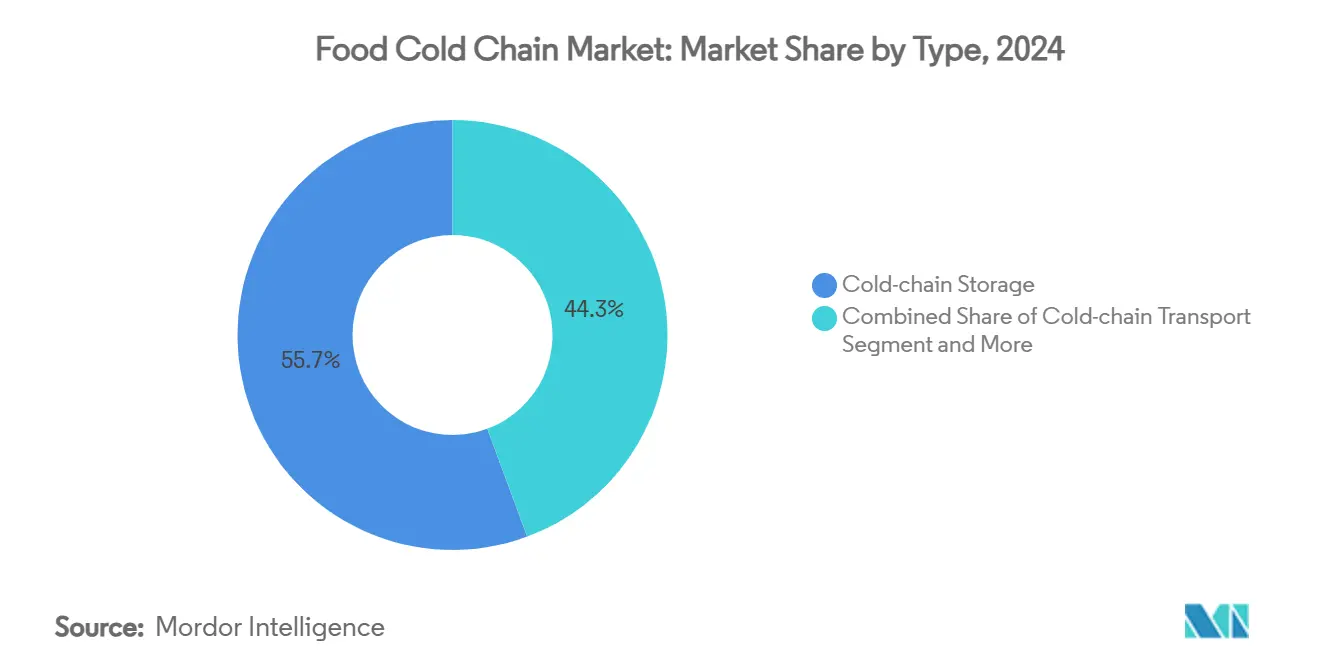

- Cold-chain storage led with 55.66% of the Food Cold Chain market share in 2024; monitoring components are set to expand at a 14.45% CAGR to 2030.

- Chilled (0-4 °C) captured 60.15% revenue share in 2024, whereas frozen (-18 °C) is poised for a 15.49% CAGR through 2030.

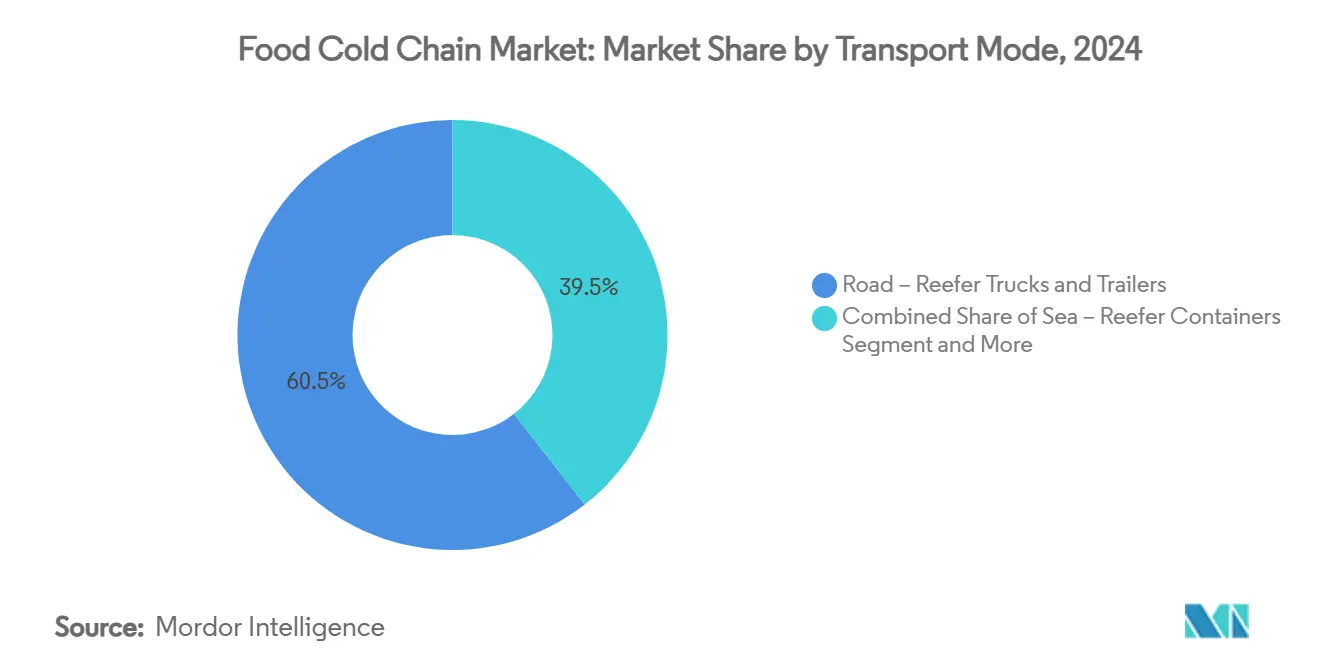

- Road transport held 60.55% of the Food Cold Chain market size in 2024; air cargo is projected to grow at 14.97% CAGR between 2025-2030.

- Meat & seafood commanded 26.46% of 2024 sales, while ready-to-eat meals will rise fastest at 16.54% CAGR.

- RFID and basic real-time monitoring formed 42.14% of the 2024 base; IoT-enabled telematics should log the highest 15.78% CAGR.

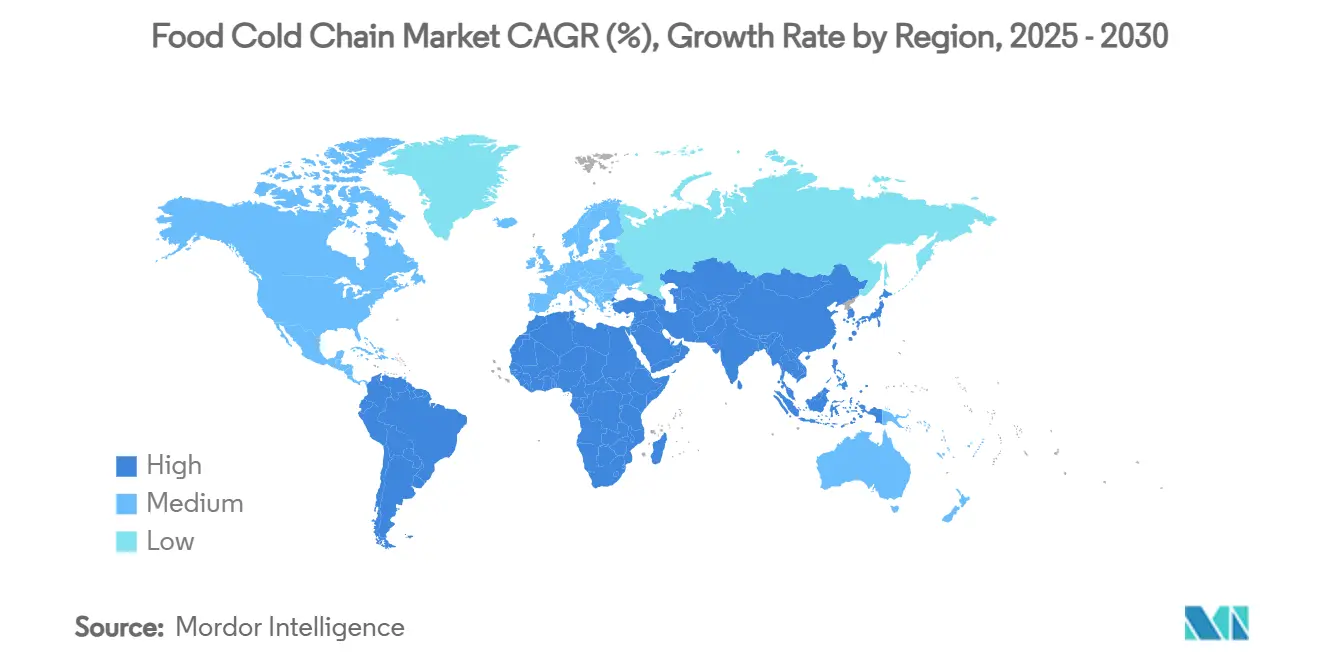

- North America led with a 40.46% share in 2024, yet Asia-Pacific is forecast to climb at a 16.56% CAGR to 2030.

Global Food Cold Chain Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for frozen and perishable food products globally | +2.1% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in international food trade and cross-border food transportation | +1.8% | Global, particularly Asia-Pacific to North America/Europe corridors | Long term (≥ 4 years) |

| Increasing consumer preference for fresh and ready-to-eat convenience foods | +2.3% | North America, Europe, urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Expansion of organized retail and food service sectors | +1.9% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| Technological advancements in refrigeration and temperature monitoring systems | +1.7% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Implementation of strict food safety regulations and quality standards | +1.5% | North America, Europe, with gradual expansion to Asia-Pacific | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Demand for Frozen and Perishable Food Products Globally

The increase in frozen food consumption has changed cold chain capacity requirements globally, with particular impact on warehousing, transportation, and distribution networks. This growth has created high demand for cold storage infrastructure to address supply-demand gaps, leading to significant investments in refrigerated warehouses, temperature-controlled vehicles, and advanced monitoring systems. Consumer behavior changes during the pandemic transformed frozen foods from convenience items to essential products, driving increased purchases across categories including ready meals, vegetables, meat, and seafood, thereby establishing long-term demand patterns that necessitate permanent infrastructure expansion. Cold chain operators emphasize that maintaining consistent temperature controls throughout the supply chain is essential, from production facilities through distribution centers to retail locations, as temperature variations can cause product losses, compromise food safety, trigger costly recalls, and result in regulatory non-compliance. The complexity of temperature management extends to last-mile delivery, where maintaining product integrity requires specialized equipment and precise monitoring protocols.

Growth in International Food Trade and Cross-Border Food Transportation

Cross-border food transportation has evolved into a sophisticated orchestration of temperature-controlled logistics, with China's Ministry of Commerce targeting 25% cold chain circulation rates for fruits and vegetables and 45% for meat by 2027 under its modern commercial circulation system enhancement plan [2]Ministry of Commerce, "Action Plan for Improving the Modern Commercial and Trade Circulation System and Promoting the High-quality Development of the Wholesale and Retail Industry," mofcom.gov.cn . This regulatory push reflects the critical role of international trade in food security, particularly as climate change and geopolitical tensions disrupt traditional supply chains. The complexity of maintaining temperature integrity across multiple jurisdictions has created opportunities for specialized logistics providers who can navigate varying regulatory requirements while ensuring product quality. The integration of blockchain technology and IoT sensors has become essential for providing end-to-end traceability required by importing countries, transforming cross-border food trade from a logistics challenge into a technology-enabled competitive advantage. Temperature-controlled container shipping has emerged as a critical bottleneck, with specialized reefer containers commanding premium rates due to their sophisticated monitoring and control systems.

Increasing Consumer Preference for Fresh and Ready-to-Eat Convenience Foods

The ready-to-eat meals segment's 16.54% CAGR reflects a fundamental shift in consumer behavior that extends beyond convenience to encompass health consciousness and time optimization. Urban professionals increasingly view fresh, minimally processed foods as essential rather than premium options, driving demand for cold chain solutions that can maintain nutritional integrity and sensory qualities throughout distribution. The packaging innovations in this segment, particularly the adoption of retort pouches with PET/Al Foil/PP configurations, demonstrate how cold chain requirements are evolving to support dual ovenable packaging that maintains product quality while reducing preparation time. This trend has created new challenges for cold chain operators, as ready-to-eat products often require multiple temperature zones within the same facility to accommodate different preservation requirements. The integration of modified atmosphere packaging with cold chain logistics has become a competitive differentiator, allowing products to maintain freshness for extended periods while reducing dependency on preservatives.

Expansion of Organized Retail and Food Service Sectors

The organized retail expansion has created a ripple effect throughout the cold chain ecosystem, with major retailers like Walmart and Kroger investing in automated cold storage facilities strategically located to serve urban areas more efficiently. These facilities feature higher storage capacity and advanced cooling technologies that reduce energy consumption while improving inventory turnover rates. The food service sector's growth has been particularly transformative, as restaurants and institutional kitchens demand just-in-time delivery of temperature-sensitive ingredients, creating new requirements for last-mile cold chain solutions. The integration of micro-fulfillment centers with traditional cold storage has emerged as a strategic response to e-commerce demands, allowing retailers to maintain product quality while reducing delivery times. India's Digital Agriculture Mission, with its USD 2,817 crore budget, exemplifies how governments are supporting organized retail expansion through digital infrastructure that enhances supply chain visibility and efficiency [3]Press Information Bureau, “Digital Agriculture Mission Approved,” pib.gov.in. The shift toward organized retail has also standardized cold chain requirements, creating economies of scale that benefit both operators and consumers through improved efficiency and reduced costs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment requirements for cold storage facilities and refrigerated transport vehicles | -1.8% | Global, particularly acute in emerging markets | Long term (≥ 4 years) |

| Power-supply volatility in emerging markets | -1.2% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Temperature control challenges during transportation and storage transitions | -0.9% | Global, with higher impact in regions with inadequate infrastructure | Short term (≤ 2 years) |

| Competition from alternative preservation methods | -0.7% | North America and Europe primarily | Medium term (2-4 years) |

Source: Mordor Intelligence

High Initial Capital Investment Requirements for Cold Storage Facilities and Refrigerated Transport Vehicles

The capital intensity of cold chain infrastructure creates significant barriers to entry, with specialized construction materials and energy-efficient designs commanding premium costs that can exceed conventional warehousing by 300-400%. The construction of cold facilities requires sophisticated insulation systems, specialized flooring, and advanced refrigeration equipment that must operate reliably in extreme temperature conditions, driving up both initial investment and ongoing maintenance costs. Refrigerated transport vehicles face similar cost pressures, with reefer trucks and trailers requiring double-digit rate increases to justify equipment expansion. The financing challenge is compounded by the specialized nature of cold chain assets, which have limited alternative uses and require specialized maintenance expertise.

Competition from Alternative Preservation Methods

Aseptic processing and packaging present a formidable challenge to traditional cold chain logistics by creating shelf-stable products that eliminate refrigeration requirements entirely. The FDA's strict regulations for aseptic processing, including compliance with Current Good Manufacturing Practices and HACCP programs, have validated this technology as a viable alternative for many food categories. This method involves sterilizing products and containers separately, allowing manufacturers to bypass cold chain costs while extending shelf life and preserving nutritional quality. The competitive threat is particularly acute in the beverage and prepared food segments, where aseptic packaging can reduce total supply chain costs by 20-30% compared to refrigerated alternatives. Advanced packaging technologies, including modified atmosphere packaging and active packaging systems, further erode the cold chain's value proposition by extending product shelf life at ambient temperatures. The integration of smart packaging with temperature indicators and freshness sensors creates hybrid solutions that combine the benefits of ambient storage with quality assurance traditionally associated with cold chain logistics. However, consumer preferences for fresh, minimally processed foods continue to favor cold chain solutions, particularly in premium market segments where perceived quality and naturalness command price premiums.

Segment Analysis

Type: Storage Infrastructure Dominates Amid Monitoring Revolution

Cold-chain storage commands the largest market share at 55.66% in 2024, reflecting the fundamental infrastructure requirements for temperature-controlled logistics across all food categories. The segment's dominance stems from the capital-intensive nature of refrigerated warehousing, where specialized facilities with advanced insulation, automated racking systems, and energy-efficient cooling technologies represent the largest cost component in the cold chain ecosystem.

Monitoring components, despite representing a smaller absolute market share, exhibit the fastest growth trajectory at 14.45% CAGR through 2030, driven by regulatory mandates such as FSMA 204 and the increasing sophistication of IoT-enabled temperature tracking systems. The monitoring components segment's rapid expansion reflects a technological inflection point where passive temperature logging is being replaced by real-time, predictive analytics systems that can anticipate equipment failures and optimize energy consumption. Companies like Rivercity Innovations have introduced IoT automated temperature monitoring solutions featuring Early Catastrophic Failure Detection (ECFD) capabilities that predict compressor failures, allowing for timely maintenance and preventing costly product losses.

Note: Segment shares of all individual segments available upon report purchase

Temperature Range: Chilled Dominance Faces Frozen Acceleration

The chilled temperature range (0-4°C) maintains market leadership with a 60.15% share in 2024, reflecting the broad applicability of this temperature zone across fresh produce, dairy products, and prepared foods that constitute the majority of perishable food consumption. However, the frozen segment (-18°C) demonstrates superior growth momentum with a 15.49% CAGR through 2030, driven by changing consumer preferences toward frozen convenience foods and the expansion of frozen food manufacturing capacity globally.

The frozen segment's growth trajectory has prompted major retailers to invest in dual-temperature facilities that can efficiently manage both chilled and frozen products within the same operation, optimizing space utilization and reducing operational complexity. The Move to -15°C coalition, supported by Emirates SkyCargo and other major logistics providers, represents an industry-wide effort to optimize frozen food transportation by adjusting standard temperatures from -18°C to -15°C, potentially reducing energy consumption while maintaining product quality. This initiative demonstrates how temperature range optimization can create competitive advantages through reduced operational costs and environmental impact, while maintaining food safety standards.

Transport Mode: Road Leadership Challenged by Air Cargo Innovation

Road transport via reefer trucks and trailers dominates the transport mode segment with a 60.55% market share in 2024, reflecting the flexibility and cost-effectiveness of trucking for regional and national distribution networks. The segment benefits from established infrastructure, driver availability, and the ability to provide door-to-door service that other transport modes cannot match. Moreover, the development of autonomous vehicle technology and electric refrigerated trucks represents potential disruptors that could reshape the transport mode landscape, though widespread adoption remains several years away.

However, air cargo emerges as the fastest-growing transport mode with a 14.97% CAGR through 2030, driven by the premium food segment's demand for rapid, long-distance transportation and the growth of international food trade. Sea transport via reefer containers serves the bulk commodity trade, while rail transport provides cost-effective solutions for long-distance, high-volume shipments in regions with developed rail infrastructure. The air cargo segment's exceptional growth reflects the premiumization of food logistics, where time-sensitive, high-value products justify the higher transportation costs associated with air freight.

Note: Segment shares of all individual segments available upon report purchase

Application: Meat and Seafood Leadership Yields to Ready-to-Eat Innovation

Meat and seafood applications command the largest market share at 26.46% in 2024, reflecting the stringent temperature requirements and high value of protein products that necessitate sophisticated cold chain infrastructure. This segment benefits from established supply chains, regulatory frameworks, and consumer willingness to pay premium prices for quality assurance. The meat and seafood segment continues to drive infrastructure investment due to its strict regulatory requirements and the high cost of product loss from temperature excursions. The integration of blockchain technology for traceability has become particularly important in this segment, as food safety incidents can have severe financial and reputational consequences for all supply chain participants.

Ready-to-eat meals represent the fastest-growing application segment at 16.54% CAGR through 2030, driven by urbanization trends, changing lifestyles, and the expansion of food service delivery platforms that require reliable cold chain logistics. The ready-to-eat meals segment's rapid growth reflects fundamental changes in consumer behavior and food preparation patterns, particularly in urban markets where convenience and time savings command premium pricing. The segment's growth has created new requirements for cold chain operators, as ready-to-eat products often require multiple temperature zones and specialized packaging to maintain quality and safety throughout distribution.

Technology: RFID Maturity Enables IoT Telematics Acceleration

RFID and real-time monitoring technologies dominate the market with a 42.14% share in 2024. These technologies form the core infrastructure for cold chain operations by enabling temperature monitoring, location tracking, and compliance verification. Their widespread adoption reflects their essential role in maintaining visibility and traceability throughout the cold chain network. RFID tags and sensors continuously transmit data about product conditions, while real-time monitoring systems process this information to provide instant alerts and historical analytics. This comprehensive monitoring capability ensures product quality, reduces spoilage, and helps companies maintain regulatory standards across storage facilities, transportation routes, and distribution centers.

IoT-enabled telematics demonstrates the highest growth potential at 15.78% CAGR through 2030, reflecting the evolution toward predictive analytics, automated decision-making, and integrated supply chain optimization. The technology segment evolution reflects a transition from reactive monitoring to proactive management, where IoT-enabled systems can predict equipment failures, optimize energy consumption, and automatically adjust storage conditions based on product requirements and external factors. The partnership between Trustwell and Wiliot exemplifies this trend, utilizing battery-free smart sensor tags that provide continuous tracking from origin to consumer while reducing manual scanning requirements and enhancing food safety.

Geography Analysis

North America's 40.46% market share in 2024 reflects decades of infrastructure investment and regulatory development that created the world's most sophisticated cold chain ecosystem, yet the region now confronts modernization challenges as legacy facilities struggle with e-commerce demands and sustainability requirements. Major retailers are responding with strategic investments in automated facilities, exemplified by Walmart and Kroger's development of urban-centric cold storage facilities that reduce transportation distances and improve sustainability metrics. The region benefits from established regulatory frameworks and consumer willingness to pay premium prices for quality assurance, yet faces headwinds from aging infrastructure and the need for substantial capital investment to meet modern operational requirements.

The Asia-Pacific cold chain market is projected to grow at a CAGR of 16.56% through 2030, representing the highest growth rate globally. This expansion is primarily driven by supportive government policies aimed at reducing food waste and improving supply chain efficiency. The rapid urbanization across countries like China, India, and Indonesia has increased demand for temperature-controlled storage and transportation services. Modern food distribution networks are replacing traditional infrastructure, incorporating advanced technologies and automated systems. In India, the Pradhan Mantri Kisan Sampada Yojana has approved 394 cold chain projects as of February 2025. These projects focus on establishing integrated cold chain facilities, including refrigerated transportation, cold storage units, and processing centers. The initiative supports India's expanding food processing industry by enabling better preservation of perishable goods, reducing post-harvest losses, and ensuring food safety standards. The program also promotes private sector investment in cold chain infrastructure development, creating a more robust and efficient food distribution system.

Europe maintains steady growth supported by stringent food safety regulations, cross-border trade facilitation, and sustainability initiatives that are reshaping cold chain operations across the continent. The region's focus on sustainability has accelerated the adoption of emission-free refrigerated trailers and advanced digitalization technologies, including digital twin systems for real-time data management that optimize energy consumption and operational efficiency. The region's mature regulatory environment and consumer preferences for fresh, locally sourced foods continue to drive demand for sophisticated cold chain solutions that can maintain product quality while minimizing environmental impact.

Note: Segment shares of all individual regions will be available upon report purchase

Competitive Landscape

The food cold chain market exhibits high fragmentation with a concentration score of 3 out of 10. Major players in the market include Americold Logistics LLC, AGRO Merchants Group, Lineage Logistics Holding LLC, Nichirei Corporation, and VersaCold Logistics Services. This concentration has intensified through aggressive acquisition strategies, with Lineage considering a USD 30 billion IPO following expansion to over 400 temperature-controlled facilities globally, while Americold operates 239 warehouses with 1.4 billion cubic feet capacity, serving approximately 3,300 customers

Strategic patterns reveal a focus on vertical integration and technology-enabled differentiation, with major players investing heavily in automated storage and retrieval systems, IoT monitoring capabilities, and predictive analytics to optimize capacity utilization and reduce operational costs. Americold's disciplined growth strategy emphasizes fixed commitment contracts and operational efficiencies, while maintaining an investment-grade rating that provides access to capital for continued expansion

The market faces competition from new companies using advanced technologies like IoT sensors, blockchain tracking, and automated warehousing systems, along with different business models such as asset-light operations and shared logistics platforms. However, the high capital requirements for refrigerated warehouses, temperature-controlled vehicles, and specialized equipment, combined with the complex operations in cold chain logistics including temperature monitoring, regulatory compliance, and multi-point distribution networks, provide significant advantages to established companies. These incumbent firms benefit from their extensive distribution networks, decades of operational experience, existing customer relationships, and economies of scale in equipment procurement and facility management.

Food Cold Chain Industry Leaders

-

Lineage Logistics Holding LLC

-

Americold Logistics LLC

-

Nichirei Corporation

-

AGRO Merchants Group

-

VersaCold Logistics Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lineage Inc. acquired four cold-storage warehouses from Tyson Foods, for USD 247 million, including facilities in Pottsville, PA, Olathe, KS, Rochelle, IL, and Tolleson, AZ, adding approximately 49 million cubic feet and 160,000 pallet positions while establishing Tyson as an anchor customer for Lineage's new automated warehouses.

- April 2025: Vertical Cold Storage acquired Arctic Logistics in Canton, Michigan, adding 140,000 square feet and over 20,000 pallet positions to strengthen its position as the sixth-largest cold storage company in North America, with storage temperatures ranging from -20°F to 40°F and enhanced capabilities for U.S.-Canada trade.

- January 2024: Kenco Logistic Services acquired The Shippers Group, adding 3.8 million square feet of warehousing space across eight sites in Florida, Georgia, and Texas, significantly expanding its multi-client capabilities and North American cold chain footprint.

Global Food Cold Chain Market Report Scope

The food cold chain is the facility provided for the storage and transportation of frozen food products.

The food cold chain market is segmented by type, application, and geography. By type, the market is segmented into cold chain storage and cold chain transport. By application, the market is segmented into fruits and vegetables, meat and seafood, dairy and frozen dessert, bakery and confectionery, ready-to-eat meals, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

For each segment, the market sizing and forecast have been done based on the value (in USD million).

| By Type | Cold-chain Storage | ||

| Cold-chain Transport | |||

| Monitoring Components | |||

| By Temperature Range | Chilled (0–4 °C) | ||

| Frozen (-18 °C) | |||

| Deep-Frozen/Ultra-low (<-40 °C) | |||

| By Transport Mode | Road – Reefer Trucks and Trailers | ||

| Sea – Reefer Containers | |||

| Rail – Refrigerated Railcars | |||

| Air Cargo | |||

| By Application | Fruits and Vegetables | ||

| Meat and Seafood | |||

| Dairy and Frozen Dessert | |||

| Bakery and Confectionery | |||

| Ready-to-Eat Meals | |||

| Other Applications | |||

| By Technology | RFID and Real-time Monitoring | ||

| IoT-Enabled Telematics | |||

| Automated Storage and Retrieval Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

| Cold-chain Storage |

| Cold-chain Transport |

| Monitoring Components |

| Chilled (0–4 °C) |

| Frozen (-18 °C) |

| Deep-Frozen/Ultra-low (<-40 °C) |

| Road – Reefer Trucks and Trailers |

| Sea – Reefer Containers |

| Rail – Refrigerated Railcars |

| Air Cargo |

| Fruits and Vegetables |

| Meat and Seafood |

| Dairy and Frozen Dessert |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Other Applications |

| RFID and Real-time Monitoring |

| IoT-Enabled Telematics |

| Automated Storage and Retrieval Systems |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current Food Cold Chain Market size?

The Food Cold Chain Market is projected to register a CAGR of 8.79% during the forecast period (2025-2030)

What is the current size of the Food Cold Chain market?

The market stands at USD 70.55 billion in 2025 and is projected to climb to USD 121.77 billion by 2030.

Which region is growing fastest?

Asia-Pacific is forecast to register a 16.56% CAGR through 2030, outpacing all other regions.

Which transport mode is expanding quickest?

Air cargo leads with a 14.97% CAGR, driven by premium perishables and long-haul e-commerce.

Which application segment offers the highest growth?

Ready-to-eat meals are expected to advance at a 16.54% CAGR, reflecting lifestyle shifts toward convenience.

Page last updated on: July 6, 2025