Coal Handling Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 30.40 Billion |

| Market Size (2031) | USD 36.67 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coal Handling Equipment Market Analysis by Mordor Intelligence

The Coal Handling Equipment Market is projected to reach USD 29.18 billion in 2025, USD 30.40 billion in 2026, and USD 36.67 billion by 2031, growing at a CAGR of 3.82% from 2026 to 2031. Market demand remains stable as emerging Asian economies continue to add coal-fired capacity at a faster rate than OECD countries are retiring plants. Additionally, operators globally face increasing pressure to automate aging equipment such as conveyors, crushers, and stacker-reclaimers. In the first half of 2025, China approved 74.7 GW of new coal capacity and brought 21 GW online, while India commissioned 5.1 GW against a pipeline of 92 GW, driving global greenfield orders. Simultaneously, upgrade cycles are gaining momentum. Initiatives such as India’s INR 31,367.66 crore First Mile Connectivity program, South Africa’s stacker-reclaimer refurbishments, and rail-running conveyor pilot projects are boosting aftermarket revenues and accelerating digital retrofits. Automation is increasingly integrated with mechanical scopes. For instance, Metso enhanced its control software capabilities through the acquisition of MRA Automation in February 2026, and Caterpillar’s MineStar platform continues to expand its autonomous haulage solutions. In Europe and North America, ESG-driven financing constraints are limiting new coal infrastructure development. However, these constraints are encouraging original equipment manufacturers (OEMs) to focus on lifecycle services that help operators minimize capital expenditures.

Key Report Takeaways

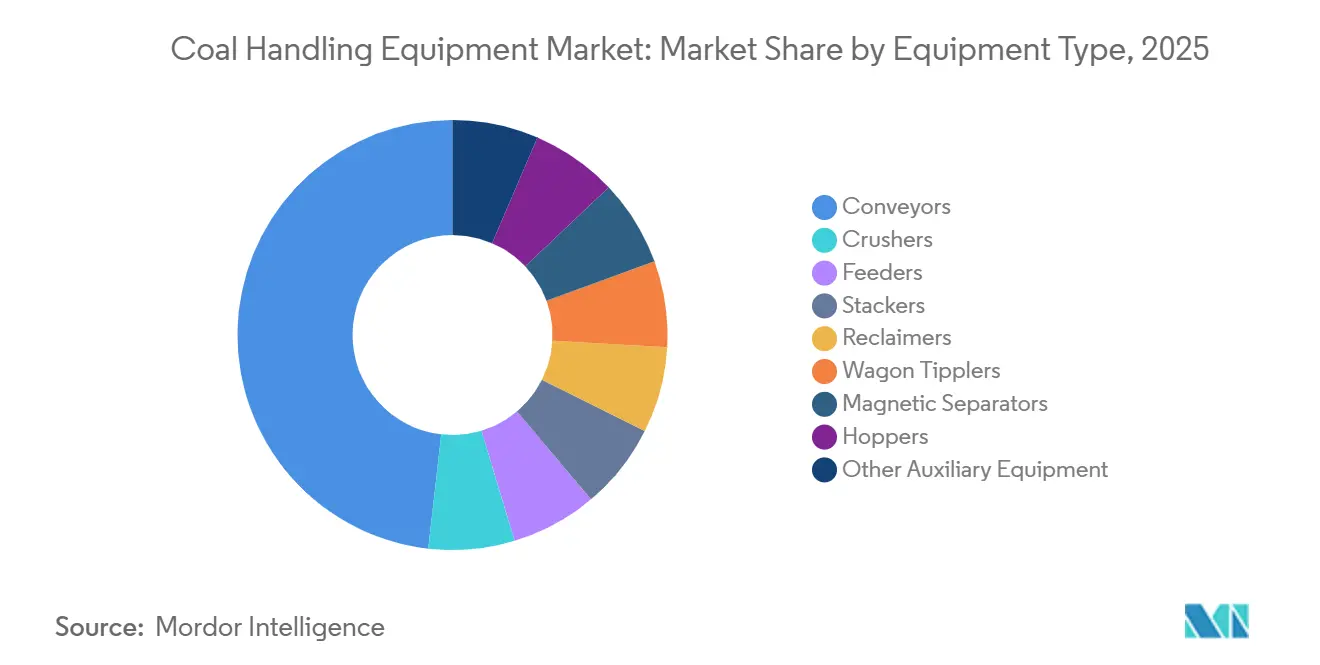

- By equipment type, conveyors accounted for 48.2% of the coal handling equipment market share in 2025 and are forecast to expand at a 4.5% CAGR through 2031.

- By operation type, material conveying also represented 48.2% of the coal handling equipment market size in 2025 and is projected to match a 4.5% CAGR to 2031.

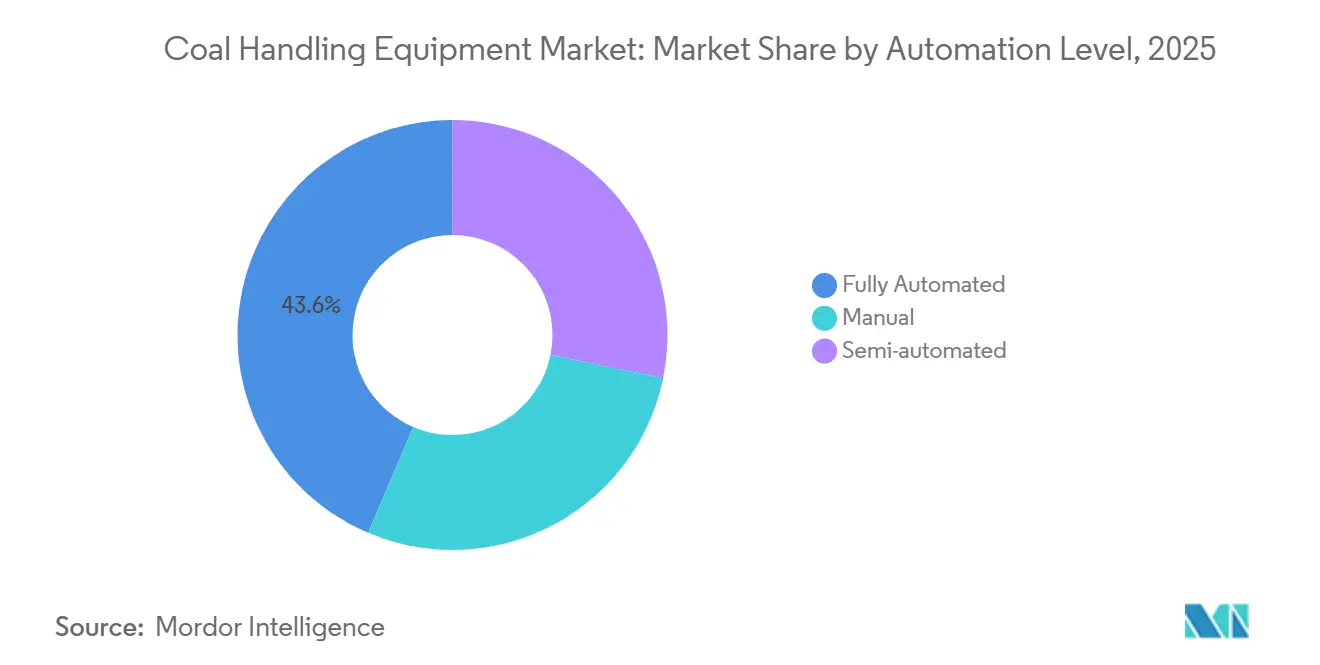

- By automation level, fully automated systems are advancing at the fastest 4.7% CAGR during 2026-2031 while holding 43.6% of 2025 installations.

- By end-user, power generation captured 37.5% of 2025 demand, yet mining operations are on course for the highest 5.0% CAGR through 2031.

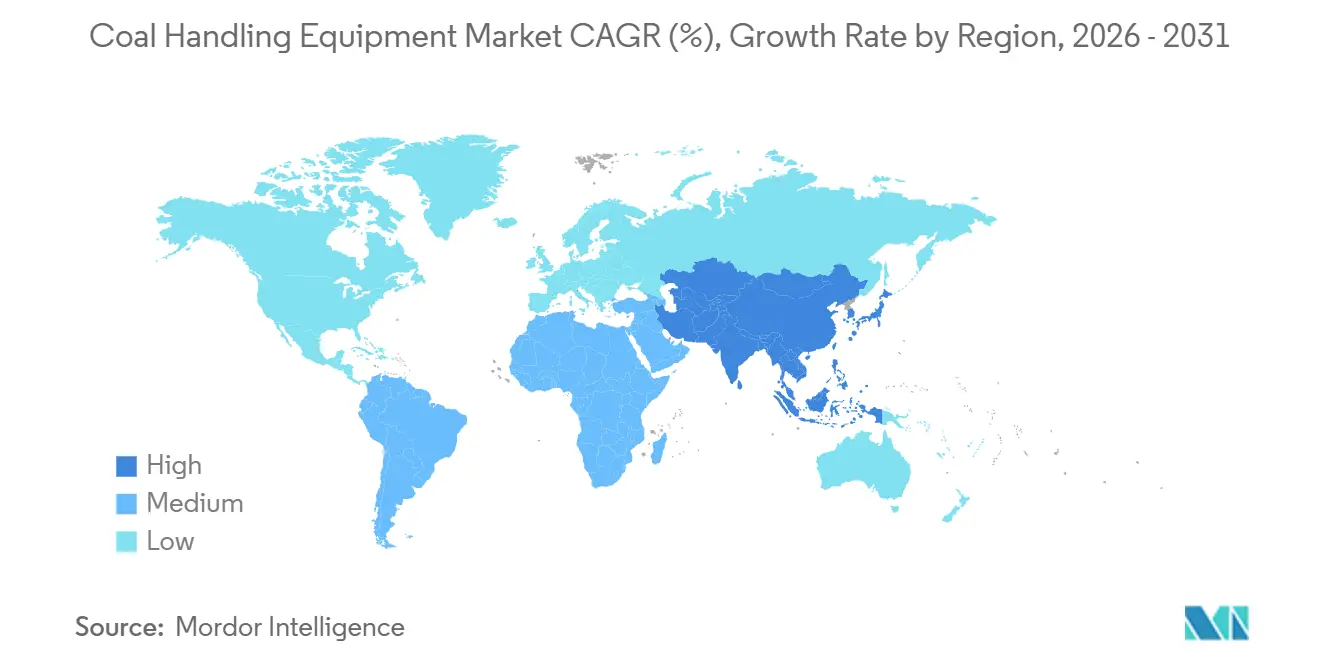

- By geography, Asia-Pacific accounted for 45.0% of 2025 revenue and is expected to rise at a 4.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coal Handling Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of coal-fired capacity in emerging Asia | +1.20% | Asia-Pacific core; spillover to Middle East | Medium term (2-4 years) |

| Aging infrastructure upgrade cycle | +0.80% | North America & Europe | Long term (≥ 4 years) |

| Surge in surface-mined output | +0.70% | Asia-Pacific, North America, Australia | Short term (≤ 2 years) |

| Adoption of automation & digital twins | +0.60% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Hybrid renewable-coal micro-grids | +0.30% | Asia-Pacific, selected emerging markets | Long term (≥ 4 years) |

| Coal-to-chemicals build-out | +0.50% | China, India, ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging infrastructure upgrade cycle across existing plants

Many conveyors, crushers, and stackers installed in the 1990s have exceeded their design life. India’s 102 First Mile Connectivity initiatives focus on replacing low-capacity belts with digitally monitored systems capable of handling over 10,000 tons per hour. (1)Press Information Bureau, “First Mile Connectivity Projects Update,” pib.gov.in Martin Engineering reported a surge in belt-cleaner retrofits in 2025 as operators aimed to reduce spillage and implement real-time belt tracking. South Africa’s Richards Bay Coal Terminal is refurbishing stacker-reclaimers to address rail bottlenecks and restore throughput. (2) Transnet, “Richards Bay Coal Terminal 2025 Performance,” transnet.net These upgrade projects provide consistent parts and service revenue, helping OEMs mitigate the impact of regional demand fluctuations.

Surge in surface-mined coal output requiring high-capacity conveyors

Surface mining is gaining market share from underground operations due to lower extraction costs and the use of ultra-high-capacity conveyors that eliminate the need for truck haulage. Warrior Met Coal's Blue Creek No.1 mine, commissioned in 2025 with a USD 1 billion investment, features a Sempertrans ST7500 belt and a BEUMER 9-mile overland conveyor system capable of handling 6 million short tons annually over a 40-year mine life. Peabody Energy's Centurion Mine allocated USD 12 million to a 2.5-kilometer underground conveyor, replacing diesel truck haulage to reduce fuel costs and emissions. Indonesia's PT Bukit Asam installed two 3,000-tonne-per-hour train loading stations at Tanjung Enim, supported by 13-kilometer and 17-kilometer conveyors, enabling a throughput of 20 million tonnes per year. These developments indicate that high-capacity conveyors, defined as systems handling over 5,000 tonnes per hour, are becoming the standard for new surface mines. This shift is driving demand for gearless drives, advanced belt materials, and real-time tension monitoring systems, while displacing traditional truck-and-shovel logistics.

Adoption of automation & digital twins for OPEX reduction

Xinjiang’s Shitoumei No. 1 mine operates 91 autonomous trucks, eliminating 200 operator positions while improving payload consistency. At Mt. Arthur South, Caterpillar drill rigs have achieved over 1 million autonomous meters, demonstrating the life-cycle value of integrated autonomy suites. Conveyor digital twins, which combine vibration data with thermal imaging, identify belt mis-tracking issues before they lead to significant damage, reducing unscheduled downtime by 18%. Early adopters of automation report 40% profit margins despite declining coal prices, prompting slower adopters to increase their automation investments. Vendors are generating additional revenue through software-as-a-service subscriptions that integrate with existing PLC controls, expanding their income streams beyond capital equipment sales.

Hybrid renewable-coal micro-grids needing modular handling systems

Island grids in Southeast Asia are increasingly integrating small coal boilers with solar and battery systems to mitigate duck-curve volatility. Modular handling skids, designed to fit within ISO containers, facilitate rapid deployment and relocation. Original Equipment Manufacturers (OEMs) are developing plug-and-play crushers and stacker-reclaimers tailored for 150-MW units, which differ significantly from traditional 1-GW plant configurations. While the compound annual growth rate (CAGR) increase is modest, early market entry helps establish brand presence before local EPC firms enhance their capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated coal phase-out policies | -0.90% | Europe, North America | Short term (≤ 2 years) |

| Coal-price volatility | -0.50% | Global, price-sensitive markets | Short term (≤ 2 years) |

| Rising insurance & credit restrictions | -0.40% | Western financial markets | Medium term (2-4 years) |

| Shift to biomass-coal co-firing | -0.30% | Europe, North America, parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated coal phase-out policies in Europe & North America

Europe and North America are expected to shut down 15-20 GW of capacity during 2025-2026, with the U.K. finalizing its exit and Germany closing several blocks. This will eliminate both greenfield demand and long-tail parts revenue. OEMs are redirecting their sales efforts toward Asia and expanding into biomass handling to safeguard their backlogs.

Coal-price volatility delaying equipment CAPEX

In early 2025, Australian benchmark thermal coal prices declined by 20% to USD 108.39 per ton, while hard coking coal prices fell to USD 250 per ton. This reduction in prices has compressed margins, prompting operators to postpone multi-year conveyor projects. In response, vendors have introduced lease-to-own and performance-based payment models, aligning fees with throughput levels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Conveyors Drive Infrastructure Backbone

Conveyors accounted for 48.2% of the coal handling equipment market in 2025 and are projected to grow at a 4.5% CAGR through 2031. This segment experienced growth as the market size for conveyor-integrated projects at mines and ports surpassed USD 14 billion in 2025. Innovations in ultra-long overland conveyor designs, such as Thyssenkrupp’s rail-running conveyor offering up to 80% friction savings, are reducing haulage costs and gaining traction among Asian mining companies.

Replacement initiatives are also driving demand for conveyors. India’s First Mile Connectivity upgrades include 102 projects replacing truck dumps with high-capacity conveyor belts. Additionally, BEUMER’s new Taicang plant supports regional production of long-distance systems, reducing delivery lead times for Asia-Pacific customers. Crushers, stackers, and feeders collectively hold the remaining market share. Crushers are witnessing increased demand from coal-to-chemicals plants requiring sub-6 mm feed. Stackers and reclaimers are attracting investments at export terminals, such as McDuffie, where a USD 200 million modernization project is enhancing metallurgical coal loading efficiency.

By Operation Type: Material Conveying Dominates Logistics Chains

Material conveying accounted for 48.2% of the coal handling equipment market share in 2025 and is expected to grow at a CAGR of 4.5% through 2031. Continuous belts connecting pits, preparation plants, stockyards, and ports contribute to long-term service revenues, representing nearly half of the segment's value.

Receiving and crushing remain critical but are increasingly commoditized. Indonesian rail-linked hubs are incorporating wagon tipplers and electric apron feeders, while India’s centralized receiving facilities focus on under-car discharge systems and high-capacity dumpers. Storage and reclaim upgrades at ports, ranging from Richards Bay to terminals in the Russian Far East, require new stacker-reclaimers, although budget limitations often restrict the scope of full automation.

By Automation Level: Fully Automated Systems Capture Premium

Fully automated installations accounted for 43.6% of 2025 deliveries and are projected to grow at a CAGR of 4.7%, outpacing semi-automated and manual systems. Features such as digital twins, collision avoidance, and predictive maintenance have become essential requirements in bids.

Semi-automated retrofits remain prevalent in legacy plants as they retain manual oversight while incorporating interlocks. Manual systems persist in smaller mines with low labor costs; however, funding agencies increasingly prioritize partial automation to meet safety regulations. As a result, vendors offer tiered packages, enabling brownfield sites to transition gradually to full automation without incurring high upfront costs.

By End-user: Power Generation Dominates, Mining Accelerates

In 2025, power generation accounted for the largest share at 37.5%, driven by China’s 21 GW and India’s 5.1 GW of commissioned capacity. However, mining companies are projected to experience the highest compound annual growth rate (CAGR) of 5.0% through 2031, as they expand surface extraction capacity.

Projects such as Warrior Met’s Blue Creek No.1 and PT Bukit Asam’s 100 million-ton program highlight a transition toward pit-to-plant conveyor systems capable of moving over 10,000 tons per hour. While ports, steel, cement, and emerging coal-to-chemicals industries contribute to niche growth, their volumes remain comparatively lower. Consequently, original equipment manufacturer (OEM) order books currently emphasize mine infrastructure, whereas utility contracts focus on refurbishment and long-term service agreements.

Geography Analysis

Asia-Pacific accounted for 45.0% of the revenue in 2025 and is expected to grow at a 4.8% CAGR through 2031, driven by increasing power and industrial coal demand in China, India, and Indonesia. The coal handling equipment market size associated with First Mile Connectivity schemes is projected to exceed USD 3.7 billion by 2030. Additionally, Sinopec’s Inner Mongolian olefins project is intensifying China's demand for fine-coal preparation lines. Original Equipment Manufacturers (OEMs) with facilities in Taicang, Pune, or Jakarta benefit from reduced freight and duty costs, providing a competitive advantage in state-run tenders.

North America recorded a 4% increase in coal output in 2025, reaching 527.5 million short tons, primarily due to heightened winter demand caused by extreme weather. However, investments remain focused on maintenance rather than expansion. Notable projects include the modernization of Alabama’s McDuffie coal terminal and Norfolk Southern’s USD 200 million 3B Corridor, which emphasizes selective capital expenditure where export economics are favorable.

Europe continues to experience a decline in coal demand due to the rapid retirements of coal-fired plants. However, opportunities exist in biomass-ready retrofits, such as Poland’s pellet blend upgrades, which cater to evolving energy needs.

South Africa, Russia, and select South American ports represent additional opportunity areas. South Africa’s Richards Bay exported 57.66 million tons in 2025 and is investing in stacker-reclaimers to enhance capacity. In Russia, expansions at Vanino and Vostochny ports, which collectively add over 20 million tons of annual throughput, necessitate new shiploaders and yard equipment. The Middle East remains a negligible market for coal handling equipment due to its reliance on natural gas for power generation.

Competitive Landscape

The coal handling equipment market exhibits moderate fragmentation. Prominent global OEMs such as Metso, Sandvik, FLSmidth, and Thyssenkrupp compete with regional specialists like Elecon Engineering and McNally Bharat. The competitive focus has shifted towards bundled offerings that integrate mechanical systems with software and outcome-based service models. For instance, Metso's acquisition of MRA Automation has enhanced its capabilities in supervisory control and predictive analytics, increasing its active Life Cycle Services contracts to over 600 by 2025.

BEUMER's 23,000 m² facility in Taicang, completed in 2025, has significantly reduced delivery lead times for overland conveyors intended for Chinese mines and Southeast Asian ports. Meanwhile, Thyssenkrupp's rail-running conveyor, which can reduce electrical capital expenditure (CAPEX) by up to 50%, is undergoing first-metal trials with a Tier 1 copper miner. This innovation has the potential to be applied to long-distance coal transportation corridors.

Smaller players are establishing niches through digital service offerings. For example, Caterpillar now includes the Helios analytics platform in its equipment leases, while Sandvik provides performance-linked financing, where payments are tied to conveyor uptime. Additionally, supply chain localization and integrated automation capabilities are becoming key differentiators in tenders, surpassing the importance of base equipment costs.

Coal Handling Equipment Industry Leaders

FLSmidth & Co. A/S

Metso Corporation

Sandvik AB

Caterpillar Inc.

Thyssenkrupp AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BHEL has approved an equity investment of INR 3,064.46 crore (USD 367 million) in Bharat Coal Gasification and Chemicals Limited (BCGCL), a joint venture with Coal India, where BHEL holds a 49% stake and Coal India holds 51%. This investment is intended to support the development of coal-to-chemicals projects, including the establishment of a 2,000 tonnes per day ammonium nitrate plant in Jharsuguda, Odisha. The investment will be made in cash at face value over a four-year period, aligning with BHEL's strategic focus on upstream integration in coal gasification and preparation systems.

- January 2025: CONSOL Energy and Arch Resources have merged to form Core Natural Resources, establishing a unified entity with increased capacity in Appalachian coal production.

- January 2025: Caterpillar celebrated its centennial at CES 2025, showcasing innovations in autonomy and electrification, including the Cat 972 Wheel Loader hybrid retrofit and 24-hour electrified jobsite simulation.

Global Coal Handling Equipment Market Report Scope

Coal handling equipment refers to the integrated machinery and systems designed to transport, crush, screen, store, and feed coal within power plants, mines, and ports. These systems, which include conveyors, crushers, and stacker-reclaimers, ensure efficient, safe, and continuous movement of coal from delivery to final consumption.

The coal handling equipment market report is segmented by equipment type, operation type, automation level, end-user, and geography. By equipment type, the market is segmented into conveyors, crushers, feeders, stackers, reclaimers, wagon tipplers, magnetic separators, hoppers, and other auxiliary equipment. By operation type, the market is segmented by material receiving, material crushing, material conveying, material storage & reclaim. By automation level, the market is segmented into manual, semi-automated, and fully automated. By end-user, the market is segmented into power generation, steel and cement industries, mining operations, ports and terminals, and others. The report also covers the market size and forecasts for the coal handling equipment market across 18 countries major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Conveyors |

| Crushers |

| Feeders |

| Stackers |

| Reclaimers |

| Wagon Tipplers |

| Magnetic Separators |

| Hoppers |

| Other Auxiliary Equipment |

| Material Receiving |

| Material Crushing |

| Material Conveying |

| Material Storage & Reclaim |

| Manual |

| Semi-automated |

| Fully Automated |

| Power Generation (Thermal Power Plants) |

| Steel and Cement Industries |

| Mining Operations |

| Ports and Terminals |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Equipment Type | Conveyors | |

| Crushers | ||

| Feeders | ||

| Stackers | ||

| Reclaimers | ||

| Wagon Tipplers | ||

| Magnetic Separators | ||

| Hoppers | ||

| Other Auxiliary Equipment | ||

| By Operation Type | Material Receiving | |

| Material Crushing | ||

| Material Conveying | ||

| Material Storage & Reclaim | ||

| By Automation Level | Manual | |

| Semi-automated | ||

| Fully Automated | ||

| By End-user | Power Generation (Thermal Power Plants) | |

| Steel and Cement Industries | ||

| Mining Operations | ||

| Ports and Terminals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the Coal handling equipment market?

The market is valued at USD 30.40 billion in 2026, on track to reach USD 36.67 billion by 2031.

Which equipment category leads spending?

Conveyors lead with 48.2% revenue share in 2025 and are expected to grow at a 4.5% CAGR through 2031.

Where is demand growing fastest?

Asia-Pacific, holding 45.0% of 2025 revenue, is projected to rise at a 4.8% CAGR to 2031, supported by China, India, and Indonesia.

How is automation changing purchasing criteria?

Fully automated yards made up 43.6% of 2025 installations and are advancing at a 4.7% CAGR as operators seek lower OPEX and better safety.

What risks could slow market growth?

Accelerated phase-outs in Europe and North America, volatile coal prices, tighter ESG financing, and rising biomass co-firing all weigh on new equipment orders.

Which companies are most active in acquisitions?

Metso acquired MRA Automation to strengthen digital bulk-handling control, and Caterpillar continues to invest in autonomous haulage platforms.

Page last updated on: