Clean Coal Technology Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

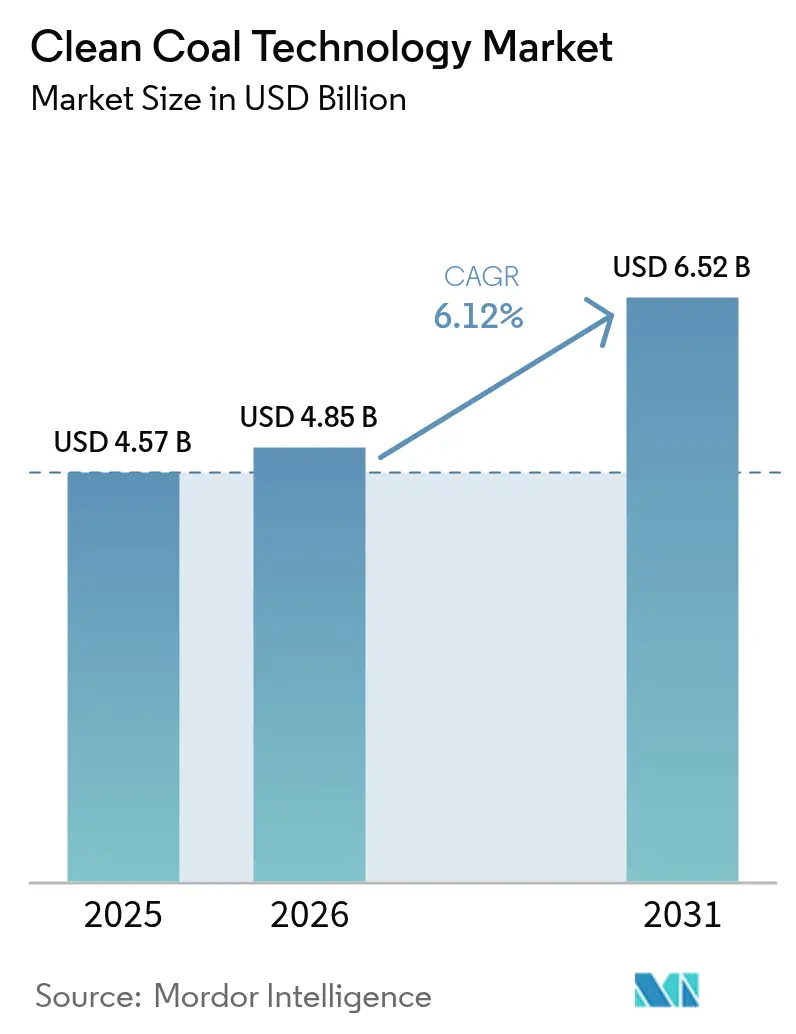

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clean Coal Technology Market Analysis by Mordor Intelligence

Clean Coal Technology market size in 2026 is estimated at USD 4.85 billion, growing from 2025 value of USD 4.57 billion with 2031 projections showing USD 6.52 billion, growing at 6.12% CAGR over 2026-2031.

Regulatory pressure on carbon intensity, rapid innovation in carbon capture, utilization, and storage (CCUS), and rising demand for reliable baseload power together propel investment flows. Supercritical and ultra-supercritical systems are displacing legacy subcritical units as operators target thermal efficiencies beyond 45%, while CCUS retrofits help avoid premature plant retirements and stranded-asset risks. Public-sector incentives, notably the United States 45Q tax credit and comparable schemes in Canada and the European Union, are reshaping project economics in favor of large-scale carbon capture retrofits. Meanwhile, plant digitalization—ranging from artificial-intelligence-based control software to predictive maintenance—strengthens operating margins and shortens payback periods. These factors collectively reinforce the medium-term growth outlook for the Clean Coal Technology market(1)International Energy Agency, “IEA High Efficiency, Low Emissions Coal Technology Roadmap – Workshop Summary,” iea.org .

Key Report Takeaways

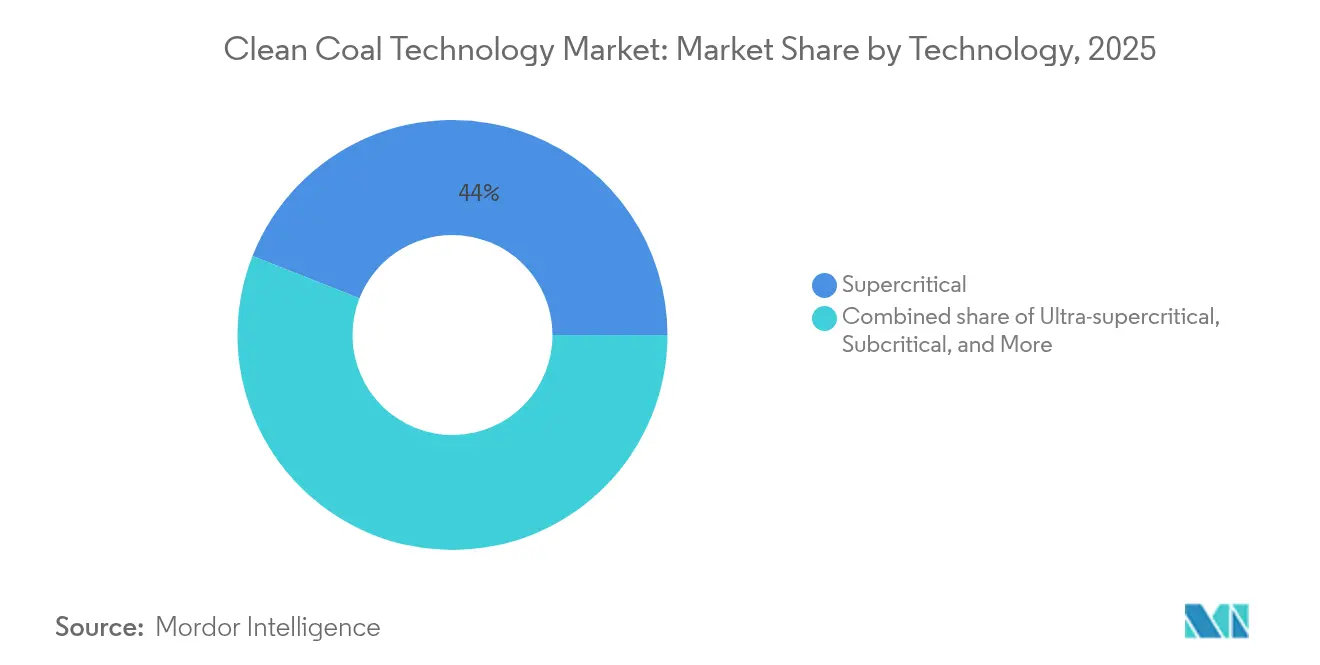

- By technology, supercritical systems captured 44.02% of the Clean Coal Technology market share in 2025, whereas ultra-supercritical technology is poised to log the fastest growth at 17.26% CAGR through 2031.

- By component, equipment retained a 70.65% share of the Clean Coal Technology market size in 2025, while services are projected to expand at a 9.35% CAGR to 2031.

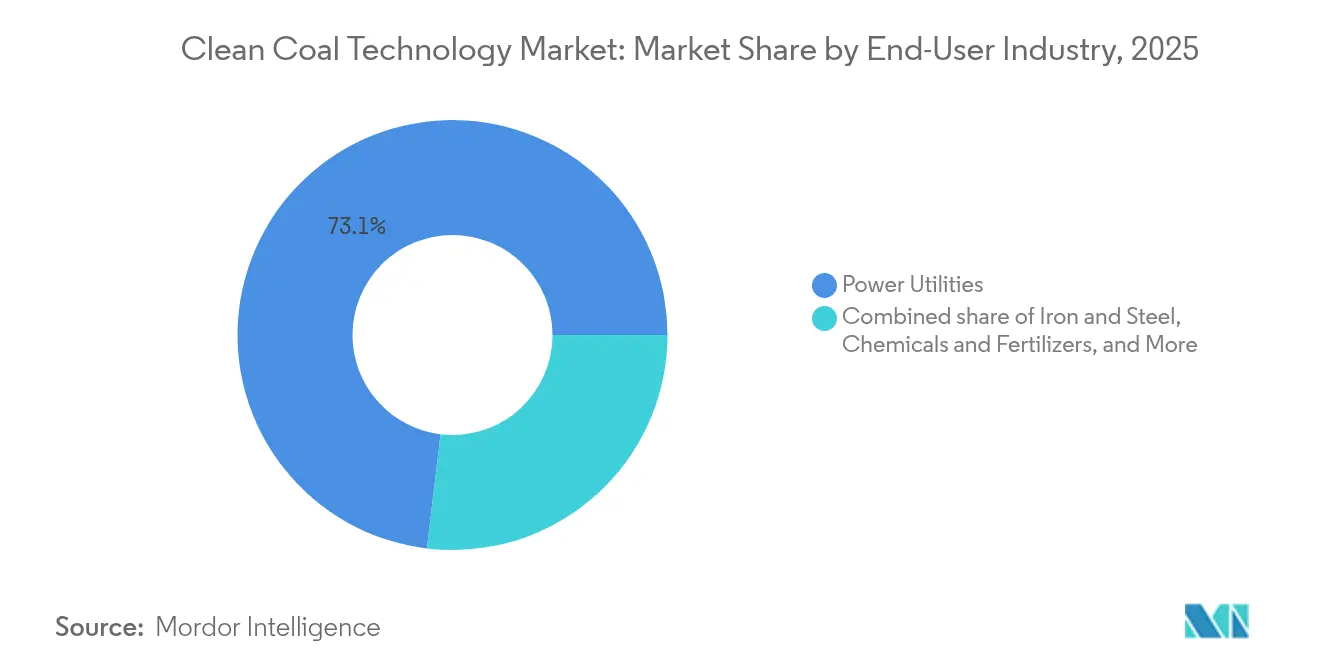

- By end-user, power utilities accounted for a 73.10% share of the Clean Coal Technology market size in 2025; iron and steel applications are expected to represent the fastest uptake at a 9.84% CAGR toward 2031.

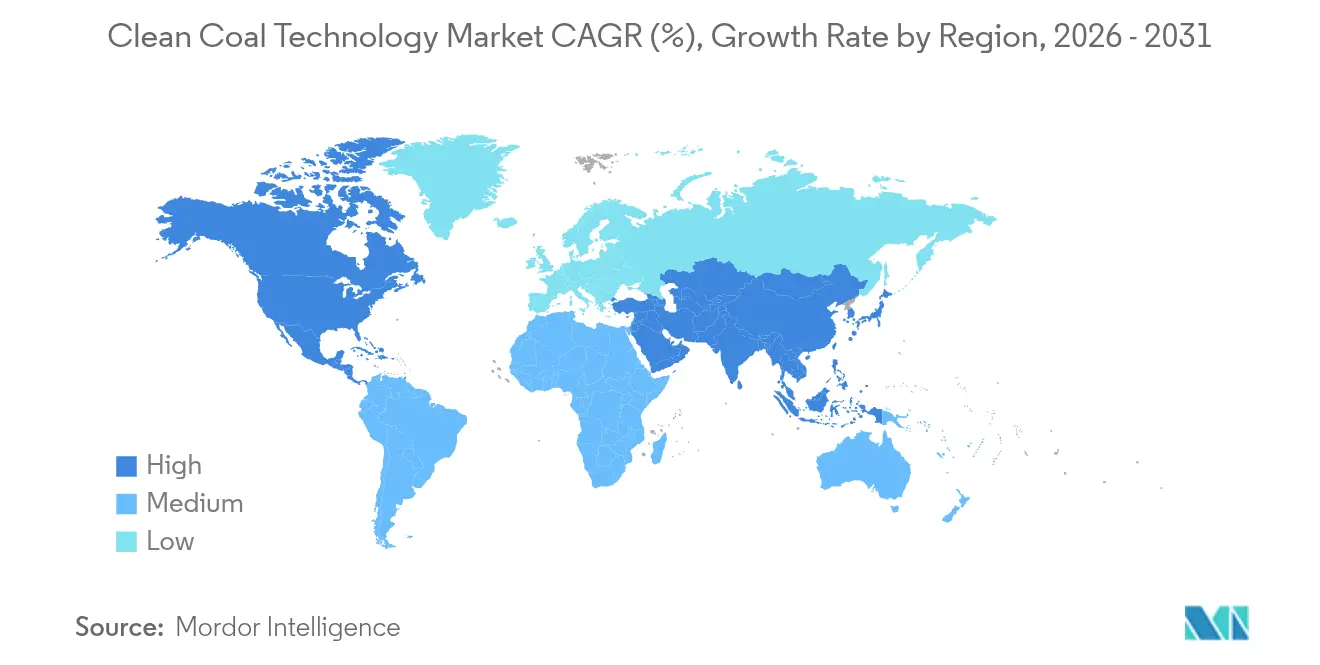

- By geography, the Asia-Pacific region led with a 38.85% revenue share in 2025, whereas North America is forecast to post the fastest regional CAGR of 8.12% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clean Coal Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter emission norms accelerating adoption of HELE plants | 1.80% | Global, strongest in EU & North America | Medium term (2-4 years) |

| Government incentives & tax credits for CCUS retrofits | 1.50% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Surging baseload demand in emerging Asia requiring coal fleet upgrades | 1.20% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Hydrogen-ready retrofits of USC boilers | 0.80% | Japan, South Korea, Germany | Medium term (2-4 years) |

| Synthetic fuel co-firing mandates | 0.60% | Japan & South Korea | Short term (≤ 2 years) |

| Advanced process-control software | 0.40% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Emission Norms Accelerating Adoption of HELE Plants

Global regulators now require existing coal units to achieve significant CO₂ reduction milestones, triggering immediate demand for supercritical and ultra-supercritical retrofits. The U.S. Environmental Protection Agency’s 2024 rule requires 90% capture by 2032 or retirement by 2039, effectively prioritizing HELE upgrades over conventional refurbishments(2)U.S. Environmental Protection Agency, “Clean Air Act Section 111 Regulation of Greenhouse Gas Emissions from Electric Generating Units,” epa.gov . China’s September 2024 directive emphasizes advanced combustion and management practices to curb pollutants while maintaining grid reliability(3)National Development and Reform Commission, “Opinions on Strengthening Clean and Efficient Utilization of Coal,” ndrc.gov.cn . Europe treats HELE as a transitional asset class that bridges near-term security needs and 2050 net-zero targets. Utilities thus favor efficiency-centric investments where renewables alone cannot yet guarantee 24/7 service. The result is a growing project pipeline for high-efficiency boilers, turbines, and associated CCUS integration across mature and developing grids.

Government Incentives & Tax Credits for CCUS Retrofits

Public-sector funding is reshaping the commercial calculus for carbon capture and storage. The United States offers up to USD 85 per ton via 45Q, while the Department of Energy earmarked USD 1.3 billion for plant-scale capture projects in 2024. Canada committed CAD 21.5 million (USD 15.8 million) in 2025 to develop transport and storage hubs in Alberta. The European Union’s Innovation Fund allocated EUR 220 million to cement-sector capture initiatives, indicating technology spillovers beyond power generation(4)Air Liquide, “Air Liquide and Cementir Holding Secure EU Innovation Fund Support,” airliquide.com . With improved internal rates of return, private investors are allocating increasing capital to retrofit programs, thereby accelerating commercialization timelines. These incentives jointly lower financial risk and encourage developers to scale pilot plants into full commercial operations.

Surging Baseload Demand in Emerging Asia Requiring Coal Fleet Upgrades

Industrialization and urban growth across India, China, and Southeast Asia drive electricity demand that intermittent renewables alone cannot meet. BloombergNEF projects significant capital deployment for low-carbon coal technologies to maintain energy security while lowering emissions. India has completed a domestic Advanced Ultra-Supercritical design capable of achieving 46% efficiency, targeting an 800 MW demonstration unit that exemplifies the regional momentum for modernization. China’s clean-coal directive frames efficiency upgrades as an essential transition bridge while renewables scale. Multilateral lenders identify a USD 1.1 trillion yearly investment gap, underscoring opportunities for HELE and CCUS installations that minimize carbon intensity without undermining economic expansion. Such dynamics underpin long-run demand for the Clean Coal Technology market.

Hydrogen-Ready Retrofits of USC Boilers

Plant owners invest in hardware compatible with future hydrogen or ammonia firing, extending asset life in anticipation of zero-carbon fuels. GE Vernova supplied hydrogen-ready H-Class turbines for China’s Huizhou combined heat and power plant, demonstrating 10% H₂ co-firing without efficiency loss. IHI and GE Vernova established full-scale combustion test facilities in 2025, aiming for 100% ammonia firing by 2030. Mitsubishi Power signed multiple memoranda for ammonia co-firing across Asia and Latin America, reflecting global interest in hydrogen-linked decarbonization pathways. The U.S. Department of Energy, through its harsh-environment materials program, supports research and development to ensure metallurgical resilience under hydrogen combustion. These developments render hydrogen-ready retrofits a compelling hedge against evolving fuel policies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost declines of solar-plus-storage alternatives | -1.40% | Global, strongest in high-irradiance zones | Medium term (2-4 years) |

| Global shortage of nickel-based alloys for AUSC plants | -0.70% | Global, supply concentrated | Long term (≥ 4 years) |

| Water-stress limits in key coal basins | -0.50% | Australia, Western US, China & India | Long term (≥ 4 years) |

| ESG-driven financing constraints for new coal projects | -1.10% | Global, pronounced in EU & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Declines of Solar-Plus-Storage Alternatives

Falling costs in solar photovoltaics and battery storage squeeze the value proposition of certain coal upgrades. Lazard’s 2024 LCOE study shows that renewables are widening their cost advantage, although baseload needs keep coal competitive in grid stability roles(5)Lazard, “LCOE+ 2024,” lazard.com . Higher interest rates have slowed some renewable energy buildouts; however, financing costs in developing markets remain a pivotal determinant of technology choice, as evidenced by peer-reviewed research in Nature Energy. Water requirements also factor in: CCUS integration can raise plant water consumption, a disadvantage in arid regions. Nonetheless, coal facilities continue to deliver dispatchable power and high-temperature process heat, maintaining their relevance despite the momentum of renewable energy.

ESG-Driven Financing Constraints for New Coal Projects

Over 200 financial institutions have adopted coal exclusion policies, curtailing debt and equity channels for greenfield coal assets(6)Institute for Energy Economics and Financial Analysis, “200 and Counting – Global Financial Institutions Committed to Coal Divestment,” ieefa.org . Yet carve-outs persist for projects with carbon capture, as signaled by U.S. banking policies that allow lending if CCUS is integral. World Resources Institute notes that credible bank transition frameworks can still finance retrofits that demonstrably lower emissions. South Africa’s central bank echoes the systemic risk of unmanaged coal exposure, magnifying pressure on borrowers to adopt cleaner technologies. Capital scarcity, therefore, steers spending toward retrofit projects within the Clean Coal Technology market that meet ESG thresholds while delivering dispatchable power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Efficiency and Capture Dominate Upgrades

Ultra-supercritical systems registered the quickest uptake at an 17.26% CAGR through 2031, benefiting from efficiencies that surpass 45% and cut fuel consumption per kilowatt-hour. Supercritical platforms maintained their leadership position with a 44.02% share of the Clean Coal Technology market in 2025, supported by proven supply chains and lower integration risk. Circulating fluidized bed units remain popular in markets handling variable coal grades, offering intrinsic sulfur capture that eases environmental compliance. The Clean Coal Technology market size for IGCC and oxy-fuel configurations is poised for gradual acceleration as carbon capture mandates ramp up, with GE Vernova’s Edwardsport IGCC plant highlighting operational viability and steady emissions performance. Post-combustion retrofit packages, especially modular solid-sorbent and amine systems, offer faster deployment for plants constrained by boiler refurbish windows.

Subcritical technology, constrained by efficiencies of around 35%, continues to cede ground; yet, units under 300 MW still find acceptance in emerging areas that require low-complexity builds. The technology mix is also shaped by fuel transport logistics and local emission norms, prompting many operators to adopt circulating fluidized bed combustion for flexible fuel portfolios. Oxy-fuel and chemical looping pilots underscore future-readiness but await broader cost improvements. Overall, innovation in high-temperature materials and digital-twin predictive models continues to enhance the Clean Coal Technology market, enabling life-extension pathways and incremental emission reductions without compromising grid reliability.

By Component: Lifecycle Services Gain Momentum

Equipment captured a 70.65% share of the Clean Coal Technology market in 2025, reflecting the large capital needs for boilers, turbines, flue-gas desulfurization systems, and carbon capture hardware. Artificial-intelligence-enhanced control systems are now standard with most hardware sales, reducing unplanned downtime and optimizing combustion profiles. The services segment, forecasted to grow at a 9.35% CAGR, mirrors the industry’s gradual shift from one-time procurement toward ongoing value capture through engineering, procurement, construction, and long-term operations and maintenance (O&M) contracts.

EPC contractors package retrofits with performance guarantees, relieving operators of integration risk and unlocking finance through energy-as-a-service models. Digital twins and remote monitoring cut maintenance lead times and extend asset life, anchoring sticky service revenues for OEMs. In parallel, plant owners seek end-to-end partners for CCUS additions, boiler hydrogen readiness, and process control upgrades, reinforcing demand momentum in the Clean Coal Technology market. Equipment vendors that bundle analytics and field services thus position themselves for recurring cash-flow streams.

By End-User Industry: Utilities Still Rule but Industry Closes In

Power utilities held a 73.10% market share in the Clean Coal Technology market in 2025, as baseload obligations remain vital for system resilience. Dispatch reliability elevates coal’s role during renewable curtailments or extreme weather events. Industrial sectors, particularly iron and steel, show a 9.84% CAGR on the strength of combined electricity and high-temperature heat needs, plus emerging hydrogen-based steel pilot projects that still demand backup coal-based steam.

Cement producers accelerate post-combustion capture pilots, spearheaded by Denmark’s ACCSION project, which targets 95% capture rates. Chemical and fertilizer makers integrate syngas-derived hydrogen with CO₂ sequestration, exemplified by CF Industries’ Yazoo City initiative, which plans to capture 500,000 tons of CO₂ yearly. District-heating coal cogeneration plants across Scandinavia and Eastern Europe explore carbon capture and biomass co-firing to comply with tightening emission ceilings while meeting urban heat demand. Such diversification cushions overall market revenue streams and broadens addressable opportunities for technology providers.

Geography Analysis

The Asia-Pacific region commanded 38.85% of 2025 revenue, thanks to extensive modernization programs in China and India that support rapid industrial growth while aligning with updated efficiency mandates. National policies encourage retrofit over retirement, so operators pursue supercritical and ultra-supercritical conversions alongside first-wave CCUS pilots. Government facilitation in permitting and grid tariff adjustments further accelerates the adoption of advanced equipment within the Clean Coal Technology market.

North America ranks as the fastest-growing region, with an 8.12% projected CAGR through 2031, driven by the United States’ generous 45Q credit, USD 1.3 billion in federal funding, and Canadian provincial incentives for capture and storage infrastructure. Demonstration projects such as Louisiana’s USD 4.5 billion clean-energy complex illustrate the scale of private capital willing to co-invest under supportive policy frameworks. These measures reduce risk premiums and catalyze a robust EPC and services ecosystem.

Europe presents a mixed outlook: outright coal phase-outs proceed in some Western markets, yet selective CCUS retrofits emerge in nations balancing security-of-supply concerns. The EU Innovation Fund’s EUR 220 million disbursement to multiple projects underscores its commitment to capturing technology across cement, waste-to-energy, and legacy coal assets. South American, Middle Eastern, and African markets are adopting a more cautious stance due to capital scarcity and evolving policy environments, although industrial users in Brazil and South Africa are evaluating CCUS for steel and chemicals applications amid tightening carbon-border measures. Overall, regional divergences create a mosaic of opportunity sets that vendors must address via flexible offerings.

Regulatory Landscape

In the United States, the U.S. Environmental Protection Agency finalized carbon pollution standards for fossil fuel-fired power plants in April 2024. The rule effectively required deep CO2 abatement, with pathways aligned with 90% capture for certain coal units. The EPA also published a proposal on June 11, 2025 to repeal power-sector greenhouse gas standards, with the Federal Register release on June 17, 2025 adding material uncertainty for federal carbon-specific compliance drivers.

Competitive Landscape

The Clean Coal Technology market shows moderate fragmentation, with the top five players accounting for an estimated 55-60% combined revenue share in 2024. General Electric, Siemens Energy, and Mitsubishi Heavy Industries anchor this group through comprehensive product portfolios that span boilers, steam turbines, gas turbines, flue-gas cleanup, and CCUS technologies. GE Vernova’s alliance with Svante on solid-sorbent capture and its exhaust-gas-recirculation study, backed by the U.S. Department of Energy, positions the firm to lower capture costs by more than 6%, reinforcing its cost leadership credentials. Siemens Energy leverages digital offerings, such as SPPA-T3000 control upgrades that integrate carbon capture modules, while Mitsubishi Heavy Industries capitalizes on its KM CDR Process and ammonia-co-firing pilots across the Asia-Pacific region.

Mid-tier challengers include Babcock & Wilcox, Andritz, and Sumitomo SHI FW, each focusing on niche strengths like fluidized-bed boilers or proprietary hydrogen-ready combustion systems. EPC giants—Fluor, Worley, and KBR—extract value through integrated project delivery, particularly where owners seek single-package solutions for plant retrofits. Service-heavy revenue mixes shield these firms from capital expenditure (capex) cyclicality and deepen customer relationships. New-generation disruptors, such as ION Clean Energy, NET Power, and 8 Rivers, craft specialized capture chemistries or Allam-cycle gasification pathways, attracting strategic equity from major companies like Chevron and Copenhagen Infrastructure Partners.

Competitive intensity is rising as governments tie funding access to technology readiness and commercial-scale validation. Partnerships proliferate, exemplified by GE Vernova’s collaboration with Svante and Siemens Energy’s venture investments in modular capture start-ups. Players that combine OEM expertise, digital analytics, and long-term service agreements hold a clear edge because they can offer performance guarantees spanning multiple decades. Consequently, differentiation now hinges on the total cost-of-ownership metrics rather than upfront hardware prices alone.

Clean Coal Technology Industry Leaders

General Electric Company

Siemens Energy AG

Shanghai Electric Group Co Ltd

Mitsubishi Heavy Industries Ltd

Harbin Electric Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Global CCUS capacity is around 50 million tonnes per year across nearly 50 facilities, highlighting the move toward multi-site programs and the operational need for modular capture trains, integration engineering, and long-term services. Much of the near-term whitespace clusters where capture projects can connect to transport and storage networks, which extends opportunities beyond equipment-only retrofits into integrated CCUS value chains.

In early 2026, RWE Generation UK issued an Environmental Statement for the Staythorpe Power Station Carbon Capture Project, describing a capture retrofit tied to a new pipeline connection to the Viking storage infrastructure in the North Sea. Competitive Power Ventures also published a March 2026 fact sheet for the CPV Shay Energy Center in West Virginia, where the design includes an onsite carbon-capture facility. In January 2026, Orsted advanced logistics for cross-border CO2 transport through a transportation agreement with Northern Lights to ship captured CO2 from the Kalundborg CO2 Hub to Norway storage.

Recent Industry Developments

- July 2026: Mitsubishi Heavy Industries (MHI) Group and Entergy signed an MoU to develop a roadmap targeting a 50% reduction in CCS costs through integration of gas turbine and carbon capture technologies. The collaboration outlines cost-down pathways focused on combined equipment and system integration, supporting more bankable retrofit and new-build decarbonization configurations across thermal fleets.

- April 2026: Shanghai Electric reported 2025 results and stated a strategic focus for 2026 on low-carbon upgrades for traditional coal-fired power assets. The emphasis on retrofit-oriented offerings and low-carbon systems aligns its order pipeline with coal fleet modernization, including efficiency improvements and emissions-reduction packages.

- February 2026: Harbin Electric announced progress on its 660 MW USC-CFB power project. The update signals further advancement of high-efficiency clean coal configurations and improved export positioning for Chinese OEMs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers clean-coal technologies and related equipment and services that reduce emissions from coal-based power generation and industrial coal use. The scope includes higher-efficiency boilers and systems that cut SOx, NOx, particulates, and CO2 during combustion or through capture.

Scope exclusions: We exclude coal mining, raw coal trading, and general power-plant maintenance that is not directly tied to emissions reduction or capture retrofits.

Segmentation Overview

- By Technology

- Subcritical

- Supercritical

- Ultra-supercritical

- Circulating Fluidized Bed Combustion (CFB)

- Integrated Gasification Combined Cycle (IGCC)

- Oxy-fuel Combustion

- Post-combustion Capture Retrofits

- By Component

- Equipment

- Boilers and Furnaces

- Steam Turbines and Generators

- Pollution-control Systems (FGD, SCR, etc.)

- Carbon-capture Systems

- Control and Instrumentation

- Services

- Engineering, Procurement and Construction (EPC)

- Operations and Maintenance (OandM)

- Equipment

- By End-User Industry

- Power Utilities

- Iron and Steel

- Cement

- Chemicals and Fertilizers

- District Heating

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by aligning the market definition to measurable activity in coal generation and industrial stacks, then mapping where clean coal spend shows up in public data. We reviewed sources such as the International Energy Agency for coal generation trends, the US Energy Information Administration for plant and fuel indicators, and the US EPA for emissions rules and compliance patterns. For non-US visibility, we also used sources such as Eurostat, the World Bank, and UN Comtrade to sanity-check trade flows for major equipment categories and to ground country-level energy context.

To convert these signals into model inputs, we screened annual reports, investor presentations, and project announcements from utilities and industrial operators, then cross-checked with reputed press and association pages tied to power and air-quality control. Where needed, paid subscriptions supporting company financials and intelligence, patent lookups, and shipment-level import-export records were used to fill gaps on supplier activity and equipment movement. These desk sources are not exhaustive, and many other public documents were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary inputs were built through expert interviews and structured surveys with technology providers, engineering and service firms, utilities, and large industrial users that operate coal-fired assets. We used these discussions to confirm what is being installed versus what remains only at the announcement stage, validate typical retrofit scope and timelines, and pressure-test pricing and utilization assumptions across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 53% |

| Mid tier: 48% | Functional/Unit leaders: 40% | EMEA: 29% |

| Smaller Players: 17% | Managers: 47% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where regional power and industrial coal activity was reconstructed, then translated into an addressable clean-coal spend pool using adoption and retrofit rates. In practice, we linked demand to indicators such as coal-fired capacity additions and retirements, flue gas desulfurization and denitrification compliance needs, announced carbon capture retrofit pipelines, and EPC timelines for major plant upgrades. Input assumptions were kept grounded by tracking typical equipment replacement cycles, average retrofit scope per unit, and regional policy intensity that affects project starts.

The totals were then corroborated with selective bottom-up checks, including supplier-side revenue splits for relevant equipment and services, sampled price bands for major systems, and channel checks on active versus delayed projects. When project data was incomplete, gaps were handled by applying region- and asset-age based penetration assumptions reviewed with practitioners, and then adjusting if the implied spend did not match observed procurement behavior.

For forecasting, we mainly used scenario analysis, since the outlook depends heavily on policy enforcement, financing conditions, and the timing of large retrofit awards. The scenarios were parameterized using the same core variables, then narrowed using expert consensus on likely commissioning schedules and price progression.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number does not rely on one dataset or one assumption. We compare model outputs against independent signals such as coal generation trends, emissions compliance actions, public retrofit and capture project pipelines, and trade movement for key equipment categories, then investigate unusual jumps before sign-off. When major variances show up by region or year, analysts re-check the input series, revisit conversion factors, and re-contact sources if the gap is tied to project timing or pricing.

Reports are refreshed annually, and interim updates are made when material events occur, such as large regulatory changes, major project cancellations, or sharp shifts in coal utilization. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view based on newly available public information.

Mordor Intelligence's Clean Coal Technology Market Sizing Compared With Other Published Estimates

Published market sizes for clean coal technology can look far apart because the boundary of what gets counted is not the same, and recognition timing also differs across studies. The split often comes from whether the estimate is tied to installed equipment and retrofit services, or if it also pulls in broader coal and power value chain items that are adjacent but not directly tied to emissions-reduction spend.

Evidence such as active retrofit project pipelines, regional coal-fired capacity and utilization trends, and equipment trade movement is used to keep Mordor Intelligence's estimate aligned to technology deployment and related services, rather than wider coal activity. Gaps can also appear when studies treat carbon capture as always included, use aggressive policy-driven adoption rates without field validation, apply different currency conversion timing, or do not separate equipment from long-term O&M that is not specific to clean-coal systems.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.85 B (2026) | |

| Industry Publisher A | USD 4.10 B (2024) | Uses an earlier base year and a broader technology list that can blend emissions-control spend with coal-type and application buckets, which can shift what is treated as in-scope market revenue. |

| Industry Publisher B | USD 4.40 B (2026) | Emphasizes a policy-led growth path over a longer horizon and may count a wider set of mitigation systems and enabling services around capture, which can change recognition timing and the included service envelope. |

Taken together, the spread mainly comes from scope boundaries, base year alignment, and how retrofit timing is recognized in revenue. By keeping the model tied to observable coal-asset activity and real project execution signals, our approach stays traceable to clear inputs and can be repeated when new capacity, policy, and project data are released.

Key Questions Answered in the Report

What was the global value of the Clean Coal Technology market in 2026?

The market was valued at USD 4.85 billion in 2026.

How quickly is the sector expected to expand through 2031?

Industry revenue is forecast to rise at a 6.12% CAGR, reaching USD 6.52 billion by 2031.

Which region leads demand for advanced coal upgrades?

Asia-Pacific holds the largest share thanks to extensive modernization in China and India.

Why are services gaining momentum in this space?

Complex retrofits and digital operations drive demand for engineering, procurement, construction, and maintenance support, yielding a 9.35% CAGR for services.

What policy mechanisms most influence project economics?

Incentives such as the U.S. 45Q tax credit and EU Innovation Fund grants substantially improve CCUS retrofit returns.

Which technology segment is growing fastest?

Ultra-supercritical systems lead growth at an 17.26% CAGR as operators chase efficiencies above 45%.

Page last updated on: