Cleanroom Consumables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.01 Billion |

| Market Size (2031) | USD 8.51 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

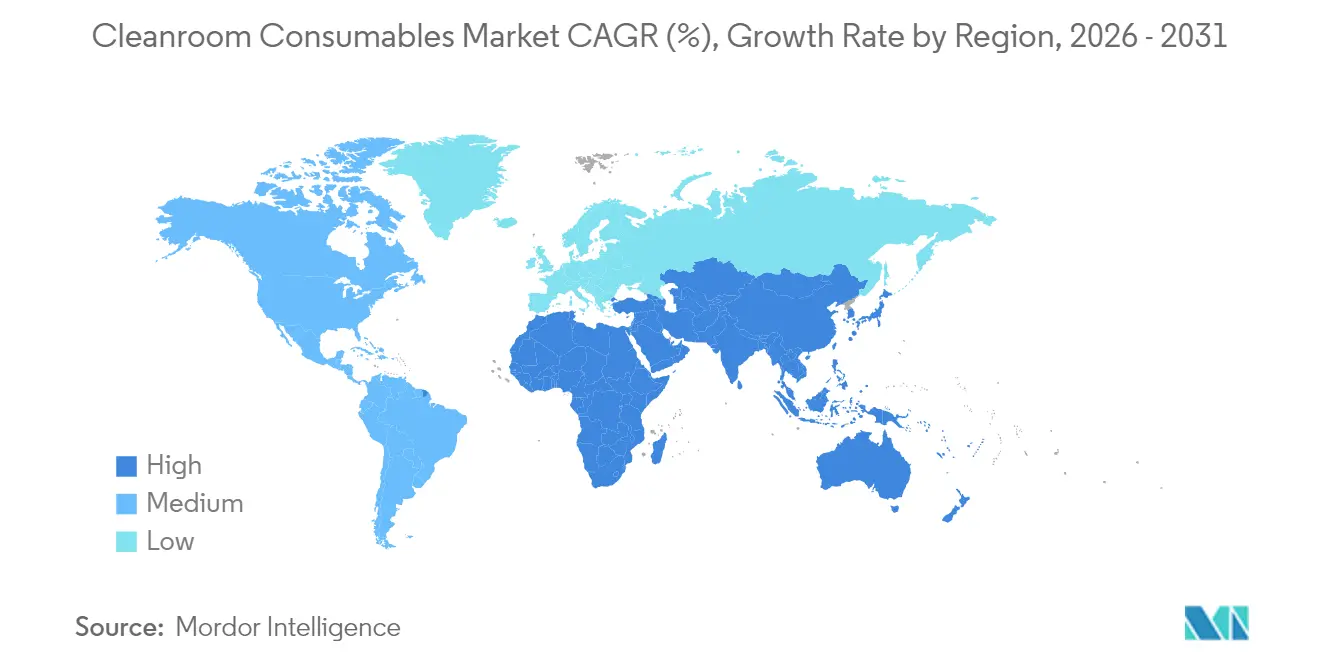

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

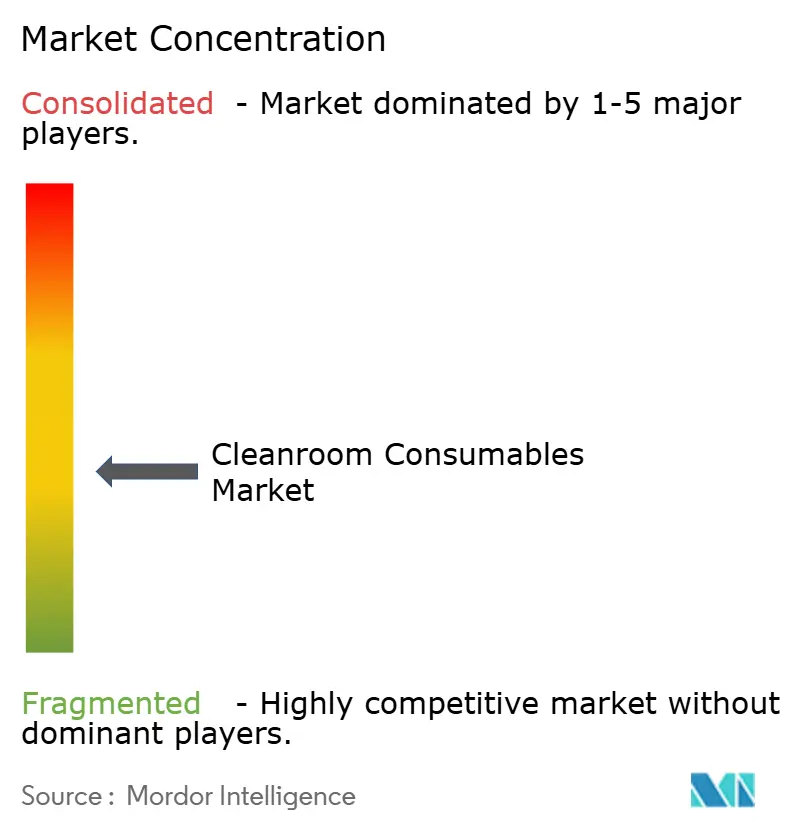

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cleanroom Consumables Market Analysis by Mordor Intelligence

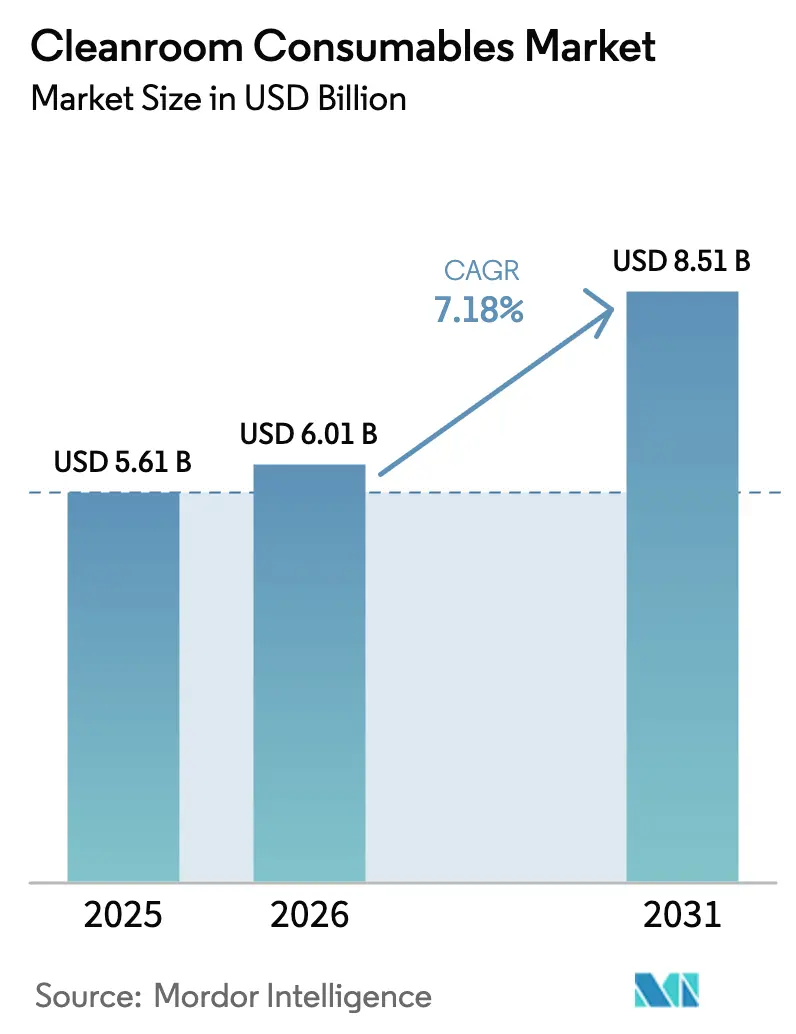

The cleanroom consumables market was valued at USD 5.61 billion in 2025 and estimated to grow from USD 6.01 billion in 2026 to reach USD 8.51 billion by 2031, at a CAGR of 7.18% during the forecast period (2026-2031). Robust investment in advanced semiconductor fabs, stricter sterile-drug rules, and electrified vehicle battery plants collectively sustain this growth trajectory. The cleanroom consumables market benefits from rising 300 mm fab equipment outlays, escalating demand for single-use apparel under the revised EU GMP Annex 1, and widening adoption of specialized wipes within cell and gene therapy suites. Energy considerations also play a role, as facilities move from energy-intensive reusable garments toward validated disposables that cut laundering loads. Competitive intensity has sharpened after high-profile acquisitions that bolster product breadth and manufacturing scale, while regional incentives accelerate domestic supply chains for critical contamination-control items.

Key Report Takeaways

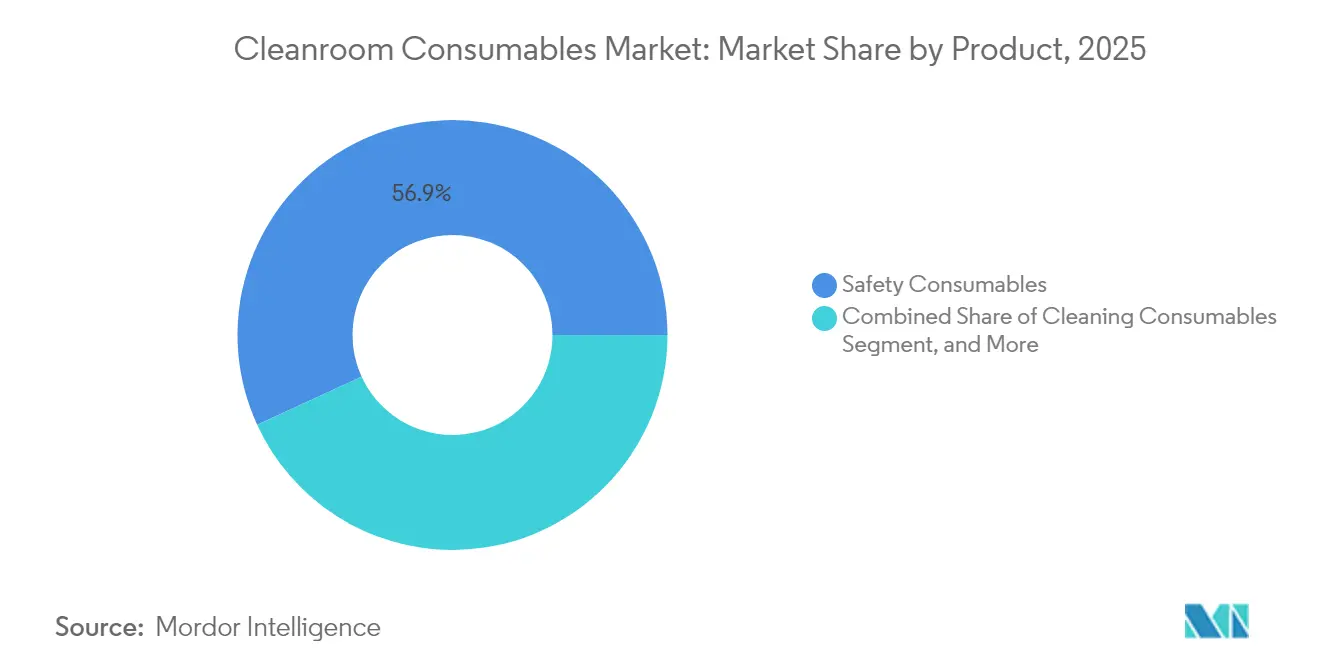

- By product category, safety consumables held 56.85% of the cleanroom consumables market share in 2025, while cleaning consumables are forecast to expand at an 8.29% CAGR through 2031.

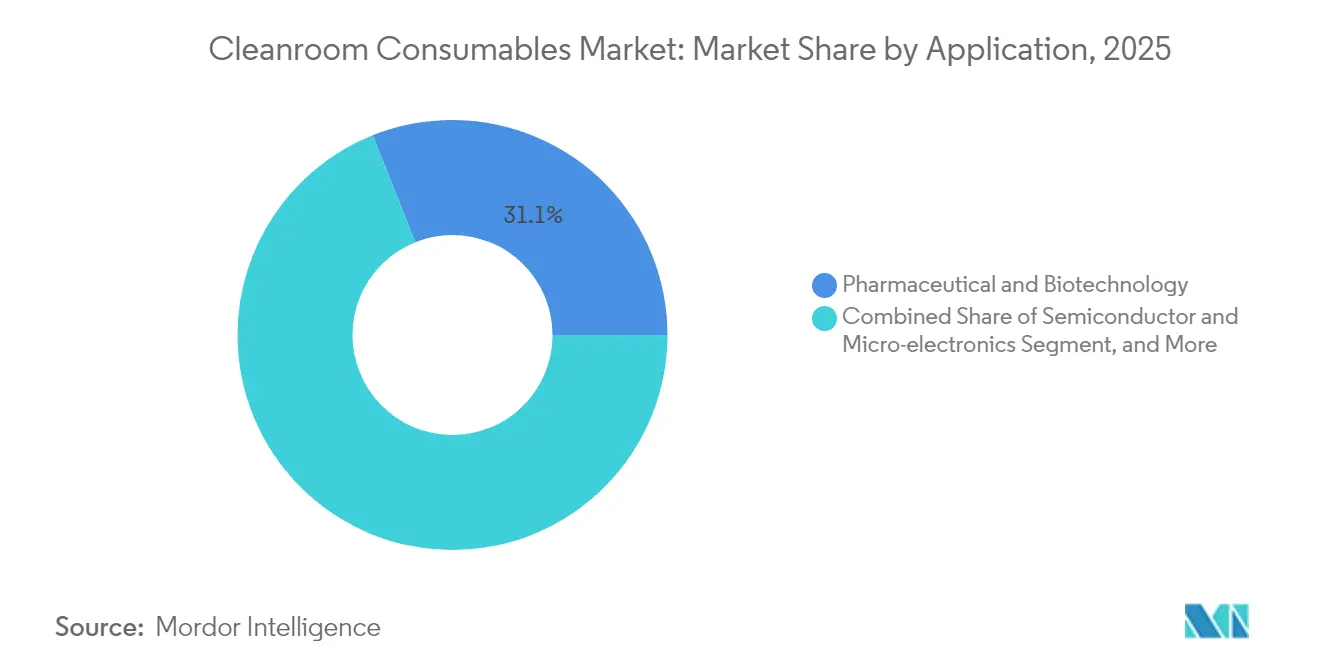

- By application, the pharmaceutical and biotechnology segment accounted for 31.05% of the cleanroom consumables market size in 2025, whereas automotive and battery manufacturing is projected to register the fastest 7.73% CAGR to 2031.

- By geography, Asia-Pacific commanded 41.35% revenue share in 2025, and South America is expected to post the highest 8.49% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cleanroom Consumables Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor capacity expansion in Asia | +1.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Stringent EU GMP Annex 1 revisions | +1.5% | Europe primary, global adoption | Short term (≤ 2 years) |

| Ramp-up of cell and gene therapy suites | +1.2% | North America, expanding to Europe | Medium term (2-4 years) |

| Fast-track COVID-19 vaccine facilities | +0.9% | Emerging markets globally | Short term (≤ 2 years) |

| Electrification of automotive industry | +1.1% | Europe primary, China secondary | Long term (≥ 4 years) |

| Rising outsourced fill-finish services | +1.0% | Global, concentrated in CDMO hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor capacity expansion in Asia driving ultra-low-particulate consumable demand

Global wafer-fab capacity is set to rise 6% in 2024 and 7% in 2025, hitting 33.7 million wafers per month, and advanced 5 nm nodes alone are on track for 13% growth in 2024. Asia-Pacific fabs require ISO Class 1-3 environments, amplifying demand for gloves, garments, and wipes engineered for sub-micron particulate removal. Chinese capacity is forecast to climb 14% by 2025, while Taiwan and South Korea boost leading-edge lines. Memory makers scaling high-bandwidth DRAM for AI workloads reinforce a steady pull for barrier-grade consumables across the cleanroom consumables market.

Stringent EU GMP Annex 1 revisions elevating sterile-grade apparel adoption

The 59-page revision, effective August 2023, mandates contamination-control strategies, zero bioburden in Grade A areas, and wider use of RABS isolators.[1]European Commission, “Guidelines for Good Manufacturing Practice for Medicinal Products for Human and Veterinary Use,” health.ec.europa.eu EU guidance prompts pharmaceutical sites worldwide to upgrade to validated disposable coveralls and aseptic wipes that meet microbial and particulate thresholds, shortening changeover times and easing documentation. Compliance timelines of one to two years have already catalyzed bulk orders for single-use gowns and pre-saturated wipers, reinforcing momentum within the cleanroom consumables market.

Ramp-up of cell and gene therapy suites requiring single-use wipes in North America

CDMO plant pipelines for viral-vector and autologous cell therapies, valued at USD 31.92 billion by 2032, rely on Grade C/D suites with rigorous segregation.[2]BioSpace, “Biopharmaceuticals Contract Manufacturing Market Size To Hit USD 31.92 Bn By 2032,” biospace.com Single-use polyester-cellulose wipes minimize cross-product carryover in multimodal facilities, while accelerated batch cycles raise consumption intensity per square foot. Such dynamics translate into structurally higher per-site spending on consumables, supporting the cleanroom consumables market expansion.

Electrification of automotive industry spurring battery cleanrooms in Europe

Gigafactory projects targeting lithium-ion pack output for electric vehicles call for ISO Class 5-8 cells and sub-1% relative humidity dry rooms. Battery plants from Spain to Scandinavia specify specialty gloves, antistatic mats, and ionic-extract-controlled wipes. With 4.5 million ft² under construction at Canada’s NextStar facility alone, European and North American vendors of contamination-control products are scaling output to meet emerging cleanroom consumables market demand.

Restraints Impact Analysis

| Restraint | (∼) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in nitrile and latex raw-material prices | −0.8% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Energy-intensive laundering costs for reusable garments | −0.6% | Developed markets primarily | Medium term (2-4 years) |

| Complex multi-jurisdictional ISO 14644 certification for SMEs | −0.4% | Global, pronounced in emerging markets | Long term (≥ 4 years) |

| Limited availability of Class 1 laundry services in Africa and Oceania | −0.3% | Africa and Oceania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in nitrile and latex raw-material prices impacting glove margins

Nitrile butadiene rubber (NBR) shortages led the U.S. government to issue supply waivers for federal glove purchases, confirming domestic supply gaps lasting until late 2025. Price spikes - Top Glove’s average selling price hit USD 70 per 1,000 pieces in 2024 - compress margins for distributors, complicating budgeting for high-volume semiconductor and pharma facilities. This uncertainty tempers order visibility within portions of the cleanroom consumables market.

Energy-intensive laundering costs curtailing reusable garment adoption

Life-cycle assessments show reusable coveralls demand 34% more process energy than HDPE disposables and 59% more than SMS polypropylene equivalents. A typical Class 1 laundry consumes high-pressure air showers, sterile packaging labor, and compliance audits, elevating the total cost of ownership. While CO₂ wash systems lower electricity and gas use by up to 60%, upfront capital outlays restrict uptake. These economics pivot many operators toward single-use garments, bolstering the cleanroom consumables market yet introducing waste-management challenges.

Segment Analysis

By Product: Safety Consumables Lead Through Regulatory Compliance

Safety consumables delivered 56.85% revenue in 2025 and will grow at 7.21% CAGR through 2031. Gloves alone represented 39.35% of the safety segment and are on track for 7.42% CAGR, reflecting strict particulate limits in advanced nodes and aseptic suites. At the segment level, safety commanded 56.85% of the cleanroom consumables market size in 2025, while adhesive mats are forecast to widen their presence within cleaning consumables, expanding at 8.29% CAGR as entry-point contamination controls harden.

Disposable nitrile glove demand continues to outstrip NBR supply, as U.S. federal orders for 55.5 million boxes highlight persistent shortages. Coveralls and frocks benefit from Annex 1’s heightened barrier provisions that discourage textile permeation. Cleaning consumables account for roughly 35.00% of the cleanroom consumables market, with pre-saturated wipes holding a 42.30% share in that subset. Their convenience and cross-contamination safeguards resonate in cell-therapy work cells that require validated residue profiles. Niche stationery, such as ion-controlled journals and ESD-safe pens, safeguards lithography steppers and wafer-inspection stations from electrostatic excursions.

Note: Segment shares of all individual segments available upon report purchase

By Application: Pharmaceutical Dominance Amid Automotive Emergence

Pharmaceutical and biotechnology producers contributed 31.05% of 2025 revenue and maintain volume leadership thanks to Annex 1’s rigorous contamination-risk mandates. The sterile-manufacturing niche is progressing at a double-digit pace, and CDMOs scale single-use filling lines that trim turnaround times. Ready-to-use containers streamline small-batch biologics, boosting cleanroom consumables market penetration across supplier frameworks.

Automotive and battery operations record the quickest 7.73% CAGR, mirroring rapid EV adoption. Dry-room glove and wipe specifications focus on very-low outgassing and lithium-compatible material chemistries, prompting suppliers to introduce novel nitrile blends with reduced ionic extractables. Semiconductor fabrication holds a stable share, grounded in 6-7% annual wafer-fab capacity expansion and a record USD 137 billion in 300 mm equipment outlays by 2027. Medical-device lines adopt ISO 14644-5 gowning modules, widening demand for disposable head-to-toe ensembles that meet dual particulate and microbial limits.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific contributed 41.35% of 2025 turnover, sustained by Chinese, Taiwanese, and Korean fabs that together represent the bulk of leading-edge capacity. China alone is slated for 14% capacity growth in 2025. Government incentives under India’s semiconductor mission funnel investment into new ISO Class 3 process halls, expanding the cleanroom consumables market footprint. Battery gigafactory roll-outs across Japan and Indonesia further thicken regional order pipelines for antistatic garments and ionic-filtered wipes.

North America ranks second, strengthening via domestic chip capacity gains funded through the CHIPS Act. Entegris’ planned Colorado Springs FOUP factory illustrates vertical integration investments that secure contamination-control supply chains. The region’s maturing cell-therapy cluster intensifies the flow of single-use gowns, gloves, and pre-saturated alcohol wipes that mitigate cross-batch vectors. A resilient regulatory environment inflates demand for third-party validated consumables that facilitate U.S. FDA and Health Canada inspections.

South America, though smaller, records the highest 8.49% CAGR to 2031 as Brazilian and Argentinian pharma plants align with WHO PIC/S guidance and EU authorizations. Cleanroom upgrades for biosimilar filling lines, alongside growing local semiconductor packaging interests, lift shipments of disposable coveralls and modular sticky mats. Europe sustains mid-single-digit growth, propelled by Annex 1 compliance and battery gigafactory programs in Germany, Spain, and Scandinavia. The Middle East and Africa exhibit gradual momentum hindered by scarce ISO Class 1 laundry capacity, pushing many operators toward imports of disposable kits and limiting local value capture in the cleanroom consumables market.

Competitive Landscape

The market shows moderate concentration. The top five vendors collectively represent an estimated 55-60% of global revenue, enabling price leverage but leaving room for niche specialists. Ansell’s USD 640 million purchase of Kimberly-Clark’s PPE unit augmented its Kimtech and KleenGuard brands, expanding portfolio coverage from ISO Class 3 critical gloves to Class 8 single-use apparel. Thermo Fisher’s USD 4.1 billion addition of Solventum’s purification arm bolsters filtration and single-use flow-path capacity, targeting biologics workflows.

Suppliers pursue material science differentiation; sub-0.5 µm-rated wipes with validated low NVR extractables answer EU and FDA scrutiny. Environmental metrics form a new battleground: several vendors now publish cradle-to-gate CO₂-equivalent footprints, appealing to sustainability scorecards. Regional manufacturing expansion continues, with glove-dipping lines under construction in Mexico to sidestep import tariffs and freight volatility. Digital traceability solutions - embedding QR-coded lot numbers on packaging - gain favor as regulators demand tighter chain-of-custody records within the cleanroom consumables market.

Cleanroom Consumables Industry Leaders

Kimberly-Clark Corporation

The Texwipe Company, LLC (Illinois Tool Works, Inc.)

Nitritex Ltd. (Ansell Limited)

Valutek Inc.

Azbil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific announced the USD 4.1 billion acquisition of Solventum’s Purification & Filtration business, aiming for USD 125 million operating-income gains by year five.

- July 2024: Ansell completed the USD 640 million takeover of Kimberly-Clark’s PPE division to deepen scientific-segment penetration.

- July 2024: DuPont finalized the purchase of Donatelle Plastics, reinforcing medical-device assembly offerings.

- June 2024: Entegris secured up to USD 75 million CHIPS Act funding for a Colorado Springs FOUP and filtration plant expected to create 600 jobs.

Global Cleanroom Consumables Market Report Scope

Clean Room Consumables are defined as clean room products that workers in the workshop use during manufacturing, such as wipes, shoe coverings, gloves, face masks, sterile coveralls, hairnets, goggles, aprons, and lab coats. The market for the study defines the revenue accrued from the sales of cleanroom consumable products across various end-users considered within the scope. The market also tracks the consumption trends of cleanroom consumable products across the world.

The Cleanroom Consumables Market is segmented by Product (Safety Consumables (Frocks, Boot Covers, Shoe Covers, Bouffants, Pants and Face Masks, and Other Safety Consumables), Cleaning Consumables (Mops, Buckets, Wringers, Squeegees and Validation Swabs, and Other Cleaning Consumables), Cleanroom Stationery (Papers, Notebooks and Adhesive Pads, Binders, and Clipboards, Labels, and Other Cleanroom Stationery)), Application (Electronics, Pharmaceutical and Biotechnology, Food and Beverage, Aerospace and Defense, University Research, Medical Device, and Automotive), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Safety Consumables | Gloves |

| Coveralls and Frocks | |

| Boot and Shoe Covers | |

| Bouffants and Hoods | |

| Face Masks and Goggles | |

| Other Safety Consumables | |

| Cleaning Consumables | Pre-Saturated Wipes |

| Dry Wipes | |

| Mops and Mop Buckets | |

| Squeegees and Wringers | |

| Validation Swabs | |

| Adhesive Mats | |

| Other Cleaning Consumables | |

| Cleanroom Stationery and Miscellaneous | Papers and Notebooks |

| Labels and Adhesive Pads | |

| Binders and Clipboards | |

| ESD-Safe Pens and Markers | |

| Other Stationery |

| Semiconductor and Micro-electronics |

| Pharmaceutical and Biotechnology Manufacturing |

| Medical Device Production |

| Food and Beverage Processing |

| Aerospace and Defense Laboratories |

| Automotive and Battery Manufacturing |

| University and Government Research Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product | Safety Consumables | Gloves |

| Coveralls and Frocks | ||

| Boot and Shoe Covers | ||

| Bouffants and Hoods | ||

| Face Masks and Goggles | ||

| Other Safety Consumables | ||

| Cleaning Consumables | Pre-Saturated Wipes | |

| Dry Wipes | ||

| Mops and Mop Buckets | ||

| Squeegees and Wringers | ||

| Validation Swabs | ||

| Adhesive Mats | ||

| Other Cleaning Consumables | ||

| Cleanroom Stationery and Miscellaneous | Papers and Notebooks | |

| Labels and Adhesive Pads | ||

| Binders and Clipboards | ||

| ESD-Safe Pens and Markers | ||

| Other Stationery | ||

| By Application | Semiconductor and Micro-electronics | |

| Pharmaceutical and Biotechnology Manufacturing | ||

| Medical Device Production | ||

| Food and Beverage Processing | ||

| Aerospace and Defense Laboratories | ||

| Automotive and Battery Manufacturing | ||

| University and Government Research Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the cleanroom consumables market?

The market is valued at USD 6.01 billion in 2026 and is forecast to reach USD 8.51 billion by 2031, growing at a 7.18% CAGR.

Which product category leads global demand?

Safety consumables, especially gloves and coveralls, accounted for 56.85% revenue in 2025 and remain the largest category.

Why is Asia-Pacific the largest regional market?

High-density semiconductor fabs and expanding battery gigafactories underpin Asia-Pacific’s 41.35% share, while government incentives accelerate local supply chains.

How have EU GMP Annex 1 revisions affected purchasing patterns?

The August 2023 revision compels pharmaceutical producers to switch to sterile-grade, single-use apparel and wipes, boosting global demand for validated disposables.

What is the biggest restraint on market growth?

Volatile prices for nitrile and latex feedstocks compress glove margins and create budgeting uncertainty, particularly in Asia-Pacific where most gloves are produced.

Which application segment is growing fastest?

Automotive and battery manufacturing cleanrooms exhibit a 7.73% CAGR as global EV demand drives new lithium-ion cell plants requiring stringent contamination control.