Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

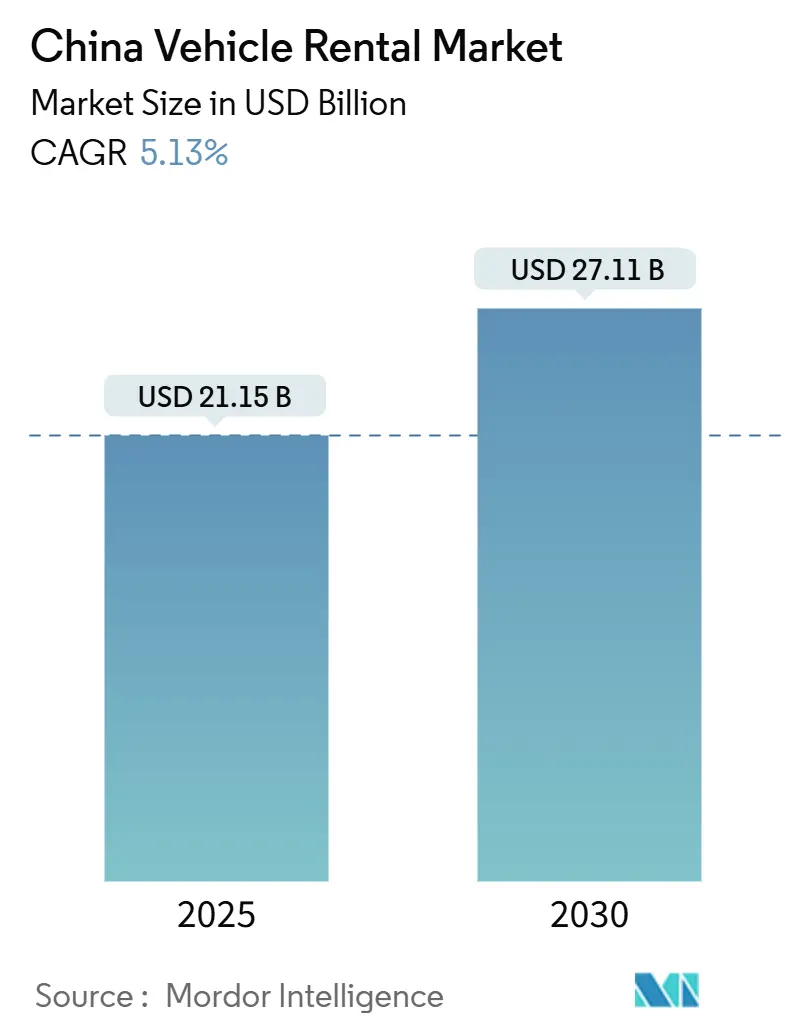

| Market Size (2025) | USD 21.15 Billion |

| Market Size (2030) | USD 27.11 Billion |

| Growth Rate (2025 - 2030) | 5.13% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Vehicle Rental Market Analysis by Mordor Intelligence

The China Vehicle Rental Market size is estimated at USD 21.15 billion in 2025, and is expected to reach USD 27.11 billion by 2030, at a CAGR of 5.13% during the forecast period (2025-2030). A rebound in domestic leisure travel, stricter license-plate quotas in tier-1 cities, and a nationwide 80% new-energy fleet mandate are aligning to keep demand elevated across consumer and corporate channels. Rising middle-class licensed-driver numbers in tier-2 and tier-3 cities, the rapid diffusion of AI-enabled booking apps, and a policy tilt toward electric models are reshaping fleet composition faster than in any prior five-year period.

Key Report Takeaways

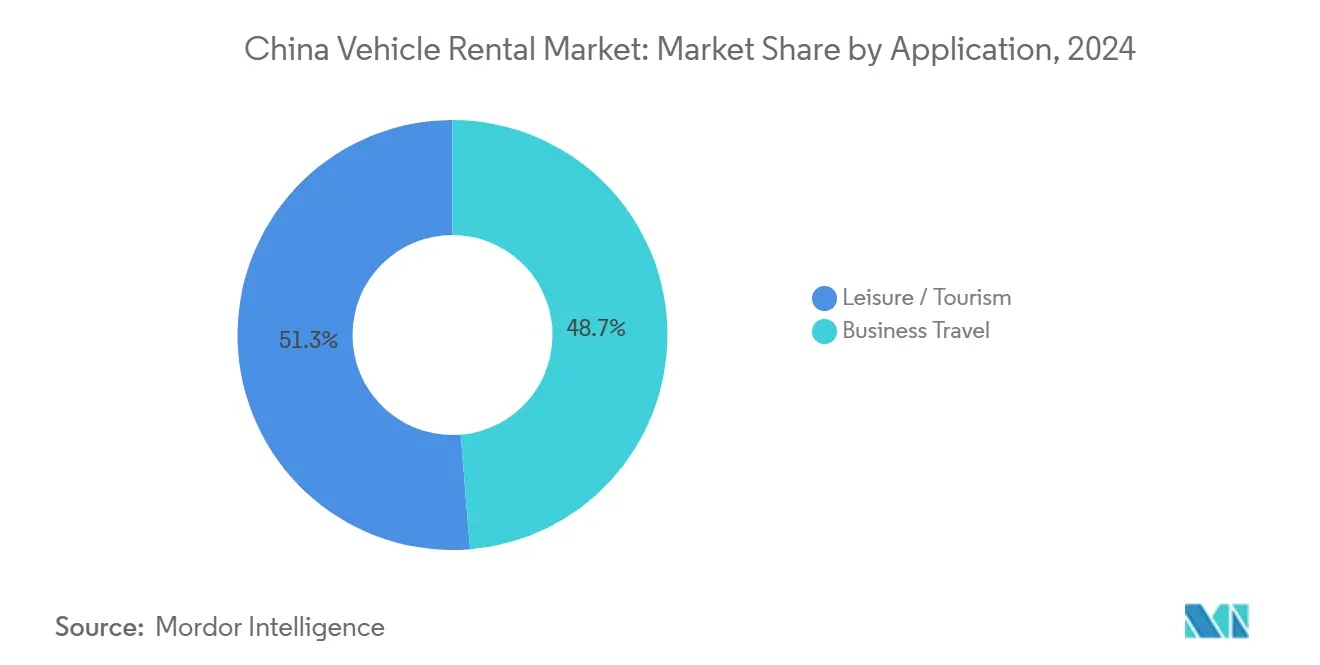

- By application, leisure and tourism held 51.27% of China vehicle rental market share in 2024; business travel is forecast to expand at a 5.22% CAGR to 2030.

- By booking type, online platforms accounted for 64.38% revenue share in 2024, while offline–to–online hybrid models register the fastest projected CAGR at 5.41% through 2030.

- By end-user type, self-driven customers commanded 71.32% of China vehicle rental market size in 2024, yet chauffeur-driven services are set to grow 5.45% annually to 2030.

- By vehicle class, economy cars led with 48.75% revenue share in 2024; the SUV/MPV segment is projected to expand at a 5.61% CAGR through 2030.

- By powertrain, internal combustion engine models accounted for 62.11% of China vehicle rental market share in 2024, while hybrid electric vehicles are forecast to grow at a 5.78% CAGR to 2030.

- By rental duration, short-term contracts of one week or less captured 58.83% revenue share in 2024; medium-term rentals of one week to one month are expected to rise at a 4.97% CAGR through 2030.

- By service channel, off-airport and downtown locations held 64.51% revenue share in 2024, whereas on-airport outlets are set to advance at a 5.33% CAGR to 2030.

- By region, East China captured 34.71% revenue share in 2024; South-Central China is advancing at a 5.76% CAGR through 2030.

China Vehicle Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Tourism Rebound | +1.2% | National, with early gains in East China, South-Central China | Short term (≤ 2 years) |

| License-Plate Quotas in Tier-1 Cities | +0.9% | East China, North China (Beijing, Shanghai focus) | Long term (≥ 4 years) |

| Growing Licensed-Driver Middle Class | +0.8% | National, concentrated in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Fleet-Electrification Mandates Open Zero-Emission | +0.7% | National, priority in tier-1 cities | Medium term (2-4 years) |

| Shift to Digital and Mobile Booking | +0.6% | National, led by East China technology adoption | Short term (≤ 2 years) |

| Corporate ESG Targets | +0.5% | National, concentrated in East China, South-Central China | Long term (≥ 4 years) |

Source: Mordor Intelligence

Domestic Tourism Rebound Fuels Leisure Rentals

Leisure bookings surged after authorities reported 295 million domestic trips during the 2024 May Day holiday, spending more than 20 billion and lifting vehicle demand in county-level destinations. Cities such as Liuzhou and Zibo attracted first-time visitors who preferred self-drive access over public transport, pushing average rental duration above four days in many inland locations. Zuzuche responded by onboarding 3,000 domestic supplier partners inside four months, demonstrating the platform scalability advantage of digital marketplaces. Cultural-nighttime tourism at heritage sites kept utilization high into late evenings, supporting premium pricing windows. Momentum remains intact as the Ministry of Culture and Tourism forecasts domestic trips to exceed 6 billion in 2025, cementing leisure as the backbone of the China vehicle rental market.[1]“Domestic Holiday Travel Bulletin 2024,” Ministry of Culture and Tourism, gov.cn

License-Plate Quotas in Tier-1 Cities Spur Rental Demand

Beijing’s annual lottery caps private cars at 100,000 new plates, 70% reserved for EVs, while Shanghai auctions often exceed CNY 95,000 per plate. These restrictions make daily rental cheaper than ownership for many commuters. Tianjin plans to issue 80,000 more green plates yearly but retains fossil-fuel limits, keeping cost pressure in place. Plate quotas have cut fuel consumption and tailpipe emissions by nearly 50% in affected cities, but they have simultaneously created a reliable flow of renters who view cars as occasional utilities rather than assets. The policy also skews fleets toward EVs, reinforcing government carbon goals and reshaping the China vehicle rental market.[2]“Private Car Plate Auction Results,” Shanghai Municipal People’s Government, shanghai.gov.cn

Growing Licensed-Driver Middle Class

China added more than 22 million licensed drivers in 2024, most residing in tier-2 hubs such as Chengdu and Changsha where rising disposable income meets limited metro rail coverage. A 26-month average wait for Beijing license plates and 70% EV plate allocation redirect ownership intent into rental demand, especially for weekend and holiday usage. Studies from Tsinghua University show a 16% decline in planned commuting by private car among quota-constrained households, yet occasional rental uptake has risen in parallel. The latent demand effect remains visible in showroom surveys indicating new-car sales could have been 72% higher without plate controls, underscoring the structural boost to the China vehicle rental market.

Shift to Digital & Mobile Booking Platforms

Online channels majority of bookings in 2024 and continue to outpace offline growth through predictive pricing and self-service vehicle handover. AI algorithms now match 80% of pick-ups to within 200 meters of the renter, trimming idle mileage and cutting fleet costs. Zuzuche’s API links 600 city fleets to a single interface, giving even small local operators national reach. Super-apps integrate ride-hailing, rail tickets, and hotel reservations, nudging consumer touchpoints toward one-stop mobility ecosystems. As 5G penetration exceeds 80% in East China, real-time inventory visibility becomes a standard expectation across the China vehicle rental market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ride-Hailing and Robotaxi Substitution Risk | -1.1% | National, concentrated in tier-1 cities | Medium term (2-4 years) |

| Rising Vehicle Acquisition and Financing Costs | -0.8% | National, acute in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Provincial Plate-Quota Volatility Disrupts Fleet Logistics | -0.7% | East China, North China (Beijing, Shanghai, Tianjin focus) | Medium term (2-4 years) |

| EV Residual-Value Uncertainty Pressures Profitability | -0.6% | National, concentrated in tier-1 and tier-2 cities | Long term (≥ 4 years) |

Source: Mordor Intelligence

Ride-Hailing & Robotaxi Substitution Risk

Baidu’s Apollo Go completed 839,000 autonomous rides in Q4 2023 at fares 60-70% beneath traditional taxis, illustrating a disruptive price gap. Pony.ai targets a 1,000-vehicle fleet by 2025, while WeRide launched unmanned services linking Beijing Daxing International Airport in February 2025. Robotaxi operators benefit from 24/7 availability and lower driver-related expenses, diverting demand that historically favored rentals for airport transfers and intra-city errands. Consultancy forecasts place the robotaxi segment at nearly USD 76 billion by 2030, signalling competitive headwinds for the China vehicle rental market if incumbents cannot secure autonomous partnerships.[3]“Apollo Go 2023 Q4 Operations Report,” Baidu Apollo, baidu.com

Rising Vehicle Acquisition & Financing Costs

Semiconductor shortages and higher lithium prices added up to CNY 15,000 per unit in OEM cost inflation during 2024, widening the capital hurdle for fleet renewals. BYD alone invested more than USD 5 Billion in R&D that year, translating into pricier invoice rates for rental companies buying in bulk. Transition to electric fleets compounds capital strain because residual values remain volatile and charging infrastructure requires upfront outlays. Smaller operators often face interest rates 150–200 basis points above prime, squeezing margins further in the China vehicle rental market.

Segment Analysis

By Application: Leisure Demand Sustains Market Leadership

Leisure and tourism held 51.27% of China vehicle rental market share in 2024, underpinned by a 7.6% jump in holiday trips and renewed interest in county-level cultural sites. Short road vacations and family reunions make self-drive cars the preferred option, driving average utilization to 74% during peak weeks. Business travel trails in absolute size but records the highest growth; its projected 5.22% CAGR benefits from border reopenings and corporate ESG targets favoring rental over owned fleets.

Second-order effects are already visible in spending patterns: leisure customers reserve 2.1 days longer than pre-pandemic averages, while business travelers increasingly opt for chauffeur-driven packages that bundle telematics and emissions dashboards for reporting purposes. Platform integrations with tourist attractions enable one-click car plus ticket bundles, extending the monetization window per rental.

By Booking Type: Online Dominance Deepens

Online reservations captured 64.38% of revenue in 2024—proof that frictionless mobile journeys have become table stakes, it is also growing at a CAGR of 5.41% through 2030. Predictive pricing engines reduce search-to-booking windows to four minutes on average and increase ancillary upselling by 18%, raising lifetime value per customer. Offline stores still matter in lower-tier cities where walk-in foot traffic remains notable, but omnichannel hand-over stations now allow QR-code key retrieval without staff, closing the convenience gap.

Investment continues to tilt toward cloud CRM and in-car IoT sensors that feed usage data back to the platform, enabling same-day inventory rotation across multiple districts. As a result, fleet operators using dynamic online allocation achieve 12% higher revenue-per-vehicle than peers relying on static offline reservations, a differential expected to expand in the China vehicle rental market.

By End-User Type: Self-Drive Reigns While Chauffeur Services Scale

Self-drive contracts controlled 71.32% of total revenue in 2024, fuelled by the cultural preference for independent travel and growing confidence behind the wheel. Yet chauffeur-driven packages advance at 5.45% annually because corporate procurement teams view them as safer and more compliant with ESG audit trails. Chauffeur fleets feature NEV penetration above 60%, exceeding the broader average and positioning them well for low-emission zones in Beijing or Shenzhen Central Business Districts.

Self-drive growth remains robust through family-oriented itineraries, outdoor camping trends, and the ease of app-based navigation in unfamiliar provinces. Simultaneously, chauffeur products diversify into event logistics and cross-border shuttles into Hong Kong, expanding addressable demand inside the China vehicle rental market.

By Vehicle Class: Economy Volume, SUV Momentum

Economy cars represented 48.75% of fleet deployments in 2024, valued for affordability amid inflationary pressures. SUV/MPV categories, however, post a 5.61% CAGR as multi-generational travel requires extra seating and luggage capacity. Hybrids dominate new SUV orders, reflecting consumers’ wish to ease range anxiety without sacrificing sustainability metrics. Luxury rentals thrive mainly in Shanghai and Beijing, where corporate hospitality accounts for more than half the segment’s revenue. The mid-scale category bridges price and comfort, appealing to start-ups that balance image with cost.

Technology rather than trim now guides purchase decisions: integrated dashcams, voice-controlled infotainment, and ADAS levels 2+ are standard in 70% of new units ordered for the China vehicle rental market, augmenting safety and lowering insurance premiums.

By Powertrain: ICE Still Leads but Hybrids Accelerate

Internal combustion engines held 62.11% of 2024 volume, thanks to legacy fleet stocks and broader refuelling infrastructure. Hybrid electric vehicles grow fastest at 5.78% CAGR, offering a near-term compliance path for operators wary of full battery electrics. Fleet electrification gains momentum as MIIT expects public-sector fleets to reach 80% NEV penetration by 2025, pushing rental companies to align quickly. Battery EV rentals face charging downtime challenges, yet solutions like BYD’s 5-minute ultra-charging system promise to slash turn-around intervals and tilt cost-benefit calculus toward full electric in major airports.

Residual-value risk remains the main deterrent; however, OEM-backed buy-back guarantees now cover 36 months on most high-volume EV models, reducing uncertainty and supporting broader rollout across the China vehicle rental market.

Note: Segment shares of all individual segments available upon report purchase

By Rental Duration: Short-Term Dominance Meets Mid-Term Upswing

Contracts under seven days claimed 58.83% of 2024 bookings, reflecting holiday and project travel cycles. Mid-term rentals, spanning one week to one month, register a 4.97% CAGR as corporates move from fixed fleets to subscription-based mobility budgets. Subscription packages include insurance, maintenance, and CO₂ reporting dashboards, attracting finance and consulting firms concerned with ESG disclosure. Long-term rentals remain a niche but stable stream serving project sites and government tenders that require guaranteed uptime.

Flexible duration add-ons—where customers convert a three-day hire into a month-long plan without penalties—are gaining popularity, reducing churn and stabilizing cash flow for operators within the China vehicle rental market.

By Service Channel: Off-Airport Sites Expand Access

Off-airport and downtown locations delivered 64.51% of 2024 revenue because they fit daily urban mobility needs and lower last-mile search costs. Mall-based kiosk pick-ups, cycle-sharing style unlock points, and residential parking-lot depots now form a dense grid in tier-1 and tier-2 cities. On-airport counters recover fastest, clocking 5.33% CAGR, as inbound business travel normalizes and flight connections multiply. Increased bilateral flights into Guangzhou and Shenzhen feed premium categories and chauffeur-driven demand.

Operators integrate route-planning APIs with airport authority traffic feeds, allowing drop-and-go hand-over inside 45 seconds on average, which lifts turnover rates in the China vehicle rental market.

Geography Analysis

East China generated 34.71% of 2024 turnover, buoyed by Shanghai’s financial services cluster, Jiangsu’s export factories, and Zhejiang’s thriving e-commerce hub. Strong disposable incomes, high licence-plate premiums, and sophisticated digital adoption keep utilization and yield above national averages. Fleet renewal cycles here shorten to 18 months, reflecting customer appetite for latest-tech hybrids and EVs.

South-Central China is the fastest-growing region at 5.76% CAGR through 2030. Shenzhen’s semiconductor corridor and Guangzhou’s export-import backbone recreate stable business travel flows, while proximity to Hong Kong adds cross-border rental demand. Local authorities subsidize public charging networks, enabling operators to push EV penetration beyond 50% by 2026.

North China, anchored by Beijing, benefits from political events, international summits, and high cultural tourism volumes. Stringent plate quotas continue to convert failed lottery applicants into renters, supporting steady revenue despite slower macro growth. West and Northeast China still lag in share but accelerate as infrastructure, tourism circuits, and mining investments unlock fresh routes, collectively enlarging the China vehicle rental market footprint.

Competitive Landscape

A massive number of firms operate nationwide, yet top six brands control near-half the fleet, signalling moderate concentration. CAR Inc. leverages more than 1,000 city outlets and deep ties with SAIC to maintain scale advantages. eHi Car Service partners with Didi to pool demand algorithms and integrate ride-hailing cross-selling.

Zuzuche differentiates via a meta-platform that hosts almost 6,000 micro-operators and runs AI fraud detection on each booking request within 200 milliseconds.Automakers such as BYD deploy captive leasing arms to seed new EV models, while tech giants Baidu and Pony.ai pilot robotaxis that could bypass rental middlemen.

Defensive strategies range from corporate long-term subscription bundles to exclusive charging-station access for loyalty members. ESG-linked offerings, dynamic pricing, and on-app carbon calculators now decide wallet share inside the China vehicle rental market.

China Vehicle Rental Industry Leaders

-

Avis Budget Group, Inc.

-

The Hertz Corporation

-

eHi Car Service (Enterprise Holdings)

-

Shouqi Car rental (Europcar Mobility Group)

-

Beijing China Auto Rental (CAR Inc.)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: BYD introduced its Super E-Platform 5-minute charger and announced 4,000 national ultra-fast stations, easing EV turnaround for fleet operators.

- February 2025: WeRide launched Robotaxi GXR on unmanned airport routes in Beijing, targeting several hundred vehicles by year-end.

- May 2024: NIO unveiled the Onvo L60 SUV at CNY 219,900, broadening lower-price EV options for rental fleets through a 100-store retail plan.

China Vehicle Rental Market Report Scope

Vehicle rental is hiring a vehicle for short periods of time that generally ranges from a few hours to a few weeks. The aforementioned scope has been considered in the market study.

China vehicle rental market has been segmented by application, by booking type and by end-user type.

| By Application | Leisure / Tourism |

| Business Travel | |

| By Booking Type | Offline Access |

| Online Access | |

| By End-User Type | Self-Driven |

| Chauffeur-Driven | |

| By Vehicle Class | Economy |

| Mid-Scale | |

| Luxury | |

| SUV / MPV | |

| By Powertrain | Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Battery Electric Vehicle (BEV) | |

| By Rental Duration | Short-Term (Less than or equal to 1 Week) |

| Medium-Term (1 Week to 1 Month) | |

| Long-Term (More than 1 Month) | |

| By Service Channel | On-Airport |

| Off-Airport / Downtown | |

| By Region | East China |

| South-Central China | |

| North China | |

| West China | |

| Northeast China |

By Application

| Leisure / Tourism |

| Business Travel |

By Booking Type

| Offline Access |

| Online Access |

By End-User Type

| Self-Driven |

| Chauffeur-Driven |

By Vehicle Class

| Economy |

| Mid-Scale |

| Luxury |

| SUV / MPV |

By Powertrain

| Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Battery Electric Vehicle (BEV) |

By Rental Duration

| Short-Term (Less than or equal to 1 Week) |

| Medium-Term (1 Week to 1 Month) |

| Long-Term (More than 1 Month) |

By Service Channel

| On-Airport |

| Off-Airport / Downtown |

By Region

| East China |

| South-Central China |

| North China |

| West China |

| Northeast China |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the China vehicle rental market in 2025?

The China vehicle rental market size stands at USD 21.15 billion in 2025 and is on track for a 5.13% CAGR through 2030.

Which application dominates the China vehicle rental market?

Leisure and tourism leads with 51.27% revenue share in 2024, driven by a national rebound in domestic trips.

What booking channel is most popular?

Online platforms command 64.38% share, supported by AI-driven pricing and mobile self-service pick-ups.

How fast are hybrid rentals growing?

Hybrid vehicles are expected to expand at 5.78% CAGR, the highest among all powertrains, as they bridge range and sustainability goals.

Which region is growing quickest?

South-Central China shows the strongest momentum at 5.76% CAGR, propelled by Shenzhen and Guangzhou’s technology and trade sectors.

Are robotaxis a threat to rental firms?

Yes; autonomous fleets from Baidu, Pony.ai, and WeRide already offer rides priced up to 70% lower than traditional taxis, pressuring conventional rental demand in tier-1 cities.

Page last updated on: June 27, 2025