China Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

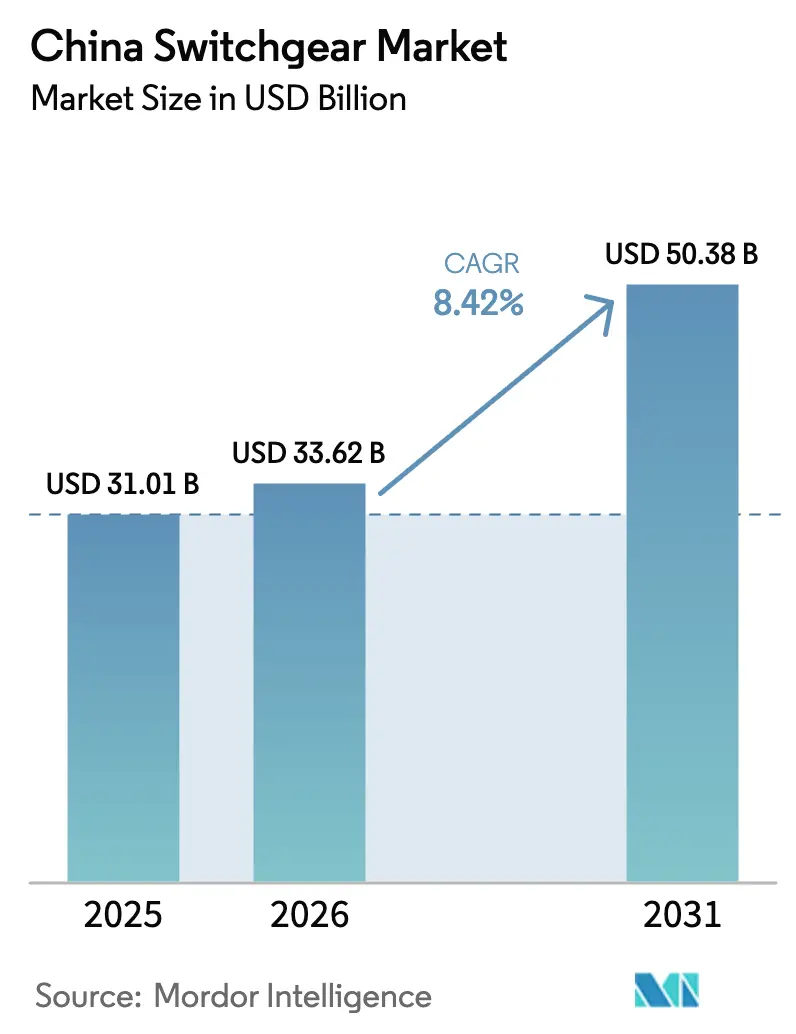

| Base Year Market Size (2025) | USD 31.01 Billion |

| Market Size (2026) | USD 33.62 Billion |

| Market Size (2031) | USD 50.38 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Switchgear Market Analysis by Mordor Intelligence

The China Switchgear Market size is expected to grow from USD 31.01 billion in 2025 to USD 33.62 billion in 2026 and is forecast to reach USD 50.38 billion by 2031 at 8.42% CAGR over 2026-2031.

Accelerated ultra-high-voltage (UHV) transmission construction, rapid renewable additions, and the build-out of data centers and 5G base stations underpin steady demand across voltage classes. Momentum also comes from Beijing’s SF₆-phase-out policy that is shifting procurement toward vacuum and fluoroketone technologies. Medium-voltage gear benefits from urban smart-grid upgrades, while high-voltage equipment gains from new ±800 kV DC and 1 000 kV AC corridors that move western wind and solar power east. Manufacturers that embed AI-driven diagnostics and IEC 61850 communication are capturing premium pricing despite intensifying price competition.

Key Report Takeaways

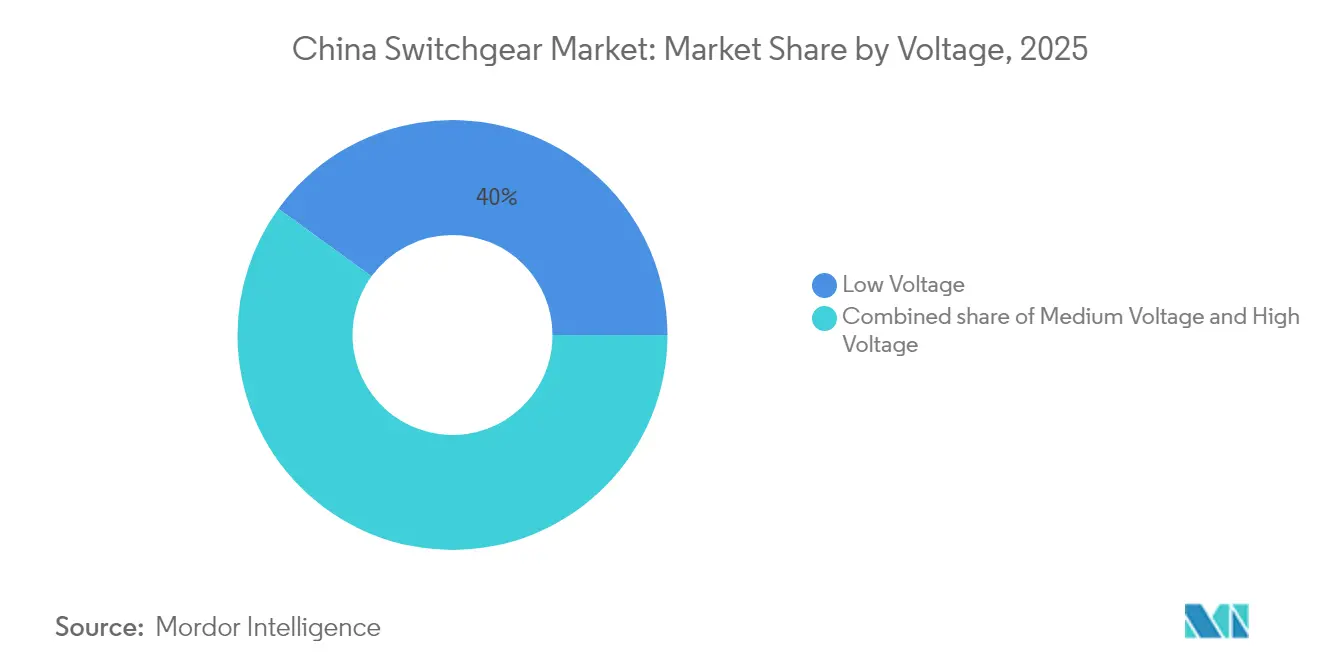

- By voltage, low-voltage equipment led with 40.02% revenue share of the China switchgear market in 2025, whereas high-voltage products are forecast to expand at a 10.41% CAGR to 2031.

- By insulation, air-insulated systems accounted for a 70.35% share in 2025; the “others” category, including vacuum and solid-state solutions, is advancing at a 16.22% CAGR through 2031.

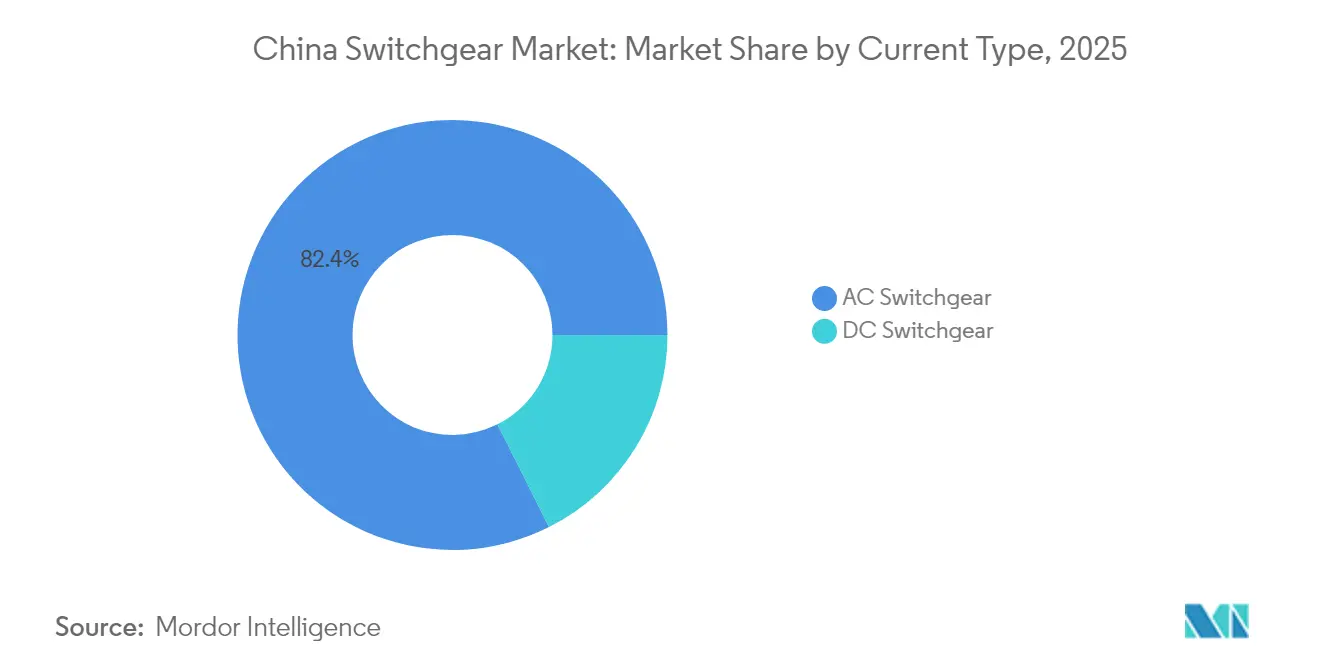

- By current type, AC installations held 82.41% of demand in 2025, while DC switchgear records the fastest 9.32% CAGR to 2031.

- By installation, indoor assemblies commanded an 80.85% share in 2025; outdoor units are growing at an 11.08% CAGR on the back of remote renewable projects.

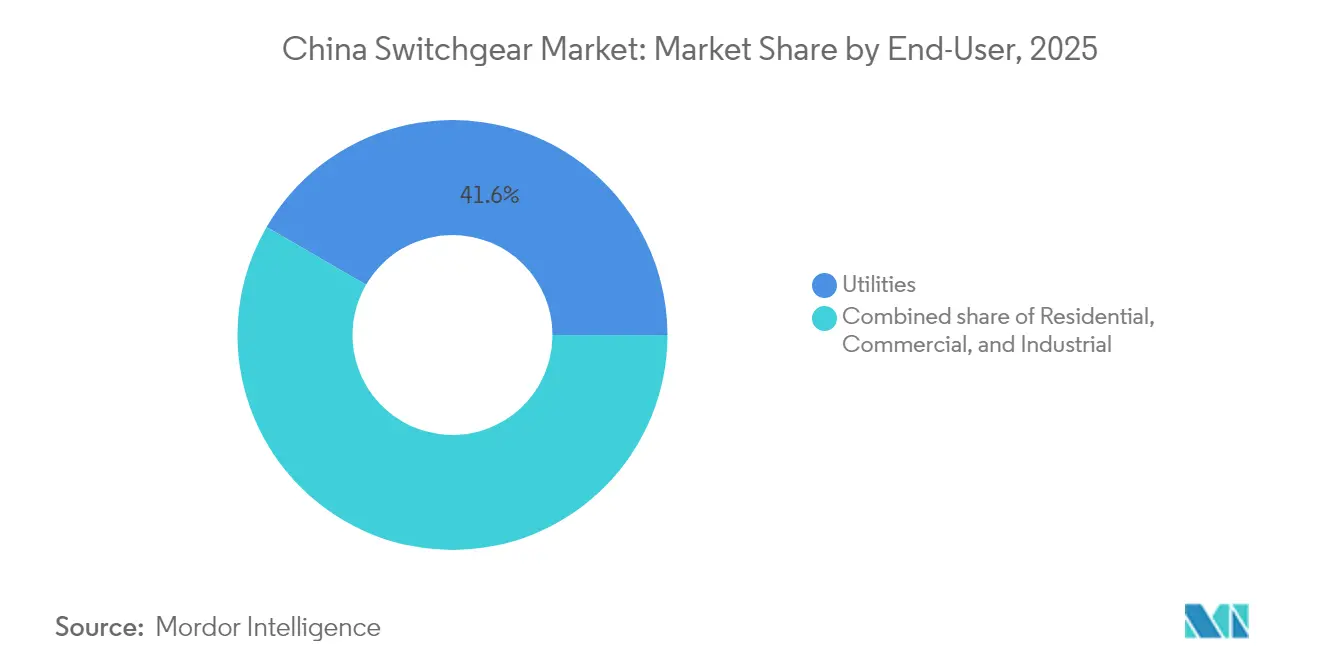

- By end-user, utilities captured 41.62% of 2025 spend and will continue to lead with a 8.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high-voltage transmission build-out | +2.10% | Northwest-to-east corridors | Medium term (2-4 years) |

| Renewable capacity additions accelerating upgrades | +1.80% | Western renewables, offshore Jiangsu & Guangdong | Long term (≥ 4 years) |

| Urban distribution smart-grid retrofits | +1.30% | Tier-1 and tier-2 cities | Medium term (2-4 years) |

| Data-center & 5G rollouts boosting MV demand | +1.50% | Greater Bay Area, Yangtze River Delta, Beijing-Tianjin-Hebei | Short term (≤ 2 years) |

| SF₆-free eco-switchgear replacement cycle | +1.20% | Coastal provinces with strict emission policies | Long term (≥ 4 years) |

| AI-enabled digital switchgear | +1.00% | National pilot deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-High-Voltage Transmission Build-Out

China energized the 1000 kV Sichuan-Chongqing AC line in late 2024, adding 3.4 GW of transfer capacity and ordering more than 200 GIS bays rated at 1,100 kV.(1)National Development and Reform Commission, “UHV Transmission Investment Plan,” ndrc.gov.cn Each corridor raises one-off demand for breakers that interrupt 63 kA fault currents. State Grid’s 14th Five-Year Plan sets annual UHV capex near CNY 500 billion, translating into 15-18 new cross-provincial links by 2025 [NDRC.GOV.CN]. High-voltage switchgear, therefore, outpaces the broader China switchgear market as provincial bidders fight for supply slots. However, price ceilings of roughly CNY 2.5 million per 1,100 kV bay keep gross-margin expansion limited.

Renewable Capacity Additions Accelerating Grid Upgrades

China added 217 GW of solar and 76 GW of wind in 2024, lifting cumulative renewables above 1450 GW.(2)National Energy Administration, “2024 Renewable Installation Statistics,” nea.gov.cn Inverter-based resources need fast-acting protection that recognizes sub-cycle transients. Gansu’s Jiuquan wind hub retrofitted 340 kV collector substations with IEC 61850-90-5 relays, cutting coordinated-trip times to 15 ms. National grid-code updates require new projects above 50 MW to install fault-ride-through-capable switchgear, adding 8-12% to substation costs yet curbing curtailment. Offshore wind farms adopt 66 kV subsea gear that avoids platforms and trims installation time by 30%.

Urban Distribution Smart-Grid Retrofits

Tier-1 cities face rising peak loads from electric vehicles and air-conditioning. Distribution utilities now specify ring-main units with solid insulation, embedded sensors, and Modbus-enabled breakers that push real-time data to control centers. Shanghai has mandated IEC 61850 profiles for all 10 kV feeders since mid-2024, spurring secondary demand for retrofit-friendly cabinets that occupy 40% less floor space. The upgrade cycle underpins medium-voltage strength within the China switchgear market from 2025-2028.

Data-Center & 5G Roll-Outs Boosting MV Demand

China’s data-center spend hit USD 47.23 billion in 2024 and could double by 2030. Each 10 MW hall needs four to six medium-voltage line-ups that step down utility feeds. Meanwhile, 680,000 new 5G base stations installed in 2024 require outdoor ring-main units that secure 99.99% uptime. Vendors offering compact, IP65-rated cabinets that can be installed by a single crew win a share of the China switchgear market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent SF₆ phase-out compliance cost | -0.80% | Coastal provinces with strict enforcement | Medium term (2-4 years) |

| Margin squeeze from price competition | -1.10% | Low-voltage and air-insulated segments nationwide | Short term (≤ 2 years) |

| Power-electronics chip supply bottlenecks | -0.60% | Digital switchgear and DC gear countrywide | Short term (≤ 2 years) |

| Slow standardization of grid protocols | -0.40% | Provincial grid variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent SF₆ Phase-Out Compliance Cost

Utilities replacing SF₆ bays face outlays 30% above original prices, plus CNY 150 000-250 000 per site for continuous monitoring.(3) Smaller municipalities choose between costly retrofits and rising carbon offset liabilities under the national ETS. Vacuum breakers introduce chopping overvoltages that need extra surge protection, adding 6-9% to the bill-of-materials. Procurement consortia in Guangdong and Zhejiang negotiate multi-year fluoroketone supply to spread risk, yet not all utilities enjoy this leverage.

Margin Squeeze from Intense Domestic Price Competition

Over 100 domestic makers compete in low-voltage panels, driving 2-3 percentage-point margin erosion since 2023. Provincial tenders often award contracts on price alone, pushing vendors to bundle IoT software to preserve value. Mid-tier firms lacking R&D scale risk consolidation as they struggle to fund digital upgrades demanded by buyers of the Chinese switchgear market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: High-Voltage Growth Accelerates

Low-voltage equipment retained 40.02% revenue in 2025, anchored by residential and commercial builds. High-voltage products between 72.5 kV and 1,100 kV are on a steep 10.41% CAGR, reflecting fifteen new UHV projects in State Grid’s pipeline. Medium-voltage remains the backbone of urban distribution networks, yet its share inches down as high-voltage units claim a larger revenue mix. The Sichuan-Chongqing 1,000 kV link alone required 220 fluoroketone-insulated GIS bays. Schneider Electric’s smart molded-case breakers with plug-and-play Modbus captured 22% of Chinese MCCB sales in 2024. Solid-insulation ring-main units save 35% of floor space, a critical advantage where real estate exceeds CNY 80 000/m². Premature retirements of legacy electromechanical gear installed before 2000 add a replacement wave that sustains double-digit high-voltage expansion.

The China switchgear market size for the high-voltage segment is expected to climb from USD 12.83 billion in 2025 to USD 23.25 billion by 2031. High-voltage products thereby widen their contribution to more than 44.60% of total revenue in 2031. Conversely, the China switchgear market share of low-voltage gear is projected to slide below 35.40% as building code-driven demand loses weight against grid investments.

By Insulation: Vacuum and Solid-State Disrupt Air Dominance

Air-insulated systems held 70.35% of 2025 sales. Utilities, however, favor vacuum interrupters that avoid greenhouse-gas handling. Vacuum already powers 62% of medium-voltage shipments, and solid dielectric designs now target coastal regions where salt-fog accelerates metal corrosion. ABB’s VD4 range boasts 40,000 mechanical operations and 100 fault interruptions, underpinning wide adoption. Siemens’ 8DJH fluoronitrile GIS met Chinese type tests in 2024 and entered mass production in Jinan. Solid-insulation switchgear positions epoxy-embedded busbars inside compact enclosures, reducing footprint by 50%.

The China switchgear market size tied to the “others” category is forecast to jump from USD 9.78 billion in 2025 to USD 24.12 billion in 2031, reflecting a 16.22% CAGR. Air-insulated units remain price leaders for rural greenfield sites, yet face gradual dilution in urban settings as land costs and emission rules tighten.

By Current Type: DC Gains Critical Mass

AC systems still dominate at 82.41% but DC solutions grow at 9.32% annually. ±800 kV and ±1 100 kV HVDC corridors, DC-coupled solar farms, and 350 kW fast-charging corridors propel demand. Shenzhen’s 10 MW DC microgrid isolates from the main grid in under 1 ms using solid-state breakers. HVDC breakers remain expensive, yet policy favors local sourcing, spurring R&D among domestic firms.

By Installation: Indoor Prevalence Meets Outdoor Expansion

Indoor assemblies commanded 80.85% in 2025, backed by urban substations that value controlled environments. Outdoor gear records 11.08% CAGR as western renewable bases and offshore wind farms require IP65-rated cabinets resilient to sand, salt, and temperature extremes. Modular outdoor units that integrate protection relays and communication gateways cut civil-works costs by near 20%.

By End-User: Utilities Remain Demand Anchor

Utilities held 41.62% of spend in 2025 and will expand at a 8.97% CAGR as grid modernization and renewable integration intensify. Industrial users upgrade to harmonic-filtering switchgear to meet GB/T 14549 limits, while commercial buildings adopt intelligent low-voltage boards that link with building-management systems.

Geography Analysis

Eastern coastal provinces, Jiangsu, Zhejiang, Guangdong, and Shandong, generated 47.60% of 2025 revenue. Jiangsu installed 12 GW of offshore wind last year, needing 66 kV subsea switchgear and onshore collectors.The Greater Bay Area pilots AI-enabled substations that anticipate failures six months ahead. Western provinces, Gansu, Qinghai, Inner Mongolia, Xinjiang, supplied 28.30% of revenue despite sparse populations, owing to their role as renewable power bases. Substations in these regions specify outdoor IP65 cabinets capable of handling -40 °C winters and +50 °C summers.

Central provinces, Henan, Hubei, Hunan, and Anhui, captured 16.20% of demand, fueled by automotive and machinery clusters. Zhengzhou and Wuhan deploy smart-grid pilots that merge distributed solar and battery storage, calling for bi-directional switchgear. The northeast, Liaoning, Jilin, and Heilongjiang, took 7.90% share and are upgrading grids to support electric heating. Provincial SF₆ rules vary: Zhejiang and Guangdong enforce stricter standards, accelerating vacuum uptake. The Yangtze River Delta pilots cross-provincial grid interconnection that requires unified IEC 61850 profiles.

Tier-three cities in Sichuan, Yunnan, and Guizhou see annual growth near 12.60%, backed by hydropower and rural electrification. As disposable incomes rise, residential upgrades contribute modest yet rising low-voltage demand.

Competitive Landscape

The top five suppliers, ABB, Siemens, Schneider Electric, CHINT Group, and Pinggao Electric, hold roughly 35% of the Chinese switchgear market. Multinationals dominate UHV tenders by leveraging advanced R&D, while domestic players lead in volume-driven low- and medium-voltage orders. ABB’s USD 300 million Xiamen smart-factory expansion strengthens local presence. Siemens co-develops SF₆-free solutions with provincial utilities. Schneider partners with CHINT’s 8,000-dealer network to widen reach.

Domestic consolidation continues: TBEA’s 51% stake in NR Electric created a CNY 40 billion group spanning transformers and protection relays. Pinggao and China XD benefit from State Grid ties, but face mandated cost reductions. Start-ups like Starpower Semiconductor raise capital for silicon-carbide DC breakers targeting solar farms and EV chargers. Digital platforms that bundle cloud analytics secure service contracts worth 12-15% of revenue, cushioning hardware margin pressure.

China Switchgear Industry Leaders

Pinggao Group Co. Ltd

China XD Electric Co. Ltd

CHINT Group Co. Ltd

ABB Ltd (China operations)

Siemens AG (China operations)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hitachi Energy delivered the world’s first SF₆-free 550 kV GIS to State Grid, proving large-scale eco-design viability.

- May 2025: ABB finalized its USD 150 million purchase of Siemens’ wiring-accessory business in China, expanding smart-building channels.

- March 2025: Hitachi Energy’s Beijing and Datong plants earned National Green Factory status, pledging 100% fossil-free electricity use.

- January 2025: State Grid announced a record USD 88.7 billion investment program for 2025, focusing on UHV and digitalization.

China Switchgear Market Report Scope

A switchgear is a term associated with power system protection and is used for regulating, switching on or off the electrical circuit, and controlling the electrical power system. The different components of switchgear are circuit breakers, isolators, relays, switches, fuses, and control panels. It is used to de-energize the equipment for testing, maintenance, and clearing the fault.

The China Switchgear Market is segmented by voltage, insulation, current type, installation, and end-user. By voltage market is segmented into low voltage, medium voltage, and high voltage. By insulation, the market is segmented into gas-insulated switchgear, air-insulated switchgear, and others. By current type, the market is segmented into AC switchgear, DC switchgear. By installation, the market is segmented into Indoor and outdoor, and by end-user, the market is segmented into utilities, residential, commercial, and industrial. For each segment, the market sizing and forecasts have been provided based on value (USD).

| Low Voltage |

| Medium Voltage |

| High Voltage |

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| By Voltage | Low Voltage |

| Medium Voltage | |

| High Voltage | |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial |

Key Questions Answered in the Report

What is the current value of the China Switchgear Market?

The China Switchgear Market size was USD 33.62 billion in 2026 and is projected to reach USD 50.38 billion by 2031.

Which segment is growing fastest within Chinese switchgear?

High-voltage equipment, buoyed by UHV projects, is expanding at a 10.41% CAGR through 2031.

How strict are China’s new SF₆ regulations?

Draft rules cap leak rates at 0.5% and mandate annual reporting, effectively pushing utilities toward vacuum and fluoronitrile solutions by 2028.

Why is DC switchgear gaining ground?

Growth in HVDC links, DC-coupled solar farms, and 350 kW fast-charging corridors lifts DC switchgear demand at a 9.32% CAGR.

Which provinces buy the most switchgear?

Coastal Jiangsu, Zhejiang, Guangdong, and Shandong together generated 47.60% of 2025 demand due to dense urban loads and offshore wind installs.

Who are the top suppliers in China’s switchgear field?

ABB, Siemens, Schneider Electric, CHINT Group, and Pinggao Electric account for about 35% of total revenue.

Page last updated on: