Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

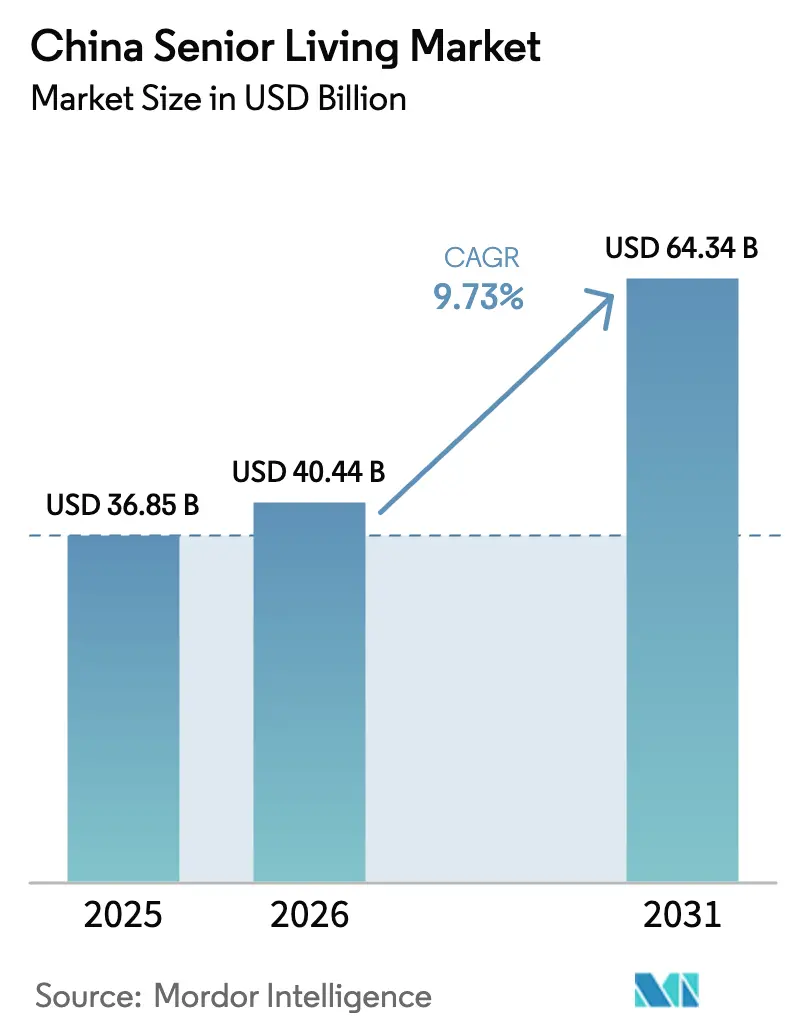

| Base Year Market Size (2025) | USD 36.85 Billion |

| Market Size (2026) | USD 40.44 Billion |

| Market Size (2031) | USD 64.34 Billion |

| Growth Rate (2026 - 2031) | 9.73% CAGR |

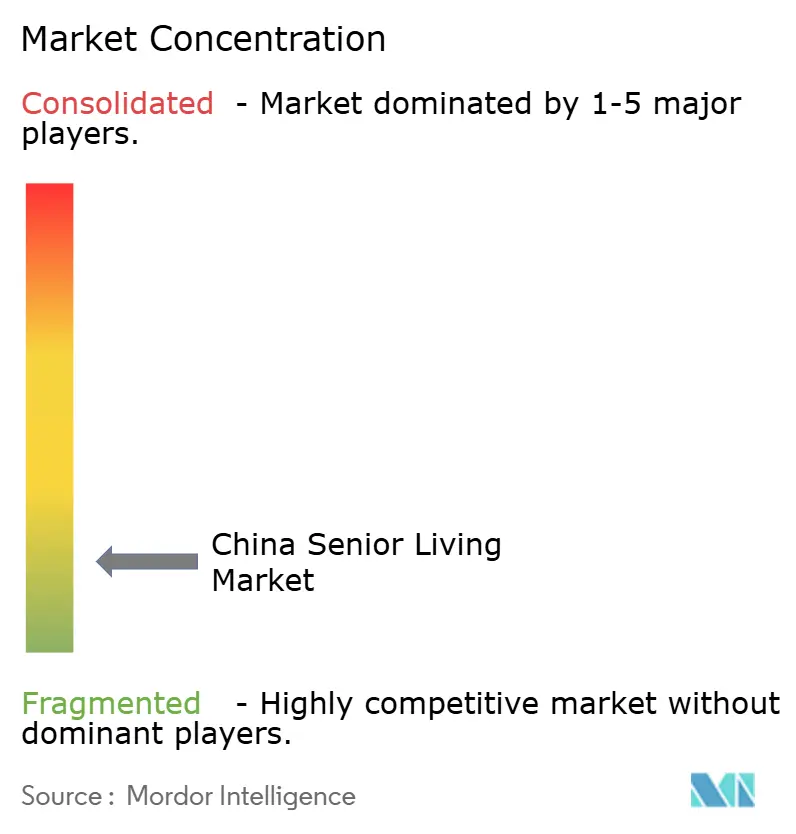

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Senior Living Market Analysis by Mordor Intelligence

The China Senior Living Market size was valued at USD 36.85 billion in 2025 and is estimated to grow from USD 40.44 billion in 2026 to reach USD 64.34 billion by 2031, at a CAGR of 9.73% during the forecast period (2026-2031).

Accelerated urban wealth accumulation, widening long-term care insurance (LTCI) pilots, and the erosion of multi-generational co-residence continue to widen demand-supply gaps, particularly in higher-acuity settings. Assisted living remains the anchor offering, but national dementia-care rules issued in late 2024 have shifted investor sentiment toward certified memory-care units that command premium pricing. Operators with integrated health campuses are redirecting capital toward rehabilitation suites, telehealth hubs, and chronic-disease clinics, while public–private partnership (PPP) land packages in inland provinces lower entry costs for newcomers. Competition is fragmenting between insurance-backed conglomerates and property developers repositioning unsold residential stock as senior housing, a divide intensified by technology investments that cut emergency-room transfers by up to 20% in Beijing and Shanghai facilities.

Key Report Takeaways

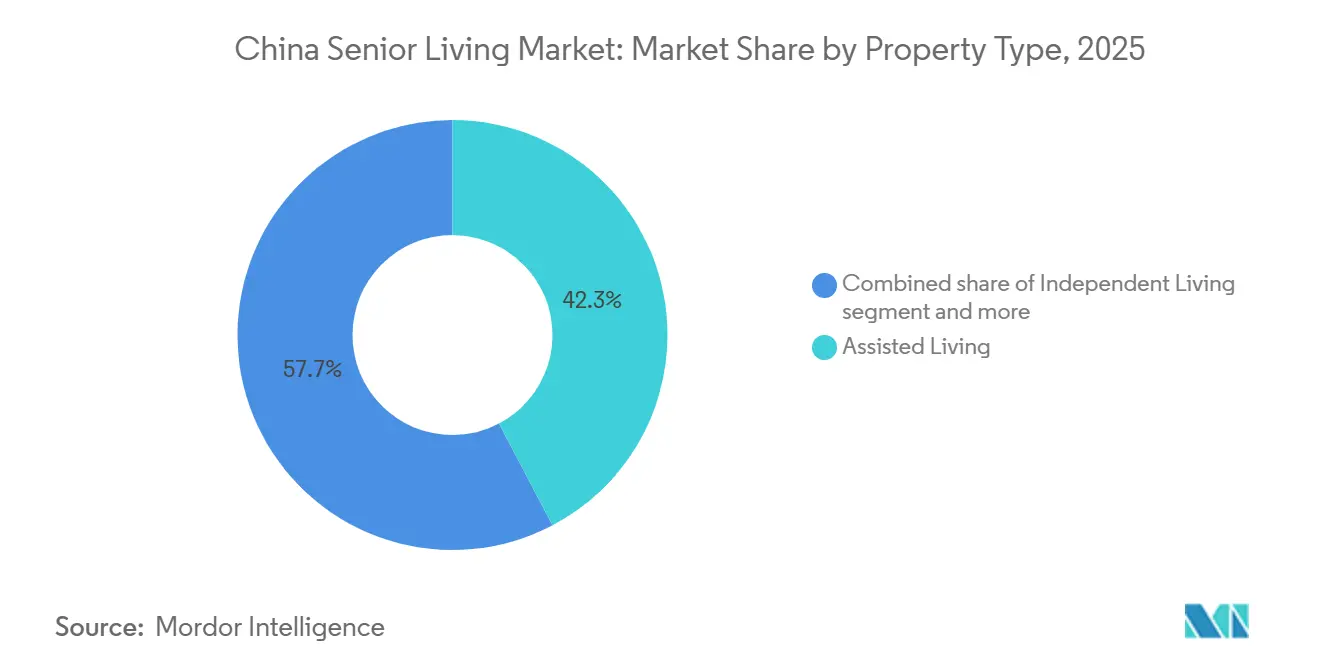

- By property type, assisted living accounted for 42.3% of China's senior living market share in 2025, while memory care is forecast to grow at a 10.55% CAGR through 2031.

- By business model, long-lease and rental contracts accounted for 45.9% of the China senior living market in 2025 and are projected to expand at a 10.81% CAGR through 2031.

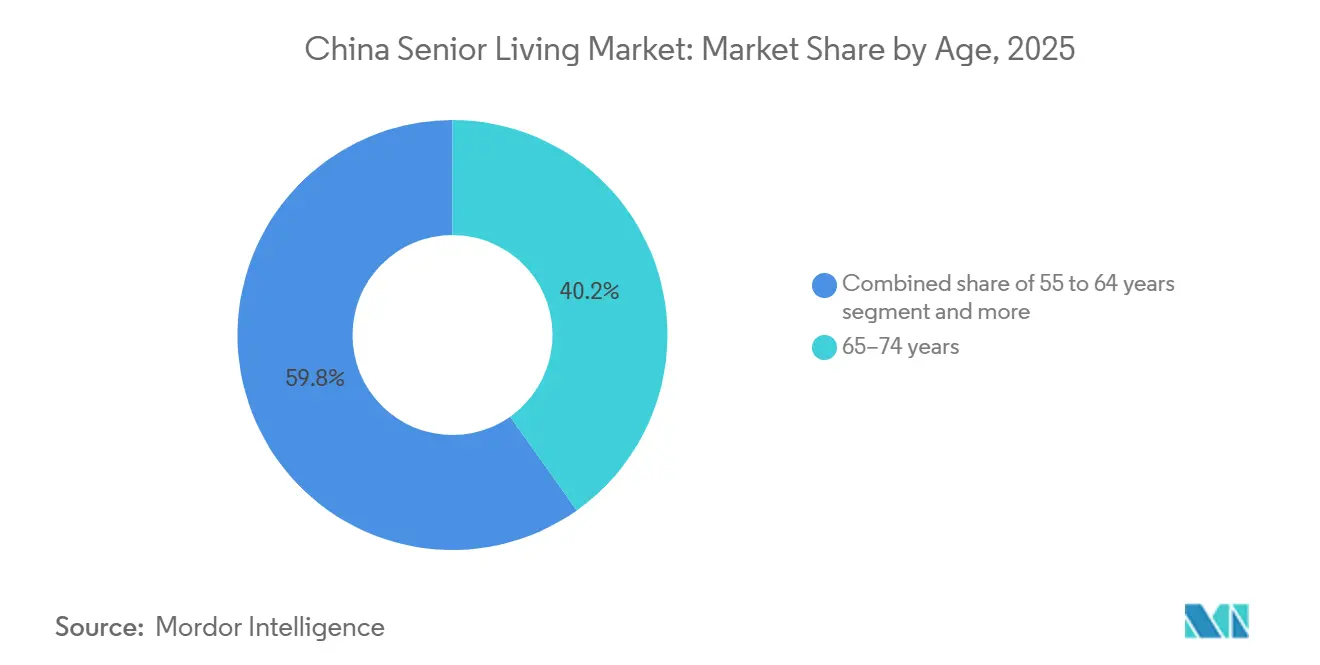

- By age, the 65–74 cohort accounted for 39.8% of demand in 2025; the above-85 group is expected to grow at an 11.08% CAGR, the fastest among all brackets.

- By city, Shanghai led with 26.1% revenue in 2025, whereas Chengdu is set to record the highest growth at 11.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Senior Living Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid aging 75–85+ cohort | +2.8% | National, concentrated in Beijing, Shanghai, Jiangsu, Zhejiang, Guangdong | Long term (≥ 4 years) |

| Rising household wealth in Tier 1–2 cities | +2.3% | Beijing, Shanghai, Shenzhen, Guangzhou, Chengdu, Hangzhou | Medium term (2–4 years) |

| Healthcare-integration opportunities | +1.9% | National, early adoption in Beijing, Shanghai, Guangzhou | Medium term (2–4 years) |

| Government supply incentives and LTCI pilots | +1.6% | National, 49 pilot municipalities | Short term (≤ 2 years) |

| Technology-enabled operations | +1.2% | Tier 1 cities, gradual Tier 2 diffusion | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Aging Cohort Expansion Reshaping Care-Level Mix

China will see its population aged 75 and above outpace all other age brackets by 2031, lifting demand for assisted living, memory care, and skilled nursing. By end-2024, seniors 65 and older totaled 220.23 million, equal to 15.6% of the population[1]National Bureau of Statistics of China, “Statistical Communiqué on National Economic and Social Development 2024,” stats.gov.cn. Higher prevalence of diabetes, cardiovascular disease, and cognitive impairment among this group pushes operators to retrofit independent-living wings into dementia-ready units and to embed geriatric clinics on campus. Early adopters tied into LTCI pilots have begun billing bundled rehabilitation services, raising utilization while cutting emergency transfers. The WHO Integrated Care for Older People framework, piloted since 2024, is accelerating the adoption of functional-ability assessments and interoperable electronic records[2]World Health Organization, “Integrated Care for Older People Pilot in China,” who.int . Operators capable of staffing higher-dependency units are rewarded with longer lengths of stay and pricing power that outstrips inflation.

Wealth Accumulation in Coastal Hubs: Unlocking Premium Segments

Household savings in Tier 1 and Tier 2 cities now support monthly fees ranging from USD 1,100 to USD 2,750 for assisted living, a level unattainable a decade earlier. Rising pension income and property gains underpin a lifestyle-oriented view of professional care. Taikang Life’s Wu Garden in Suzhou, opened in 2024, markets “migratory bird” retirement, leveraging China’s high-speed rail to shuttle residents seasonally. Ping An’s USD 1.7 billion buy-out of its digital-health unit in January 2025 further signals confidence that telehealth ecosystems can justify premium pricing. Despite strength at the top end, mid-market facilities in inland cities still face occupancy below 60%, underscoring uneven wealth dispersion.

Healthcare Integration Blurring Institutional and Clinical Boundaries

Ministries overseeing civil affairs and health formally endorsed “medical-eldercare integration” in 2024, allowing qualified communities to bill provincial insurance schedules for select clinical services[3]Ministry of Human Resources and Social Security, “Eldercare Workforce Report 2024,” chinadaily.com.cn. China Everbright stations geriatricians on-site two days a week across 190 institutions, lowering readmissions and unlocking bundled-payment revenue. Cross-border schemes such as the Hong Kong–Guangdong RCHE initiative let Hong Kong residents use social-welfare vouchers at licensed mainland homes, effectively creating a new reimbursement channel. While integration diversifies cash flow, compliance costs tied to staff ratios and equipment standards raise capital needs, favoring larger chains.

Government Land and Financing Incentives Accelerating Supply

The 14th Five-Year Plan sets national bed-supply targets and requires new urban projects to allocate eldercare space. Guangdong’s 2024 work report earmarked USD 4.2 billion in subsidies for 31,000 home modifications and 3,431 community canteens, with PPP land made available below market rates. LTCI pilots already cover 180 million citizens, reimbursing part of nursing-home bills and stabilizing operator revenue. Insurance giants such as Taikang Life have announced USD 14 billion in allocated capital, while property developers convert unsold apartments to meet mandated supply. Bottlenecks persist in zoning approvals and fire-safety compliance, stretching project lead times.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for family-based care | -1.4% | Nationwide, acute in rural and Tier 3+ cities | Long term (≥ 4 years) |

| Staffing shortages and uneven capability | -1.1% | Nationwide, acute in Tier 2–3 cities | Medium term (2–4 years) |

| Affordability gaps and complex regulation | -0.9% | Nationwide, severe in municipalities with limited LTCI | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cultural Norms Slowing Institutional Adoption Beyond Tier 1 Cities

Deep-rooted filial piety sustains a family-care bias, especially in smaller cities and rural counties. Surveys in Chengdu during 2024 showed parents resisting relocation despite adult children’s willingness to pay, keeping occupancy below 60% in many Tier 2 projects. The Hong Kong–Guangdong RCHE scheme, though cost-efficient, had limited uptake because seniors prefer familiar culture and food. Operators reframe facilities as lifestyle communities with art studios and excursions, but messaging resonates mainly with urban elites. Consequently, the Chinese senior living market grows unevenly, with conversion highest where cultural barriers are weakest.

Workforce Shortages and Quality Gaps Constraining Service Delivery

China needs roughly 13 million trained caregivers, yet employs about 1 million in 2024, only 300,000 of whom hold formal credentials. Average monthly pay of USD 690 trails other urban jobs, pushing annual turnover to 23.3% and burnout above 51%. Premium chains fund in-house training academies and elevate wages, but budget operators rely on untrained migrant labor, perpetuating quality gaps. Regulation mandating higher staffing ratios under dementia-care guidelines raises costs, yet without parallel wage subsidies, many facilities postpone compliance, slowing the overall scaling of the Chinese senior living market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Memory-Care Upswing Reshapes Portfolio Mix

Assisted living held a commanding 42.3% of China senior living market share in 2025, reflecting its versatility in meeting daily activity assistance needs. Independent living attracts younger retirees, yet operators now pivot to memory care after national dementia-care rules took effect in December 2024. Memory-care units are projected to post a 10.55% CAGR between 2026 and 2031, outpacing every other property type. Taikang Life and Ping An are rolling out secured floors with sensory-stimulation rooms and certified staff, creating high-margin, differentiated products within the Chinese senior living market.

Adding dementia-ready wings raises capital expense but boosts average revenue per occupied bed. Compliance with the new framework requires minimum nurse-to-resident ratios and family-support programs, barriers that tilt competition toward well-funded chains. Independent-living operators retrofit existing campuses to retain couples aging at different paces, while nursing-care facilities leverage LTCI pilots to bill post-acute rehab sessions, strengthening cross-selling. As more residents transition from independent living to higher-acuity care, integrated campuses gain occupancy resilience, supporting long-term cash flow.

By Business Model: Rental and Long-Lease Options Gain Investor Favor

Long-lease and rental arrangements generated 45.9% of the China senior living market size in 2025 and will expand at a 10.81% CAGR to 2031. The model secures recurring cash and limits refund liabilities that plagued freehold projects during past downturns. Ping An’s premium facilities scheduled for late 2025 will bundle housing, meals, and telehealth without requiring multi-million-yuan deposits, appealing to asset-light younger retirees. Regulators now cap upfront deposits and mandate escrow accounts, pushing operators toward rental formats that better align revenue recognition with service delivery.

Freehold and hybrid schemes still attract affluent households wanting estate-planning flexibility, but stricter oversight has cooled pre-sales. Long-lease contracts, often 10–20 years, provide visibility while allowing operators to re-price units at renewal. Developers in Tier 2 cities trial shorter leases to widen affordability, yet success hinges on secondary-market transfer mechanisms, an area where only top-tier chains possess the legal infrastructure. The rental shift is reshaping underwriting standards for senior-living loans, integrating occupancy sensitivity and wage inflation into lender stress tests across the Chinese senior living market.

By Age: Oldest-Old Drives Demand for High-Acuity Services

Residents aged 65–74 accounted for 39.8% of the China senior living market in 2025, reflecting the first wave of baby-boomer retirees. However, the above-85 cohort is forecast to post an 11.08% CAGR through 2031, catalyzing expansion of skilled-nursing and memory-care beds. This group presents multiple co-morbidities and higher functional dependency, driving up nurse staffing and physician oversight requirements. China Everbright’s 32,000-bed network uses step-down care pathways to keep late-stage residents within the same campus, retaining revenue that would otherwise shift to hospitals.

The 55–64 “young-old” segment favors active-adult amenities and remains marginal to facility-based care. Meanwhile, the 75–85 bracket represents a strategic hinge where independent-living residents transition into assisted care, a pattern operators exploit by offering tiered packages. As longevity increases, end-of-life and palliative services will command a greater share of the wallet, prompting policy debate around hospice reimbursement and advance-care planning within the Chinese senior living market.

Geography Analysis

Shanghai remains the single largest city-level cluster, responsible for more than one-quarter of 2025 revenue and hosting premium campuses with average monthly fees above USD 2,000. However, its tight land pipeline forces operators to expand through vertical redevelopment and brownfield conversions, strategies that favor incumbents with existing parcels. Beijing leverages its role as a policy sandbox; early adoption of smart-eldercare standards and LTCI pilots provides operators clarity on reimbursement streams, supporting stable financing terms.

Shenzhen and Guangzhou benefit from Greater Bay Area initiatives that enable Hong Kong residents to use social-welfare vouchers on the mainland, expanding addressable demand and raising service standards. The corridor also encourages technology diffusion, with wearables and ambient monitoring appearing first in Bay Area facilities before cascading inland. Chengdu’s double-digit growth outlook reflects Sichuan’s push to attract capital with concessional land and tax breaks, capitalizing on a rising middle class in Western China.

Beyond the marquee cities, many Tier 2 and Tier 3 locations face slower adoption due to lower household incomes and entrenched family-care norms. Provincial subsidies for community canteens and home modifications aim to postpone institutional demand, yet they also act as feeders by familiarizing families with professional services. Operators that embed community outreach programs and day-care centers improve brand recognition, smoothing future conversion and enlarging the Chinese senior living market over the long term.

Competitive Landscape

The Chinese senior living market is fragmented, with no operator exceeding a 5% nationwide share, but insurance groups and diversified property developers are widening their lead. Insurance-backed players such as Taikang Life, China Taiping, and New China Life deploy long-dated liabilities to fund integrated campuses, positioning eldercare as both an investment asset and a hedge against longevity risk. Taikang Life alone has committed USD 14 billion to build 26 communities totaling 11,000 units, knitting together housing, rehabilitation, and chronic-disease clinics to lower claim costs and deepen client engagement.

Property developers—China Vanke, Poly Developments, Greentown, Country Garden—entered the sector to diversify away from a slow residential cycle, converting unsold condos into assisted-living units. Yet operational complexity and modest margins have prompted some to switch to asset-light management contracts or joint ventures with healthcare specialists. Vanke’s 2023 partnership with Banyan Tree exemplifies a strategy to import hospitality know-how and wellness branding into senior projects.

Technology alliances are emerging as a competitive wedge. Ping An’s January 2025 acquisition of its healthcare-tech arm for USD 1.7 billion will integrate telehealth, remote monitoring, and family dashboards into five premium campuses, offering a closed-loop ecosystem from home care to institutional services. Early adopters of wearables in Beijing and Shanghai have documented 20% drops in emergency transfers, an outcome that draws higher-paying families and positions facilities for bundled-payment contracts. As regulation tightens staffing ratios and fire-safety rules, under-capitalized independents are likely to exit or consolidate, gradually raising the market concentration of the Chinese senior living market.

China Senior Living Industry Leaders

China Vanke

Sino-Ocean Group

Taikang Life

Poly Developments & Holdings

Cherish-Yearn

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ping An Insurance Group acquired the remaining stake in Ping An Healthcare Technology for USD 1.7 billion, announcing premium campuses in Shanghai and Shenzhen slated for late 2025.

- January 2025: China Everbright reported operating 190 senior-health institutions with 32,000 beds across 50 cities.

- December 2024: China issued comprehensive dementia-care guidelines mandating certified memory-care units and staffing ratios.

- December 2024: Taikang Life opened Phase III of Wu Garden in Suzhou, adding 618 units and introducing “migratory bird” retirement for affluent seniors.

- December 2024: China Everbright reported operating 190 senior-health institutions with 32,000 beds across 50 cities.

China Senior Living Market Report Scope

Senior living is a concept that refers to a variety of housing and lifestyle options for senior citizens that are adapted to the challenges of aging, such as limited mobility and susceptibility to illness. The Chinese senior living market is segmented by city. The report offers market size and forecast in value (USD billion) for all the above segments.

By Property Type

| Assisted Living |

| Independent Living |

| Memory Care |

| Nursing Care |

By Business Model

| Outright Sale (Freehold) |

| Long-Lease / Rental |

| Hybrid (Sale + Lease) |

By Age

| 55 to 64 years |

| 65 to 74 years |

| 75 to 85 years |

| Above 85 years |

By Major Cities

| Beijing |

| Shanghai |

| Shenzhen |

| Guangzhou |

| Chengdu |

| Rest of China |

| By Property Type | Assisted Living |

| Independent Living | |

| Memory Care | |

| Nursing Care | |

| By Business Model | Outright Sale (Freehold) |

| Long-Lease / Rental | |

| Hybrid (Sale + Lease) | |

| By Age | 55 to 64 years |

| 65 to 74 years | |

| 75 to 85 years | |

| Above 85 years | |

| By Major Cities | Beijing |

| Shanghai | |

| Shenzhen | |

| Guangzhou | |

| Chengdu | |

| Rest of China |

Key Questions Answered in the Report

How large is the Chinese senior living market today?

The market was valued at USD 40.44 billion in 2026 and is forecast to reach USD 64.34 billion by 2031, reflecting a 9.73% CAGR.

Which property type dominates current revenue?

Assisted living leads with 42.3% of revenue in 2025, owing to its balance of support services and moderate pricing.

What is driving rapid growth in memory-care units?

National dementia-care rules effective December 2024 require certified memory-care wings, spurring a projected 10.55% CAGR through 2031.

Why are rental and long-lease models expanding quickly?

Escrow rules and deposit caps have reduced freehold appeal, while long-lease and rental contracts provide recurring revenue and lower upfront cost to residents.

Which city is expected to grow fastest?

Chengdu is projected to advance at an 11.21% CAGR (2026–2031), driven by PPP land incentives and rising middle-class demand.

What is the biggest operational constraint for providers?

A shortage of trained caregivers—the sector needs 13 million but had only 1 million in 2024—continues to limit quality scale-up.

Page last updated on: