Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

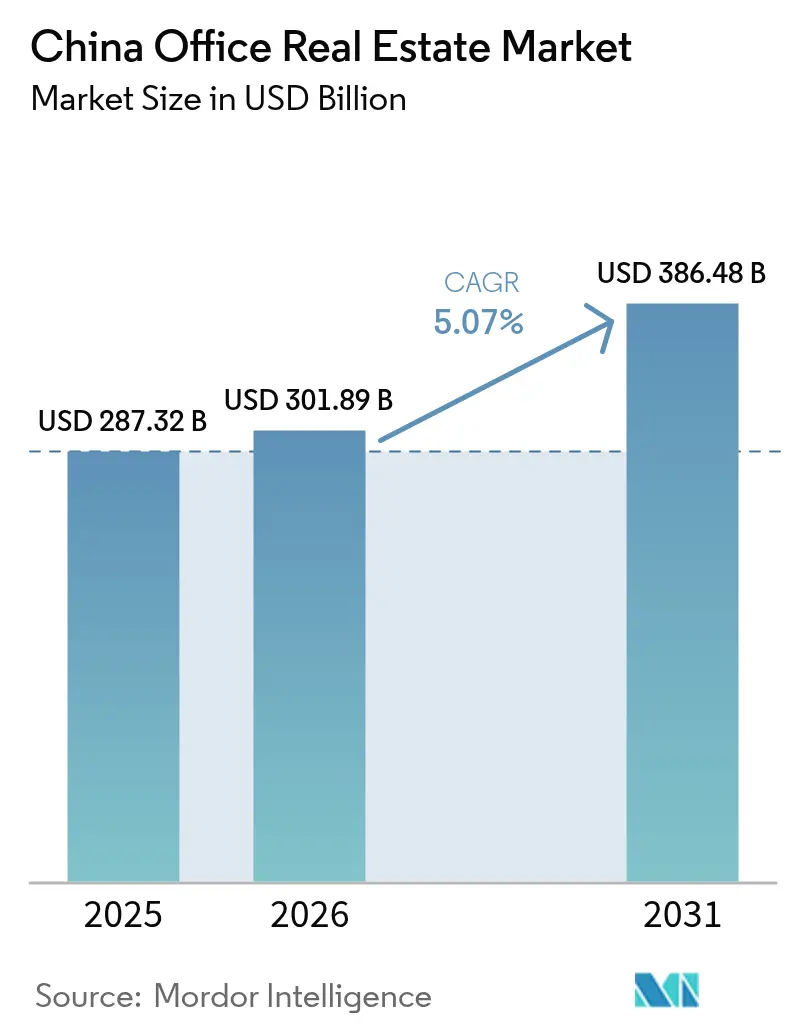

| Base Year Market Size (2025) | USD 287.32 Billion |

| Market Size (2026) | USD 301.89 Billion |

| Market Size (2031) | USD 386.48 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

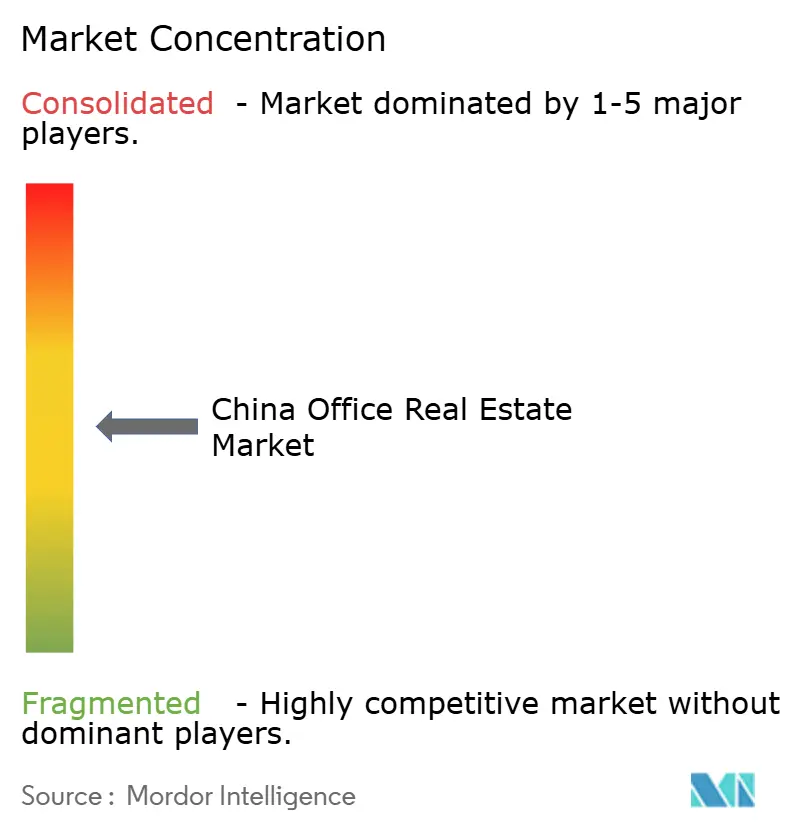

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Office Real Estate Market Analysis by Mordor Intelligence

The China Office Real Estate Market size is expected to grow from USD 287.32 billion in 2025 to USD 301.89 billion in 2026 and is forecast to reach USD 386.48 billion by 2031 at 5.07% CAGR over 2026-2031. The market’s near-term stability draws strength from the government’s partial relaxation of the “three red lines” leverage caps, which have unlocked new balance-sheet capacity for distressed-asset purchases. Liquidity has also broadened through the USD 1.5 trillion housing provident fund, which has outpaced banks in mortgage issuance and signaled official resolve to underpin commercial real-estate confidence. Meanwhile, the China Securities Regulatory Commission’s decision to extend the public REIT framework to consumption-linked infrastructure has created a USD 11.9 billion listed platform that channels equity capital directly into the sector. At the demand level, hybrid work has accelerated a flight to quality: Grade A space now captures 51.2% of occupied stock and is expanding fastest at 5.71%, thanks to firms consolidating team hubs to retain talent. Regional policy, notably the “Chengdu 2025 Manufacturing Plan,” is redirecting supply-chain nodes inland and lifting office absorption in interior cities, with Chengdu posting a 6.31% CAGR as the country’s fastest-growing metro market[1]China Real Estate Association, “2024 Annual Office Property Report,” China Real Estate Association, crea.org.cn.

Key Report Takeaways

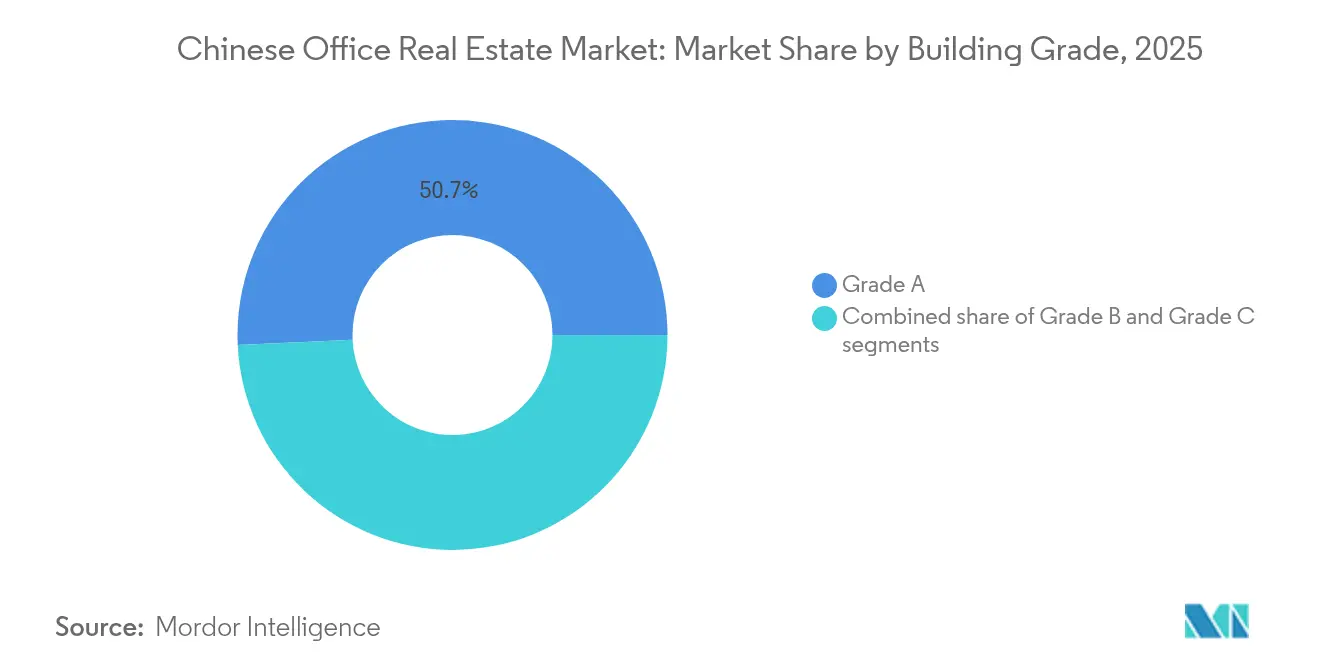

- By building grade, Grade A offices led with 50.74% of China office real estate market share in 2025; Grade A stock is also the fastest-growing segment at a 5.63% CAGR through 2031.

- By transaction type, rentals commanded 70.62% of the China office real estate market size in 2025, while sales transactions are projected to expand at a 5.79% CAGR to 2031.

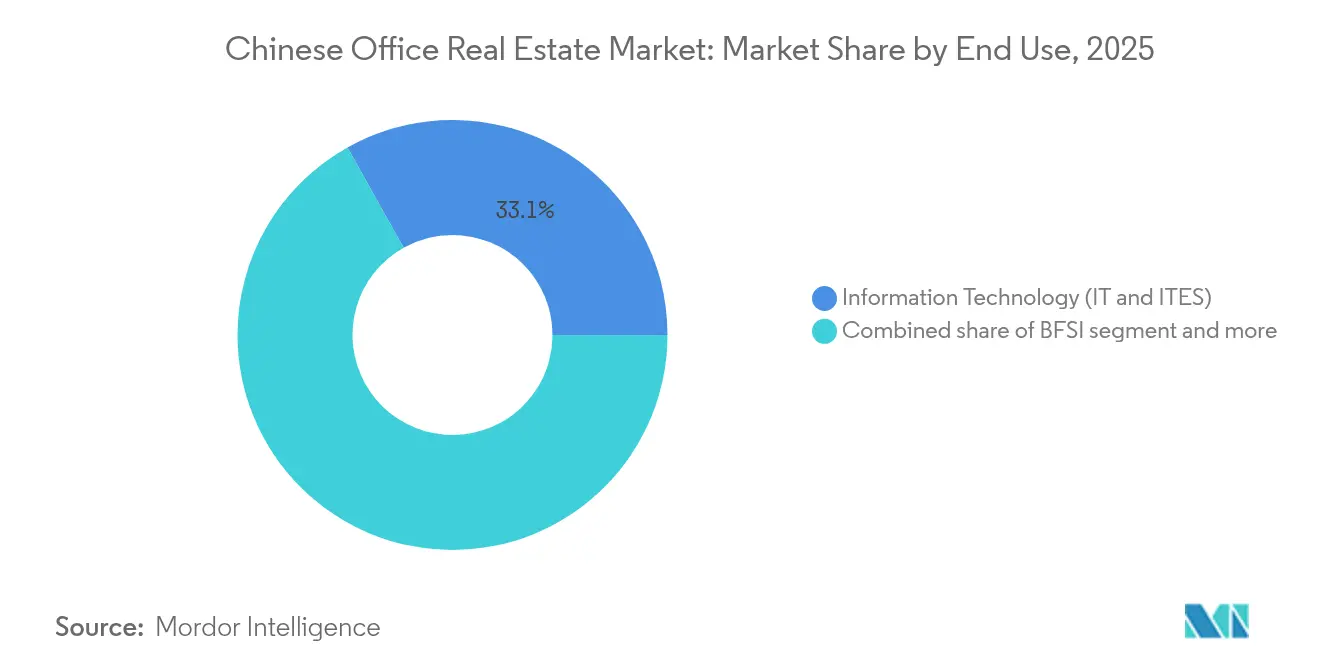

- By end use, the Information Technology segment held 33.12% share of the China office real estate market size in 2025 and is advancing at a 5.96% CAGR through 2031.

- By geography, Shanghai controlled 22.05% of 2025 revenue, whereas Chengdu is forecast to post the quickest 6.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-work–led flight to quality | +1.2% | Core CBDs in Shanghai, Beijing, Shenzhen | Short term (≤ 2 years) |

| Near-shoring of supply chains to interior cities | +0.9% | Chengdu, Chongqing, Wuhan, Xi’an | Long term (≥ 4 years) |

| Government stimulus for REIT expansion | +0.8% | Tier-1 cities nationwide | Medium term (2-4 years) |

| Digital-services uptake from Gen-AI roll-outs | +0.7% | Beijing Zhongguancun, Shanghai Pudong, Shenzhen Nanshan | Medium term (2-4 years) |

| “Greening” mandates for public buildings | +0.5% | Nationwide, stricter in tier-1 | Long term (≥ 4 years) |

| Growth of corporate innovation centres | +0.6% | Beijing, Shanghai, Shenzhen, Hangzhou | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Stimulus for REIT Expansion

The broadening of China’s public REIT regime to encompass shopping malls and department stores has transformed how commercial assets secure long-term capital. Allowing investors to trade securitised stakes in stabilized projects tackles the duration mismatch between short-term bank debt and multi-decade real-estate income streams. The timing dovetails with a measured easing of “three red lines” tests for qualified asset takeovers, yielding a coordinated liquidity backstop that supports asset repricing without undermining financial-stability goals. As domestic investors already account for more than 80% of deal flow, the upgraded REIT channel furnishes them with scalable exit routes while giving developers an alternative to on-balance-sheet borrowing. Tier-1 properties stand to benefit first because they offer the cash-flow visibility demanded by institutional allocators.

Hybrid-Work–Led Flight to Quality Demand

Post-pandemic occupancy surveys show that employees are willing to return only to workspaces that improve well-being and collaboration; employers consequently rationalise footprints yet upgrade locations. This pivot has lifted Grade A effective rents by 2.4% since 2023 even as Grade B/C rates slipped 1.2%. Data from Hong Kong indicates 27% of staff would require minimum 6% pay increases to revert to a five-day office week, prompting companies to invest in amenities rather than compensation updates. In Shanghai, premium towers post an 11.5% vacancy rate, far below the city-wide 22.9% figure, underscoring an expanding premium-vs-secondary rent spread. The resulting bifurcation concentrates capital allocation on trophy assets and intensifies pressure on older stock to redevelop or reposition[2]Qian Wang, “Hybrid Work and Office-Space Consolidation in Post-Covid China,” Journal of Real Estate Research, jrer.org.

Near-Shoring of Supply Chains to Interior Cities

Companies are shifting ancillary operations inland to moderate wage bills and diversify geopolitical exposure. Under the “Chengdu 2025 Manufacturing Plan,” office take-up in Chengdu’s Jiaozi Park Financial & Business District has grown alongside the High-tech Zone’s USD 48.5 billion GDP in 2024. The resulting 6.31% CAGR makes Chengdu the fastest-expanding node in the China office real estate market, helped by integrated transport links, a deep graduate pool, and local incentives that lower entry costs for advanced-manufacturing tenants.

Digital-Services Uptake from Gen-AI Roll-Outs

Enterprise Gen-AI programs are fuelling requirements for secure, power-dense workplaces. Huawei’s USD 1.4 billion R&D hub in Shanghai’s Qingpu district exemplifies demand for campus-style environments embedding redundant power feeds and high-capacity cooling. Foreign enterprises boosted on-shore R&D staff to 716,000 in 2024, doubling spending to CNY 338 billion over the past decade, which directly elevates leasing by IT and ITES occupiers.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oversupply pressure in Tier-2 and Tier-3 cities impacting rental growth | -1.3% | Tier-2 & Tier-3 cities nationwide | Medium term (2-4 years) |

| Economic slowdown and regulatory tightening affecting corporate leasing appetite | -1.1% | National | Short term (≤ 2 years) |

| High vacancy rates in newly developed CBDs delaying absorption | -1.0% | Emerging CBDs in major metros | Medium term (2-4 years) |

| Space rationalization by large occupiers due to hybrid work adoption | -0.8% | National, weighted toward Tier-1 CBDs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent High Vacancy in Grade B/C Stock

Shanghai’s non-CBD vacancy of 12.2% (versus 11.5% in Grade A core) illustrates how tenants siphon out of secondary assets, forcing landlords to grant concessions of up to 50% to hold occupiers. Beijing mirrors this gap, recording a 21% city-wide vacancy rate in 2024 despite stable demand from state-owned enterprises. Supply risks persist, with 953,000 m² of new Shanghai Grade A completions hitting in 2H 2024, more than double 1H deliveries and compounding shadow stock burdens. Until owners recapitalise and reposition dated premises, structurally weaker cash flows will cap rent growth at the broader market level.

Tighter Developer Financing (“Three Red Lines”)

Although rescue exemptions apply to distressed buy-outs, the core thresholds—liabilities/asset ratio below 70%, net gearing under 100%, and cash/short-term debt above 1—still bind the majority of mid-tier developers[3]National Development and Reform Commission, “14th Five-Year Plan for Building Energy Efficiency and Green Buildings,” National Development and Reform Commission, ndrc.gov.cn. Aggregate financing for the top-100 builders fell 26% in 2024 as cautious banks maintained tighter underwriting. The funding squeeze diverts capital toward residential inventory with faster turnover, constraining the speculative pipeline for new offices and limiting future absorption choices for tenants. Well-capitalised institutions may benefit through discounted asset purchases, but overall deal counts shrink and development diversity narrows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Drive Market Bifurcation

Grade A offices held a commanding 50.74% share of the China office real estate market in 2025, far surpassing other tiers. Driven by consolidating occupiers, the segment is forecast to expand at a 5.63% CAGR to 2031, consistently outpacing the broader China office real estate market size. Consolidation enables companies to curtail total square footage while elevating location quality, technology readiness, and ESG credentials. Landlords able to deliver WELL-categorized amenities such as touchless access, enhanced air filtration, and flexible meeting suites are commanding rent premiums of 10%–15% over 2023 pre-lease rates.

Class B assets face prolonged selection pressure, with many towers approaching functional obsolescence. Owners are considering conversions to co-warehousing, life-science incubators, or live-work lofts, yet such projects carry heavy capex. A cohort of investors has begun acquiring Class B/C bundles at discounts exceeding 35% of peak 2018 pricing, betting on urban-renewal benefits. The initiative dovetails with municipal guidance to re-energise dormant footprints, though regulatory permitting for structural retrofits remains a multi-year endeavour.

By Transaction Type: Rentals Underpin Market Stability

Rental agreements accounted for 70.62% of 2025 revenue, anchoring the China office real estate market share as the primary format for corporate occupancy. These contracts offer occupiers risk-mitigated flexibility and allow asset-heavy developers to blend recurring income with capital-event upside. Pure-sale transactions, while smaller, are set to clock the fastest 5.79% CAGR because repricing has drawn in value-oriented domestic groups that missed the previous up-cycle. The accelerated uptake marks a tactical window created by foreign divestments totaling USD 11.2 billion since 2021.

Momentum in the leasing arena is underwritten by state policy that targets a minimum 3% cash yield for professionally managed rental portfolios. Nationwide rent-to-income ratios hover closer to 35% for middle-income households, which caps rent inflation yet secures durable occupancy pipelines for financially disciplined landlords. In parallel, the public REIT platform blends leasehold cash flow with listed-equity liquidity, effectively hybridising the rent-and-sale continuum and deepening market participation.

By End Use: Technology Sector Anchors Digital Transformation

Information Technology and ITES occupiers controlled 33.12% of 2025 demand, the largest slice of China office real estate market size, and are poised to grow at a 5.96% CAGR to 2031. Critical mass stems from Beijing’s S&T‐intensive enterprises and Shenzhen’s hardware ecosystems, each nurturing vertically integrated clusters that prefer high-specification plug-and-play floors. Banking and financial services tenants represent the second-largest category, yet their space usage is flattening as digital channels replace branch-based models.

Life-sciences and energy multinationals add incremental absorption under generous provincial incentive schemes, but retail corporates are net space releasers amid e-commerce disintermediation. The upshot is a widening demand skew in favour of advanced-tech tenants whose budgets allow brownfield customisation. Building owners now embed powered-shell designs capable of 120 W/m² densities, N+1 cooling, and Tier III cloud-connect rooms to future-proof against hardware refresh cycles.

Geography Analysis

Shanghai dominated the 2025 landscape with a 22.05% revenue share, yet its office sector is wrestling with 22.9% vacancies as foreign firms consolidate offshore or relocate to cost-efficient satellite hubs. Effective rents in peripheral submarkets have slipped to USD 41.6 per m² per month, while prime Pudong towers maintain a narrower USD 58.3 rate, illustrating the durability of core Grade A exposure. Shanghai’s policy mix—tax credits for tech exporters and green-retrofit subsidies—seeks to spur absorption, but tenant decision cycles remain elongated.

Beijing, the political nerve centre, logged a 21% vacancy rate in 2024 despite steady state-enterprise commitments. International legal and asset-management brands such as Cleary Gottlieb and BlackRock trimmed central-CBD floorspace, sending Grade A rents down 7.3% year on year to USD 41.3 per m² per month. Local authorities are now pairing tax rebates with three-year rent holidays for AI-startup tenants in Zhongguancun to stabilise net absorption.

Chengdu stands out with a forecast 6.21% CAGR through 2031, catalysed by its manufacturing pivot and Section B Western Financial Innovation Pilot Zone that promotes cross-border RMB settlement. Multinationals such as Intel and Siemens have recently leased 13,000 m² and 9,000 m² respectively in Tianfu New Area, citing lower labour costs and proximity to component suppliers. Land release quotas remain constrained, underpinning landlord pricing power despite rising completions.

Competitive Landscape

The China office real estate market is moderately concentrated. Foreign funds recorded their fourth consecutive year of net selling in 2024, unloading USD 11.2 billion worth of towers since 2021 and retreating from speculative ground-up ventures. Domestic insurers, securities firms, and local government financing vehicles filled the gap, capturing more than 80% of deal volume, up from 60% five years ago. The shift reflects both global risk-aversion and Beijing’s continuing encouragement for “national team” entities to acquire strategic assets at cyclically advantageous valuations.

Strategically, large-cap developers are trimming non-core holdings to raise liquidity for deleveraging. Shanghai Lujiazui Finance & Trade Zone Development Co. placed 20 buildings valued at USD 4.1 billion on the market, while BlackRock accepted a 30% haircut on a pair of Shanghai towers bought in 2018 to expedite exit. The re-pricing wave is resetting yields closer to 6.2% for Grade A core CBD assets compared with sub-5% peaks in 2019, presenting a total-return upswing for patient capital.

Technology adoption has emerged as a decisive differentiator. CapitaLand Integrated Commercial Trust and Yuexiu REIT each upgraded portfolio towers with smart-metering, digital twin modelling, and app-based wellness services to capture relocation demand from TMT occupiers. Conversely, smaller cash-constrained landlords have struggled to finance retrofits, creating a widening gulf in occupancy performance and investor attention.

China Office Real Estate Industry Leaders

WANDA Group

Country Garden Property Development Co., Ltd

Vanke Co., Ltd.

Sunac China Holdings Limited

Poly Developments & Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Colliers logged a seventh straight quarter of positive net take-up in the capital’s Grade-A sector, with over 70 % of new leases signed by TMT occupiers; one new tower reached completion in the Olympic Park sub-market during Q1.

- June 2025: A Goldman Sachs–PAG–Gaw Capital consortium entered final negotiations to sell the 50,000 m² Ciro’s Plaza complex on West Nanjing Road at roughly 37 % below its 2015 valuation, extending the year’s string of discounted trophy-tower trades.

- May 2025: Co-working operators signed more than 10,000 m² of new leases in emerging Shanghai sub-markets, taking advantage of landlords’ rent concessions to backfill large floor plates left by multinational consolidations.

- April 2025: Knight Frank reported four new Grade-A completions totaling 219,000 m² in Q1, pushing the city’s vacancy to 22.2 %. Financial, TMT and professional-services tenants absorbed only 5,000 m², highlighting leasing pressure despite fresh stock.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China office real estate market as the total annual value derived from leasing and outright sale of purpose-built Grade A, Grade B, and Grade C office buildings across Tier 1, emerging Tier 2, and select Tier 3 cities. Revenues from modern business parks and refurbished legacy stock are included once the asset is officially re-commissioned for corporate occupancy.

Scope Exclusion: Owner-occupied headquarters expansions, mixed-use projects where office floors contribute less than sixty percent of gross leasable area, and short-term coworking sub-leases are outside the study.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifescience, Energy, Legal)

- By Major Cities

- Beijing

- Shanghai

- Shenzhen

- Guangzhou

- Chengdu

- Rest of China

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed building owners, regional leasing managers, asset managers of C-REITs, and tenant-side real estate heads in Beijing, Shanghai, Shenzhen, Chengdu, and Guangzhou. These conversations tested rental benchmarks, pre-lease ratios, and service sector hiring plans, giving us confidence to fine-tune model assumptions and align them with on-ground realities.

Desk Research

We began by mining authoritative public datasets such as the National Bureau of Statistics' floor-space completions, Ministry of Housing and Urban-Rural Development bulletins on new supply, and customs data on steel and cement consumption that signal construction intensity. Trade associations, including the China Real Estate Association, Shanghai Land Exchange, and Asia Pacific Real Estate Association, add annual vacancy surveys and REIT inflow updates. Financial disclosures in listed developer 10-Ks, municipal planning documents, and credible business media further clarify pipeline timing and transaction sentiment. Where depth is required, analysts tap paid resources like D&B Hoovers for developer financials and Dow Jones Factiva for deal flow. This list is illustrative; many other sources support data gathering and cross-checks.

Second-hand material alone rarely answers price-per-square-meter or absorption nuances city by city, so desk findings act as a factual springboard that our team later validates through direct outreach.

Market-Sizing and Forecasting

A transparent top-down reconstruction starts with gross stock and average effective rents by city, producing a notional revenue pool that we validate through selective bottom-up checks, including developer roll-ups and sampled grade-specific price-times-area calculations. Key variables feeding the model include new Grade A completions, prime CBD rent index, nationwide service sector GDP, vacancy rates, REIT capital raised, and foreign direct investment into commercial property. Multivariate regression, complemented by ARIMA for short-term shocks, projects each driver before results cascade into the five-year forecast. Gaps in bottom-up inputs, for instance, undisclosed private transactions, are bridged using proxy metrics such as construction permits and fit-out contract values confirmed during expert calls.

Data Validation and Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst scrutiny, and senior sign-off. If macro releases or policy shifts materially alter any driver, we re-contact key respondents and refresh the file. Reports update annually, with mid-cycle revisions when market-moving events occur, ensuring clients always receive our latest view.

Why Mordor's Chinese Office Real Estate Baseline Commands Reliability

Published figures often diverge because firms adopt different asset scopes, rental conversion factors, and update cadences. We acknowledge these inevitable gaps and clarify how our disciplined scope selection and cross-source validation deliver a decision-ready baseline.

Key gap drivers include some publishers restricting analysis to prime CBD towers only, others bundling undeveloped land sales or entire mixed-use complexes, and several relying on static rent surveys that miss quarterly concessions. Mordor models adjust for all three factors and refresh variables every twelve months, thereby balancing optimism and caution.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 287.32 bn (2025) | Mordor Intelligence | - |

| USD 156 bn (2024) | Regional Consultancy A | Focuses solely on Grade A CBD stock and omits strata-title sales |

| >USD 2,000 bn (2025) | Trade Journal B | Aggregates land auctions and uncompleted pipeline, inflating base estimate |

In sum, while alternative numbers serve niche needs, Mordor's balanced treatment of asset classes, refreshed rents, and dual-path validation offers the most reproducible and transparent baseline for strategy teams and investors.

Key Questions Answered in the Report

What is the current value of the China office real estate market?

The market is valued at USD 301.89 billion in 2026 and is projected to reach USD 386.48 billion by 2031.

Why are Grade A offices outperforming other segments?

Hybrid work encourages firms to consolidate into high-spec locations with better amenities and ESG credentials, pushing Grade A to a 5.63% CAGR.

Which city is the fastest-growing office market in China?

Chengdu leads with a forecast 6.21% CAGR, helped by manufacturing near-shoring and innovation policies.

How does the public REIT program affect office investment?

The expanded REIT framework channels equity capital into stabilized office projects, offering owners alternative exits and investors liquid exposure.

What impact do green-building mandates have on vacancy?

Certified buildings command rent premiums and lower vacancy, while non-compliant stock faces obsolescence and higher leasing risk.

Who are the dominant buyers in China’s office market today?

Domestic institutions now account for more than 80% of transactions, filling the gap left by four straight years of foreign net selling.

Page last updated on: