China Refurbished Smartphone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

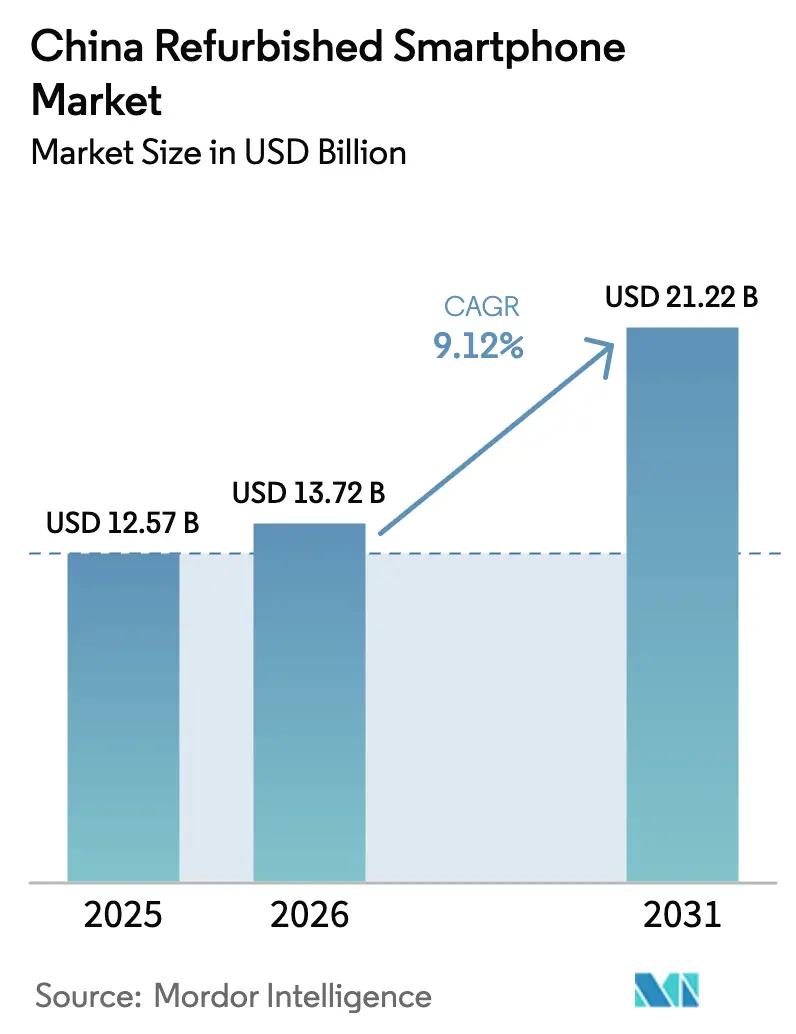

| Base Year Market Size (2025) | USD 12.57 Billion |

| Market Size (2026) | USD 13.72 Billion |

| Market Size (2031) | USD 21.22 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

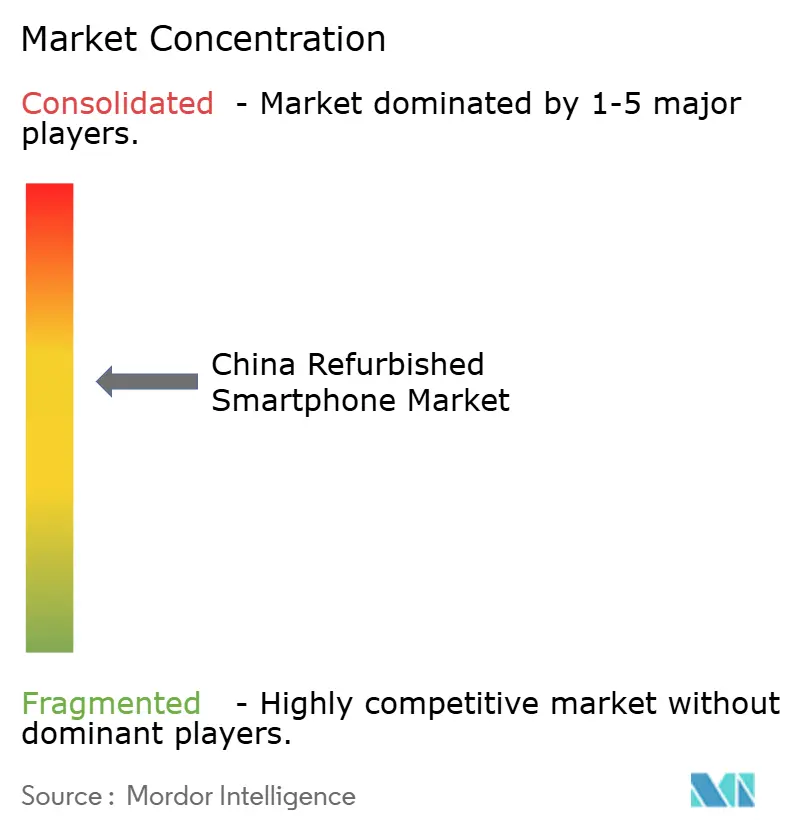

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Refurbished Smartphone Market Analysis by Mordor Intelligence

The China Refurbished Smartphone Market size is expected to grow from USD 12.57 billion in 2025 to USD 13.72 billion in 2026 and is forecast to reach USD 21.22 billion by 2031 at 9.12% CAGR over 2026-2031. Growing consumer acceptance of certified pre-owned devices, strengthened government support for circular-economy initiatives, and rapid improvements in device authentication technology are converging to unlock sustained value creation. Price gaps of 30–50% compared to new flagships, coupled with shorter 5G-driven upgrade cycles, are expanding the supply pool and encouraging repeat trade-in behavior. Online marketplaces dominate distribution by pairing escrow services with blockchain-backed inspection records that improve trust, particularly in tier-3 and tier-4 cities. Standardization pilots launched by the Ministry of Commerce are aligning grading criteria and logistics practices, further lowering market frictions. Meanwhile, OEM-sponsored certified programs ensure consistent refurbishment quality and help reclaim residual value that would otherwise leak to informal channels.

Key Report Takeaways

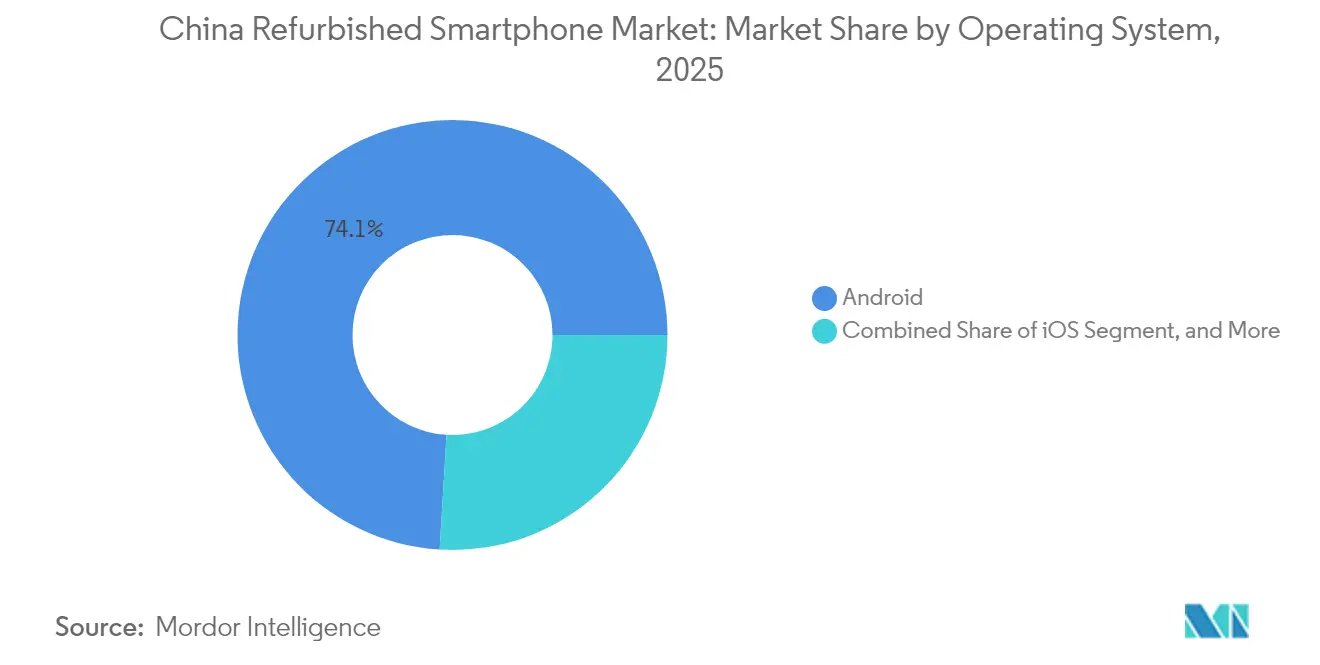

- By operating system, Android led with 74.05% revenue share of the China refurbished smartphone market in 2025, while iOS posted the highest projected CAGR of 11.25% through 2031.

- By price band, the CNY 1,000–1,999 segment commanded a 43.25% share of the China refurbished smartphone market size in 2025, whereas the CNY 2,000–2,999 tier is forecast to expand at a 11.35% CAGR through 2031.

- By sales channel, online marketplaces held 67.85% of the Chinese refurbished smartphone market share in 2025; offline outlets are expected to advance at a 8.85% CAGR through 2031.

- By network technology, 4G LTE accounted for a 59.95% share of the China refurbished smartphone market size in 2025; however, 5G devices are growing fastest at an 11.05% CAGR through 2031.

- By end user, consumer (B2C) activity represented 82.95% share of the China refurbished smartphone market in 2025, whereas enterprise (B2B) transactions are projected to rise at a 10.1% CAGR through 2031.

- By region, East China dominated the China refurbished smartphone market with a 35.95% share in 2025, while Southwest China is expected to record the strongest regional CAGR of 11.4% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Refurbished Smartphone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing e-commerce penetration and trust-building escrow services | +2.1% | Global, with strongest gains in tier-3 and tier-4 cities | Medium term (2-4 years) |

| Competitive pricing gap versus new smartphones | +1.8% | National, with early gains in East China, Southwest China | Short term (≤ 2 years) |

| Government e-waste and circular-economy policies | +1.5% | National, spill-over to cross-border trade | Long term (≥ 4 years) |

| OEM-backed certified pre-owned programs | +1.3% | Global, concentrated in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Shortened upgrade cycles created by 5G rollout | +1.2% | National, accelerated in urban centers | Short term (≤ 2 years) |

| Rising adoption in tier-3 and tier-4 cities | +0.9% | Southwest China, Central China regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing E-commerce Penetration and Trust-Building Escrow Services

Digital payments and blockchain authentication have raised consumer confidence by enabling real-time verification of device condition and ownership. Xianyu’s “鱼力值” credit system evaluates user reliability and integrates dispute-resolution voting panels that settle claims within 24 hours.[1]Tencent News, “新经济观察丨如何构建二手商品交易的信用机制,” news.qq.com Third-party labs upload video audits to immutable ledgers, giving buyers transparent access to inspection results. These measures are most impactful in smaller inland cities, where formal retail options remain scarce, thereby broadening the China refurbished smartphone market footprint beyond coastal metropolitan areas.

Competitive Pricing Gap Versus New Smartphones

Premium devices depreciate rapidly, creating a compelling value proposition in the secondary channel. An iPhone 13 traded at roughly CNY 1,720 on leading platforms in mid-2025, a level 45% below its 2024 launch price yet still supported by five years of iOS updates.[2]Tencent News, “新经济观察丨如何构建二手商品交易的信用机制,” news.qq.com As consumers become accustomed to better cameras and higher refresh-rate screens, older flagships meet performance expectations at a fraction of the cost of new devices, reinforcing steady demand across the Chinese refurbished smartphone market.

Government E-waste and Circular-Economy Policies

The Ministry of Commerce designated pilot cities in April 2025 to standardize reverse logistics workflows, data wipe protocols, and warranty formats, thereby providing legal clarity for both merchants and buyers.[3]CCTV, “‘国家队’入场,废旧手机回收市场如何突围,” cctv.com Parallel efforts by China Resources Recycling Group introduced “national team” recycling depots with tamper-proof labeling and blockchain-issued destruction certificates for irreparable units. These initiatives expand formal supply, reduce informal scrap leakage, and integrate sustainability metrics into local regulatory scorecards, thereby bolstering long-term growth prospects.

OEM-backed Certified Pre-owned Programs

Manufacturers such as Huawei and Apple now refurbish in-house, issuing new-device-length warranties on inspected units. ATRenew’s warehouse-to-retail model shortens logistics by an average of three days and offers same-day pickup for bulk enterprise orders. Direct involvement by OEMs enhances grading consistency, reduces counterfeit risk, and supports price discovery, all of which contribute to increased trust across the Chinese refurbished smartphone market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and grey-market devices harming brand trust | -1.4% | National, concentrated in online C2C platforms | Short term (≤ 2 years) |

| Lack of unified quality-grading standards | -1.1% | National, affecting cross-platform compatibility | Medium term (2-4 years) |

| Higher refurbishment costs due to China PIPL data-wipe rules | -0.8% | National, compliance-driven cost increases | Long term (≥ 4 years) |

| Competition from ultra-low-cost new devices narrowing price gap | -0.7% | National, intensified in budget segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Grey-Market Devices Harming Brand Trust

Instances of misgraded stock and significant discrepancies between online quotes and final payouts have eroded consumer confidence, particularly on peer-to-peer forums. A March 2025 spike in complaints against JD.com’s trade-in partner Aihuishou prompted regulators to call for auditable quality reports and mandatory price-adjustment explanations. Until enforcement tightens, skeptical buyers may defer purchases or pay a premium for certified channels, which will weigh on the trajectory of the China refurbished smartphone market.

Lack of Unified Quality-Grading Standards

Each platform employs its own descriptors, such as “99 new,” “A-grade,” or “lightly used,” which often differ in terms of allowable bezel scuffs or battery wear. Industry experts advocate for a national five-tier scale supported by video evidence and smart-contract escrow to reduce disputes and enable cross-platform listings. Consistency would improve liquidity and encourage institutional buyers to commit larger volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: iOS Gains Ground Through Premium Accessibility

Android accounted for 74.05% of 2025 revenue, underpinned by an abundance of high-spec domestic devices and HarmonyOS integration, which sustains resale value. Huawei alone supplied more than 18% of refurbished Android inventory in Q2 2025. The segment benefits from wide carrier compatibility and delayed eSIM uptake, which simplifies activation. Conversely, iOS posted an 11.25% forecast CAGR as budget shoppers tap second-hand iPhone 13 units priced close to CNY 1,700. That momentum positions Apple to capture incremental share within the China refurbished smartphone market, even as HarmonyOS explores cross-device synergies that may extend Android's asset life.

The China refurbished smartphone market size for iOS devices is projected to reach USD 7.62 billion by 2031, equivalent to more than one-third of the total segment value. Android remains dominant, yet incremental iOS uptake demonstrates how value-pricing can democratize premium ecosystems.

By Price Band: Mid-tier Segments Drive Volume Growth

The CNY 1,000–1,999 tier accounted for 43.25% of 2025 sales, reflecting an ample supply of year-old flagships and strong consumer confidence in the certified pre-owned status. Trade-in subsidies and rapid innovation cycles funnel nearly new devices into this band every quarter, reinforcing its scale. Meanwhile, the CNY 2,000–2,999 range is forecast to grow at an annual rate of 11.35% as shoppers stretch their budgets for 5G connectivity and larger storage. This tier captures Xiaomi Ultra and Samsung S22 series units that depreciate faster than ultra-premium counterparts but still deliver four more years of software support.

The China refurbished smartphone market share for the CNY 2,000–2,999 tier is expected to rise to 28.60% by 2031, up from 22.15% in 2025. The demand below CNY 1,000 is moderating as new devices close the feature gap, indicating a gradual shift toward mid-priced refurbished options.

By Sales Channel: Online Platforms Dominate Through Innovation

Online marketplaces processed 67.85% of the 2025 transaction value, primarily driven by verification services and zero-interest escrow, which releases funds only after seven-day acceptance windows. Xianyu alone logged a 191.4% YoY surge in phone GMV in 2023 as rural users entered the circular economy. B2C leaders, such as Zhuanzhuan, offer professional inspection and 180-day warranties to reduce uncertainty. Offline stores, which represent 32.15% of sales, remain relevant in major electronics clusters. ATRenew’s Shenzhen flagship showcases 10,000 devices and offers on-site diagnostics that mimic the speed of online purchasing.

Despite digital dominance, hybrid models are gaining traction. The China refurbished smartphone market size handled through warehouse-to-retail hubs could exceed USD 9.46 billion by 2031, reflecting buyer demand for touch-and-feel validation before purchase.

By Network Technology: 5G Transition Accelerates Market Dynamics

4G LTE devices held a 59.95% share in 2025, owing to a vast installed base and lower price points. Nevertheless, 5G units are expected to outpace overall market growth at an 11.05% CAGR, supported by China’s 810 million active 5G connections in 2023 and a projected 1.6 billion by 2030.

Early adopters swapping first-generation 5G models create a steady supply, while expanding mid-band coverage motivates mainstream buyers to leapfrog directly to refurbished 5G. That dynamic compresses 3G and below into a residual niche as carriers sunset legacy networks.

By End User: Consumer Market Drives Adoption

Consumers generated 82.95% of 2025 spending, propelled by students embracing refurbished premium brands and professionals maximizing value in high-spec handsets. Seniors are an emerging cohort as simplified UI overlays reduce learning barriers.

Enterprises, although smaller, are expected to grow at a rate of 10.1% annually, as sustainability targets require measurable reductions in e-waste. ATRenew’s B2B portal serves 850,000 SMEs nationwide with bulk discounting and same-day data-wipe certification, signaling latent demand for controlled-cost fleet devices.

Geography Analysis

East China led with a 35.95% share in 2025, leveraging Shanghai’s international logistics corridors and Zhejiang’s manufacturing depth. Regional operators integrate return flows from factory reject lines, ensuring a predictable, high-grade supply that feeds local refurbishment hubs. North China, anchored by Beijing, maintains high ASPs due to upper-income demographics and early 5G awareness.

Southwest China is projected to grow at an annual rate of 11.4% through 2031. Rising disposable income in Chongqing and Sichuan, combined with the rapid adoption of mobile payments, encourages first-time smartphone owners to opt for affordable refurbished 5G units. Government e-commerce subsidies and improved express delivery networks are erasing the geographic premium that once favored coastal cities.

The South Central, Northwest, and Northeast regions exhibit mid-single-digit growth, linked to varied infrastructure readiness and consumer preferences. Yet, standardized online grading is flattening regional price disparities, positioning the Chinese refurbished smartphone market to evolve into a truly national ecosystem.

Competitive Landscape

The competitive field is moderately concentrated. ATRenew, Xianyu, and JD-affiliated Aihuishou together commanded roughly 43% of 2024 GMV. ATRenew differentiates itself via proprietary AI grading modules and a warehouse-to-retail model that reduces the average turnover time by three days. Xianyu leverages Alibaba identity data to underwrite escrow safety and nurture community moderation. JD.com integrates trade-in bonuses with new-device sales, locking users into its ecosystem.

Government-backed China Resources Recycling Group recently entered with blockchain certification and post-office partnerships, indicating a potential path toward sector consolidation and stricter compliance. Smaller specialists, such as SuiHuishou and Huishoubao, carve out niches through rapid urban pickup and real-time video audits, respectively. Competitive intensity now hinges less on traffic acquisition and more on data security compliance under PIPL rules and ISO 14001 certification, driving investment in secure-erase technology and AI-based anomaly detection.

China Refurbished Smartphone Industry Leaders

ATRenew Inc.

Alibaba Group Holding Limited

JD.com Inc.

Suning.com Co. Ltd.

Xiaomi Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Analysts profiled five leading recycling platforms, highlighting SuiHuishou’s 30-minute pickup guarantee and Zhuanzhuan’s C2B2C model, which processes over CNY 1 billion in daily transactions.

- April 2025: China Resources Recycling Group launched blockchain-validated recycling depots in provincial capitals, marking “national team” participation in formalized refurbished electronics.

- March 2025: ATRenew opened the Paijitang flagship in Shenzhen’s Huaqiangbei district, displaying 10,000 inspected devices and serving 850,000 SMEs nationwide.

- March 2025: JD.com and Aihuishou faced regulatory scrutiny after consumer complaints highlighted opaque grading and price discounting on trade-in programs.

- February 2025: Industry forums reported repeated instances of large gaps between online quotes and final payouts, fueling calls for auditable inspection videos.

- January 2025: China’s Ministry of Commerce initiated a three-year pilot program in select cities to standardize logistics, data wiping, and warranty formats for second-hand smartphones.

China Refurbished Smartphone Market Report Scope

The refurbished phone is a pre-owned handset sent back due to a fault and repaired for resale. Refurbished smartphones are a cost-effective solution for customers looking to save money when purchasing a smartphone.

| Android |

| iOS |

| HarmonyOS |

| Others |

| Below CNY 1,000 |

| CNY 1,000–1,999 |

| CNY 2,000–2,999 |

| CNY 3,000–3,999 |

| CNY 4,000 and Above |

| Online Marketplace | C2C Platforms |

| B2C Platforms | |

| Carrier Online Stores | |

| Offline | Brand Stores |

| Carrier Stores | |

| Independent Retailers |

| 5G |

| 4G LTE |

| 3G and Below |

| Consumer (B2C) | Student Segment |

| Working Professionals | |

| Seniors | |

| Enterprise (B2B) | Small and Medium Enterprises |

| Large Enterprises |

| By Operating System | Android | |

| iOS | ||

| HarmonyOS | ||

| Others | ||

| By Price Band | Below CNY 1,000 | |

| CNY 1,000–1,999 | ||

| CNY 2,000–2,999 | ||

| CNY 3,000–3,999 | ||

| CNY 4,000 and Above | ||

| By Sales Channel | Online Marketplace | C2C Platforms |

| B2C Platforms | ||

| Carrier Online Stores | ||

| Offline | Brand Stores | |

| Carrier Stores | ||

| Independent Retailers | ||

| By Network Technology | 5G | |

| 4G LTE | ||

| 3G and Below | ||

| By End User | Consumer (B2C) | Student Segment |

| Working Professionals | ||

| Seniors | ||

| Enterprise (B2B) | Small and Medium Enterprises | |

| Large Enterprises | ||

Key Questions Answered in the Report

How large is the China refurbished smartphone market in 2026?

The market generated USD 13.72 billion in revenue in 2026 and is forecast to grow steadily through 2031.

What is the expected CAGR for refurbished smartphones in China?

The China refurbished smartphone market is projected to expand at a 9.12% CAGR between 2026 and 2031.

Which price band dominates refurbished smartphone sales in China?

Devices priced between CNY 1,000 and CNY 1,999 represented 43.25% of 2025 sales, making it the leading tier.

Why are online channels so important for second-hand smartphones?

Online marketplaces account for 67.85% of 2025 value because escrow payments, blockchain inspection records, and wide reach lower trust barriers.

Which region is growing fastest for refurbished smartphones in China?

Southwest China is set to register the quickest pace, with an 11.4% forecast CAGR through 2031 as tier-3 and tier-4 cities adopt certified pre-owned devices.

How are government policies shaping the refurbished smartphone ecosystem?

Pilot programs for standardizing grading and data wiping, along with national recycling depots, are formalizing supply chains and boosting consumer confidence.

Page last updated on: