Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

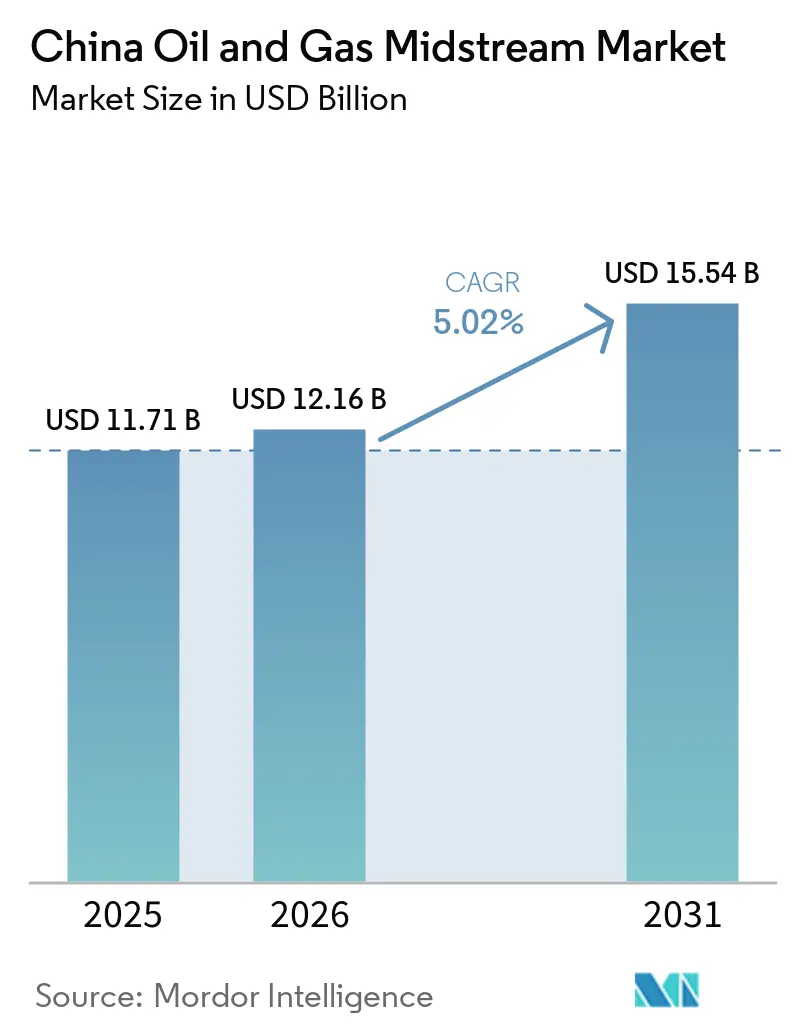

| Base Year Market Size (2025) | USD 11.71 Billion |

| Market Size (2026) | USD 12.16 Billion |

| Market Size (2031) | USD 15.54 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

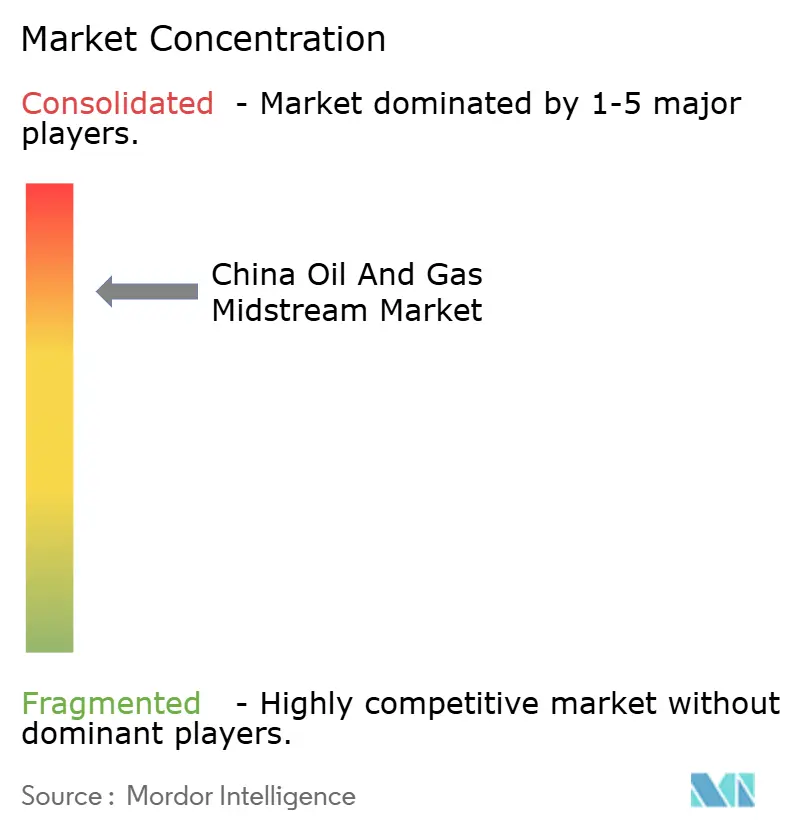

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Oil And Gas Midstream Market Analysis by Mordor Intelligence

The China Oil And Gas Midstream Market size is expected to grow from USD 11.71 billion in 2025 to USD 12.16 billion in 2026 and is forecast to reach USD 15.54 billion by 2031 at 5.02% CAGR over 2026-2031.

A cost-plus tariff regime in long-distance transmission coexists with third-party access at ten LNG terminals, letting municipal distributors and large industrial buyers bypass national oil companies. Investment priorities illustrate this structural pivot. Competitive intensity splits along asset class. PipeChina controls roughly 90,000 kilometers of trunk lines under regulated tariffs that leave little room for rivalry. By contrast, more than 500 city-gas franchises compete on connection fees and digital metering, while LNG terminals face under-utilization after eight new projects came onstream in 2025. An environmental approval cycle of 18-24 months, volatile steel prices, and coastal water scarcity remain headline risks that together hinder the growth over the forecast horizon.[1]National Energy Administration, “Gas Storage Mandate 2030,” NEA.GOV.CN

Key Report Takeaways

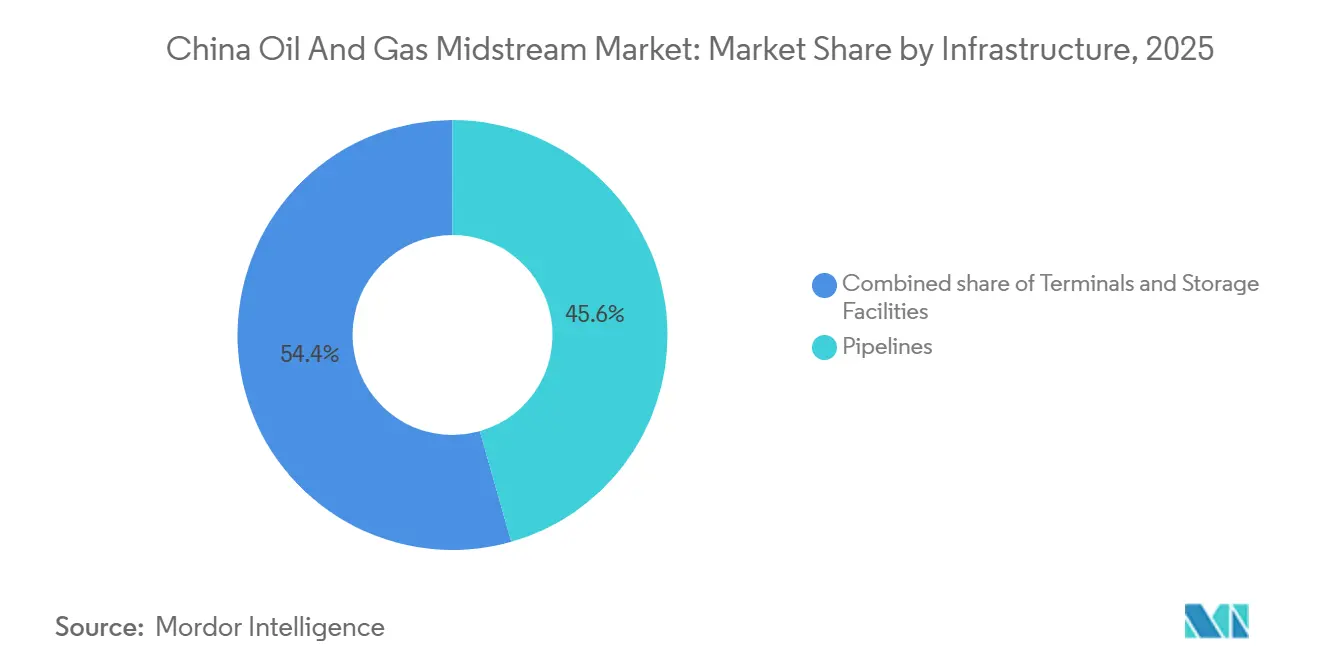

- By infrastructure, pipelines accounted for 45.6% of 2025 value, whereas terminals are expected to grow 8.6% CAGR to 2031.

- By product type, LNG throughput is projected to rise at 9.1% CAGR between 2026 and 2031, outpacing natural gas that held 33.2% share in 2025.

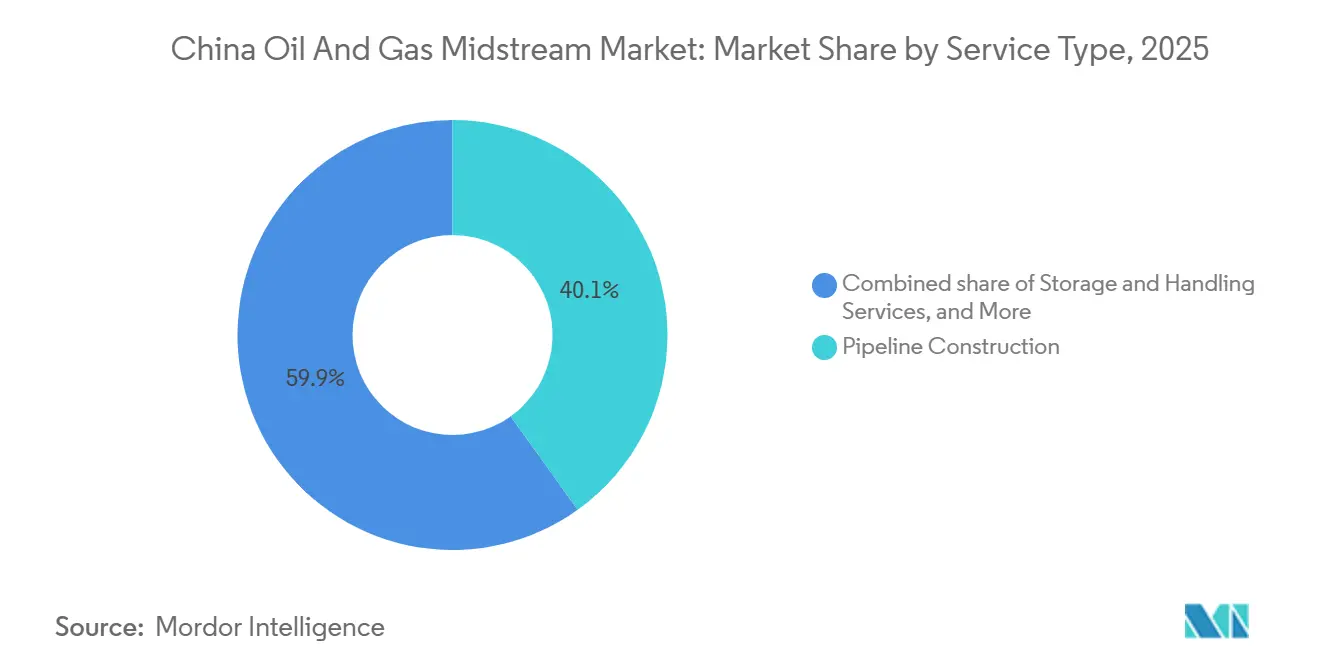

- By service, pipeline construction held 40.1% of the China oil and gas midstream market share in 2025, while storage and handling are expected to grow at an 8.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Oil And Gas Midstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of national gas-pipeline mileage | 1.20% | Western provinces, Beijing-Tianjin-Hebei | Medium term (2-4 years) |

| Accelerated build-out of LNG regasification terminals | 1.50% | Guangdong, Zhejiang, Jiangsu, Fujian, Liaoning | Short term (≤ 2 years) |

| Coal-to-gas switching mandates in industrial & residential sectors | 0.80% | Hebei, Shanxi, Shandong, Yangtze Delta | Long term (≥ 4 years) |

| AI-driven pipeline-health analytics adoption | 0.40% | National trunk lines | Medium term (2-4 years) |

| Boom in LNG-fueled heavy-duty trucking | 0.70% | National logistics corridors | Short term (≤ 2 years) |

| Strategic gas-storage capacity mandates | 0.90% | North China Plain, Yangtze Delta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Build-Out of LNG Regasification Terminals

China commissioned eight LNG terminals and expanded three facilities in 2025, lifting national nameplate capacity to 190 million tonnes per annum, with a 245 million-tonne target for 2030. CNOOC’s Yancheng terminal added 3 million tpa, yet LNG imports fell 9% in the same year, forcing operators to discount tolls. Ten open-access terminals now let city distributors bid directly for cargo slots, exposing end-users to global spot swings and complicating greenfield finance.

Coal-to-Gas Switching Mandates in Industrial & Residential Sectors

Clean-heating pilots in Hebei and Shanxi improved winter air quality, prompting targeted fuel-switching in urban clusters. Stricter emissions caps on cement and chemical producers sustain industrial gas demand, but rural residential conversions slow because subsidized connections of CNY 3,000–5,000 remain prohibitive for lower-income households.[2]National Bureau of Statistics, "Household Energy Survey 2024," stats.gov.cn Concentrating projects in dense corridors raises utilization rates yet leaves hinterlands underserved, compelling distributors to secure industrial anchor loads.

AI-Driven Pipeline-Health Analytics Adoption

PipeChina deployed a large-language model trained on 30 years of data that locates corrosion hot-spots and schedules maintenance.[3]PipeChina, “Technology Report 2024,” PIPECHINA.COM.CN Changqing oilfield cut unplanned downtime 18% with predictive analytics, highlighting capital-efficiency gains. Smaller municipal franchises lag in data infrastructure, widening performance gaps, and reinforcing national oil company advantages.

Boom in LNG-Fueled Heavy-Duty Trucking

LNG truck sales reached 178,000 units in 2024, lifting market penetration to 29.6% as LNG retained a CNY 1.50 per-liter-equivalent cost edge over diesel. Over 5,000 refueling stations serve Beijing-Shanghai and Guangzhou-Chengdu corridors, stimulating satellite liquefaction and mobile bunkering networks.[4]CAAM, “LNG Truck Sales Report 2024,” CAAM.ORG.CN

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy environmental & land-use permitting process | -0.60% | Cross-provincial routes, Western ecologic zones | Long term (≥ 4 years) |

| Capex escalation amid commodity-price volatility | -0.50% | Steel-intensive pipelines, coastal terminals | Medium term (2-4 years) |

| Shipping chokepoints inflating landed LNG costs | -0.40% | Guangdong, Zhejiang, Fujian | Short term (≤ 2 years) |

| Coastal water-stress limits on new LNG terminals | -0.30% | Guangdong, Zhejiang, Jiangsu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Environmental & Land-Use Permitting Process

Cross-provincial pipelines need 18-24 months for environmental clearance. Western alignments that cross protected zones often exceed 30 months, shrinking project revenue windows and deterring private capital.

Capex Escalation Amid Commodity-Price Volatility

Per-kilometer pipeline costs surpassed CNY 6 million in 2024 as steel rallied, while recent LNG terminals ranged from USD 500 million to USD 2.7 billion. Regulators now scrutinize procurement premiums, leaving developers to absorb overruns that erode regulated returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Terminals Outpace Pipelines on Import Dependency

Terminals will expand at an 8.6% CAGR to 2031 while pipelines mature. Underground storage commands strategic attention because the China oil and gas midstream market size for reserves is tied to a 90-day inventory rule. Yet suitable salt caverns cluster in Jiangsu and Liaoning, leaving Guangdong to rely on higher-cost above-ground tanks. Under-utilized terminal capacity, usage fell as imports dropped 9% in 2025, which may prompt smaller owners to pool assets or sign tolling deals.

By Product Type: LNG Surges as Trucking and Peaking Demand Reshape Flows

LNG throughput will rise 9.1% a year, carving share from pipeline gas during winter peaks. Heavy-duty trucking and spot-driven utility purchases underpin the China oil and gas midstream market share held by LNG segments in 2025, and elevated volatility sustains demand for flexible cargoes. Crude pipelines plateau as refining capacity nears its ceiling, redirecting investment toward short-haul refined-product links that feed petrochemical sites.

By Service Type: Storage & Handling Gains as Operators Prioritize Resilience

Storage and handling services will climb 8.0% through 2031, helped by open-access terminals and inventory mandates. Predictive analytics and robotic inspection diversify pipeline-maintenance outsourcing, though pipeline construction still dominated 40.1% of 2025 revenue. Independent contractors flourish in city-gas spur lines where projects cost under USD 50 million.

Geography Analysis

The Beijing-Tianjin-Hebei, Yangtze Delta, and Pearl River Delta corridors represent about 60% of national gas demand and host 40% of LNG terminals. Dagang’s 3 billion m³ storage cluster fortifies supply for the capital, while Jintan salt cavern’s expanded inject-withdraw swing addresses seasonal peaks in the Yangtze region. Guangdong’s water scarcity curbs coastal terminal siting, shifting some projects inland with air-cooled vaporizers that raise delivered costs. Western Xinjiang and Sichuan act as supply hubs feeding the West-to-East Grid. Northeastern Liaoning enjoys diversified flows from Power of Siberia and Bohai offshore fields, cushioning regional prices from global LNG shocks.

Competitive Landscape

PipeChina is a regulated monopoly in trunk transmission, but over 500 municipal gas franchises fragment downstream distribution. ENN, Towngas, and China Gas Holdings compete on bundled services and connection fees, whereas 10 open-access LNG terminals enable independent buyers to purchase spot cargoes, tilting bargaining power away from national oil companies. AI-enabled maintenance elevates operational efficiency for PipeChina and CNPC, widening the digital gap with smaller distributors. Small-scale LNG distribution for trucking and bunkering offers white space for logistics specialists who integrate fuel supply with fleet services.

China Oil And Gas Midstream Industry Leaders

-

China National Petroleum Corporation

-

PipeChina

-

Sinopec

-

CNOOC Gas & Power

-

ENN Natural Gas

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Venture Global will supply Trafigura with 0.5 MTPA of U.S. LNG from 2026 to 2031. Although U.S.-based, the deal is significant for China’s midstream players as Trafigura, a major LNG trader in Asian markets, influences procurement competition and diversifies regional LNG flows.

- November 2025: Harvest acquired a significant gas-gathering and processing network in the Uinta/Green River Basin. While U.S.-focused, this deal highlights increasing global midstream consolidation, which Chinese NOCs monitor closely as they expand storage, pipelines, and LNG regasification capacity to support China’s evolving gas market.

- August 2025: PetroChina will acquire three CNPC gas-storage hubs for ¥40 billion ($5.6 billion), adding approximately 11 bcm of working capacity. This acquisition enhances China’s midstream resilience by improving seasonal balancing, supply security, and integration across the natural gas industrial chain amid increasing national gas demand.

- May 2025: China’s GPRIMG signed its first long-term LNG deal with ConocoPhillips, securing a 15-year U.S.-linked LNG supply starting in 2028. This agreement marks renewed China–US LNG engagement post-tariffs, enhancing China’s midstream security through long-term LNG sourcing and strengthening GPRIMG’s presence in the international gas value chain.

China Oil And Gas Midstream Market Report Scope

Midstream operations is one of the three oil and gas industry nodes. Midstream is the second node, and it involves storing and transporting oil, natural gas, and natural gas liquids to refineries. Midstream operations also involve treating the products to remove waste and compressing them before transporting them to the downstream markets and end-users.

The Chinese oil and gas midstream market is segmented by infrastructure, product type, and service type. By infrastructure, the market is segmented by pipeline, terminals, and storage facilities. By type, the market is segmented by crude oil, natural gas, refined products, and LNG. By service type, the market is segmented into pipeline construction, pipeline maintenance and repair, storage and handling services, and transportation and logistics. For each segment, the market size and forecasts are provided in terms of value (USD).

By Infrastructure

| Pipelines |

| Terminals |

| Storage Facilities (Underground and Above-ground) |

By Product Type

| Crude Oil |

| Natural Gas |

| Refined Products |

| LNG |

By Service Type

| Pipeline Construction |

| Pipeline Maintenance and Repair |

| Storage and Handling Services |

| Transportation and Logistics |

| By Infrastructure | Pipelines |

| Terminals | |

| Storage Facilities (Underground and Above-ground) | |

| By Product Type | Crude Oil |

| Natural Gas | |

| Refined Products | |

| LNG | |

| By Service Type | Pipeline Construction |

| Pipeline Maintenance and Repair | |

| Storage and Handling Services | |

| Transportation and Logistics |

Key Questions Answered in the Report

What is the projected 2031 value for China's midstream oil and gas sector?

It is forecast to reach USD 15.54 billion, reflecting a 5.02% CAGR from 2026 to 2031.

Which infrastructure segment is expanding fastest through 2031?

LNG terminals will post an 8.6% CAGR as import dependence deepens.

How do inventory mandates affect storage investment?

Rules requiring 90 days of peak-winter supply are driving an 8.0% CAGR in storage and handling services.

Why are LNG terminals under-utilized despite capacity growth?

Expansion of pipeline imports, notably Power of Siberia gas, reduced 2025 LNG demand by 9%, depressing terminal load factors.

Which region faces the greatest water constraint for new terminals?

Guangdong and neighboring coastal provinces must adopt costlier closed-loop vaporization to protect limited water resources.

Page last updated on: