Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 10.77 Billion |

| Market Size (2026) | USD 11.37 Billion |

| Market Size (2031) | USD 14.94 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Road Freight Transport Market Analysis by Mordor Intelligence

Chile Road Freight Transport Market size in 2026 is estimated at USD 11.37 billion, growing from 2025 value of USD 10.77 billion with 2031 projections showing USD 14.94 billion, growing at 5.61% CAGR over 2026-2031.

The country’s 4,300-kilometer north–south spine, favorable Pacific-facing trade orientation, and mining-led export base collectively underpin steady demand for truck services. Nearshoring of automotive parts from neighboring Argentina and Brazil, rising e-commerce penetration, and public works such as the Ruta 5 North upgrade reinforce growth prospects, while toll inflation, driver shortages, and climate-related disruptions create operating headwinds. Multimodal corridor projects that connect Chilean ports with the Atlantic side of South America promise new long-haul volumes and stronger asset utilization for carriers. Technology adoption from digital freight matching to AI-enabled route planning continues to improve load factors and lower empty-mile ratios, especially for smaller fleets that dominate the fragmented competitive landscape.

Key Report Takeaways

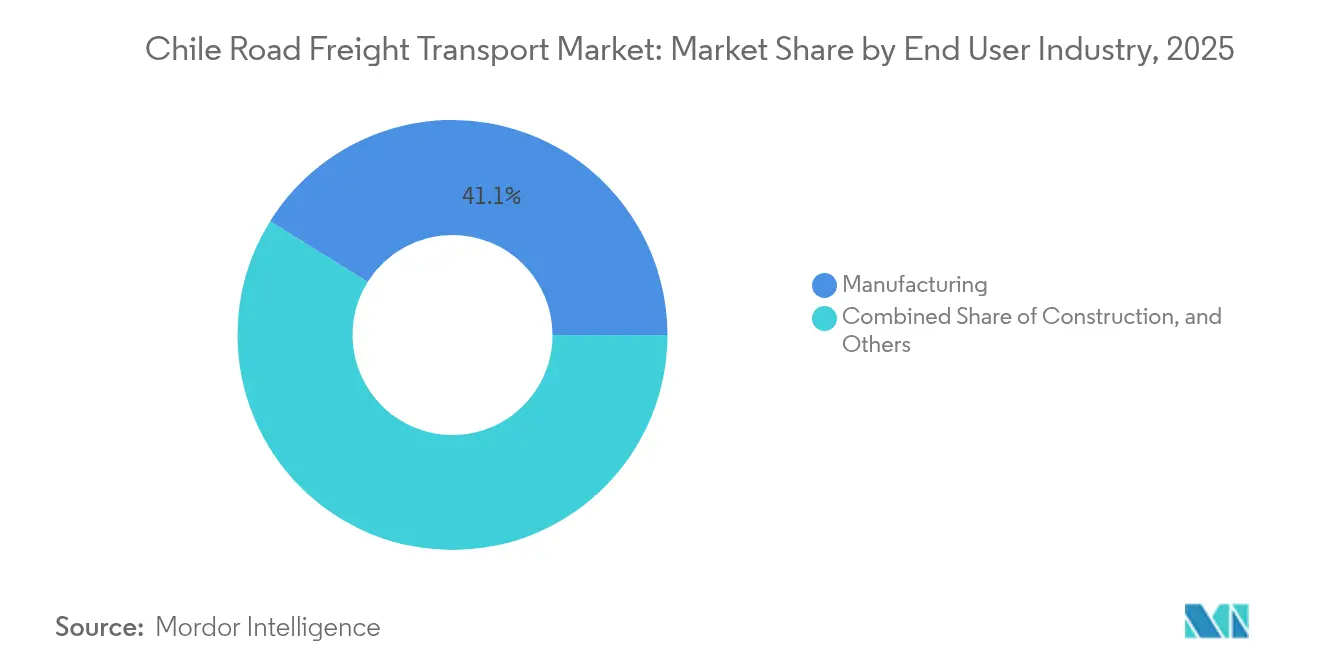

- By end-user industry, manufacturing led with 41.12% share of the Chile road freight transport market in 2025; wholesale and retail trade is projected to accelerate at a 5.85% CAGR through 2031.

- By destination, domestic moves accounted for 62.35% of the Chile road freight transport market size in 2025, while international freight is advancing at a 5.98% CAGR on the back of the bioceanic corridor plan.

- By truckload specification, FTL commanded 78.55% of Chile road freight transport market share in 2025, whereas LTL is the fastest-growing format at 5.74% CAGR through 2031.

- By containerization, non-containerized freight held 85.35% of Chile road freight transport market size in 2025; containerized traffic is poised for 5.27% CAGR as manufacturing and high-value perishables expand.

- By distance band, long-haul trips represented 73.25% of overall moves in 2025, with short-haul urban deliveries projected to climb 5.41% annually to 2031.

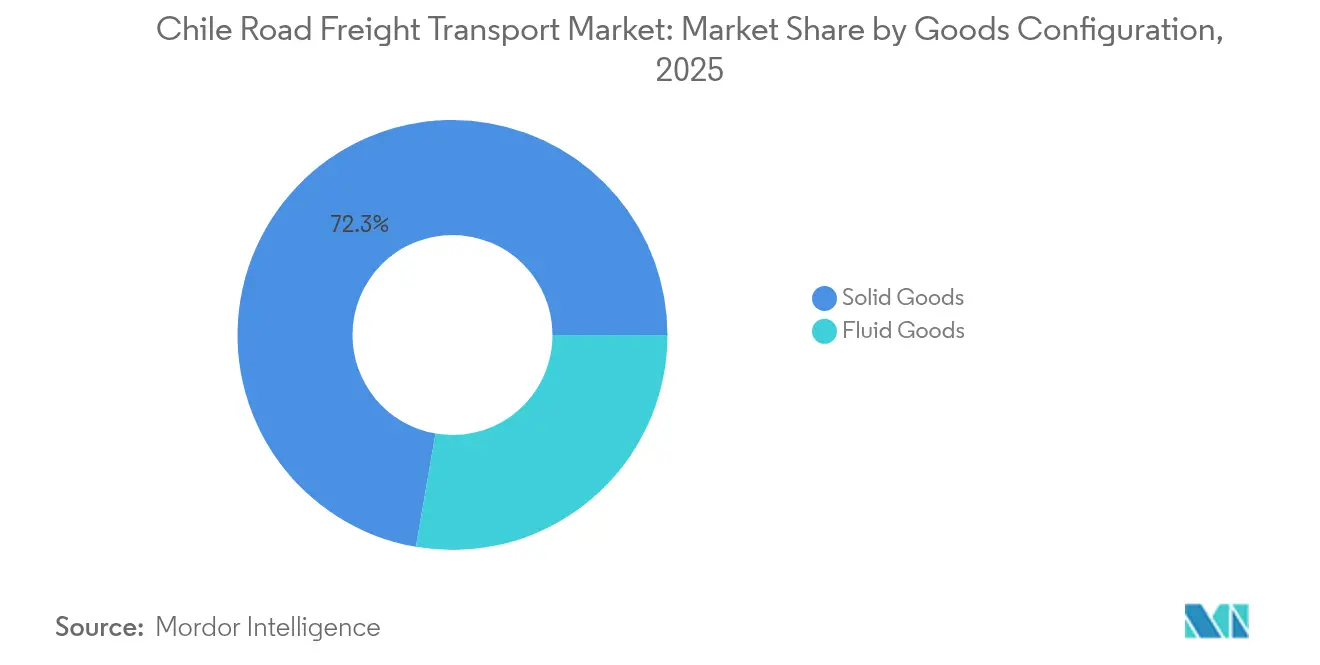

- By goods configuration, solid goods commanded 72.28% share in 2025, but fluid goods mainly chemicals used in lithium processing—are growing 5.64% each year.

- By temperature control, non-refrigerated loads dominated with 94.52% share in 2025; temperature-controlled cargo is gaining 5.70% annually as fruit exports and grocery home-delivery develop.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of Chilean e-commerce sector | +1.2% | National (Santiago, Valparaíso, Concepción first) | Medium term (2-4 years) |

| Growing demand from lithium-mining supply chains in the north | +0.8% | Antofagasta, Tarapacá | Long term (≥ 4 years) |

| Government highway concession upgrades (Ruta 5 & bioceanic corridor) | +1.0% | Nationwide, cross-border | Long term (≥ 4 years) |

| Nearshoring of automotive parts manufacturing | +0.7% | Central Chile & cross-border corridors | Medium term (2-4 years) |

| Digital freight-matching platforms | +0.5% | Urban logistics hubs | Short term (≤ 2 years) |

| OEM investment in Euro VI/alt-fuel fleets | +0.6% | National (early uptake in Santiago) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Chilean E-commerce Sector

Online retail continues to reshape freight flows, with food-and-beverage web sales leaping 133% between 2020 and 2024 and maintaining double-digit growth into 2025. Smaller, more frequent consignments favor LTL and last-mile operators, especially in Santiago where 34% of large food outlets are located. Digital payment localization drives order conversion and boosts shipment counts as 94% of Latin American consumers demand friction-free checkout. Retailers answer with omnichannel logistics investment, creating a larger addressable base for tech-savvy carriers that can orchestrate hub-and-spoke urban deliveries over distances often surpassing 500 kilometers between major Chilean cities[1]“Presidente de la República encabezó presentación del Plan de Acción del Corredor Bioceánico Vial,” Ministerio de Obras Públicas, mop.gob.cl.

Growing Demand from Lithium-Mining Supply Chains in the North

The National Lithium Strategy seeks an additional 300,000 LCE by 2030 via public-private partnerships such as the Codelco-SQM alliance. Bulk sulfuric acid, mineral reagents, heavy machinery, and outbound lithium carbonate must travel 1,400 kilometers from the Atacama to central ports, requiring specialized ADR-compliant tankers and robust fleet maintenance regimes to withstand desert extremes. Cochilco highlights 49 mining projects worth USD 65.71 billion slated for 2023-2032, ensuring sustained freight volumes for both construction inputs and outbound concentrates[2]“Global truck driver shortage to double by 2028,” International Road Transport Union, iru.org.

Government Highway Concession Upgrades (Ruta 5 & Bioceanic Corridor)

The USD 10 billion, 2,400-kilometer bioceanic plan unveiled in April 2025 links Pacific terminals with Brazil, Argentina, and Paraguay and could trim Atlantic-Pacific transit times by 67%. Complementary investments—such as the USD 1.27 billion Route 5 North widening and Santiago-Valparaíso’s USD 3.8 billion rail concession—raise corridor capacity, standardize electronic tolling, and open intermodal options that de-bottleneck main arteries. Improved infrastructure supports just-in-time export supply chains and may catalyze emerging green-hydrogen equipment flows tied to Chile’s renewable ambitions.

Nearshoring of Automotive Parts Manufacturing from Argentina/Brazil

More suppliers reroute production to Chile’s tariff-light environment under 65 trade accords, seeking to reduce geopolitical risk and shorten lead times. The bioceanic roadway slashes Asia-bound transit for automotive components by roughly 17 days, aiding just-in-time models that depend on schedule-reliable cross-border trucking. Parts warehouses around Santiago and Los Andes increasingly contract secure, temperature-stable FTL units capable of customs-integrated tracking as value density of shipments rises[3]“Walmart will test a green-hydrogen fuel-cell truck in Chile,” IEEE Spectrum, ieee.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortage and aging workforce | -0.8% | National, acute in remote north | Long term (≥ 4 years) |

| Road-toll inflation outpacing freight rates | -0.6% | Route 5 and Santiago network | Short term (≤ 2 years) |

| Cabotage restrictions on cross-border back-hauls | -0.4% | Borders with Argentina, Peru, Bolivia | Medium term (2-4 years) |

| Climate-induced landslides on mountain corridors | -0.5% | Andean passes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Driver Shortage and Aging Workforce

The International Road Transport Union warns global unfilled driver posts could double by 2028, and Chile mirrors this trend with dwindling interest among younger workers and female participation still below 6%. The 2024 labor reform that cuts the workweek to 40 hours strains scheduling flexibility and raises overtime costs, especially for lithium-route carriers working multi-day cycles. Mining operators finance shared rest facilities and training programs, yet industry surveys still flag a 34,000-head talent gap.

Road-Toll Inflation Outpacing Freight Rates

Annual CPI + 3.5% indexation pushes Route 5 South tolls to CLP 3,000–3,700 for cars and roughly double for trucks, eroding margins on Santiago–Puerto Montt lanes of more than 1,400 kilometers. Mandatory TAG transponders eliminate cash flexibility, and weekend surcharges of up to 20% further raise cost volatility. Freight brokers struggle to pass increases downstream in a price-competitive environment, squeezing owner-operators who dominate 80% of the fleet.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing Anchors Diversification

Manufacturing commanded 41.12% of the Chile road freight transport market share in 2025, thanks to sustained inflows of automotive parts and electronics under nearshoring deals. This dominance translates into stable FTL call-offs for just-in-time lines, while LTL opportunities arise from tier-2 suppliers delivering sub-assemblies. The Chile road freight transport market size attributable to wholesale and retail trade is smaller today but expands the fastest, mirroring the 5.85% CAGR projection driven by omnichannel grocery and Walmart’s USD 1.3 billion warehouse spree.

Mining, oil, and quarrying freight remains a backbone segment, buoyed by 49 active projects with a USD 65.71 billion capex pipeline and the National Lithium Strategy’s target of 300,000 LCE additional output. Agriculture adds significant seasonal elasticity; a single cherry harvest can boost container demand by 75%, forcing carriers to reposition reefers from central-southern orchards to San Antonio port under tight dwell-time windows. Construction volumes ebb and flow with infrastructure outlays—Ruta 5 upgrades alone inject more than seven million tons of aggregates and steel into the network through 2027.

By Destination: International Corridor Momentum Builds

Domestic lanes held 62.35% of the Chile road freight transport market in 2025, reflecting dense north–south trade along Ruta 5 between Santiago, Valparaíso, and Concepción. Yet international volumes now record a 5.98% CAGR through 2031 as bioceanic projects near completion and landlocked Paraguay taps Pacific gateways to Asia. Cross-border hauls typically involve soybean, beef, and auto parts flowing west and containerized consumer goods heading east.

Cabotage limits hamper back-haul yields, but harmonized customs procedures under the corridor plan and expanded use of electronic consignment notes shorten border dwell times by up to 30 minutes per truck. Currency risk remains: peso volatility against the Brazilian real can swing cross-border trucking rates by 4-5 percentage points within a quarter, prompting carriers to hedge via USD-denominated contracts.

By Truckload Specification: FTL Dominates, LTL Innovates

FTL represented 78.55% of the Chile road freight transport market size in 2025, supplying bulk copper, lithium, and agriculture. Mining consignors contract fixed-route FTL to mitigate hazardous-goods compliance complexity, which supports higher asset turns but leaves limited back-haul cargo. LTL expands at 5.74% CAGR as online retail proliferates, making multi-stop milk-runs viable in cities where e-delivery density exceeds 250 orders per square kilometer.

Digital brokers slice administrative time by combining rate benchmarking, e-bill-of-lading issuance, and automated proof-of-delivery flows, lowering entry barriers for small fleets. Higher touch-point LTL also drives demand for telematics, refrigerated micro-depots, and AI-based consolidation.

By Containerization: Bulk Reigns, Boxes Gain

Non-containerized bulk cargo holds 85.35% share because of Chile’s resources orientation. Copper concentrate moving from inland concentrators to Antofagasta port alone consumes thousands of tipper-truck runs daily. Even so, containerized loads now notch a 5.27% CAGR as manufactured goods, seafood, and fruit exports rise. The Chile road freight transport market size tied to reefer boxes grows in tandem with cherry and table-grape seasons that each require more than 3,500 controlled-atmosphere TEU per peak month.

DP World’s MoorMaster automated mooring in San Antonio cuts vessel turnaround by 30 minutes, smoothing truck gate scheduling and elevating box velocity. Manufacturers also favor containers for automotive components to mitigate theft and weather damage over long desert transits.

By Distance: Long-Haul Still Commands Volume

Long-haul trips account for 73.25% of 2025 tonnage as cities and mines lie hundreds of kilometers apart. Future bioceanic corridors could extend average trip length beyond 1,800 kilometers door-to-door when linking Paraguay or Brazil to Pacific hubs. These distances make diesel cost swings and toll escalators highly consequential—Route 5 tolls alone can reach USD 250 per tractor-trailer round trip.

Short-haul traffic gains pace in urban clusters, driven by same-day delivery promises that fuel micro-fulfillment centers within 20 kilometers of end consumers. Pilot programs with electric rigid trucks in Santiago aim to cut operating cost per kilometer by 35% once battery pack prices fall below USD 90 per kWh.

By Goods Configuration: Solids Dominate, Fluids Expand

Solid goods controlled 72.28% of 2025 freight value, led by copper cathodes, iron ore, and sawn timber. Growing lithium processing lifts demand for fluid chemicals—sulfuric acid haulage rose 11% year-on-year to 2025 as well as specialized ISO tank containers capable of desert heat operation. The Chile road freight transport market share attributed to fluids remains modest but posts a 5.64% CAGR, underpinned by future hydrogen-related liquids once commercial projects materialize in Biobío.

Hazardous-goods regulations heighten compliance costs for fluid carriers, yet also shelter margins; insurers now require telematics with geofencing alarms for all acid transport above 25 MT—a specification that 60% of fleets still lack.

By Temperature Control: Ambient Dominates but Cold Chain Accelerates

Ambient freight held 94.52% share in 2025. However, the rise of high-value fruit and expanding grocery e-commerce push the cold-chain segment toward a 5.70% CAGR. Reefer fleet capacity remains tight, especially during December–January cherry harvests when demand can double weekly. Carriers invest in solar-assisted reefer units to shave diesel genset consumption, lowering per-trip fuel cost by up to 12%.

Green hydrogen pilots could eventually power refrigerated trailers, aligning with shippers’ Scope 3 emission pledges and reinforcing Chile’s image as a low-carbon logistics hub.

Geography Analysis

Santiago’s metropolitan area anchors domestic distribution thanks to its one-third share of national population and its concentration of major DCs. The Ruta 5 North and South corridors connect the capital to ports and agrarian zones, while a USD 1.27 billion widening project boosts resilience against El Niño-driven storms. Northern hubs such as Antofagasta serve the lithium triangle, with specialized ADR fleets running sulfuric acid south-north and returning with concentrates; distances exceed 1,400 kilometers. Southern regions, notably Biobío and Los Lagos, rely on long-haul flatbeds for timber and salmon feed, yet also host emerging green-hydrogen clusters.

Internationally, the April 2025 bioceanic roadmap formalizes a 2,400-kilometer corridor that replaces multi-week Cape Horn detours, stimulating truck traffic to Argentine and Paraguayan grain belts and shaving door-to-port lead times by roughly 11 days. Customs digitization and weight harmonization agreements cut border queues, though cabotage rules still prevent foreign tractors from loading domestic legs. Pacific-Atlantic rates compress as asset turns improve—one Antofagasta-Campo Grande-Antofagasta loop now completes in 6 days rather than 10.

Chile’s 65+ trade deals make it a re-export platform; trans-shipment imports of Asian consumer electronics head to Bolivia and Peru via the Arica corridor, stimulating growth for regional forwarders. Toll heterogeneity and FX volatility across borders keep pricing opaque, promoting interest in end-to-end USD contracts and dynamic fuel surcharges.

Competitive Landscape

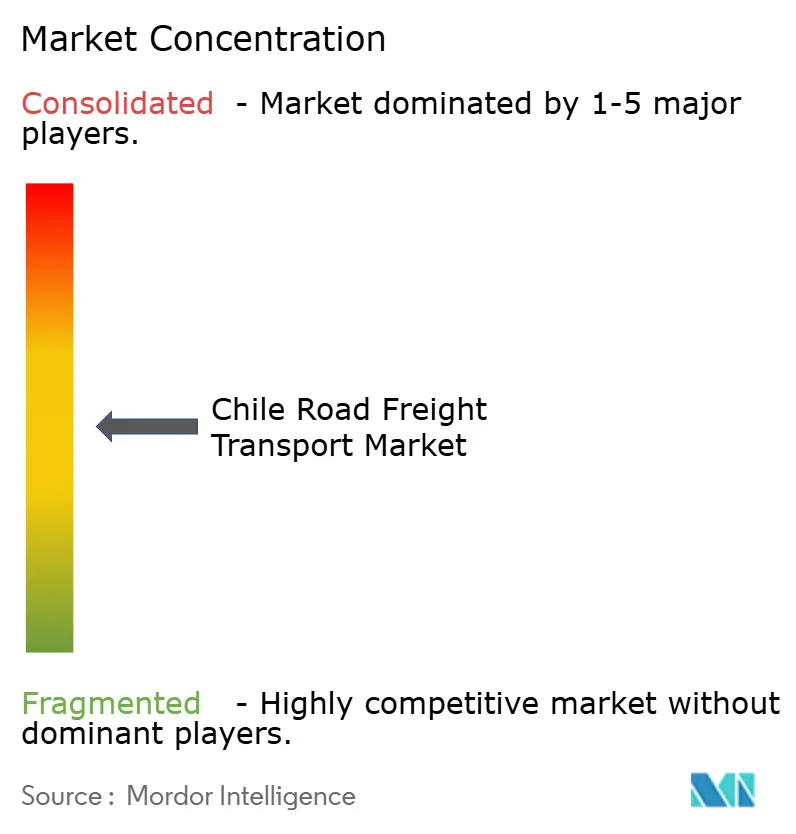

The market remains fragmented. Global giants intensify consolidation after DSV closed its EUR 14.3 billion (USD 15.78 billion) takeover of DB Schenker in April 2025, creating a 160,000-employee behemoth with Chilean coverage through inherited Schenker depots. Regional mid-caps respond by deepening vertical niches: some target temperature-controlled horticulture, others specialize in dangerous-goods mining runs.

Digital disruptors such as EnviaMe and Cargainteligente scale by licensing SaaS routing modules to owner-operators, winning market share in e-commerce segments. Legacy fleets modernize with Euro VI powertrains—Volvo delivered Latin America’s first heavy-duty EVs to a Santiago carrier in late 2024—to comply with upcoming emission norms and appeal to ESG-focused shippers. Investment circles note rising M&A chatter among mid-tier operators looking to gain negotiating power against toll-road concessions and fuel suppliers.

Strategic bets on intermodal integration emerge: three carriers bid for a 15-year service contract related to the USD 3.8 billion Santiago–Valparaíso rail concession, aiming to bundle road drayage with block-train operations once the line opens in 2030. Meanwhile, Walmart Chile’s hydrogen-fuel-cell pilot demonstrates shippers’ willingness to co-invest in alternative-energy fleets to hedge against diesel price volatility. Carriers lacking capital for these transitions risk margin erosion and eventual buyouts.

Chile Road Freight Transport Industry Leaders

Andes Logistics de Chile S.A.

Agunsa (Agencias Universales S.A.)

Transportes Casablanca

Transportes Nazar

Sotraser

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its EUR 14.3 billion (USD 15.78 billion) acquisition of DB Schenker, creating the world’s largest logistics group and targeting DKK 9 billion (USD 1.44 billion) in annual synergies by 2028.

- April 2025: Chile’s president unveiled the bioceanic corridor action plan that will link Pacific ports to Brazil, Argentina, and Paraguay through 2,400 kilometers of multimodal assets.

- April 2025: The government introduced a USD 5 million subsidy for green-hydrogen development in Biobío, expanding future freight categories for specialized equipment.

- March 2025: Fishermen’s protests in Valparaíso ended, restoring truck access to key berths after week-long cargo delays.

Chile Road Freight Transport Market Report Scope

The transportation of goods/products via roadways is referred to as road freight transport. It is also one of the world's most traditional kinds of logistics, as well as the most widely used mode of transportation worldwide. If and when needed, road freight is utilized in combination with air and sea freight modes to provide door-to-door delivery. A comprehensive background analysis of the Chile road freight market covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry is provided in this report. The impact of COVID-19 has also been incorporated and considered during the study.

The Chile Road Freight Market is segmented by destination (domestic and international), by end user (manufacturing (including automotive), oil and gas, mining and quarrying, agriculture, fishing, and forestry, construction, pharmaceuticals and healthcare, and other end users). The report offers market size and forecast values in (USD) for all the above segments.

By Destination

| Domestic |

| International |

By End-User Industry

| Manufacturing |

| Oil, Gas, Mining and Quarrying |

| Agriculture, Fishing and Forestry |

| Construction |

| Wholesale and Retail Trade |

| Other End-Users |

By Truckload Specification

| Full Truckload (FTL) |

| Less-than-Truckload (LTL) |

By Containerization

| Containerised |

| Non-Containerised |

By Distance

| Long Haul |

| Short Haul |

By Goods Configuration

| Fluid Goods |

| Solid Goods |

By Temperature Control

| Non-Temperatured Controlled |

| Temperatured Controlled |

| By Destination | Domestic |

| International | |

| By End-User Industry | Manufacturing |

| Oil, Gas, Mining and Quarrying | |

| Agriculture, Fishing and Forestry | |

| Construction | |

| Wholesale and Retail Trade | |

| Other End-Users | |

| By Truckload Specification | Full Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| By Containerization | Containerised |

| Non-Containerised | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperatured Controlled |

| Temperatured Controlled |

Key Questions Answered in the Report

How large is the Chile road freight transport market in 2026?

The Chile road freight transport market size is valued at USD 11.37 billion in 2026.

What is the projected growth rate for Chilean trucking services through 2031?

The market is expected to expand at a 5.61% CAGR, reaching USD 14.94 billion by 2031.

Which end-user sector moves the most road freight in Chile?

Manufacturing leads with 41.12% of total market share in 2025, driven by automotive parts nearshoring.

Which destination segment is growing fastest for Chilean carriers?

International freight traffic shows the highest momentum with a 5.98% CAGR through 2031, supported by the bioceanic corridor initiative.

How significant is e-commerce for trucking demand in Chile?

Rapid e-commerce expansion adds 1.2 percentage points to forecast market CAGR, fueling LTL and last-mile volumes.

What challenges do Chilean road freight operators face?

Key hurdles include driver shortages, rising tolls, cabotage limits on back-hauls, and climate-driven disruptions on mountain routes.

Page last updated on: