Chile Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

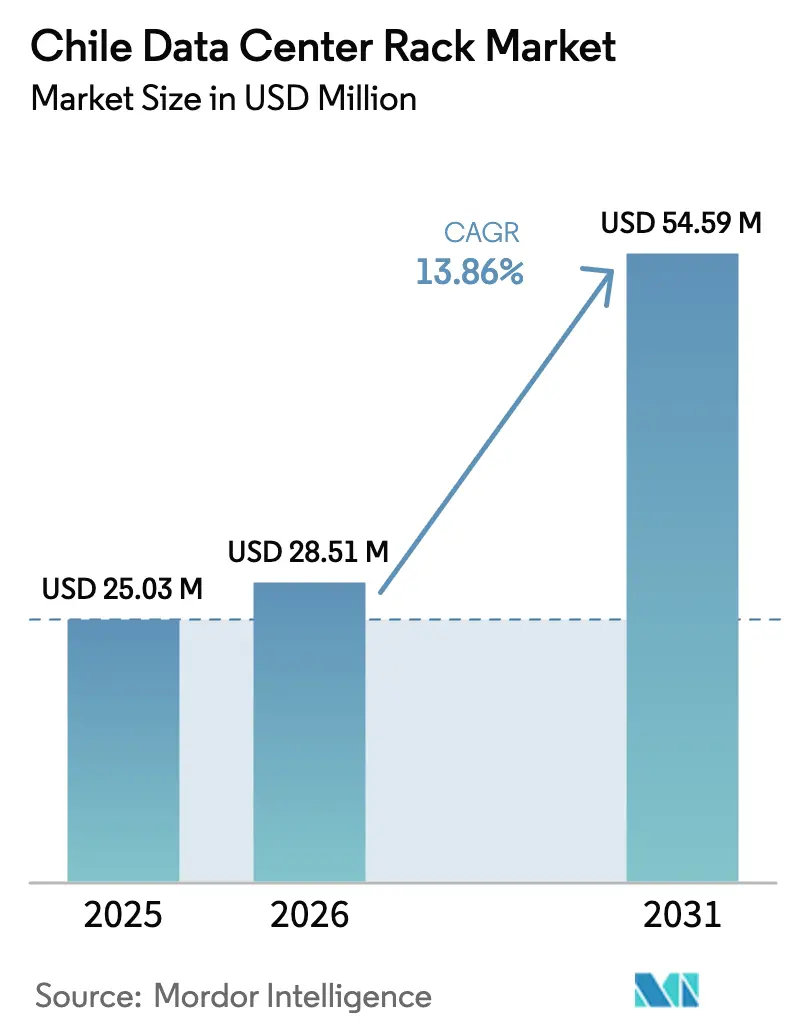

| Base Year Market Size (2025) | USD 25.03 Million |

| Market Size (2026) | USD 28.51 Million |

| Market Size (2031) | USD 54.59 Million |

| Growth Rate (2026 - 2031) | 13.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Data Center Rack Market Analysis by Mordor Intelligence

The Chile data center rack market size is expected to grow from USD 25.03 million in 2025 to USD 28.51 million in 2026 and is forecast to reach USD 54.59 million by 2031 at 13.86% CAGR over 2026-2031. Sustained hyperscale commitments—most notably Amazon’s USD 4 billion AWS build-out—anchor fresh capacity pipelines and underpin robust cabinet demand in Santiago, Valparaíso, and emerging edge locations .[1]Amazon Web Services, “AWS Announces USD 4 Billion Investment in Chile,” aws.amazon.com Operators continue to standardize around 42U and full-rack footprints to speed fit-outs, reduce procurement complexity, and support 20–40 kW densities demanded by AI and cloud workloads.[2]Schneider Electric, “2024 Full-Year Results,” se.com Government incentives that link tax credits to renewable-power sourcing further strengthen the Chile data center rack market’s value proposition as global firms pursue net-zero targets. Taken together, submarine cable landings, 5G rollouts, and AI-focused research programs reinforce Chile’s status as Latin America’s fastest-scaling digital-infrastructure node, driving supplier competition across steel and aluminum form factors.

Key Report Takeaways

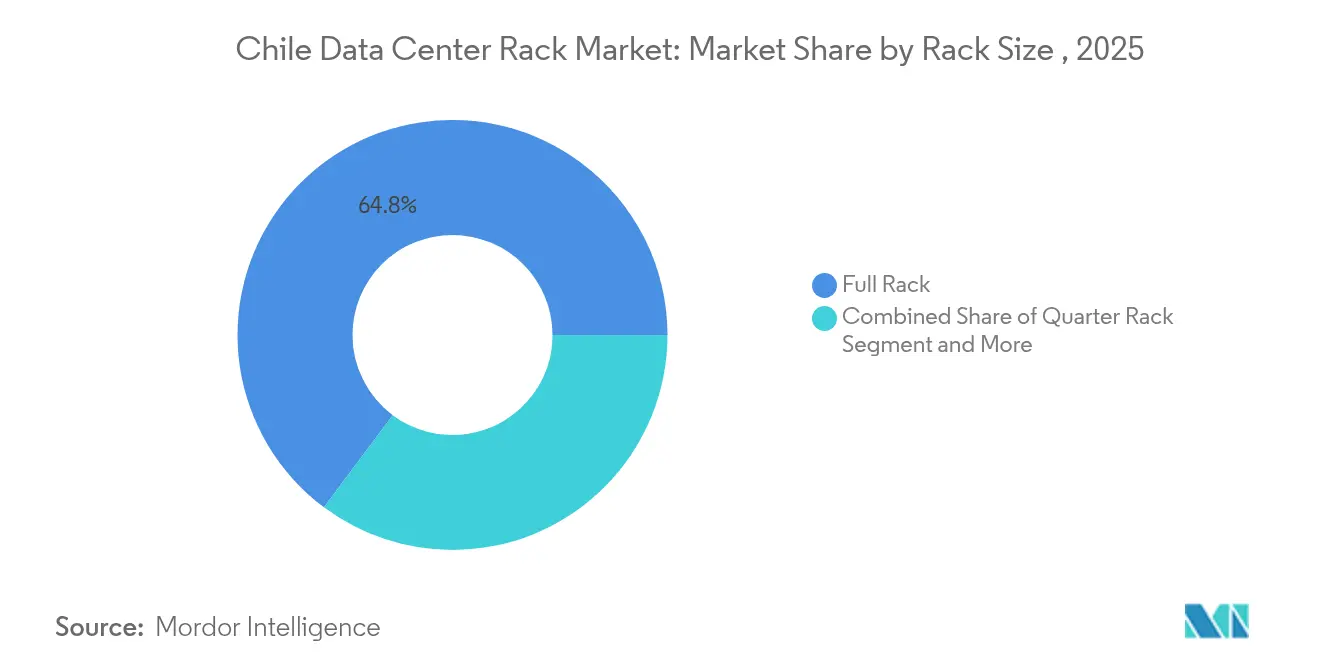

- By rack size, full-rack configurations led with 64.80% of Chile data center rack market share in 2025.

- By rack height, 42U systems held 55.90% share of the Chile data center rack market size in 2025, while 48U is projected to post a 14.84% CAGR through 2031.

- By rack type, cabinet solutions accounted for 71.60% share of the Chile data center rack market size in 2025 and are set to grow at a 15.25% CAGR to 2031.

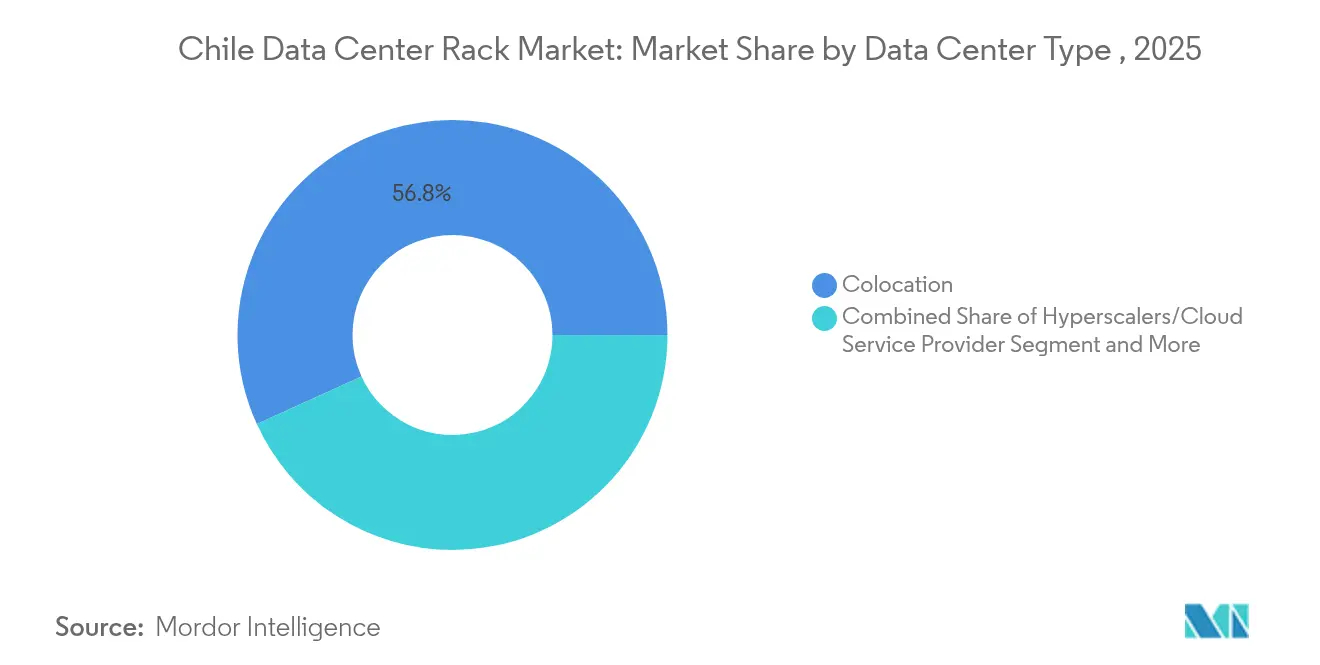

- By data-center type, colocation operators captured 56.80% revenue in 2025; hyperscale and cloud facilities are forecast to expand at 15.75% CAGR through 2031.

- By material, steel dominated with 77.50% share in 2025, while aluminum is the fastest-growing material at a 16.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile operates as part of an interconnected international environment rather than as a self-contained country level unit. The data center rack market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Chile Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cloud-first digital strategy among Chilean enterprises | +2.8% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| 5G-led edge-data-center build-outs | +2.1% | National, concentrated in Santiago metro and port cities | Short term (≤ 2 years) |

| Government incentives for renewable-powered data centers | +1.9% | National, with focus on northern solar regions | Long term (≥ 4 years) |

| Hyperscale investments linked to new submarine cables | +3.2% | Coastal regions, particularly Valparaíso and Santiago metro | Medium term (2-4 years) |

| Shift to high-density (20-40 kW) racks | +2.4% | Santiago metro and hyperscale facilities | Short term (≤ 2 years) |

| Emergence of Santiago as a regional AI model-training hub | +1.8% | Santiago metro, with spillover to Valparaíso | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cloud-First Digital Strategy Among Chilean Enterprises

Chilean companies accelerate cloud adoption to modernize public-service platforms and core business workloads, pushing steady cabinet uptake across the Chile data center rack market. Internet penetration stands at 91% and mobile connections at 147%, giving enterprises the bandwidth foundation for hybrid migrations. The Chile Digital 2035 program mandates 100% digital public services, prompting agencies to replace legacy hardware with standardized 42U racks that ease multi-colocation interoperability. Financial-services and mining firms further favor cabinet enclosures for compliance and dust mitigation. Consequently, demand for full racks capable of 20–40 kW densities rises in line with enterprise AI pilots.

5G-Led Edge-Data-Center Build-Outs

Entel’s national 5G coverage, extended even to Antarctica’s Presidente Eduardo Frei base, accelerates micro-data-center rollouts that prefer quarter-rack and wall-mount solutions.[3]Ericsson, “Entel Brings 5G to All Chilean Regions,” ericsson.com Low-latency use cases—such as remotely piloted salmon-farm equipment and automated port cranes—need resilient racks that fit small footprints and withstand coastal humidity. As operators chase Chile’s 90% 5G-coverage target for 2025, suppliers able to deliver ruggedized form factors register faster order cycles, strengthening regional distribution channels outside Santiago.

Government Incentives for Renewable-Powered Data Centers

Chile aims for 70% renewable electricity by 2030—a policy that fuels global cloud entrants seeking carbon-neutral sites and energizes aluminum rack adoption because of weight and cooling advantages. Microsoft’s pledge to source 100% renewable power for its local campuses by 2025 spotlights high-efficiency rack designs with minimized airflow obstruction. Tax credits and streamlined permits under the National Data Centers Plan reward operators that certify low power-usage effectiveness, prompting upgrades to liquid-ready cabinets compatible with direct-to-chip cooling.

Hyperscale Investments Linked to New Submarine Cables

The Humboldt cable’s Valparaíso landing will add 144 Tbps of transpacific capacity by 2027, inducing hyperscale players to pre-lease megawatt blocks and specify taller 48U racks that house extensive fiber-cross-connect gear. Scala Data Centers already built a 30 MW site in Curauma to exploit this route, filling its halls before project completion. Tall racks consolidate switching, optics, and compute inside a single footprint, optimizing space economics where land prices rise sharply.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe water-stress regulations on cooling systems | -1.8% | National, particularly acute in Santiago metro | Short term (≤ 2 years) |

| High land-acquisition costs in Santiago metro | -1.2% | Santiago metropolitan region | Medium term (2-4 years) |

| Slow power-grid permitting for >20 MW campuses | -0.9% | National, with delays concentrated in Santiago | Medium term (2-4 years) |

| Peso volatility impacting imported rack prices | -1.1% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe Water-Stress Regulations on Cooling Systems

Court challenges over aquifer use halted Google’s USD 200 million Santiago build, underscoring how strict water rules can derail large projects. Developers pivot toward immersion and direct-to-chip cooling that cut evaporative loss by design, requiring racks pre-configured for coolant manifolds. AI training clusters, often exceeding 10.2 kW per rack with NVIDIA DGX H100 systems, intensify this shift. Consequently, open-frame architectures gain traction where airflow is unhindered, while sealed cabinets must integrate rear-door heat exchangers to stay viable in water-scarce districts.

High Land-Acquisition Costs in Santiago Metro

Scarce seismic-qualified plots and premium power feeds push land prices above regional norms, encouraging operators to secure suburban campuses like TECfusions’ 100 MW Puente Alto site. Larger parcels lower unit land cost but add logistical hurdles, from longer delivery routes for steel frames to extended permitting timelines. Smaller rack vendors lacking volume leverage face margin pressure when serving dispersed builds, prompting strategic alliances with local assemblers to offset haulage and currency risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full-Rack Dominance Drives Hyperscale Adoption

Full racks captured 64.80% of Chile data center rack market share in 2025 as global operators standardized on uniform footprints across multiregion campuses. The Chile data center rack market size for full racks is forecast to rise at 15.68% CAGR, propelled by Amazon’s USD 4 billion expansion program that replicates AWS’s global cabinet blueprint. Enterprise colocation tenants favor the same format to simplify capacity upgrades and maintain SLA consistency. Quarter and half racks remain relevant for telecom edge nodes and mid-market migrations but see slower uptake as cloud-first strategies mature.

Schneider Electric’s acquisition of Motivair aligns with this trend—liquid-ready full racks allow 20–40 kW loads without costly room-level retrofits. NVIDIA DGX H100 clusters, already deployed in local AI pilots, require the depth and cable-management clearances available only in full-size cabinets. Consequently, supply chains favor bulk orders of identical SKUs, trimming lead times and reducing per-rack cost for Chilean hyperscale sites.

By Rack Height: 42U Standard Meets AI Density Requirements

The 42U profile held 55.90% share of the Chile data center rack market size in 2025 due to its ergonomic serviceability and compatibility with mainstream PDUs. However, taller 48U frames are growing at 14.84% CAGR as submarine-cable operators and AI clusters add network spines and rear-door exchangers that need extra vertical space. 45U and custom heights serve telecom and research use cases where unique airflow or seismic bracing is specified.

Chile’s AI research community, spearheaded by the Franco-Chilean Binational Center launched in 2025, often demands unconventional rack heights to host experimental liquid tanks and sidecar GPUs . Operators balance this flexibility with maintenance safety: keeping heavy switch gear below eye level to meet local labor standards. Ongoing seismic-code updates also influence height choices, nudging facilities toward braced 42U designs for production workloads while relegating taller frames to isolated high-density halls.

By Rack Type: Cabinet Security Drives Enterprise Adoption

Cabinets represented 71.60% revenue in 2025 because enclosed designs safeguard mission-critical workloads from dust and unauthorized access, priorities for Chile’s banking and mining verticals. The Chile data center rack market is expected to see cabinet demand increase at a 15.25% CAGR as data-sovereignty rules mandate in-country retention of sensitive records iticolombia. Open-frame racks gain adoption where airflow is paramount, especially in immersion-cooling rooms that eliminate need for solid side panels.

Financial regulators enforce strict audit trails, prompting operators to integrate electronic locks and environmental sensors within cabinet doors for real-time compliance reporting. Earthquake-risk mitigation also favors cabinets because factory-welded structures outperform bolt-together open frames during lateral shocks. Equipment vendors respond by shipping pre-populated, vibration-tested cabinets, enabling enterprises to deploy rack-level mini-clouds in remote mining sites with minimal onsite assembly.

By Data Center Type: Colocation Leadership Reflects Market Maturity

Colocation providers held 56.80% share in 2025, signifying corporate preference for turnkey data halls operated by seasoned specialists. However, hyperscale campuses, buoyed by Amazon and Microsoft projects, will register a 15.75% CAGR to 2031, gradually shifting the center of gravity of the Chile data center rack market. Enterprise on-premise facilities persist for latency-sensitive SCADA and government workloads but account for declining volume as cloud economics improve.

Vertiv’s 2024 revenue mix illustrates this shift: stronger growth came from colocation orders where racks, PDUs, UPS, and monitoring ship as bundles. Hyperscale operators insist on rack SKUs matched to global data-center design kits, driving bulk orders multiple quarters in advance. Edge installations, linked chiefly to 5G nodes, favor rugged wall-mount enclosures engineered for constrained telecom shelters, expanding vendor portfolios beyond traditional IT cabinets.

By Material: Steel Dominance Faces Aluminum Challenge

Steel framed 77.50% of racks installed during 2025 because it combines affordability with seismic-grade rigidity, critical in a country lying on the Pacific Ring of Fire. Aluminum, though only a modest base, is projected to grow 16.55% annually through 2031 as weight savings enable higher floor loads without reinforcement, especially in retrofit buildings. Hybrid composites find niche adoption in electromagnetic-shielded military and healthcare sites.

Lighter alloys also shorten installation time; two technicians can position an empty aluminum cabinet without forklifts, a key advantage in edge sites lacking loading docks. Cost parity remains a hurdle, yet currency swings favor locally extruded aluminum when imported steel prices spike on peso volatility. Suppliers hedge by offering dual-material portfolios—steel for cost-sensitive enterprise halls and aluminum for AI clusters where power and cooling density offset higher upfront rack spend.

Geography Analysis

Santiago’s metro area concentrates the bulk of Chile data center rack market deployments thanks to mature fiber rings, multiple neutral IXPs, and proximity to financial customers. The capital’s racks increasingly serve AI training workloads initiated by the Binational Center on Artificial Intelligence, pushing power densities beyond historical norms and necessitating liquid-ready 42U and 48U format. Yet severe water-stress regulations and escalating land costs prompt operators to scout peripheral communes and neighboring regions to mitigate permitting delays.

Valparaíso has emerged as a strategic alternative built around submarine-cable landings, most notably the Humboldt route scheduled to activate in 2027 with 144 Tbps capacity dw. Scala Data Centers pre-leased its 30 MW Curauma build on the cable’s doorstep, stacking 48U cabinets to integrate dense fiber cross-connect panels. Coastal climate benefits free-air cooling days, lowering PUE for operators that certify renewable energy mixes to meet tax-credit thresholds.

Secondary cities such as Concepción and Antofagasta serve mining, logistics, and telecom edge applications. Entel’s 5G footprint in every Chilean region opens demand for compact quarter-racks and wall-mount enclosures inside rugged shelters serving automated salmon farms and remote dredging operations. Grid-expansion plans—adding 4,000 km of new transmission by 2031—will widen viable sites, though seismic zoning continues to dictate structural rack material choices. Suppliers with regional inventory hubs gain competitive lead times when serving these dispersed projects, reinforcing domestic assembly value chains.

The data center rack market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as South America, Europe, and North America, along with detailed country-level analysis for Mexico, Brazil, Switzerland, Poland, Norway, and Italy.

Competitive Landscape

Global vendors and regional specialists share a moderately concentrated field as hyperscale builds scale sharply. Schneider Electric posted EUR 38 billion 2024 revenue, citing double-digit growth in South American data-center projects, with Chile contributing strongly across mining and cloud builds. The Motivair acquisition equips the firm with in-house liquid-cooling know-how, letting it package racks, CDUs, and containment under a single SKU—an appealing proposition in water-stressed jurisdictions.

Vertiv recorded USD 8.0 billion 2024 sales, rising 17% year-on-year on heavy Americas colocation orders, and now bundles cabinet power-train kits tailored to Chilean seismic code Zone 3 requirements. Eaton’s USD 24.9 billion 2024 topline underscores its diversification into modular plants; local distributors offer fast-ship steel frames to bridge peso-driven price spikes. Regional player Scala, though primarily a landlord, influences rack standards through design-build partnerships with OEMs for its 100+ MW Latin assets.

Strategic themes emphasize integrated rack-plus-cooling stacks, earthquake resilience, and renewable-aligned efficiency. Vendors localize manufacturing where feasible to hedge currency swings and meet rapid delivery windows demanded by hyperscale contracts. Alliances with construction firms familiar with Chilean seismic and environmental codes accelerate campus commissioning. As hyperscale share grows, purchasing power consolidates; yet diverse edge and enterprise niches maintain entry points for smaller fabricators offering bespoke or ruggedized enclosures.

Chile Data Center Rack Industry Leaders

Schneider Electric SE

Vertiv Group Corporation

Eaton Corporation plc

Legrand SA

Delta Electronics, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: TECfusions and Baeza Group secured a landmark land deal for Chile’s largest planned data center campus, marking a significant expansion in the country’s hyperscale infrastructure capacity

- June 2025: Google and Chile signed a first-of-its-kind agreement for the Humboldt submarine cable project, connecting South America, Asia, and Oceania with 144 Tbps capacity by 2027

- May 2025: Amazon Web Services announced a USD 4 billion investment in Chilean data center infrastructure, representing the largest technology investment in the country’s history

- February 2025: Inria and Chile’s Ministry of Science launched the Franco-Chilean Binational Center on Artificial Intelligence, including shared computing infrastructure initiatives

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Chile's data center rack market as all newly manufactured, factory-assembled enclosures, open frames, and wall-mount cabinets that house IT, power, and networking gear inside colocation, hyperscale, enterprise, and edge facilities across Chile. Racks procured for test labs, broadcast closets, and refurbished or second-hand units are outside the measured universe.

Scope exclusion: Used, refurbished, and non-data-center IT closets are not part of this valuation.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls with rack OEM product managers, Chile-based colocation facility engineers, and two regional EPC contractors. These conversations clarified average racks-per-MW ratios, current lead times, and discount structures, which helped us validate secondary findings and refine utilization assumptions.

Desk Research

We began by gathering quantitative indicators from public sources such as Chile's Subsecretaria de Telecomunicaciones, the National Customs Service import database, the National Energy Commission's tariff files, and international datasets from UN Comtrade and the International Energy Agency. Trade association briefs (Uptime Institute Latin America chapter, IDCA), academic papers on high-density cooling, and credible press releases supplied context on buildouts and PPA contracts. Company 10-Ks, investor decks, and product data sheets rounded out price and specification benchmarks. Select subscription resources, including D&B Hoovers for vendor revenues and Dow Jones Factiva for project news, provided additional depth. This list is illustrative; many other secondary materials supported fact-checking and gap filling.

Market-Sizing & Forecasting

A hybrid top-down and bottom-up framework underpins our model. We first reconstructed demand from the top down by mapping commissioned IT load (MW) and applying primary-validated racks-per-MW coefficients that vary by facility type. Results were then cross-checked bottom up through sampled ASPxshipment calculations drawn from import declarations and channel checks. Key variables include annual data-center power additions, average rack density (kW), share of 48U cabinets, retail colocation vacancy, and steel price trends that influence cabinet ASPs. Multivariate regression combined with scenario analysis projects these drivers forward to 2030, while manual overrides address pipeline slippage or fast-tracked hyperscale deals.

Gap areas in supplier roll-ups, particularly for micro-edge deployments, were bridged by applying occupancy factors derived from interview feedback and CBRE absorption reports before finalizing totals.

Data Validation & Update Cycle

Every output passes a three-layer review: automatic variance checks, senior-analyst cross-audits, and a final sign-off just before publication. We refresh the model annually and trigger interim revisions if new capacity announcements, currency swings, or material policy shifts exceed preset thresholds.

Why Mordor's Chile Data Center Rack Baseline Commands Credibility for Decision-Makers

Published estimates differ because firms choose distinct scopes, density assumptions, and refresh cadences. According to Mordor Intelligence, discipline in isolating only in-country, new-build racks and in adjusting coefficients for high-density migrations keeps our figure grounded, whereas others often fold broader mechanical infrastructure or apply static densities.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 25.03 million (2025) | Mordor Intelligence | - |

| USD 26.1 million (2025) | Regional Consultancy A | Uses constant rack-density assumption and omits micro-edge sites |

| USD 50.0 million (2024) | International Analytics B | Aggregates cabinets with cooling frames and includes refurbished units |

The comparison shows that our carefully delimited scope, annual refresh cycle, and dual-approach validation give stakeholders a balanced, transparent baseline that aligns closely with on-the-ground capacity additions and real purchase transactions.

Key Questions Answered in the Report

What is the current size of the Chile data center rack market?

The Chile data center rack market size reached USD 28.51 million in 2026 and is projected to hit USD 54.59 million by 2031.

Which rack configuration leads the market in Chile?

Full racks dominate with 64.80% share, favored by hyperscale and colocation operators for standardized, high-density deployments.

How are water-stress regulations affecting data-center design?

Strict oversight is pushing operators toward liquid cooling systems, driving demand for racks compatible with immersion and direct-to-chip cooling technologies.

Why is Valparaíso attracting hyperscale investments?

The city hosts submarine-cable landings, including the Humboldt route, providing low-latency links to Asia-Pacific markets and easing coastal cooling requirements.

Page last updated on: