CBD Pet Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

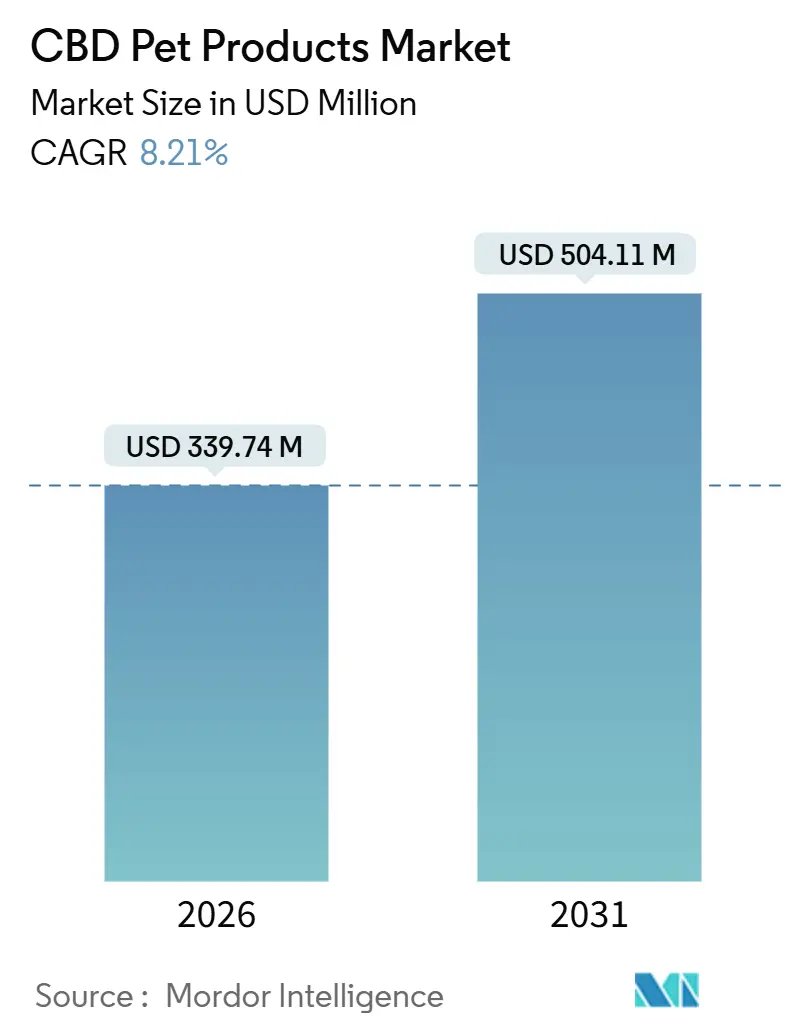

| Market Size (2026) | USD 339.74 Million |

| Market Size (2031) | USD 504.11 Million |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

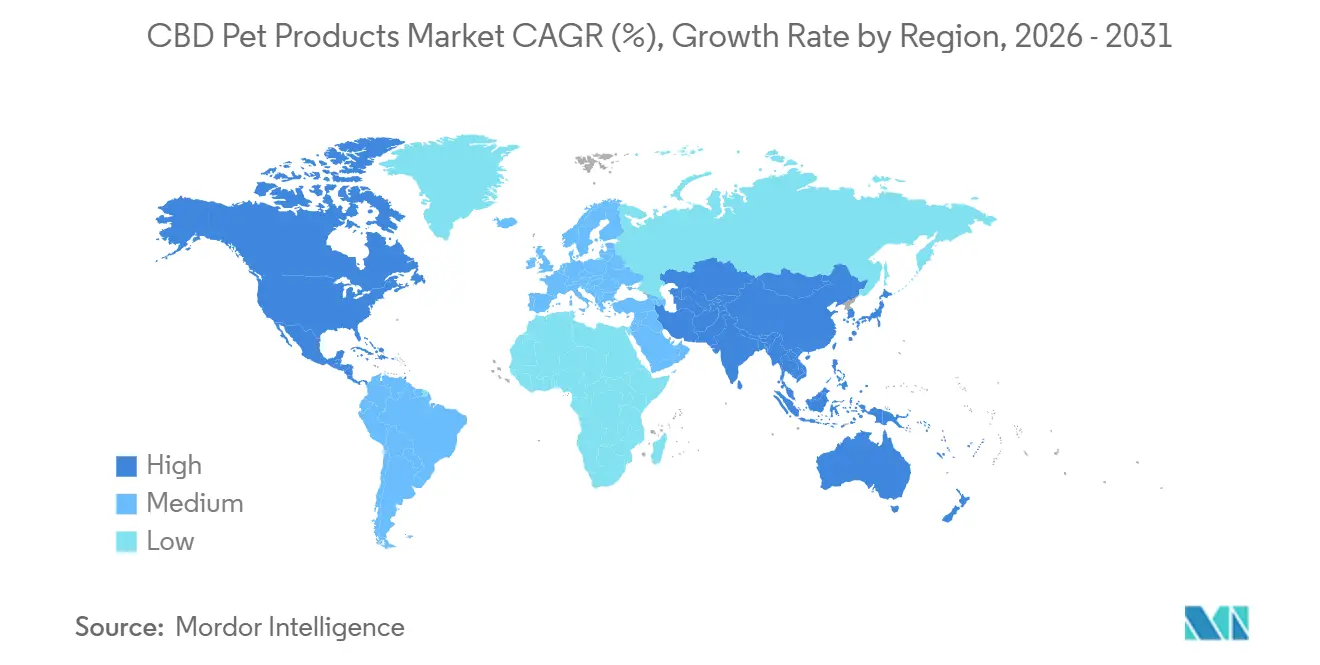

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CBD Pet Products Market Analysis by Mordor Intelligence

The CBD pet products market size is USD 339.74 million in 2026 and is projected to reach USD 504.11 million by 2031, advancing at an 8.21% CAGR over the forecast period. Robust demand arises from pet humanization, macro-policy shifts that legalized hemp derivatives, and growing clinical evidence that cannabidiol reduces pain, anxiety, and seizure frequency. Therapeutic-grade tinctures, subscription-based e-commerce, and organic formulations with third-party certificates of analysis capture the greatest attention as owners seek transparency and precise dosing. Online platforms accelerate trial rates through influencer marketing and bundled replenishment plans, trimming acquisition costs. North America holds the largest market share, while the Asia-Pacific region demonstrates the fastest growth, driven by clear legislative frameworks in Australia and increasing discretionary income among pet owners in China and India.

Key Report Takeaways

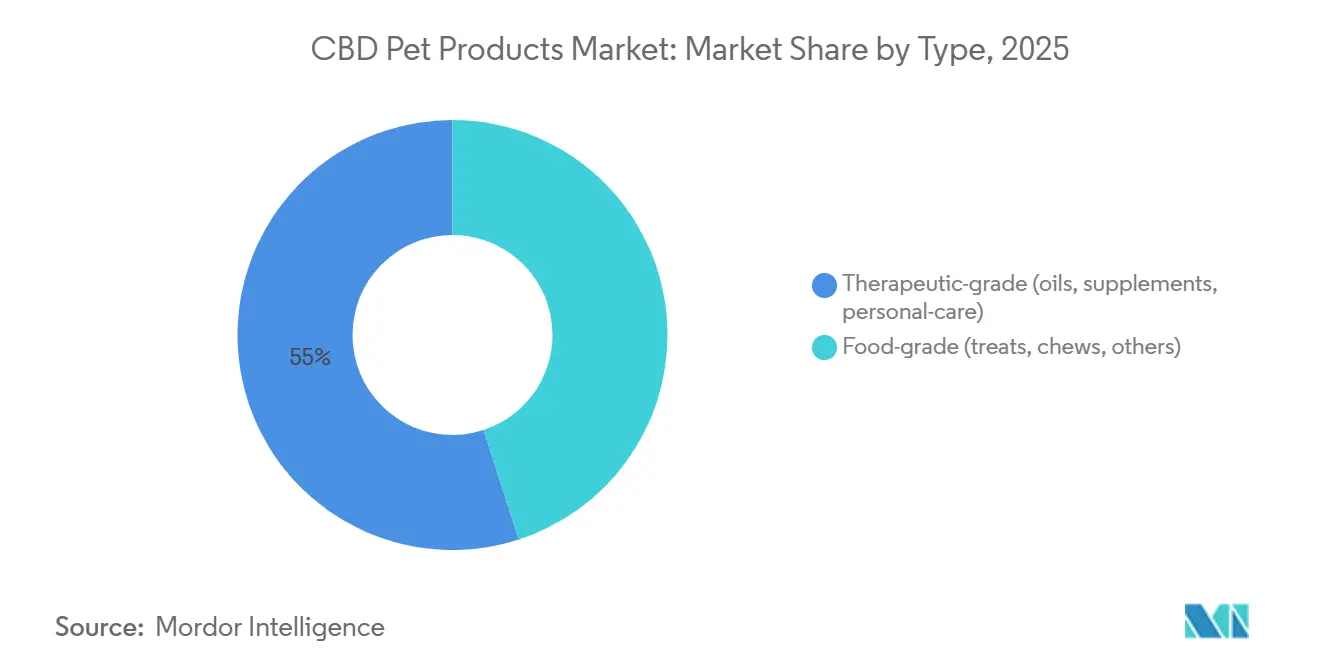

- By type, therapeutic-grade oils accounted for 55% of the CBD pet products market share in 2025 and are projected to grow at a 15.4% CAGR through 2031.

- By animal type, dogs accounted for 61% of the CBD pet products market size in 2025, while cats are projected to grow at a CAGR of 14.8% through 2031.

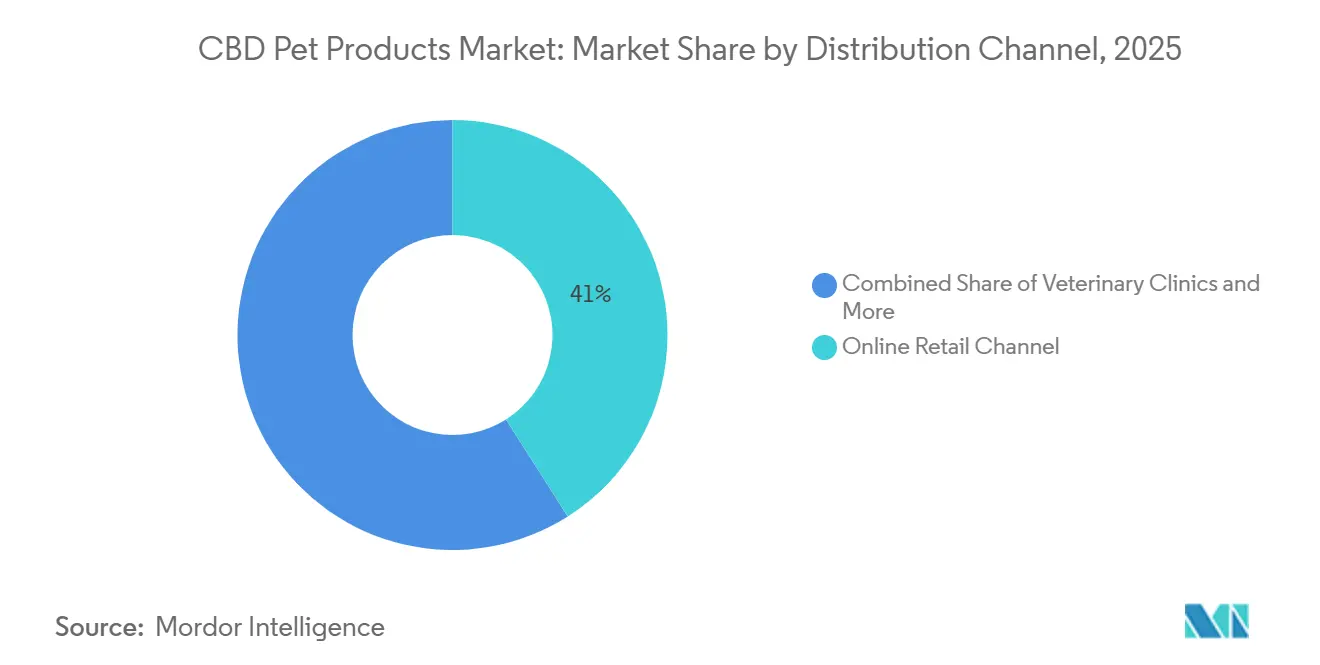

- By distribution channel, online retail accounted for 41% of the CBD pet products market size in 2025, and is advancing at an 18.7% CAGR through 2031.

- By geography, North America accounted for 48% of the CBD pet products market size in 2025, while the Asia-Pacific region is projected to rise at a 15.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CBD Pet Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of chronic disorders in pets | +2.30% | North America and Europe | Medium term (2-4 years) |

| Rising pet ownership and humanization trends | +3.10% | Global urban centers | Long term (≥4 years) |

| Increased focus and expenditure on pet health and wellness | +2.70% | North America and Western Europe | Long term (≥4 years) |

| Expanding retail and e-commerce channels that allow CBD sales | +2.40% | Americas, Europe, and Australia | Short term (≤2 years) |

| Veterinary endorsements backed by emerging clinical evidence | +1.50% | North America and Europe | Medium term (2-4 years) |

| Low-THC veterinary drug legislation in key markets | +1.80% | United States, Canada, Australia, Germany, and the United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Chronic Disorders in Pets

Degenerative joint disease, epilepsy, and anxiety now afflict a sizable share of aging companion animals, prompting sustained demand for non-pharmaceutical interventions[1]Source: American Holistic Veterinary Medical Association, “2024 Member Survey,” AHVMA.ORG. Owners worry about the hepatotoxicity of long-term NSAID use and are turning to cannabinoid-based solutions that interact with CB1 and CB2 receptors. Clinical trials reported a 35% pain-score reduction in osteoarthritic dogs given full-spectrum CBD at 2 mg/kg twice daily, without liver-enzyme elevation. These outcomes nurture veterinary confidence and widen prescriptive adoption. The trend is especially evident in North America, where 40% of dogs aged seven years or older exhibit chronic arthritis symptoms. Parallel patterns emerge across Europe, positioning CBD as a bridge therapy for refractory conditions. The resulting uptick in daily dosing drives repeat purchases and strengthens lifetime customer value.

Rising Pet Ownership and Humanization Trends

In 2024, 67% of American households owned at least one pet, marking a significant increase from 2021[2]Source: American Veterinary Medical Association, “U.S. Pet Ownership Statistics,” AVMA, AHVMA.ORG. Millennials and Gen Z lead this expansion and treat animals as family, allocating monthly budgets of USD 60-120 for CBD treats in lieu of generic supplements costing one-third as much. Comparable sentiment in Germany, where pet ownership penetration reached 47% in 2024, reinforces tolerance for premium pricing. These consumers actively research ingredients, prefer organic hemp, and reward brands that publish batch-level potency tests. Social media amplifies personal testimonials, normalizing cannabidiol as a preventive wellness tool. As owners adopt adaptogen habits for their pets, demand for USDA-certified CBD tinctures increases across metropolitan areas worldwide.

Increased Focus and Expenditure on Pet Health and Wellness

Pet owners in North America spent significantly on veterinary care and wellness products during 2024, with preventive supplements accounting for a notable share of this spending. Growth aligns with rising pet-insurance penetration in the United States, with policies increasingly reimbursing alternative therapies such as CBD. Preventive positioning is critical, as brands market oils for daily maintenance of joint mobility and cognitive function before clinical symptoms appear. Insured owners perceive lower out-of-pocket risk, raising conversion rates. The dynamic is mirrored in Western Europe, where wellness subscriptions bundle CBD chews with routine flea protection, reinforcing monthly order cadence. Consequently, the CBD pet products market experiences stable baseline demand, insulating suppliers from seasonal volatility.

Expanding Retail and E-Commerce Channels That Allow CBD Sales

Amazon’s 2024 decision to list hemp-derived CBD for pets unlocked access to 200 million Prime subscribers. Chewy promptly followed, creating a curated storefront that highlights third-party lab reports, improving brand credibility. Brick-and-mortar giants Petco and PetSmart expanded their CBD assortments after favorable state guidelines reduced compliance uncertainty across multiple markets. Omnichannel presence compresses discovery barriers, allowing owners to add CBD products to existing shopping baskets rather than seeking specialty stores. Lower fulfillment costs and subscription discounts convert first-time buyers into repeat customers. The rapid scale achievable through online distribution positions digital-native brands to challenge legacy veterinary-clinic channels and capture incremental share in the CBD pet products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of premium CBD pet products | -1.40% | Global price-sensitive regions | Short term (≤2 years) |

| Stringent regulatory requirements for product approval | -1.80% | United States and Europe | Long term (≥4 years) |

| Quality and consistency issues from lack of standards | -1.20% | Global | Medium term (2-4 years) |

| Limited veterinarian education on cannabinoid pharmacokinetics | -0.90% | South America, Africa, parts of Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium CBD Pet Products

Full-spectrum organic CBD oils retail at USD 0.15-0.25 per milligram, roughly triple the cost of glucosamine-chondroitin supplements, creating affordability barriers in emerging economies. A month-long CBD regimen for a medium-sized dog can be costly, positioning cannabidiol as a discretionary luxury rather than a staple. Upstream expenses include certified-organic cultivation, supercritical CO₂ extraction, and batch-level contaminant screening, all of which contribute significantly to production costs. When regulators do not mandate testing, price-sensitive owners often choose cheaper, uncertified products or abandon CBD altogether. Consequently, penetration remains low across South America and Africa, where disposable incomes are constrained. Persistent cost differentials in the CBD pet products market temper volume growth despite rising global awareness.

Stringent Regulatory Requirements for Product Approval

The Food and Drug Administration lacks a defined pathway for CBD pet products, creating compliance ambiguity that invites warning letters and stifles marketing claims[3]Source: U.S. Food and Drug Administration, “Regulation of Cannabis and Cannabis-Derived Products,” FDA.GOV. European Medicines Agency novel-food dossiers require extensive toxicology and stability studies, favoring well-capitalized firms and delaying entry for smaller brands. Even Australia’s recently streamlined Schedule 4 route mandates pharmacokinetic submissions. Lengthy approval timelines consume capital and create uncertainty that may deter investors. Firms unable to meet data requirements risk delisting or forced reformulation. These regulatory frictions slow SKU refresh cycles and limit the breadth of therapeutic indications offered within the CBD pet products industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Therapeutic-Grade Oils Drive Premium Positioning

Therapeutic-grade oils captured 55% of the 2025 value, followed by food-grade treats, while personal-care topicals accounted for the remainder. Concentrated tinctures with 300-1,500 mg cannabidiol per bottle lead the CBD pet products market because they allow weight-based dose titration. Food-grade chews maintain share by masking hemp taste, yet they suffer lower bioavailability. Topicals remain niche but appeal to owners treating localized dermatitis without oral administration.

Therapeutic-grade oils will post a 15.4% CAGR through 2031, the fastest within the category, propelled by nano-emulsion technologies that cut onset time to 15 minutes. Food-grade treats are estimated to grow strongly, supported by new flavors and soft-chew formats. Topicals are also projected to expand steadily as veterinary dermatology increasingly embraces cannabinoid-infused shampoos and balms.

By Animal Type: Canine Dominance Faces Feline Disruption

Dogs contributed 61% of 2025 revenue, followed by cats, while other pets contributed a smaller share. Large-breed dogs consume more CBD per dose to manage osteoarthritis and anxiety, anchoring canine leadership in the CBD pet products market. Cats remained below one-third share because early coconut-oil carriers impaired palatability.

Cats will expand at a 14.8% CAGR to 2031, outstripping other species after fish-oil-based tinctures improved acceptance. Dogs are projected to grow strongly, supported by increasing insurance coverage for chronic pain management. Other pets, including horses and rabbits, are also estimated to expand steadily, driven by demand from performance-horse segments and the growth of specialty e-commerce offerings for exotic pets.

By Distribution Channel: E-Commerce Rewrites Access Economics

Online retail held 41% of 2025 spend, and veterinary clinics, retail pharmacies, and pet stores represent significant distribution channels. Digital channels, however, dominate the CBD pet products market by offering subscription discounts, rapid consumer education, and easy display of product certifications. Clinics leverage professional trust but face stocking hesitancy. Physical pet stores benefit from impulse buys but must comply with varying state rules.

Online retail will surge at 18.7% CAGR to 2031, far ahead of offline formats. Veterinary clinics are estimated to grow strongly as greater legal clarity boosts in-house sales. Retail pharmacies and pet stores are likely to trail, constrained by ongoing regulatory checks and increasing competition from direct-to-consumer brands.

Geography Analysis

North America generated 48% of 2025 revenue and is estimated to continue expanding at a strong pace. United States households spend an average of USD 1,480 per pet annually and readily adopt organic CBD oils endorsed by veterinarians. Canada’s 2024 Cannabis Act amendments removed pre-market hurdles for hemp-derived pet products, letting provincial chains stock CBD alongside traditional supplements. Mexico is estimated to issue formal guidelines by 2027, unlocking pent-up demand currently served through gray imports.

Asia-Pacific is forecast to grow at 15.1% CAGR, the highest among all regions. Australia reclassified low-THC CBD as Schedule 4 in 2025, enabling prescription fulfillment through pharmacies and fueling immediate volume gains. China’s draft hemp-supplement regulations signal market opening in a country with rising middle-class expenditure and pet population. India awaits Food Safety and Standards Authority clarity, yet rising urban pet ownership is flagging a latent market opportunity once rules crystallize.

Europe will advance at a strong pace. Germany, the United Kingdom, France, and Spain together represent the majority of regional spend. Stricter Veterinary Medicines Directorate rules in the United Kingdom slow product launches but elevate overall quality standards, while Germany’s guidance excluding low-THC hemp extracts from narcotic regulations streamlines distribution. South America is also estimated to expand steadily, led by Brazil’s over-the-counter approval framework for CBD pet oils. Africa remains a nascent market, while South Africa’s prescription-only stance confines distribution primarily to licensed veterinary practices.

Competitive Landscape

The CBD pet products market is fragmented. Charlotte’s Web, cbdMD (Paw CBD), Pet Releaf, Honest Paws, and Holista LLC are key players, leveraging strategies such as vertically integrated hemp farms, brand recognition, THC-free broad-spectrum extracts, organic certification, and functional botanicals like L-theanine.

Strategic themes include vertical integration to control quality, third-party testing to build trust, and veterinary partnerships to access clinical endorsement. Pet Releaf became one of the first suppliers to offer USDA-certified organic hemp across the entire supply chain in 2025, enabling placement in natural product retailers. HolistaPet collaborated with Colorado State University on feline pharmacokinetic studies that underpin dosing guides, fostering veterinary acceptance in 2024. Nano-emulsion and microencapsulation technologies spread across portfolios, delivering water-soluble formats that improve onset time and flavor masking.

Mergers and acquisitions accelerate scale. Swedencare’s acquisition of NaturVet’s hemp division adds USD 8,500 retail doors for European brands seeking North American entry in 2025. Competitive intensity is projected to rise as human-CBD incumbents enter the pet arena, pressing smaller labels to differentiate via breed-specific formulations or subscription services.

CBD Pet Products Industry Leaders

Charlotte's Web, Inc.

cbdMD (Paw CBD)

Pet Releaf

Honest Paws

Holista LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fusion CBD Products launched two new CBD pet products, Wiggles and Paws Dog Treats, and Wiggles and Paws Pet Drops. The drops are unflavored, while the treats are crafted using apple sauce, almond butter, and coconut flour. These products aim to promote healthy aging by alleviating arthritis symptoms and reducing anxiety and reactivity.

- February 2025: Kradle has expanded its product portfolio by introducing its first line of cat wellness products, featuring CBD formulations. The range includes three lickable supplements designed to address common feline health concerns, urinary health, skin and allergy support, and hairball control. Each product is salmon-flavored to improve palatability, making daily supplementation easier for pet owners.

- June 2024: Awaken CBD expanded its product line with CBD-infused pet treats and drops designed to reduce stress and promote calmness in dogs. This product introduction strengthened the company's presence in the pet care segment of the CBD market.

- March 2024: CV Sciences, Inc. launched CBD-infused chews for pets, including +PlusCBD Pet Hip and Joint Health Chews for dogs and +PlusCBD Pet Calming Care Chews. These products address common health issues in dogs, particularly joint pain and anxiety.

Global CBD Pet Products Market Report Scope

Cannabidiol (CBD) is a chemical in the Cannabis sativa plant, also known as cannabis or hemp. For the scope of the study, the food-grade use of CBD in pet products is limited to treats, chews, and others, while the therapeutic-grade use is limited to pet supplements, pet CBD oils, and pet personal care products. The CBD Pet Products Market is segmented by Type (Food-grade and Therapeutic-grade), Animal Type (Dog, Cat, and Other Pets), Distribution Channel (Online Retail Channels, Retail Pharmacies, Veterinary Clinics, and Other Distribution Channels), and Geography (North America, Europe, Asia-Pacific, South America, and Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Food-grade |

| Therapeutic-grade |

| Dog |

| Cat |

| Other pets |

| Online retail channel |

| Retail pharmacies and pet stores |

| Veterinary clinics |

| Other channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Africa | South Africa |

| Rest of Africa |

| By Type | Food-grade | |

| Therapeutic-grade | ||

| By Animal Type | Dog | |

| Cat | ||

| Other pets | ||

| By Distribution Channel | Online retail channel | |

| Retail pharmacies and pet stores | ||

| Veterinary clinics | ||

| Other channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the CBD pet products market today and what is its growth outlook?

The CBD pet products market size is USD 339.74 million in 2026 and is forecast to reach USD 504.11 million by 2031 at an 8.21% CAGR.

Which product type leads sales in cannabidiol formulations for pets?

Therapeutic-grade oils hold 55% of 2025 revenue due to precise dosing and faster bioavailability versus treats and topicals.

Why are online channels gaining such fast momentum?

Amazon and Chewy now allow hemp-derived CBD listings, letting brands reach millions of shoppers and grow online revenue at an 18.7% CAGR through 2031.

What region is anticipated to offer the highest growth opportunity?

Asia-Pacific is projected to post a 15.1% CAGR through 2031 as Australia, China, and India ease regulatory barriers and pet ownership climbs.

Page last updated on: