Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

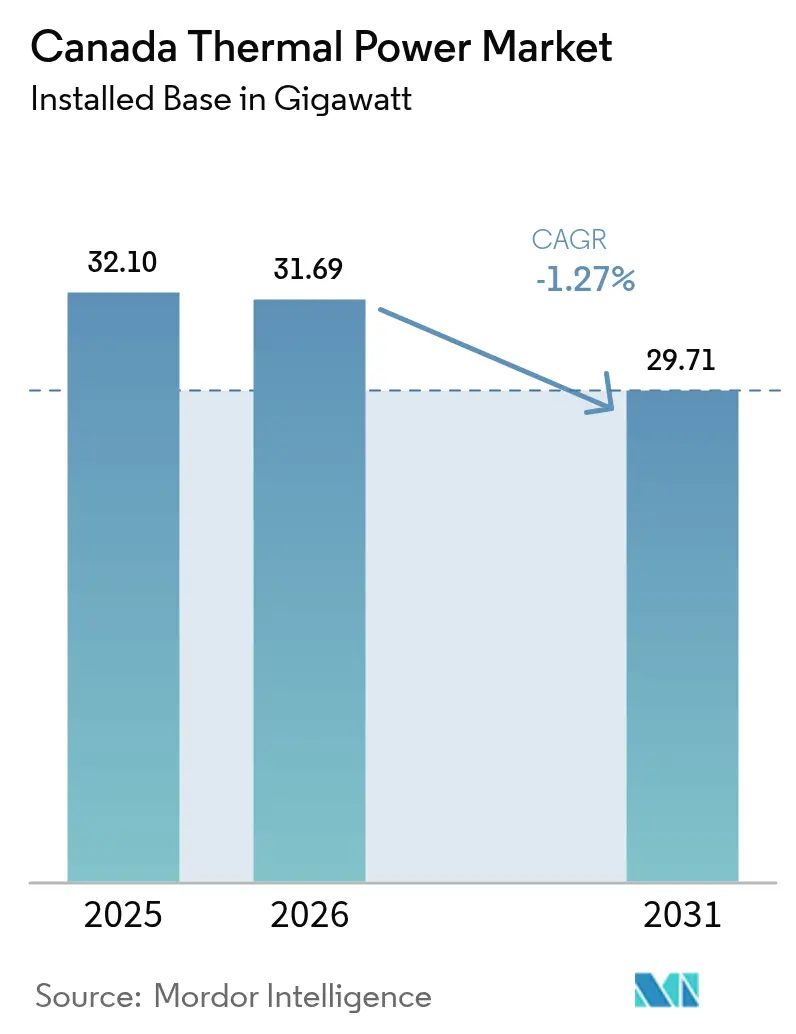

| Base Year Market Size (2025) | 32.10 gigawatt |

| Market Volume (2026) | 31.69 gigawatt |

| Market Volume (2031) | 29.71 gigawatt |

| Growth Rate (2026 - 2031) | -1.27% CAGR |

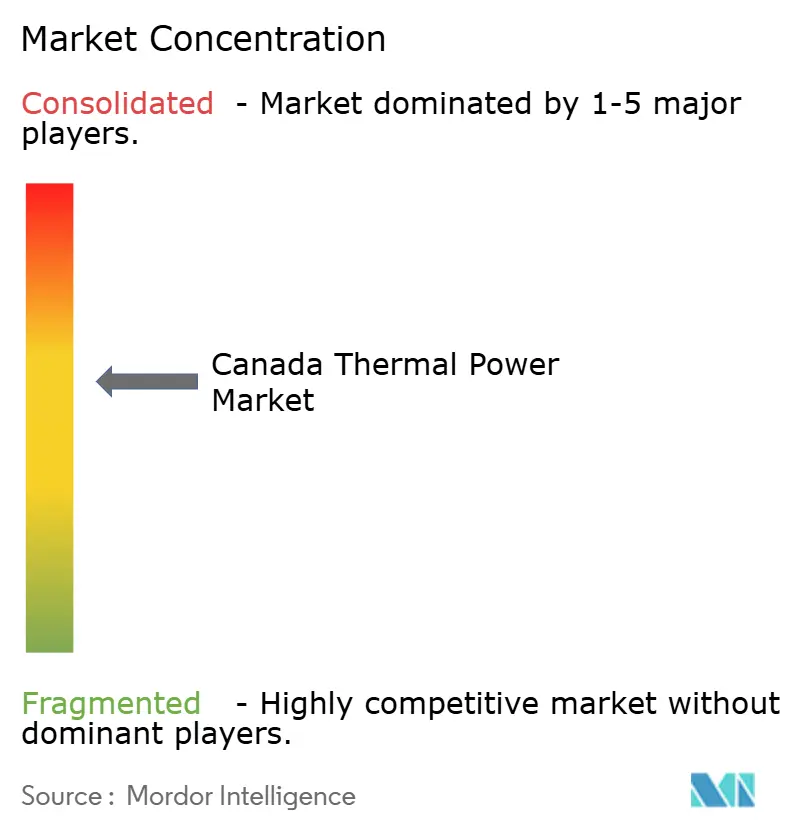

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Thermal Power Market Analysis by Mordor Intelligence

Canada Thermal Power Market size in 2026 is estimated at 31.69 gigawatt, growing from 2025 value of 32.10 gigawatt with 2031 projections showing 29.71 gigawatt, growing at -1.27% CAGR over 2026-2031.

Coal’s accelerated retirement under the federal phase-out mandate and the 65 tCO₂/GWh ceiling embedded in the 2024 Clean Electricity Regulations are the core shrinkage catalysts, yet natural-gas combined-cycle upgrades cushion the headline decline by lifting fleet efficiency and lowering per-unit emissions. Alberta’s deregulated power market, British Columbia’s LNG-driven load growth, and Saskatchewan’s post-coal reliability gap collectively underpin replacement demand, while federal investment and carbon-capture tax credits tilt project economics toward gas-fired assets with CCS. Industrial cogeneration additions inside the oil sands, fast-start peakers chasing capacity payments, and hydrogen-ready turbines that future-proof plants against rising carbon prices are the primary opportunity nodes. Meanwhile, corporate renewable PPAs, expanding Québec intertie capacity, and rising carbon costs compress merchant spark spreads and reinforce the shift from baseload to flexibility-focused revenue streams.

Key Report Takeaways

- By fuel type, natural gas captured 46.85% of Canada thermal power plant market share in 2025, and the segment is forecast to expand at a 2.66% CAGR through 2031.

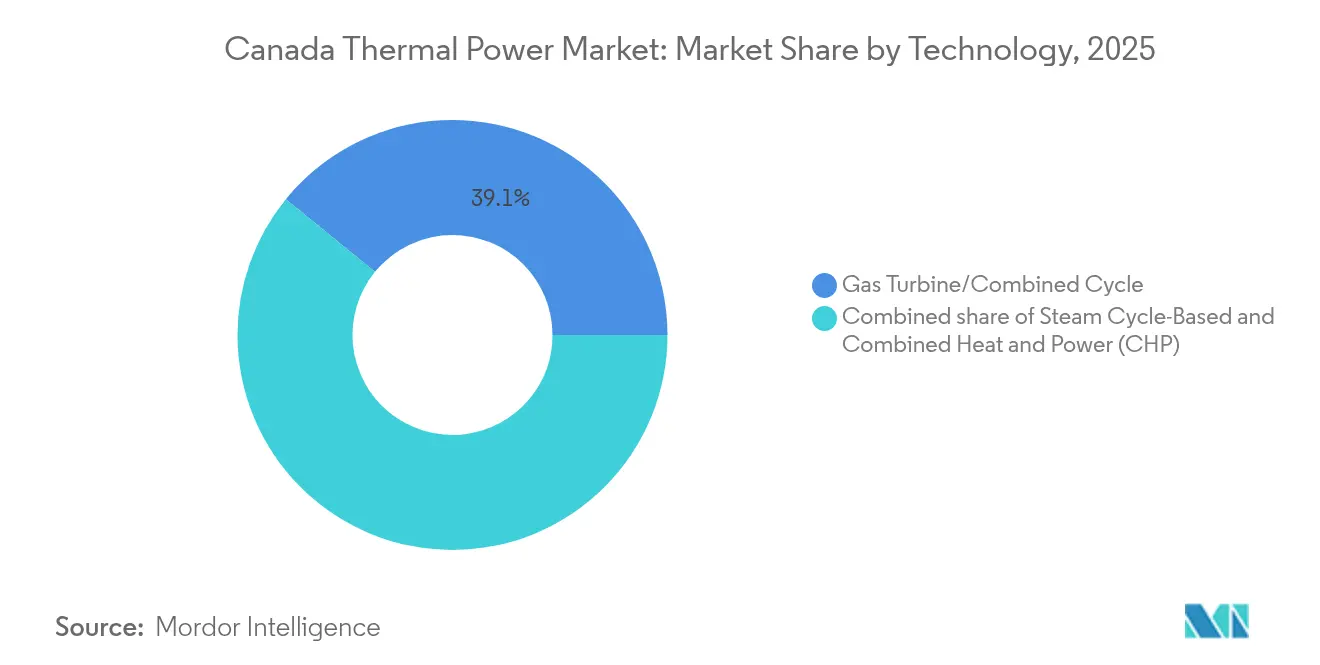

- By technology, gas turbine and combined-cycle units held 39.12% share of the Canada thermal power plant market size in 2025 and are expected to climb at a 2.02% CAGR up to 2031.

- By combustion method, turbine-based systems accounted for 59.15% share of the Canada thermal power plant market size in 2025 and will advance at a 2.55% CAGR between 2026 and 2031.

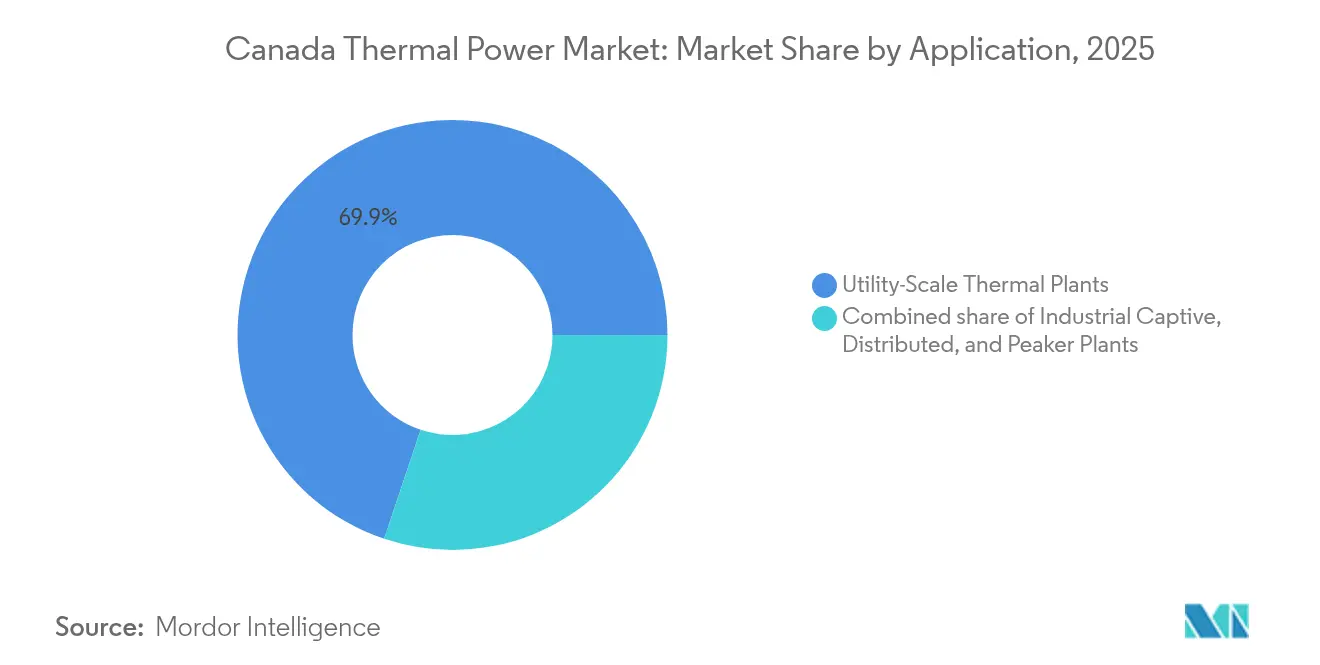

- By application, industrial captive power plants posted 15.35% of the Canada thermal power plant market share in 2025 and are forecast to record the fastest 3.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Thermal Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging coal fleet replacements with high-efficiency CCGT plants | +2.1% | Alberta, Saskatchewan | Medium term (2–4 years) |

| Increasing grid-reliability concerns amid rising variable renewables | +1.4% | Alberta, Ontario | Short term (≤ 2 years) |

| LNG export growth spurring western-Canada gas-fired capacity | +0.9% | British Columbia, northern Alberta | Long term (≥ 4 years) |

| Provincial carbon-credit floor catalyzing efficiency retrofits | +0.6% | Alberta, Saskatchewan | Medium term (2–4 years) |

| Small modular reactor pilots reshaping long-term baseload mix | +0.3% | Ontario, Saskatchewan, New Brunswick | Long term (≥ 4 years) |

| Oil-sands cogeneration expansions for steam & power self-sufficiency | +0.8% | Alberta oil sands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Aging Coal Fleet Replacements With High-Efficiency CCGT Plants

Ottawa’s 2030 coal ban compressed a decade of retirements into six years, forcing utilities to swap 8 GW of coal with dispatchable alternatives.[1]Canada Energy Regulator, “Canada’s Power Generation Outlook,” cer-rec.gc.ca Alberta finalized its coal exit in June 2024, and Saskatchewan shuttered Boundary Dam Units 4-6 the same year, leaving a reliability gap that only modern CCGT capacity can close. Capital Power’s 1,857 MW Genesee repowering, online since December 2024, sets a 64% thermal-efficiency benchmark and slices emissions intensity by 60%. The Clean Electricity Regulations permit compliant gas units to run to 2050, locking in 25-year revenue visibility and stimulating a USD 2 billion project pipeline. Developers are also designing new turbines with carbon-capture tie-ins or hydrogen co-fire options to future-proof assets against stricter post-2035 rules.

Increasing Grid-Reliability Concerns Amid Rising Variable Renewables

Alberta added more than 4 GW of wind and solar between 2023 and 2024, lifting renewable penetration above 20% on peak days and producing sub-hourly frequency swings that exposed the AESO to reserve shortfalls.[2]Alberta Electric System Operator, “2024 Market Statistics,” aeso.ca The province’s delayed capacity market, now scheduled for 2027, aims to procure 4,500 MW of firm supply, with aeroderivative gas turbines favored for their ten-minute start capability. Ontario faces a parallel 3,000 MW supply gap by 2027 as Pickering nuclear retires and EV-driven load accelerates, pushing the IESO to contract fast-ramp peakers and batteries. January 2024 cold snaps saw Alberta pool prices spike to CAD 999/MWh, reinforcing the economic case for quick-start thermal flexibility.

LNG Export Growth Spurring Western-Canada Gas-Fired Capacity

LNG Canada’s 14 Mtpa Phase 1 terminal, operational since October 2024, devours roughly 300 MW of electricity and anchors a future requirement of 500-700 MW once Phase 2 doubles liquefaction volumes. Joint-venture partners are contemplating on-site cogeneration to trim bought power, a model mirrored by Woodfibre and Cedar LNG. Rising petrochemical investments in Alberta’s Industrial Heartland add another demand node, with pipeline-adjacent merchant CCGTs emerging as the lowest-cost supply choice.

Provincial Carbon-Credit Floor Catalyzing Efficiency Retrofits

Alberta’s TIER scheme generated CAD 500 million of credit trades in 2024 and sets declining intensity baselines that reward CCGT efficiency upgrades or CCS integration. Saskatchewan’s OBPS mirrors TIER and, alongside a federal CCUS investment tax credit covering up to 50% of capture equipment, narrows payback for large-scale retrofits such as Capital Power’s 2 Mtpa Genesee CCS unit.[3]Capital Power, “Genesee Repowering Project Update,” capitalpower.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal 2030 coal phase-out mandate | –3.2% | Alberta, Saskatchewan, Nova Scotia | Short term (≤ 2 years) |

| Escalating federal & provincial carbon pricing | –1.8% | National (highest in Alberta, Saskatchewan) | Medium term (2–4 years) |

| Corporate renewable PPAs eroding baseload demand | –1.1% | Alberta, Ontario | Medium term (2–4 years) |

| Inter-provincial transmission favoring hydro imports from Québec | –0.9% | Ontario, New Brunswick | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal 2030 Coal Phase-Out Mandate

The coal ban removes 8 GW of capacity by end-2029, stranding CAD 2-3 billion in book value and triggering 8–12% retail-rate hikes in Alberta and Saskatchewan.

Escalating Federal & Provincial Carbon Pricing

The industrial carbon floor climbs toward CAD 170/tonne by 2030, inflating unabated gas-plant variable costs by CAD 68-77/MWh and narrowing merchant spark spreads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Natural Gas Extends Its Lead As Coal Exits

Natural gas-fired assets held 46.85% of the Canada thermal power plant market in 2025 and will climb at a 2.66% CAGR as CCGT replacements fill the coal vacuum. Coal capacity will collapse to negligible relevance by 2029, while oil-fired generation in Atlantic Canada and remote communities retreats below 5% share, squeezed by hydro imports and battery storage. Western Canada's abundant Montney supply anchors gas prices below CAD 3/GJ, keeping dispatch economics competitive even under rising carbon costs. The natural-gas slice of Canada's thermal power plant market size is projected at 17.53 GW in 2031, equivalent to 58.98% of fleet capacity. Hydrogen-ready turbines and CCUS tax incentives provide a hedge against future carbon tightening.

Regional supply dynamics reinforce the trend. Alberta's post-coal demand plus LNG Canada's load in British Columbia lock in 1.5-2 GW of greenfield gas builds through 2030. Oil-fired peakers at Coleson Cove and maritime diesel units face a rapid utilization decline once Churchill Falls exports scale. With no new coal or heavy-oil projects in the pipeline, natural gas secures the only positive growth path within the fuel mix.

By Technology: CCGT Efficiency Sets The Competitive Bar

Gas turbine and combined-cycle units made up 39.12% of installed capacity in 2025 and will advance at a 2.02% CAGR, buoyed by 64% thermal-efficiency benchmarks set by GE 7HA.03 turbines at Genesee. The Canada thermal power plant market size tied to CCGT technology is expected to reach 13.88 GW in 2031. CHP systems linked to oil-sands operations, although smaller, deliver the fastest 2.86% CAGR because waste-heat recovery pushes plant thermal efficiency past 75% and qualifies for provincial TIER credits. Steam-cycle coal stations, down to 2 GW by 2025, are on an irreversible exit trajectory.

Digital-twin analytics reduce forced outages and extend maintenance cycles, slicing LCOE by up to CAD 5/MWh. Aeroderivative simple-cycle units plug peak gaps and win capacity auctions thanks to zero-to-full-load ramps under ten minutes. Older 55-58% CCGTs become marginal unless retrofitted with dry-low-NOx combustors, hydrogen capability, or CCS modules.

By Combustion Method: Turbine-Based Systems Outpace Legacy PF

Turbine-based firing methods controlled 59.15% of installed capacity in 2025 and will grow at a 2.55% CAGR as pulverized-fuel combustion shrinks from 40.85% share to near zero by 2029. Turbine-based capacity within the Canada thermal power plant market size will expand from 18.98 GW in 2025 to 22.05 GW in 2031. Fluidized-bed installations linger in niche biomass and CCS pilots, while internal-combustion engines recede under renewable-plus-storage microgrids in the North. Hydrogen co-firing certification at 50% blend ratios future-proofs large turbines, albeit with cost barriers until green hydrogen drops below CAD 3/kg.

Operational agility defines the method split. Aeroderivative turbines assure ten-minute starts, enabling ancillary-service revenues during renewable volatility, whereas PF boilers need multiple hours, eroding marketability under new capacity market rules. Cap-ex for PF-to-gas conversions rivals greenfield CCGT builds, sealing PF’s phase-out.

By Application: Industrial Captive Power Surges Ahead

Utility-scale stations commanded a 69.85% share in 2025 but hold flat outlooks as corporate PPAs siphon baseload loads. Industrial captive plants, now 15.35%, will post a 3.19% CAGR on the back of oil-sands cogeneration, lifting their share to 19.62% by 2031. Captive additions of 1.2-1.4 GW, led by Suncor and Imperial Oil, push the Canada thermal power plant market size for industrial power toward 5.86 GW in 2031. Distributed plants under 50 MW fade in urban centers where rooftop PV and batteries undercut gas CHP, yet remain viable for data centers, hospitals, and campuses that prize resilience.

Peaker projects flourish: Alberta’s 2027 capacity auction and Ontario’s annual IESO procurements pay CAD 50-80/kW-year, strengthening investment cases for fast-start turbines. Merchant operators such as ENMAX and ATCO already extract 15-25% capacity factors from peaker fleets, monetizing reserve and black-start services during renewable troughs.

Geography Analysis

Alberta remains the epicenter, owning 44.70% of Canada's thermal power plant market capacity in 2025. Coal’s June 2024 exit and a deregulated pool structure fuel a 2 GW queue of CCGT builds, while peak-period pool prices above CAD 999/MWh validate fast-start gas economics. TIER credit liquidity, worth CAD 500 million in 2024, offsets carbon-price escalation and accelerates CCS retrofits.

Saskatchewan’s market contracts as 1.2 GW of coal shut in 2024, yet Aspen CCGT and prospective SMRs plug part of the gap. Ontario pivots to nuclear refurbishments and 2 GW of firm hydro imports from Québec, constraining gas dispatch mainly to peaking duty. British Columbia’s northeast emerges as a growth pocket, where LNG Canada’s rising load could trigger 700 MW of gas builds post-2025. Atlantic Canada leans on hydro imports via Hydro-Québec’s CAD 10 billion intertie, eroding thermal utilization at Coleson Cove below 30%. Manitoba and Québec, both hydro-dominant, keep thermal to diesel backup in remote grids.

Competitive Landscape

Competitive Landscape

Provincial incumbents, TransAlta, Capital Power, Ontario Power Generation, SaskPower, and Emera, control around 60% of total capacity, but divestitures and strategy pivots generate churn. TransAlta’s CAD 1.0 billion Sundance sale to Heartland in March 2024 funds renewable and battery moves, while Capital Power offloaded the 144 MW Joffre cogeneration unit to Pembina and poured proceeds into Genesee CCS.[4]TransAlta Corporation, “Asset Portfolio Review 2024,” transalta.com Alberta’s merchant arena adds competitive tension, with Maxim, ATCO, and ENMAX battling on dispatch economics against carbon costs nearing CAD 95/tonne.

Oil-sands producers emerge as embedded-generation challengers; Suncor, Imperial Oil, and CNRL collectively add over 1 GW of cogeneration and bypass grid suppliers. Technology leadership swings to operators of GE 7HA.03 and Siemens D-Series turbines, which enjoy 64% efficiency and digital-twin availability gains that older plants struggle to match. Federal CCUS and Clean Electricity credits tilt the playing field toward balance-sheet-strong incumbents able to underwrite capture units or hydrogen pilots, potentially squeezing out thinly capitalized merchants by 2030.

Regulatory certainty under the Clean Electricity Regulations secures 25-year runways for compliant gas assets but obliges 65 tCO₂/GWh or better performance from 2035, effectively making CCS or hydrogen readiness a license to operate. White-space investment concentrates in Alberta peakers, Saskatchewan CCGTs, and industrial CHP, where dual heat-power revenues sweeten project IRRs.

Canada Thermal Power Industry Leaders

SaskPower International Inc

TransAlta Corporation

Ontario Power Generation Inc

Capital Power Corporation

Emera Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TransAlta finalized the CAD 542 million acquisition of Heartland Generation, cementing its leadership in Alberta’s gas fleet.

- April 2025: Capital Power closed its purchase of Hummel and Rolling Hill stations, expanding its Alberta gas portfolio and advancing the Atlas Carbon Storage Hub with Shell Canada.

- March 2025: The federal government allocated CAD 304 million for SMR development across Saskatchewan, Alberta, and Ontario, including CAD 54 million for SaskPower’s pre-development work.

- February 2025: Pembina Pipeline acquired a 50% stake in Greenlight Electricity Centre Partnership with Kineticor to build up to 1,800 MW of gas-fired capacity with carbon capture, targeting 2027 connection.

Canada Thermal Power Market Report Scope

Thermal power plants are power stations that transform heat energy into electric energy. Burning oil, liquid natural gas (LNG), nuclear fuel, and other materials results in thermal power, which turns generators and generates electricity. This generation usually provides electricity because it can cater to various power demands from industrial, commercial, and residential customers.

The Canada thermal power market is segmented by fuel type, technology, combustion method, application, and geography. By fuel type, the market is segmented into coal-fired, natural gas-fired, and oil-fired. By technology, the market is segmented into steam cycle-based, gas turbine/combined cycle, and combined heat and power (CHP). By combustion method, the market is segmented into pulverized fuel (PF) combustion, fluidized bed, gasification, internal combustion engines, and turbine-based. By application, the market is segmented into utility-scale, industrial captive, distributed, and peaker. For each segment, market sizing and forecasts have been done based on installed capacity (MW).

By Fuel Type

| Coal-Fired Power Plants |

| Natural Gas-Fired Power Plants |

| Oil-Fired Power Plants |

By Technology

| Steam Cycle-Based |

| Gas Turbine/Combined Cycle |

| Combined Heat and Power (CHP) |

By Combustion Method

| Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion |

| Gasification |

| Internal Combustion Engines |

| Turbine-Based Combustion |

By Application

| Utility-Scale Thermal Plants |

| Industrial Captive Power Plants |

| Distributed Thermal Plants |

| Peaker Plants |

| By Fuel Type | Coal-Fired Power Plants |

| Natural Gas-Fired Power Plants | |

| Oil-Fired Power Plants | |

| By Technology | Steam Cycle-Based |

| Gas Turbine/Combined Cycle | |

| Combined Heat and Power (CHP) | |

| By Combustion Method | Pulverized Fuel (PF) Combustion |

| Fluidized Bed Combustion | |

| Gasification | |

| Internal Combustion Engines | |

| Turbine-Based Combustion | |

| By Application | Utility-Scale Thermal Plants |

| Industrial Captive Power Plants | |

| Distributed Thermal Plants | |

| Peaker Plants |

Key Questions Answered in the Report

What capacity did the Canada thermal power plant market add or retire in 2024?

The fleet shed 3.8 GW of coal in Alberta and 1.2 GW in Saskatchewan while adding 1.9 GW of new CCGT at Genesee.

Which province currently has the largest share of Canada's operating thermal capacity?

Alberta, with about 44.70% of installed gas-fired capacity after its complete coal exit.

How will the Clean Electricity Regulations affect new gas projects after 2035?

Gas plants must meet or offset a 65 tCO?/GWh intensity cap, steering developers toward CCS integration or hydrogen blends to stay compliant.

Where are the fastest-growing captive power opportunities?

Oil-sands sites in northern Alberta are adding more than 1 GW of high-efficiency cogeneration by 2030.

What incentives support carbon-capture retrofits on Canadian gas plants?

A federal CCUS investment tax credit covering up to 50% of eligible capital and a 15% Clean Electricity ITC significantly improve project economics.

Which technology currently sets the efficiency benchmark in Canadian CCGT plants?

GE's 7HA.03 turbine, operating at 64% combined-cycle efficiency at the Genesee site in Alberta.

Page last updated on: