Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

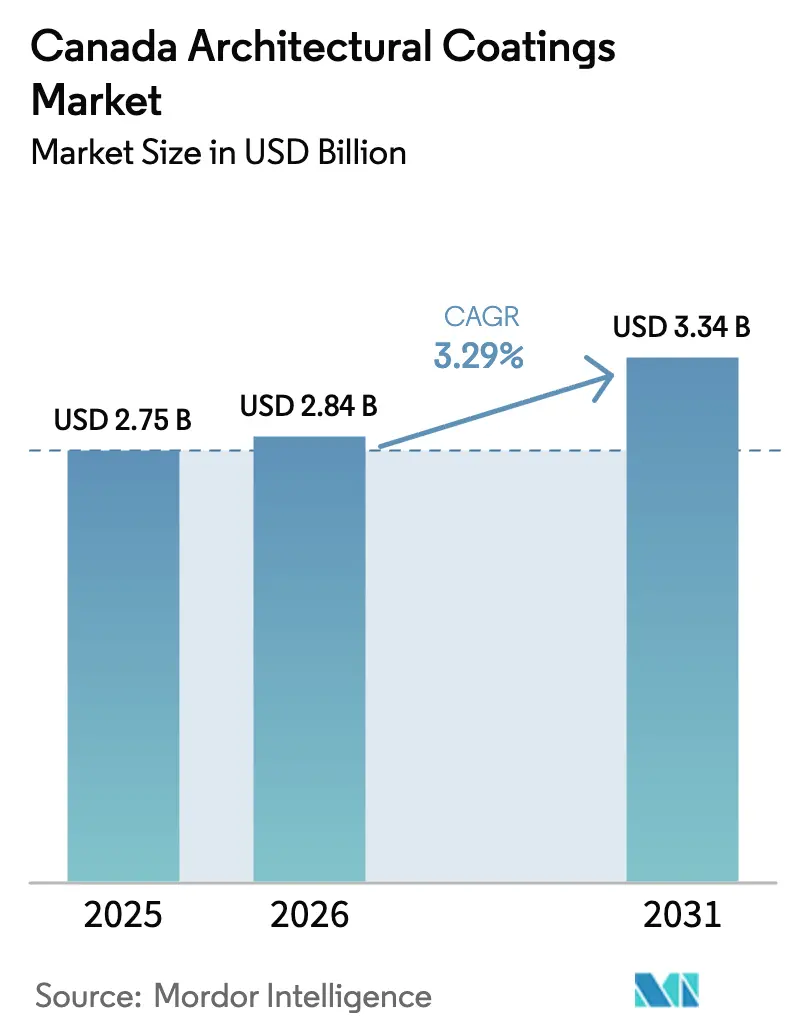

| Base Year Market Size (2025) | USD 2.75 Billion |

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 3.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Architectural Coatings Market Analysis by Mordor Intelligence

The Canada Architectural Coatings Market size is expected to grow from USD 2.75 billion in 2025 to USD 2.84 billion in 2026 and is forecast to reach USD 3.34 billion by 2031 at 3.29% CAGR over 2026-2031. This expansion is driven by stringent VOC regulations, rising renovation expenditures, and sustained residential repaint cycles that have shortened to 8–12 years from the historic 15-year norm. Regulatory pressure has elevated water-borne systems from alternative to default status, while climate-adaptive chemistry and e-commerce retail are opening new revenue streams. Manufacturers able to balance raw material cost swings, invest in digital color platforms, and offer cold-weather formulations are poised to gain market share in the Canada Architectural Coatings market. Competitive positioning now hinges less on store count and more on supply-chain resilience, R&D depth, and omnichannel reach, as rising titanium-dioxide prices and labor shortages squeeze margins. The steady trajectory confirms Canada’s role as a mature yet innovation-driven arena within North America, where environmental compliance shapes every strategic decision in the Canada architectural coatings market.

Key Report Takeaways

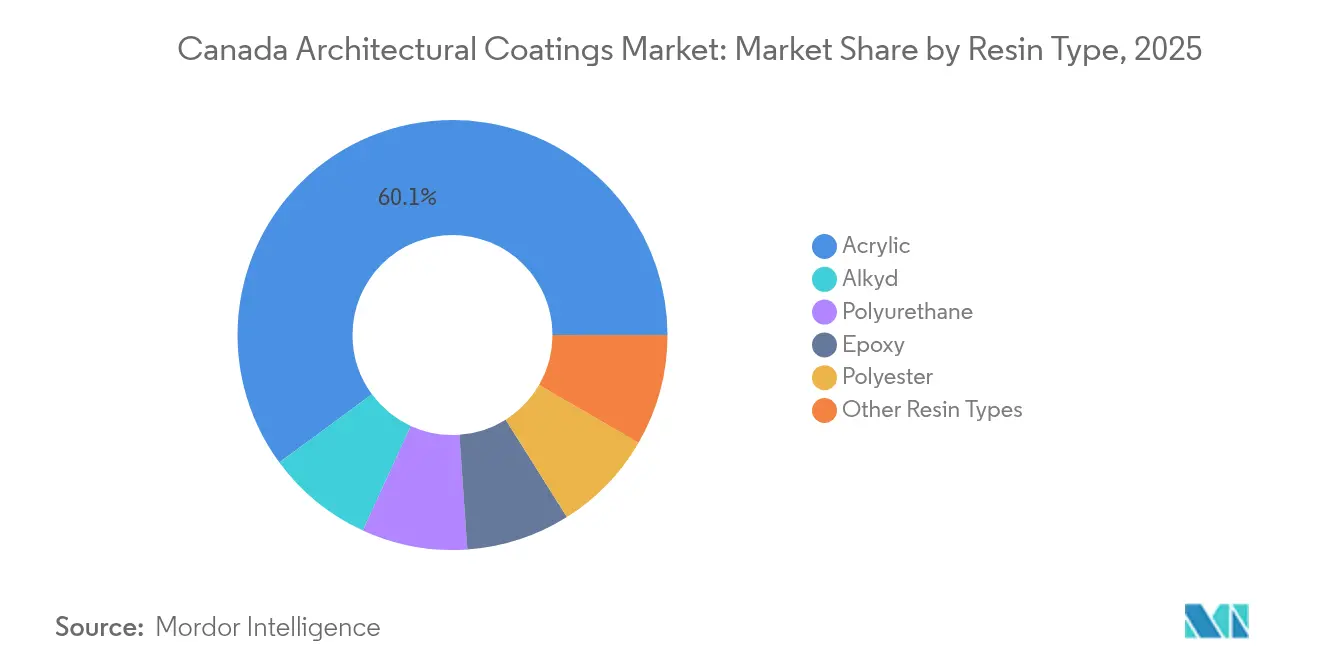

- By resin type, acrylic accounted for the largest share of 60.10% in 2025, and this is expected to grow at a CAGR of 3.82% during the forecast period (2026-2031).

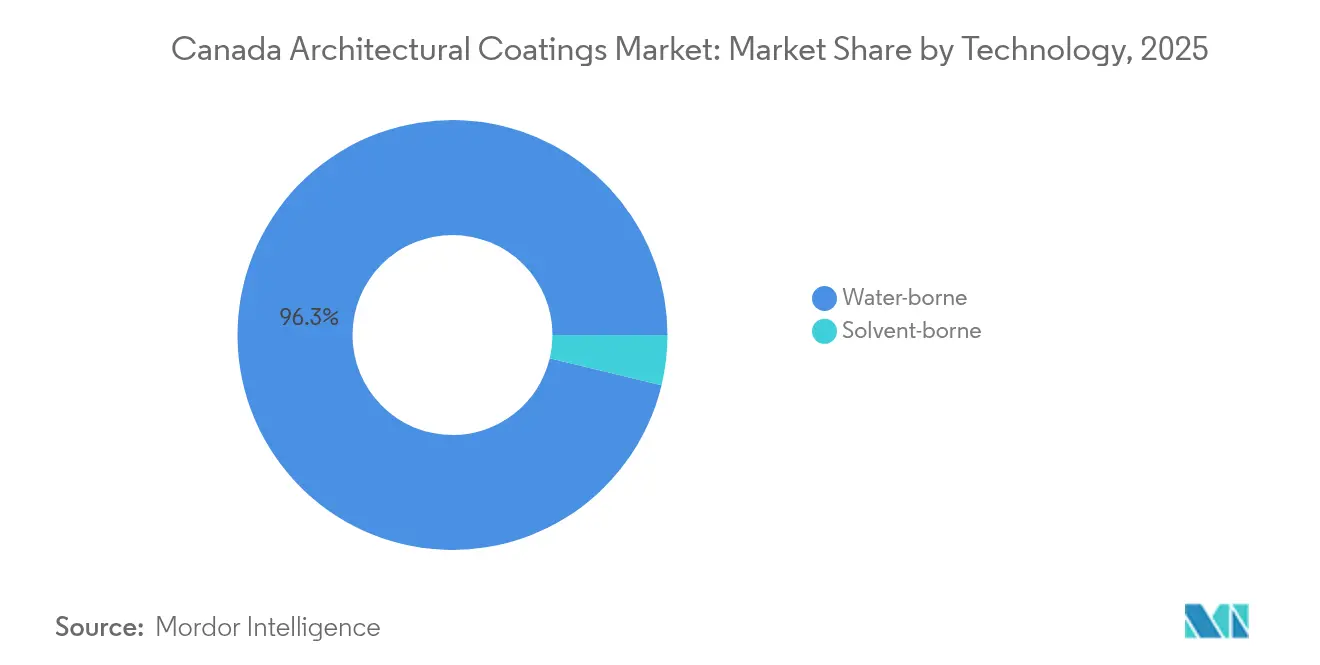

- By technology, waterborne systems accounted for 96.25% of the Canada Architectural Coatings market size in 2025 and are expected to advance at a 3.47% CAGR through 2031.

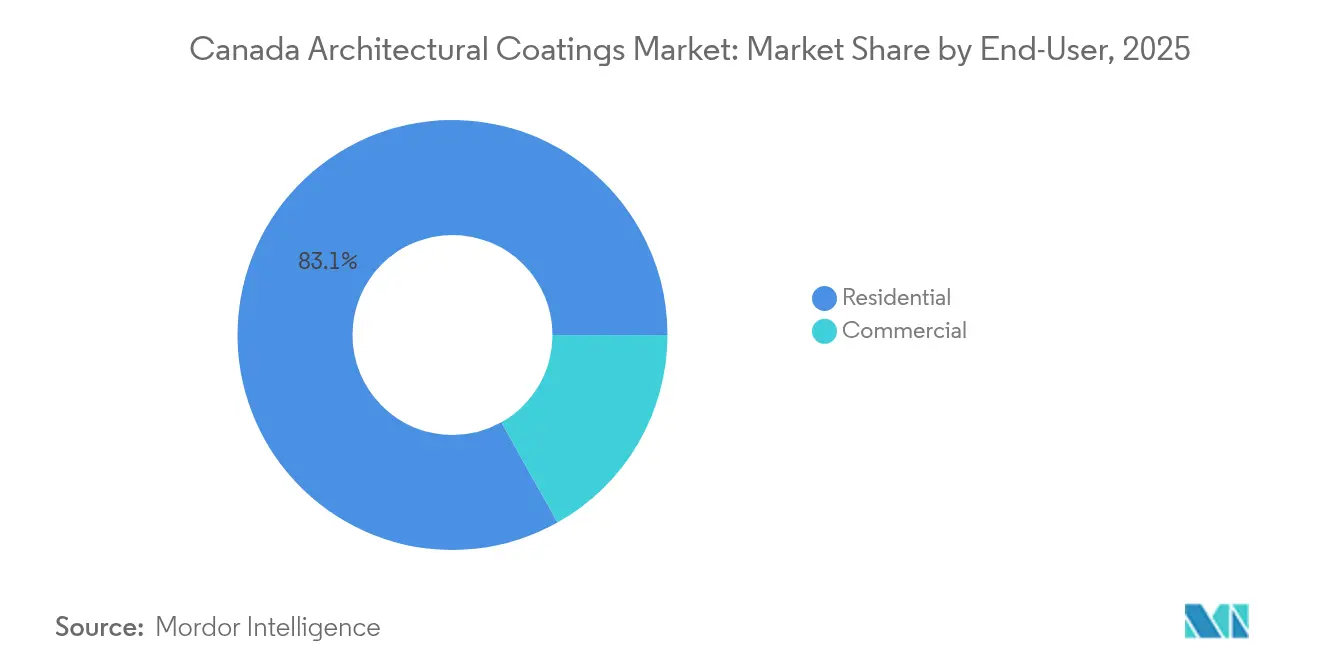

- By end-user, the residential segment held an 83.12% share of the Canada Architectural Coatings market size in 2025, while commercial applications are expected to expand at a 3.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation boom in aging housing stock | +1.0% | National, concentrated in Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Stricter VOC regulations accelerating water-borne shift | +0.8% | National, with provincial variations | Long term (≥ 4 years) |

| Post-COVID DIY & e-commerce paint retail surge | +0.6% | National, urban centers leading adoption | Short term (≤ 2 years) |

| Indigenous timber construction driving specialty coatings | +0.4% | Northern regions, British Columbia, Alberta | Long term (≥ 4 years) |

| AI-driven colour visualisation & digital tinting adoption | +0.3% | Urban centers, major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renovation Boom in Aging Housing Stock

Nearly 46% of Canadian households completed painting-related upgrades in the past 12 months, and average renovation spend doubled to CAD 19,000 (USD 14,100) since 2019[1]Statistics Canada, “Household Spending on Home Renovations, 2025,” statcan.gc.ca. Homes built during the 1960s–1980s account for the bulk of repaint demand, trimming cycle lengths to 8–12 years. Premium interior finishes with superior washability and low odor now command higher price points, repositioning coatings from discretionary to essential products. Contractors and DIY consumers alike are gravitating to surface-tolerant primers that offset sub-optimal substrate conditions common in older dwellings. The resulting uptick in volume and value firmly supports steady gains for the Canada architectural coatings market across repaint channels.

Stricter VOC Regulations Accelerating Water-Borne Shift

Federal limits cap interior architectural coatings at 100 g/L VOC and exterior coatings at 150 g/L VOC, ensuring that water-borne technology holds a 96.39% share nationwide. British Columbia and Quebec layer additional thresholds, prompting formulators to chase even lower emissions. Investments in surfactant technology and advanced coalescents now deliver flow and leveling on par with solvent-borne products even at 2°C application temperatures. These regulatory guardrails have raised barriers for small producers lacking R&D scale, effectively consolidating market power in the Canada architectural coatings market among firms with deep formulation expertise and compliance track records.

Post-COVID DIY & E-Commerce Paint Retail Surge

DIY activity spiked during lockdowns, making interior painting Canada’s top stay-at-home project. E-commerce penetration leapt from negligible to a mid-single-digit share in under two years as consumers increasingly adopted click-and-collect or home delivery. Retailers responded with virtual room visualizer apps, curbside tinting pickup, and rapid fulfillment options. Large brands with integrated digital storefronts and inventory APIs captured early growth, whereas independent dealers pivoted toward value-added services such as same-day color consultation. The behavior shift is durable, sustaining omnichannel investment and funneling incremental volume into the Canada architectural coatings market.

Indigenous Timber Construction Driving Specialty Coatings

Mass-timber mid-rises and Indigenous community projects are on the rise, particularly in British Columbia and the North. The National Building Code’s acceptance of 12-story mass-timber structures underscores the demand for fire-resistant, breathable coatings that preserve wood aesthetics[2]National Research Council Canada, “Cold-Weather Coatings Performance Study,” nrc.canada.ca. Formulators are developing intumescent layers compatible with cedar and spruce substrates that meet the CAN/ULC-S102 flame-spread requirements. Though niche in gallons, these specialty lines command premium margins and reinforce sustainability credentials across the Canada architectural coatings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ & petro-resin costs | –0.9% | Nationwide | Short term (≤ 2 years) |

| Skilled labor shortage | –0.5% | Western provinces, national | Medium term (2–4 years) |

| Climate-driven short construction season | –0.3% | Northern regions, Prairie provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ & Petro-Resin Costs

Titanium-dioxide spot prices remain vulnerable to supply shocks, and petro-resin inputs closely track crude oil swings, exposing manufacturers to sudden margin erosion. Domestic TiO₂ mining provides partial insulation, yet global benchmarks dictate contract resets. Bidding for fixed-price commercial jobs increases risk when pass-through costs lag input price spikes. Resin expenses, which can account for up to 40% of formulation costs, compel firms to deploy hedging strategies, dual-source procurement, and early-order incentives. Some producers accelerate bio-based resin pilots to moderate exposure, though performance gaps persist for high-traffic topcoats.

Skilled Labor Shortage Affects Application Quality

Tradespeople counts fell 5.7% between 2016 and 2021, and only 14.8% of painters hold certifications, limiting application bandwidth and increasing warranty incidence. Western provinces contend with wage competition from energy projects, which are pulling labor away from the finishing trades. Manufacturers respond with extended-open-time coatings that level despite novice technique and contractor academies offering mobile spray-equipment clinics. Yet site backlogs and quality concerns can defer repaint schedules, shaving near-term gallons from the Canada architectural coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Drives Innovation

Acrylic platforms accounted for 60.10% of Canada's architectural coatings market share in 2025 and are projected to grow at a 3.82% CAGR through 2031. Their chemistry balances cost, flex-temperature range, and low-VOC compliance, supporting year-round demand. Alkyds, although penalized by VOC rules, retain a foothold in trim enamels and historic restorations where flow is paramount. Polyurethane and epoxy chemistries occupy durability niches in healthcare and institutional corridors. Polyester powders service OEM metal storefronts, while “other” resins capture nascent bio-based hybrids addressing sustainability procurement clauses.

Innovation focuses on modified acrylic lattices that solidify at 2°C, adding valuable weeks to the shoulder seasons. The National Research Council validated the adhesion of such systems to damp wood, encouraging contractors to extend production into late fall. Suppliers integrate self-crosslinking polymers to enhance scrub resistance, while low-gloss, matte finishes align with design trends toward minimal-sheen interiors. Continuous incremental gains ensure acrylics remain the default backbone of the Canada architectural coatings market.

By Technology: Water-Borne Supremacy Reshapes Competition

Water-borne formats represent 96.25% of the technology split, leaving solvent-borne at a marginal 3.75% tail that serves industrial touch-ups and heritage metalwork. Annual growth for water-borne hovers near the market average at 3.47% but siphons volume from remaining solvent niches as additives close performance gaps. Zero-VOC lines featuring polyurethane-modified acrylics are gaining traction in hospital renovations where indoor air quality credits are highly valued. Solvent systems persist where cure-through-cold thresholds or line-shop cycles demand fast solvent flash-off.

The waterborne ascendancy reshuffles supplier ranks: firms with pilot reactors for small-batch resin trials iterate quickly, while tolling-dependent brands struggle with formulation agility. Digital tint bases are universally water-borne, aligning technology supremacy with retail merchandising. This near-monopoly status underpins margin stability, as raw-material indices for water-based binders are less volatile than those for aromatics, easing cost forecasting across the Canada Architectural Coatings market.

By End-User: Commercial Growth Outpaces Residential Volume

Residential repaints underpin 83.12% of 2025 demand, fueled by CAD 19,000 average renovation spend and 46% household participation. DIY share remains high, yet professional painters capture premium interiors with washable eggshells and antimicrobial eggshells. Color-trend marketing, exemplified by Benjamin Moore’s Blue Nova CC-860, stimulates faster palette turnover and incremental gallons per project.

Commercial facilities—spanning healthcare, offices, and education—are set to expand at a 3.45% CAGR through 2031, topping volume growth rates. Federal retrofit programs channel CAD 81 billion into energy-efficient envelope upgrades, specifying high-reflectance roof coatings and low-odor interior products. Facility managers prioritize life-cycle costs, endorsing 15-year elastomeric façades over cheaper 7-year flat options. Compliance with Green Seal or LEED v4 sooner guides specifiers toward zero-formaldehyde formulas, shifting product mix toward ultra-premium tiers within the Canada Architectural Coatings market.

Geography Analysis

Ontario and Quebec jointly consume roughly 60% of the national gallons, thanks to their dense housing stocks and active condo refurbishment pipelines. Repeat cycles every 10 years for common-area corridors to secure a predictable urban baseline demand. Water-borne satin wall finishes tailored to high-traffic elevators dominate bids in Toronto’s 1970s high-rise belt.

British Columbia’s coastal mindset pushes consumers toward ultra-low-VOC and bio-based labeling ahead of federal mandates. The province’s mild winters allow nearly year-round exterior touch-ups, smoothing factory production schedules. Vancouver’s municipal rebates for low-emission interiors further amplify premium uptake.

Alberta and Saskatchewan experience temperature deltas of 40°C between January and July. Polycarbonate-reinforced acrylics rated for –10°C application see brisk spring demand as crews hustle to beat sudden thaw. Resource price swings drive commercial maintenance: when oil royalties swell, pipeline camps and equipment shops order thick-film epoxies for steel protection, lifting regional volumes above trend.

Atlantic Canada—though only mid-single-digit share—values mildew-resistant and ocean-salt tolerant alkyd-modified acrylics for clapboard homes. Local contractors champion quick-dry alkyd hybrids that seal raw cedar before overnight dew.

Northern territories buy limited gallons yet at high value per liter. Two-component polysiloxane topcoats with breathable primers protect modular classrooms flown into permafrost settlements. Government grants for Indigenous capital works anchor steady though small orders, providing footholds for agile distributors in the Canada architectural coatings market.

Climate change overlays every region. Doubling-rate warming accelerates UV exposure and freeze-thaw attacks on coatings, nudging specifiers toward elasticity and higher pigment-volume-concentration systems. Manufacturers with regional sales engineers attuned to micro-climatic stressors can tailor solutions, securing loyalty among local contractors navigating relentless weather variability.

Competitive Landscape

The Canada Architectural Coatings market is concentrated. Digital engagement defines the new frontline. Firms lacking AR visualization or next-day fulfillment slip in bidding wars for millennial DIY budgets. Yet brick-and-mortar remains crucial for tactile sample swatches and on-site tint corrections. Localized technical reps who troubleshoot jobsite humidity or tint anomalies further cement relational moats across the Canada architectural coatings market.

Canada Architectural Coatings Industry Leaders

Cloverdale Paint Inc.

Masco Corporation

PPG Industries, Inc.

The Sherwin-Williams Company

Benjamin Moore & Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Rodda Paint Company, in partnership with the Cloverdale Group based in Surrey, Canada, announced the acquisition of Miller Paint Company, a manufacturer of architectural coatings in the United States. This will enable the sharing of industry know-how and products in the future.

- December 2024: PPG Industries, Inc. completed the sale of 100% of its architectural coatings business in the United States (US) and Canada at a transaction value of USD 550 million to American Industrial Partners (AIP), an industrials investor.

Canada Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.

By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms