Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

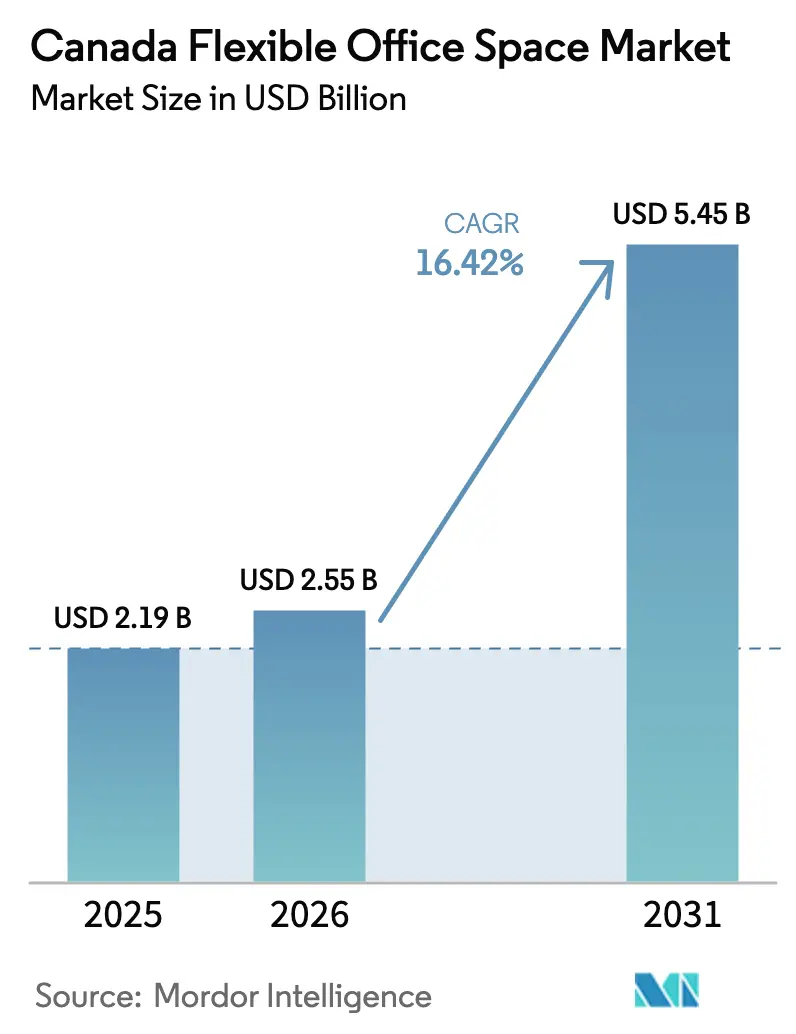

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 5.45 Billion |

| Growth Rate (2026 - 2031) | 16.42% CAGR |

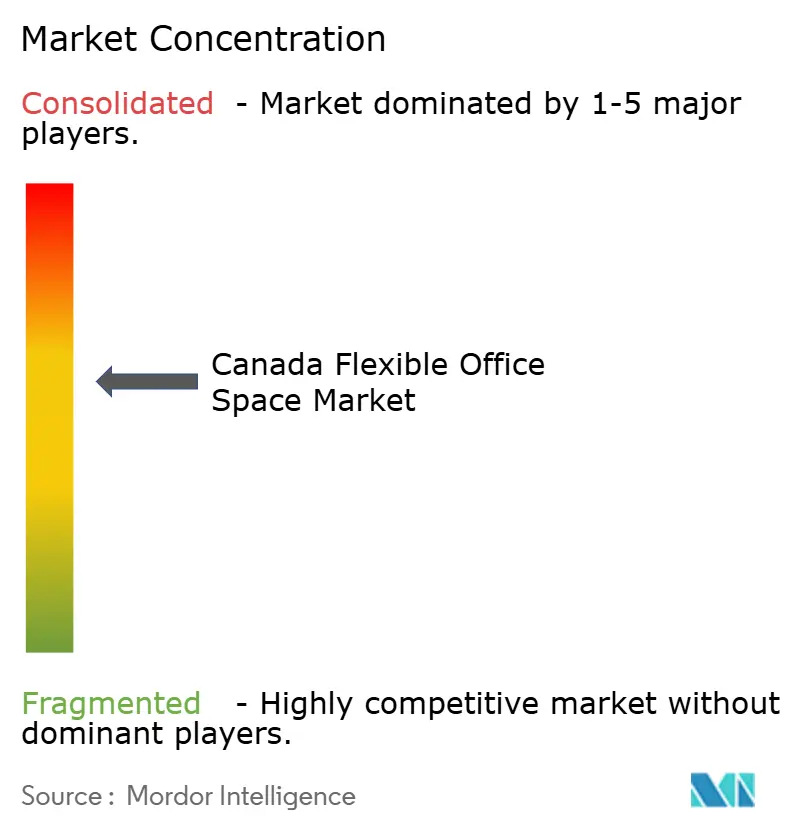

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Flexible Office Space Market Analysis by Mordor Intelligence

Canada Flexible Office Space Market size in 2026 is estimated at USD 2.55 billion, growing from 2025 value of USD 2.19 billion with 2031 projections showing USD 5.45 billion, growing at 16.42% CAGR over 2026-2031. Accelerated adoption of hybrid work policies, the push for real-time space utilization data, and the rise of asset-light partnership models are reshaping workplace strategies across provinces. Demand is no longer confined to cost-conscious startups; large enterprises now integrate flexible space into core portfolios to boost talent retention and operational agility. Technology-enabled services, green certifications, and provincial diversification help operators counter rental inflation in core cities. Consolidation—best illustrated by CBRE’s USD 800 million purchase of Industrious—confirms investor confidence in the Canada flexible office space market.

Key Report Takeaways

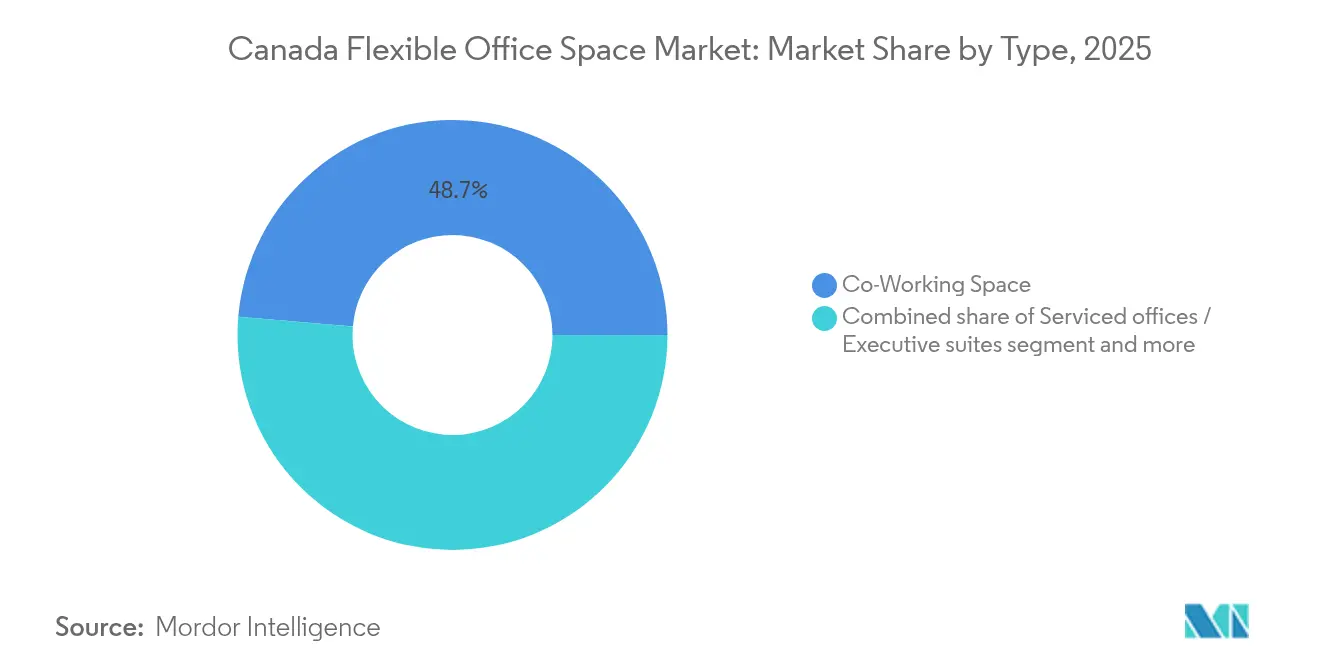

- By type, co-working led with 48.65% of Canada flexible office market share in 2025, while hybrid and virtual office solutions are forecast to grow at a 17.32% CAGR through 2031.

- By sector, information technology accounted for 30.85% of Canada flexible office market size in 2025; business consulting and professional services show the fastest expansion at an 17.75% CAGR to 2031.

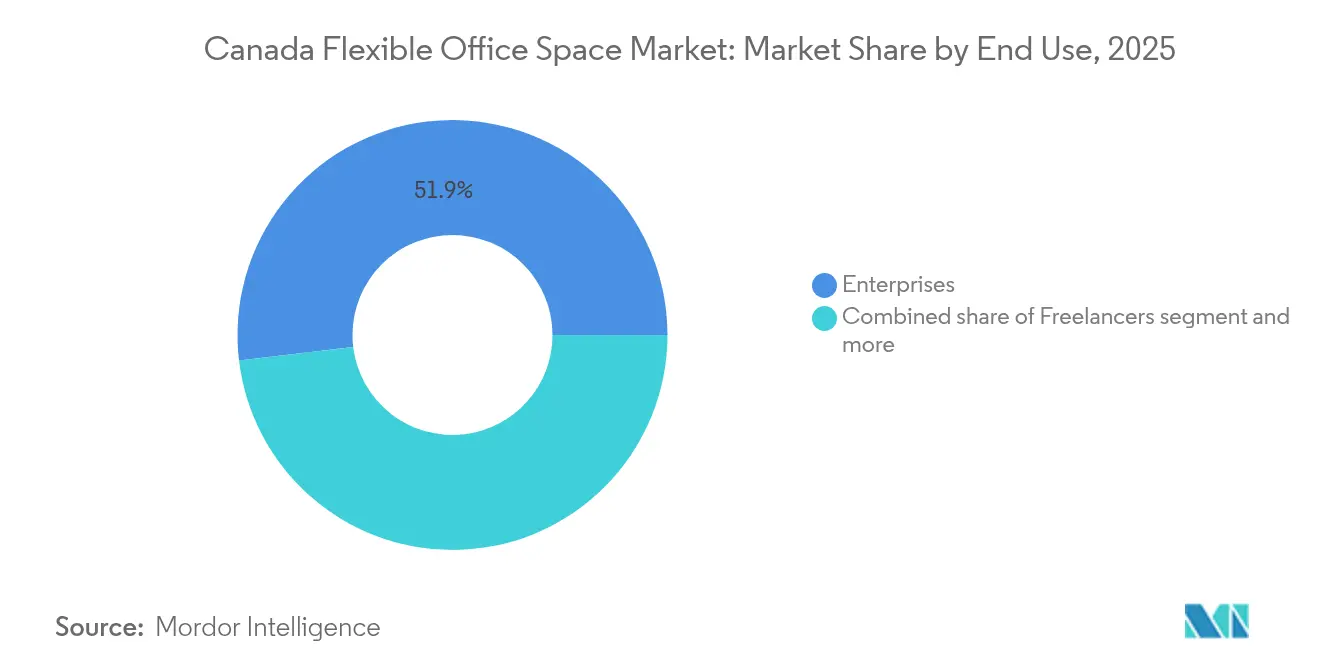

- By end user, enterprises held 51.90% of Canada flexible office market size in 2025, but startups and emerging firms will advance at an 18.29% CAGR through 2031.

- By province, Ontario captured 40.75% of Canada flexible office market share in 2025, whereas Alberta is set to expand at a 18.62% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Flexible Office Space Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise desk-as-a-service pilots | +4.1% | National focus in Ontario and Quebec | Long term (≥ 4 years) |

| Financial-sector hybrid mandates | +3.2% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Vancouver tech-startup migration | +2.8% | British Columbia; spillover into Alberta | Short term (≤ 2 years) |

| Hybrid hubs in secondary cities | +2.5% | Alberta and the rest of Canada | Medium term (2-4 years) |

| Smart-building technology adoption | +1.9% | Ontario, British Columbia | Long term (≥ 4 years) |

| ESG-led demand for green certifications | +1.5% | National, with early uptake in Ontario & B.C. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Mandates Drive Financial-Sector Transformation

The evolving workplace dynamics are driving significant changes in real estate strategies across industries. Banks and insurers are reshaping their real estate portfolios, focusing on two-to-three-day office mandates that necessitate compliant satellite spaces for secure collaboration. Flexible-office providers are now offering branded, access-controlled suites that adhere to regulatory standards, alleviating risk concerns for their highly regulated clientele. The endorsement from GCcoworking, a federal entity, adds an extra layer of credibility to these shared environments. Consequently, the flexible office market in Canada witnesses a consistent demand from enterprises, with operators clinching long-term contracts in suburban areas[1]Lucie O’Donnell, “Hybrid Work and Federal Office Utilization,” Public Services and Procurement Canada, tpsgc-pwgsc.gc.ca.

Tech-Startup Migration Accelerates Coworking Adoption

The flexible office market in Canada is undergoing a significant transformation driven by evolving business needs. Vancouver's nascent firms are moving away from traditional leases, opting instead for coworking memberships that align with their venture-funding milestones. These shared spaces have evolved into informal networks for talent acquisition and deal-making, enhancing their allure. Echoing this trend, Calgary and Toronto showcase how fiscal prudence and networking benefits are driving Canada's flexible office market. This shift underscores the growing importance of adaptability and collaboration in the modern workplace landscape.

Enterprise Desk-as-a-Service Models Reshape Corporate Real Estate

The concept of flexible workspaces is transforming how large organizations manage their office needs. Large organizations are now viewing workspaces as subscriptions, allowing them to free up capital and manage occupancy fluctuations. At Ottawa's Vanguard Building, corporates are testing the waters with sophisticated booking tools, zero-trust security measures, and trials of unassigned seating. These pilot programs are not just experiments; they validate the demand for premium, tech-driven solutions in Canada's flexible office market.

Secondary-City Expansion Creates Geographic Diversification

The shift toward suburban markets is gaining momentum as operators adapt to evolving workplace trends. Operators are expanding into Ottawa, Calgary, and Halifax, aiming to be closer to employees and to take advantage of more affordable real estate. IWG's ambitious "15-minute city" initiative, which seeks to boost Canadian locations from 150 to 250, highlights a strong belief in the rising demand for suburban spaces. This geographic diversification not only protects revenues from the unpredictability of downtown markets but also widens the potential customer base. These strategic moves reflect a proactive approach to meeting changing market demands while ensuring sustainable growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring rental rates in core cities like Toronto are reducing operator profitability | -2.1% | Ontario, British Columbia | Short term (≤ 2 years) |

| Oversupply in major hubs is leading to increased vacancy and discounting pressures | -1.8% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Varying lease and building regulations across provinces are complicating national expansion | -1.4% | National, particularly affecting multi-provincial operators | Long term (≥ 4 years) |

| Concerns around cybersecurity in shared environments are deterring enterprise clients | -1.2% | National, concentrated in BFSI and government sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rental-Rate Inflation Pressures Operator Margins

Toronto is seeing rising rental rates, squeezing flexible office operator margins and prompting changes in pricing and location strategies. The Greater Toronto Area vacancy rate rose to 12.6% in Q3 2024, yet Class A asking rents still edged up to CAD 26.15 per square foot. Providers that hold conventional leases face the sharpest margin pressure and are re-pricing memberships or relocating to suburban sites where costs are lower. Many are now favoring revenue-sharing deals with landlords to cut fixed liabilities and keep expansion plans on track. Market data show a split between Trophy assets, which enjoy their lowest vacancy in four years, and older Class B/C towers that sit half-empty, leaving operators caught between higher rents for premium floors and tenant demands for professional settings

Market Oversupply Creates Competitive Pressures

Major Canadian markets, including Toronto, Vancouver, and Montreal, are facing oversupply in flexible office spaces, driving up vacancy rates and pressuring operator profitability. National office vacancy reached 17.7% in Q1 2023, while downtown Toronto hit 15.3% and other major metros logged record highs. Sublet listings made up 18.1% of all vacancies by late 2022, signaling that many firms cannot fully use the space they already hold. Traditional landlords have joined the flex trend, adding amenities and short leases that intensify price competition for dedicated operators. Net absorption turned positive in early 2024, yet sublet inventory still stands at 15 million square feet, keeping rents in check. Deep-pocketed brands now eye distressed assets and smaller rivals, betting that takeovers will restore balance and lift long-term profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Hybrid Models Redefine Usage Patterns

Co-working spaces commanded 48.65% of Canada flexible office space market size in 2025, underscoring their entrenched appeal to startups and freelancers. However, hybrid and virtual solutions will post a 17.32% CAGR to 2031 as corporations blend remote work with ad-hoc in-person collaboration. Hybrid plans allow employees to reserve desks only when required, enabling operators to optimize seat density and enterprises to trim fixed commitments. Leading brands such as IWG and WeWork have introduced day-pass bundles and meeting-room tokens to serve this episodic demand. Community-oriented amenities, once the hallmark of coworking, now coexist with enterprise-grade privacy zones and advanced conferencing gear, reflecting the sector’s widening client mix.

Adoption of subscription-based access is accelerating as employers prioritize flexibility over square footage. Virtual-office bundles supply mailing addresses and administrative support, letting companies establish Canadian presence without physical space. As hybrid adoption rises, operators refine booking algorithms to stagger peak usage and maintain service quality. Meanwhile, traditional serviced offices retain a solid niche among legal and consulting firms that value enclosed suites and administrative help, ensuring product diversity within the Canada flexible office market.

By Sector: Professional Services Gain Momentum

Information technology firms held 30.85% of 2025 demand, cementing their role as early adopters comfortable with collaborative setups and short planning cycles. Business consulting and professional services, propelled by an 17.75% CAGR forecast, are closing the gap as project-based engagements call for rapid team scaling and nationwide client coverage. Management consultancies now leverage hub-and-spoke footprints, hosting core teams downtown and deploying project staff in regional centers. This model reduces travel costs and supports just-in-time staffing for client work. IT tenants continue to require robust connectivity and secure network rooms, nudging operators to install multi-carrier fiber and redundant power backups. The influx of professional-services occupiers is broadening demand for client-ready boardrooms and concierge-level reception, diversifying revenue streams across the Canada flexible office market.

Sectoral diversification also mitigates cyclical risk: countercyclical legal and accounting practices temper volatility associated with startup funding flows. Flexible-office brands differentiate by tailoring build-outs—sound-proof rooms for legal depositions, secure data rooms for due diligence—meeting varied compliance needs without departing from shared-service economics.

By End User: Enterprise Demand Bolsters Scale

Enterprises represented 51.90% of 2025 revenue, confirming that flexible offerings have matured into a core real-estate strategy. Pilot programs in telecommunications, banking, and insurance now convert into multi-year frameworks that anchor operator cash flows. The fastest growth, however, stems from startups and emerging firms, projected at an 18.29% CAGR through 2031. Venture-backed teams favor month-to-month memberships that mirror funding rounds, reinforcing throughput for smaller meeting rooms and communal zones. Freelancers remain a stable base, driving daytime desk utilization but exerting limited bargaining power. As both cohorts coexist, operators create tiered access packages—corporate suites, growth-company studios, and freelancer hot-desks—maximizing yield per square foot.

Enterprises are also demanding integration with HR and security systems for badgeless access and single-sign-on authentication. Operators that deliver seamless onboarding and data-driven reporting strengthen retention. Meanwhile, startup-oriented operators differentiate via mentor programs, investor pitch events, and digital talent boards, ensuring their share of the Canada flexible office market expands steadily.

Geography Analysis

Ontario remains the center of gravity, claiming 40.75% share in 2025 on the back of Toronto’s dense financial-services ecosystem and the clustering of multinational headquarters. Hybrid work policies push corporates to reserve premium, Class A suites downtown while adding satellite hubs in suburbs such as Mississauga and Markham, where lower rents bolster margins. Clear lease frameworks under the Commercial Tenancies Act simplify contract negotiations and reduce legal friction for operators. The province’s focus on smart-city initiatives further encourages IoT adoption within flexible offices, reinforcing premium positioning.

Alberta, predicted to grow at 18.62% CAGR through 2031, benefits from economic diversification initiatives that invite technology and professional-services tenants into Calgary and Edmonton. Public incentive schemes fund tower conversions, accelerating inventory growth while maintaining manageable overheads. Large energy firms establishing cleantech incubators rely on turnkey floors with advanced lab space, adding sector depth to the Canada flexible office market. Additionally, Alberta’s competitive housing costs support talent attraction, increasing corporate willingness to open western satellite offices.

British Columbia and Quebec deliver mid-teen growth rates anchored by Vancouver’s tech corridor and Montreal’s aerospace and life-sciences sectors. Vancouver’s emphasis on sustainability dovetails with ESG-oriented tenant preferences, pushing operators to secure LEED Gold and BOMA BEST Platinum labels. Montreal’s bilingual workforce requires dual-language reception and signage, prompting localization of service offerings. Beyond the four largest provinces, secondary cities such as Ottawa, Halifax, and Winnipeg enter the spotlight. Federal GCcoworking rollouts and provincial ShareSpace programs validate demand in public-sector circles, while allowing private operators to seed early positions before saturation.

Competitive Landscape

The Canada flexible office space market is moderately concentrated. International giants IWG and WeWork coexist with Canadian home-grown brands including Workhaus, iQ Offices, and TCC Canada, resulting in a moderately fragmented but tightening field. The USD 800 million CBRE–Industrious deal in January 2025 signals rising convergence between brokerage, property management, and flexible operations. Such vertical integration equips global players with capital access, enterprise sales channels, and data platforms that small independents find hard to match.

The Canadian flexible office sector is moderately concentrated. Competition increasingly revolves around asset-light revenue-sharing models rather than fixed leases, reducing risk and unlocking faster provincial rollouts. Operators partner with landlords to retrofit under-utilized floors, sharing upside while shielding themselves from rental volatility. Technology becomes the new battleground: white-label booking apps, AI-driven occupancy dashboards, and mobile access control differentiate premium offerings. Firms that integrate real-time ESG metrics also gain traction among corporates mandated to track carbon footprints[3]Competition Bureau Canada, “Merger Review of Real-Estate Service Firms 2025,” competitionbureau.gc.ca.

Specialization emerges as an effective defense for mid-sized brands. Workhaus focuses on community-centric environments with curated networking events for scale-ups, whereas iQ Offices targets boutique, design-forward suites appealing to legal and finance tenants. Regional operators such as The Hive Vancouver and Launch Coworking capture niche demand through hyper-local programming and partnerships with municipal innovation agencies. Meanwhile, traditional landlords increasingly offer spec-suite flex floors, intensifying competition but also validating the broader Canada flexible office market.

Canada Flexible Office Space Industry Leaders

International Workplace Group plc

Spaces

WeWork

Workhaus

iQ Offices

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CBRE Group completed its acquisition of Industrious National Management Company for approximately USD 800 million, creating a new Building Operations & Experience segment expected to generate USD 20 billion in revenue. The deal broadens CBRE’s flexible-office footprint across Canada, giving corporate clients integrated brokerage, facilities, and on-demand space services.

- January 2025: Yardi Systems bought Hubble in the United Kingdom and Deskpass in North America, combining two top booking platforms for flexible workspaces. The move enlarges Yardi’s real-estate technology stack and offers operators scalable reservation, billing and analytics tools.

- November 2024: WeWork launched a Coworking Partner Network with Vast Coworking Group, adding more than 75 suburban sites in Canada and the United States to its member roster. The alliance lets WeWork serve commuters closer to home while giving Vast locations access to WeWork’s global sales engine and app.

- September 2024: British Columbia Public Service partnered with private operators to roll out ShareSpace hubs in Greater Victoria, extending flexible-workspace access to provincial employees and validating demand in secondary markets.

Canada Flexible Office Space Market Report Scope

A flexible workspace is also known as a shared office space. This type of office space is fitted with basic equipment, like phone lines, desks, and chairs, a setup that allows employees who normally work from home or telecommute to have a physical office for a few hours every week or every month.

Flexible office space is a type of workspace that allows employees to work in a number of locations and different ways. Workers in a flexible office space can choose the section of the workplace that best matches the type of work they need to complete at the time, as opposed to typical offices with fixed and assigned desk locations.

Canada's flexible office space market is segmented by type (private offices, co-working spaces, and virtual offices), by end-user (IT and telecommunications, media and entertainment, retail and consumer goods, and other end-users), and by key cities (Toronto, Vancouver, Montreal, and other key cities).

The report offers market size and forecasts in Values (USD) for all the above segments.

By Type

| Co-Working Space |

| Serviced offices / Executive suites |

| Others (Hybrid, Virtual Office) |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Type | Co-Working Space |

| Serviced offices / Executive suites | |

| Others (Hybrid, Virtual Office) | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

What is the current value of the Canada flexible office market?

The market is valued at USD 2.55 billion in 2026 and is projected to reach USD 5.45 billion in 2031.

How fast will the Canada flexible office market grow through 2031?

It is expected to expand at a 16.42% CAGR, pushing total value to USD 5.45 billion by 2031.

Which space type leads the Canada flexible office market?

Co-working spaces lead with a 48.65% share, while hybrid and virtual solutions show the strongest forecast growth.

Why is Alberta the fastest-growing province for flexible offices?

Economic diversification, lower real-estate costs, and municipal incentives drive Alberta’s 18.62% CAGR outlook.

How are enterprises using flexible offices differently from startups?

Enterprises deploy desk-as-a-service models for satellite hubs, whereas startups favor short-term memberships aligned with funding cycles.

What technologies are critical in modern flexible offices?

IoT sensors, AI-driven space analytics, and mobile-first booking platforms improve utilization, energy efficiency, and tenant experience.

Page last updated on: