Canada Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

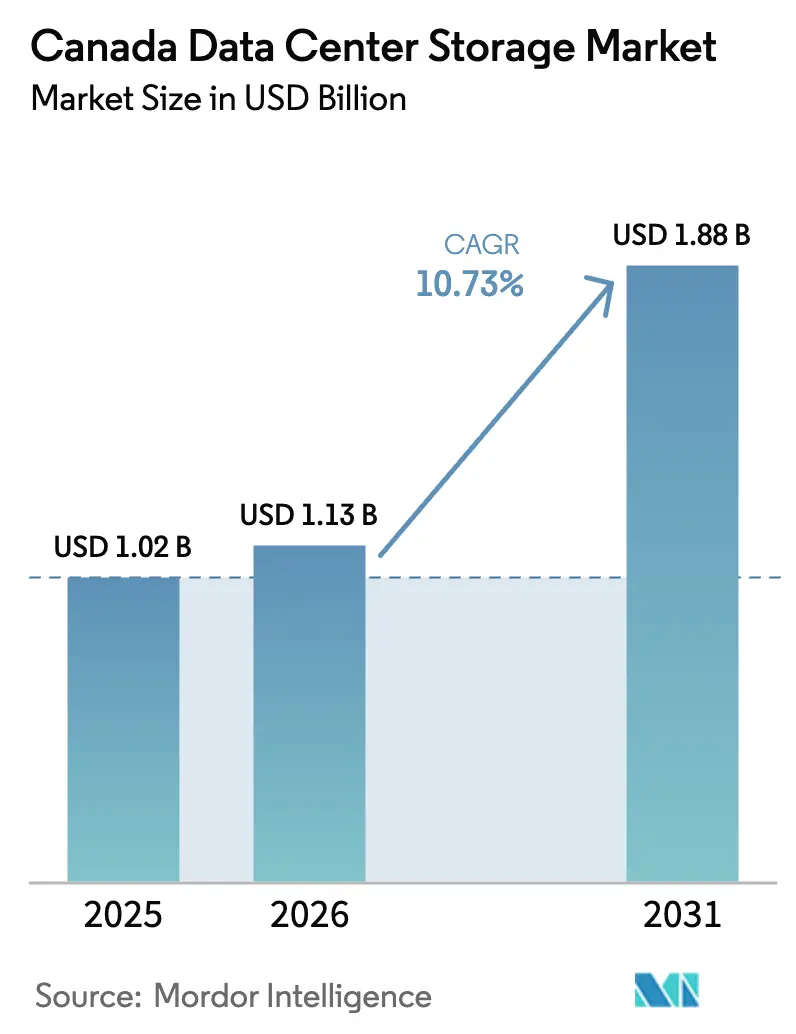

| Base Year Market Size (2025) | USD 1.02 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.88 Billion |

| Growth Rate (2026 - 2031) | 10.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Storage Market Analysis by Mordor Intelligence

Canada data center storage market size in 2026 is estimated at USD 1.13 billion, growing from 2025 value of USD 1.02 billion with 2031 projections showing USD 1.88 billion, growing at 10.73% CAGR over 2026-2031. This steady climb reflects robust national policies that keep sensitive workloads inside the country and a growing appetite for cloud, artificial intelligence, and big-data initiatives. Canadian enterprises increasingly deploy high-performance arrays to support machine-learning pipelines while public-sector mandates accelerate demand for on-shore infrastructure. The shift toward all-flash and NVMe-based systems is cutting latency, raising IOPS, and triggering a wide replacement cycle. Sustainability is also shaping buying decisions as operators look for lower-carbon, hydro-powered facilities that can reclaim waste heat for district networks. Firms that combine cutting-edge performance with local compliance are securing long-term contracts, even as tight power grids and scarce engineering talent threaten project timelines.

Key Report Takeaways

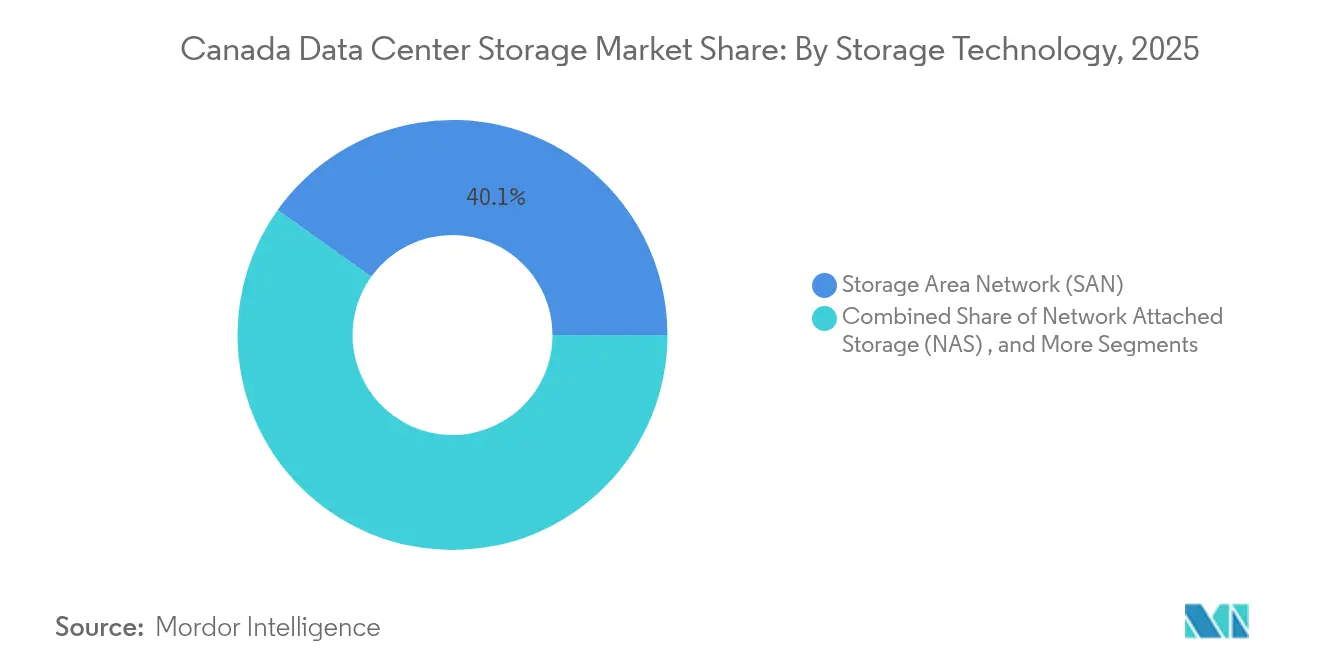

- By storage technology, Storage Area Networks held 40.12% of Canada data center storage market share in 2025, while Network Attached Storage is forecast to expand at a 12.85% CAGR through 2031.

- By storage type, traditional HDD arrays accounted for 44.25% of the Canada data center storage market size in 2025; all-flash arrays are rising fastest at a 13.05% CAGR.

- By data center type, colocation led with 56.85% revenue share in 2025, whereas hyperscalers and cloud service providers are projected to grow at 16.9% CAGR to 2031.

- By end user, IT and telecommunications commanded 35.35% of 2025 revenues, but healthcare and life sciences will post the highest 14.15% CAGR.

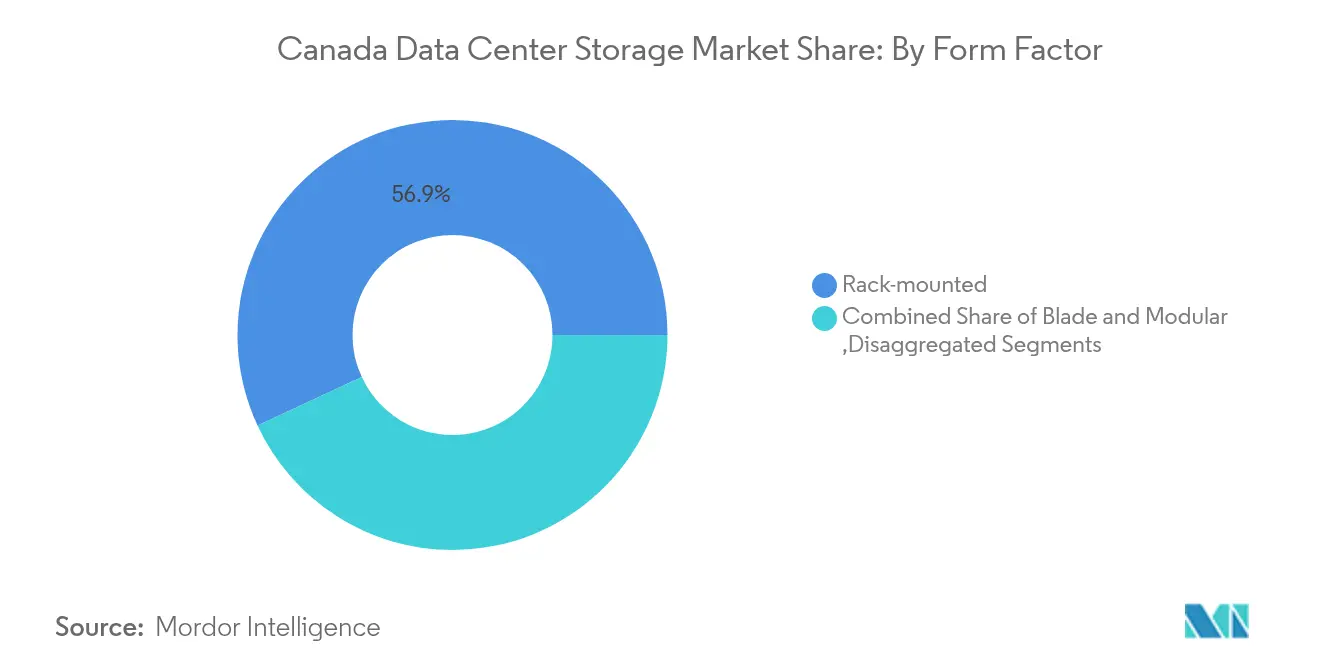

- By form factor, rack-mounted systems delivered 56.92% share of the Canada data center storage market size in 2025, while disaggregated and composable infrastructure advances at 13.35% CAGR.

- By interface, legacy SAS/SATA maintained 48.98% share, yet NVMe connections are climbing at 14.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cloud computing demand | +2.8% | National, dense in Toronto, Montreal, Vancouver | Medium term (2-4 years) |

| Surge in AI workloads needing high-performance storage | +3.1% | National, early adoption in tech hubs | Short term (≤ 2 years) |

| Stricter Canadian data sovereignty mandates | +2.2% | National, strongest in government and regulated sectors | Long term (≥ 4 years) |

| Rapid shift toward NVMe all-flash arrays | +1.9% | National, led by enterprise and hyperscale deployments | Medium term (2-4 years) |

| Hydropower-enabled green data centers | +1.4% | Quebec, British Columbia, Manitoba | Long term (≥ 4 years) |

| Government incentives for data center heat reuse | +0.8% | Urban centers with district heating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud Computing Demand

Canada’s federal cloud-first directive and a CAD 2.4 billion sovereign AI compute program are steering budgets toward hybrid and multi-cloud platforms that require large, secure storage pools. A CAD 700 million allotment earmarked for private AI-focused facilities is validating domestic cloud models for risk-averse companies ised-isde.gc.ca. Government workloads serve as proof points, encouraging banks and insurers to shift tier-1 applications to compliant providers while keeping data on Canadian soil. This momentum reinforces recurring revenue streams for vendors with local footprints and discourages offshore-only rivals.

Surge in AI Workloads Needing High-Performance Storage

The Canada Energy Regulator expects data-center electricity demand to double by 2026, primarily from AI training clusters.[1]Canada Energy Regulator, “Electricity Consumption Outlook 2026,” cer-rec.gc.ca To feed GPU farms, operators are installing PCIe 5.0 NVMe drives such as KIOXIA’s LC9 Series 122.88 TB SSD, which offers dual-port architecture for resilience.[2]KIOXIA America, “LC9 Series NVMe SSD Launch,” kioxia.com Ottawa’s USD 240 million backing of Cohere’s new AI complex underscores how public capital is fueling hyperscale rollouts that rely on ultra-low-latency flash arrays. As model sizes scale, organizations prioritize throughput over raw capacity, accelerating the all-flash replacement cycle.

Stricter Canadian Data Sovereignty Mandates

Treasury Board rules force Protected B and higher data to reside in certified domestic facilities, creating a structural tailwind for suppliers with in-country racks.[3]Treasury Board of Canada Secretariat, “Direction for Electronic Data Residency,” tbs-sct.gc.ca Private enterprises in finance, healthcare, and utilities mirror these policies to simplify compliance with provincial privacy laws. Local hosting also shields records from extraterritorial subpoenas, a concern highlighted by the Canadian Internet Registration Authority. The regulatory moat raises switching costs and locks in long-term contracts, lifting utilization rates across compliant colocation halls.

Rapid Shift Toward NVMe All-Flash Arrays

Vendors such as Kingston Digital now ship enterprise NVMe SSDs with power-loss protection for boot and data partitions, making flash viable for every server tier. Pure Storage and Micron collaborate on QLC-based arrays that deliver higher density at lower energy per bit, easing both space and carbon constraints. For real-time analytics, the latency gap between NVMe and SAS/SATA is pushing firms to bypass incremental upgrades and migrate straight to all-flash fabrics.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure | -1.8% | National, most acute for SMEs | Short term (≤ 2 years) |

| Shortage of specialized data center talent | -1.2% | Major metros nationwide | Medium term (2-4 years) |

| Urban power-grid congestion | -0.9% | Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Thermal management challenges at >30 kW racks | -0.7% | National high-density sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure

Firms must commit hundreds of millions to keep pace with AI-grade storage. eStruxture’s CAD 1.8 billion financing underscores the entry barrier, effectively sidelining smaller operators without deep capital pools. Elevated flash prices and liquid-cooling retrofits widen the gap between incumbents and new entrants, delaying fresh competition in several metro zones.

Shortage of Specialized Data Center Talent

A Robert Half survey found half of Canadian tech managers struggling to fill positions crucial for AI and cloud programs. Demand for senior architects skilled in NVMe-over-Fabric and software-defined storage is outpacing supply, raising labor costs and lengthening deployment cycles. Firms often import expertise from the United States, raising total project budgets and complicating knowledge transfer to local teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Faces NAS Disruption

The Canada data center storage market size for Storage Area Networks reached USD 409.3 million in 2025, translating into a 40.12% share of spending. Network Attached Storage is expanding at a 12.85% CAGR and is set to erode that lead by 2031. Businesses favor file-based repositories to enable analytics teams working across geographic locations and to integrate microservices into DevOps pipelines. At the same time, unified platforms blur SAN and NAS boundaries, giving IT leaders self-service provisioning without sacrificing performance.

Traditional SAN architectures still power core databases, financial ledgers, and ERP clusters that demand block-level consistency. Yet modern workloads prize agility over rigid zoning, making scale-out NAS attractive for AI model staging and collaboration. Vendors now bundle intelligent tiering so that less-critical data spills into cloud object stores, balancing cost and speed. The long-term outlook indicates convergence around protocol-agnostic fabrics rather than a strict SAN-versus-NAS dichotomy.

By Storage Type: All-Flash Arrays Accelerate Past Traditional HDDs

In 2025, HDD arrays represented 44.25% of Canada data center storage market share, equating to roughly USD 451.4 million. All-flash arrays, growing 13.05% annually, are projected to capture the majority of new deployments by 2031 as AI and fraud-detection workloads demand predictable microsecond response times. Lower power consumption and shrinking price-per-GB metrics are closing the cost gap, especially when total cost of ownership factors in rack space and cooling.

Hybrid arrays allow cautious operators to blend flash acceleration with disk capacity for cold data. Still, application owners increasingly treat flash as the default tier, relegating spinning media to archival repositories. Government institutions piloting real-time analytics for cybersecurity illustrate the shift: latency gains translate directly into threat-mitigation windows, warranting premium flash investments.

By Data Center Type: Hyperscalers Drive Market Transformation

Colocation facilities generated 56.85% of 2025 revenue but hyperscalers are scaling fastest at 16.9% CAGR as Amazon Web Services, Google Cloud, and Microsoft Azure secure land banks across Quebec and Alberta. Provincial incentives and abundant renewable energy make large campuses viable, supporting sovereign cloud services that meet federal residency laws. Enterprise adoption of hybrid models sustains colocation demand, yet the hyperscale wave is redrawing supply chains for power, fiber, and storage hardware.

Edge and enterprise data centers remain niche but critical where legal or latency needs dictate on-premises gear. Banking institutions maintain high-security vaults for settlement systems even as peripheral workloads migrate to cloud adjacency racks. Multiple footprints demand interoperable storage stacks capable of replicating data across regions without breaking compliance boundaries.

By End User: Healthcare Leads Digital Transformation

The healthcare and life-sciences vertical is rising at 14.15% CAGR, supported by telemedicine, genomic sequencing, and AI-based diagnostics that generate multi-petabyte workloads. Hospitals integrate PACS imaging repositories with AI inference engines, requiring flash arrays and high-bandwidth fabrics. In contrast, IT and telecom firms still account for 35.35% of spending thanks to 5G rollouts and content caching, anchoring baseline demand.

Regulators enforce privacy frameworks such as PIPEDA, obliging secure yet scalable storage. Drug-discovery partnerships between biotech firms and universities further spur investments in GPU-accelerated clusters backed by NVMe drives. As reimbursement systems shift to real-time analytics, providers must guarantee sub-second data retrieval, accelerating the adoption of all-flash tiers.

By Form Factor: Disaggregated Infrastructure Gains Momentum

Rack-mounted enclosures made up 56.92% of 2025 shipments, but disaggregated and composable nodes are expanding 13.35% annually. Organizations decouple compute, memory, and storage into separate pools, allocating resources on demand to improve utilization. Liquid-cooled trays now accommodate 30 kW racks without raising facility PUE beyond 1.1. Vendor roadmaps emphasize tool-less serviceability and 48-volt power backplanes to support future chipsets.

Blade servers remain popular in high-frequency trading rooms where deterministic latency trumps modular flexibility. Still, hyperscalers champion open-rack and open compute designs that simplify parts inventory and speed global deployments. Canadian operators replicate these blueprints to shorten construction timelines and to align with global supply chains.

By Interface: NVMe Disrupts Legacy Protocols

Legacy SAS/SATA links held 48.98% share in 2025, yet NVMe is rising 14.72% per year and will dominate fresh capacity by 2028. PCIe 5.0 doubles lane bandwidth, while NVMe-over-Fabric removes host-bus constraints, turning disaggregated drives into network-addressable resources. Fibre Channel persists in regulated banks for deterministic performance and segregated fabrics, though vendors now offer NVMe/FC hybrids to ease migration.

Security certifications such as FIPS 140-3 for KIOXIA’s CM7 Series reassure public-sector buyers, broadening the addressable pool for high-speed drives. As containerized applications proliferate, Kubernetes operators lean on NVMe namespaces for multi-tenant isolation, underscoring the protocol’s versatility beyond raw performance gains.

Geography Analysis

Canada’s expansive renewable resources, political stability, and privacy protections make the nation a prime host for hyperscale nodes. Quebec attracts the largest tranche of new capacity thanks to Hydro-Québec’s competitive tariffs and plentiful hydropower, which allow operators to chase sub-USD 0.04 per kWh electricity costs. The province also offers grid interconnections suited to 100-plus-MW campuses, aligning with the growth trajectory of the Canada data center storage market.

Alberta follows with a CAD 100 billion AI Data Centres Strategy that leans on natural gas-to-power turbines and geothermal loops for off-grid supply. The Wonder Valley AI Data Centre Park alone will need 1.4 GW, creating a massive pull for storage arrays, liquid cooling, and battery reserves. TransAlta’s outreach to cloud giants signals confidence in transmission upgrades, enhancing regional redundancy.

British Columbia balances strong hydropower credentials with looming supply gaps as BC Hydro warns of tightened margins. Bell’s planned 500 MW cluster suggests investors anticipate long-term fixes, keeping the Canada data center storage market size growing in western provinces. Ontario remains the country’s volume leader due to Toronto’s financial hub status, though grid congestion shifts new construction toward exurban locales with better substation capacity.

Competitive Landscape

Competition is moderate, with global giants vying against nimble Canadian specialists. Pure Storage deepens its local presence through alliances with Rubrik for cyber-resilient tiers and its role in the Ultra Ethernet Consortium that standardizes AI fabrics. Hitachi Vantara’s Virtual Storage Platform One cuts carbon emissions 40% and integrates with AWS and Google Cloud, appealing to enterprises pursuing hybrid footprints.

KIOXIA leads on capacity density, delivering 61.44 TB PCIe 5.0 SSDs that comply with government encryption rules, locking in lucrative public contracts. Supermicro ships liquid-cooled racks holding 100,000 GPUs quarterly, illustrating how hardware innovation and sustainability converge to shape buyer criteria. Domestic providers like eStruxture and Cologix leverage local approvals and bilingual support to win workloads that foreign-only firms cannot touch. White-space opportunities persist in edge nodes across the Far North, where latency-sensitive mining and remote-health projects demand ruggedized, low-touch storage appliances.

Canada Data Center Storage Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

IBM

Pure Storage

NetApp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Pure Storage and Micron Technology announced a collaboration to deliver scalable, energy-efficient storage solutions for hyperscale data centers utilizing Micron's G9 QLC NAND technology, addressing energy efficiency, density, and performance challenges.

- January 2025: Cologix secured USD 1.5 billion in capital to fund new data center development and expand its Canadian footprint.

- March 2025: The Government of Canada finalized a CAD 240 million investment in Cohere’s multi-billion-dollar AI data center project to boost domestic compute capacity

- March 2025: KIOXIA unveiled the LC9 Series 122.88 TB NVMe SSD tailored for AI workloads, featuring BiCS Flash generation 8 and PCIe 5.0 interface

- May 2025: KIOXIA introduced the CM9 Series PCIe 5.0 NVMe SSDs—the first to use 8th-generation BiCS Flash TLC—with 65% higher random write speed

- June 2025: Bell Canada announced six AI data centers nationwide, dramatically lifting domestic capacity for artificial intelligence workloads

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the Canadian data-center storage market as the annual value of purpose-built devices, subsystems, and management software that sit inside colocation, enterprise, hyperscale, or edge data-center halls and provide block, file, or object storage for production, backup, or archival workloads. Arrays delivered as SAN, NAS, DAS, HCI, or software-defined storage are included; value is recorded at first installation inside Canadian facilities.

Scope Exclusions:

Standalone external drives, consumer NAS boxes, and cloud-only storage subscriptions that never occupy a domestic data-center rack are outside our scope.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

We interviewed senior facility engineers at colocation sites in Ontario and Québec, procurement leads at hyperscale operators, and storage-practice heads at national system integrators. Their insights on rack-level density shifts, NVMe adoption speed, and typical refresh cycles calibrated the desk findings and filled gaps on in-country versus cross-border staging volumes.

Desk Research

Mordor analysts first scrape and screen open data from sources such as Statistics Canada on ICT capex, Innovation, Science and Economic Development Canada energy tariffs, Canadian Radio-television and Telecommunications Commission traffic reports, and the U.S.-Canada Harmonized Tariff Schedule for import values of HS 847170 (storage units). Trade association portals, for example, the Storage Networking Industry Association and the Canadian Cloud Council, help trace technology adoption curves, while filings on SEDAR+, investor decks, and press releases by array vendors provide shipment mix and average selling price signals. Subscription datasets, notably D&B Hoovers for company financials and Dow Jones Factiva for deal flows, sharpen vendor revenue splits. This list is illustrative; many additional sources underpin every validation step.

Market-Sizing & Forecasting

The 2025 baseline starts with a top-down reconstruction. Statistics Canada data-center construction outlays are sliced by our storage cost ratios, then adjusted using import records and vendor Canadian revenue disclosures. Supplier roll-ups (sampled array shipments × blended ASP) provide a bottom-up check. Key variables like server rack count, average capacity per rack, NVMe penetration, AI workload share, and Canadian dollar swings feed a multivariate regression that projects demand through 2030. Where bottom-up estimates under-report smaller regional builds, gaps are prorated using provincial building-permit filings.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst cross-checks, and senior-review sign-off. Models refresh yearly, with interim revisions when material events, major fab expansions, currency moves above +/-7%, or government incentives occur. Before delivery, an analyst reruns the sanity checks so clients receive the latest view.

Why Mordor's Canada Data Center Storage Baseline Earns Trust

Published estimates often diverge because firms pick different device mixes, treat hyperscale self-builds unevenly, or stretch forecast horizons.

Key gap drivers include varied inclusion of software licences, differing ASP deflators for all-flash arrays, and refresh cadences; some studies roll five-year averages, whereas Mordor locks in the base year and reapplies currency conversions quarterly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.02 B (2025) | Mordor Intelligence | - |

| USD 0.94 B (2024) | Regional Consultancy A | excludes edge micro-sites and applies single ASP across media types |

| USD 2.27 B (2023) | Industry Observer B | counts cloud-only subscriptions and converts revenue at 2020 FX rates |

These contrasts show that by fixing a clear scope, refreshing inputs each quarter, and triangulating both macro capex and rack-level data, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can replicate and defend.

Key Questions Answered in the Report

What is the current size of the Canada data center storage market?

The market is valued at USD 1.13 billion in 2026.

What compound annual growth rate (CAGR) will the market record through 2031?

It is forecast to expand at a 10.73% CAGR, reaching USD 1.88 billion by 2031.

Which storage technology segment is growing the fastest?

Network Attached Storage (NAS) is rising at a 12.85% CAGR, outpacing other technologies.

Why are NVMe interfaces gaining ground in Canada?

NVMe delivers higher IOPS and lower latency than legacy SAS/SATA, making it essential for AI and real-time analytics workloads.

Which province attracts the most hyperscale data-center investment?

Quebec draws a large share of new builds thanks to abundant hydroelectric power and competitive tariffs.

What are the leading restraints on market growth?

High capital expenditure and a shortage of specialized data-center talent are the two most significant hurdles.

Page last updated on: