Canada Chocolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

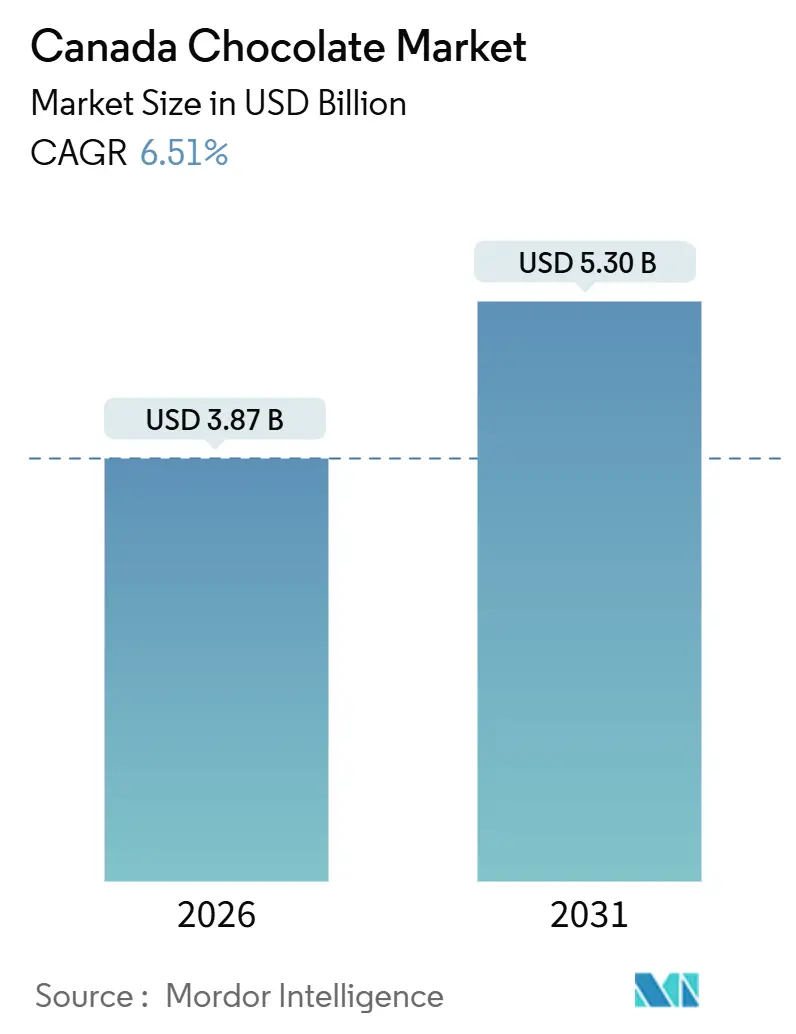

| Market Size (2026) | USD 3.87 Billion |

| Market Size (2031) | USD 5.30 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

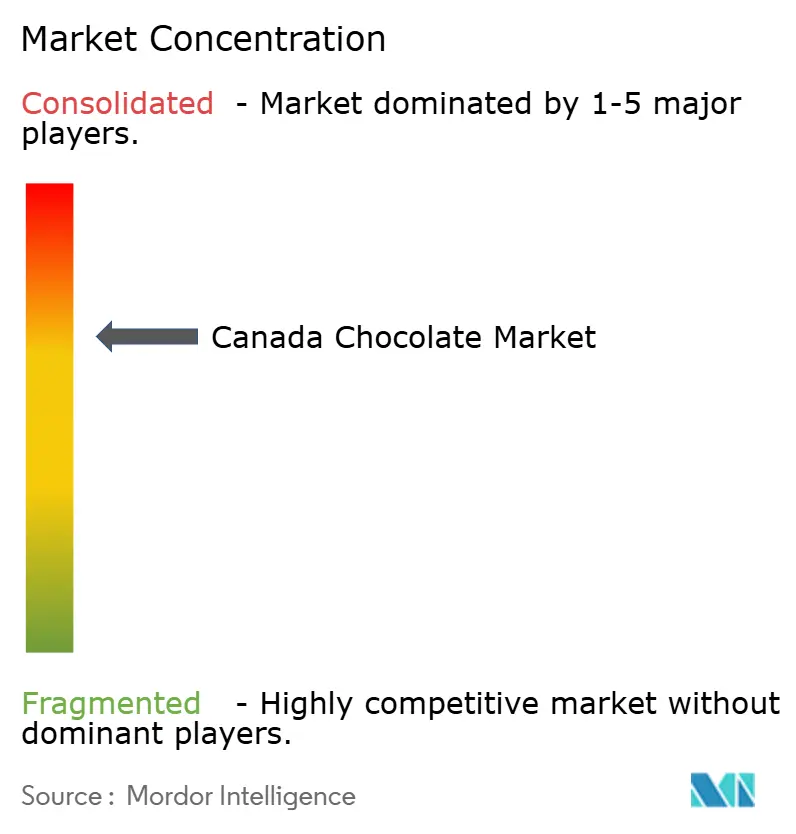

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Chocolate Market Analysis by Mordor Intelligence

The Canada chocolate market size is estimated to be valued at USD 3.87 billion in 2026 and is projected to reach USD 5.30 billion by 2031, supported by a 6.51% CAGR. Strong per-capita consumption, premiumization, and a growing “better-for-you” portfolio keep demand resilient even as volatile cocoa input costs tighten margins. Front-of-package labeling rules that take effect in 2026 are expected to accelerate reformulations with reduced sugar and functional ingredients, while plant-based offerings are projected to expand shelf space in urban centers. Premium single-origin tablets, craft bean-to-bar assortments, and seasonal gifting assortments attract higher spending despite inflation, reflecting a willingness to trade up for provenance, ethics, and flavor experimentation. At the same time, production investments topping CAD 700 million in Ontario and Quebec signal confidence in the Canadian chocolate market’s long-term demand, with automation, Internet of Things upgrades, and specialty sugar-free lines aimed at mitigating labor and ingredient cost spikes.

Key Report Takeaways

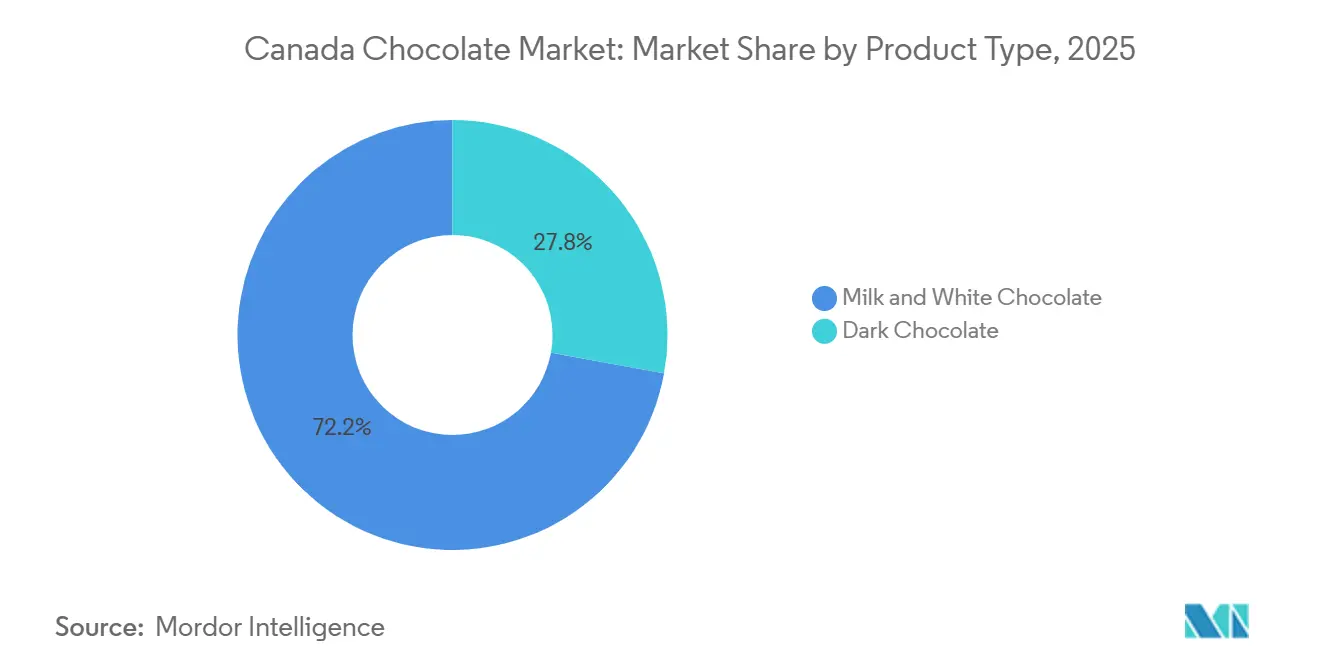

- By product type, milk and white chocolate led with 72.16% of the Canada chocolate market share in 2025, while dark chocolate is advancing at a 7.04% CAGR through 2031.

- By form, tablets and bars accounted for 44.95% share of the Canada chocolate market size in 2025, and pralines and truffles are projected to expand at a 6.54% CAGR to 2031.

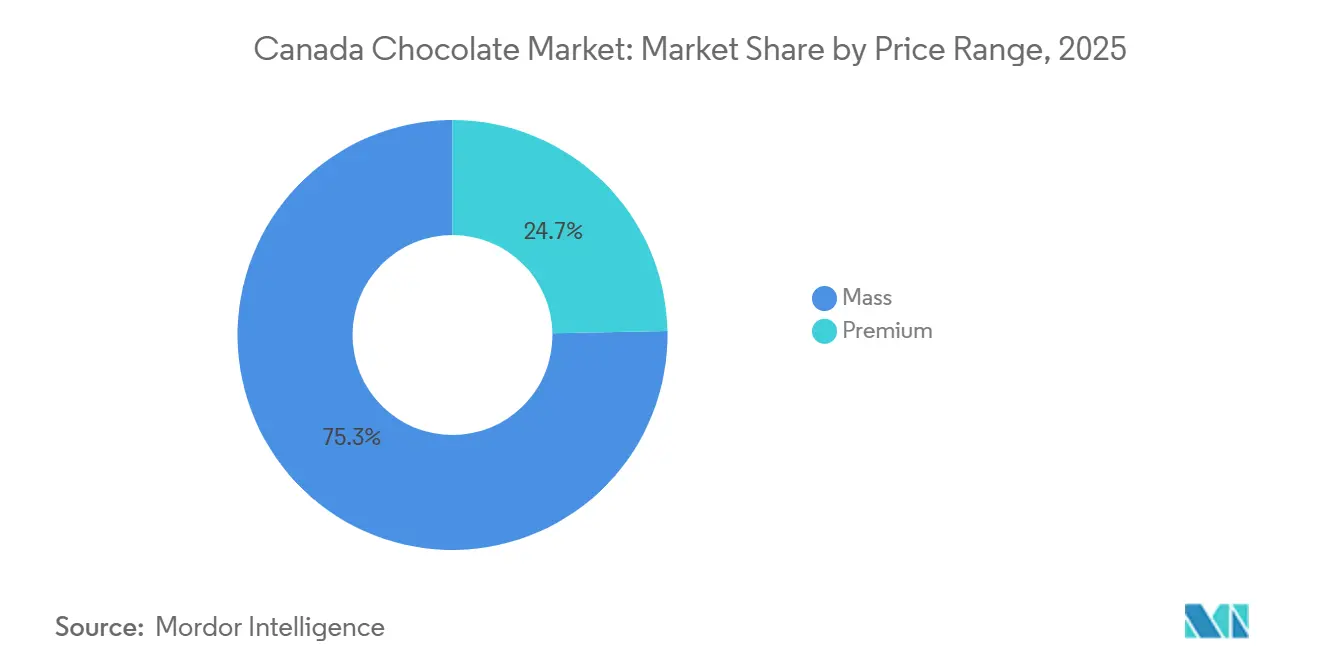

- By price range, the mass tier held 75.29% of the Canada chocolate market share in 2025, yet premium chocolate is forecast to grow at a 7.25% CAGR between 2026 and 2031.

- By distribution channel, supermarkets and hypermarkets captured 45.37% revenue share in 2025, while online retail stores are growing fastest at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Chocolate Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and wellness shift toward better-for-you chocolate | +1.2% | National, with stronger uptake in British Columbia and urban Ontario | Medium term (2-4 years) |

| Growth of plant-based and diet-specific chocolate | +0.9% | National, concentrated in Quebec and British Columbia | Medium term (2-4 years) |

| Premiumization and craft chocolate culture | +1.5% | Central Canada (Ontario, Quebec), West Coast | Long term (≥ 4 years) |

| Innovation in flavors, formats, and experiences | +0.8% | National, early gains in Montreal, Toronto, Vancouver | Short term (≤ 2 years) |

| Bean-to-Bar craft transparency initiative | +0.6% | Central Canada and West Coast, with Quebec leading artisanal production | Long term (≥ 4 years) |

| Sustainability, ethics, and transparency | +0.7% | National, with premium positioning strongest in urban centers across all regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and wellness shift toward better-for-you chocolate

Health and wellness concerns are reshaping consumer preferences in the chocolate market, with manufacturers focusing on portion control, sugar reduction, and functional ingredients as key strategies. Companies are introducing smaller portion sizes and individually wrapped minis to promote mindful consumption, exemplified by Lindt and Ferrero, which segment products into smaller, indulgent pieces that help consumers moderate intake. Concurrently, brands are reducing sucrose levels or adopting no-added-sugar formulations using alternatives like polyols or stevia, as seen in no-sugar-added lines from Hershey’s and private-label offerings in Canadian grocery chains, catering to sugar-conscious consumers. This shift is closely linked to rising concerns about metabolic health, with StatCan reporting that approximately 9% of Canadian adults were diagnosed with diabetes in 2024, intensifying scrutiny of sugar-heavy confectionery and driving demand for lower-glycemic chocolate options [1]Source: Statistics Canada, "Health Indicator Statistics, Annual Estimates", statcan.gc.ca. Dark chocolate with higher cocoa content and simpler ingredient lists has gained mainstream acceptance as a "permissible indulgence," reflected in expanded dark assortments from brands like Cadbury and other multinational players. Functional innovations, such as the inclusion of protein, fiber, or ingredients associated with mood and relaxation, are also becoming prominent alongside sugar reduction. Niche brands are leveraging these trends by offering protein-enriched chocolates or adaptogen-infused bars, positioning their products between confectionery and wellness snacks. Retailers are reinforcing this shift by clustering sugar-free, organic, and high-cacao chocolates together on shelves and online platforms, reframing chocolate as a balanced treat within the broader health-conscious category. This holistic approach, driven by medical and lifestyle concerns, is translating into tangible "better-for-you" chocolate options across the market.

Growth of plant-based and diet-specific chocolate

The demand for dairy-free chocolate is evolving from a niche category to a mainstream offering, driven by the increasing influence of plant-based and diet-specific preferences. Factors such as lactose intolerance, veganism, and environmental concerns are converging to shape innovation in this segment. Plant-based milk alternatives, including oat, almond, and coconut, are replacing dairy in chocolate formulations, enabling brands to deliver a creamy texture without animal-derived ingredients. For instance, Galaxy offers plant-based bars in the Canadian market through specialty and e-commerce channels. This trend aligns with shifting dietary habits, as approximately 1.5% of Canadians in 2023 reported following a vegan diet in the Foodbook 2.0 national survey [2]Source: Government of Canada, "Foodbook 2.0 Report", canada.ca . While this group remains relatively small, it significantly influences retail assortments and foodservice menus by normalizing vegan options. Vegan positioning also appeals to flexitarian and lactose-intolerant consumers who may not fully identify as vegan but still seek dairy-free alternatives for comfort or digestive reasons. This has encouraged mainstream brands to introduce clearly labeled “dairy-free” SKUs alongside their traditional product lines. Environmental and animal-welfare considerations further enhance the appeal of plant-based chocolate, with brands such as Endangered Species and certain Canadian bean-to-bar producers emphasizing reduced reliance on livestock and sustainable sourcing practices for cacao and plant-based milk ingredients. Packaging often highlights multiple diet-specific claims, such as vegan, lactose-free, keto-friendly, or low-sugar, enabling these products to cater to ethical, health-conscious, and allergen-aware consumers simultaneously. Retailers support this shift by merchandising plant-based chocolate in dedicated free-from sections or clearly marked plant-based aisles, simplifying the shopping experience. As plant-based chocolate options expand across supermarkets, specialty stores, and online platforms, dairy-free chocolate is increasingly viewed as a legitimate and flavorful alternative that satisfies indulgence, ethical considerations, and dietary needs in a single purchase.

Premiumization and craft chocolate culture

Consumers are increasingly trading up from mainstream chocolate offerings to premium products that emphasize provenance, single-origin transparency, and bean-to-bar craftsmanship. This shift is driven by a demand for not just superior taste but also a clear narrative about the origins and production processes of chocolate. Single-origin bars, detailing country, region, or estate-level cacao, signal quality and authenticity, while traceability assures consumers that higher prices reflect verified sourcing rather than branding. Bean-to-bar producers enhance this appeal by controlling the entire process, from cocoa bean selection to roasting, refining, and molding, showcasing craftsmanship that contrasts with the uniformity of mass-market brands. Established players like Purdys Chocolatier, operating over 75 stores nationwide and committed to 100% sustainable cocoa sourcing since 2014, exemplify how provenance and ethical sourcing can be integrated into a premium brand narrative. This approach appeals to consumers seeking indulgence paired with social responsibility. Sustainable sourcing stories reinforce the perception that premium chocolate is not only about flavor and texture but also about supporting better practices in cocoa farming communities, further differentiating craft and premium brands from lower-cost alternatives. As consumers become more informed about cacao origins, flavor profiles, and production methods, they increasingly treat chocolate like specialty coffee or wine, considering terroir and craftsmanship in their choices. Retailers are responding by dedicating more shelf space and prominent displays to premium and craft brands, grouping single-origin, fair trade, and bean-to-bar products, making the trade-up path visually clear. These dynamics position premiumization and craft culture as structural drivers, gradually shifting value share toward brands offering provenance, artisanal quality, and sustainability.

Sustainability, ethics, and transparency

Sustainability, ethics, and transparency are increasingly influencing purchasing decisions in the chocolate market, as consumers demand assurance that products are produced responsibly without harming people or the environment. Ethical cocoa sourcing initiatives, such as Fairtrade, Rainforest Alliance, or company-led sustainable cocoa programs, provide confidence that farmers are fairly compensated and critical issues like child labor and deforestation are being addressed. This drives consumer preference for brands that can document their supply chains. Transparent communication about the origin of cacao (country or region), farming practices, and traceability systems further strengthens trust by offering visibility into the journey of cocoa beans through the value chain, rather than relying on generic claims like “responsibly sourced.” Companies are responding by publishing sustainability commitments, impact reports, and sourcing milestones, while prominently displaying certification logos and origin stories on packaging to highlight ethical value propositions. Packaging sustainability is also a critical focus, with brands adopting recyclable paper wraps, reduced plastic, or compostable materials to align packaging with the ethical positioning of the product. Innovations such as upcycled or minimally wasted cacao products, which utilize more of the cocoa fruit, reflect circular-economy principles and appeal to environmentally conscious consumers seeking tangible waste-reduction efforts. Retailers are reinforcing this trend by increasing visibility and offering dedicated shelf space for ethically positioned chocolate, rewarding brands that invest in credible sustainability programs. Overall, sustainability, ethics, and transparency are driving value toward chocolate brands that demonstrate measurable progress and avoid vague environmental claims.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressures on sugar, labeling, and marketing | -0.6% | National, with Quebec facing additional child-marketing restrictions | Short term (≤ 2 years) |

| Volatility and risk in cocoa and ingredient supply | -1.1% | National, affecting all manufacturers reliant on West African cocoa | Short term (≤ 2 years) |

| Operational and margin pressures from input and packaging costs | -0.8% | National, disproportionately impacting small-to-mid-size manufacturers in Quebec and Ontario | Short term (≤ 2 years) |

| Intensifying competition and shelf saturation | -0.5% | National, most acute in Central Canada where retail density is highest | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory pressures on sugar, labeling, and marketing

Regulatory pressures related to sugar, labeling, and marketing are creating significant challenges for chocolate manufacturers in Canada. These regulations compel technical reformulations, restrict traditional promotional strategies, and increase compliance costs, which are particularly difficult to manage in price-sensitive segments. The Front-of-Package Nutrition Labeling rules, effective January 1, 2026, require "high-in" symbols for products exceeding 15% of the daily value for saturated fat, sodium, or sugar per serving [3]Source: Government of Canada, "Nutrition Labelling: Front-of-Package Nutrition Symbol", canada.ca. This forces mainstream brands to either reformulate existing products or accept prominent warnings that could drive health-conscious consumers toward competitors offering "cleaner" alternatives. Health Canada’s phased implementation grants smaller producers a two-year grace period, creating a temporary competitive imbalance as they can delay costly changes and maintain cleaner packaging, while larger companies must comply immediately. Quebec’s Consumer Protection Act further complicates marketing efforts by prohibiting advertising targeting children under 13, restricting the use of cartoon mascots, child-focused graphics, and promotional premiums still allowed in other provinces. This increases creative, packaging, and media-planning complexity for national companies like Nestlé or Mars, which must comply with Quebec’s rules while maintaining brand consistency across Canada. Additionally, strict product definitions under the Food and Drug Regulations limit cost-reduction strategies, as dark, milk, and white chocolate must meet specific cocoa and milk solid content requirements to retain their legal classification. Rising input prices and compliance demands exacerbate these constraints. Mandatory Salmonella testing and restrictions on emulsifiers like lecithin further increase quality-control and formulation costs, disproportionately affecting smaller producers without the scale or internal labs of larger players like Ferrero or Mondelez. Combined, these sugar warnings, marketing restrictions, compositional standards, and microbiological controls compress margins and reduce strategic flexibility, particularly for brands balancing premium reformulation costs with a price-sensitive consumer base.

Volatility and risk in cocoa and ingredient supply

Volatility and risks in cocoa and ingredient supply pose significant challenges for manufacturers in the chocolate industry. These businesses are structurally exposed to global shocks beyond their control, which they must either absorb or pass on to consumers. Cocoa prices reached approximately USD 12,000 per metric ton in April 2024, a 46-year high, following a 35% decline in cocoa output in Ghana and a 28% drop in Côte d’Ivoire, driven by El Niño-induced irregular rainfall, the swollen shoot virus, and aging tree stock. This price surge, representing a 65% year-over-year increase, significantly raised raw material costs for Canadian chocolate manufacturers, who rely heavily on West African cocoa supplies. The resulting cost pressures compressed margins and led to repeated adjustments in retail pricing and promotions, risking demand loss as price-sensitive consumers shifted to cheaper private-label products or alternative snacks. Larger branded players, such as Mondelez and Mars, faced difficult decisions, including reformulating products with less cocoa, reducing package sizes, or directly increasing prices, each of which carries risks to brand equity and sales volumes. Smaller chocolatiers and bean-to-bar producers were more severely impacted, as they often source higher-quality or certified cocoa beans and lack the hedging capabilities or negotiating power of larger manufacturers, leaving them vulnerable to spot-market price volatility. Compounding the issue, rising costs of related inputs like sugar, dairy ingredients, and specialty fats made it harder to offset cocoa price increases. Logistics disruptions and extended lead times further increased working capital requirements, while retailers resisted price hikes or demanded more frequent promotions, forcing suppliers to absorb a disproportionate share of the cost burden. These factors collectively create sustained profitability pressures and strategic uncertainty, limiting the ability of chocolate brands to invest in innovation while maintaining affordable prices.

Segment Analysis

By Product Type: Dark Chocolate Gains on Health Positioning

Milk and white chocolate continue to dominate the market value, accounting for approximately 72.16% of the market share in 2025. Their appeal is rooted in mass-market positioning, seasonal gifting traditions, and strong brand loyalty. Formats such as Easter figures, holiday assortments, and classic bars remain popular, driven by taste familiarity and emotional connections that often outweigh health considerations. However, growth in the milk chocolate segment is slowing as health-conscious consumers reduce consumption frequency or opt for dark chocolate alternatives. Manufacturers are addressing this trend by introducing plant-based and "lighter" milk chocolate options, such as Hershey’s Oat Made line and Lindt’s Lindor Oat Milk Truffles, which provide dairy-free alternatives while maintaining indulgence. White chocolate remains a niche product due to its regulatory definition, which limits its ability to leverage health-related narratives tied to cocoa content. Instead, it focuses on taste-driven applications such as coatings, inclusions, and desserts.

Dark chocolate is increasingly recognized as a significant growth driver within the chocolate market, with an expected annual growth rate of approximately 7.04% from 2026 to 2031. This growth trajectory surpasses that of milk and white chocolate, largely due to dark chocolate's association with health benefits. Consumers perceive higher cocoa content as a source of antioxidants and potential cardiovascular advantages, positioning dark chocolate as a "permissible indulgence" rather than a purely indulgent treat. Canadian Food and Drug Regulations define dark chocolate as containing at least 35% cocoa solids, including a minimum of 18% cocoa butter and 14% fat-free cocoa solids. This regulatory framework enables manufacturers to balance meaningful cocoa content with adjustments in sweetness and texture. Additionally, as regulatory pressures on sugar reduction and front-of-package labeling intensify, dark chocolate's naturally higher cocoa content and lower sugar profile align well with evolving consumer and regulatory expectations. Brands such as Lindt have responded by expanding their dark chocolate offerings, introducing new flavor variants, and premium formats aimed at health-conscious consumers. This shift has driven a migration of consumers from traditional milk chocolate bars to smaller, higher-cocoa-content portions, increasing the value share of dark chocolate despite moderated consumption per occasion. Collectively, dark chocolate is positioned as the fastest-growing product type, while milk and white chocolate rely on innovation in plant-based options, formats, and occasion-based positioning to sustain their market presence in a health-conscious environment.

By Form: Pralines and Truffles Capitalize on Gifting Premiumization

Pralines and truffles are gaining significant traction as a high-growth segment, fueled by the rising trend of premiumization in gifting. While tablets and bars are projected to maintain their dominant position with a 44.95% market share in 2025, driven by their role in everyday snacking and impulse purchases, pralines and truffles are expected to grow at a robust 6.54% CAGR through 2031. This growth reflects evolving consumer preferences, with buyers increasingly willing to invest in curated assortments, sophisticated packaging, and indulgent textures for special occasions or personal indulgence. Lindt Lindor truffles exemplify this trend, setting a benchmark for premium praline-style products. The brand’s introduction of oat milk variants highlights how dairy-free innovation can expand its market reach while preserving the signature melt-in-mouth filling that defines its premium positioning.

In contrast, molded blocks primarily serve industrial and foodservice applications, such as baking, coating, and dessert manufacturing, where cost efficiency, processability, and heat resistance are prioritized over brand storytelling or luxury appeal. These products, often sold business-to-business, face challenges of commoditization due to their limited visibility on retail shelves and weaker alignment with the emotional and aspirational dimensions driving premiumization. Meanwhile, "other forms" of chocolate, including chocolate-coated nuts, fruits, and novelty shapes, experience seasonal demand spikes during occasions like Easter and Christmas. Although these products capitalize on fun formats and festive packaging, their margins are increasingly under pressure as retailers promote private-label alternatives that mimic branded concepts at lower price points. This dynamic further strengthens the competitive edge of strongly branded praline and truffle assortments in the premium gifting category.

By Price Range: Premium Segment Outpaces Mass Despite Inflation

The premium chocolate segment is poised for robust growth, with an anticipated annual expansion rate of approximately 7.25% from 2026 to 2031. This growth is driven by increasing consumer preference for craft chocolate culture, single-origin transparency, and a willingness to pay a premium for attributes such as provenance, artistry, and traceability. Urban, educated consumers are leading this shift, favoring premium offerings over mass-market products. JACEK Chocolate in Alberta exemplifies this trend, operating as a bean-to-bar producer distributed through around 200 retailers. Its premium pricing is supported by International Chocolate Awards recognition and full bean-to-bar traceability, providing consumers with a compelling reason to trade up. Meanwhile, the mass chocolate segment, which held approximately 75.29% of the market share in 2025, continues to dominate due to its extensive distribution, aggressive promotions, and strong brand loyalty. However, its growth is slowing as sugar-reduction mandates and front-of-package "high-in sugar" warnings impact consumer perceptions of traditional large bars and family packs.

Private-label chocolate is capitalizing on these challenges in the mass segment, gaining traction in discount banners and mainstream supermarkets by leveraging lower cost structures and retailer-controlled shelf placement. This allows private labels to undercut branded mass players on price while narrowing perceived quality gaps. In response, established brands are adopting tiered strategies to remain competitive. For instance, Lindt offers a range of products, Swiss Luxury, EXCELLENCE, and Lindor, that span premium and accessible-premium price points. Similarly, in 2025, Ferrero’s CAD 445 million investment in its Ontario facility to produce Ferrero Rocher chocolate squares highlights how global players are extending iconic premium brands into more accessible formats. These strategies enable brands to compete effectively in both gifting and everyday indulgence categories, reinforcing the premium segment's outperformance even in an inflationary environment.

By Distribution Channel: Online Retail Surges on Convenience and Assortment

Supermarkets and hypermarkets continue to anchor the Canadian chocolate market, commanding approximately 45.37% of the market share in 2025. This dominance is driven by strong foot traffic, impulse-driven checkout purchases, and high-visibility promotional end-caps. However, the online retail segment is rapidly gaining traction, with a projected growth rate of 6.72% through 2031. This growth is underpinned by Canada’s high internet penetration of around 95% in 2025, increased consumer reliance on e-commerce post-pandemic, and manufacturers’ strategic focus on direct-to-consumer and marketplace models. The rise of same-day and next-day delivery services from platforms such as Instacart, Amazon Fresh, Walmart+, and other grocery delivery providers has further compressed the purchase-to-consumption cycle. This convenience enables consumers to address spontaneous chocolate cravings and last-minute gifting needs without visiting physical stores. Premium and specialty players are also leveraging omnichannel strategies to enhance their market presence. For example, Jeff de Bruges integrates its physical boutiques in Montreal and Laval with same-day delivery on the island of Montreal via Uber Eats, blending experiential in-store retail with digital convenience.

While supermarket sales remain resilient, with a 5.8% growth in 2023 reflecting strong traffic and promotional intensity, the channel faces mounting challenges. These include margin pressures from private-label expansion, retailer-imposed slotting fees, and the need to sustain aggressive promotions to defend market share against discounters and online competitors. In response, manufacturers are increasingly prioritizing online channels to engage Gen Z and Millennial consumers, who value convenience, diverse product assortments, and access to niche or craft brands. Investments in direct-to-consumer websites, subscription services, and targeted digital marketing are reshaping the distribution landscape, gradually shifting the channel mix in favor of e-commerce.

Geography Analysis

Central Canada, led by Ontario and Quebec, serves as the structural foundation for the country’s chocolate industry. This region combines key factors, including population density, major urban centers, and higher purchasing power, which collectively drive both mass-market and premium chocolate development. Ontario has emerged as a strategic production hub, supported by significant investments, such as Ferrero’s CAD 445 million expansion in Brantford in 2025 and Blommer Chocolate’s CAD 80 million (USD 57 million) expansion in Campbellford, which is expected to be completed by 2026. These investments underscore Ontario’s importance as a North American supply hub, leveraging its proximity to the United States border, skilled workforce, and advanced logistics infrastructure. Meanwhile, Quebec’s artisanal chocolate sector, with approximately 200 chocolateries, adds a premium dimension to the market. Renowned bean-to-bar producers such as Chaleur B Chocolat and Palette de Bine craft terroir-driven, small-batch chocolates that complement Ontario’s industrial scale. Urban centers like Toronto further enhance this ecosystem by supporting brands like ChocoSol Traders, which focus on ethical sourcing and cater to consumers seeking single-origin, stone-ground, and culturally inspired flavor profiles. Together, Ontario and Quebec not only dominate production and consumption but also set creative and quality benchmarks for the entire country.

On the West Coast, particularly in British Columbia, consumer preferences lean toward health-conscious and sustainability-driven products. The region demonstrates strong demand for craft chocolate, certifications, and plant-based options. Companies like Beanpod Chocolate in Fernie exemplify this trend by utilizing stone grinding and organic cacao sourced directly from farmers, aligning with ethical sourcing and artisanal techniques. Urban centers such as Vancouver and Victoria further reinforce this orientation by supporting premium pricing and experiential retail. Chocolateries in these cities often host tastings and workshops, transforming chocolate purchasing into an educational and social experience that fosters brand loyalty. Moving inland, the Prairie Provinces, Alberta, Saskatchewan, and Manitoba, are more value-conscious and tied to agricultural economies. However, craft chocolate brands like Alberta-based JACEK Chocolate are gaining traction, with distribution through approximately 200 retailers and recognition from multiple International Chocolate Awards, proving that design-forward, storytelling-driven brands can thrive beyond major metropolitan areas.

In Atlantic Canada, smaller provincial markets such as Nova Scotia and Prince Edward Island rely heavily on seasonal tourism. Companies like Newfoundland Chocolate Company and local artisans capitalize on this by incorporating regional ingredients and leveraging gift-shop distribution to meet niche, souvenir-driven demand during peak tourist seasons. The Northern Territories, Yukon, Northwest Territories, and Nunavut, face challenges such as high logistics costs, sparse populations, and limited infrastructure. Despite these constraints, specialty retailers and online platforms enable consumers to access both mass-market and premium chocolate brands, albeit at higher prices and with limited assortments. Collectively, these regional dynamics highlight the diverse nature of the Canadian chocolate industry. Central Canada provides the industrial backbone and innovation hub, the West Coast leads in health-conscious and sustainability-driven narratives, the Prairies balance value-consciousness with emerging craft brands, Atlantic Canada leverages tourism-driven demand, and the Northern Territories rely on hybrid access models. This mosaic of regional demand profiles underscores the importance of tailored strategies for manufacturers and retailers operating in this market.

Competitive Landscape

Dominated by multinational giants such as Mondelēz, Mars, Hershey, Nestlé, Lindt, and Ferrero, the chocolate sector in Canada reflects moderate consolidation, with a concentration score of approximately 7 out of 10. These industry leaders leverage economies of scale, extensive promotional budgets, and strong retailer partnerships to secure prime shelf placements and end-cap displays, enabling them to dictate category dynamics, from pricing strategies to seasonal activations. Smaller craft and bean-to-bar producers, on the other hand, focus on premium niches by emphasizing provenance, competition accolades, and direct-to-consumer channels that bypass traditional retail gatekeepers. The competitive landscape is distinctly bifurcated, with mass-market players prioritizing cost efficiencies, high promotional intensity, and reformulation to meet front-of-package labeling mandates, while premium brands differentiate through single-origin transparency, ethical sourcing narratives, and experiential retail formats like in-store tastings or pop-up events. Certifications such as Rainforest Alliance and Fair Trade have become essential, with companies like Nestlé and Ferrero making significant commitments to align with ethical consumer expectations and mitigate reputational risks.

Strategic investments by market leaders underscore their adaptability to evolving regulatory and consumer demands. For instance, Ferrero’s CAD 445 million (USD 318 million) Ontario expansion in 2025 integrates advanced technologies such as Internet of Things (IoT) monitoring and robotics to enhance productivity. This investment also supports the launch of localized innovations like Ferrero Rocher chocolate squares and Nutella Biscuits, targeting share gains in both premium gifting and everyday snacking categories. Meanwhile, private-label chocolate continues to erode branded mass-market territory by leveraging retailer-controlled shelf space and cost advantages, offering credible quality at lower prices. Emerging disruptors, such as Quebec artisans like Damien André, are leveraging digital platforms like Instagram and TikTok to engage Gen Z audiences, rapidly prototyping and launching viral products. These trends compel even established players to innovate, as seen with Lindt’s tiered sub-brands and Nestlé’s certification initiatives, blending defensive scale strategies with offensive innovation to maintain their competitive edge.

White-space opportunities present significant potential to reshape competitive dynamics. Hyper-local terroir positioning, using Canadian-grown ingredients or regionally inspired flavors, allows craft makers to stand out and foster loyalty among consumers seeking “made-in-Canada” authenticity. Subscription models offering curated boxes or monthly bean-to-bar drops provide recurring revenue streams and valuable consumer data, enabling smaller players to bypass retailer influence and appeal to urban professionals. Functional chocolate innovations, incorporating adaptogens, probiotics, or collagen, bridge indulgence with wellness, positioning products at the intersection of confectionery and health supplements. While these areas remain fragmented due to the specialized research and development and niche marketing they require, they represent opportunities for disruptors to evolve into influential mid-tier competitors. Success in this dynamic market hinges on balancing defensive strengths with proactive investments in emerging trends, ensuring adaptability in a landscape where consolidation coexists with vibrant competition.

Canada Chocolate Industry Leaders

-

Chocoladefabriken Lindt & Sprüngli AG

-

Mondelēz International Inc.

-

Nestlé SA

-

The Hershey Company

-

Mars Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Ferrero Canada announced the launch of its new Ferrero Rocher chocolate squares production line at the Brantford, Ontario, manufacturing facility, marking the first production of this product. This development was part of Ferrero's CAD 445 million investment in its Canadian operations.

- October 2025: Avolta partnered with Belgian chocolatier La Louvière to introduce the Toronto City Collection, an exclusive chocolate line celebrating the city of Toronto. The collection became available on 25 October in duty-free stores operated by Avolta's subsidiary, Dufry, at Toronto Pearson International Airport and Billy Bishop Toronto City Airport. The range included three flavors: milk chocolate, dark chocolate, and milk chocolate with pistachio, each packaged in designs showcasing Toronto landmarks.

- September 2025: Lindt & Sprüngli, a global leader in premium chocolate, announced the launch of the Lindt Dubai Style Chocolate Bar in Canada. Inspired by the Dubai chocolate trend, Lindt's Maître Chocolatiers developed a bar combining smooth Lindt milk chocolate with a pistachio-rich filling (45% pistachios) and crispy kadayif, delicate "angel hair" dough threads that provided a unique texture complementing Lindt's signature milk chocolate.

Canada Chocolate Market Report Scope

Dark Chocolate, Milk and White Chocolate are covered as segments by Confectionery Variant. Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others are covered as segments by Distribution Channel.| Dark Chocolate |

| Milk and White Chocolate |

| Tablets and Bars |

| Molded Blocks |

| Pralines and Truffles |

| Other Forms |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Dark Chocolate |

| Milk and White Chocolate | |

| By Form | Tablets and Bars |

| Molded Blocks | |

| Pralines and Truffles | |

| Other Forms | |

| By Price Range | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Market Definition

- Milk and White Chocolate - Milk chocolates is a solid chocolate made with milk (in the form of either milk powder, liquid milk, or condensed milk) and cocoa solids. White chocolate is made from cocoa butter and milk and contains no cocoa solids whatsoever. The scope includes regular chocolates, low-sugar, and sugar-free variants

- Toffees & Nougats - Toffees include hard, chewy, and small or one-bite candies marketed with labels as toffee or toffee-like confectionery. Nougat is a chewy confection with almond, sugar, and egg white as a basic ingredient; and it originated in Europe and Middle East countries.

- Cereals Bars - A snack composed of breakfast cereal that has been compressed into a bar shape and is held together with a form of edible adhesive. The scope includes snack bars made with cereals such as rice, oats, corn, etc. mixed with a binding syrup. These also include products labeled as cereal bars, cereal treat bars, or grain bars.

- Chewing Gum - This is a preparation for chewing, usually made of flavored and sweetened chicle or such substitutes as polyvinyl acetate. The types of chewing gums included in the scope are sugar-chewing gums and sugar-free chewing gums

| Keyword | Definition |

|---|---|

| Dark Chocolate | Dark chocolate is a form of chocolate containing cocoa solids and cocoa butter without the milk. |

| White Chocolate | White chocolate is the type of chocolate containing the highest percentage of milk solids, typically around or over 30 percent. |

| Milk Chocolate | Milk chocolate is made from dark chocolate that has a low cocoa solid content and higher sugar content, plus a milk product. |

| Hard Candy | A candy made of sugar and corn syrup boiled without crystallizing. |

| Toffees | A hard, chewy, often brown sweet that is made from sugar boiled with butter. |

| Nougats | A chewy or brittle candy containing almonds or other nuts and sometimes fruit. |

| Cereal bar | A cereal bar is a bar-shaped food product, made by pressing cereals and usually dried fruit or berries, which are in most cases held together by glucose syrup. |

| Protein bar | Protein bars are nutrition bars that contain a high proportion of protein to carbohydrates/fats. |

| Fruit & Nut bar | These are often based on dates with other dried fruit and nut additions and, in some cases, flavorings. |

| NCA | The National Confectioners Association is an American trade organization that promotes chocolate, candy, gum and mints, and the companies that make these treats. |

| CGMP | Current good manufacturing practices are those conforming to the guidelines recommended by relevant agencies. |

| Unstandardized foods | Unstandardized foods are those that do not have a standard of identity or that deviate from a prescribed standard in any manner. |

| GI | The glycemic index (GI) is a way of ranking carbohydrate-containing foods based on how slowly or quickly they are digested and increase blood glucose levels over a period of time |

| Skimmed milk powder | Skimmed milk powder is obtained by removing water from pasteurized skim milk by spray-drying. |

| Flavanols | Flavanols are a group of compounds found in cocoa, tea, apples, and many other plant-based foods and beverages. |

| WPC | Whey protein concentrate- the substance obtained by the removal of sufficient nonprotein constituents from pasteurized whey so that the finished dry product contains greater than 25% protein. |

| LDL | Low density Lipoprotein- the bad cholesterol |

| HDL | High density Lipoprotein- the good cholesterol |

| BHT | butylated Hydroxytoluene is a lab-made chemical that is added to foods as a preservative. |

| Carrageenan | Carrageenan is an additive used to thicken, emulsify, and preserve foods and drinks. |

| Free form | Not containing certain ingredients, such as gluten, dairy, or sugar. |

| Cocoa butter | It is a fatty substance obtained from cocoa beans, used in the manufacture of confectionery. |

| Pastellies | A type of of Brazilian candy made from sugar, eggs, and milk. |

| Draggees | Small, round candies that are coated with a hard sugar shell |

| CHOPRABISCO | Royal Belgian Association of the chocolate, pralines, biscuit, and confectionery industry- A trade association that represents the Belgian chocolate industry. |

| European Directive 2000/13 | A European Union directive that regulates the labeling of food products |

| Kakao-Verordnung | The German chocolate ordinance, a set of regulations that define what can be labeled as "chocolate" in Germany. |

| FASFC | Federal Agency for the Safety of the Food Chain |

| Pectin | A natural substance that is derived from fruits and vegetables. It is used in confectionery to create a gel-like texture. |

| Invert sugars | A type of sugar that is made up of glucose and fructose. |

| Emulsifier | A substance that helps to mix to liquids that does not mix together. |

| Anthocyanins | A type of flavonoid that is responsible for the red, purple, and blue colors of confectionery. |

| Functional Foods | Foods that have been modified to provide additional health benefits beyond basic nutrition. |

| Kosher certificate | This certification verifies that the ingredients, production process including all machinery, and/or food-service process complies with the standards of Jewish dietary law |

| Chicory root extract | A natural extract from the chicory root that is a good source of fiber, calcium, phosphorous, and folate |

| RDD | Recommended daily dose |

| Gummies | A chewy gelatin-based candy that is often flavored with fruit. |

| Nutraceuticals | Food or dietary supplements that are claimed to have health benefits. |

| Energy bars | Snack bars that are high in carbohydrates and calories are designed to provide energy on the go. |

| BFSO | Belgian Food Safety Organization for the food chain. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms