Calcium Channel Blocker Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

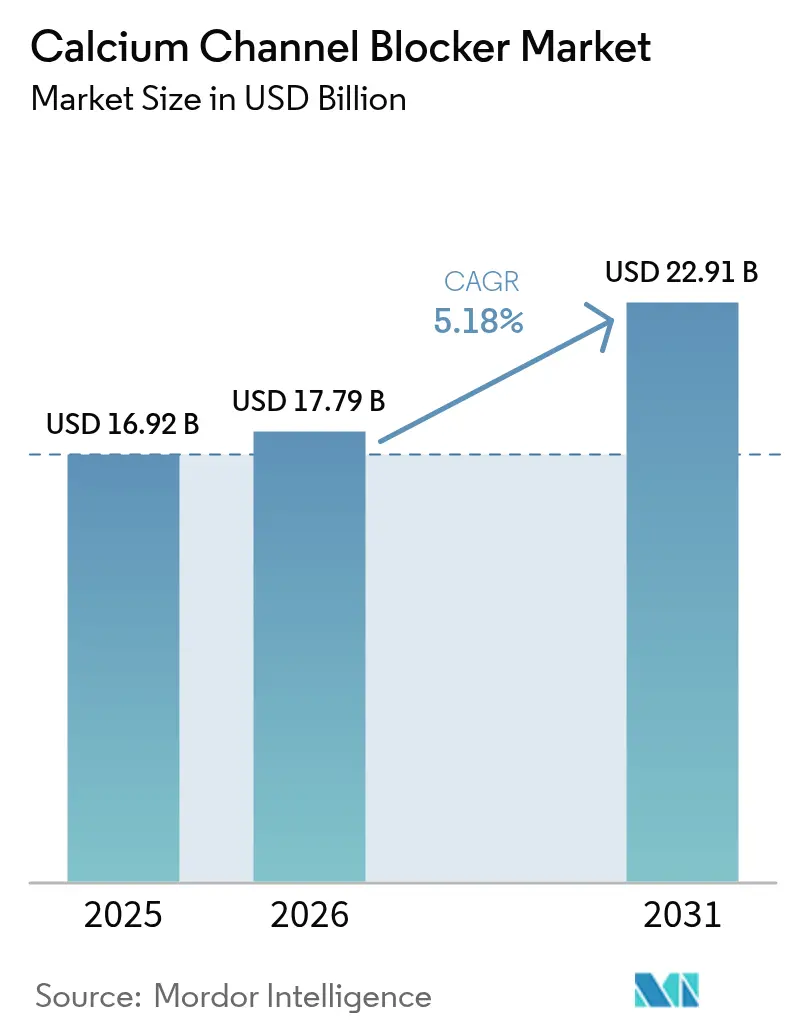

| Market Size (2026) | USD 17.79 Billion |

| Market Size (2031) | USD 22.91 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

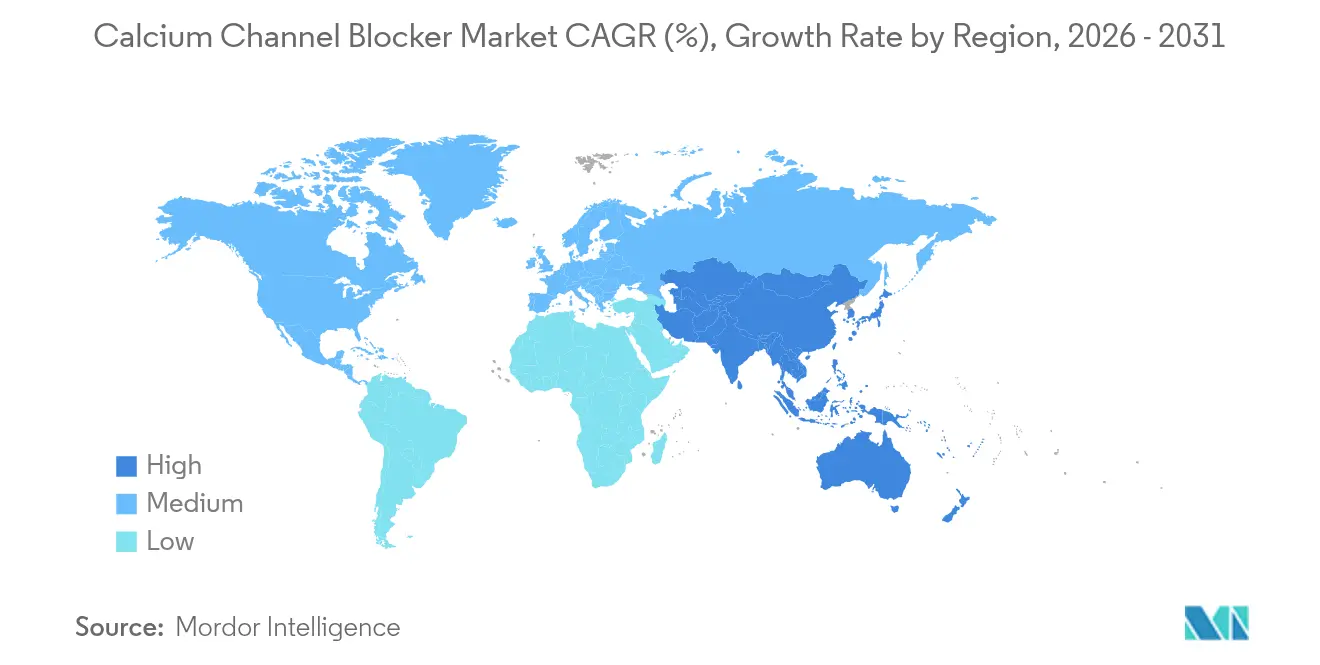

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

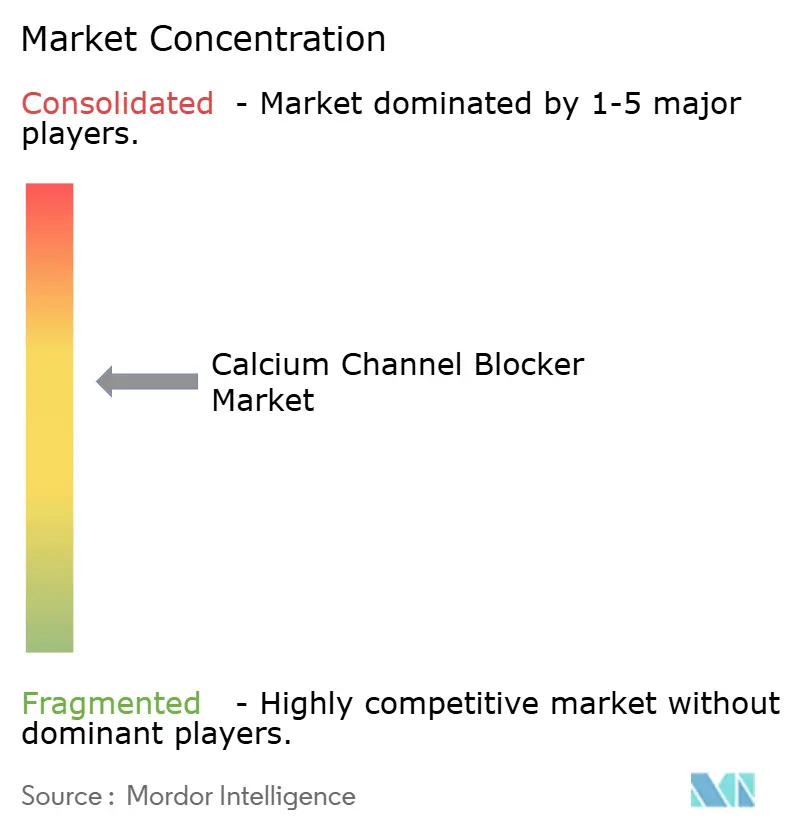

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Channel Blocker Market Analysis by Mordor Intelligence

calcium channel blocker market size in 2026 is estimated at USD 17.79 billion, growing from 2025 value of USD 16.92 billion with 2031 projections showing USD 22.91 billion, growing at 5.18% CAGR over 2026-2031. Demand continues to gain momentum because hypertension remains the most prevalent modifiable cardiovascular risk factor, the global population is aging, and combination tablets that simplify daily regimens are now standard in first-line therapy. Solid clinical evidence supports the class’s cerebrovascular protective effect, while fourth-generation agents that block multiple channel subtypes extend the therapeutic envelope. Companies are also benefitting from smoother generic entry in price‐sensitive economies, fresh fixed-dose approvals in the United States and Europe, and region-wide initiatives that expand reimbursement for chronic cardiovascular medicines. At the same time, manufacturers must manage tighter impurity limits, episodic active pharmaceutical ingredient (API) shortages, and intensifying competition from SGLT2 inhibitors and endothelin antagonists, all of which shape pricing and portfolio decisions.

Key Report Takeaways

- By drug class, dihydropyridines led with 61.78% of the calcium channel blocker market share in 2025, while non-dihydropyridines posted the fastest 7.12% CAGR through 2031.

- By indication, hypertension held 70.65% of the calcium channel blocker market size in 2025, whereas neurological disorders are projected to grow at 7.86% CAGR between 2026-2031.

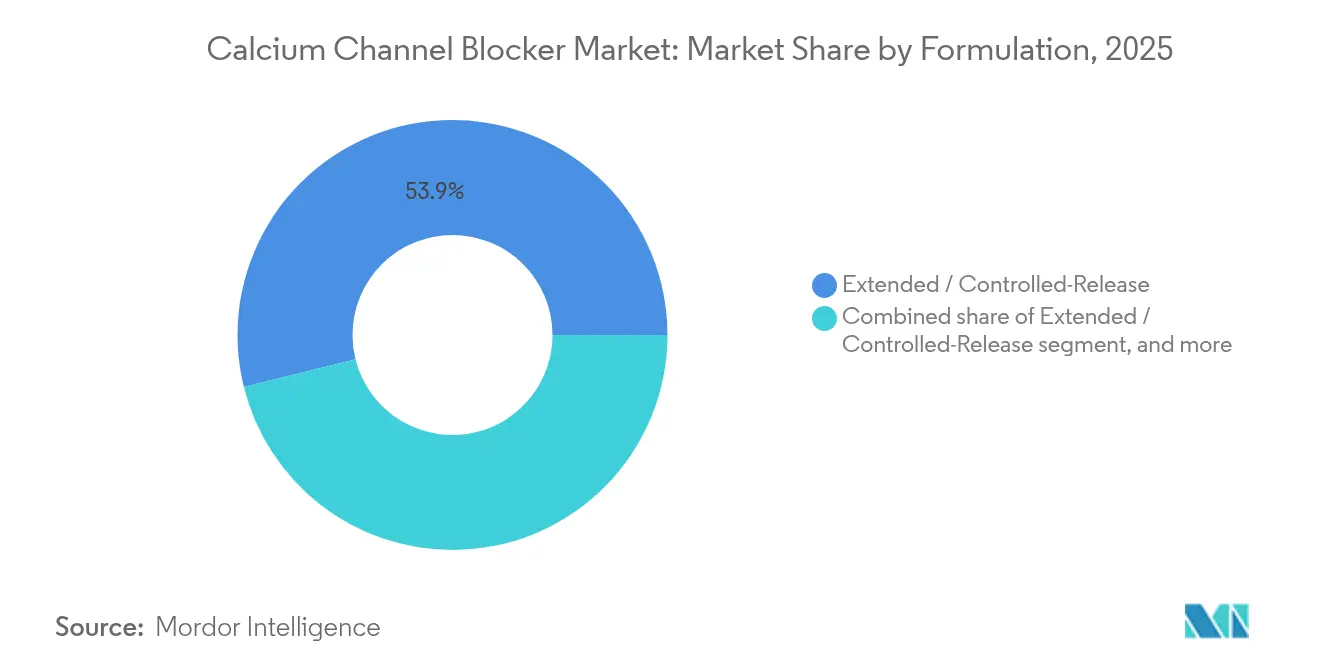

- By formulation, extended-release tablets dominated with 53.88% revenue in 2025; fixed-dose combinations are expanding at 7.41% CAGR to 2031.

- By distribution channel, retail pharmacies captured 45.96% in 2025, and hospital pharmacies are accelerating at 8.02% CAGR through 2031.

- By geography, North America commanded 39.12% regional revenue in 2025; Asia-Pacific is advancing at a 6.18% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Calcium Channel Blocker Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hypertension and cardiovascular disorders | +1.8% | Global; highest in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Growing geriatric population demanding long-term antihypertensive therapy | +1.2% | North America, Europe, Japan | Long term (≥ 4 years) |

| Increasing availability of affordable generic formulations | +0.9% | Global; strongest in price-sensitive markets | Medium term (2-4 years) |

| Expanding use of fixed-dose combination therapies to improve compliance | +0.8% | North America, Europe, global adoption | Medium term (2-4 years) |

| Emerging clinical evidence supporting neuroprotective applications | +0.4% | Developed markets | Long term (≥ 4 years) |

| Government initiatives for universal health coverage in emerging markets | +0.6% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population Demanding Long-Term Antihypertensive Therapy

The proportion of adults aged ≥ 65 years rose to 11% globally in 2024 and is climbing fastest in Japan and Southern Europe. Stroke risk doubles every decade after 55, and calcium channel blockers demonstrate durable protection without compromising renal function. A real-world study that followed 714,000 hypertensive seniors for 2.5 years linked continuous amlodipine therapy to lower dementia incidence relative to non-users. These overlapping cardiovascular and cognitive benefits encourage geriatricians to prioritize once-daily dihydropyridines in complex polypharmacy regimens, strengthening the growth trajectory of the calcium channel blocker market.

Increasing Availability of Affordable Generic Formulations

Amlodipine lost exclusivity in most territories years ago, shaving up to 70% off treatment costs and widening access among low-income patients. India and China now account for a majority of global API output, yet freight disruptions in 2025 briefly pushed ex-works prices up by double digits. Despite episodic volatility, therapeutic equivalence studies confirm that generic amlodipine delivers identical blood-pressure control, reassuring clinicians and supporting high substitution rates. Margin pressure from generics prompts originators to defend share through lifecycle strategies such as polypill launches and controlled-release reformulations.

Expanding Use of Fixed-Dose Combination Therapies to Improve Compliance

Four-in-ten treated hypertensive patients still fail to reach target blood pressure, driving the pivot toward fixed-dose combinations that merge complementary mechanisms in one tablet. The landmark ACCOMPLISH trial proved that pairing an ACE inhibitor with a dihydropyridine cut cardiovascular events more than a traditional ACE-diuretic pairing. Current guidelines in Europe and the United States now recommend initiating therapy with a two-drug combination in most patients, widening the commercial runway for products such as azilsartan-amlodipine, which posts the highest odds of blood-pressure response in network meta-analyses[1]Fadila Tahir et al., “Long-Term Amlodipine and Dementia Risk,” Journal of Hypertension, JHYPERTENSION.COM. These dynamics keep the calcium channel blocker market relevant even as newer classes capture headlines.

Emerging Clinical Evidence Supporting Neuroprotective Applications

Dihydropyridines that cross the blood-brain barrier are under evaluation for migraine prophylaxis, Parkinson’s disease risk reduction, and cerebral vasospasm prevention after subarachnoid hemorrhage. A 2024 systematic review linked chronic use to a statistically significant decrease in Parkinson’s incidence. Migraine trials using flunarizine and lomerizine show durable aura suppression, while verapamil retains a niche role in cluster headache. These exploratory indications enlarge the total addressable patient cohort and diversify revenue streams within the calcium channel blocker market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny over nitrosamine impurities | -0.8% | United States, European Union, global effect | Short term (≤ 2 years) |

| Adverse effect profile leading to therapy switches | -0.4% | Global; more pronounced in elderly populations | Medium term (2-4 years) |

| Supply chain vulnerabilities in active pharmaceutical ingredient sourcing | -0.6% | Global; China-dependent supply chains | Short term (≤ 2 years) |

| Competitive pressure from novel cardiovascular drug classes | -0.5% | Developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny Over Nitrosamine Impurities

The US FDA’s 2024 guidance requires every manufacturer to map potential nitrosamine formation pathways, tighten specification limits, and validate mitigation steps before batch release. Similar expectations now apply across Europe and Japan. Compliance forces companies to upgrade analytical methods, vet excipient suppliers, and retrofit older facilities, elevating cost of goods. Voluntary suspensions during investigation phases have temporarily restricted supply, although most firms ultimately resume production once corrective actions satisfy regulators. The extra burden trims near-term profitability but is unlikely to derail the long-term trajectory of the calcium channel blocker market.

Supply Chain Vulnerabilities in Active Pharmaceutical Ingredient Sourcing

China’s 2023 Anti-Espionage Law heightened legal exposure for foreign auditors and customs brokers, prompting temporary pauses in on-site inspections and slowing batch clearance of cardiovascular APIs[2]Olivier Lantrès and Myriam Danziger, “China’s Anti-Espionage Law and Pharma Supply Chains,” Pharmaphorum, PHARMAPHORUM.COM. The ripple effect amplified lead times into Europe, where Germany briefly suspended certain audits over staff safety concerns. Simultaneous port congestion tightened supply of amlodipine besylate and raised spot-market prices. Geographic concentration remains a structural risk, but multinational firms are diversifying second-source vendors in India and Latin America to protect continuity, thereby stabilizing the calcium channel blocker market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Dihydropyridines Maintain Therapeutic Dominance

Dihydropyridines held 61.78% of revenue in 2025, reflecting prescriber familiarity and once-daily convenience for drugs such as amlodipine, cilnidipine, and felodipine. The calcium channel blocker market size for this class is forecast to achieve mid-single-digit growth through 2031 as payers widen access to generics and physicians exploit vascular selectivity to avoid conduction disturbances. Uptake remains particularly strong in Asia-Pacific, where guideline committees often recommend amlodipine as the preferred starter drug for patients of any age group.

Non-dihydropyridines, comprising verapamil and diltiazem, are projected to post a 7.12% CAGR, outpacing the broader calcium channel blocker market. Their dual vascular and nodal activity makes them attractive in atrial tachyarrhythmias, postoperative rate control, and concomitant angina. Growth also benefits from research into N- and L-type dual inhibitors like cilnidipine that may reduce sympathetic overdrive in chronic kidney disease. Innovation therefore supports diversification without undermining the primacy of traditional dihydropyridines.

By Indication: Hypertension Leadership Faces Neurological Expansion

Hypertension accounted for 70.65% of 2025 prescriptions, preserving first-line status across North America, Europe, and most of Asia. Evidence that L-type blockade cuts stroke risk more than beta-blockade sustains confidence among primary-care physicians. In volume terms, the calcium channel blocker market size for hypertension should maintain a low-mid single-digit trajectory despite therapeutic inertia and guideline updates that encourage starting two agents at once.

Neurological disorders are on track to expand at an 7.86% CAGR to 2031, the highest among all use cases. Real-world analyses link chronic exposure to a 20% lower Parkinson’s disease incidence, and randomised trials are evaluating verapamil for cluster headache and cilnidipine for neurogenic hypertension. Small but growing off-label demand therefore provides an incremental avenue of diversification within the calcium channel blocker market.

By Formulation: Extended-Release Dominance Meets Combination Innovation

Extended-release formulations delivered 53.88% of 2025 revenue thanks to 24-hour pharmacokinetics that limit blood-pressure variability and simplify dosing schedules. Improved adherence translates into lower stroke recurrence rates, reinforcing physician preference for controlled-release designs in chronic care pathways.

Fixed-dose combinations are projected to grow 7.41% annually, the fastest among all dosage forms. Newer triple-ingredient tablets that merge amlodipine with telmisartan and chlorthalidone reduce pill burden from three to one, a benefit that resonates with value-based care mandates in North America and Europe. Early registrational data also suggest cost-effectiveness advantages when measured against traditional stepped therapy models, enlarging the addressable share of the calcium channel blocker market.

By Distribution Channel: Retail Pharmacy Accessibility Drives Hospital Growth

Retail pharmacies dispensed 45.96% of global volume in 2025 because most patients initiate therapy in primary care and continue lifelong maintenance. Generic substitution policies and predictable refills underpin channel stability.

Hospital pharmacies are forecast to post an 8.02% CAGR as cardiovascular case acuity rises. Intravenous nicardipine for perioperative blood-pressure control and diltiazem for rate-limiting rapid atrial fibrillation remain staples in critical-care formularies. Intensified monitoring for calcium channel blocker toxicity, including extracorporeal membrane oxygenation readiness, further drives hospital demand, supporting revenue upside beyond ambulatory settings.

Geography Analysis

North America retained 39.12% of global turnover in 2025 on the back of high insurance coverage and rapid adoption of novel polypills. Prescription audits show that calcium channel blocker use among Black patients jumped 41% between 2018-2019 compared with earlier years after the JNC 8 committee advocated the class as first-line therapy. Generic intensification offsets price erosion, while brand extensions like once-weekly patches attract niche cohorts with adherence challenges. Continuous medical education reinforces class familiarity, cushioning the calcium channel blocker market from short-term competition.

Europe ranked second, characterized by cost-containment and proactive safety surveillance. Class 2 recalls for amlodipine tablets in early 2025 underscored the region’s vigilance in microbial quality management. Health technology appraisal agencies such as NICE routinely favour low-priced generics but still reimburse branded combinations when economic models demonstrate fewer cardiovascular events. The advent of nifedipine-lidocaine ointment for chronic anal fissure adds a novel non-cardiac dimension, diversifying regional demand.

Asia-Pacific remains the fastest-growing territory at 6.18% CAGR. The twin forces of epidemiological transition and public insurance expansion elevate annual prescription volumes. Local firms in China and India supply competitively priced APIs and finished doses, ensuring affordability. Observational studies across 12 countries confirm that calcium channel blockers constitute the most frequently prescribed antihypertensive class, although intra-regional heterogeneity persists. Government bulk-purchase schemes continue to widen patient reach, supplying structural growth to the calcium channel blocker market.

Elsewhere, Latin America and the Middle East & Africa record steady uptake as urbanization increases cardiovascular risk. International donor programs that supply essential antihypertensive drugs to remote clinics enlarge the still-small baseline, contributing additional incremental units.

Regulatory Landscape

Regulatory oversight for calcium channel blockers is increasingly shaped by tighter quality expectations for legacy small molecules and streamlined lifecycle management rules for generics and line extensions. In the United States, the FDA continues to enforce its 2024 nitrosamine risk-evaluation expectations across marketed products, which is pushing manufacturers to map formation pathways, tighten specifications, and validate mitigation steps prior to batch release. These requirements raise the compliance bar for high-volume molecules such as amlodipine, diltiazem, and nicardipine, and can lead to temporary supply interruptions when investigations or method upgrades are underway.

In Europe, the European Medicines Agency (EMA) has operationalized updates to the variations framework, including implementation changes starting January 2025 and a cut-off in January 2026 tied to updated variation classification and electronic application form usage, which affects how companies execute site changes, formulation tweaks, and post-approval commitments. Pharmacovigilance continues to shape labeling and benefit-risk positioning; for example, the EMA published scientific conclusions for nicardipine through a PSUSA assessment in March 2026. At the global level, ICH adoption of the M12 guideline on drug interaction studies (Step 4 in May 2024) supports more harmonized development packages, reducing region-by-region study divergence for new formulations and fixed-dose combinations that include calcium channel blockers.

Value Chain Analysis

The calcium channel blocker value chain starts with key starting materials (KSMs) and chemical intermediates that feed active pharmaceutical ingredient (API) manufacturing for high-volume products such as amlodipine, diltiazem, verapamil, nifedipine, nicardipine, and clevidipine. API output is converted into finished dosage forms, including immediate-release, extended-release, and fixed-dose combinations, through formulation and tableting (and sterile manufacture for injectables), followed by packaging and batch release testing aligned with major pharmacopoeial standards (USP, EP, BP). The downstream chain runs through wholesalers and tender channels into hospital and retail pharmacies, where substitution and procurement rules shape the brand versus generic mix.

A key bottleneck sits upstream, where KSM and API concentration by geography and supplier can create lead-time volatility even when finished-dose manufacturing is diversified. In 2026, USP highlighted single-country dependency as a driver of vulnerability, including findings that a large share of shortage-linked products rely on a single country for at least one KSM, reinforcing the business case for dual sourcing and inventory buffers for mature cardiovascular drugs. Policy and industry proposals have also emphasized resilience levers such as strategic stockpiling and advanced manufacturing approaches (for example, flow chemistry and continuous processing) to reduce exposure to disruptions tied to cross-border inspections, logistics, and export controls.

Competitive Landscape

The calcium channel blocker market is moderately fragmented. Pfizer, Novartis, Teva, and Viatris together distribute branded and unbranded products across more than 100 countries, while Indian manufacturers such as Sun Pharma and Dr. Reddy’s leverage cost efficiencies to penetrate tender markets. Combined, the five largest suppliers hold an estimated 28-30% share, leaving ample room for regional generics.

Strategic focus rests on lifecycle management—new particle sizes, gastro-retentive matrices, and fixed-dose combinations—that protect value in mature molecules. Pfizer reinforced its position by rolling out an amlodipine-rosuvastatin-telmisartan triple pill in the European Union during 2025 approvals. Novartis and Orion collaborate on verapamil micro-bead technology to curb constipation by shifting release to the distal small bowel, with Phase III read-out expected in 2026.

Chinese contract development and manufacturing organizations (CDMOs) are expanding vertically into finished product marketing, heightening competitive flux in Asia and Africa. Compliance with US FDA nitrosamine guidelines has become a key differentiator; facilities that secure clean inspection records gain a volume edge in export tenders. Meanwhile, biopharma entrants explore L-type channel blockade in orphan indications such as systemic sclerosis, signalling niche innovation pathways that diversify the calcium channel blocker market.

Calcium Channel Blocker Industry Leaders

Pfizer Inc.

Viatris Inc.

Teva Pharmaceutical Industries Ltd.

Sun Pharma Industries Ltd.

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial whitespace is forming around patient-centric delivery and acute-use settings, where calcium channel blocker pharmacology can be paired with novel administration formats to expand use beyond maintenance hypertension. Milestone Pharmaceuticals received first US FDA approval in December 2025 for CARDAMYST (etripamil), an intranasal calcium channel blocker for acute, symptomatic paroxysmal supraventricular tachycardia, and in January 2026 the EMA accepted the Marketing Authorization Application for etripamil nasal spray. This supports a pathway for self- or caregiver-administered acute conversion therapy, and it has already driven regional deal-making, including Everest Medicines acquiring Greater China rights in March 2026.

A second opportunity area is hospital and critical-care utilization, where injectable dihydropyridines support hypertensive emergencies and perioperative blood-pressure control, strengthening demand through hospital pharmacies that are expanding faster than retail channels within the market. In China, CSPC Pharmaceutical Group reported NMPA registration approval in February 2026 for a clevidipine injectable emulsion, underscoring the strategic importance of local registrations and manufacturing footprints for sterile cardiovascular products. Alongside these near-term commercialization vectors, ongoing clinical and translational work evaluating calcium channel blockers in neurological and other non-cardiac indications supports portfolio broadening, while compliance readiness for impurity control and resilient API sourcing remain prerequisites for capturing volume in tenders and chronic reimbursement programs.

Recent Industry Developments

- April 2026: Teva Pharmaceutical Industries announced an agreement to acquire Emalex Biosciences. While the target is positioned in neuroscience rather than cardiovascular disease, the deal reinforces Teva's focus on specialty and branded assets alongside its large generic base, shaping competitive capital allocation that can influence mature antihypertensive portfolios.

- March 2026: Everest Medicines entered into an asset purchase agreement with Corxel Pharmaceuticals Hong Kong Limited to acquire development, manufacturing, and commercialization rights for etripamil nasal spray in Greater China for up to USD 50 million. The transaction extends geographic reach for a rapid-acting calcium channel blocker delivery platform and reflects active regional partnering around differentiated formulations rather than commodity oral generics.

- February 2026: CSPC Pharmaceutical Group Limited received NMPA drug registration approval in China for clevidipine injectable emulsion in 50 mL and 100 mL presentations. The approval expands availability of dihydropyridine options for hypertensive emergencies and supports competitive intensity in hospital-based calcium channel blocker use, where sterile manufacturing capability is a barrier to entry.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from calcium channel blocker medicines used to manage cardiovascular and related conditions through standard care channels. It includes commonly used drug classes and formulations that are prescribed or dispensed for uses such as hypertension and angina across major regions.

Scope exclusions: We exclude non-calcium-channel cardiovascular drug classes and any non-therapeutic research-only compounds that are not sold through commercial prescription or pharmacy channels.

Segmentation Overview

- By Drug Class

- Dihydropyridines

- Amlodipine

- Nifedipine

- Felodipine & Others

- Non-Dihydropyridines

- Phenylalkylamine (Verapamil)

- Benzothiazepine (Diltiazem)

- Dihydropyridines

- By Indication

- Hypertension

- Angina Pectoris

- Arrhythmia

- Raynaud's Phenomenon

- Neurological Disorders (Migraine, SAH)

- Other Indications

- By Formulation

- Immediate-Release

- Extended / Controlled-Release

- Fixed-Dose Combinations

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the starting structure of the market and to make sure each assumption has a real-world anchor. We review public health and utilization signals from sources such as the World Health Organization, the US CDC, the OECD health statistics series, and national health agencies that publish hypertension and cardiovascular burden indicators.

Along with this, pricing and access context is checked through government and regulator references such as the US FDA databases, the European Medicines Agency, and published reimbursement and formulary notes where available. We then review peer-reviewed journals on hypertension treatment patterns and fixed-dose combination adoption. We also use company filings, annual reports, investor presentations, and reputable press to understand generic entry, portfolio focus, and regional mix, with selective support from paid subscriptions focused on company financials and intelligence plus patent databases. The sources listed here are illustrative only, and many other public references are used for cross-checks and clarification during the research.

Primary Interviews and Surveys

Primary work is used to stress-test what we see in public sources and to fill gaps that are usually not written down clearly, especially around channel mix, typical price corridors, and the pace of switching between brands and generics. We speak with a balanced set of respondents across manufacturers, distributors, hospital pharmacy stakeholders, and clinical experts across APAC, EMEA, and the Americas, so the model reflects real prescribing and dispensing behavior, not only published disease counts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 38% |

| Mid tier: 51% | Functional/Unit leaders: 36% | EMEA: 35% |

| Smaller Players: 22% | Managers: 52% | Americas: 27% |

Market-Sizing & Forecasting

The sizing logic starts with a top-down build that reconstructs the treated demand pool from hypertension and other relevant condition prevalence, and then translates it into category value using therapy mix and expected pricing by channel. Once the demand pool is shaped, the totals are checked with selective bottom-up approximations, such as sampled volume by key molecules and a price-per-unit range validated through channel conversations, before final totals are adjusted.

In practice, inputs that matter include diagnosed and treated hypertension rates, prescribing share of calcium channel blockers within guideline-driven therapy, typical daily dose and duration patterns, the generic to branded split, and country-level reimbursement and formulary access that can shift volumes between hospital and retail pharmacy. We also track when fixed-dose combinations gain traction because they can change average selling price progression even if patient counts are stable. Forecasting is carried out using scenario analysis supported by expert consensus, and the scenarios are tied to visible drivers such as aging population trends, chronic disease burden, and the timing of generic introductions. Where country or channel detail is limited, gaps are handled through proxy indicators from similar markets, followed by interview-led calibration so the final output stays realistic.

Data Validation & Update Cycle

Outputs are validated through multiple checks so single-source noise does not steer the final number. We compare the model against independent signals, including disease burden direction, therapy class share movement, and the expected pricing impact from genericization, and then investigate variances that look too large for the underlying drivers.

Before sign-off, the model and assumptions go through step-by-step analyst reviews, and re-contacts are triggered when a key assumption changes, such as an access shift or an unexpected price movement. Reports are refreshed annually, and interim updates are made when material events occur that can move demand or pricing. Right before delivery, the latest public updates are reviewed once more so clients receive an up-to-date view.

Mordor Intelligence's Calcium Channel Blocker Market Size Compared Against Other Published Estimates

Published market sizes for calcium channel blockers can look far apart, even when the topic label is the same, because the underlying inclusions and the year being measured are not aligned. Differences also come from how pricing is treated across retail versus hospital channels and how aggressively generic price erosion is assumed.

Some estimates broaden the scope by mixing in adjacent antihypertensive drug classes or by rolling the market forward using optimistic price assumptions. In Mordor Intelligence, the count is limited to calcium channel blocker revenues only, and the sizing is anchored to treated-patient demand signals and channel-validated pricing ranges, which helps avoid accidental category inflation.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.79 B (2026) | |

| Global Consultancy A | USD 15.76 B (2024) | Uses an earlier base year and a different forecast window, and it can also apply broader route and application buckets that may not map cleanly to commercial dispensing value in each region. |

| Industry Publisher B | USD 9.07 B (2025) | Reports a smaller 2025 value that may reflect a narrower counted revenue pool or more conservative pricing and access assumptions, particularly if fixed-dose combinations and full channel coverage are not consistently captured. |

Taken together, the spread is mainly explained by year choice and what is counted as part of calcium channel blocker revenue, followed by how price paths are projected after generic entry. Our approach keeps the number traceable to demand indicators, channel mix, and realistic price corridors, which makes it easier for decision-makers to replicate the logic and understand what would move the market up or down.

Key Questions Answered in the Report

What is the current value of the calcium channel blocker market?

The calcium channel blocker market size is USD 17.79 billion in 2026 and is forecast to climb to USD 22.91 billion by 2031.

Which drug class dominates sales?

Dihydropyridines, led by amlodipine, captured 61.78% of 2025 sales and maintain a steady lead through 2031.

Which region is expanding the fastest?

Asia-Pacific is projected to post a 6.18% CAGR from 2026-2031 on the back of broader insurance coverage and a rising cardiovascular disease burden.

How significant are fixed-dose combinations?

Fixed-dose combinations form the quickest-growing formulation segment with a 7.41% CAGR as they improve patient adherence and cardiovascular outcomes.

What regulatory issue currently affects manufacturers?

Global agencies are enforcing stricter limits on nitrosamine impurities, prompting costly analytical upgrades and temporary batch suspensions.

Are calcium channel blockers being explored beyond cardiovascular diseases?

Yes, ongoing studies examine neuroprotective roles in migraine and ParkinsonÕs disease, while cilnidipine analogue AISA-021 is in development for systemic sclerosis.

Page last updated on: