Business Rules Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

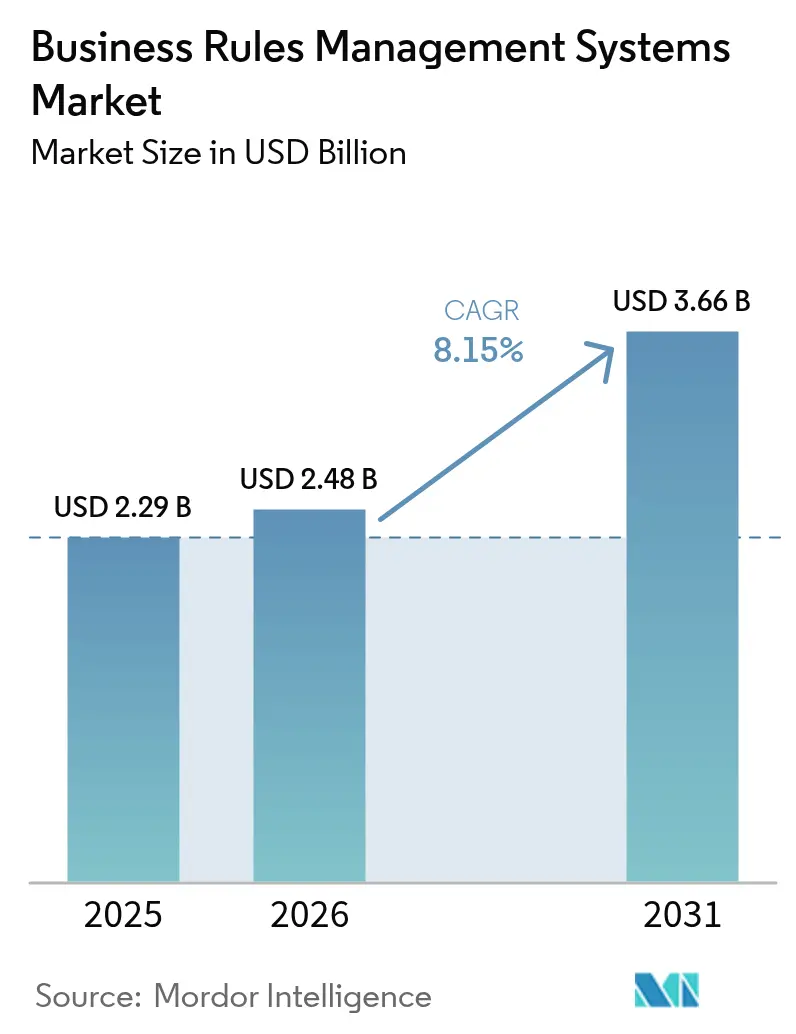

| Market Size (2026) | USD 2.48 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business Rules Management Systems Market Analysis by Mordor Intelligence

The Business Rules Management Systems market size is expected to grow from USD 2.29 billion in 2025 to USD 2.48 billion in 2026 and is forecast to reach USD 3.66 billion by 2031 at 8.15% CAGR over 2026-2031. Cloud-native rule engines, tighter regulatory oversight, and mounting pressure on enterprises to trim operational costs while safeguarding governance are reinforcing demand. Ongoing migration from embedded code to externalized rules shortens policy update cycles, lets firms respond quickly to market shifts, and improves auditability. Growth is further propelled by low-code tools that let business users author rules directly, by AI-driven decision science that improves rule accuracy, and by the integration of rules with robotic process automation that closes process gaps and reduces manual hand-offs. Vendors that package explainable AI with transparent rule flows are gaining traction as buyers require deterministic logic in regulated environments.

Key Report Takeaways

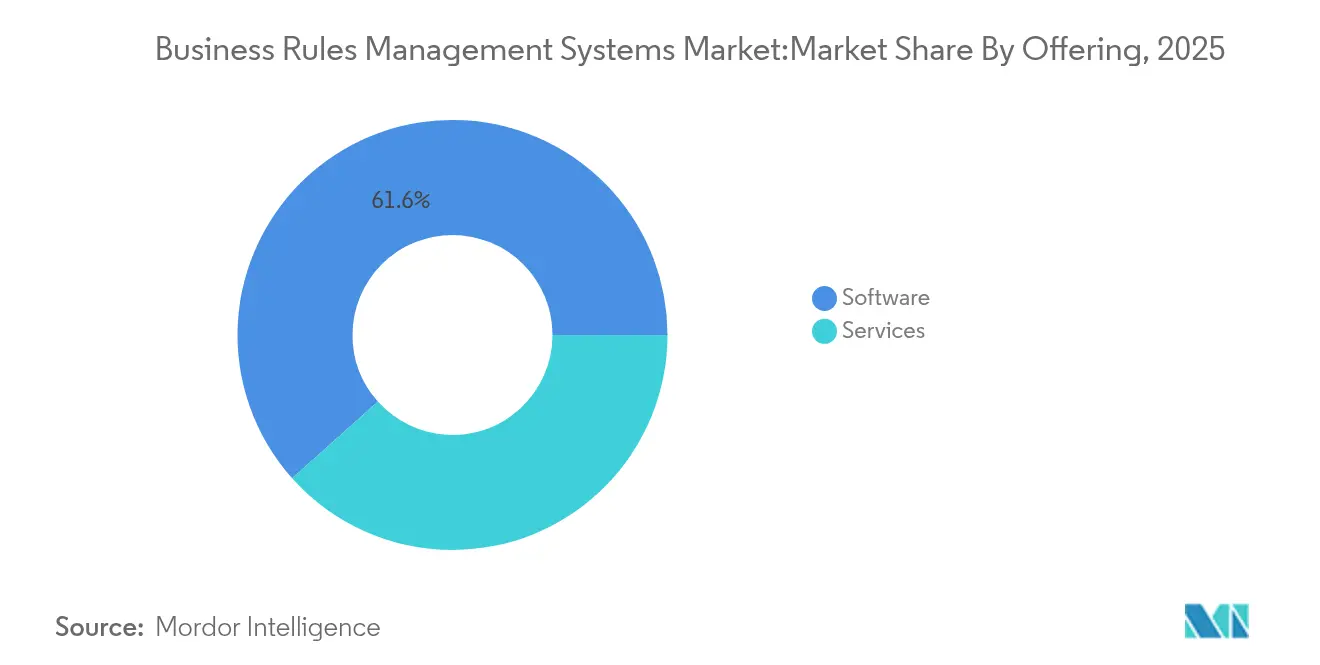

- By offering, software retained 61.60% revenue share in 2025, while services are forecast to expand at a 9.85% CAGR through 2031.

- By organization size, large enterprises held 63.10% of the business rules management systems market share in 2025, whereas small and medium enterprises are set to lead growth at an 11.05% CAGR to 2031.

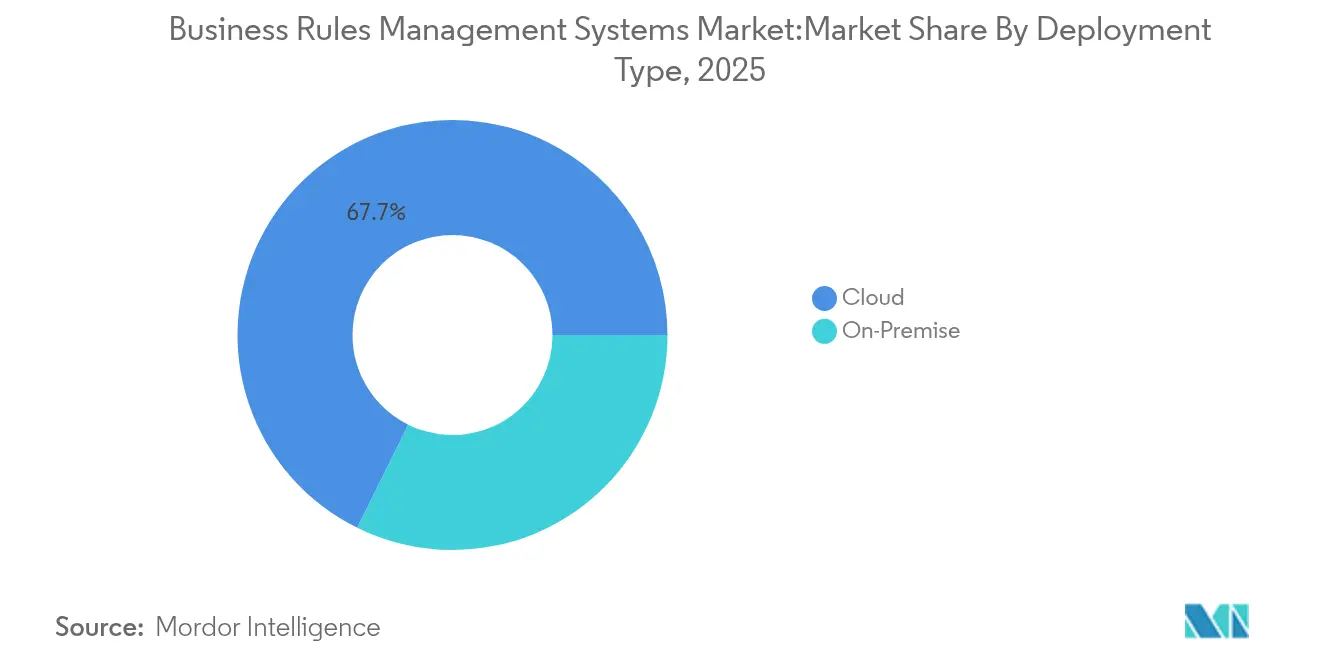

- By deployment, cloud platforms captured 67.70% of the business rules management systems market size in 2025 and are projected to advance at a 9.35% CAGR through 2031.

- By end-user vertical, the BFSI segment accounted for 43.10% of revenue in 2025; Healthcare and Life Sciences is projected to grow at a 10.02% CAGR by 2031.

- By business function, risk and compliance held 50.20% of the business rules management systems market size in 2025, while customer service workloads are rising at an 10.78% CAGR.

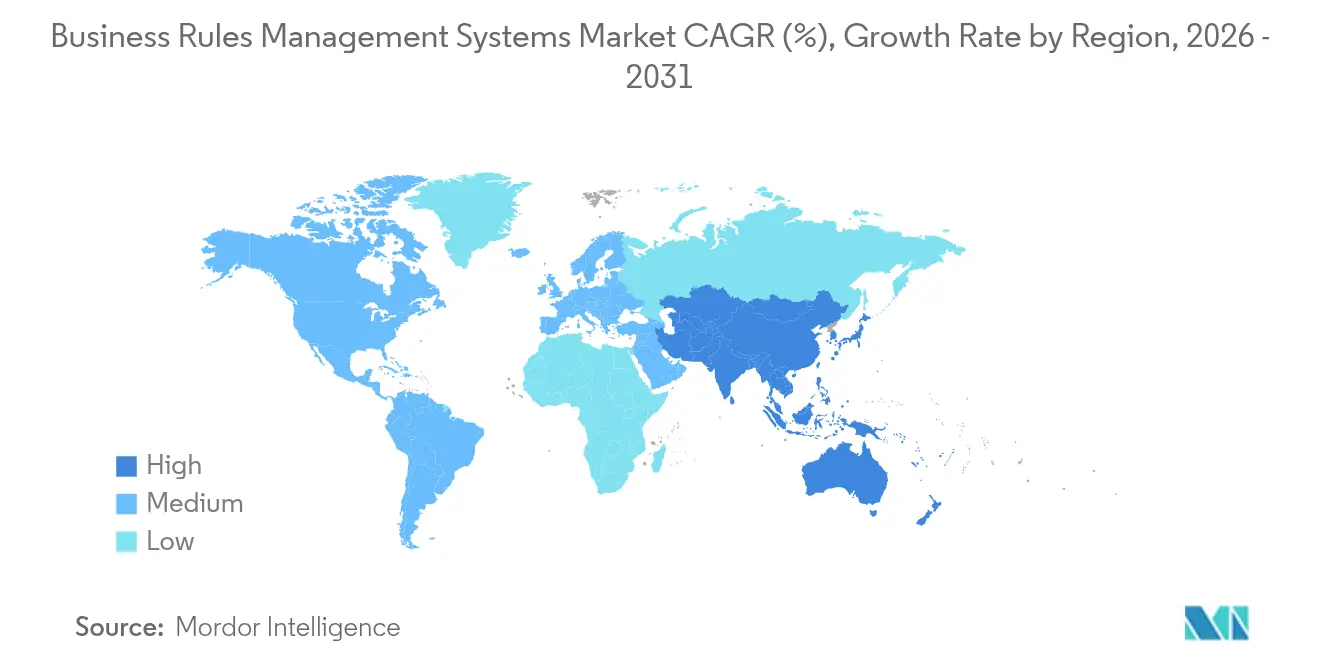

- By geography, North America commanded 37.40% revenue share in 2025, and Asia-Pacific is forecast to post an 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Business Rules Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduced dependency on IT teams for writing rules | +1.3% | North America and Europe lead | Medium term (2-4 years) |

| Increased need to manage regulatory and compliance policy | +1.5% | Global, most acute in BFSI hubs | Short term (≤ 2 years) |

| Rise of low-code/no-code platforms accelerating BRMS adoption | +1.0% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Integration with hyper-automation and RPA suites | +0.9% | Global, early adoption in manufacturing | Long term (≥ 4 years) |

| Demand for explainable AI in decisioning | +0.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Growing cloud-native micro-services architectures | +0.7% | Global, led by cloud-first organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reduced Dependency on IT Teams for Writing Rules

Business units now insist on changing rules without queuing requests for developers, shrinking policy deployment cycles, and cutting compliance lag. Federal Bank, for instance, halved its Know Your Customer update timeline after adopting an automation layer that lets analysts adjust customer identification logic directly. Visual rule designers and natural-language authoring portals in today’s platforms give non-technical staff direct control, which frees scarce IT resources for core engineering tasks. In regulated sectors, this agility neutralizes the risk of late policy rollouts whenever a regulator issues fresh guidance. The shift also builds institutional resilience because business logic no longer sits hard-coded inside legacy applications.

Increased Need to Manage Regulatory and Compliance Policy

Financial institutions absorb more than 500 rule changes a year, and manual mapping of statutes to workflows strains budgets and staff. Automated rule engines translate legal text into executable policies, cutting both interpretation errors and update latency. Regology’s platform monitors global statutes, flags potential impacts, and feeds structured obligations into rule repositories, allowing firms to stay current across multiple jurisdictions. Fines topping billions of USD have proved that non-compliance outweighs system costs, pushing boards to prioritize automated governance. Healthcare providers follow a similar path by converting treatment guidelines into machine-readable logic for clinical decision support.

Rise of Low-Code/No-Code Platforms Accelerating BRMS Adoption

Drag-and-drop canvases and rule templates eliminate heavy development cycles and drop the barrier to entry for smaller firms. Asia-Pacific SMEs leverage these tools to implement decision flows within weeks, supporting the region’s 11.1% CAGR leadership in the business rules management systems market. FICO Blaze Advisor lets analysts craft strategies without coding, cutting deployment costs, and compressing testing timelines. Citizen-developer programs have emerged, distributing rule ownership across departments yet maintaining central oversight for risk.

Integration with Hyper-Automation and RPA Suites

Combining rule engines with process bots creates unattended workflows that span data capture, decisioning, and transaction posting. Sogefi Brazil lifted on-time purchase-order approvals to 97% after embedding rules into an automated workflow that trimmed 5 approval steps while honoring segregation-of-duties policy. Modern microservices architectures fire rules in real time, so bot-driven processes adapt instantly to events such as price swings or supply shortages. Manufacturing hubs use this fusion to automate production scheduling, while finance departments automate straight-through invoice approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resistance to modern technology in legacy-system-heavy firms | -0.7% | Traditional industries worldwide | Short term (≤ 2 years) |

| Perceived high TCO for enterprise-wide roll-outs | -0.5% | Cost-sensitive and emerging markets | Medium term (2-4 years) |

| Shortage of skilled decision-management architects | -0.4% | Global, acute in specialized domains | Long term (≥ 4 years) |

| Vendor lock-in concerns limiting long-term flexibility | -0.3% | Enterprise markets, multi-vendor environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Resistance to Modern Technology in Legacy-System-Heavy Firms

Enterprises that rely on decades-old core platforms often distrust rule externalization because existing logic seems stable and well understood. Change management challenges mount when staff worry that automation will devalue institutional knowledge. Integration projects can be costly if legacy code lacks clear documentation, and senior executives may resist risking production stability. Manufacturing plants that run on embedded programmable logic controls illustrate this hesitation, preferring incremental tweaks to wholesale rule extraction.

Perceived High TCO for Enterprise-Wide Roll-Outs

Comprehensive deployments include software fees, integration services, training, and continuous optimization, all of which can exceed initial budget estimates. Legacy-to-BRMS migrations reveal hidden complexity once undocumented rule variants surface. Licensing models linked to transaction volumes may look expensive relative to departmental pilots, especially in emerging markets where capex is scarce. Small firms balance these costs against long-term compliance and efficiency gains, delaying projects until cloud subscription models and shared services narrow the affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Growth Outpaces Software Dominance

Services revenue is expanding at a 9.85% CAGR because enterprises recognize that domain expertise is vital for rule harvesting, testing, and governance. The business rules management systems market relies on consulting partners to translate policy into logic, integrate rule engines with existing applications, and coach citizen developers. Implementation engagements command premium pricing when mistakes could trigger regulatory fines. Continuous optimization retainers are also growing as firms refine rule performance after deployment.Software still represented 61.60% of 2025 revenue, but its growth is modest relative to services. Vendors increasingly bundle low-code design tools and AI-based rule analyzers to retain license value. Yet many buyers view software as a foundation and channel investments toward managed services that ensure uptime, security, and version upgrades. This pattern underscores that the business rules management systems market values outcomes over ownership.

By Organization Size: SME Acceleration Drives Market Democratization

Small and medium enterprises are registering an 11.05% CAGR, reflecting falling entry barriers linked to SaaS delivery. Cloud subscription tiers permit incremental adoption without hardware investments, letting SMEs achieve compliance parity with larger rivals. Vendor marketplaces now offer pre-built rule packs tailored to common use cases such as invoice matching or credit scoring, further simplifying uptake.Large enterprises held 63.10% revenue share in 2025, yet now focus on refining existing deployments. Their priorities include embedding machine learning predictors inside rule flows and applying decision analytics to monitor drift. Multi-region conglomerates demand sophisticated metadata management to govern thousands of rules across jurisdictions. These requirements fuel collaboration with specialized integrators and justify the business rules management systems industry’s consulting expansion.

By Deployment Type: Cloud Supremacy Reflects Architectural Evolution

Cloud platforms captured 67.70% revenue share in 2025 and keep growing at 9.35% because elasticity matches volatile transaction volumes. Organisations avoid over-provisioning by letting platforms autoscale rule evaluations during seasonal peaks. Containerized deployments on Kubernetes shorten release cycles, and serverless endpoints reduce idle costs. The business rules management systems market size attached to the cloud is set to rise as firms modernize application stacks.On-premise engines remain relevant where data residency or ultra-low latency is mandatory, yet even these users adopt hybrid designs. Development and testing often happen in the cloud, with sensitive production rules anchored on private clusters. Red Hat’s event-driven architecture blueprint shows how distributed rule components can stay synchronized under central governance. Edge deployments in manufacturing or logistics hubs process decisions locally to avoid network delays.

By End-User Vertical: Healthcare Surge Challenges BFSI Leadership

Healthcare and life sciences is the fastest-growing vertical at 10.02% CAGR as clinical guidelines evolve rapidly and require machine-readable execution. Providers deploy rules to flag contraindications, authorize procedures, and ensure compliance with safety regulations. Progress Corticon users reported up to 90% faster development for care-path logic. Real-time decision support raises care consistency and curbs liability exposure.Banking, Financial Services, and Insurance still led with 43.10% revenue share in 2025 because fraud detection, credit adjudication, and regulatory reporting rely on deterministic logic. Growth, however, is plateauing as first-generation engines mature. Manufacturers and government agencies are fresh adopters. Ceará State Government digitized case handling and cut processing time fivefold after centralizing rules. Retailers exploit rules for dynamic pricing and personalized promotions, broadening the business rules management systems market reach.

By Business Function: Customer Service Automation Accelerates

Customer service workloads exhibit an 10.78% CAGR as enterprises automate inquiry triage, escalations, and resolution tracking across chat, email, and voice channels. Rule-driven routing ensures consistent policy application regardless of channel and hour. Integration with CRM data lets firms apply context, boosting satisfaction while keeping staffing flat. Predictive analytics and rules combine to trigger proactive outreach before issues peak, reducing churn.Risk and compliance functions accounted for 50.20% of the business rules management systems market size in 2025 and remain foundational. However, they now share the stage with operations and supply chain teams that need rule-based sourcing, inventory, and logistics decisions to navigate volatile markets. Finance departments adopt rules for straight-through invoice approvals, and marketing teams embed decisioning into campaign orchestration. This diversification signals that decision automation has moved from niche to enterprise core.

Geography Analysis

North America led the business rules management systems market with 37.40% revenue share in 2025. Deep regulatory obligations in sectors such as finance and healthcare, combined with a mature culture of process automation, sustain demand. Institutions like NatWest compressed product governance lead times from 4.5 days to under 20 minutes using automated risk oversight. Vendors headquartered in the region provide extensive partner ecosystems and professional services that accelerate adoption.

Asia-Pacific is the fastest-growing territory, posting an 10.62% CAGR through 2031. Government digitalization programs and cloud-first strategies among SMEs drive the uptake of subscription-based rule engines. The Asia-Pacific Trade Facilitation Report projected 11% cost savings from digitized trade procedures, a catalyst for automating customs and logistics decisions. Banks in markets such as Indonesia and the Philippines embed rules to accelerate credit processing, while manufacturers in Vietnam automate supplier qualification.Europe maintains steady expansion as cross-border commerce and stringent data-protection law require transparent, auditable decision systems. Firms adopt explainable AI layered on rule engines to meet audit mandates. Manufacturing clusters implement rules for environmental compliance. Meanwhile, the Middle East and Africa represent emerging whitespace. Energy producers and public agencies modernize workflows through cloud platforms that minimize infrastructure hurdles, indicating long-term upside for the business rules management systems market.

Competitive Landscape

The business rules management systems market is moderately concentrated. IBM, Oracle, and SAP capitalize on legacy footprints and broad portfolios, integrating rules with analytics and workflow modules. IBM’s repositioned software catalog now highlights automation and hybrid cloud capabilities, aligning with decisioning demand. Oracle blends rule services into its Fusion middleware to retain database clients, while SAP positions its Business AI roadmap to enrich rule-driven applications.

Specialists such as FICO, Progress Software, and Red Hat target domain or architectural niches. FICO excels in credit risk and fraud, with a robust rule editor for financial institutions. Progress recorded USD 238 million in Q1 2025 revenue, up 29%, and lifted annual guidance on growing automation subscriptions. Red Hat embeds its open-source Drools engine into OpenShift AI to attract developers seeking container-native decision services.

Cloud-native challengers offer flexible pricing and developer-friendly APIs. Their microservice rule components appeal to digital-born firms that dislike monolithic suites. Established vendors respond by rolling out managed services and pursuing acquisitions. Progress acquired ShareFile for USD 875 million to add secure content collaboration, while SAP’s transformation program invests in embedded AI to maintain relevance. Market rivalry is intensifying as platforms converge around hyper-automation, explainable AI, and low-code orchestration.

Business Rules Management Systems Industry Leaders

IBM Corporation

Fair Isaac Corporation (FICO)

Pegasystems Inc.

Oracle Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Progress Software reported USD 238 million Q1 revenue, a 29% rise year over year, and highlighted 48% growth in annualized recurring revenue.

- February 2025: Red Hat released OpenShift AI 2.15, featuring model registry, bias detection, and GPU optimization.

- January 2025: SAP unveiled a transformation program centered on Business AI and reaffirmed a EUR 10 billion non-IFRS operating profit target for 2025.

- November 2024: Red Hat introduced Lightspeed to embed generative AI across its hybrid cloud portfolio.

- September 2024: Progress Software completed the USD 875 million ShareFile acquisition to expand automation capabilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Business Rules Management Systems (BRMS) market as all packaged software platforms and cloud services that let enterprises author, deploy, and maintain automated decision logic through externalized rule engines. Revenue streams covered include license or subscription fees and standard support updates.

Scope Exclusions: Custom-coded rule libraries embedded in bespoke applications, standalone workflow tools lacking a dedicated rules engine, and pure professional-services income sit outside this scope.

Segmentation Overview

- By Offering

- Software

- Services

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Deployment Type

- Cloud

- On-Premise

- By End-user Vertical

- BFSI

- Telecommunication and IT

- Retail and E-Commerce

- Manufacturing

- Healthcare and Life Sciences

- Government and Public Sector

- Other End-user Verticals

- By Business Function

- Finance and Accounting

- Operations and Supply Chain

- Sales and Marketing

- Risk and Compliance

- Customer Service

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with product leads at leading BRMS vendors, implementation partners, and IT architects in BFSI, telecom, and healthcare across North America, Europe, and Asia-Pacific. These conversations validated unit pricing ranges, cloud migration rates, and regional regulatory triggers that secondary data only hinted at.

Desk Research

We began with public datasets such as US Bureau of Labor Statistics ICT spend tables, Eurostat digital-enterprise surveys, and the World Bank Digital Adoption Index, which anchor enterprise software outlays across 45 economies. Industry bodies, including the Object Management Group's DMN repository and the Basel Committee's compliance bulletins, provided adoption triggers, while company 10-Ks, investor decks, and patent filings traced vendor revenue splits for rules engines. Paid databases, such as D&B Hoovers for company financials and Dow Jones Factiva for product launches, filled granular gaps. The sources listed here are illustrative; many additional references informed data collection, cross-checks, and scope clarification.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the numbers. First, we allocated a share of global enterprise application software spending to dedicated rule engines using penetration ratios derived from primary interviews; results were corroborated with bottom-up vendor revenue roll-ups and sampled average selling price multiplied by active subscription counts before final reconciliation. Key market fingerprints, such as cloud workload share, average rule-base complexity (rules per deployment), regulatory fine frequency, enterprise digital-transformation budgets, and GDP-weighted compliance spending, drive both base year estimates and scenario testing. Forecasts employ multivariate regression supplemented by ARIMA trend checks, letting us capture cyclical IT-budget swings while preserving rule-adoption momentum. Data gaps in smaller geographies were bridged by scaling regional IT spend with digital-maturity multipliers agreed upon with expert respondents.

Data Validation & Update Cycle

Outputs pass three analyst reviews, variance screens against external software trackers, and peer consultations. We refresh every twelve months and trigger interim revisions when material events, such as major regulatory mandates or vendor consolidations, shift underlying drivers. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Business Rules Management Systems Baseline Earns Decision-Maker Trust

Published figures often diverge because firms pick different revenue streams, deployment boundaries, and update cadences.

Key gap drivers include (i) whether services and maintenance are counted, (ii) cloud subscription recognition policies, and (iii) refresh timing that can miss mid-year regulatory surges. Mordor Intelligence aligns scope with real monetization points, pulls cloud and on-premise data straight from vendor filings, and refreshes annually, which reduces undercounting common in older or narrower studies.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.29 B (2025) | Mordor Intelligence | - |

| USD 1.80 B (2025) | Global Consultancy A | Excludes subscription support and SME cloud deals |

| USD 1.51 B (2024) | Industry Journal B | Uses earlier base year and omits service revenue |

| USD 1.90 B (2023) | Regional Consultancy C | Counts only on-premise licenses; older refresh cycle |

Taken together, the comparison shows how narrower scopes or outdated baselines compress market value. By pairing clearly stated inclusions with disciplined variable tracking, Mordor delivers a balanced, transparent starting point for strategic planning and investment sizing.

Key Questions Answered in the Report

What is the current value of the business rules management systems market?

The market reached USD 2.48 billion in 2026 and is projected to climb to USD 3.66 billion by 2031 at an 8.15% CAGR.

Which segment grows fastest in the business rules management systems market?

Services revenue is expanding at a 9.85% CAGR as enterprises rely on consulting and managed services for complex rule deployments.

Why are SMEs accelerating adoption of business rules technology?

SaaS pricing, low-code tools, and pre-configured rule packs remove large upfront costs, enabling SMEs to automate decisions at an 11.05% CAGR.

How does cloud deployment influence the business rules management systems market size?

Cloud platforms hold 67.70% revenue share and are growing at 9.35% because they offer elastic capacity and simplified upgrades.

What industries drive future growth?

Healthcare and life sciences lead future expansion at a 10.02% CAGR, while BFSI maintains the largest share based on risk and compliance use cases.

Which regions show strongest momentum?

Asia-Pacific is the fastest-growing region with an 10.62% CAGR, fueled by government digitalization programs and SME cloud adoption.

Page last updated on: