Building Insulation Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 33.79 Billion |

| Market Size (2031) | USD 40.99 Billion |

| Growth Rate (2026 - 2031) | 3.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Building Insulation Materials Market Analysis by Mordor Intelligence

The Building Insulation Materials Market size is expected to increase from USD 32.51 billion in 2025 to USD 33.79 billion in 2026 and reach USD 40.99 billion by 2031, growing at a CAGR of 3.94% over 2026-2031. Demand is migrating from discretionary spending toward mandated compliance as energy-performance codes tighten worldwide. Material suppliers are reformulating foams to meet low-GWP blowing-agent rules, while contractors push mineral and fiber products that avoid future regulatory risk. Petrochemical price swings and labor shortages are compressing margins, elevating prefabricated panels and digital specification tools that save time on-site. Asia-Pacific’s dual-carbon policies and North American retrofit incentives underpin medium-term volume growth, although installation-cost inflation continues to slow adoption in price-sensitive regions.

Key Report Takeaways

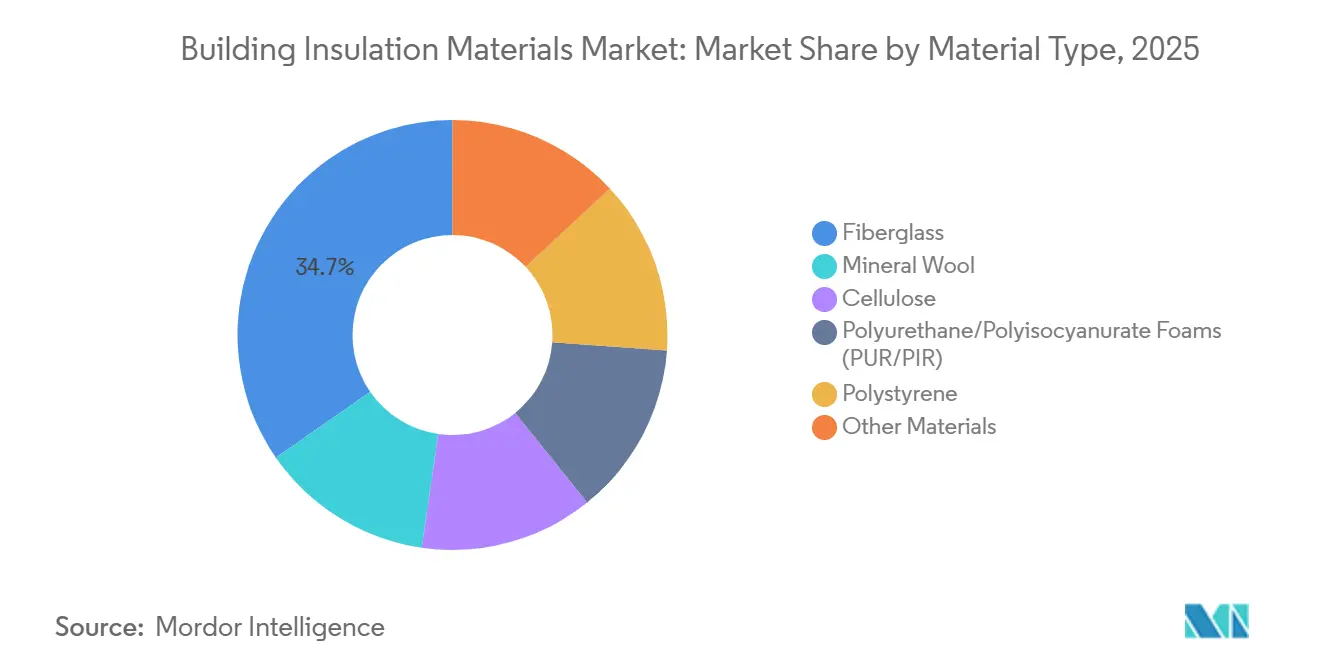

- By material type, fiberglass led with 34.65% of the building insulation materials market share in 2025, while polystyrene is projected to expand at a 4.18% CAGR through 2031.

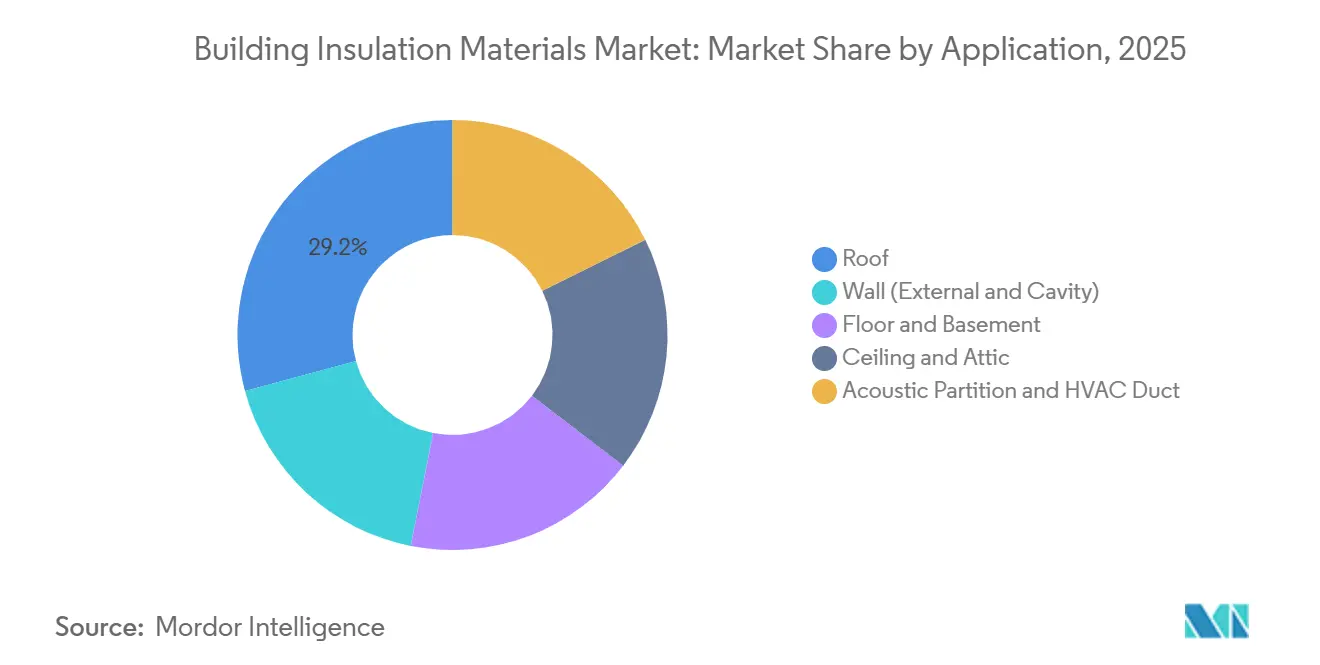

- By application, roof installations captured a 29.19% share in 2025; acoustic partition and HVAC duct demand are advancing at a 4.85% CAGR over 2026-2031.

- By end-user, residential construction accounted for a 56.77% share in 2025 and is growing at a 4.05% CAGR to 2031.

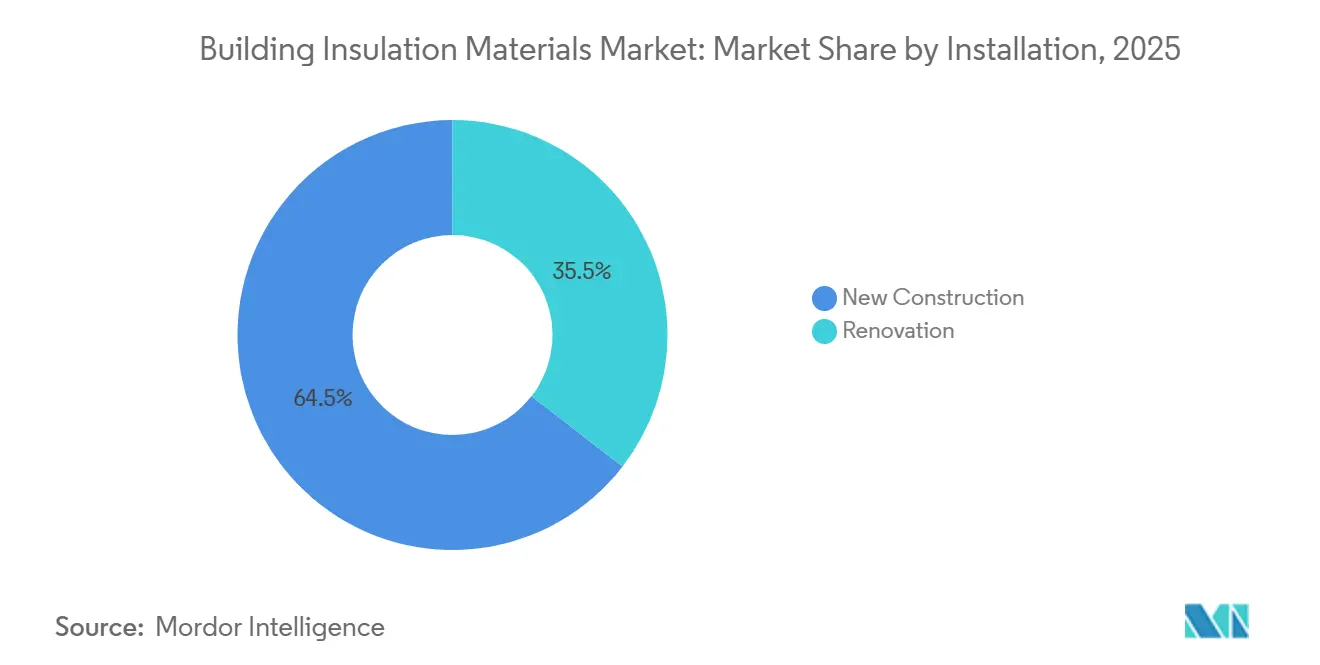

- By installation, new construction held a 64.52% share in 2025, whereas renovation is set to rise at a 5.36% CAGR through 2031.

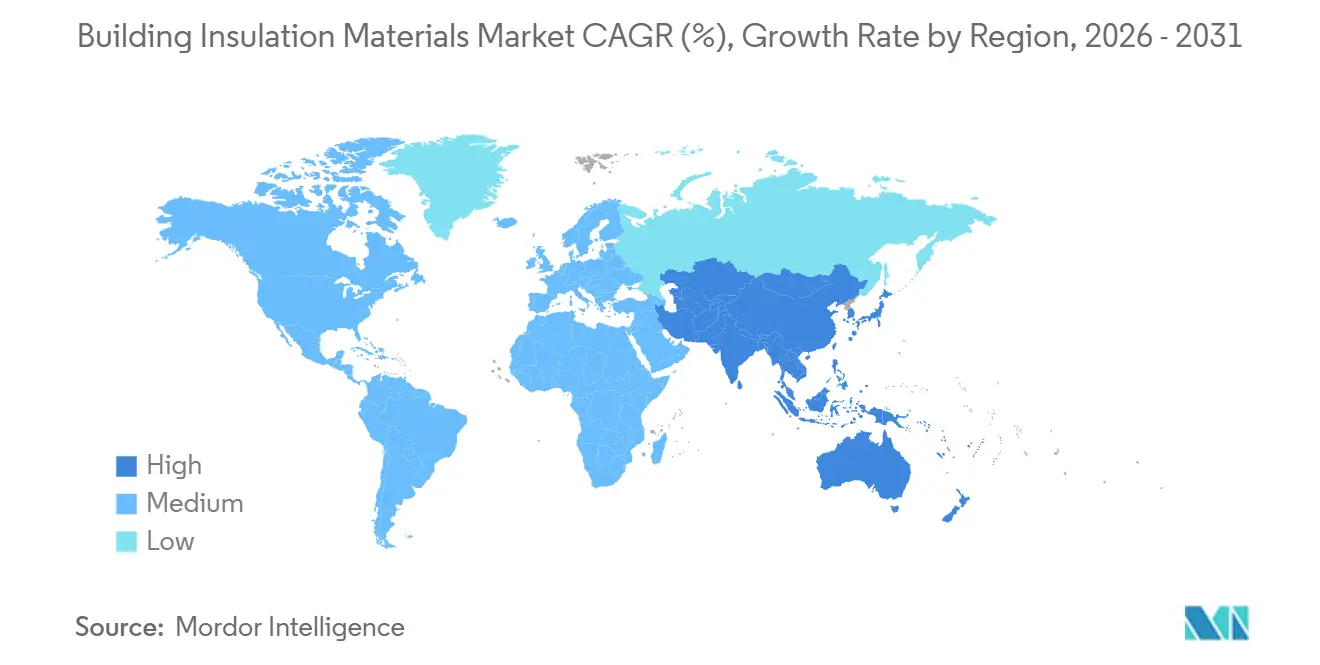

- By geography, Europe retained a 36.91% share in 2025, yet Asia-Pacific is tracking the fastest growth at a 4.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Building Insulation Materials Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Energy Efficient Buildings | +1.2% | Global, with peak intensity in EU, California, Japan | Medium term (2-4 years) |

| Increasing Green Retrofitting Incentives in North America | +0.8% | North America, spill-over to Canada and Mexico | Short term (≤ 2 years) |

| Increasing Government Support for Eco-Friendly and Sustainable Materials | +0.6% | EU, APAC core (China, South Korea), emerging in MEA | Long term (≥ 4 years) |

| Growing Preference for Low-VOC Bio-based Foams | +0.4% | North America and EU, early adoption in Australia | Medium term (2-4 years) |

| Rising Infrastructure and Industrialization in Asia-Pacific | +1.1% | APAC core (China, India, ASEAN), spill-over to South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Buildings

Forty-seven countries strengthened envelope standards in 2024 as buildings consumed 30% of global final energy[1]International Energy Agency, “Energy Efficiency 2024,” iea.org. California’s Title 24-2025 increased attic minimums to R-49, displacing lower-value fiberglass in favor of blown-in cellulose[2]California Energy Commission, “2025 Building Energy Efficiency Standards,” energy.ca.gov. The EU EPBD recast obliges member states to upgrade 3% of public floor area each year, adding roughly 240 million m² of façade insulation by 2030. Japan now requires third-party certification for non-residential structures above 300 m², which is accelerating continuous-insulation systems that eliminate thermal bridges. These rules collectively position high-R-value products as default specifications rather than premium add-ons.

Increasing Green Retrofitting Incentives in North America

The U.S. Inflation Reduction Act offers a 30% tax credit on insulation materials up to USD 1,200 annually, while the 179D deduction pays USD 5 per square foot for deep-energy retrofits. Canada’s Greener Homes Grant provided USD 3,700 equivalent per homeowner in 2024-2025 and drove attic and basement projects where heat loss surpasses 35%. Utility rebates such as Pacific Gas & Electric’s USD 0.15 per square foot wall-cavity incentive shorten payback periods to under five years. These fiscal levers have shifted insulation from a long-term payback purchase to near-term cash-flow positive upgrades, lifting renovation demand ahead of the new-build cycle.

Increasing Government Support for Eco-Friendly and Sustainable Materials

From 2027 the EU Construction Products Regulation will require environmental product declarations for all insulation, disadvantaging high-embodied-energy foams. South Korea’s Green Building Certification System grants bonus points for bio-based content above 25%. China’s 14th Five-Year Plan targets 30% recycled content in thermal insulation by 2025. Germany’s BEG subsidy adds five percentage points for materials certified under QUV, steering buyers toward mineral wool. Collectively, procurement rules are embedding circularity and life-cycle carbon limits into every specification.

Growing Preference for Low-VOC Bio-based Foams

California’s Section 01350 caps VOC emissions at 0.5 mg/m³, excluding many traditional polyurethane foams from schools and hospitals. LEED v4.1 supplies up to three credits for disclosed ingredient hazards, steering architects toward soy-based and mycelium foams. Covestro’s cardyon polyol, which replaces 20% of fossil feedstock with captured CO₂, won approvals across 12 U.S. states in 2025. Although bio-based options still cost 25-35% more than petrochemical foams, tightening IAQ limits are transferring that premium from the contractor to the code ledger.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Materials and Installation Cost | -0.9% | Global, acute in emerging markets with limited skilled labor | Short term (≤ 2 years) |

| Availability of Affordable Alternatives | -0.5% | Price-sensitive markets in South America, MEA, South Asia | Medium term (2-4 years) |

| Regulatory Scrutiny on Global Warming Potential of Blowing Agents | -0.3% | EU, North America, Japan; phased rollout in developing economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Materials and Installation Cost

Spray polyurethane foam averages USD 1.50-2.00 per board foot installed in the United States, double fiberglass batts, while delivering only 30-40% higher R-value. Contractor shortages left North America 15,000 insulators short in 2025, pushing lead times to 12 weeks. Glass-fiber rovings rose 9% on Europe’s energy spike, and styrene volatility added USD 80 per cubic meter to foam costs. These economics split the market into premium projects that adopt aerogels and value segments that postpone upgrades.

Availability of Affordable Alternatives

Reflective bubble wraps at USD 0.30-0.50 per square foot meet radiant-barrier codes in hot climates and are displacing rigid foam in U.S. attics. Recycled denim batts cost 10-15% less than fiberglass yet comply with ASTM C764. Emerging-market builders substitute rice husk or coconut coir at one-third the cost of imported mineral wool. Fourteen U.S. states now credit the inherent R-value of mass timber, reducing the amount of supplementary insulation required.

Segment Analysis

By Material Type: Fiberglass Anchors Volume, Foams Accelerate

Fiberglass held 34.65% of the building insulation materials market share in 2025, reflecting its low installed cost and contractor familiarity. Polystyrene materials are forecast to grow at a 4.18% CAGR through 2031 as continuous-insulation codes favor rigid boards that break thermal bridges. Mineral wool volume climbed 11% in European high-rise retrofits after tighter flame-spread rules. Polyurethane and polyisocyanurate foams are transitioning to HFO blowing agents, while aerogels and vacuum panels take niche share in space-constrained retrofits.

The building insulation materials market size for premium aerogel solutions commands 40-50% price premiums. Contractors default to fiberglass in code-minimum residential walls, reserve polystyrene for R-30+ commercial envelopes, and adopt bio-based foams for green-certified projects. Mineral wool’s non-combustibility exempts it from costly intumescent coatings, giving it an embedded cost edge where fire testing is strict.

Note: Segment shares of all individual segments available upon report purchase

By Application: Roofs Dominate, Acoustic and HVAC Lead Growth

Roof assemblies captured 29.19% of the 2025 demand. However, acoustic partitions and HVAC duct wraps are projected to expand at a 4.85% CAGR as open-plan retrofits seek better sound privacy and ASHRAE 90.1-2022 tightens duct leakage limits. Wall insulation applications are mainly driven by EU façade upgrades, which account for a significant share. Floor and basement products grow modestly where frost-protected foundations need under-slab foam.

Ceiling and attic applications favor blown-in cellulose that trims labor costs by 30%. LEED’s new Acoustic Performance credit is pivoting commercial builders toward mineral-wool batts and tiles. The building insulation materials market size for HVAC wraps is poised to reach USD 5 billion by 2031 as data centers specify R-6 duct jackets to cut fan energy, while cool-roof assemblies are pulling polyiso into steep-slope housing.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Residential Holds the Lion’s Share

Residential construction represented 56.77% of 2025 revenue and is advancing at 4.05% CAGR through 2031 on net-zero mandates and aggressive retrofit subsidies. Commercial and civic buildings account for the balance, with office-to-residential conversions generating full envelope re-insulation.

Single-family homes are adopting spray foam faster than multi-family projects because custom builders target low HERS scores. Multi-family relies on fiberglass and rigid foam to manage costs, while manufactured housing is moving to thicker wall batts after the 2024 HUD update. Non-residential retrofits center on adaptive reuse: Kingspan projects that 120 million ft² of U.S. space will require new façades by 2028.

By Installation: Renovation Surpasses New-Build Growth

New construction delivered 64.52% of 2025 volume, yet renovation is set to grow faster at 5.36% CAGR through 2031 as fiscal incentives collide with aging building stock. Germany’s BEG program, France’s MaPrimeRénov, and U.S. utility pay-for-performance schemes compress paybacks below six years.

Retrofit complexity adds lead-paint and asbestos abatement costs, but prefabricated panels such as Kingspan’s QuadCore reduce on-site labor by 35% and mitigate schedule risk. The building insulation materials market size for renovation projects now exceeds USD 18 billion and will widen its lead as interest-rate volatility tempers new-build starts.

Geography Analysis

Europe held 36.91% of 2025 revenue as the EPBD recast steers every member state toward zero-emission buildings by 2030. Germany processed 420,000 retrofits in 2024 under BEG, and France’s ban on F- and G-rated rentals from 2025 affects 4.8 million dwellings. Sweden now requires U-values below 0.15 W/m²K, achieved only with thick mineral wool or vacuum panels.

Asia-Pacific is the fastest-growing region at 4.89% CAGR, propelled by China’s plan for 75% of urban buildings to meet green standards by 2025. India’s 2024 code extension covers commercial buildings above 100 m² and tightens wall U-values to 0.40 W/m²K. Japan requires new non-residential buildings to beat baseline energy use by 20% from 2025. Emerging ASEAN markets adopt EDGE and Green Mark in premium projects, though residential penetration remains below 15%.

North America commands a significant market share, with growth rooted in tax-driven retrofits rather than new homes, as mortgage rates dampen housing starts. Canada’s interest-free loans up to USD 29,600 are targeting 9.5 million pre-1980 homes. Mexico’s updated NOM-020-ENER introduces mandatory envelope resistance in air-conditioned zones. South America and MEA together contribute under 10% but show episodic surges; Saudi Arabia’s code now mandates R-13 walls in all government projects, relying on 60% imports.

Competitive Landscape

The building insulation materials market is moderately fragmented. Owens Corning’s 2025 purchase of an Indian glass-fiber plant cut costs 8% and bolstered its Asia-Pacific play. Kingspan’s pentane-blown QuadCore captured 12% of UK commercial work by pre-qualifying for BREEAM Excellent. Saint-Gobain leverages direct-to-contractor rebates to lock in 70% repeat sales.

Specialty entrants fill high-performance gaps. Aspen Aerogels supplies R-10 per inch blankets that preserve historic façades. Ecovative’s mycelium foam delivers R-3 per inch at 40% lower embodied carbon than EPS, securing pilots with three U.S. developers in 2025. ROCKWOOL’s BIM-enabled Product Pilot slashed architect specification time 50% and reached 18% European adoption within a year.

Patent filings for 50-year-life vacuum panels rose 28% over 2024-2025. Private-label fiberglass at 15-20% discounts is eroding branded share in North American big-box channels. At the same time, upstream styrene swings and HFO premiums strain foam-maker margins. The competitive emphasis is shifting from commodity volume toward differentiated low-GWP formulas and digital tools that de-risk specification.

Building Insulation Materials Industry Leaders

Owens Corning

Kingspan Group

Saint-Gobain

ROCKWOOL A/S

Knauf Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kingspan committed EUR 180 million to expand insulated-panel capacity in Poland by 40%, producing QuadCore boards that meet EU F-Gas limits with pentane blowing agents.

- November 2025: Owens Corning closed a USD 215 million acquisition of Jiangsu Changhai Composite Materials, achieving 8-10% glass-fiber cost reductions in Asia-Pacific.

Global Building Insulation Materials Market Report Scope

Building insulation materials are essential for reducing heat transfer and creating a thermal envelope for structures. These materials significantly lower energy consumption, enhance cost efficiency, and improve the performance of building components such as walls, roofs, floors, windows, and mechanical systems. They also support on-site renewable and thermal systems. Primarily used for thermal and acoustic insulation, these materials additionally provide impact resistance and fire protection.

The building insulation materials market is segmented by material type, application, end-user, installation, and geography. The market is segmented by material type into fiberglass, mineral wool, cellulose, polyurethane/ polyisocyanurate (PUR/PIR) foams, polystyrene, and other insulation materials (cork, aerogel and vacuum insulation panels, spray foams, hemp, calcium-silicate, etc.).By application, the market is segmented into roof, wall (external and cavity), floor and basement, ceiling and attic, and acoustic partition and HVAC duct. By end-user, the market is segmented into residential and non-residential (commercial, infrastructure, and other non-residential industries). By installation, the market is segmented into new construction and renovation. The report also covers the market sizes and forecasts for the building insulation materials market in 16 countries across major regions. For each segment, the market sizing and forecasts are provided in terms of revenue (USD).

| Fiberglass |

| Mineral Wool |

| Cellulose |

| Polyurethane/Polyisocyanurate Foams (PUR/PIR) |

| Polystyrene |

| Other Materials (Cork, Aerogel and Vacuum Insulation Panels, Spray Foams, Hemp, Calcium-Silicate, etc.) |

| Roof |

| Wall (External and Cavity) |

| Floor and Basement |

| Ceiling and Attic |

| Acoustic Partition and HVAC Duct |

| Residential | |

| Non-Residential | Commercial |

| Infrastructure | |

| Other Non-Residential Industries (Education, Healthcare, Civic and Religious,etc.) |

| New Construction |

| Renovation |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Fiberglass | |

| Mineral Wool | ||

| Cellulose | ||

| Polyurethane/Polyisocyanurate Foams (PUR/PIR) | ||

| Polystyrene | ||

| Other Materials (Cork, Aerogel and Vacuum Insulation Panels, Spray Foams, Hemp, Calcium-Silicate, etc.) | ||

| By Application | Roof | |

| Wall (External and Cavity) | ||

| Floor and Basement | ||

| Ceiling and Attic | ||

| Acoustic Partition and HVAC Duct | ||

| By End-User | Residential | |

| Non-Residential | Commercial | |

| Infrastructure | ||

| Other Non-Residential Industries (Education, Healthcare, Civic and Religious,etc.) | ||

| By Installation | New Construction | |

| Renovation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the building insulation materials market in 2031?

The building insulation materials market is forecast to reach USD 40.99 billion by 2031 at a 3.94% CAGR over 2026-2031.

Which material currently holds the largest share?

Fiberglass commanded 34.65% global share in 2025 due to its low installed cost and contractor familiarity.

Why is renovation demand growing faster than new construction?

Retrofit tax credits, subsidy programs, and an aging building stock push renovation to 5.36% CAGR, outpacing new-build growth tied to slower housing starts.

Which region is expanding fastest?

Asia-Pacific leads with a 4.89% CAGR through 2031, driven by China’s dual-carbon goals and India’s tighter energy codes.

How are regulations influencing material choices?

Low-GWP mandates and VOC limits are steering buyers toward mineral wool, bio-based foams, and pentane-blown polyiso while phasing out high-GWP HFC foams.

What strategic moves define current competition?

Leaders invest in low-GWP technologies, backward integration to cut raw-material costs, and digital BIM tools that simplify specification and lock in repeat sales.