Europe Robotic Lawn Mower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

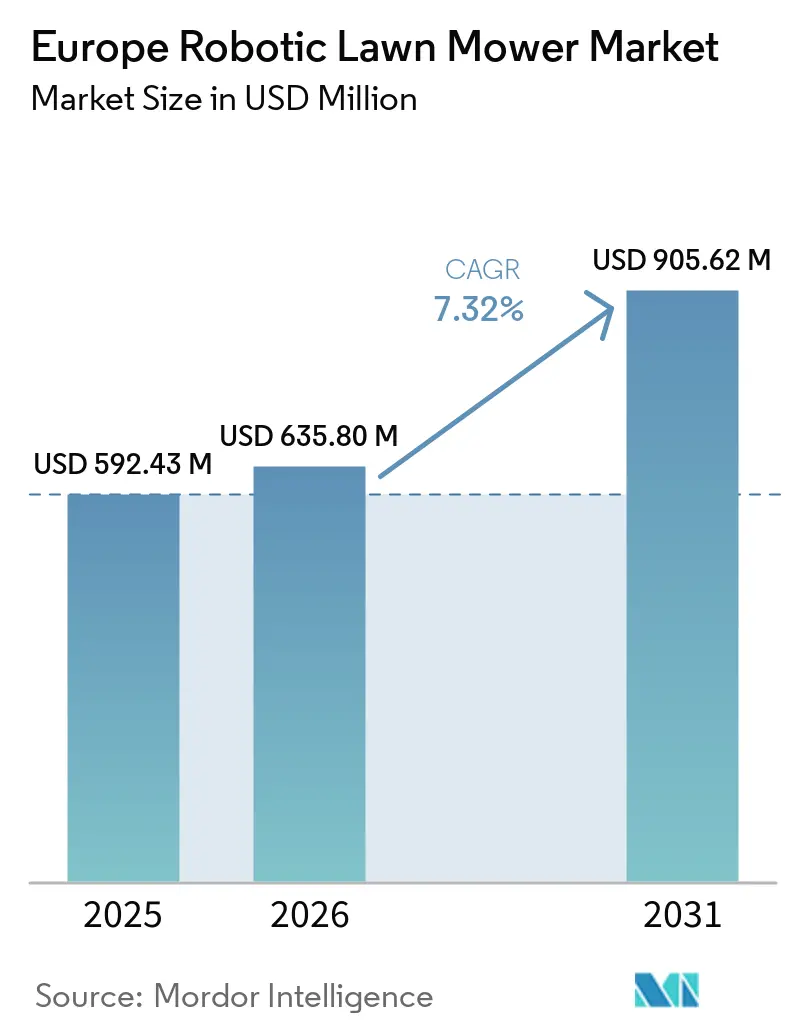

| Base Year Market Size (2025) | USD 592.43 Million |

| Market Size (2026) | USD 635.80 Million |

| Market Size (2031) | USD 905.62 Million |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Robotic Lawn Mower Market Analysis by Mordor Intelligence

The Europe robotic lawn mower market size in 2026 is estimated at USD 635.8 million, growing from 2025 value of USD 592.43 million with 2031 projections showing USD 905.62 million, growing at 7.32% CAGR over 2026-2031. The outlook reflects steady migration from niche automation toward mainstream household equipment as boundary wire-free navigation, AI-enhanced obstacle detection, and larger battery packs converge with supportive European Union eco-design regulations. Medium-range models anchor unit demand, yet premium high-range systems are scaling rapidly because advanced vision guidance eliminates installation complexity. Battery capacities above 30 V are gaining share from the Net Zero Industry Act incentives, prioritizing electric equipment manufacturing inside the bloc. Commercial landscapers are accelerating adoption in response to chronic labor shortages, while online channels reshape purchase journeys by enabling specification comparison, peer reviews, and direct-to-consumer sales. Competitive momentum is shifting toward suppliers able to combine wire-free navigation, subscription plans, and circular-economy battery strategies.

Key Report Takeaways

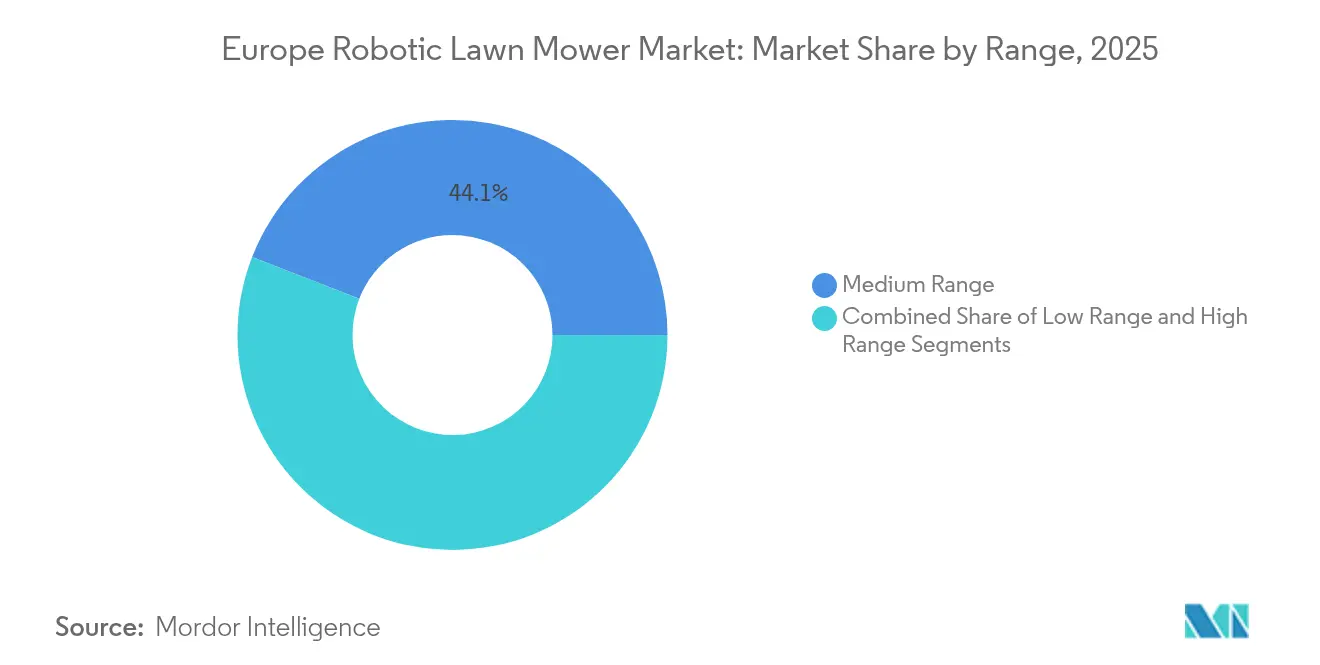

- By range, medium-range units captured 44.10% revenue share of the Europe robotic lawn mower market in 2025, whereas high-range models are advancing at a 15.55% CAGR through 2031.

- By battery capacity, the 20-30 V segment accounted for 50.25% share of the Europe robotic lawn mower market size in 2025; systems above 30 V are projected to expand at a 13.2% CAGR to 2031.

- By application, residential mowing represented 68.50% of the Europe robotic lawn mower market share in 2025, while commercial deployments are forecast to grow at 11.9% CAGR to 2031.

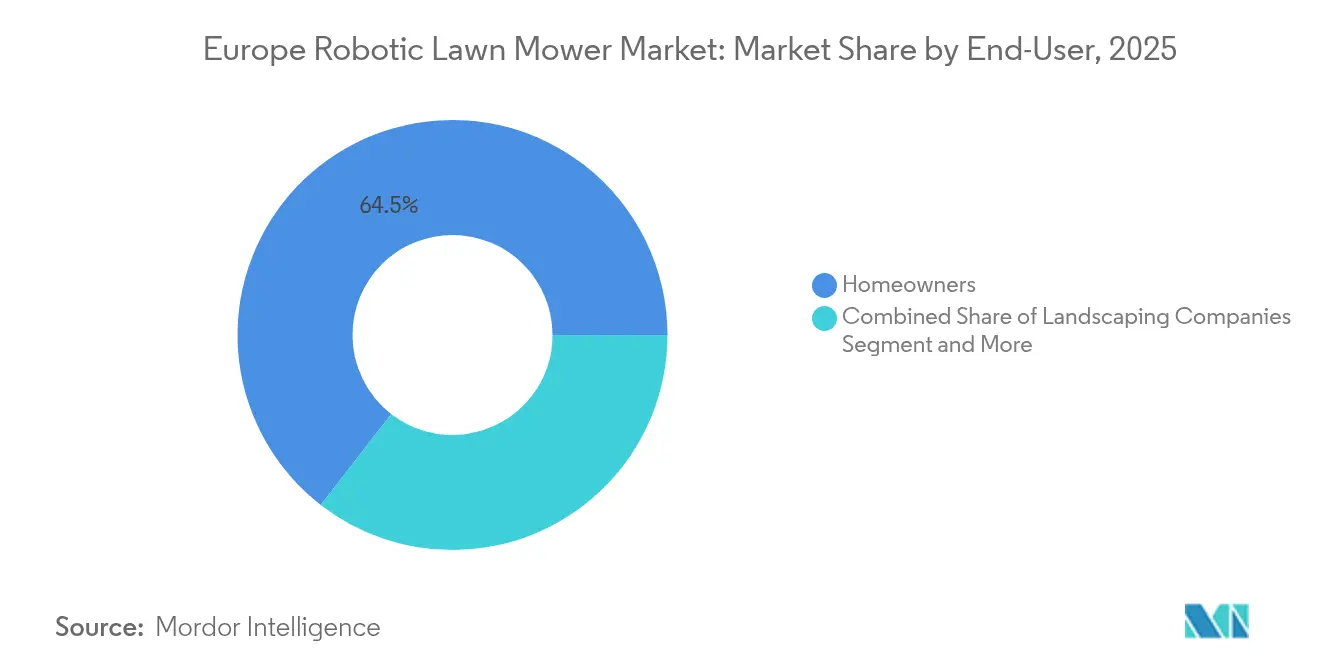

- By end-user, homeowners held a 64.50% share of the Europe robotic lawn mower market in 2025; landscaping companies exhibit the fastest CAGR at 11.2% through 2031.

- By connectivity, boundary-wire models commanded a 52.70% share in 2025, but vision-guided platforms are expanding at a 19.1% CAGR.

- By channel, retailers controlled 58.00% of 2025 sales; online platforms are rising at 16.4% CAGR.

- By country, Germany led with 17.45% share in 2025, whereas Spain is the fastest-growing geography at 12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on robotic lawn mower market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Robotic Lawn Mower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Time-Saving Home Automation | +1.6% | Global, with Highest Penetration in Germany, Netherlands, Sweden | Medium Term (2–4 Years) |

| EU Incentives Favor Battery Equipment | +1.2% | EU-Wide, Strongest in Western Europe | Long Term (≥ 4 Years) |

| Edge AI Enables Wire-Free Installation | +1.1% | Technology-Forward Markets: Germany, Netherlands, Switzerland | Short Term (≤ 2 Years) |

| Smart Homes With Turf Management Integration | +0.9% | Northern Europe, Germany, Netherlands, Sweden | Medium Term (2–4 Years) |

| Aging Homeowners Drive Low-Effort Lawn Care | +0.8% | Western Europe, Particularly Germany, France, Italy | Long Term (≥ 4 Years) |

| Rise of Subscription & Robot-as-a-Service Models | +0.7% | Urban Markets Across Major EU Cities | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Rising Demand for Time-Saving Home-Automation Devices

European homeowners increasingly integrate robotic lawn mowers into comprehensive smart home ecosystems, driven by time constraints and lifestyle preferences. The trend accelerates as manufacturers develop seamless connectivity with existing home automation platforms, enabling voice control and smartphone management. STIHL's iMOW series now integrates smart home systems and voice command capabilities, reflecting consumer demand for unified automation experiences[1]"Smart lawn care with ¡MOW® robotic lawn mowers", STIHL, stihl.co.uk.. This integration extends beyond basic mowing to include weather-responsive scheduling and maintenance alerts. The demographic shift toward dual-income households amplifies demand for autonomous solutions that eliminate weekend lawn care obligations. Smart home penetration rates in Northern European markets correlate directly with robotic mower adoption patterns, suggesting that technology familiarity drives purchase decisions.

EU Green Deal Incentives Favoring Battery-Powered Equipment

The European Union's regulatory framework creates structural advantages for battery-powered robotic mowers through multiple policy channels. The Net Zero Industry Act prioritizes local manufacturing of clean technologies, while new battery regulations under EU 2023/1542 establish sustainability requirements that favor electric equipment over fossil fuel alternatives[2]"REGULATION (EU) 2023/1542 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL", EUR-Lex, eur-lex.europa.eu. . Ecodesign requirements mandate product lifecycle assessments that inherently favor robotic mowers due to their energy efficiency and reduced emissions profiles. Member states are implementing complementary incentives, including tax credits for electric garden equipment and restrictions on gas-powered tools in urban areas. The regulatory momentum creates competitive disadvantages for conventional mowers while establishing long-term market tailwinds for robotic alternatives. Battery recycling mandates under the new framework also drive innovation in sustainable power systems, benefiting manufacturers investing in circular economy approaches.

Ageing Homeowner Population Boosting Demand for Low-Effort Lawn Care

Demographic transitions across Western Europe fundamentally reshape lawn care preferences as aging homeowners seek alternatives to physically demanding maintenance routines. The trend is particularly pronounced in Germany and Italy, where homeownership rates among seniors exceed 70% and physical limitations increasingly constrain traditional mowing capabilities. Robotic mowers eliminate the physical exertion, noise exposure, and safety risks associated with conventional equipment, making them attractive to older demographics. Healthcare cost considerations also influence adoption as seniors recognize the injury prevention benefits of automated systems. The market response includes simplified installation processes and enhanced safety features designed for less tech-savvy users. Manufacturers are developing larger-capacity models capable of handling extensive properties without frequent intervention, addressing the needs of suburban retirees with significant lawn areas.

Construction of Smart-Homes with Integrated Turf-Management Hubs

New residential construction increasingly incorporates dedicated infrastructure for robotic lawn care systems, reflecting builder recognition of automation as a standard amenity. Smart home developers are pre-installing charging stations, weather sensors, and connectivity infrastructure that seamlessly integrate with robotic mowing systems. The trend is most pronounced in Northern European markets where new construction standards emphasize energy efficiency and automation readiness. Builders report that robotic mower compatibility has become a selling point for premium residential developments, particularly in suburban markets targeting tech-savvy buyers. Integration extends to landscape design, with architects incorporating mower-friendly layouts and obstacle-free zones that optimize autonomous operation. The infrastructure investment creates switching costs that favor robotic solutions over conventional alternatives throughout the property lifecycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost vs. Conventional Mowers | -0.9% | Price-sensitive markets: Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| Theft Risk in Urban & Shared Housing | -0.6% | Dense urban areas: Paris, London, Berlin, Amsterdam | Medium term (2-4 years) |

| Low Efficiency on Steep or Tiered Lawns | -0.4% | Mountainous regions: Switzerland, Austria, Northern Italy | Long term (≥ 4 years) |

| Fragmented EU Standards Delay Regional Launches | -0.3% | EU-wide, particularly affecting smaller manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Mowers

Price sensitivity remains the primary barrier to robotic mower adoption, particularly in Eastern and Southern European markets where household disposable income lags Western European levels. Premium boundary wire-free models command prices exceeding EUR 3,000, representing 3-5 times the cost of equivalent conventional mowers. The cost differential is most pronounced for larger-capacity systems, where advanced GPS navigation and AI-powered obstacle detection drive significant price premiums. Consumer financing options and leasing programs are emerging to address affordability constraints, though adoption remains limited compared to the automotive or appliance sectors. The total cost of ownership calculation often favors robotic systems over 5-7 year periods when factoring labor savings and fuel costs. Yet, consumers typically focus on initial purchase price rather than lifecycle economics. Manufacturers are developing entry-level models to expand market accessibility, though feature limitations may constrain appeal among demanding users.

Theft-Vulnerability in Shared-Housing and Urban Settings

Security concerns significantly constrain adoption in dense urban environments where robotic mowers face elevated theft risks due to limited storage options and high visibility during operation. The problem is particularly acute in apartment complexes and shared housing arrangements where secure storage is unavailable, and multiple residents have access to common areas. Insurance coverage for robotic equipment remains inconsistent across European markets, creating financial risk that deters potential buyers. Anti-theft technologies including GPS tracking, alarm systems, and smartphone alerts are becoming standard features, though determined thieves can still overcome these protections. Urban adoption patterns show strong correlation with secure storage availability, suggesting infrastructure limitations rather than technology constraints drive the restraint. Manufacturers are developing more robust security features and exploring partnership models with property management companies to address shared-space challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Range: High-End Models Drive Premium Growth

Medium-range robotic mowers hold the largest market share at 44.10% in 2025, while high-range models are experiencing accelerated adoption with a CAGR of 15.55% through 2031.The premium segment benefits from technological sophistication, including advanced AI navigation, extended battery life, and comprehensive connectivity features that justify higher price points. Low-range models serve price-sensitive consumers but face margin pressure from feature-rich alternatives. Professional landscapers increasingly specify high-end systems for commercial applications where reliability and coverage capacity outweigh cost considerations. The shift toward boundary wire-free technology benefits high-end segments where GPS precision and obstacle detection capabilities command premium pricing. Husqvarna's launch of 13 new boundary wire-free models in 2025 demonstrates the manufacturer's focus on premium market expansion.

The range segmentation reflects evolving consumer sophistication as early adopters graduate from basic models to feature-rich alternatives. Medium-range products occupy the sweet spot for suburban homeowners seeking reliable automation without premium pricing, explaining their dominant market position. High-range growth acceleration suggests successful value proposition communication around advanced features and long-term reliability benefits.

By Battery Capacity: Power Density Evolution Favors Higher Voltages

The 20 to 30V models hold the largest market share at 50.25% in 2025, while more-than-30V systems drive a technological transition with a CAGR of 13.2% through 2031. Higher-voltage systems enable extended runtime, faster charging, improved cutting performance on challenging terrain, driving adoption among demanding users. Less-than-20V models serve compact lawn applications but face competitive pressure from more capable alternatives. The voltage evolution parallels broader power tool industry trends toward higher-capacity lithium-ion systems that deliver superior performance per unit weight. STIHL's battery product strategy targets 35% of sales from battery-operated tools by 2027, indicating the manufacturer's commitment to higher-capacity systems.

Manufacturing economies of scale in lithium-ion production are reducing cost premiums for higher-voltage systems, accelerating market transition. The capacity segmentation also reflects lawn size distributions across European markets, where larger suburban properties increasingly demand extended runtime capabilities. Battery recycling regulations under EU 2023/1542 favor manufacturers investing in sustainable, higher-capacity systems over disposable, lower-voltage alternatives.

By Sales Channel: Digital Commerce Transforms Distribution

Retailers maintain the largest market share at 58.00% in 2025, but online sales channels are rapidly expanding with a CAGR of 16.4% through 2031, challenging traditional retail dominance. Digital platforms offer superior product comparison capabilities, customer reviews, and technical specifications that inform complex purchase decisions for robotic systems. Specialty stores provide expert consultation and demonstration capabilities that remain valuable for first-time buyers evaluating automation solutions. The channel evolution reflects broader consumer electronics trends toward online research and purchase, particularly among tech-savvy demographics driving robotic adoption. E-commerce growth accelerates during seasonal peaks when immediate availability and competitive pricing become critical factors. Manufacturers invest in direct-to-consumer platforms and digital marketing capabilities to capture online channel growth.

Traditional retail channels maintain advantages in after-sales service, warranty support, and hands-on demonstration that remain important for complex robotic systems. The multichannel approach allows consumers to research online while completing purchases through preferred channels, suggesting complementary rather than substitutional relationships between digital and physical distribution.

By Application: Commercial Adoption Accelerates Beyond Residential Base

Residential applications hold the largest market share at 68.50% in 2025, while commercial applications are growing rapidly with a CAGR of 11.9% through 2031, fueled by labor shortages and operational efficiency demands. Professional landscaping companies increasingly deploy robotic systems to reduce labor costs and improve service consistency across multiple client properties. Golf courses represent a particularly attractive commercial segment where turf quality improvements and reduced maintenance costs justify premium system investments. The ROBO-GOLF Project across five European countries demonstrated that robotic mowers maintain acceptable turf quality while reducing weed and disease occurrence, supporting commercial adoption. Sports facilities and municipal parks are evaluating robotic solutions for large-area maintenance where labor availability constraints limit conventional approaches.

Residential applications benefit from declining prices and improved ease-of-use, though growth rates lag commercial segments where return-on-investment calculations favor automation. The application segmentation suggests market maturation as robotic technology proves viable across diverse use cases beyond its initial residential focus.

By End-User: Professional Services Drive Growth Acceleration

Homeowners hold the largest market share at 64.50% in 2025, while landscaping companies represent the fastest-growing end-user segment with an 11.2% CAGR through 2031. Professional adoption reflects labor market constraints and client demand for consistent service quality that robotic systems can deliver. Sports grounds and parks management increasingly specify robotic solutions for large-area maintenance where traditional approaches face scalability limitations. Golf courses benefit from improved turf conditions and reduced operational costs, driving adoption across European facilities. Municipalities evaluate robotic systems for public space maintenance where budget constraints and environmental considerations favor efficient electric alternatives. The professional segment growth suggests successful value proposition development around operational efficiency and service quality improvements.

Homeowner adoption continues expanding as prices decline and technology sophistication increases, though growth rates moderate as early adopter segments reach saturation. The end-user evolution indicates market broadening beyond initial residential focus toward diverse professional applications with distinct value propositions.

By Connectivity: Vision-Guided Systems Disrupt Traditional Approaches

Boundary-wire connectivity systems hold the largest market share at 52.70% in 2025, while vision-guided systems are achieving the fastest growth with a 19.1% CAGR through 2031. GPS and Wi-Fi-enabled models eliminate installation complexity while providing superior navigation precision and obstacle avoidance capabilities. Smart connectivity features, including smartphone control, weather integration, and maintenance alerts, drive consumer preference toward advanced systems. The technology transition reflects broader automation trends toward sensor-based navigation rather than physical boundary definition. Husqvarna's EPOS satellite navigation system and EdgeCut technology demonstrate the performance advantages driving vision-guided adoption.

Boundary-wire systems maintain market leadership through lower costs and proven reliability, though installation complexity increasingly constrains adoption among less technical users. The connectivity evolution suggests fundamental technology disruption as vision-guided systems eliminate traditional limitations while providing enhanced functionality.

Geography Analysis

Germany commands European market leadership with 17.45% market share in 2025, reflecting early technology adoption and strong consumer acceptance of automation solutions. The German market benefits from high homeownership rates, substantial suburban development, and cultural preferences for precision engineering that align with robotic mower capabilities. Consumer electronics familiarity and environmental consciousness drive the adoption of battery-powered alternatives over conventional fuel-based equipment. Technology reviews in German media consistently highlight boundary wire-free models from Segway, Ecovacs, and Husqvarna, indicating strong consumer interest in advanced navigation systems. The market shows price premiums for feature-rich models, suggesting consumers prioritize performance over cost considerations.

Spain is the fastest-growing market at 12% CAGR through 2031, driven by expanding suburban development and rising household disposable income. The Spanish market benefits from favorable climate conditions that extend mowing seasons and justify automation investments. New residential construction increasingly incorporates smart home infrastructure that supports robotic integration. France and Italy represent substantial opportunities with large suburban populations and growing environmental awareness, favoring electric equipment. These markets show increasing acceptance of premium pricing for innovative solutions, though adoption rates lag Northern European levels. The United Kingdom maintains steady growth, supported by strong garden culture traditions and consumer willingness to invest in lawn care innovation.

Smaller European markets, including the Netherlands, Belgium, and Switzerland, demonstrate high per-capita adoption rates driven by elevated disposable income and technology acceptance. Sweden and Austria show consistent growth supported by environmental regulations that favor electric equipment over conventional alternatives. The Nordic markets particularly benefit from government incentives for sustainable technologies and consumer preferences for quiet operation in dense residential areas. Eastern European markets remain underpenetrated despite suitable demographic conditions, suggesting significant expansion opportunities as economic development continues and technology costs decline.

Competitive Landscape

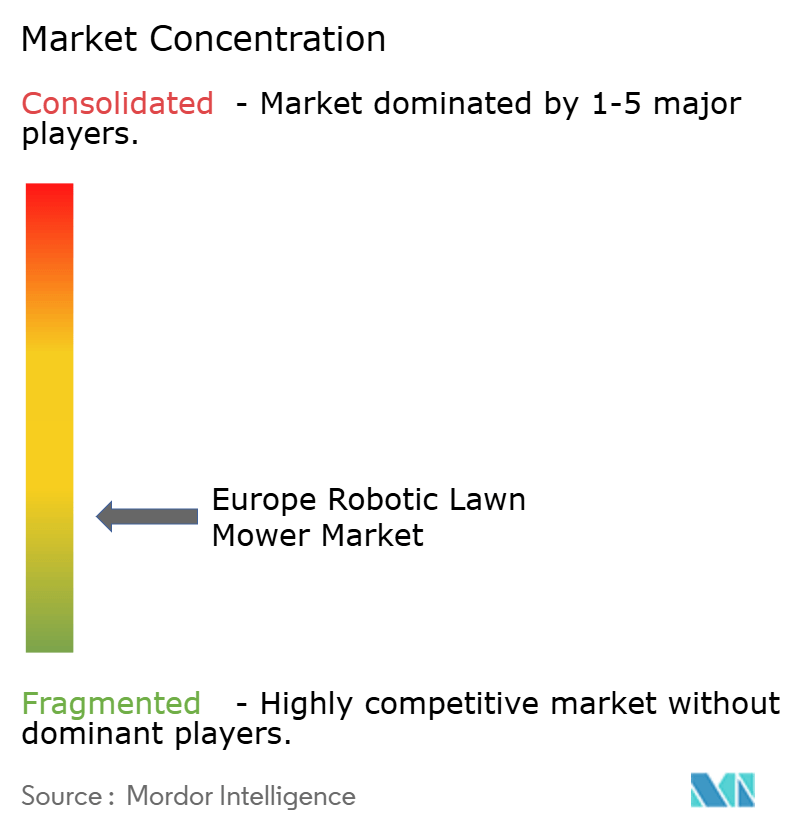

The Europe robotic lawn mower market is moderately concentrated. Husqvarna Group retains leadership by launching 13 new boundary wire-free models for the 2025 season, expanding coverage from small gardens to 50,000 m² sports fields.

Robert Bosch GmbH invests EUR 7.3 billion annually in R&D, leveraging AI expertise from its Consumer Goods division to enhance SLAM algorithms and energy-management firmware. STIHL is scaling battery production capacity with a new Romanian factory opening in 2025, aiming to increase battery product share to 35% by 2027.

Emerging challengers like Lymow and Segway infuse the field with RTK satellite positioning and dual-blade designs that promise faster cut cycles. Market entry barriers persist in the form of IEC 60335-2-107 safety certification costs and cybersecurity requirements, which tilt the playing field toward incumbents possessing dedicated compliance laboratories. Strategic alliances between OEMs and smart-home platform providers intensify as connectivity becomes the primary battleground differentiator.

Europe Robotic Lawn Mower Industry Leaders

-

AL-KO Gardentech

-

Belrobotics

-

Deere & Company

-

Husqvarna Group

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lymow unveiled the Lymow One smart robotic mower at CES 2025, featuring advanced RTK satellite positioning, VSLAM navigation, and a dual-blade system operating at 6,000 rpm.

- October 2024: Husqvarna Group unveiled four new robotic lawnmowers for professional green space management, including the Automower 580L EPOS, 580 EPOS, 560 EPOS, and updated 535 AWD EPOS models. These boundary wire-free systems feature GPS navigation and advanced cutting patterns for areas ranging from 6,000 m² to 16,000 m², targeting sports fields and golf courses.

Europe Robotic Lawn Mower Market Report Scope

A robotic lawn mower is an autonomous device equipped with sensors and programming to perform grass-cutting tasks without human intervention. These are used for residential and commercial purposes by homeowners, apartment owners, in parks and playgrounds, and other places.

The scope of the European Robotic Lawn Mower Market is segmented by Range, Battery Capacity, Sales Channel, Application, End User, and Country. By Range, the market is segmented into Low, Medium, and High. By Battery Capacity, the market is segmented into Less than 20V, 20V to 30V, and Above 30V. By Sales Channel, the market is segmented into Retailers, Specialty Stores, and Online. By Application, the market is segmented into Residential and Commercial. By End User the market is segmented into Homeowners, Landscaping Companies, and Sports Grounds & Parks. By Country, the market is segmented into Germany, United Kingdom, France, Italy, Spain, Sweden, Netherlands, and the Rest of Europe.

The report offers the market size in value (USD) and forecasts for all the above segments.

| Low Range |

| Medium Range |

| High Range |

| Less Than 20 V |

| 20 to 30 V |

| More Than 30 V |

| Retailers |

| Specialty Stores |

| Online |

| Residential |

| Commercial |

| Homeowners |

| Landscaping Companies |

| Sports Grounds and Parks |

| Municipalities |

| Golf Courses |

| Others |

| Boundary-Wire |

| Smart-GPS / Wi-Fi |

| Vision-Guided (Camera/LiDAR) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Sweden |

| Netherlands |

| Belgium |

| Austria |

| Switzerland |

| Poland |

| Rest of Europe |

| By Range | Low Range |

| Medium Range | |

| High Range | |

| By Battery Capacity | Less Than 20 V |

| 20 to 30 V | |

| More Than 30 V | |

| By Sales Channel | Retailers |

| Specialty Stores | |

| Online | |

| By Application | Residential |

| Commercial | |

| By End-User | Homeowners |

| Landscaping Companies | |

| Sports Grounds and Parks | |

| Municipalities | |

| Golf Courses | |

| Others | |

| By Connectivity | Boundary-Wire |

| Smart-GPS / Wi-Fi | |

| Vision-Guided (Camera/LiDAR) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Netherlands | |

| Belgium | |

| Austria | |

| Switzerland | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe robotic lawn mower market?

The market stands at USD 635.8 million in 2026 and is projected to reach USD 905.62 million by 2031.

Which range segment is growing fastest?

High-range models exhibit the highest growth at a 15.55% CAGR owing to AI navigation and extended battery life.

How important is battery capacity in purchase decisions?

Systems Above 30 V are gaining traction at a 13.2% CAGR because they deliver longer runtimes and faster charging.

Which country leads in market share?

Germany holds 17.45% share, driven by early technology adoption and strict noise regulations.

Page last updated on: