Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

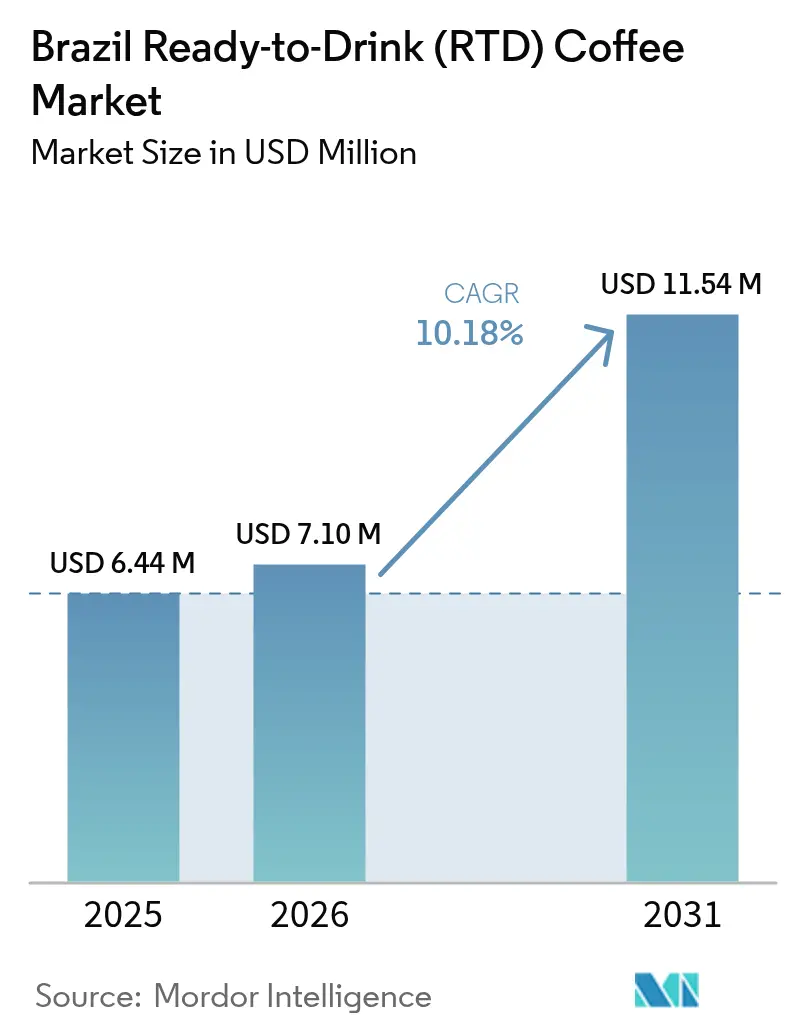

| Base Year Market Size (2025) | USD 6.44 Million |

| Market Size (2026) | USD 7.1 Million |

| Market Size (2031) | USD 11.54 Million |

| Growth Rate (2026 - 2031) | 10.18% CAGR |

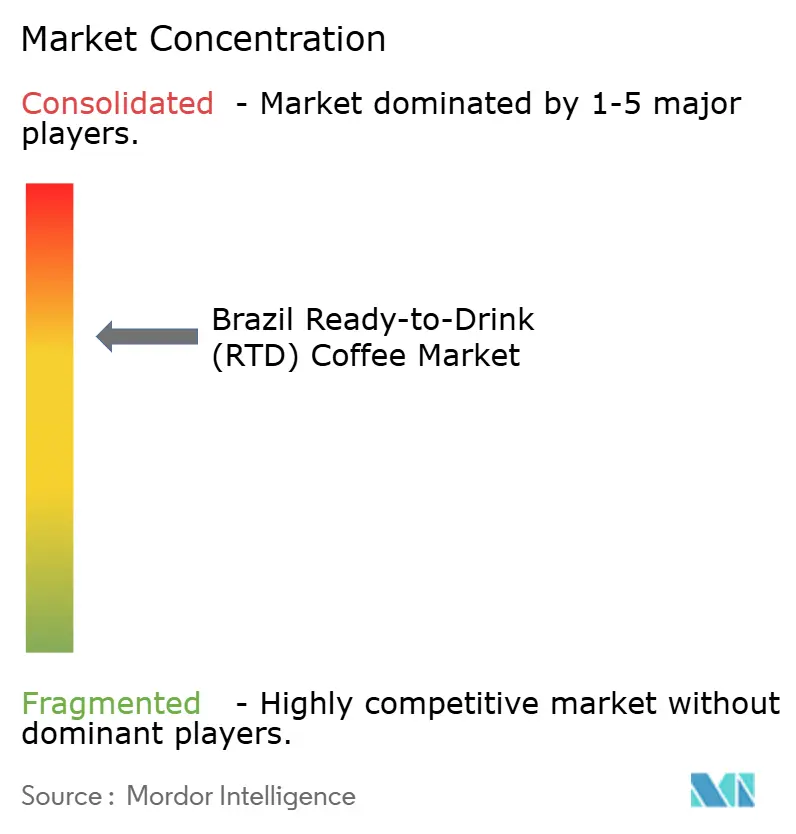

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Ready-to-Drink (RTD) Coffee Market Analysis by Mordor Intelligence

The Brazil ready-to-drink coffee market size in 2026 is estimated at USD 7.1 million, growing from 2025 value of USD 6.44 million with 2031 projections showing USD 11.54 million, growing at 10.18% CAGR over 2026-2031. This growth is being driven by several key factors, including the increasing mobility of urban populations, the introduction of innovative premium flavors, and sustained capital investments by leading beverage companies. These trends are reshaping consumer preferences, with more individuals opting for chilled, single-serve coffee as a convenient alternative to traditional carbonated soft drinks. Corporate confidence in the market is evident, with investment commitments exceeding BRL 9.2 billion (Brazilian Real) since 2024. Furthermore, improvements in cold-chain infrastructure and the expansion of digital commerce platforms are reducing distribution challenges and enhancing product accessibility. Health-conscious reformulations, the adoption of sustainable packaging solutions, and the incorporation of functional ingredients are also influencing the competitive dynamics of the market. To secure consumer loyalty, brands are focusing on achieving a balance between indulgence, natural product positioning, and maintaining price competitiveness. The market remains moderately consolidated, with the top two suppliers holding a combined 60% market share, leaving significant opportunities for regional players and niche innovators to establish and grow their presence.

Key Report Takeaways

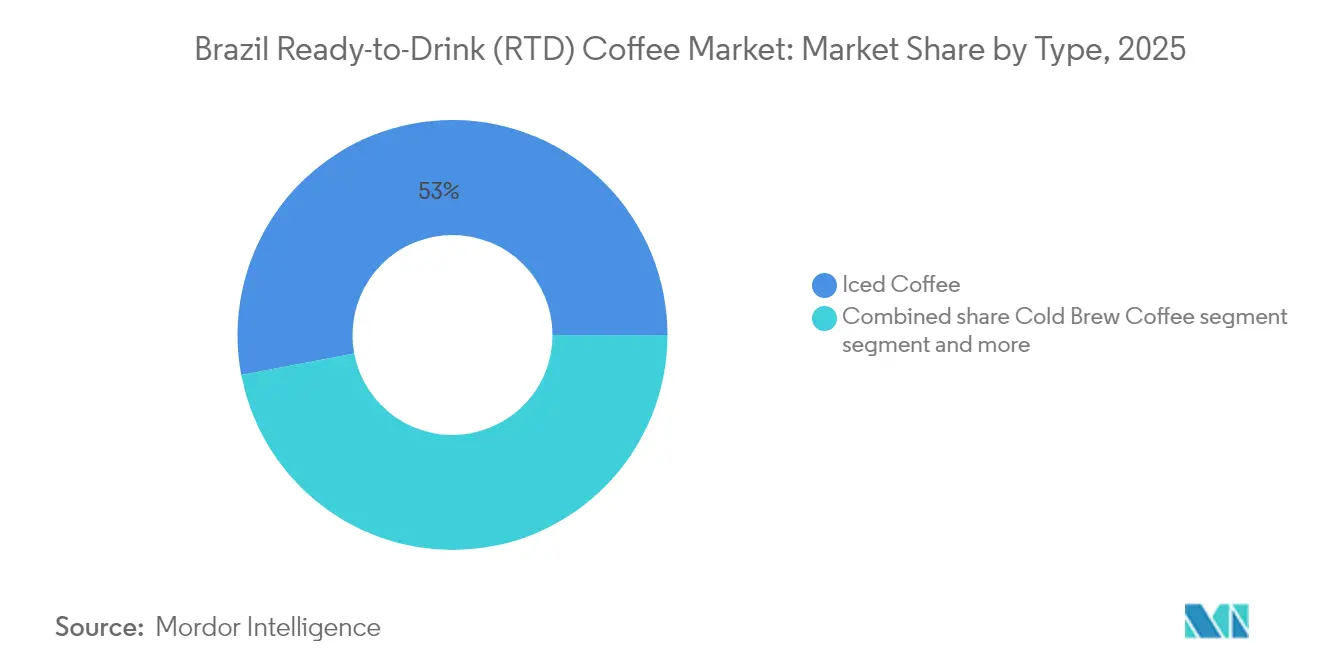

- By type, iced coffee led with 52.98% share in 2025, whereas cold brew is poised to outpace the Brazil ready-to-drink coffee market at an 11.37% CAGR through 2031.

- By packaging, PET bottles held 34.84% of the Brazil ready-to-drink coffee market share in 2025, and metal cans are forecast to register the fastest growth at 11.42% CAGR to 2031.

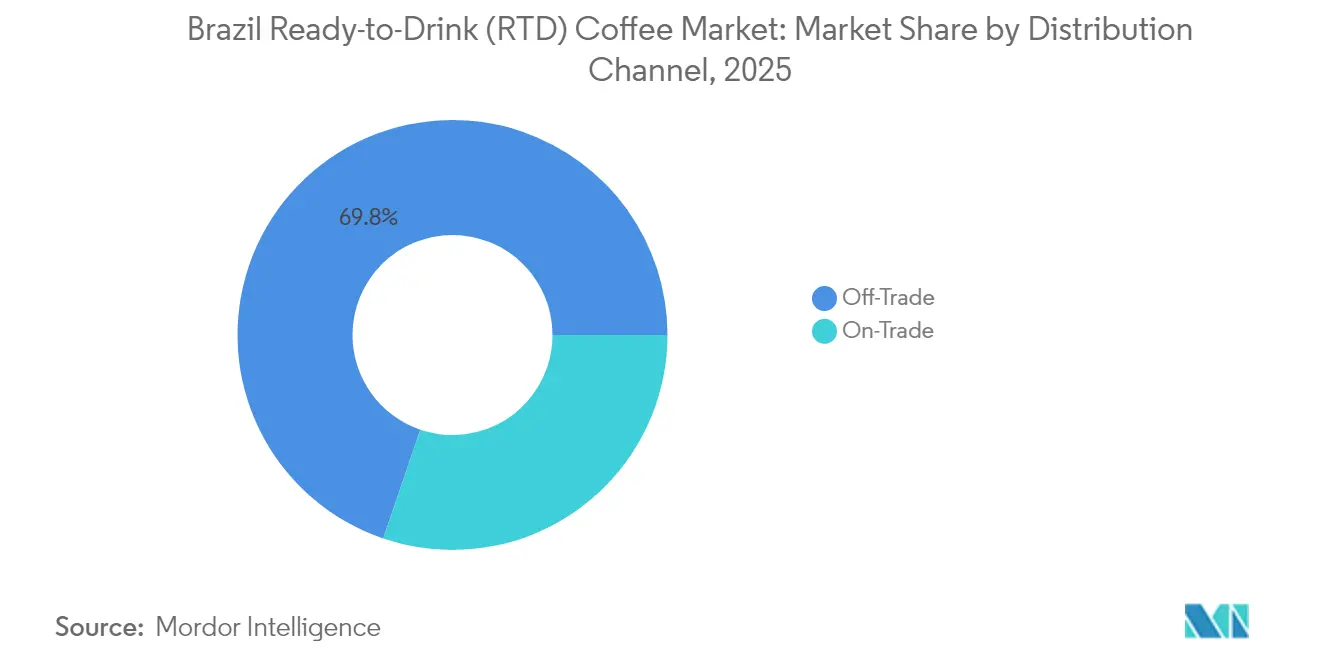

- By distribution channel, off-trade dominated with 69.78% share in 2025 and is anticipated to grow at an 10.87% CAGR, underpinned by e-commerce volumes rising at 25.4% CAGR between 2025 and 2029.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Ready-to-Drink (RTD) Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising on-the-go lifestyle and demand for convenient caffeine formats | +2.8% | National, with concentration in São Paulo, Rio de Janeiro, Belo Horizonte metropolitan areas | Short term (≤ 2 years) |

| Growing popularity of cold brew and iced coffee for smoother, less-acidic profile | +2.1% | National, with early adoption in urban centers and specialty coffee shops | Medium term (2-4 years) |

| Shift from carbonated soft drinks toward more purposeful beverages like RTD coffee | +1.9% | National, driven by health-conscious millennials and Gen Z in urban markets | Medium term (2-4 years) |

| Expansion of flavored and indulgent variants attracting younger consumers | +1.6% | National, with premium positioning in São Paulo, Rio de Janeiro, Brasília | Short term (≤ 2 years) |

| Rising interest in low-sugar/no-sugar formulations in response to health consciousness | +1.4% | National, accelerated by ANVISA front-of-pack labeling regulations | Medium term (2-4 years) |

| Product diversification into energy-style RTD coffees competing with energy drinks | +1.2% | National, targeting fitness and professional segments in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising on‑the‑go lifestyle and demand for convenient caffeine formats

Urbanization and increasing commute times in Brazilian metropolitan areas are significantly influencing coffee consumption habits, leading to a shift from traditional sit-down café experiences to more convenient grab-and-go formats that cater to fragmented daily schedules. Nestlé, recognizing this trend, has strategically emphasized single-serve ready-to-drink (RTD) coffee products and out-of-home vending machines to meet the needs of younger consumers under 24 years old. This demographic values convenience and speed over traditional brewing rituals, making them a key target for such offerings. Nestlé projects an impressive 15% annual growth for its RTD coffee portfolio, far outpacing the broader Brazilian coffee market's growth rate of 5-6%, which underscores the growing consumer preference for convenience-driven formats over legacy categories. Supporting this trend, Oxxo, a convenience-store chain, has expanded its footprint to 564 stores in Brazil, adding 184 new locations in the past year, and introduced its Andatti coffee brand in November 2024. This move illustrates how convenience-store chains are positioning RTD coffee as both a driver of customer traffic and a contributor to higher profit margins, complementing traditional snack and beverage offerings. Furthermore, Starbucks Frappuccino's availability through Drogal pharmacy chains at a price of BRL 14.99 per 280ml unit highlights the potential for RTD coffee to command premium pricing even in non-traditional retail settings, provided that convenience and brand equity are effectively aligned.

Growing popularity of cold brew and iced coffee for their smoother, less‑acidic profile

Cold brew's 20-hour infusion process produces a coffee concentrate with 67% lower acidity compared to hot-brewed coffee. This lower acidity makes it particularly appealing to consumers who experience gastrointestinal discomfort from traditional espresso-based beverages or those who prefer a smoother, milder flavor profile. This flavor profile is well-suited for customization with milk, sweeteners, and flavor additions, as it avoids the bitterness often associated with hot-brewed coffee. Dark Angel Cold Brew introduced Brazil's first nationally available organic cold brew coffee in a 200ml format, originating from Florianópolis. The product is positioned as a premium, health-conscious alternative to mass-market iced coffee options. In São Paulo, iced coffee sales represented 12% of total café sales, with the largest purchasing demographic being consumers under 30 years old. This trend suggests that cold coffee formats are increasingly becoming a generational preference rather than a seasonal novelty. In 2024, major brands such as McDonald's, Havanna, Momo, and Bendito launched cold coffee products priced between BRL 14.90 and BRL 26.00. These products targeted "Starbucks orphans," a term referring to consumers seeking premium cold coffee experiences following the closure of Starbucks stores in Brazil. This development underscores the growing demand for accessible luxury within the ready-to-drink (RTD) coffee market.

Shift from carbonated soft drinks toward “more purposeful” beverages like RTD coffee

A consumer study conducted by Kerry Group in August 2024, involving 225 Brazilian participants, highlighted significant shifts in beverage consumption preferences. The study found that 49% of respondents intend to reduce their soda consumption, while 54% expressed a willingness to increase their beverage intake if the formulations included more natural ingredients and reduced sugar content. Additionally, 49% of those surveyed actively seek beverages with functional or nutritional benefits. These findings underscore the growing demand for Ready-to-Drink (RTD) coffee, which can cater to these preferences by incorporating ingredients such as protein, adaptogens (natural substances believed to help the body adapt to stress), and nootropics (compounds that may enhance cognitive function). In Brazil, the market for functional beverages and specialty coffees is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) from 2023 to 2034, reflecting a structural shift in consumer spending toward products perceived to offer health benefits. Guarana, a flavor synonymous with Brazilian soft drinks, is increasingly being integrated into RTD coffee formulations to deliver a combination of caffeine synergy and cultural familiarity. Globally, the guarana market is anticipated to grow at a CAGR of 9.6%, with South America contributing approximately 46% of the total demand. Among the various forms, liquid guarana extracts are particularly preferred for applications in RTD beverages.

Expansion of flavored and indulgent variants attracting younger consumers

In April 2025, Nestlé plans to launch Nescafé Ready-to-Drink (RTD) coffee in latte, cappuccino, and mocha variants, featuring chocolate and caramel flavors. This initiative aims to cater to younger consumers who favor indulgent, dessert-like coffee experiences that blend the characteristics of a beverage and a treat. Millennials and Generation Z, who constitute 60-70% of specialty coffee consumers in Brazil, are open to paying premium prices—ranging from BRL 10 to BRL 45 per unit in café settings—for distinctive flavor profiles, visually appealing presentations, and a sense of authenticity. Third-wave coffee shops in Brazil are growing at an annual rate of 15-20%, fostering a trend that supports premium pricing and encourages flavor experimentation in RTD products available through retail channels. Café Caramello, a Brazilian company founded in 2012, produces coffee cream in over 30 flavors. These products are offered hot or cold, are lactose-free, gluten-free, preservative-free, and contain 27 calories per tablespoon. The company operates more than 200 locations and has manufacturing facilities in Brazil, the United States, and Portugal, with plans to establish additional factories in France, Dubai, and Italy by the end of 2025. This global expansion underscores how Brazilian coffee flavor innovation can achieve international success by addressing dietary restrictions and calorie-conscious preferences without compromising on taste. Additionally, flavor diversity encourages consumer trials, as individuals who may not prefer black cold brew are more inclined to try caramel macchiato or mocha options. This broadens the market to include not only traditional coffee enthusiasts but also soft-drink consumers and those seeking dessert-like beverages.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer concerns about high caffeine intake and artificial additives in some formulations | -0.9% | National, with heightened awareness in health-conscious urban demographics | Medium term (2-4 years) |

| High sugar content in many RTD coffees clashing with health-and-wellness trends | -1.3% | National, accelerated by ANVISA front-of-pack labeling and public health campaigns | Short term (≤ 2 years) |

| Cold-chain dependence leading to higher logistics and merchandising costs | -1.1% | National, with acute challenges in North and Northeast regions due to infrastructure gaps | Long term (≥ 4 years) |

| Regulatory complexity around dairy, coffee, and functional claims on labels | -0.7% | National, governed by ANVISA RDC 429/2020 and IN 75/2020 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer concerns about high caffeine intake and artificial additives in some formulations

Caffeine content in ready-to-drink (RTD) coffee varies significantly, ranging from 80 milligrams in a 240ml serving of standard iced coffee to over 200 milligrams in energy-focused cold brew concentrates. This variation poses a risk of overconsumption, particularly for consumers who may underestimate their caffeine intake or combine RTD coffee with other caffeinated beverages throughout the day. According to a study by Kerry Group in August 2024, 49% of Brazilian consumers actively seek beverages with functional or nutritional benefits. However, this growing health awareness also leads consumers to closely examine ingredient lists for artificial additives, preservatives, and synthetic flavorings. This trend places pressure on manufacturers to adopt clean-label formulations, which can increase production costs and limit options for extending shelf life. Additionally, the Brazilian Health Regulatory Agency's (ANVISA) proposed warning label for non-sugar sweeteners highlights regulatory concerns regarding artificial additives. Such labeling could reduce consumer willingness to purchase RTD coffee products sweetened with aspartame, sucralose, or acesulfame potassium (acesulfame-K). As a result, brands may need to invest in more expensive natural sweeteners, such as stevia or monk fruit, to avoid the negative perception associated with these labels.

High sugar content in many RTD coffees clashing with health‑and‑wellness trends

Mass-market ready-to-drink (RTD) coffee products typically contain 20-30 grams of added sugar per 300ml serving to mask bitterness and provide a dessert-like sweetness. This sugar content exceeds the threshold set by the Brazilian Health Regulatory Agency (ANVISA) of 7.5 grams per 100ml, requiring front-of-pack warning labels that indicate "high in sugar" to consumers. Research conducted by Kerry Group in August 2024 found that 54% of Brazilian consumers would increase their beverage consumption if products contained less sugar and more natural ingredients. This highlights that high-sugar RTD coffee formulations are not aligned with consumer preferences and may risk losing market share as low-sugar alternatives become more prevalent. While coffee consumption reduces sugar-sweetened beverage intake by 47-57 milliliters per day among Brazilian adults, this substitution effect is negated if RTD coffee contains sugar levels similar to the soft drinks it replaces, undermining its positioning as a healthier alternative.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cold Brew Captures Premium Positioning

Cold brew coffee is expected to grow at a compound annual growth rate (CAGR) of 11.37% from 2026 to 2031, outpacing the growth of iced coffee and other ready-to-drink (RTD) coffee segments. This growth is driven by its smoother and less-acidic profile, which resonates with consumers seeking premium coffee experiences without the bitterness typically associated with traditional espresso-based beverages. In 2025, iced coffee held 52.98% of the market share, supported by mass-market offerings from companies such as Nestlé, Coca-Cola, and PepsiCo. These products emphasize affordability and extensive distribution rather than artisanal production methods.

Dark Angel Cold Brew launched Brazil's first nationally available organic cold brew in a 200ml format, utilizing a 20-hour infusion process. Priced at BRL 14.90, the product targets health-conscious consumers willing to pay a 30-40% premium over standard iced coffee. Similarly, Café Constantino's 269ml cold brew, also priced at BRL 14.90, highlights the use of 100% Arabica beans. This reflects a growing trend where origin transparency and quality are becoming essential factors for differentiation within the cold brew segment.

By Packaging Type: Metal Cans Gain Momentum

Metal cans are projected to grow at a compound annual growth rate (CAGR) of 11.42% from 2026 to 2031, representing the fastest growth rate among all packaging type segments. This growth is driven by their sustainability credentials, portability, and compatibility with energy drink aesthetics, which appeal to younger consumers. PET (Polyethylene Terephthalate) bottles held a 34.84% market share in 2025, supported by lower unit costs, transparency that highlights product color, and an extensive recycling infrastructure. For instance, Brazil's PET post-consumer recycled (PET-PCR) recycling rate stands at 56.4%, one of the highest globally. CANPACK partnered with São Geraldo to supply 350ml aluminum cans for ready-to-drink (RTD) coffee, indicating that packaging suppliers are investing in dedicated capacity to meet the increasing demand for metal cans. Aluminum cans offer 100% recyclability, rapid chilling, and on-the-go convenience. However, input costs increased by 18 to 30 percent over the 24-month period ending in 2024, compressing margins and prompting brands to assess whether premium pricing can offset higher packaging expenses.

Glass bottles occupy a premium niche, often associated with artisanal quality and café-style presentation. However, their weight, fragility, and higher logistics costs limit their adoption to specialty retail channels and direct-to-consumer sales. Aseptic packages, such as Tetra Pak cartons, pouches, and other laminated formats, enable ambient shelf-stable ready-to-drink (RTD) coffee, eliminating the need for cold-chain logistics. Despite this advantage, consumer perception often associates ambient RTD coffee with inferior taste, creating a trade-off between cost efficiency and brand positioning.

By Distribution Channel: E-commerce Accelerates Off-Trade Dominance

Off-trade channels represented 69.78% of the market share in 2025 and are expected to grow at a compound annual growth rate (CAGR) of 10.87% from 2026 to 2031. This growth is attributed to factors such as the increasing penetration of e-commerce, the expansion of convenience stores, and promotional activities in supermarkets that boost the visibility and trial of ready-to-drink (RTD) coffee. In Brazil, coffee e-commerce is projected to grow from USD 136.5 million in 2025 to USD 337.9 million by 2029, at a CAGR of 25.4%. However, e-commerce currently accounts for only 0.6% of total coffee retail, indicating significant room for growth in the online channel.

Mercado Livre generated USD 830 million in grocery gross merchandise value (GMV) in 2024, making it Brazil's leading e-commerce platform for packaged food and beverages. This positions the platform as a key discovery channel for RTD coffee brands looking to bypass traditional retail gatekeepers. Furthermore, Ambev's BEES business-to-business (B2B) marketplace and Ze Delivery direct-to-consumer service are expanding their third-party product offerings, including non-alcoholic RTD beverages. These platforms utilize Ambev's logistics infrastructure and customer relationships to strengthen the beverage ecosystem, enabling the distribution of RTD coffee to bars, restaurants, and small retailers.

Geography Analysis

The ready-to-drink coffee market in Brazil is primarily concentrated in the Southeast region, which includes São Paulo, Rio de Janeiro, Minas Gerais, and Espírito Santo. This region accounts for 60% of the national population, has a per capita income above the national average, and boasts a strong coffee culture deeply ingrained in daily routines. Nestlé has committed to a BRL 1 billion investment through 2026, focusing on single-serve RTD coffee and out-of-home vending machines in metropolitan areas. This initiative targets consumers under 24 years old who prioritize convenience and are open to exploring new coffee formats. In São Paulo, cafés report that iced coffee contributes to 12% of total café sales, with consumers under 30 years old forming the largest purchasing group. This underscores the Southeast region as the center of cold coffee adoption, a trend expected to persist through 2030.

The Northeast region, which includes Bahia, Pernambuco, Ceará, and Maranhão, represents a growing opportunity due to rising disposable incomes, increasing urbanization, and a young demographic that aligns with RTD coffee's target audience. However, the lack of cold-chain infrastructure in this region results in higher logistics costs and spoilage risks. These challenges make ambient shelf-stable RTD coffee formats, which use ultra-high temperature (UHT) processing and aseptic packaging, more favorable compared to refrigerated polyethylene terephthalate (PET) bottles and metal cans.

The North and Central-West regions remain less developed markets due to sparse population density, lower per capita income, and limited cold-chain infrastructure. Despite these challenges, these regions hold long-term growth potential as urbanization accelerates and modern retail formats expand. Brazil's transport and logistics infrastructure requires investment equivalent to 2.26% of gross domestic product (GDP) to meet demand. However, current spending is only 0.39% of GDP, resulting in a 1.87 percentage-point shortfall. This gap disproportionately affects interior regions and provides a competitive advantage for ambient shelf-stable RTD coffee, which can bypass cold-chain limitations.

Regulatory Landscape

Brazil RTD coffee operates under dual oversight: ANVISA governs sanitary, safety, and labeling requirements for packaged foods and beverages, while MAPA sets identity and quality rules for beverages and manages product registration. Nutritional labeling requirements under ANVISA RDC 429/2020 (and related implementation rules) shape pack design and reformulation decisions, particularly for sugar and ingredient declarations that drive front-of-pack communication.

Manufacturers also need to meet process and documentation requirements tied to MAPA registration through the SIPEAGRO system, which centralizes product registration for wines and beverages. In 2025, ANVISA issued IN 344/2025 to streamline evaluation of food-related petitions by accepting documentation from equivalent foreign authorities, while updated rules for food-contact cellulosic materials (RDC 979/2025) increased the importance of packaging compliance alongside beverage formulation and claims management.

Value Chain Analysis

The Brazil RTD coffee value chain starts with green coffee sourcing via producers, cooperatives, and trader networks concentrated in traditional origins such as Sul de Minas, Parana, and Bahia, then moves into roasting and extraction. RTD manufacturing adds beverage-specific steps, including coffee extraction, blending with dairy or alternatives, sweeteners and flavors, and stabilization, followed by packaging in PET, cans, glass, or aseptic formats. Integration of roasting, extraction, and aseptic filling within specialized beverage facilities is a key efficiency lever for lead-time control and consistency.

Downstream, cold-chain and merchandising execution are central, since chilled single-serve formats depend on refrigerated transport and in-store refrigeration, which tends to favor modern trade and high-traffic locations such as fuel-station convenience and convenience-store networks. Industry bodies and councils such as ABIC (quality and purity references for coffee products) and Cecafe (export ecosystem coordination, including sustainability programs such as Programa Trabalho Sustentavel with MTE) act as enabling nodes for standards alignment and supply credibility, while dairy ingredient procurement and refrigeration constraints remain recurring bottlenecks outside the main urban corridors.

Competitive Landscape

The Brazil ready-to-drink coffee market shows moderate consolidation, with significant investments from major companies. Nestlé's investment of BRL 1 billion through 2026, Coca-Cola's commitment of BRL 7 billion by 2025, and PepsiCo's expenditure of BRL 1.2 billion in 2023 highlight the efforts of large-scale players to establish dedicated RTD coffee production lines, expand distribution networks, and implement marketing campaigns. These initiatives create challenges for smaller competitors to enter the market.

JDE Peet's acquisition of Maratá's coffee and tea business in January 2024 reflects a consolidation strategy where global coffee companies acquire local brands with established distribution networks. This approach accelerates market entry and reduces the time and cost required to build brand equity organically. On the other hand, Starbucks Brazil's closure of over 30 stores and exit from six cities during 2024 to 2025 demonstrates that brand equity alone cannot overcome operational inefficiencies or high retail rental costs. However, Starbucks continues to sustain revenue through RTD product distribution via Drogal pharmacy chains and supermarkets, even as its physical store presence decreases.

There are opportunities in functional RTD coffee formulations that include protein, adaptogens, nootropics, and prebiotics, catering to consumer demand for morning alertness and afternoon productivity. Additionally, low-sugar and organic RTD coffee segments align with the Brazilian Health Regulatory Agency's (ANVISA) front-of-pack labeling regulations and growing consumer health awareness. Ambev's BEES business-to-business (B2B) marketplace and Ze Delivery direct-to-consumer service provide digital distribution channels that lower entry barriers for emerging RTD coffee brands. These platforms enable smaller brands to reach bars, restaurants, and small retailers without relying on traditional distributor relationships.

Brazil Ready-to-Drink (RTD) Coffee Industry Leaders

Nestlé S.A.

The Coca-Cola Company

Starbucks Corporation

PepsiCo Inc.

WOW! Nutrition

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One near-term opportunity is developing RTD coffee propositions that match tightening transparency and compliance expectations across the coffee supply chain. In February 2026, CONAB launched the Plataforma Parque Cafeeiro to map coffee-growing areas and support traceability and zero-deforestation verification tied to EU environmental rules. The initiative creates a clearer data backbone that brands can use for origin storytelling and compliant sourcing in branded RTD coffee, particularly for premium and organic positioning.

Distribution and format whitespace remain visible in Brazil outside the strongest refrigerated corridors, which keeps shelf-stable RTD coffee (aseptic/UHT) and hybrid routes (online retail and B2B platforms) relevant for scaling assortment. Evidence of industrial capacity focus also supports the broader productization of coffee into ready-to-consume formats: Nestle cited activity around its Araras industrial plant in Sao Paulo state in 2026, reinforcing the role of large, integrated coffee processing hubs that can feed RTD innovation pipelines, including flavor, functional, and reduced-sugar reformulations, while supporting wider availability across off-trade channels.

Recent Industry Developments

- April 2026: Nestle Brasil highlighted a 2026 plan built around higher soluble coffee shipments, with the Araras industrial plant in Sao Paulo state positioned as a key production hub. While framed around soluble formats, the move strengthens upstream processing and industrial scale that can support ready-to-consume coffee product portfolios and broaden availability across Brazilian retail.

- December 2025: Oxxo (FEMSA) introduced the Andatti coffee brand across its Brazil network of 564 stores after expanding by 184 locations over the prior year. This increased dedicated shelf and cooler presence for grab-and-go coffee beverages in convenience retail, improving trial and repeat purchase dynamics in urban corridors.

- April 2024: Nestle launched Nescafe RTD coffee in Brazil in latte, cappuccino, and mocha variants featuring chocolate and caramel notes. The rollout anchored RTD coffee as an accessible premium single-serve option and aligned with the companys investment focus on metropolitan distribution and out-of-home points of sale.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers ready-to-drink coffee products that are pre-brewed, packaged, and sold in Brazil for immediate consumption, typically in single-serve formats such as cans and bottles, across retail and online channels.

Scope exclusions: It does not include dry coffee (beans, ground, pods) or coffee served and prepared on-site in cafes and foodservice.

Segmentation Overview

- By Type

- Cold Brew Coffee

- Iced Coffee

- Other RTD Coffee

- By Packaging Type

- PET Bottles

- Glass Bottles

- Metal Can

- Aseptic packages (tetra pak, cartons, pouches)

- Others

- By Distribution Channel

- On-Trade

- Off-Trade

- Supermarket/Hypermarket

- Convenience Stores

- Specialty Stores

- Online Retail

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to keep the definitions aligned with how packaged beverages are tracked in Brazil. We leaned on public statistics and reference sources such as Brazil government economic and inflation series for price normalization, trade and customs statistics for coffee-derived inputs, and food and beverage labeling rules published by regulators to understand what gets sold as a packaged RTD coffee.

To avoid building assumptions in a vacuum, we reviewed company filings and investor presentations for beverage portfolios, association websites, and reputable press coverage on RTD launches and packaging shifts. We also looked at peer-reviewed papers that discuss chilled beverage consumption and reformulation trends to corroborate category-level behavior. Where needed, paid subscriptions were used only for company financials and intelligence, along with general news and financials screening and patent databases to spot product and packaging innovation signals. These are illustrative examples, and additional public sources were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating what is actually counted as RTD coffee in Brazil, and on stress-testing the key inputs that drive value such as channel mix, pack sizes, and price tiers. We spoke with a mix of brand-side and distribution-side respondents, including retail and specialty channel perspectives, so the desk inputs could be corrected where the market behaves differently across major states and income cohorts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | |

| Mid tier: 47% | Functional/Unit leaders: 34% | |

| Smaller Players: 15% | Managers: 51% |

Market-Sizing & Forecasting

The sizing model starts from a top-down reconstruction of Brazil RTD coffee demand by linking packaged beverage consumption signals to distribution-channel sales dynamics, and then converting that demand pool into value using observed price bands. Once that core view is built, selective bottom-up checks are run using sampled pack-level price points across key channels and a supplier and brand roll-up for the most visible SKUs. Those checks are used to adjust any over or under counts.

Inputs that matter in this market include single-serve pack mix (can versus bottle), average pack size, cold-chain availability and shelf placement for chilled RTD, the split between supermarkets and specialty stores, and price moves tied to inflation and promotional intensity. We also track how product type mix changes, for example cold brew versus other RTD coffee styles, because the price ladder and velocity can differ by format.

Forecasts are built using scenario analysis supported by simple time-series smoothing on the base demand indicators, and then moderated using what interviewees expect on distribution expansion, innovation cadence, and pricing behavior. Where bottom-up visibility is weak for smaller regional labels, gaps are handled by applying channel-level velocity ranges to the estimated shelf presence and then rechecking totals against the overall demand pool.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple independent checks, including channel mix sanity tests, price progression review, and year-over-year growth reasonableness versus known category shifts. When a line item looks off, the underlying assumption is reopened, and follow-up calls are triggered to confirm whether it is a real shift or a data artifact.

Before sign-off, the model is reviewed in steps, first at the input level and then at the full-market level, so that definitions and math stay aligned. The report is refreshed annually, with interim updates when material changes occur in regulation, packaging, or distribution. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Brazil Ready to Drink Rtd Coffee Market Sizing Compared With Other Published Estimates

Published market sizes for Brazil RTD coffee can look far apart because the counted product set is not always the same, and because pricing and channel assumptions are applied differently. Differences also show up when one publisher anchors on retail value while another mixes in broader ready-to-drink coffee adjacencies.

The main gap comes from whether wider coffee-flavored ready-to-drink beverages are folded into the total, and in Mordor Intelligence's model, only packaged, ready-to-consume RTD coffee sold in single-serve containers through defined retail and online channels is counted. In that approach, prices are normalized to the stated year before forecasting forward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.44 M (2025) | |

| Industry Publisher A | USD 513.16 M (2025) | This estimate appears to use a much broader inclusion set and likely captures adjacent ready-to-drink coffee beverages beyond the narrow single-serve RTD coffee definition, which can inflate the value base even if channel coverage looks similar. |

| Market Publisher B | USD 1.40 B (2023) | The much larger figure is consistent with a wider scope and earlier base year, where retail value may include additional end-user or beverage categories and may apply different price ladders or currency timing that are not aligned to a like-for-like RTD coffee only count. |

The spread is mostly explained by scope and the price base year rather than by a true disagreement on trend direction. By keeping inputs tied to observable pack formats, channel mix, and year-specific pricing, the resulting number stays easier to replicate and to update when new launches or channel shifts occur.

Key Questions Answered in the Report

How large is the Brazil ready to drink coffee market in 2026?

The Brazil ready to drink coffee market size is USD 7.1 million in 2026 and is forecast to reach USD 11.54 million by 2031.

Which type is growing fastest within this beverage segment?

Cold brew coffee is set to expand at an 11.37% CAGR between 2026 and 2031, outpacing iced coffee and other ready to drink formats.

What share do off-trade channels hold?

Off-trade channels capture 69.78% of 2025 value and are projected to grow at 10.87% CAGR on rising e-commerce and convenience-store sales.

Why are metal cans gaining traction?

Metal cans combine full recyclability, rapid chilling, and an energy-drink aesthetic, driving an 11.42% CAGR through 2031.

Page last updated on: