Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

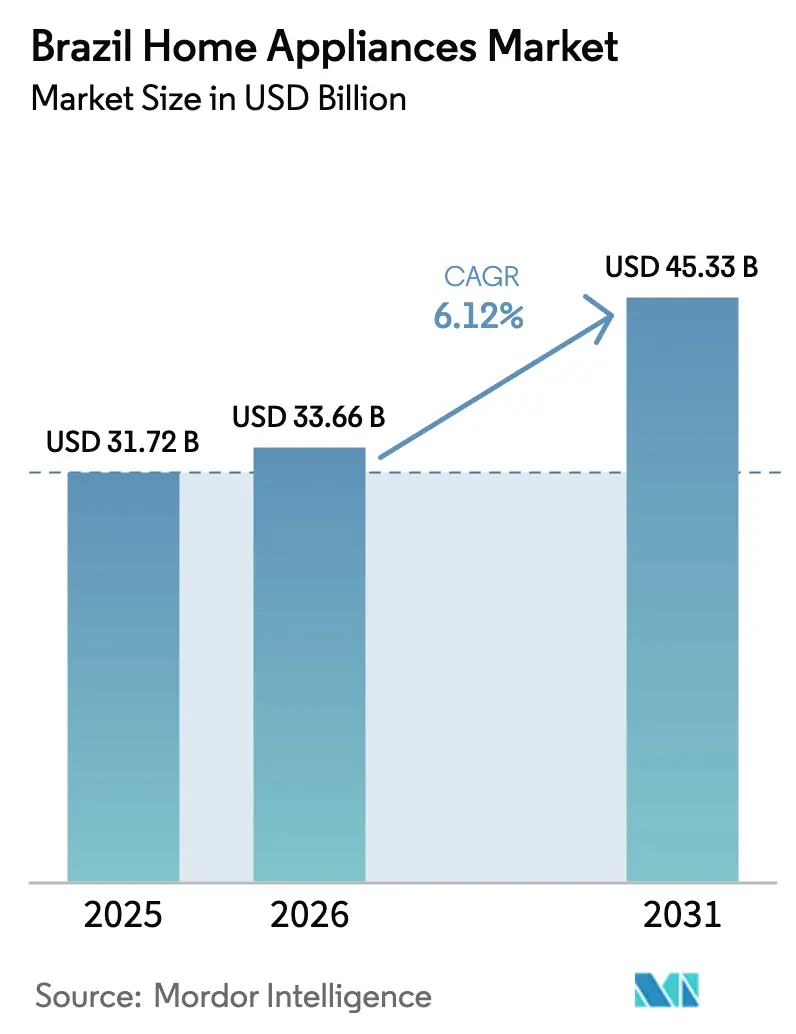

| Market Size (2026) | USD 33.66 Billion |

| Market Size (2031) | USD 45.33 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Home Appliances Market Analysis by Mordor Intelligence

The Brazil Home Appliances Market size is estimated at USD 33.66 billion in 2026, and is expected to reach USD 45.33 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

This momentum stems from resilient household consumption, a 29% expansion in the consumer‐electronics sector that moved 117.7 million units in 2024 [1]Agência Brasil, “Indústria de eletrônica de consumo no Brasil cresceu 29% em 2024,” agenciabrasil.ebc.com.br, and persistent upgrades to energy-efficient models. Pent-up replacement demand following the pandemic, record temperatures that lifted air-conditioner production to 5.9 million units, and widening broadband coverage that enables smart-appliance adoption collectively reinforce the Brazil home appliances market. Rising middle-class incomes, particularly in the Northeast, boost premium purchases even as value brands expand their foothold through localized plants. Meanwhile, credit innovations such as BNPL and PIX settlements soften the impact of elevated benchmark rates on durable-goods financing, keeping the Brazil home appliances market on an upward path. Intensifying competition from Chinese entrants that are shifting from OEM to their own brands continues to pressure incumbent pricing, yet it also accelerates technology diffusion and manufacturing automation in domestic facilities.

Key Report Takeaways

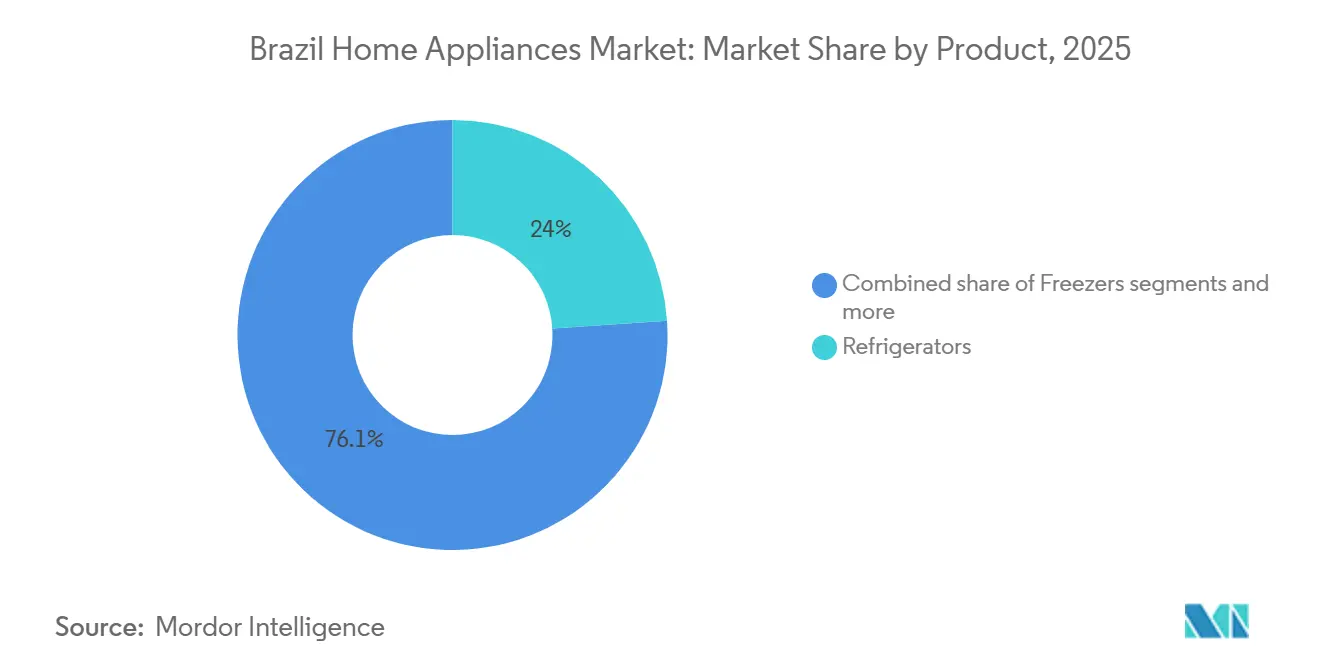

- By product, refrigerators accounted for 23.95% of Brazil home appliances market share in 2025, whereas coffee makers posted the fastest 6.58% CAGR that will shape growth through 2031.

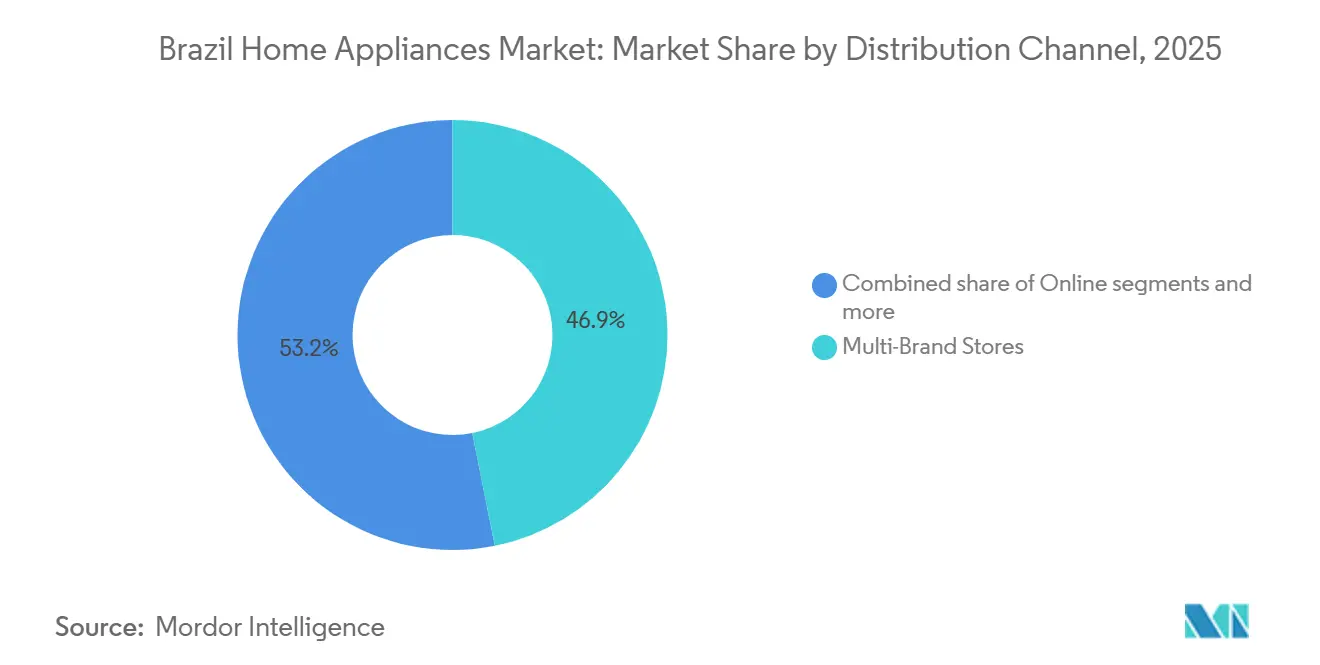

- By distribution channel, multi-brand stores held 46.85% revenue share in 2025, while online platforms are expanding at a 7.62% CAGR and will keep eroding brick-and-mortar dominance.

- By geography, the Southeast region claimed 52.05% of Brazil home appliances market size in 2025, yet the Northeast is forecast to advance at a 6.34% CAGR between 2026 and 2031 thanks to above-average GDP growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class disposable income | +1.8% | National, strongest in Northeast and Center-West | Medium term (2-4 years) |

| Expansion of BNPL & retail-credit facilities | +1.2% | National, with urban concentration | Short term (≤ 2 years) |

| Government energy-efficiency incentives (PROCEL) | +0.9% | National, utility-dependent regions | Long term (≥ 4 years) |

| Rapid adoption of smart-connected appliances (IoT) | +1.1% | Southeast and South regions initially | Medium term (2-4 years) |

| Growing penetration of Chinese value brands | +0.7% | National, price-sensitive segments | Short term (≤ 2 years) |

| Climate-driven demand spikes for cooling products | +0.8% | National, acute in North and Northeast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Disposable Income

Robust wage gains in services and manufacturing lifted household purchasing power, especially in Paraíba and Rio Grande do Norte, where 2024 GDP growth of 6.60% and 6.10% respectively, surpassed the national average [2]Superintendência do Desenvolvimento do Nordeste, “Estados do Nordeste registram maiores taxas de crescimento do PIB em 2024,” sudene.gov.br.. More income means families can replace legacy refrigerators or washing machines with larger-capacity, inverter-motor models that promise lower utility bills. Retailers report higher attach rates for extended warranties and premium finishes, underscoring willingness to pay for quality. Local employment in appliance logistics and after-sales services has expanded, further catalyzing consumption through multiplier effects. Younger consumers, notably Generation Z, now sway 60% of purchase decisions and gravitate toward voice-enabled or app-controlled products that align with connected lifestyles. This demographic preference supports the Brazil home appliances market by sustaining demand cycles that center on both functionality and status signaling.

Expansion of BNPL and Retail-Credit Facilities

Buy-now-pay-later schemes allow households to stretch payments over 24 to 60 installments, sidestepping steep credit-card rates that climbed near 30% in early 2025 [3]O Tempo Economia, “Faturamento de pequenas empresas cresce no Sudeste,” otempo.com.br. . Retailers such as Casas Bahia leverage proprietary scorecards to pre-approve shoppers, driving higher ticket sizes and lower cart abandonment. Fintech providers embed PIX instant payments into BNPL checkouts, cutting settlement costs and shortening confirmation times to seconds. Manufacturers co-finance interest-free periods that soften rate shocks, an approach evidenced by LG’s offers of 12 monthly installments at zero interest. This credit democratization widens the sales funnel for midrange and premium products, thereby fortifying the Brazil home appliances market against macroeconomic volatility. Nonetheless, portfolio risk must be monitored because delinquency upticks would raise provisioning costs and temper promotional pricing.

Government Energy-Efficiency Incentives (PROCEL)

Brazil’s PROCEL label compels appliance makers to hit stringent kWh consumption benchmarks, nudging consumers toward A-rated models that promise lower electricity bills. Utilities must earmark 0.5% of revenue for efficiency subsidies, enabling swap-out campaigns that replace outdated units with certified products and thus enlarge the addressable base. The mechanism also accelerates manufacturer R&D as higher ratings translate into shelf-space priority at retailers. Annual maintenance audits by Inmetro keep compliance high and weed out subpar imports, indirectly safeguarding domestic assembly plants that meet local standards. Over time, these measures heighten entry barriers for fringe brands and anchor the Brazil home appliances market to a sustainability narrative that resonates with environmentally conscious buyers. They also shield households from energy-price spikes, reinforcing replacement incentives during heat waves that elevate cooling loads.

Climate-Driven Demand Spikes for Cooling Products

Record heat pushed air-conditioner production up 83% year on year to 3.28 million units through July 2024 [4]Letícia Lopes, “Produção de ar-condicionado bate recorde e salta 83% no ano,” oglobo.globo.com. . Window units rose 88% while split systems climbed 54%, collectively making Brazil the world’s second-largest AC maker behind China. Penetration remains only 22% of households, leaving vast headroom as meteorologists forecast more frequent heatwaves. Manufacturers operate at near-capacity, yet 20% idle slack persists, enabling rapid scale-up when temperatures soar. Price increases of 14.60% for ACs in 2024 barely dented demand, signaling inelasticity for climate-control products. These dynamics reinforce the Brazil home appliances market outlook by ensuring sustained growth even when broader discretionary spending cools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest-rate sensitivity of durable sales | -2.1% | National, acute in credit-dependent segments | Short term (≤ 2 years) |

| Exchange-rate volatility inflating import costs | -1.3% | National, import-heavy categories | Medium term (2-4 years) |

| Persistent grey-market & counterfeit inflows | -1.0% | National, pronounced in urban informal retail channels | Medium term (2–4 years) |

| Logistics bottlenecks in North & Northeast regions | -0.8% | Regional (North & Northeast Brazil) | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Sensitivity of Durable Sales

Selic-linked consumer loans climbed toward 30% in early 2025, prompting a 6.40% year-over-year decline in February furniture and appliance sales. Brazilian households typically finance high-ticket appliances over 10 or more installments, so the cost of capital directly curtails demand. Even promotional plans with interest-free periods transfer carrying costs to retailers that must absorb higher working-capital charges. Credit rationing disproportionately impacts middle-income buyers who exceed thresholds for subsidized programs yet lack liquidity for cash purchases. Manufacturers respond with temporary rebates and bundle deals, but these tactics compress margins and have finite budgets. Until monetary policy eases, the Brazil home appliances market will face periodic dips that offset other growth drivers.

Exchange-Rate Volatility Inflating Import Costs

Brazil imports most of its compressors, electronic boards, and premium washer-dryer units, leaving profit sensitive to dollar swings. Tariff hikes on selected Chinese goods in October 2024, plus a 20% duty on foreign parcels under USD 50, raised landed costs. LG still sources 90% of washing machines from Asia, although its Paraná plant will localize production by 2026. Raw-material price pass-through often trails currency moves, so margin squeezes linger for several quarters. Retailers hedge with forward contracts but cannot fully offset volatility, leading to abrupt shelf-price adjustments that unsettle consumer budgets. This friction tempers the Brazil home appliances market trajectory, especially for import-intensive small appliances where domestic substitutes remain scarce.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Essential Majors Support, While Small Appliances Accelerate Upsell

Refrigerators captured 23.95% of Brazil home appliances market share in 2025, underpinning baseline demand that stabilizes factory utilization even during credit contractions. Cooler penetration is effectively universal, yet upgrades to inverter compressors and French-door formats sustain replacement cycles and expand average selling prices. Washing machines leverage urban densification trends, while AC units benefit from climate change as the split-system market size surged 54.36% in 2024. Large appliances also anchor service revenues because installation and maintenance create annuity streams for retailers and third-party technicians. Small appliances represent the innovation frontier, with air fryers, blenders, and electric kettles benefiting from health and convenience narratives. Coffee makers, supported by Brazil’s deep coffee culture, register a 6.58% CAGR through 2031 and exemplify premiumization as consumers trade up to capsule systems with app connectivity.

Profitable cross-selling emerges when retailers bundle major and small appliances, such as offering a discounted air fryer with a new refrigerator purchase, lifting basket value and customer retention. Chinese entrants intensify price competition in majors, but local incumbents counterbalance by marketing superior after-sales networks and energy efficiency credentials. Domestic sourcing of metal cabinets and plastic components has improved, cushioning forex shocks for majors, while small appliances still rely heavily on imported motors and heating elements. Sub-category specialization grows: pet-hair-removing washing-machine cycles, barista-grade espresso makers, and allergen-filtering vacuum cleaners meet niche lifestyle demands.

By Distribution Channel: Store Networks Remain Pillars While Online Accelerates Reach

Multi-brand stores retained 46.85% revenue share in 2025, reflecting consumer trust in face-to-face demos and the immediate gratification of taking products home the same day. Sales associates provide financing guidance and coordinate installation appointments, services that pure-play e-commerce struggles to replicate. Even so, rapid mobile adoption propels online sales at a 7.62% CAGR as checkout via PIX simplifies transactions, and nationwide delivery lead times shrink. E-tailers leverage algorithmic pricing and affiliate influencers to unlock opportunities in interior cities underserved by large chains, thereby broadening the Brazil home appliances market. Omnichannel models emerge, where physical stores double as micro-fulfillment hubs, cutting last-mile costs and supporting same-day pickup. Exclusive brand outlets cater to premium segments, letting manufacturers showcase AI features in experiential settings that validate price premiums.

The interplay between channels drives continual SKU rationalization. Online analytics surface long-tail demand that brick-and-mortar would overlook, prompting brands to launch web-only color variants or bundle offers. Conversely, in-store shoppers often test products and then finalize purchases online to exploit flash promotions, illustrating showrooming behavior. Retailers deploy loyalty apps that integrate purchase histories to present targeted installment plans, boosting conversion rates. Logistics partnerships with regional carriers offset Brazil’s vast geography, and locker pickup points grow in condo complexes, lowering missed-delivery incidences. These channel synergies enhance customer experience and lift the Brazil home appliances market size by capturing latent demand among digitally savvy households.

Geography Analysis

Southeast Brazil generated the bulk of the 2025 value, amounting to 52.05% of Brazil home appliances market size, thanks to dense urbanization, mature retail ecosystems, and per-capita incomes that exceed the national mean. São Paulo alone accounts for nearly one-third of national e-commerce consumption, serving as the logistical nerve center where seven in ten online orders originate. This concentration enables rapid product launches because distributors maintain high inventory turnover and efficient reverse logistics for returns. Minas Gerais and Rio de Janeiro augment demand through growing middle-class suburbs and tourism-driven hospitality upgrades, reinforcing steady replacement cycles for large appliances.

The Northeast is emerging as the standout growth engine, with regional GDP rising 3.80% in 2024 compared to the national 3.50%. Federal development banks provide tax incentives and subsidized credit that entice manufacturers to set up assembly plants, reducing freight costs and aligning product lines with local taste preferences. Sweltering summers accelerate air-conditioner penetration, and rising disposable income elevates aspirations toward premium small appliances such as capsule coffee makers. Retailers expand store footprints in secondary cities like Campina Grande and Petrolina, creating localized service hubs that secure customer loyalty. This virtuous circle sustains a 6.34% CAGR for the region, narrowing the gap with the historically dominant Southeast and enlarging Brazil home appliances market coverage.

The South benefits from established manufacturing in Santa Catarina, where Whirlpool modernized facilities with R$550 million (USD 110 million) in 2024, reinforcing production for domestic and Mercosur export demand. High human‐development indices support the uptake of connected appliances, while cooler winters drive purchases of dryers and heaters that complement national cooling demand. The Center-West rides agribusiness wealth yet faces scattered population centers, limiting big-box retail density, though e-commerce mitigates reach constraints. The North grapples with logistics bottlenecks due to low paved-road ratios and seasonal river transport disruptions, raising last-mile costs by up to 50% during droughts. Even so, climate extremes spur cooling product purchases, and targeted utility subsidies help low-income households upgrade old refrigerators.

Competitive Landscape

The top five suppliers dominated the majority of 2024 sales, reflecting a moderately concentrated market where scale advantages in procurement, R&D, and marketing provide strong competitive barriers. Whirlpool holds the leading position through its Brastemp and Consul brands, capitalizing on strong brand recognition, a nationwide service network, and a diverse product portfolio aligned with Brazilian consumer preferences. Its 2024 revenue hit BRL12.9 billion (USD 2.58 billion) after the company invested BRL 550 million (USD 110 million) to automate São Paulo and Santa Catarina lines, trimming production cycle times and elevating tolerance standards. Electrolux capitalizes on Scandinavian design cues and energy-efficiency credentials, while Samsung and LG compete on smart-home integration, riding AI marketing to premium niches.

Chinese brands intensify rivalry by pivoting from OEM supply to own-brand penetration. Midea’s BRL 630 million (USD 126 million) Pouso Alegre plant, inaugurated in December 2024, can churn out 1.3 million units annually and slashes lead-time to retailers to under ten days. TCL and Hisense expand distribution agreements with national chains and deploy aggressive point-of-sale promotions to gain shelf visibility. Pricing skirmishes compress gross margins, prompting incumbents to emphasize after-sales guarantees and compliance with the Selo Procel, which smaller entrants struggle to meet at scale. Component localization strategies accelerate, exemplified by LG’s BRL 1.5 billion (USD 300 million) Paraná factory slated for 2026 that targets washing-machine self-sufficiency and hedges forex exposure.

Innovation remains the chief competitive lever. Samsung secured TÜV Rheinland carbon certifications for around 80 AI TV and monitor models in 2025, underscoring its commitment to environmental stewardship that resonates with affluent consumers. Whirlpool sold its Brastemp water-purifier rental business to Culligan in July 2024, freeing capital to focus on core appliance R&D. Partnerships such as SILL Brasil and Maytag bring commercial-grade laundry equipment to hospitality and healthcare clients, diversifying revenue. As localization advances, supply-chain resiliency improves, but certification audits and energy-efficiency mandates raise compliance costs, favoring firms with robust quality infrastructures. Consequently, rivalry shapes the Brazil home appliances market around dual themes of affordability and intelligence, with sustainable production practices emerging as the next frontier for differentiation.

Brazil Home Appliances Industry Leaders

Whirlpool (Brastemp, Consul)

Electrolux do Brasil

Midea Carrier

Samsung

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Midea inaugurated a BRL 630 million Pouso Alegre factory with 1.3-million-unit annual capacity focused on refrigerators and washing machines.

- November 2024: LG launched its Family Club loyalty program, securing 5,900 initial members.

- September 2024: Samsung unveiled its 2025 AI TV lineup at Brasil Game Show 2024 with a 1,300 m² booth.

- July 2024: Whirlpool finalized the divestiture of its Brastemp water purifier rental business to Culligan to concentrate on core categories.

Brazil Home Appliances Market Report Scope

A home appliance is referred to as a domestic electrical appliance that will assist in household work and ease human efforts. A complete background analysis of the Brazilian home appliances market, which includes an assessment of the industry associations, overall economy, and emerging market trends by segments, significant changes in the market dynamics, and market overview, is covered in the report. The Brazil Home Appliances Market is segmented by Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, and Cookers and Ovens), Small Appliances (Vacuum Cleaners, Small Kitchen Appliances, Hair Clippers, Irons, Toasters, Grills and Roasters, Hair Dryers and other Small Appliances), and by Distribution Channel (Multi-brand Stores, Exclusive Stores, Online, and Other Distribution Channels). The report offers market size and forecasts for the Blinds Market in value (USD million) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region

| Southeast |

| South |

| Northeast |

| North |

| Centre-West |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | Southeast | |

| South | ||

| Northeast | ||

| North | ||

| Centre-West | ||

Key Questions Answered in the Report

How large is the Brazil home appliances market in 2026?

The market stands at USD 33.66 billion in 2026, backed by resilient household spending and climate-induced demand.

What is the expected CAGR for appliances in Brazil till 2031?

Sales are projected to grow at a 6.12% CAGR, lifting the market to USD 45.33 billion by 2031.

Which product segment is expanding fastest?

Coffee makers lead with a 6.58% CAGR through 2031 as consumers upgrade to premium brewing systems.

Which region is showing the highest growth?

The Northeast is projected to rise at a 6.34% CAGR because of rapid GDP gains and rising disposable incomes.

How are high interest rates affecting appliance sales?

Elevated consumer-loan rates near 30% have trimmed monthly volumes, but BNPL options and manufacturer subsidies are cushioning declines.

What competitive moves are shaping the market?

Localization investments like Midea’s new Minas Gerais plant and LG’s planned Paraná facility are intensifying competition while reducing import dependence.

Page last updated on: