Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

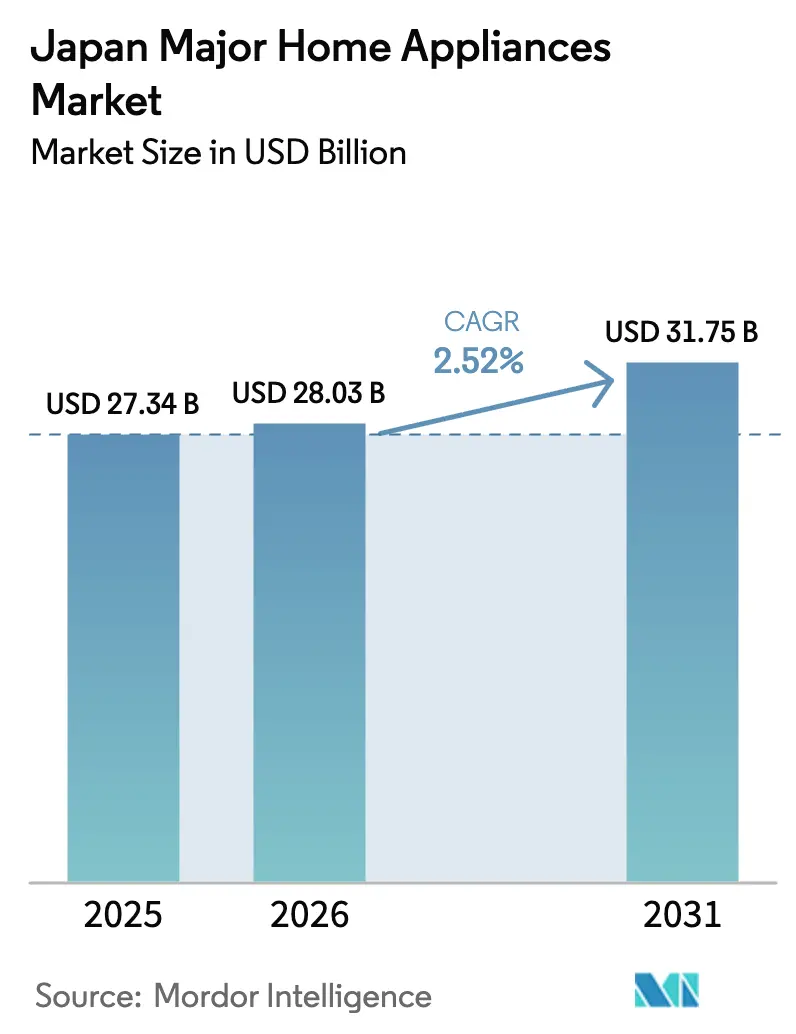

| Base Year Market Size (2025) | USD 27.34 Billion |

| Market Size (2026) | USD 28.03 Billion |

| Market Size (2031) | USD 31.75 Billion |

| Growth Rate (2026 - 2031) | 2.52% CAGR |

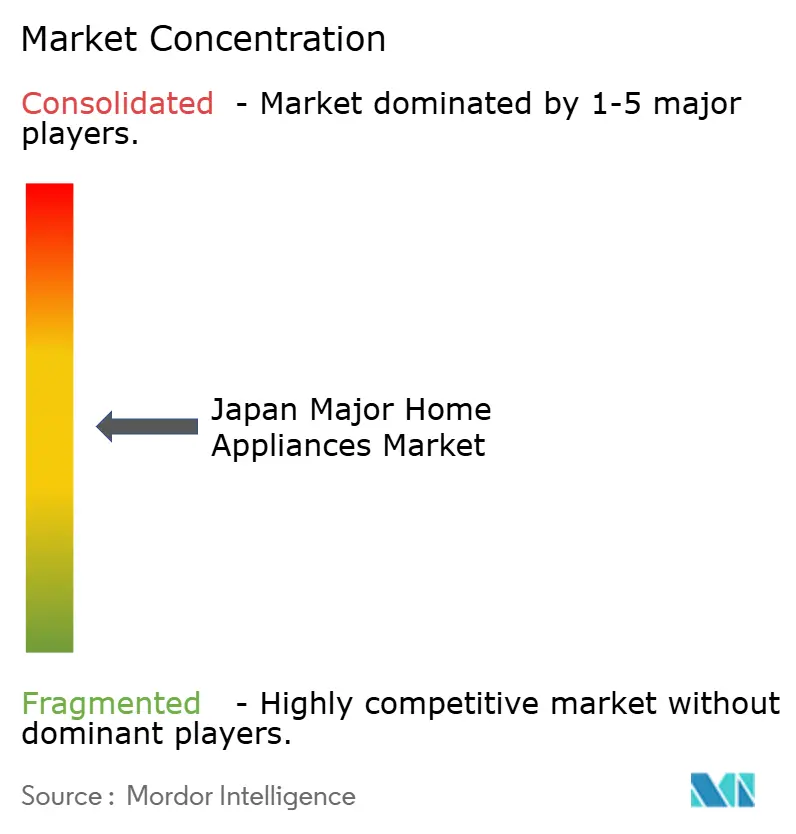

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Major Home Appliances Market Analysis by Mordor Intelligence

The Japan major home appliances market size is expected to grow from USD 27.34 billion in 2025 to USD 28.03 billion in 2026 and is forecast to reach USD 31.75 billion by 2031 at a 2.52% CAGR over 2026-2031. Rising energy-efficiency thresholds and targeted subsidies are steering replacement cycles toward compliant models that balance lower running costs with premium features. Aging demographics and smaller households are shifting product design toward compact, voice-enabled, and easier-to-operate appliances that improve daily routines for seniors and single residents. E-commerce adoption has changed purchasing behavior and delivery expectations, and it has pushed retailers to expand click-and-collect, ship-from-store, and curated online assortments. Smart-grid deployments and time-of-use pricing are creating new value for connected white goods that can flex consumption to off-peak windows. Together, these changes support a steady modernization path for the Japan major home appliances market, even as volumes track the broader demographic trend.

Key Report Takeaways

- By product type, refrigerators led with 27.71% of the Japan major home appliances market share in 2025, while dishwashers are forecast to expand at a 3.35% CAGR to 2031.

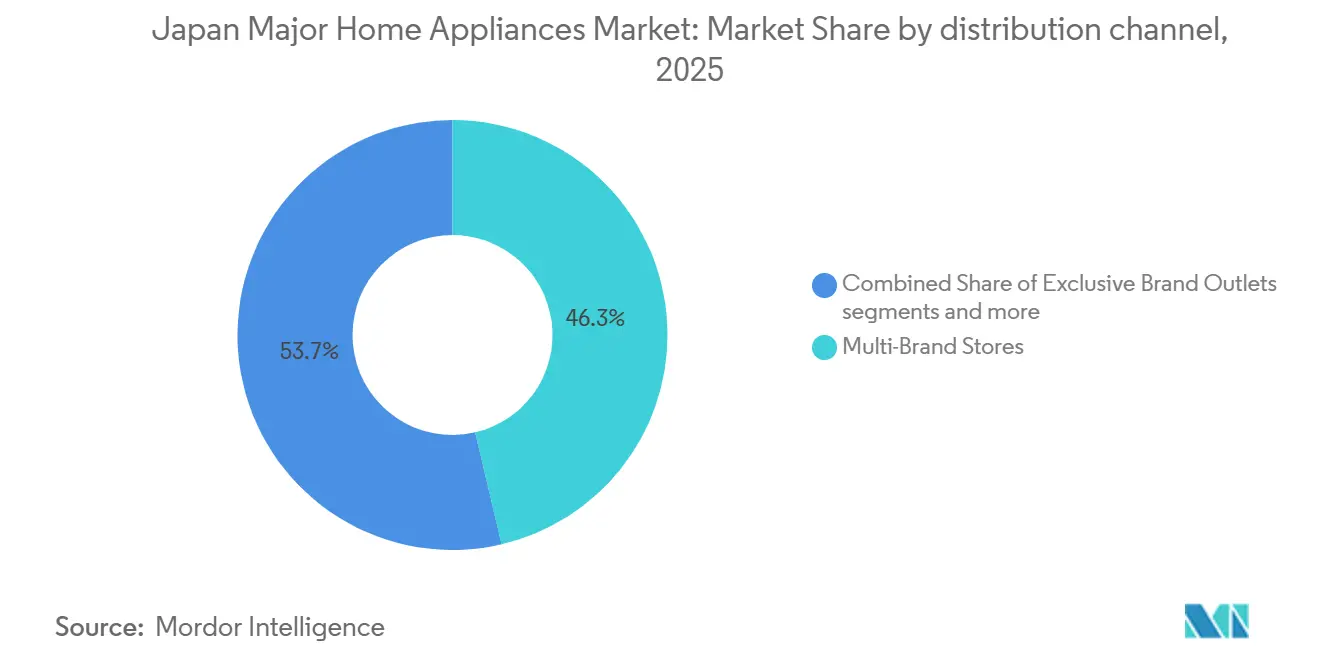

- By distribution channel, multi-brand stores held 46.34% of the Japan major home appliances market value in 2025, while online channels are projected to record the highest growth at a 4.87% CAGR through 2031.

- By geography, the Kanto region held 40.34% of the Japan major home appliances market share in 2025, while the Kansai region is expected to register the fastest growth at a 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inbound tourism and short-term rentals | +0.3% | Kanto, Kansai, and national gateway cities | Short term (≤ 2 years) |

| Top Runner energy standards and subsidies | +0.8% | National, stronger in urban prefectures with higher compliant uptake | Medium term (2-4 years) |

| Urban micro-living and multi-functional demand | +0.4% | Tokyo, Osaka, spill over to Nagoya and Fukuoka | Long term (≥ 4 years) |

| Subscription or rental adoption among millennials | +0.2% | National, early gains in Tokyo, Yokohama, Osaka | Medium term (2-4 years) |

| Smart-grid roll-out for connected white goods | +0.5% | Kanto to Kansai and Chubu expansion | Long term (≥ 4 years) |

| An aging population and the replacement of legacy units | +0.4% | National, pronounced in Tohoku, Hokkaido, rural prefectures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government “Top Runner” Energy-Efficiency Standards and Subsidy Schemes

The Top Runner Programme, Japan's mandatory energy-efficiency cornerstone since 1998, sets targets by benchmarking the most efficient model in each category, then enforcing a weighted-average compliance deadline for manufacturers. The program benchmarks performance to leading models and enforces weighted-average targets, which lifts the baseline for the entire category and keeps replacement cycles tied to compliance milestones. Local subsidies stack on national incentives and can reach JPY 300,000, which lowers the initial cost to consumers and supports faster adoption of efficient models in 2024 and 2025. This approach benefits brands that integrate efficiency enhancements into user-centric features such as better food preservation and quieter operation across constrained floor plans. The emphasis on secure connectivity stands out, with IoT security rules and labeling that favor players with compliance infrastructure and device lifecycle management. These policy frameworks sustain premium positioning for efficient and connected appliances within the Japan major home appliances market, which tightens the link between regulation and product roadmaps[1]International Energy Agency, “Top Runner Programme, Policies,” International Energy Agency, iea.org.

Urban Micro-Living Fueling Demand for Multi-Functional Appliances

Tokyo's micro-apartments, some as compact as 9 square meters, have ballooned as one-room rental rates spiked 29% year-over-year in 2025, prompting cost-conscious residents to trade square footage for location and savings. Over 11% of Tokyo's twenty-somethings now occupy units under 6 tatami mats (~10 sqm), and single-person households exceed 50% city-wide[2]E-Housing, “Tiny Apartments in Tokyo for Foreigners: Rental Costs and Where to Find Them,” E-Housing, e-housing.jp. Space scarcity elevates washer-dryer combos, slim-depth refrigerators, and one-burner induction cooktops from niche to necessity. Design ethos shifts to "form follows storage": appliances must either collapse, fold, or present aesthetically when left visible, aligning with the danshari decluttering philosophy. Japanese brands develop tall, narrow refrigerator formats and low-vibration stackable laundry sets that suit apartment codes and noise expectations. Visual simplicity and decluttering principles guide feature choices, as consumers seek convenience without visual clutter. This shift in living patterns aligns with growth in single-person households, which concentrates demand in smaller capacities and multi-function units that simplify daily tasks. The result is an enduring design and feature focus that benefits multi-functional appliances within the Japan major home appliances market across dense urban prefectures.

Smart-Grid Roll-Out Boosting Demand for Connected White Goods

Smart-meter deployments and time-of-use pricing are giving connected white goods clearer value by enabling off-peak scheduling and demand-response integration. Heat-pump water heaters that shift load to nighttime hours and coordinate with solar PV through app control illustrate how flexible demand can lower household operating costs while smoothing grid load. Appliance ecosystems that align with demand response and energy management platforms set a foundation for new service models and recurring revenue. Panasonic's Eco Cute heat-pump water heater—10 million cumulative units shipped by March 2025[3]Heat Pump & Thermal Storage Technology Center of Japan, “Eco Cute 10 million Units Achievement Commemorative Ceremony,” Heat Pump & Thermal Storage Technology Center of Japan, hptcj.or.jpleverages nighttime electricity to produce hot water, cutting costs and flattening grid load. Digitalization enables demand-response (DR) integration: surplus solar PV can trigger Eco Cute heating cycles via app control, strengthening industrial competitiveness ahead of global roll-out. The Japan major home appliances market benefits when grid programs reward flexible consumption and when manufacturers tie software updates to new energy features. These linkages help accelerate the adoption of connected white goods in regions that can leverage time-of-use tariffs and energy services.

Aging Population Accelerating Replacement of Legacy Appliances

Aging demographics are reshaping user interfaces and product ergonomics so that appliances are easier to operate and maintain. Larger displays, simplified cycles, clear status indicators, and voice assistance reduce friction for users who prefer straightforward operation. Replacement cycles are aligning to features that reduce energy costs without adding complexity, and brands are responding with intelligent modes that optimize cycles based on load, usage patterns, and comfort needs. Connected features that support caregiving and safety use cases, such as remote monitoring and alerts, are gaining attention in categories with high daily touch points. Brands that balance reliability with access-friendly design and smart assistance are well-positioned to serve older households. This shift underpins steady replacement demand in the Japan major home appliances market as more seniors choose to age in place with supportive technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stagnant household formation and slower unit growth | -0.5% | National, sharper in rural prefectures with population outflow | Long term (≥ 4 years) |

| High electricity tariffs and purchase hesitation | -0.4% | Eastern Japan regions, gap versus Western Japan | Medium term (2-4 years) |

| Price volatility in the rare-earth and compressor supply chain | -0.3% | National, higher exposure for China-reliant inputs | Short term (≤ 2 years) |

| Culture of repair and second-hand reuse | -0.3% | National, institutionalized reuse and recycling flows | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stagnant Household Formation Curbing Unit Growth

Japan logged fewer than 670,000 births in 2025, the lowest since record-keeping began a century ago. Slower household formation reduces the number of first-time buyers for large white goods, which constrains organic unit growth. Fewer new households translate into lower demand for appliance bundles tied to new-home moves, so brands pivot to replacement-driven strategies. Housing starts fell 8.5% year-over-year in November 2025, marking the seventh decline of the year and reversing a brief October uptick. New-home appliance bundles, historically tied to household formation, face structural headwinds. The population shrank by 900,000 in 2024[4]Edward Conard, “Japanese Births Set To Fall Below Lowest Official Forecasts In 2025, www.edwardconard.com, and projections see further decay to 100 million by 2050. Premiumization remains a key lever to protect value even as unit volumes face demographic headwinds. This dynamic keeps the Japan major home appliances market concentrated on replacement and feature-led upgrades where households see clear value.

Culture of Repair and Second-Hand Use Limiting New Sales

Japan’s established reuse channels and device refurbishment practices reduce the share of consumers buying new units at the first sign of performance decline. The Home Appliance Recycling Law shapes end-of-life processes for major categories, which helps route products into formal collection and material recovery streams. Manufacturers also expand refurbishment and resale programs that extend the lifecycle of quality units, building circular-economy credentials and serving price-sensitive households. Panasonic’s Factory Refresh approach illustrates how manufacturers can recover units, refurbish them to a high standard, and sell them to new owners. These practices lift sustainability outcomes while moderating demand for brand-new purchases, which affects sell-through in price-sensitive segments. The net effect is a stable but competitive environment where the Japan major home appliances market balances new sales with elevated reuse activity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Anchor Share, Dishwashers Gain From a Low Base

Refrigerators held the highest share in 2025 at 27.71%, which reflects steady replacement cycles and enduring demand for multi-door, large-capacity formats that support infrequent shopping and bulk-purchase habits. Panasonic’s food-preservation feature set, including Prime Fresh cooling that maintains texture while extending shelf life, is a recognized differentiator that supports premium tiers. Sharp’s Plasmacluster ion feature reduces odor and inhibits bacteria in refrigerators and other categories, which strengthens hygiene positioning where health preferences factor into purchase decisions. Smart refrigerators add internal cameras and inventory management features, and while they grow from a lower base, their value proposition improves as app experiences and interoperability mature. Feature upgrades that reduce energy use, improve food quality, and enhance convenience continue to sustain consumer interest in premium formats. These product characteristics reinforce the leadership of refrigerators within the Japan major home appliances market as brands balance efficiency with practical, space-aware designs.

Dishwashers extend the growth profile from a small installed base, with the category set to expand at a 3.35% CAGR to 2031. Built-in formats gain traction in new construction for seamless integration, and compact countertop models support retrofits in existing small kitchens. Hygiene features such as steam-assisted cleaning and self-sanitizing cycles remain points of differentiation as dual-income households trade time savings for convenience. Washing-machine demand is supported by front-load inverter models and washer-dryer combinations that optimize water and energy use while delivering deep-clean efficacy for urban homes. Feature sets like Hitachi’s BeatWash agitation and Panasonic’s ActiveFoam system elevate wash performance with lower resource use, and voice assistance aligns with ease-of-use preferences for aging users. The product mix continues to favor appliances that combine efficient performance with slim profiles suited to micro-living, which supports sustained interest across core categories in the Japan major home appliances market.

By Distribution Channel: Multi-Brand Stores Anchor, Online Sprints Ahead

Multi-brand stores maintained the largest channel position at 46.34% value share in 2025, leveraging broad assortments, on-site service desks, and expert guidance for high-involvement purchases. Store networks across urban and suburban locations anchor click-and-collect and ship-from-store fulfillment models that complement strong traffic during promotional cycles. Retailers expand experiential zones that showcase smart features and energy-saving modes, which help translate specifications into practical benefits for consumers. Repair desks, part availability, and delivery-installation services also reinforce the channel’s value, where older consumers prefer human assistance. These strengths keep multi-brand retail central to discovery and conversion for the Japan major home appliances market despite the ongoing rise of online channels. The result is a hybrid shopper journey that relies on both store experiences and digital tools to complete purchases and schedule service.

Online channels are set to expand at a 4.87% CAGR through 2031 as same-day delivery, transparent pricing, and richer product content improve convenience for shoppers. Kanto residents generate a higher share of online volume than their share of total demand, which indicates that urban-digital behavior continues to lead national patterns. Rising platform compliance requirements around warranties and seller verification also elevate attention to after-sales service and return processes, which benefits scaled platforms and brand stores. The interplay between store networks and online marketplaces continues to evolve around convenience-led features like appointment delivery and installation scheduling. These capabilities underpin a sustained digital shift in the Japan major home appliances market while keeping service execution at the center of channel differentiation.

Geography Analysis

Kanto leads with a 40.34% share in 2025, supported by dense population centers, logistics reach for same-day delivery, and a high concentration of early adopters for connected devices. Online adoption is stronger than the national baseline, and it sustains a high share of e-commerce volume relative to the region’s overall demand. Smart-home adoption trends are more visible in suburban communities around Tokyo, where newer housing stock integrates wiring and space for built-in dishwashers and energy-efficient HVAC. Residential developers promote smart-home bundles as part of value-add packages to attract buyers with enhanced convenience and energy savings. The presence of millions of smart meters enables time-of-use tariffs and off-peak scheduling for laundry and HVAC, which raises the utility of connected white goods in the region. These conditions reinforce Kanto’s role as the anchor region for the Japan major home appliances market and a launchpad for connected use cases that spread nationally.

Kansai is the fastest-growing region at a 4.12% CAGR through 2031, helped by the concentration of leading manufacturers and strong retail infrastructure. The region’s duty-free retail formats and brand showrooms serve international visitors and domestic shoppers looking for premium or design-led appliances. Design influences that combine modern minimalism with traditional aesthetics are visible in product displays and store formats that highlight harmony in living spaces. Local incentives that align with national energy-efficiency programs lead to targeted sales spikes when budgets are allocated to compliant models. The region also benefits from strong service networks and demonstration centers that help explain features to older consumers and first-time buyers of connected appliances. Taken together, these factors reinforce Kansai’s position as a growth engine for the Japan major home appliances market within a balanced national profile.

Chubu holds a small share and concentrates demand around durability, energy efficiency, and practical features that support daily use in mixed residential and commercial settings. Regional manufacturing activity and supplier networks inform a strong preference for reliable products that balance performance and cost. Kyushu and Okinawa combine renewable-integration pilots and smart-living adoption, which reflects a younger demographic and active startup ecosystems in key cities. Hokkaido and Tohoku together represent less than 10% share with specialized cold-climate needs, and they rely on efficient heating technologies and robust service coverage to support adoption. Replacement activity forms a stable base where older consumers value quiet operation, compact footprints, and strong support for delivery and installation. These regional dynamics keep the Japan major home appliances market anchored in distinct local needs while following a common path of efficiency and smart features.

Competitive Landscape

The Japan major home appliances market shows moderate consolidation, with the top five players accounting for slightly greater than half of the revenue, underscoring the strength of national brands and their service reach. Panasonic, Hitachi, Sharp, Mitsubishi Electric, and Toshiba sustain scale through deep product portfolios, strong after-sales coverage, and designs tailored to Japanese living patterns. Panasonic’s heat-pump water heater installed base reached a key shipment milestone by March 2025, and the brand is expanding air-to-water heat-pump manufacturing capacity in Europe to serve rising decarbonization demand. Panasonic’s AI-linked strategy connects appliance hardware to predictive maintenance and adaptive energy modes, and it complements cooking experiences showcased at global events. These approaches reinforce Panasonic’s position across refrigerators, laundry, kitchen appliances, and HVAC within the Japan major home appliances market.

Hitachi emphasizes durable performance and connected features that address the needs of smaller and aging households, including advanced washing technologies and intelligent food management in refrigeration. The company has streamlined its focus on climate segments and prioritized areas where it can differentiate through core technologies and user experience. Sharp builds on AI and IoT capabilities to deliver voice-guided cooking and home assistance, and it continues to develop air-quality and hygiene features that resonate with health-conscious buyers. Mitsubishi Electric and Toshiba compete with reliability-led propositions and steady feature upgrades, with a focus on improved efficiency and integrated control. These brands apply design principles and connectivity standards that simplify household integration and management for non-technical users. Their collective investments in AI, IoT, and energy-saving features support competitive intensity across the Japan major home appliances market.

Daikin’s leading position in air conditioning features refrigerant strategies and control platforms that reduce energy use and improve comfort, supported by ongoing digital transformation recognition by national authorities. The company’s programs at major events, product design awards, and next-generation controllers demonstrate an integrated approach that spans hardware innovation and user experience. Good Design award citations and selection as a DX Stocks recipient reflect the brand’s progress in product design and digital capability building. These differentiators strengthen Daikin’s profile in home and commercial segments with a focus on energy savings, control simplicity, and interoperable solutions. Together, incumbents and specialty players shape a market where regulation, design, and software are key levers for differentiation and loyalty. This competitive posture will continue as brands align with energy programs and connected-home standards that guide the Japan major home appliances market through the forecast period.

Japan Major Home Appliances Industry Leaders

Panasonic Corporation

Sharp Corporation

Toshiba Corporation

Hitachi Global Life Solutions

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bosch Group completed the acquisition of Johnson Controls’ residential and light commercial HVAC business: Robert Bosch GmbH finalized the purchase of Johnson Controls’ residential and light commercial HVAC business, including the Johnson Controls–Hitachi air-conditioning joint venture, in an approximately USD 8 billion deal, significantly expanding Bosch’s global HVAC footprint.

- August 2025: Panasonic started operations at its expanded Czech air-to-water heat-pump factory: Panasonic Heating & Ventilation Air-Conditioning Czech began operations at its expanded Plzeň facility, increasing annual air-to-water heat-pump production capacity from 150,000 to approximately 700,000 units to meet rising European demand.

- April 2025: Toshiba launched its ifLink open IoT platform: Toshiba expanded its smart-home services internationally by launching the ifLink open IoT platform, enabling interoperability across third-party devices and strengthening its smart-living ecosystem.

Japan Major Home Appliances Market Report Scope

Major home appliances are essential household products designed to support daily living through food preservation, cooking, cleaning, and climate control. In Japan, demand for major home appliances is influenced by urban lifestyles, space-efficient housing, high energy-efficiency standards, and growing adoption of smart and connected technologies. The Japan major home appliances market is segmented by product type, distribution channel, technology, and region. By product type, the market is segmented into refrigerators, freezers, washing machines, dishwashers, cooktops & ranges, microwave ovens, air conditioners, and others. By distribution channel, the market is segmented into multi-brand stores, exclusive brand outlets, online, and other distribution channels. By technology, the market is segmented into conventional appliances and smart/connected appliances. By region, the market is segmented into Kanto, Kansai, Chubu, and the rest of Japan. The report offers the market size in value terms in USD for all the above-mentioned segments.

By Product Type

| Refrigerators |

| Freezers |

| Washing Machines |

| Dishwashers |

| Cooktops & Ranges |

| Microwave Ovens |

| Air Conditioners |

| Others (Electric Hobs etc) |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region

| Kanto |

| Kansai |

| Chubu |

| Rest of Japan |

| By Product Type | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Cooktops & Ranges | |

| Microwave Ovens | |

| Air Conditioners | |

| Others (Electric Hobs etc) | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Region | Kanto |

| Kansai | |

| Chubu | |

| Rest of Japan |

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan major home appliances market?

The Japan major home appliances market size is estimated USD 28.03 billion in 2026 and is projected to reach USD 31.75 billion by 2031 at a 2.52% CAGR.

Which product categories lead demand in Japan’s large appliances?

Refrigerators lead with 27.71% share in 2025, supported by large-capacity formats and food-preservation features, while dishwashers are expanding from a low base with a 3.35% CAGR through 2031.

How are channels shifting for appliance sales in Japan?

Multi-brand stores remain the largest channel with 46.34% share in 2025, while online is the fastest-growing channel with a projected 4.87% CAGR through 2031, reflecting strong urban adoption.

Where are the strongest regional opportunities within Japan?

Kanto holds a 40.34% share with high digital adoption and grid-enabled use cases, while Kansai is the fastest-growing region with a 4.12% CAGR through 2031.

What role do smart-grid programs play in appliance adoption?

Smart meters and time-of-use pricing improve the value of connected appliances by enabling off-peak scheduling and demand-response features that reduce operating costs and support grid flexibility.

How are aging demographics shaping appliance design and replacement?

Aging households favor simpler interfaces, voice assistance, and reliability, which influences replacement cycles and supports steady demand for accessible, connected features.

Page last updated on: