Botulinum Toxin In Urology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.01 Billion |

| Market Size (2030) | USD 1.45 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

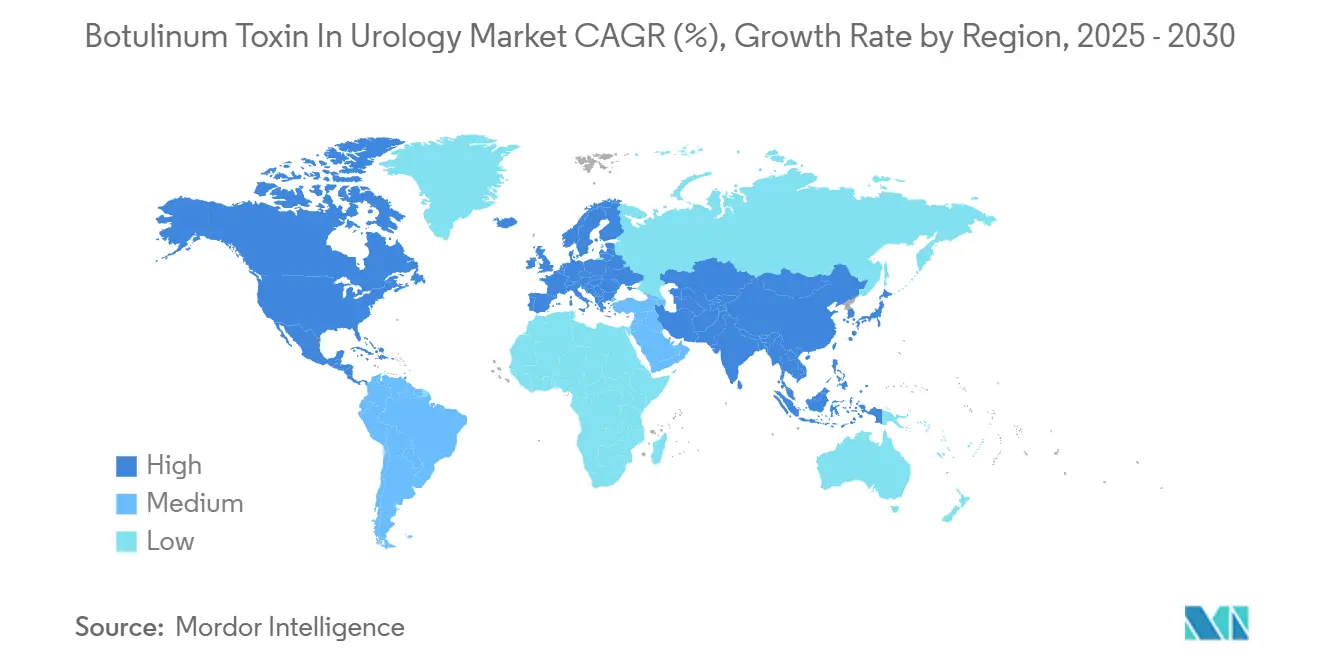

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

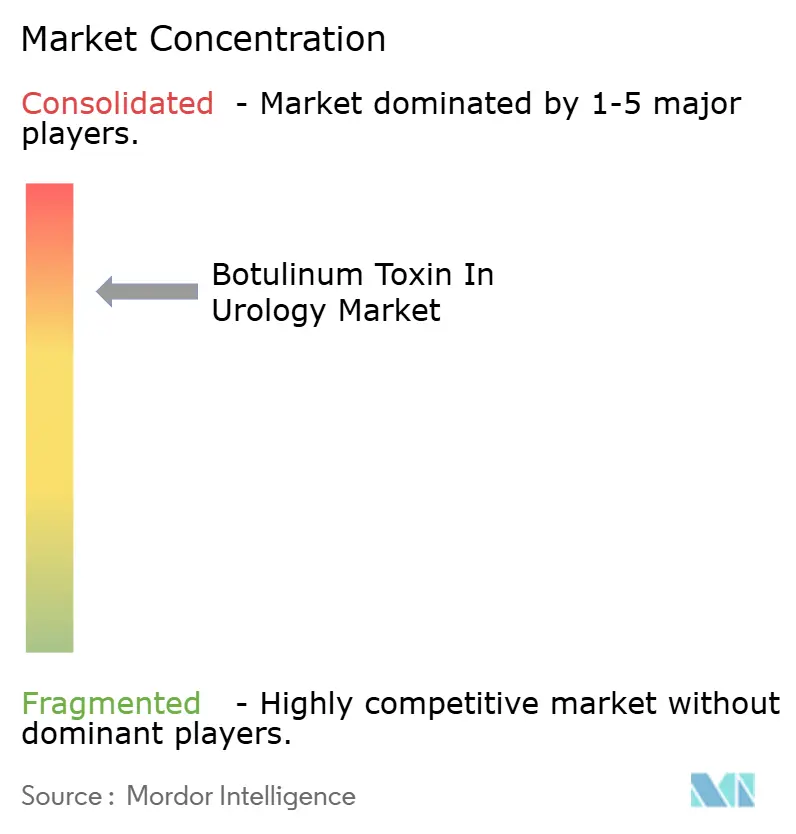

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Botulinum Toxin In Urology Market Analysis by Mordor Intelligence

The botulinum toxin for urological disorders market size stands at USD 1.01 billion in 2025 and is forecast to reach USD 1.45 billion in 2030, advancing at a 6.1% CAGR. Strong growth springs from expanding clinical indications, steady reimbursement revisions, and continued technology upgrades in injection guidance systems. OnabotulinumtoxinA maintains a commanding 70.3% botulinum toxin for urological disorders market share in 2025, but competitive pressure intensifies as PrabotulinumtoxinA posts the highest segment CAGR at 7.1%. Geographic dispersion favors North America, which secures 43.1% revenue owing to favorable Medicare billing codes and high specialist density, while Asia-Pacific records the fastest regional CAGR of 6.1% on the back of regulatory harmonization and infrastructure expansion. The hospital channel still contributes 42.6% of global sales; nonetheless, ambulatory surgery centers grow briskly as clinicians migrate routine cystoscopic injections to lower-cost outpatient settings. Growth headwinds—immunogenicity, short treatment duration, and supply concentration—are mitigated by liquid-stable formulations, complexing-protein-free technologies, and strategic investment in domestic good-manufacturing-practice capacity.

Key Report Takeaways

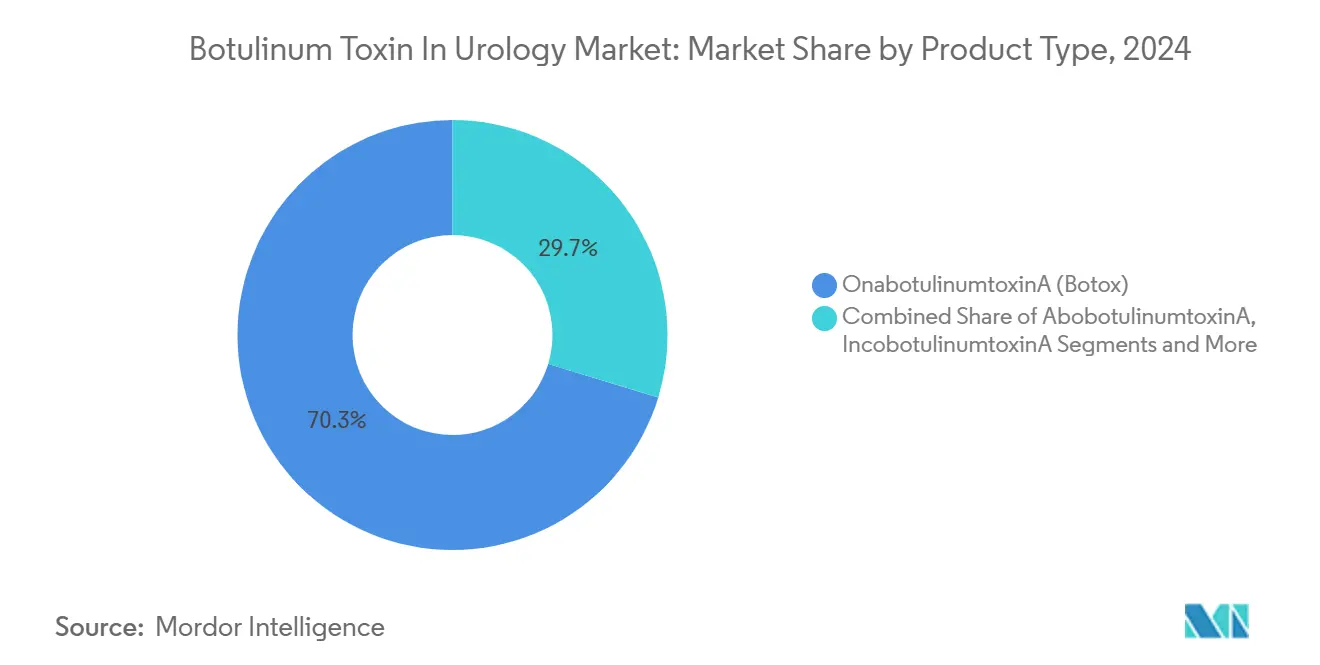

- By product type, OnabotulinumtoxinA (Botox) led with 70.3% revenue share in 2024; PrabotulinumtoxinA (Jeuveau) recorded the highest projected CAGR at 7.1% through 2030.

- By application, overactive bladder accounted for 51.4% share of the botulinum toxin for urological disorders market size in 2024, while benign prostatic hyperplasia is projected to expand at a 6.2% CAGR through 2030.

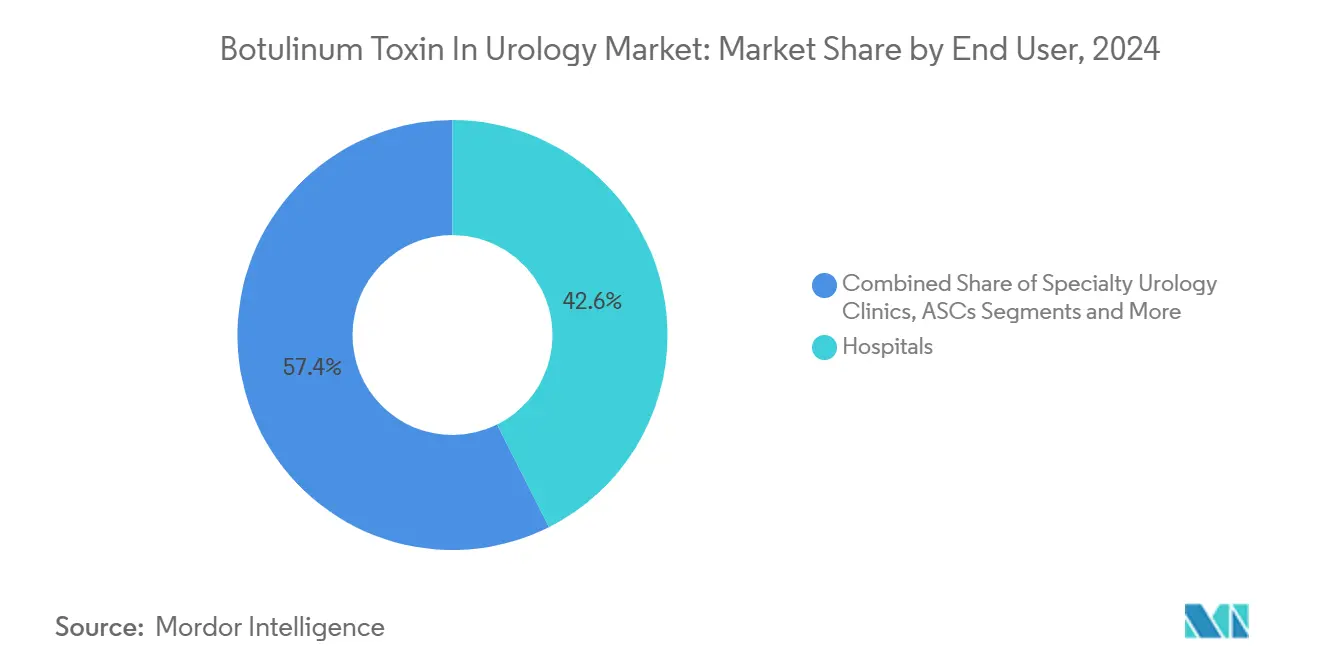

- By end user, hospitals held 42.6% of the botulinum toxin for urological disorders market share in 2024, whereas ambulatory surgery centers are advancing at a 5.5% CAGR during the forecast period.

- By geography, North America captured 43.1% market share in 2024, while Asia-Pacific is on track to grow at a 6.1% CAGR through 2030.

Global Botulinum Toxin In Urology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of overactive bladder and neurogenic detrusor overactivity | +1.80% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Expanding on-label use of OnabotulinumtoxinA for benign prostatic hyperplasia | +1.20% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Favorable reimbursement revisions for in-office cystoscopic injections | +1.00% | North America & EU | Short term (≤ 2 years) |

| Rapid adoption of high-precision flexible cystoscopes enabling office-based therapy | +0.90% | Global, early adoption in developed markets | Medium term (2-4 years) |

| First-in-class liquid-stable toxin formulations easing cold-chain constraints | +0.70% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Growing tele-urology platforms driving patient funnel for minimally invasive care | +0.50% | North America, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Overactive Bladder and Neurogenic Detrusor Overactivity

Growing life expectancy, higher diagnostic vigilance, and better patient education explain the steady rise in overactive bladder (OAB) and neurogenic detrusor overactivity (NDO) diagnoses worldwide. Claims analytics show a 431% jump in botulinum-toxin-A injections for urological indications in France between 2014 and 2022, proving rapid real-world uptake beyond early-adopter markets.[1]MDPI Editorial Office, “Real-World Utilization of Botulinum Toxin in France 2014-2022,” mdpi.com Expanded Medicare coverage that explicitly reimburses office-based cystoscopic injections cements financial viability for urology practices in the United States. Because botulinum toxin targets acetylcholine-mediated detrusor overactivity, OAB and NDO patients receive symptom relief that oral antimuscarinics often fail to deliver. Standardized injection templates issued by the U.S. Food and Drug Administration (FDA) strengthen procedure uniformity and boost clinician confidence.[2]U.S. Food and Drug Administration, “CPT Coding Guidance for OnabotulinumtoxinA Injection,” fda.gov Taken together, epidemiological momentum and policy support sustain long-run demand in every major geography.

Expanding On-Label Use of OnabotulinumtoxinA for Benign Prostatic Hyperplasia

Benign prostatic hyperplasia (BPH) treatment represents the fastest-growing application in the botulinum toxin for urological disorders market. Randomized trials show statistically significant reductions in prostate volume and improvements in maximum urinary-flow rate after intraprostatic botulinum toxin administration, encouraging FDA label extensions in 2024 and 2025. New BPH devices such as HYDROS and Optilume complement toxin injections, allowing multimodal care pathways that lower retreatment rates. Ultrasound-guided delivery systems improve accuracy, thereby reducing the incidence of urinary retention events. Reimbursement is well-defined, further lowering adoption barriers. As more urologists seek minimally invasive alternatives to transurethral resection of the prostate, botulinum toxin gains credibility as an intermediate option between drug therapy and surgery.

Favorable Reimbursement Revisions for In-Office Cystoscopic Injections

From January 2025, the U.S. Centers for Medicare & Medicaid Services (CMS) raised ambulatory payment classifications for cystoscopic botulinum toxin injections, boosting practice revenue per case by 12%. Parallel revisions occurred within several European social-insurance systems, narrowing physician-office and hospital payment gaps. Transparent billing codes facilitate claims administration and remove ambiguity around drug add-ons. Because payer clarity aligns economic incentives with clinical benefit, utilization widens beyond tertiary referral centers into community-based clinics. Over the next two years, reimbursement improvements will directly add an estimated 1.0 percentage point to global CAGR.

Rapid Adoption of High-Precision Flexible Cystoscopes Enabling Office-Based Therapy

Fourth-generation flexible cystoscopes equipped with narrow-band imaging and 4K visualization enable accurate trigone and bladder-wall targeting without general anesthesia. The ability to perform high-quality injections in procedural suites reduces hospital overhead and shortens patient scheduling queues. Adoption began in the United States and Germany in 2024 and quickly permeated Japan by late 2025. Device vendors now bundle cystoscopes with botulinum-toxin procedural kits, an arrangement that simplifies inventory management for ambulatory surgery centers (ASCs). Clinical studies report procedure times below 10 minutes with minimal post-operative observation. Shorter turnaround multiplies daily case volumes, indirectly accelerating toxin unit sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short duration of therapeutic effect necessitating repeated injections | −1.5% | Global | Medium term (2-4 years) |

| Supply concentration risk due to limited GMP toxin manufacturers | −0.8% | Global, acute in supply-constrained regions | Short term (≤ 2 years) |

| Regulatory uncertainty over long-term immunogenicity in off-label use | −0.6% | North America & EU | Long term (≥ 4 years) |

| Rising litigation on adverse urinary retention events dampening physician uptake | −0.4% | North America, spill-over to other litigious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short Duration of Therapeutic Effect Necessitating Repeated Injections

Median symptom-control spans range from 16 to 24 weeks, compelling many patients to undergo two or three treatment sessions a year. A French cohort study documented that 28.7% of OAB patients request re-treatment while still reporting partial relief, implying a preference for maintaining submaximal control rather than waiting for complete symptom return.[3]B. Truong, “Efficacy Remaining at Time of Requested Re-Treatment for Cervical Dystonia: A Potential New Treatment Paradigm with DaxibotulinumtoxinA,” Toxins, mdpi.com Re-injection frequency elevates out-of-pocket expenses and magnifies scheduling burdens for providers. Payers evaluate cumulative annual costs relative to sacral neuromodulation, potentially capping procedure volumes in cost-constrained systems. Pipeline solutions—extended-release carriers and serotype E toxins—aim to lengthen effect duration, but they will not reach commercial scale before 2027.

Supply Concentration Risk Due to Limited GMP Toxin Manufacturers

Five companies control more than 90% of global GMP-grade botulinum toxin output, leaving the supply chain vulnerable to single-site disruptions. Mechanical upgrades at AbbVie’s Westport Ireland site in late 2024 temporarily reduced output and forced allocation to priority markets, highlighting the fragility of current capacity utilization. Governments now classify botulinum toxin as dual-use biological material, imposing export-licensing steps that can create additional bottlenecks. To alleviate risk, the U.S. Biomedical Advanced Research and Development Authority signed a USD 250 million manufacturing accord with National Resilience in 2024. Nevertheless, multi-source redundancy will take years to materialize, dampening growth potential in the interim.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Competition Intensifies Around Formulation Innovation

OnabotulinumtoxinA generated 70.3% of worldwide revenue in 2024, equal to roughly USD 0.71 billion of the botulinum toxin for urological disorders market size. Brand longevity, broad label coverage, and far-reaching distributor networks uphold its primacy. Yet, price-sensitive institutions increasingly trial PrabotulinumtoxinA, spurring its 7.1% forecast CAGR. Developers of AbobotulinumtoxinA and IncobotulinumtoxinA differentiate through complexing-protein-free profiles, addressing immunogenicity worries that loom in chronic-care settings. FDA clearance of Letybo in February 2024 opened the door for Asian manufacturers to compete head-to-head, adding downward price pressure. Meanwhile, AbbVie’s TrenibotulinumtoxinE Biologics License Application in April 2025 introduces a serotype with a faster onset and shorter half-life, targeting retreatment frustration for high-frequency users. Competitive moats thus evolve from brand equity to science-based claims about duration and safety, forcing incumbents to invest in next-generation technologies.

Growth prospects hinge on payers’ willingness to reimburse new entrants at par with Botox’s average selling price. If price parity stalls, market seepage stays limited; if payers adopt reference-pricing cliffs, share migration accelerates. Early hospital pharmacy data from Germany indicate that formularies admit at least two licensed toxins, signaling an appetite for negotiated discounts over single-vendor dependence. R&D investment, therefore, concentrates on head-to-head non-inferiority trials and real-world registries to persuade budget committees. This environment spurs steady but incremental diversification rather than abrupt displacement.

By Application: BPH Surges Ahead but OAB Retains Scale Advantage

Overactive bladder kept 51.4% application share in 2024, equating to roughly USD 0.52 billion of the botulinum toxin for urological disorders market size. Physicians possess robust clinical algorithms, and Medicare coverage widens access among seniors. Treatment algorithms frequently tier oral antimuscarinics, β-3 agonists, and finally botulinum toxin, conserving its demand durability over time. Neurogenic detrusor overactivity, anchored in spinal-cord-injury and multiple-sclerosis cohorts, contributes stable baseline revenue because neurologists refer eligible patients consistently.

Benign prostatic hyperplasia, however, advances with a 6.2% CAGR, the fastest among all indications. Evidence shows intraprostatic toxin reduces prostate volume by up to 25% at six months, giving BPH patients a reversible, minimally invasive alternative to transurethral resection. Complementary approvals, such as Sumitomo Pharma’s GEMTESA for OAB in men with BPH, multiply combined-therapy permutations. Interstitial cystitis and bladder pain syndrome remain nascent indications; their share may rise once robust Phase III data arrive in 2026. Between 2025 and 2030, oncology supportive-care use remains negligible, leaving ample white space for exploratory trials.

By End User: ASC Expansion Reshapes Care Delivery Economics

Hospitals commanded 42.6% global revenue in 2024, underpinned by tertiary-care capabilities, bundled procurement, and in-house pharmacy managed services. Complex cases—such as neurogenic detrusor overactivity with concurrent spasticity—often require multidisciplinary teams only large centers provide. Academic teaching hospitals also serve as pivotal sites for investigator-initiated trials, bolstering their role in evidence generation.

Ambulatory surgery centers achieve a 5.5% CAGR through 2030, the quickest among settings, thanks to regulatory changes that authorize in-office anesthesia and reimbursement parity relative to hospital outpatient departments. Enhanced instruments facilitate same-day discharge without catheterization, a selling point for patients. Specialty urology clinics hold steady market position by emphasizing personalized follow-up and flexible scheduling. Future growth within ASCs hinges on negotiating group-purchasing contracts that lock in favorable vial pricing while maintaining high throughput to amortize capital equipment.

Geography Analysis

North America accounted for 43.1% of 2024 revenue, supported by well-funded insurance mechanisms and high procedural density. Botulinum toxin for urological disorders market size in the United States reached USD 0.44 billion, and CMS billing guidance published in 2025 codified separate payment for physician work and drug cost. Canada follows similar reimbursement tracks, though provincial-budget reviews introduce periodic price caps. Trade-policy volatility still threatens Irish-sourced supply, prompting AbbVie to explore U.S. fill-and-finish expansion.

Europe maintains solid share through harmonized European Medical Device Regulation alignment, enabling cross-border device and drug-device combination approvals. France exemplifies rapid adoption, with a 431% increase in urological botulinum toxin use over eight years. Germany and Italy are migrating large fractions of OAB cases to outpatient settings, lifting volume growth above the regional average. National health systems continue to negotiate mandated discounts, channeling price-compression risk to manufacturers but keeping procedural uptake elevated.

Asia-Pacific drives future upside with a 6.1% regional CAGR. China streamlined New Drug Application review timelines to 12 months on average in 2024 and approved 92 novel drugs, including letibotulinumtoxinA and TraBOTOX kits. Japan’s Pharmaceutical and Medical Devices Agency updates its conditional approval framework in 2025, shortening post-marketing surveillance requirements once safety endpoints are met. India’s Central Drugs Standard Control Organization ratified abbreviated dossiers for biosimilar botulinum formulations, intensifying local competition. Infrastructure modernization, combined with rising middle-class disposable income, converts latent demand into realized procedures. Medical-tourism corridors in Thailand and South Korea further augment regional patient volumes.

Competitive Landscape

The botulinum toxin for urological disorders market exhibits moderate concentration: the top five companies account for roughly 70% of global revenue. AbbVie anchors leadership with USD 866 million in Botox Therapeutic sales for Q1 2025, marking 15.8% year-over-year growth. Ipsen sustains a competitive presence via Dysport’s complexing-protein-free positioning and robust investigator-initiated trial network. Merz leverages Xeomin’s purification profile to penetrate patient segments wary of antibody formation. Hugel’s FDA-authorized Letybo and pending Europe-China reciprocity approvals demonstrate the globalization of Korean manufacturing prowess, reflecting the eastward shift in capacity.

Strategic playbooks focus on extending the duration of action and mitigating immunogenicity. AbbVie’s serotype E candidate aims for three-month efficacy with 50% reduced neutralizing-antibody risk versus serotype A. Revance’s peptide-stabilized DaxibotulinumtoxinA (acquired by Crown Laboratories) targets six-month durability and reaches its pivotal Phase III cystitis endpoints in 2025. Manufacturers also deploy bundled solutions that integrate single-use cystoscope sheaths, premixed toxin syringes, and electronic health-record templates. Digital-health partnerships, such as Ipsen’s pilot with a leading tele-urology start-up, streamline virtual assessment and automated refill scheduling.

Supply-chain resilience constitutes a new competitive battleground. The U.S. Biomedical Advanced Research and Development Authority–Resilience agreement anchors domestic emergency inventory and could evolve into contract-manufacturing lines for commercial toxin brands. European Union authorities incentivize duplication of critical GMP processes across borders to prevent single-site shock. Counterfeit-prevention programs—QR-coded vial authentication and blockchain ledger tracking—gain urgency after the U.S. Centers for Disease Control and Prevention reported multi-state incidents involving falsified toxin in 2024. Companies that master quality-assurance transparency will consolidate trust with regulators and prescribers.

Botulinum Toxin In Urology Industry Leaders

AbbVie Inc. (Allergan Aesthetics)

Ipsen Pharma

Merz Pharma

Daewoong Pharmaceutical

Revance Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AbbVie submitted a Biologics License Application to the FDA for TrenibotulinumtoxinE, the first serotype E formulation intended for urological disorders.

- February 2025: Crown Laboratories finalized its USD 924 million acquisition of Revance Therapeutics, acquiring DaxibotulinumtoxinA extended-duration technology.

- February 2024: Hugel’s Letybo became the first Korean botulinum toxin cleared by the FDA, introducing added price competition in urological care.

Global Botulinum Toxin In Urology Market Report Scope

| OnabotulinumtoxinA (Botox) |

| AbobotulinumtoxinA (Dysport) |

| IncobotulinumtoxinA (Xeomin) |

| PrabotulinumtoxinA (Jeuveau) |

| Others |

| Overactive Bladder |

| Neurogenic Detrusor Overactivity |

| Interstitial Cystitis & Bladder Pain Syndrome |

| Benign Prostatic Hyperplasia |

| Others |

| Hospitals |

| Specialty Urology Clinics |

| Ambulatory Surgery Centers |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | OnabotulinumtoxinA (Botox) | |

| AbobotulinumtoxinA (Dysport) | ||

| IncobotulinumtoxinA (Xeomin) | ||

| PrabotulinumtoxinA (Jeuveau) | ||

| Others | ||

| By Application | Overactive Bladder | |

| Neurogenic Detrusor Overactivity | ||

| Interstitial Cystitis & Bladder Pain Syndrome | ||

| Benign Prostatic Hyperplasia | ||

| Others | ||

| By End User | Hospitals | |

| Specialty Urology Clinics | ||

| Ambulatory Surgery Centers | ||

| Research & Academic Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will global revenue for botulinum toxin in urological care be in 2030?

Forecasts place the botulinum toxin for urological disorders market size at USD 1.45 billion by 2030, reflecting a 6.1% CAGR.

Which formulation dominates physician prescribing?

OnabotulinumtoxinA holds 70.3% 2024 share, driven by extensive clinical data and wide reimbursement coverage.

What is the fastest-growing clinical indication?

Benign prostatic hyperplasia is projected to grow at a 6.2% CAGR through 2030 due to emerging evidence of prostate-volume reduction.

Which end-user channel is expanding the quickest?

Ambulatory surgery centers register a 5.5% CAGR as procedures migrate from hospital outpatient departments to cost-efficient settings.

Why are liquid-stable toxins important?

Liquid-stable formulations lessen cold-chain dependence, improving access in emerging markets and simplifying clinic workflows.

How does tele-urology influence demand?

Virtual consultation platforms funnel additional patients into minimally invasive injection pathways, raising utilization in practices that adopt digital triage tools.

Page last updated on: