BLDC Fan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 10.80% CAGR |

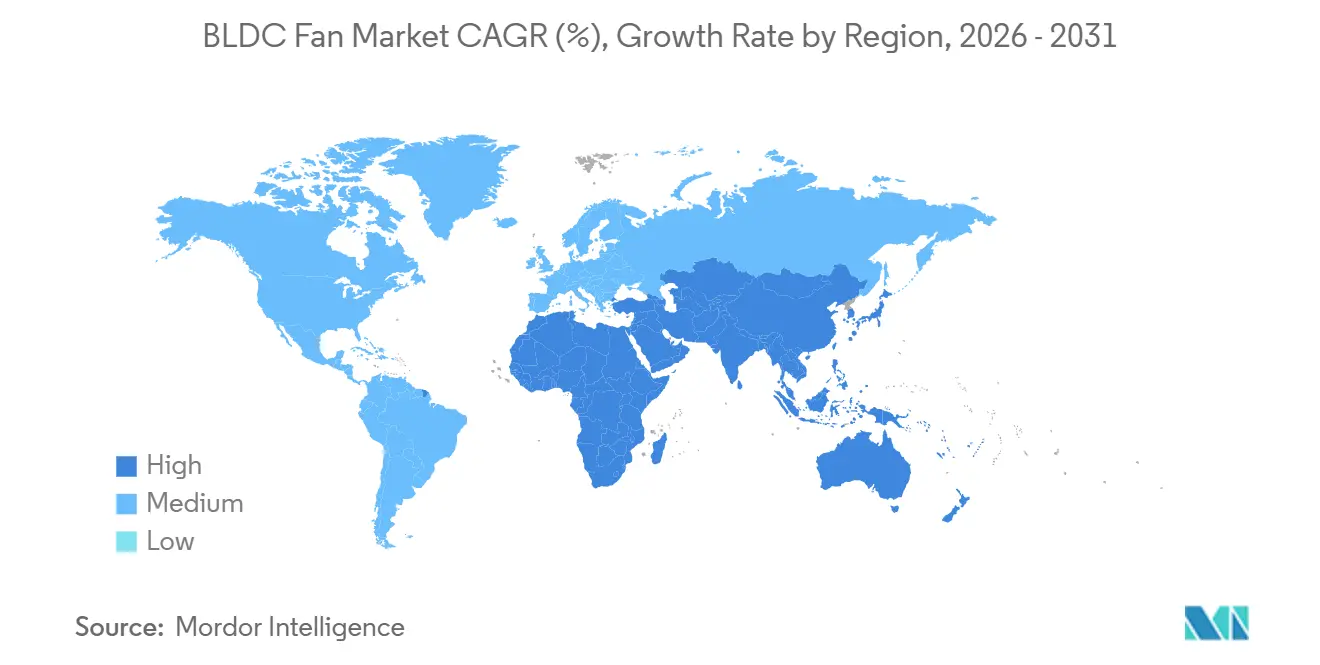

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

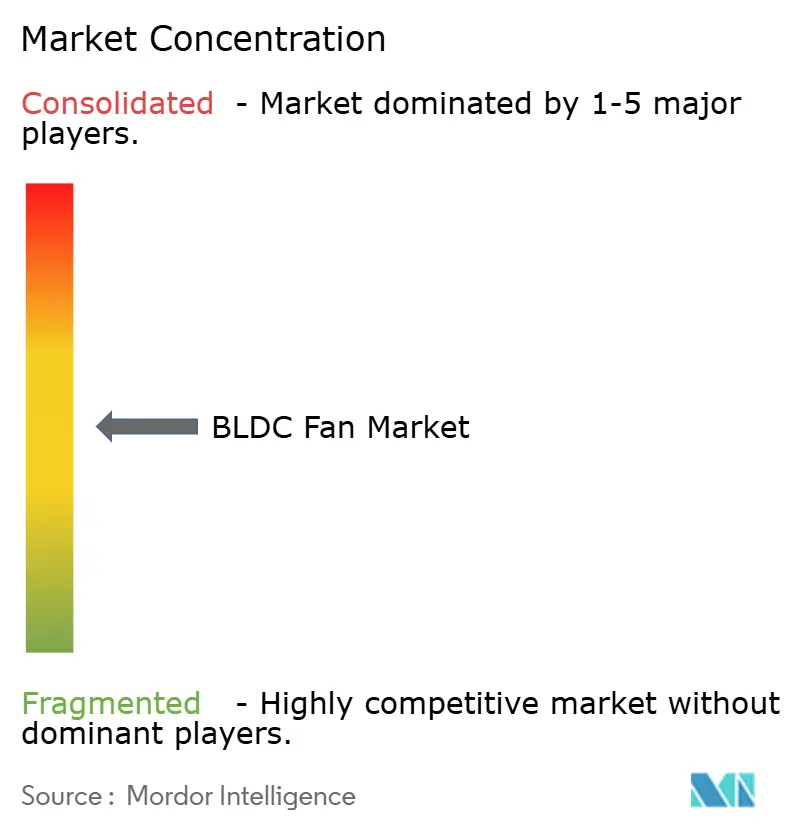

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

BLDC Fan Market Analysis by Mordor Intelligence

The BLDC fan market size is projected to expand from USD 1.38 billion in 2025 and USD 1.52 billion in 2026 to USD 2.54 billion by 2031, registering a CAGR of 10.80% between 2026 and 2031. Market momentum in 2026 reflects tighter energy-efficiency regulations that reward variable-speed electronic commutation, a shift that lifts adoption across residential, commercial, industrial, and data center settings. State-level rules in the United States and upcoming ecodesign measures in Europe drive platform standardization around FEI-compliant EC and BLDC designs, while India’s mandatory star labeling increases consumer awareness of wattage-to-airflow performance for ceiling fans. Data center cooling and electronics thermal management contribute a high-value layer of demand as operators pursue higher reliability and tighter control ranges that favor BLDC architectures. Distribution models are also evolving as D2C and connected products gather usage data that improve designs and shorten product cycles, while offline channels remain important for installation quality and after-sales service in complex projects.

Key Report Takeaways

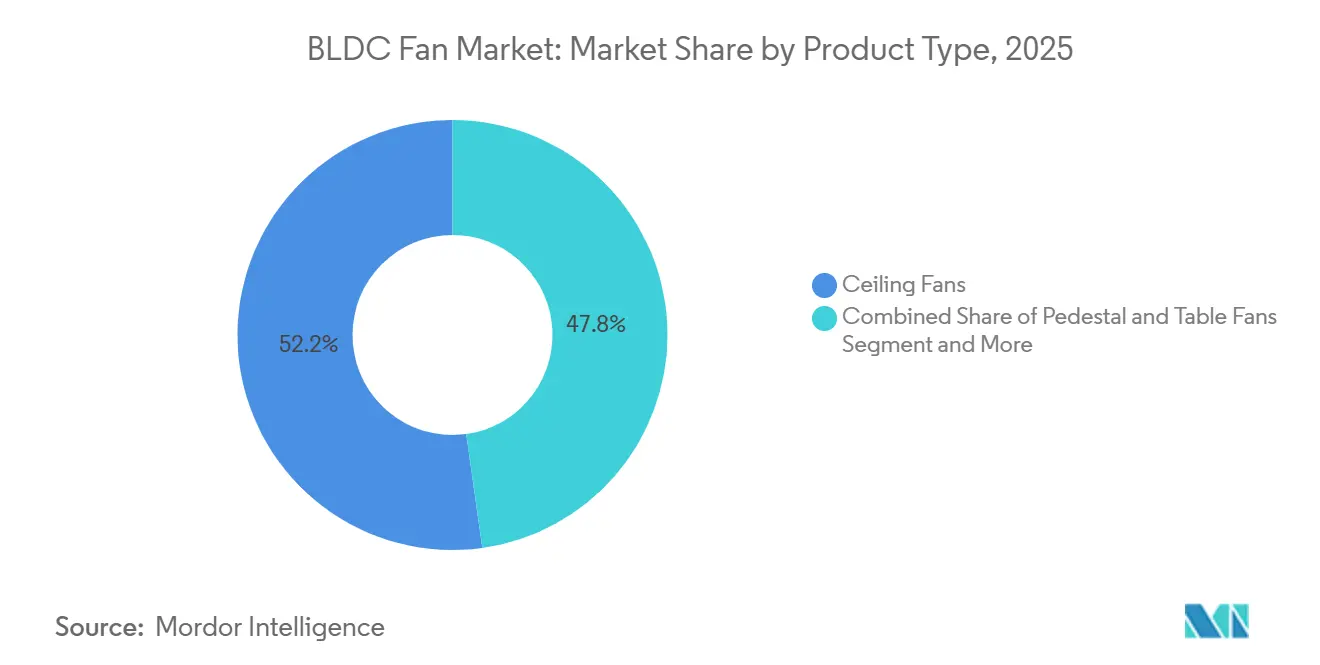

- By product type, ceiling fans captured 52.21% of the BLDC fan market share in 2025, while industrial HVLS and commercial ventilation fans are projected to grow at 11.95% CAGR between 2026 and 2031.

- By motor architecture, inner-rotor motors captured 68.87% of the BLDC fan market in 2025, while outer-rotor EC designs are projected to grow at 9.99% CAGR between 2026 and 2031.

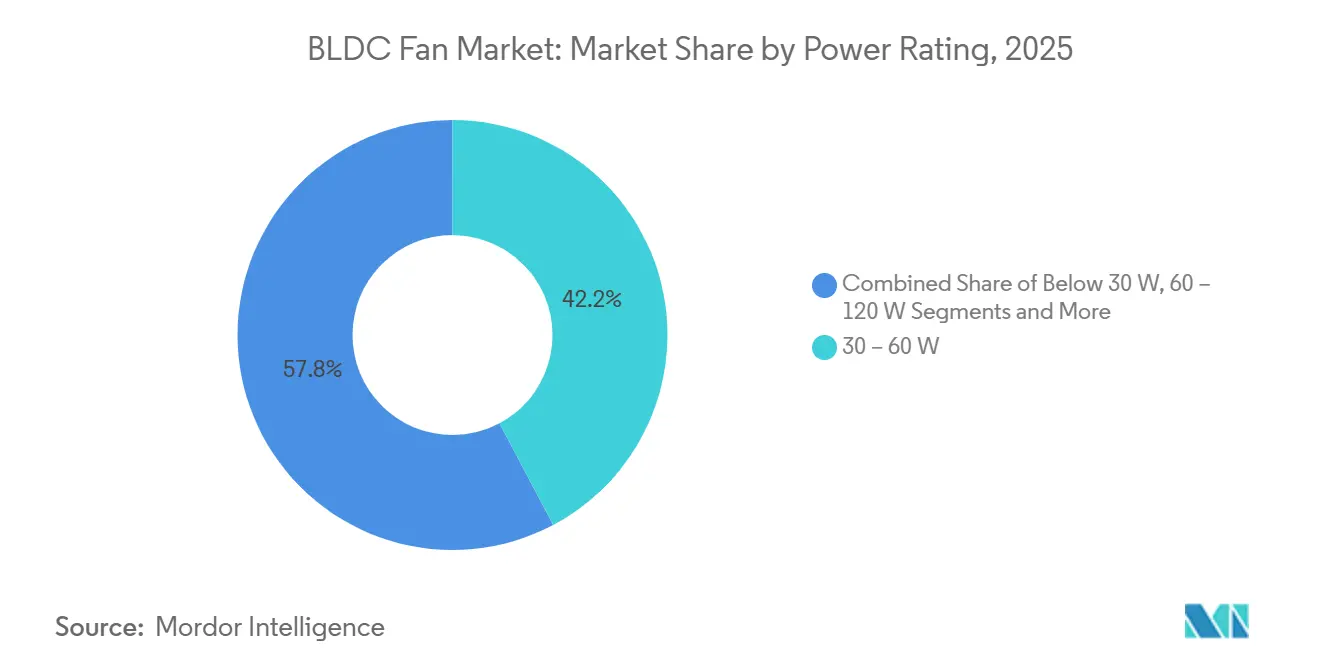

- By power rating, the 30-60W band captured 42.23% of the BLDC fan market in 2025, while the 60-120W band is projected to grow at 13.69% CAGR between 2026 and 2031.

- By application, residential captured 56.62% of the BLDC fan market size in 2025, while industrial and warehouse are projected to grow at 10.23% CAGR between 2026 and 2031.

- By distribution channel, offline retail captured 75.25% of the BLDC fan market in 2025, while online is projected to grow at 15.52% CAGR between 2026 and 2031.

- By geography, Asia-Pacific captured 45.75% of the BLDC fan market in 2025 and is projected to grow at 12.68% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global BLDC Fan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tighter energy-efficiency standards and star labeling for fans | +2.8% | Global, with earliest adoption in EU (2026), California (2024), India (BEE mandatory program) | Short term (≤ 2 years) |

| Payback-led residential replacement of AC induction with BLDC ceiling fans | +2.3% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Rapid EC fan adoption in commercial HVAC for variable-speed control and IAQ | +1.9% | North America & EU commercial building stock | Medium term (2-4 years) |

| Data center and electronics thermal loads favoring high-reliability BLDC fans | +2.1% | Global, concentrated in US, Ireland, Singapore, Frankfurt data center hubs | Short term (≤ 2 years) |

| 48V DC distribution in racks/buildings enabling direct BLDC fan deployments | +0.9% | North America hyperscale data centers, select EU greenfield projects | Long term (≥ 4 years) |

| Utility and green-building incentives bundling smart BLDC fans with BMS/EMS | +1.0% | North America (LEED, WELL), Europe (BREEAM), Asia-Pacific (Green Star) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tighter Energy-Efficiency Standards and Star Labeling for Fans

Converging regulations in the United States, European Union, and India reset the baseline for fan performance by using holistic wire-to-air metrics and labeling schemes that expose system losses, which elevate the value of electronically commutated machines in both comfort and process ventilation. California’s Title 20 requires FEI ≥ 1.00 across a wide range of commercial and industrial fan types, a standard backed by AMCA test procedures and certification pipelines that already count large numbers of compliant models in MAEDbS[1]Air Movement and Control Association International, “California Title 20 Fan-Efficiency Regulations Update,” AMCA, amca.org . The European Commission’s 2024 ecodesign rules for fans from 125W to 500kW project 31 TWh of annual electricity savings by 2030 and begin applying in June 2026, which pushes manufacturers to simplify portfolios around higher-efficiency platforms and provide richer performance data for designers. ENERGY STAR Most Efficient criteria for 2025 ventilating fans raise the most practical efficacy thresholds to achieve with EC motors and robust controls rather than with capacitor-start induction systems. Building codes like California Title 24 integrate FEI into mandatory requirements, which turns energy performance into a specification gate rather than a marketing option and positions BLDC fans as default selections in compliant projects.

Payback-Led Residential Replacement of AC Induction with BLDC Ceiling Fans

In India and across parts of Asia-Pacific, electricity tariffs and long daily runtimes compress payback periods for BLDC ceiling fans to below two years at typical price premiums, which makes the switch compelling even without subsidies and lifts repeat purchase intent. Manufacturer data show a conventional 75W induction ceiling fan can cost over INR 2,400 in annual electricity for high-usage homes, while a 28-35W BLDC model can cut that cost by more than half at common usage patterns and tariffs, reinforcing the upgrade case on household economics alone[2]ORIENTELECTRIC.COM BLDC Fans vs Normal Fans: The Ultimate Buying Guide ( 2025 ). India’s mandatory star labeling for ceiling fans further amplifies this shift by requiring disclosure on service value, letting consumers compare air delivery per watt at the point of purchase, and pushing manufacturers to redesign portfolios around more efficient BLDC platforms. Product strategies in China center less on energy savings and more on connectivity and integration into smart ecosystems, where BLDC motors support quiet, precise speed control as part of larger home automation and IAQ solutions. Wide-voltage designs and controller robustness are also crucial in emerging markets with grid instability, which guides platform choices and value engineering in the BLDC fan market.

Rapid EC Fan Adoption in Commercial HVAC for Variable-Speed Control and IAQ

Commercial buildings are adopting EC fans as core components of ventilation strategies that rely on variable-speed control to align air changes with occupancy and to support modern IAQ frameworks. ASHRAE Standard 62.1 defines minimum ventilation rates and supports demand-controlled ventilation approaches that favor granular fan speed modulation, with updated provisions adopted for improved humidity control and emergency ventilation functions that benefit electronically commutated solutions. Green building programs such as LEED v5 emphasize performance optimization across HVAC components and acknowledge FEI-based design practices that reward high-efficiency motors and integrated controls in both new builds and retrofits[3]US Green Building Council, “BMS-Agnostic Building Optimisation,” USGBC, usgbc.org. EC platforms create a measurable value proposition through lower part-load energy, better controllability for zone-level ventilation, and improved acoustic outcomes at reduced fan speed compared with induction alternatives. European suppliers have introduced high-diameter axial and centrifugal EC fans with native digital interfaces and system-optimization software that enhance installation, commissioning, and ongoing performance. The combined impact of standards, certifications, and intelligent control has reinforced the case for EC fans in commercial HVAC, where energy, IAQ, and acoustic performance converge as core design priorities.

Data Center and Electronics Thermal Loads Favoring High-Reliability BLDC Fans

Rising rack power densities and wider allowable temperature envelopes in data centers increase the need for tightly controlled airflow that maintains stability across temperature and load variations, a requirement suited to electronically commutated fans. ASHRAE TC 9.9 guidelines outline classes with extended inlet temperature ranges that demand consistent fan operation under higher thermal stress, favoring BLDC drives with precise speed control and robust thermal performance. Vendors targeting data center applications now emphasize reliability metrics, modularity, and integrated diagnostics, alongside compatibility with high-density cooling strategies for AI clusters and liquid-to-air heat exchange stages. Manufacturer disclosures indicate growth in precision fans and thermal modules for server and cooling infrastructure, with active pilots in water-cooling subsystems supporting next-generation racks. Platforms with vibration sensing, MODBUS connectivity, and digital twinning for thermal simulation have become mainstream in offerings oriented to hyperscale and colocation facilities. As data center operators seek lower PUE through system-level efficiency, high-performance BLDC fans enable both incremental and step improvements, and they strengthen the case for 48V DC distribution and native DC component integration where architecture shifts allow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront cost premium from rare-earth magnets and controllers | -0.8% | Global, most acute in price-sensitive South America, Africa, Southeast Asia markets | Medium term (2-4 years) |

| Rare-earth magnet price volatility and supply concentration risks | -0.6% | Global, with procurement hedging costs concentrated in North America and EU manufacturers | Short term (≤ 2 years) |

| After-sales electronics service gaps and reliability concerns in harsh environments | -0.4% | Industrial/warehouse applications in Middle East, Africa, South Asia high-dust/high-temperature zones | Long term (≥ 4 years) |

| EMI/acoustic compliance constraints slowing global SKU rollouts | -0.3% | Global, regulatory fragmentation between FCC (US), CE (EU), KC (Korea), CCC (China) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Upfront Cost Premium from Rare-Earth Magnets and Controllers.

Capital cost remains a barrier in price-sensitive markets, particularly where fans compete with basic induction alternatives that meet minimum airflow requirements at lower purchase prices. Procurement strategies and bill-of-material choices reflect an ongoing balance between higher-efficiency motors, controller sophistication, and acceptable payback periods at local tariffs. Supply concentration of rare-earth processing and permanent magnet manufacturing elevates input risk for BLDC bill of materials, which sustains premiums over time and complicates pricing strategies for mass-market segments. Manufacturers respond with platform standardization and controller reuse across product lines to improve scale economics and reduce certification overhead. Over the forecast, larger players are better positioned to absorb input volatility, which supports the relative strength of integrated vendors within the BLDC fan market.

Rare-Earth Magnet Price Volatility and Supply Concentration Risks

Concentration in upstream processing and magnet fabrication makes price and availability volatile, and it introduces a procurement management cost that can widen differentials between EC or BLDC and induction-based alternatives. Industry and government mineral reports continue to show high reliance on a few processing hubs for critical rare earths used in high-performance magnets, which sustains the need for long-term contracts and inventory strategies among major motor makers. Platform design choices that allow partial substitution or reduced magnet mass can moderate exposure but may impose performance or acoustic trade-offs. These dynamics influence both initial equipment price and after-sales pricing for critical spares within the BLDC fan market. Vendors with deeper supply partnerships display more stable pricing and lead times during periods of disruption, which can steer project specifications toward incumbents[4]Nidec Corporation, “Fiscal 2024 Financial Results,” Nidec Investor Relations, nidec.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceiling Fans Hold Share, Yet HVLS Leads Growth

Ceiling fans commanded 52.21% share in 2025, making them the largest product category by volume and revenue, while industrial HVLS and commercial ventilation fans deliver the fastest expansion at 11.95% CAGR through 2031, a split that reflects replacement cycles in homes and greenfield growth in logistics, data center, and industrial settings within the BLDC fan market. The installed base and familiarity of ceiling fans sustain their lead, and mandatory labeling in countries like India increases transparency that favors BLDC models with high service value and quiet operation. Product innovation cycles in residential categories now emphasize connectivity, aesthetic options, and lower noise, while commercial and industrial products lean toward controls integration, predictive diagnostics, and high static pressure performance aligned with HVAC design standards. Vendors in Europe and North America have also brought large-diameter EC axial and centrifugal models to market with native digital protocols and AI-supported optimization that build lifetime performance advantages over induction solutions. This mix sustains a strong ceiling fan core while shifting marginal growth to HVLS and specialized ventilation use cases inside the BLDC fan market.

Across product lines, portable, wall, and exhaust fans retain solid roles in code-driven ventilation and spot cooling, but they show more incremental innovation relative to HVLS and advanced commercial systems. Premium consumer products in desk, tower, and bladeless formats compete on design and quietness, with integrated app control and sensor feedback that adapts airflow to room conditions. Industrial HVLS solutions emphasize destratification benefits and year-round comfort in large facilities, where variable-speed EC drives offer smoother control, reduced energy use, and better acoustic performance at low RPM. In warehouses and logistics, BLDC fans combine with demand-based controls to meet both IAQ and comfort targets during peak periods, and manufacturers now include features such as vibration sensing and BMS integration for predictive maintenance. The BLDC fan market continues to balance volume-driven ceiling applications with the growing premium and specification-led opportunity in HVLS and advanced commercial ventilation.

By Motor Architecture: Inner-Rotor Dominates, Outer-Rotor Accelerates in HVAC

Inner-rotor designs helda 68.87% share in 2025 and remain the architecture of choice for many ceiling, pedestal, and compact fans, while outer-rotor EC designs are the fastest-growing with 9.99% CAGR through 2031 as HVAC systems favor low-speed, high-torque configurations in the BLDC fan market. Inner-rotor motors deliver high torque density in compact footprints and serve reversible, oscillating, and smart ceiling fans well, where rapid speed changes and quiet operation are emphasized in residential and light commercial settings. Their constraints lie in thermal management at higher continuous power, which curbs scalability for large HVAC fans without added conduction paths or heat sinks that raise cost and weight. Outer-rotor EC designs distribute mass around the perimeter for higher torque at low RPM, which suits larger diameters and higher airflows with lower noise and extended bearing life. In air handling applications, these fans can maintain efficiency across wide turndown ranges, which is central to meeting ventilation standards at variable occupancy levels in commercial buildings.

Product launches reinforce these themes with larger-diameter EC platforms and compact diagonal modules that substitute for axial units at lower noise and higher efficiency. European suppliers emphasize modular frames, wide voltage tolerances, and digital communication protocols for faster commissioning and system-level optimization, which improves delivered performance over time. Residential suppliers focus on refinement of connectivity, app control, and silent profiles at low speeds, where user experience drives differentiation in crowded retail categories. Over the forecast period, inner-rotor platforms should retain dominant share by unit volumes, while outer-rotor EC configurations expand share in HVAC, clean room, and process ventilation due to static pressure and low-noise advantages. This architecture mix keeps the BLDC fan market responsive to both consumer preferences and commercial performance targets.

By Power Rating: Mid-Range Dominates, High-Power Surges with Industrial Demand

The 30-60W band accounted for 42.23% share in 2025 and remains the core of residential ceiling and small commercial ventilation, while the 60-120W band is the fastest-growing at 13.69% CAGR as industrial and logistics facilities expand use of higher-airflow fans within the BLDC fan market. In India and other high-usage markets, 28-35W BLDC ceiling fans are positioned to satisfy energy-labeled performance targets and to cut monthly bills, with published specifications underscoring wattage and airflow balance as key purchase drivers. Improvements within this power class are now more about aerodynamics, low-speed comfort, and connectivity than large steps down in wattage, which suggests steady growth anchored to replacement cycles and new construction. The 60-120W band benefits from deployment in industrial and warehouse areas where airflow over larger zones and destratification needs drive higher connected loads per fan, and EC efficiency gains unlock both energy savings and control precision. Data-center-adjacent cooling solutions in this power class also boost demand where rack and row-level airflow must integrate with monitoring, alarms, and predictive maintenance.

Segments below 30W remain relevant in electronics, telecom, and appliances where compact geometries and low noise outweigh marginal efficiency differences, while segments above 120W focus on industrial blowers and process ventilation that still have headroom for EC retrofits. Vendors in higher power classes leverage controls integration to meet FEI-based targets and to provide transparent part-load curves to system designers, which is essential for Title 20 and European ecodesign compliance journeys. Across these classes, the BLDC fan market size allocation will tilt moderately toward higher-power bands as logistics, manufacturing, and edge data centers multiply sites where airflow needs exceed residential norms. The combination of energy savings and digital readiness should keep higher-power BLDC designs on a favorable growth path as industrial and commercial projects scale up. These shifts also reinforce the importance of channel partners who can size and commission higher-power equipment within building projects that have performance guarantees.

By Application: Residential Volume Meets Industrial Growth, Data Centers Redefine Specs

Residential held 56.62% share in 2025 and remains the largest application by units, while industrial and warehouse show the highest growth at 10.23% CAGR to 2031 as facilities expand and modernize ventilation with variable-speed fans in the BLDC fan market. In homes, BLDC ceiling fans respond to higher tariff environments and long runtimes with lower wattage and quieter operation, and mandatory labeling in markets like India strengthens value communication to buyers. Urban adoption is reinforced by smart features, voice assistants, and app ecosystems that add convenience and usage analytics over the product life. Commercial building demand revolves around IAQ and code compliance under ASHRAE 62.1 and energy targets, where FEI-aligned EC fans enable demand control and data for verification. Together, these uses advance BLDC penetration based on transparent performance and controllability advantages.

In industrial and warehouse settings, destratification, comfort, and ventilation standards drive deployment of HVLS and large EC fans with integrated controls and diagnostics that support uptime and safety outcomes. Logistics hubs and manufacturing floors are key users where consistent airflow and low noise enhance productivity, and specification decisions now include digital protocol compatibility and integration with BMS. Data centers and electronics cooling emphasize high reliability, modular replacement, and telemetry, which pushes suppliers to publish MTBF figures, conformal coating practices, and compatible connectors while aligning with thermal design changes at the rack and row level. Automotive thermal subsystems continue to expand BLDC use in cabin airflow and battery-pack cooling due to precise control and low noise, which complements broader electrification trends in vehicles. Across applications, the BLDC fan market integrates energy savings with digital features and service operations in ways that deepen switching incentives relative to induction systems.

By Distribution Channel: Offline Persists on Service, Online Scales Through D2C

Offline retail held 75.25% share in 2025 and remains essential to delivery, installation, and warranty resolution for residential and small commercial purchases, while online and D2C channels grow the fastest at 15.52% CAGR by leveraging content, reviews, and direct engagement in the BLDC fan market. Dealers provide immediate availability, bundled installation, and local service that reduce friction at the point of need, especially for replacement situations where speed matters. Commercial and industrial deals are even more offline-centric due to specification support, site surveys, and commissioning requirements that demand engineering input. As connected features spread, offline channels differentiate through commissioning validation and integration with BMS, which mitigates performance and warranty risks for buyers. This model supports the BLDC fan market size allocation to channels where service quality and compliance outcomes are part of the value proposition.

Online and D2C models excel at education, SKU breadth, configurability, and direct feedback loops that inform next-generation designs and software updates. Brands with focused offerings have built share by communicating energy savings and smart features clearly, and by using their online hubs to manage firmware and diagnostics over product life. The main online challenge is post-purchase fulfillment that includes installation, fast repairs, and commissioning checks in commercial contexts. Hybrid models that pair online selection with certified local installers continue to expand, especially in urban areas where service density supports quick turnaround. Over time, this blended approach should keep the BLDC fan market flexible across buyer preferences, while preserving the technical depth needed to deliver consistent performance.

Geography Analysis

Asia-Pacific held 45.75% share in 2025 and leads regional growth at 12.68% CAGR through 2031, with India’s high-usage households and mandatory labeling catalyzing BLDC upgrades and China’s commercial and industrial deployments aligning with broader electrification and IAQ goals in the BLDC fan market. In India, value communication around wattage and air delivery helps consumers weigh total ownership cost against premiums, while connected features and color choices win share in urban tiers. Southeast Asia presents varied adoption, from high BLDC penetration in Singapore’s commercial projects influenced by advanced green building rules to early-stage transitions in large, price-sensitive markets. Japan and Australia show a strong preference for quiet, clean, and connected ventilation in homes and small commercial sites, which underpins premium EC product lines. Across the Asia-Pacific region, standards, labeling, and power stability shape platform designs and marketing narratives in the BLDC fan market.

North America balances mature replacement volumes with high-value commercial and data center deployments that demand integrated controls, reliability, and FEI-aligned specifications. The federal withdrawal of a proposed fan efficiency rule in 2025 kept the regulatory vector at the state and local levels, with California’s appliance and building codes establishing baseline performance that guides national portfolios. ENERGY STAR criteria continue to shape ventilating fan performance goals, and BMS-led optimization in certified buildings lifts EC adoption. Data center ecosystems emphasize advanced thermal solutions and 48V-ready components, where BLDC fans with telemetry and modularity integrate best into next-generation power topologies. These factors keep North America a high-value deployment region within the BLDC fan market.

Europe’s share reflects smaller absolute volumes compared with Asia-Pacific but strong policy pull from ecodesign, high energy prices, and tightening building performance standards that favor EC solutions in both new builds and retrofits. The European Commission’s 2024 update on fans from 125W to 500kW directly raises the efficiency bar, with application in June 2026 and a significant electricity reduction target by 2030, which accelerates portfolio shifts to FEI-aligned systems. Markets like Germany and the UK have seen pronounced adoption in commercial ventilation and clean environments, where large EC centrifugal and axial fans with digital control are now the norm. UK case material demonstrates that BMS optimization combined with efficient fans can drive measurable energy and CO₂ reductions, validating longer-run economic outcomes for these investments. Southern and Eastern Europe advance more gradually due to climate and cost factors, but policy, labeling, and incentive structures continue to close gaps. Over the forecast period, Europe’s regulatory clarity and designers' familiarity with EC platforms support consistency in the BLDC fan market.

Competitive Landscape

Competition in residential categories is broad, with many brands competing on aesthetics, features, and price within a similar component ecosystem, while commercial and industrial segments show higher concentration around integrated players with motor and controls expertise plus service coverage. Asian consumer brands focus on design, quiet operation, and star-labeled energy performance in ceiling fans, and partnerships with leading voice assistants and app ecosystems are now common in the BLDC fan market. Premium entrants use distinctive industrial design and low-noise configurations to defend pricing power and brand equity. In commercial and industrial settings, European specialists emphasize AI-enabled optimization, platform modularity, and data-rich commissioning for HVAC and data center uses. Vendors with vertical integration in motors, magnets, drives, and now thermal modules can better manage input volatility and capture system-level margins. These factors create moderate fragmentation in residential with rising premium niches, and tighter competitive sets in commercial and industrial, where integration, service, and compliance rule specifications.

Strategic moves since 2024 show consistent investment in EC platforms, digital interfaces, and thermal systems that position fan suppliers as solution providers rather than commodity hardware vendors. Data center offerings highlight 48V-ready fans, sensor integration, and predictive maintenance features, often bundled with CDU infrastructure and digital twins for performance modeling. European manufacturers launched high-diameter axial and centrifugal EC fans with expanded diameter choices and firmware that interface with BMS and optimization platforms to produce measurable site-level savings. Japanese multinationals outlined R&D strategies that include intelligent power modules and next-generation motor drives that further improve fan system efficiency under tightening regional energy codes. Consumer-focused suppliers extended app-based control and acoustical improvements into mainstream product lines, which helps expand premium share where quietness and design are priced in. These moves maintain multi-segment traction for the BLDC fan market.

Looking ahead, white-space opportunities persist in drop-in EC retrofits for legacy HVAC units, harsh-environment designs with upgraded protection and explosion-proof ratings, and native DC products for DC microgrids and battery-backed sites. Retrofit kits that include mounting solutions, pre-programmed controllers, and clear commissioning documentation can unlock large installed bases at replacement intervals. Industrial environments demand higher ingress protection, coatings, and hazard compliance that not all general-purpose EC fans can meet, and specialist lines with these attributes can sustain price premiums. Markets exploring DC microgrids are ideal for DC-native BLDC fans that avoid conversion losses, and this match has particular relevance in regions with reliability challenges or distributed energy at the edge. Vendors that combine product, software, and service in outcomes-based packages stand to grow their share as performance guarantees proliferate in the BLDC fan market.

BLDC Fan Industry Leaders

Atomberg Technologies

Crompton Greaves Consumer

Havells India

Orient Electric

Nidec Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Panasonic Eco Systems announced its new Intelli-Balance Elite Energy Recovery Ventilator series at AHR Expo 2026, with units achieving 90% sensible recovery efficiency, addressing cold-climate operation and aligning with American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE) Standard 62.2.

- October 2025: Panasonic launched WhisperFit DC with Bluetooth speakers, combining premium audio with ENERGY STAR certified ventilation performance.

Global BLDC Fan Market Report Scope

| Ceiling Fans |

| Pedestal & Table Fans |

| Wall & Exhaust Fans |

| Industrial HVLS / Commercial Ventilation Fans |

| Inner-Rotor BLDC |

| Outer-Rotor BLDC (EC) |

| <30 W |

| 30 – 60 W |

| 60 – 120 W |

| >120 W |

| Residential |

| Commercial Buildings |

| Industrial / Warehouse |

| Data-Centre & Electronics Cooling |

| Automotive Cabin & Battery-Thermal |

| Offline Retail (Dealer / MBO) |

| Direct Institutional & OEM |

| Online (E-commerce & D2C) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (SG, MY, TH, ID, VN, PH) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Ceiling Fans | |

| Pedestal & Table Fans | ||

| Wall & Exhaust Fans | ||

| Industrial HVLS / Commercial Ventilation Fans | ||

| By Motor Architecture | Inner-Rotor BLDC | |

| Outer-Rotor BLDC (EC) | ||

| By Power Rating | <30 W | |

| 30 – 60 W | ||

| 60 – 120 W | ||

| >120 W | ||

| By Application | Residential | |

| Commercial Buildings | ||

| Industrial / Warehouse | ||

| Data-Centre & Electronics Cooling | ||

| Automotive Cabin & Battery-Thermal | ||

| By Distribution Channel | Offline Retail (Dealer / MBO) | |

| Direct Institutional & OEM | ||

| Online (E-commerce & D2C) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (SG, MY, TH, ID, VN, PH) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the BLDC fan market size in 2025 and what is the forecast by 2031?

The BLDC fan market size was USD 1.38 billion in 2025 and is forecast to reach USD 2.54 billion by 2031, reflecting a 10.8% CAGR during 2026-2031.

Which segments are growing the fastest within the BLDC fan market?

Industrial HVLS and commercial ventilation fans are the fastest-growing product segments at 11.95% CAGR, and the 60-120W power band is also expanding quickly at 13.69% CAGR to 2031.

Which region leads the BLDC fan market and how fast is it growing?

Asia-Pacific leads with 45.75% share in 2025 and is growing at 12.68% CAGR to 2031, supported by labeling policies and commercial IAQ priorities.

What are the main drivers of BLDC fan adoption in commercial buildings?

ASHRAE 62.1 ventilation standards, FEI-aligned specifications, and performance-focused certifications such as LEED v5 are driving EC fan uptake for variable-speed control and better IAQ.

How are data centers influencing demand in the BLDC fan market?

Data centers require high-reliability fans with precise control, telemetry, and compatibility with 48V DC architectures, which favors advanced BLDC platforms with integrated diagnostics.

Which sales channels will gain share in BLDC fans through 2031?

Online and D2C channels are growing fastest at 15.52% CAGR, while offline remains dominant due to installation, commissioning, and warranty services that support complex deployments.

Page last updated on: