Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

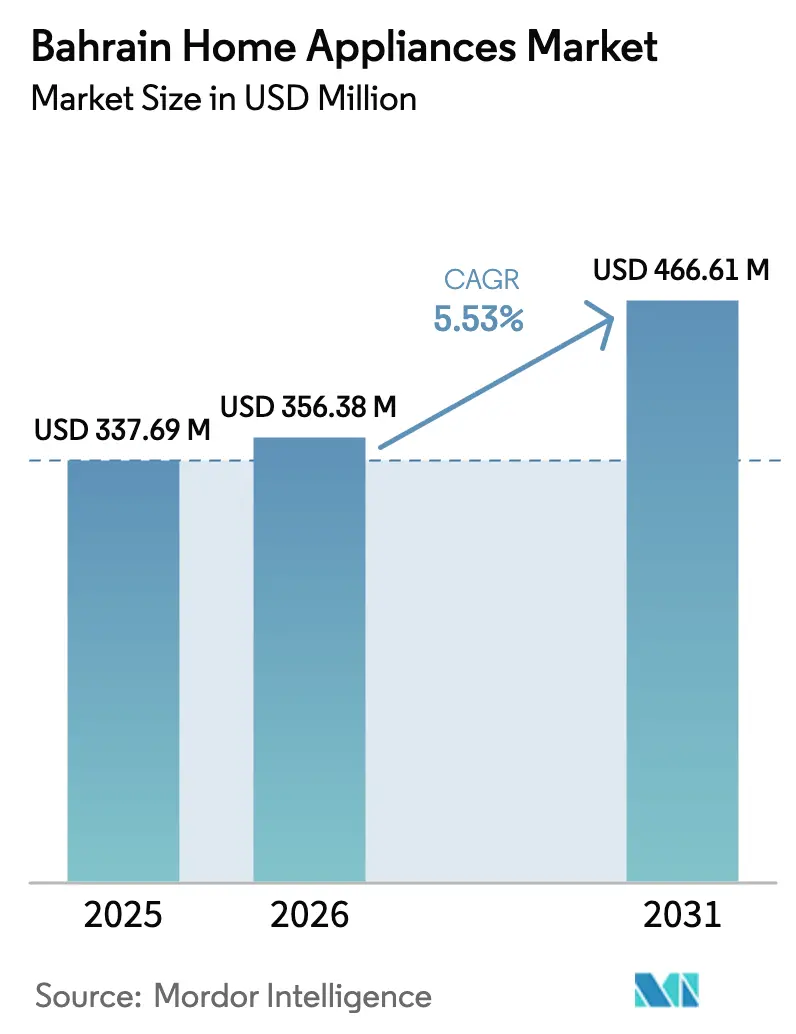

| Base Year Market Size (2025) | USD 337.69 Million |

| Market Size (2026) | USD 356.38 Million |

| Market Size (2031) | USD 466.61 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Home Appliances Market Analysis by Mordor Intelligence

The Bahrain home appliances market size in 2026 is estimated at USD 356.38 million, growing from 2025 value of USD 337.69 million with 2031 projections showing USD 466.61 million, growing at 5.53% CAGR over 2026-2031. Robust economic diversification, record inward investment, and pro-manufacturing incentives keep the Bahrain home appliances market on a steady growth path despite supply-chain cost shocks. Stellar summer temperatures lift cooling-product volumes while the Golden License program and the Made in Bahrain 35% local-content requirement create sound economics for regional assembly lines. High disposable income, premium home ownership growth, and a consumer pivot toward smart, energy-efficient appliances reinforce replacement and upgrade cycles. Multi-brand retail chains remain the main sales conduit, yet rapid e-commerce uptake—supported by next-day fulfilment and omnichannel price transparency—adds new momentum. Nevertheless, freight-rate volatility and semiconductor shortages squeeze importer margins and heighten price sensitivity.

Key Report Takeaways

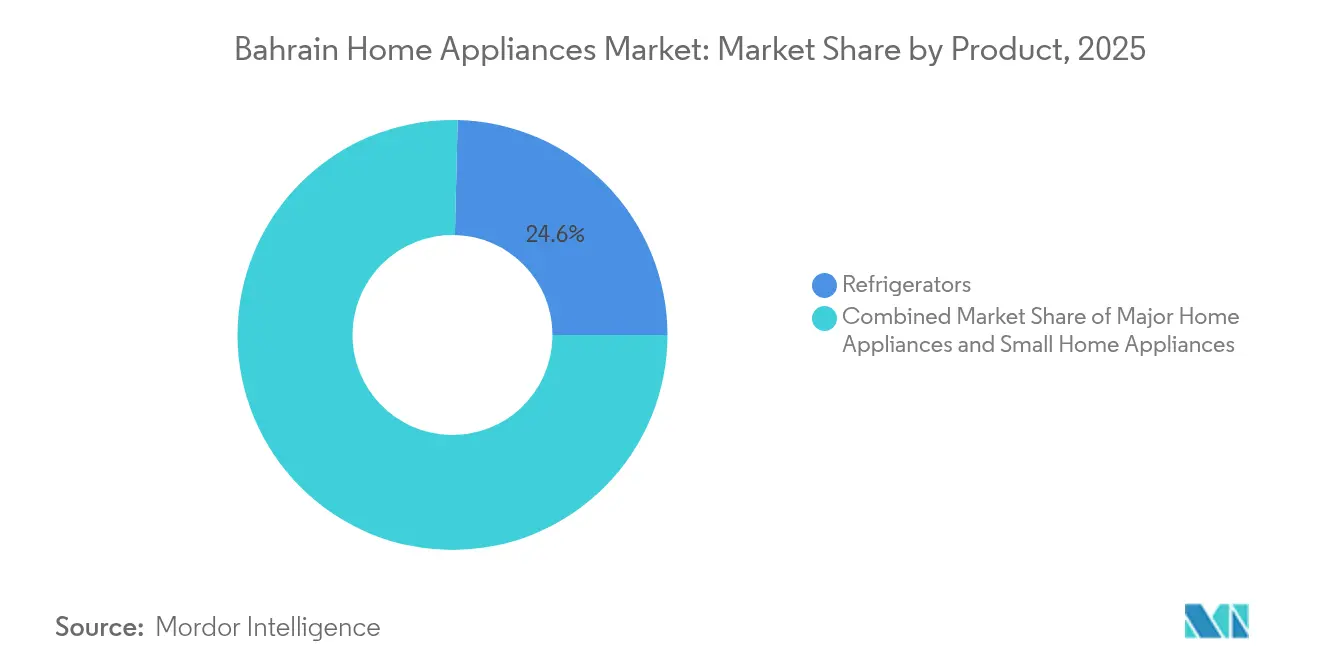

- By product category, refrigerators held 24.62% of the Bahrain home appliances market share in 2025, while air fryers are projected to advance at a 6.08% CAGR through 2031.

- By distribution channel, multi-brand stores accounted for 39.25% of the Bahrain home appliances market size in 2025; online channels are forecast to register a 6.44% CAGR between 2026-2031.

- By geography, the Capital Governorate commanded a 44.30% share of the Bahrain home appliances market size in 2025; the Northern Governorate is expected to post the fastest 5.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & housing growth | +1.2% | Capital and Muharraq Governorates | Medium term (2-4 years) |

| Rapid adoption of smart & connected devices | +0.9% | National, led by the Capital Governorate | Long term (≥ 4 years) |

| Expansion of modern retail | +0.8% | Urban centres nationwide | Short term (≤ 2 years) |

| Golden License–driven local assembly | +0.7% | National manufacturing zones | Medium term (2-4 years) |

| Solar-energy subsidies for high-efficiency AC | +0.6% | Residential sector nationwide | Long term (≥ 4 years) |

| Severe summer heat boosts cooling demand | +0.4% | Peak impact during May–September across all governorates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Housing Growth

Stronger non-oil GDP and active housing programs add fresh households that install full appliance suites within months of handover [1].Ministry of Housing and Urban Planning, “Housing Services Expansion Update 2025,” housing.gov.bh Premium income tiers are upgrading faster than the national average, which shortens replacement cycles and pushes retailers to stock higher-margin, feature-rich models. The six-month lag between housing starts and appliance purchases secures pipeline visibility for manufacturers. Higher earnings also soften the price penalty of energy-efficient SKUs, fuelling a premiumisation trend that underpins value growth across the Bahrain home appliances market.

Rapid Adoption of Smart & Connected Appliances

Strong nationwide 5G coverage and competitive data tariffs make always-on connectivity seamless for consumers. Samsung’s AI-enabled refrigerators and washers, launched in 2025, allow predictive maintenance alerts that pre-empt costly cooling failures during peak summer, cementing brand loyalty [2]Samsung Electronics, “Samsung SmartThings Energy Launch,” samsung.com. BSH’s Matter-ready ovens deepen cross-platform compatibility, removing ecosystem lock-in and encouraging broader uptake among tech-savvy households[3]BSH Hausgeräte GmbH, “Annual Report 2024,” bsh-group.com. As a result, smart SKUs command a widening price premium yet still outpace volume growth, lifting total revenue in the Bahrain home appliances market.

Expansion of Modern Retail (Hypermarkets & Online)

New hypermarkets offer shoppers live demos, bundle discounts, and instant pick-up that drive conversion. Lulu Group’s 70% year-over-year e-commerce surge in FY 2024 proves that convenience trumps legacy store loyalty when returns are friction-free and installation slots can be booked online [4]Lulu Group International, “Financial Highlights FY 2024,” lulugroupinternational.com. Retailers deploy predictive inventory algorithms to maintain optimal stock levels during summer air-conditioner peaks. Seamless click-and-collect services reduce last-mile costs and consolidate the Bahrain home appliances market’s multichannel future.

Golden License Spurring Local Assembly

Under the Golden License, appliance makers obtain accelerated permits, tax holidays, and 100% foreign ownership, lowering landed costs by 8%-10% and cutting delivery lead times from six weeks to four days. Local content quotas stimulate regional component sourcing and nurture a budding parts cluster. Manufacturers also gain preferential access to government procurement, enlarging addressable volume. The program reduces currency-volatility exposure for importers and keeps pricing stable for the Bahrain home appliances market during freight spikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global supply-chain volatility (freight & chips) | -0.8% | Global, affecting all import-dependent markets | Short term (≤ 2 years) |

| High import dependency | -0.6% | National, affecting all product categories | Medium term (2-4 years) |

| Intense price competition | -0.4% | National, concentrated in mass-market segments | Short term (≤ 2 years) |

| Water-scarcity rules limiting high-usage dishwashers | -0.3% | National, residential sector focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Dependency

Heavy reliance on Asian suppliers concentrates risk in a handful of trade lanes, so a regional disruption—or an adverse tariff decision—can leave showrooms empty for weeks. Volatile commodity costs for steel and copper move straight into landed prices because local value-addition is limited. The Golden License and Made in Bahrain schemes seek to localise assembly, but component ecosystems take years to mature, meaning import exposure will remain high through the medium term. Until meaningful localisation occurs, currency shifts against the US dollar and renminbi will keep retail pricing unpredictable for the Bahrain home appliances market.

Water-Scarcity Rules Limiting High-Usage Dishwashers

Escalating block tariffs on household water make traditional dishwashers less attractive. New regulatory drafts propose a maximum of 9 litres per standard cycle, forcing R&D to spend on ultra-efficient jets and filtration. Without product upgrades, consumer adoption stays muted, capping category contribution to the Bahrain home appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Lead Amid Air-Fryer Momentum

Refrigerators generated 24.62% of 2025 revenue, anchored in an essential need to keep perishables fresh under 40°C summer peaks. High-end, inverter-compressor models with smart diagnostics now outsell conventional units by 2:1 in major urban chains. At the same time, air fryers post the fastest 6.08% CAGR, helped by compact kitchens and health-oriented diets that pivot away from deep-frying. Midea, Philips, and Black+Decker each introduced dual-zone fryers in 2025, intensifying price wars yet expanding the overall Bahrain home appliances market. Washing machines sustain mid-single-digit growth, while dishwashers remain niche under water-tariff pressure. Air conditioners, second only to refrigerators in value, benefit from solar-subsidy induced upgrades to variable-speed compressors. Small appliances such as coffee makers, blenders, and robot vacuums rise in tandem with lifestyle upgrades, adding breadth to product-mix depth.

Ovens and microwave-oven combos witness renewed interest as consumer cooking behaviour blends quick-service convenience with home-made nutrition. LG’s InstaView and Haier’s AI-bake functions entice premium customers willing to pay 20% more for connected features. Haier’s success in upscale refrigeration reveals the potency of AI-centric differentiation. Across categories, manufacturers tailor Gulf-grade specifications such as reinforced compressor coils and anti-sand filtration, raising perceived durability and reinforcing loyalty in the Bahrain home appliances market.

By Distribution Channel: Multi-Brand Stores Hold Scale, Online Gains Speed

Multi-brand showrooms captured 39.25% of 2025 sales, offering one-stop comparison shopping and immediate pick-up, critical for bulkier goods that buyers prefer to inspect physically. These outlets rely on advanced ERP systems to adjust stock based on rolling 12-week demand forecasts, thus avoiding out-of-stock penalties in the Bahrain home appliances market. In parallel, the online arena is registering a robust 6.44% CAGR. Lulu’s app features real-time delivery slots and price-match guarantees that win trust among younger demographics. Check-out conversion rates climb when shoppers can bundle extended warranties and installation in a single click.

Exclusive brand outlets keep a loyal clientele via experiential displays, free design consultation, and same-day service response. Landmark Group’s USD 1 billion omnichannel expansion will introduce showroom-plus-digital formats in underserviced neighbourhoods, further reshaping channel mix. Traditional dealers remain relevant in rural pockets but lose share each year as urbanisation accelerates and smartphone penetration pushes consumers toward digital price discovery, deepening the Bahrain home appliances market transformation.

Geography Analysis

The Capital Governorate delivered 44.30% of national revenue in 2025 on the back of high per-capita income and dense premium retail footprints along Manama’s commercial corridors. Luxury apartment towers and bespoke villas generate sizeable contract orders for built-in refrigerators, smart ovens, and connected washers. Strong after-sales service networks shorten repair lead times to under 48 hours, favouring repeat purchases within the Bahrain home appliances market. Retailers pilot experiential zones that display solar-ready HVAC and voice-controlled kitchen suites, creating high-margin upsell opportunities ita.gov.

Northern Governorate, the fastest-expanding pocket, is slated to clock a 5.58% CAGR through 2031 as large master-planned communities—such as Salman Town—reach occupancy. Younger family profiles prize multi-function cookers and app-controlled vacuum robots, reinforcing volume growth. Retail majors have earmarked six new hypermarkets and dedicated click-and-collect hubs to meet swelling demand. The governorate’s expanding 10 Gbit fibre network underpins reliable smart-home connectivity, a prerequisite for advanced SKUs in the Bahrain home appliances market.

Muharraq Governorate rides a stable replacement demand linked to airport-driven commerce and hospitality refurbishments. Southern Governorate, with its industrial clusters, prefers rugged, value-priced appliances yet benefits from logistics efficiencies—central warehouses in the Capital can deliver within two hours, minimising last-mile cost. Bahrain’s compact landmass enables centralised distribution to supply all four governorates seamlessly, smoothing inventory imbalances and reinforcing competitive pricing discipline in the Bahrain home appliances market.

Competitive Landscape

Competitive rivalry is moderate. Samsung drives AI-tier leadership with on-device learning algorithms that improve chill-cycle efficiency, while LG stakes ground in health-oriented filter technology that claims 99% airborne pathogen reduction. BSH leverages German engineering credentials, dedicating 5.5% of revenue to R&D and launching Matter-compliant lines that foster ecosystem neutrality. Chinese entrants—Haier, Midea, TCL—keep eroding price points through vertically integrated factories and regional assembly tie-ups, including TCL’s 2024 partnership with Jashanmal to roll out inverter air conditioners in Bahrain and neighbouring states.

Local assembly, though nascent, is a defining differentiator: a Middle East-made washing machine reaches Bahrain shop floors four days after order confirmation compared with six weeks for imported stock. Brand equity further hinges on after-sales excellence. Lulu’s service centre promises a two-hour response within Manama, prompting rivals to outsource to third-party technicians. Sustainability credentials—PVC-free insulation, halogen-free circuit boards—are now core marketing hooks, echoing Vision 2030 imperatives and swaying environmentally conscious buyers in the Bahrain home appliances market.

Strategic manoeuvres in 2025 highlight the race for data-driven consumer intimacy:

- Samsung integrates its SmartThings Energy dashboard into new refrigerators, offering real-time consumption analytics;

- LG pilots a subscription model for water-purifier filters bundled with annual air-conditioner servicing;

Emerging disruptors like Dubai-based Barq ship micro-batch designer kettles direct to Bahraini consumers, proving that niche players can still carve profitable pockets in the Bahrain home appliances market.

Bahrain Home Appliances Industry Leaders

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Whirlpool Corporation

Hitachi, Ltd.

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Haier Smart Home reported Q1 2025 revenue of RMB 79.12 billion, noting 12.6% overseas growth, with a 64% share in high-end refrigeration models haier.com

- February 2025: Lulu Retail logged FY 2024 sales of USD 7.6 billion, opened 21 new stores and recorded 70% e-commerce growth.

- January 2025: Samsung Electronics rolled out an AI-centric appliance roadmap aiming to lift 2025 home-appliance revenue by mid-single digits samsung.com

- December 2024: KBN Group and Whirlpool crossed 50,000 appliance units in Qatar’s B2B projects, signalling scope for B2C expansion across the Gulf.

- November 2024: Landmark Group announced a USD 1 billion plan to build 400 stores across the Gulf, India, and Southeast Asia.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Bahrain home appliances market as all newly sold major and small household devices, including refrigerators, freezers, washing machines, ovens, air-conditioners, coffee makers, blenders, air fryers, and vacuum cleaners, distributed through offline and online channels to residential and light-commercial users within the four governorates. We track value generated from first-time equipment sales only; aftermarket parts, repair services, and consumer electronics such as televisions remain outside scope.

Scope exclusion: refurbished or gray-market imports are not modeled to avoid double counting.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Capital Governorate

- Muharraq Governorate

- Northern Governorate

- Southern Governorate

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance importers, leading retailers, and HVAC installers across Manama, Riffa, and Muharraq, while short online surveys captured buying frequency and average selling prices from household decision-makers. These conversations verified secondary assumptions, filled gaps on channel margins, and anchored uptake rates for smart, inverter-based models.

Desk Research

We began by mapping Bahrain's appliance demand against macro signals drawn from publicly available sources such as the Information & eGovernment Authority's household expenditure survey, Central Bank of Bahrain inflation releases, UN COMTRADE import codes 8418-8450, and GCC Customs tariff books. Trade association insights from the Gulf Organization for Industrial Consulting and appliance energy-label registration data from Bahrain's Sustainable Energy Authority helped clarify product mix shifts toward high-efficiency units. Company 10-Ks, distributor presentations, and reputable press articles rounded out brand-level pricing and channel developments. To validate firm financials and shipment splits, we tapped D&B Hoovers and news archives on Dow Jones Factiva. The sources listed here are illustrative; many additional datasets informed intermediate checks and clarifications.

A second sweep covered regional housing completions, consumer sentiment, and summer cooling degree-days, giving our analysts the contextual variables needed to scale demand pools over time.

Market-Sizing & Forecasting

We reconstructed 2024 sales using a top-down import-reexport reconciliation, which was then sense-checked through sampled average selling price x unit volume roll-ups shared by five retailers. Key model drivers include new housing handovers, disposable income per capita, average unit price inflation, retailer floor-space additions, and mean July-August temperature anomalies that influence cooling appliance penetration. Forecasts to 2030 deploy multivariate regression blended with ARIMA overlays, allowing scenario tweaks when primary experts flag policy or supply-chain shocks. Bottom-up gaps, such as unreported direct factory shipments, are bridged by proportional allocation from known distributor shares before final totals are locked.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review that flags deviations versus historic elasticities, regional shipment benchmarks, and customs tallies. We refresh every twelve months, and we trigger unscheduled updates when material events, such as currency shifts, subsidy changes, or import bans, occur. A final analyst sweep just before publication ensures clients always receive the latest view.

Why Mordor's Bahrain Home Appliances Baseline Commands Reliability

Published figures often diverge because firms pick different product baskets, pricing bases, and refresh cadences.

Key gap drivers emerge when one publisher treats only 'white goods,' another folds in small gadgets, and a third annualizes 2023 prices without local inflation adjustments; methodology depth and update frequency also vary.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 337.69 M (2025) | Mordor Intelligence | - |

| USD 328 M (2024) | Regional Consultancy A | Excludes small appliances; rolls forward prior-year ASP without Bahrain-specific inflation |

| USD 276.10 M (2024) | Trade Journal B | Covers only white goods; omits online sales channel and Capital Governorate specialty outlets |

The comparison shows how scope choices and price assumptions swing totals by up to USD 60 million. By grounding estimates in verified customs data, timely price audits, and clearly stated inclusions, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the Bahrain home appliances market?

It reached USD 356.38 million in 2026 and is forecast to hit USD 466.61 million by 2031 at a 5.53% CAGR.

Which product category generates the most revenue?

Refrigerators lead with a 24.62% 2025 share because food preservation is critical in Bahrain’s extreme heat.

How fast is online appliance retail growing?

Online channels are expanding at a 6.44% CAGR, helped by 70% year-over-year e-commerce gains at Lulu Group.

Why are manufacturers setting up local assembly in Bahrain?

The Golden License grants tax breaks and fast-track permits, trimming landed costs by up to 10% and cutting delivery lead times to days.

Which governorate is the fastest-growing appliance market?

Northern Governorate is projected to grow 5.58% annually through 2031 on the back of large housing projects.

How do water-scarcity rules affect dishwasher sales?

Higher block tariffs and upcoming efficiency standards curb demand for traditional dishwashers, keeping the category niche unless ultra-efficient models become mainstream.

Page last updated on: