Background Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

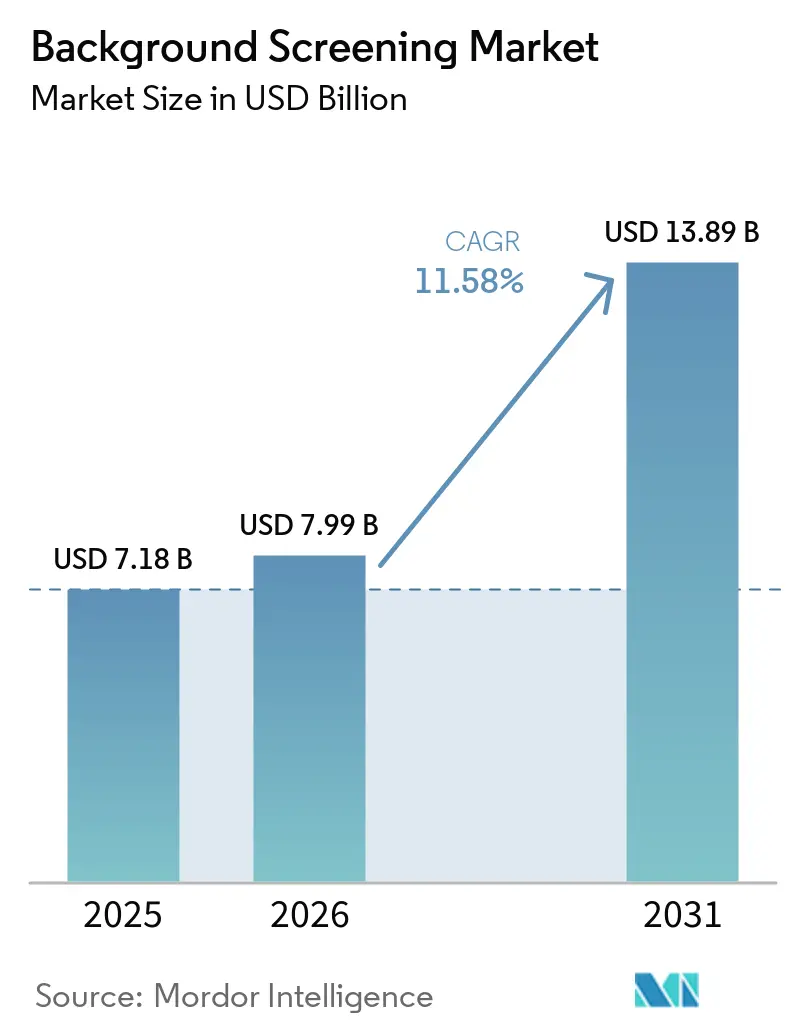

| Market Size (2026) | USD 7.99 Billion |

| Market Size (2031) | USD 13.89 Billion |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Background Screening Market Analysis by Mordor Intelligence

The Background Screening Market size is projected to expand from USD 7.18 billion in 2025 and USD 7.99 billion in 2026 to USD 13.89 billion by 2031, registering a CAGR of 11.58% between 2026 to 2031.

Growth reflects tighter global regulations, rising cross-border hiring, and widespread cloud adoption that lowers implementation friction. Companies extend pre-hire checks into recurring, post-hire monitoring that mitigates brand and safety risks while satisfying evolving data-protection mandates. Technology investment concentrates on artificial intelligence for pattern recognition, blockchain for tamper-proof credentials, and multilingual verification engines that simplify complex regional compliance. Competitive intensity rises as private equity capital funds M&A aimed at product breadth and geographic reach; meanwhile, niche specialists remain relevant where local data fragmentation demands deep expertise. Organizations continue to pivot toward integrated platforms rather than point solutions, favoring vendors that embed screening within existing HR ecosystems and deliver analytics that guide risk-based hiring decisions.

Key Report Takeaways

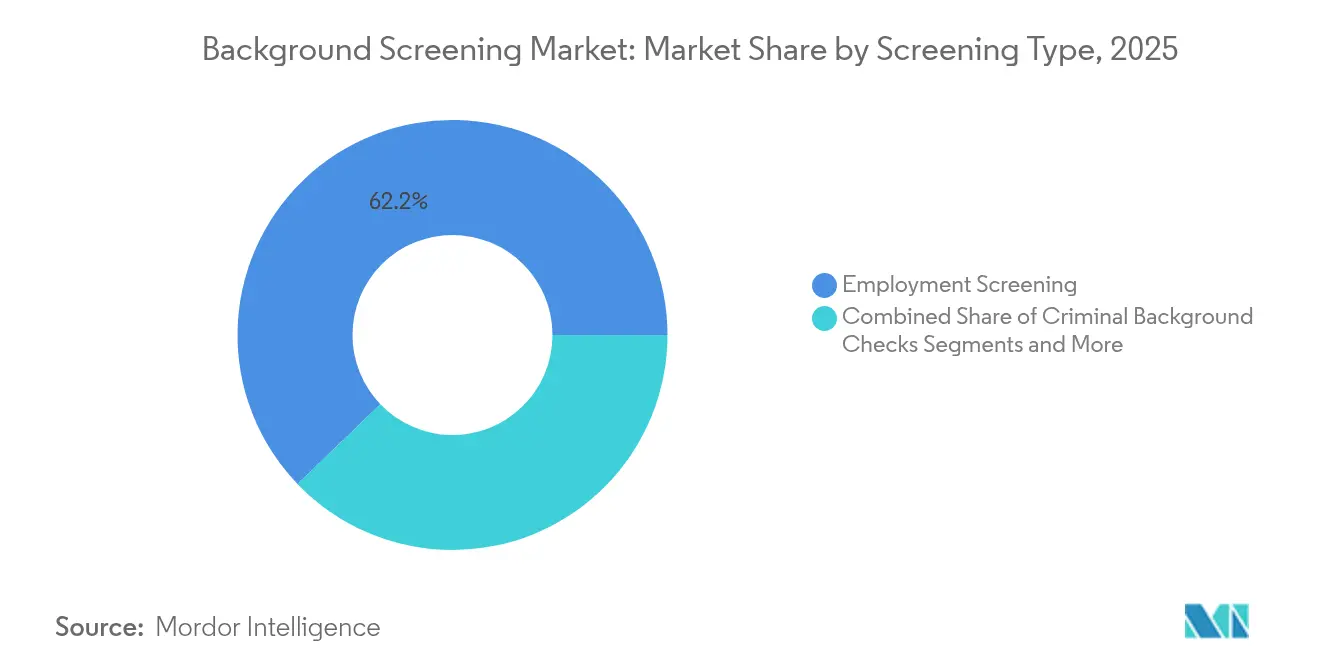

- By screening type, employment verification held 62.18% of background screening market share in 2025, while criminal checks are forecast to advance at a 11.78% CAGR through 2031.

- By deployment, cloud captured 71.05% of the background screening market size in 2025 and is projected to grow at a 11.95% CAGR to 2031.

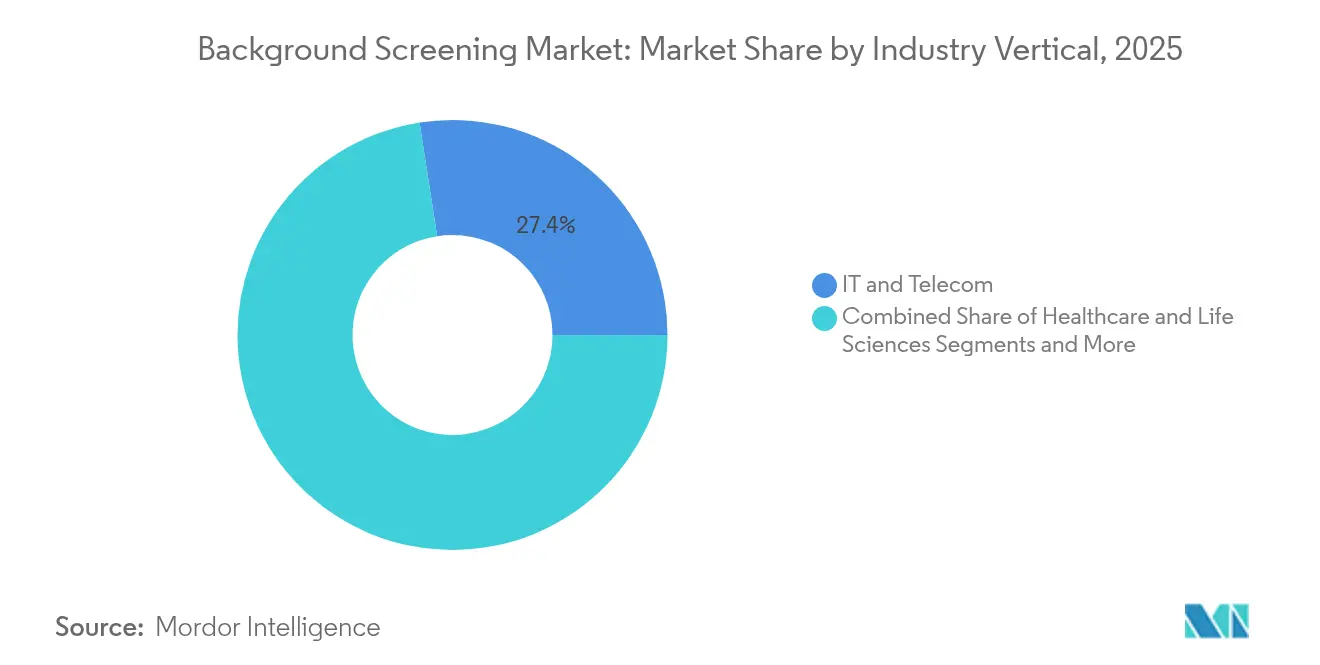

- By industry vertical, IT and telecom led with 27.45% revenue share in 2025; gig-platforms and shared mobility are set to expand at a 12.05% CAGR to 2031.

- By organization size, large enterprises commanded 67.20% of the background screening market size in 2025, while SMEs registered the fastest 12.34% CAGR through 2031.

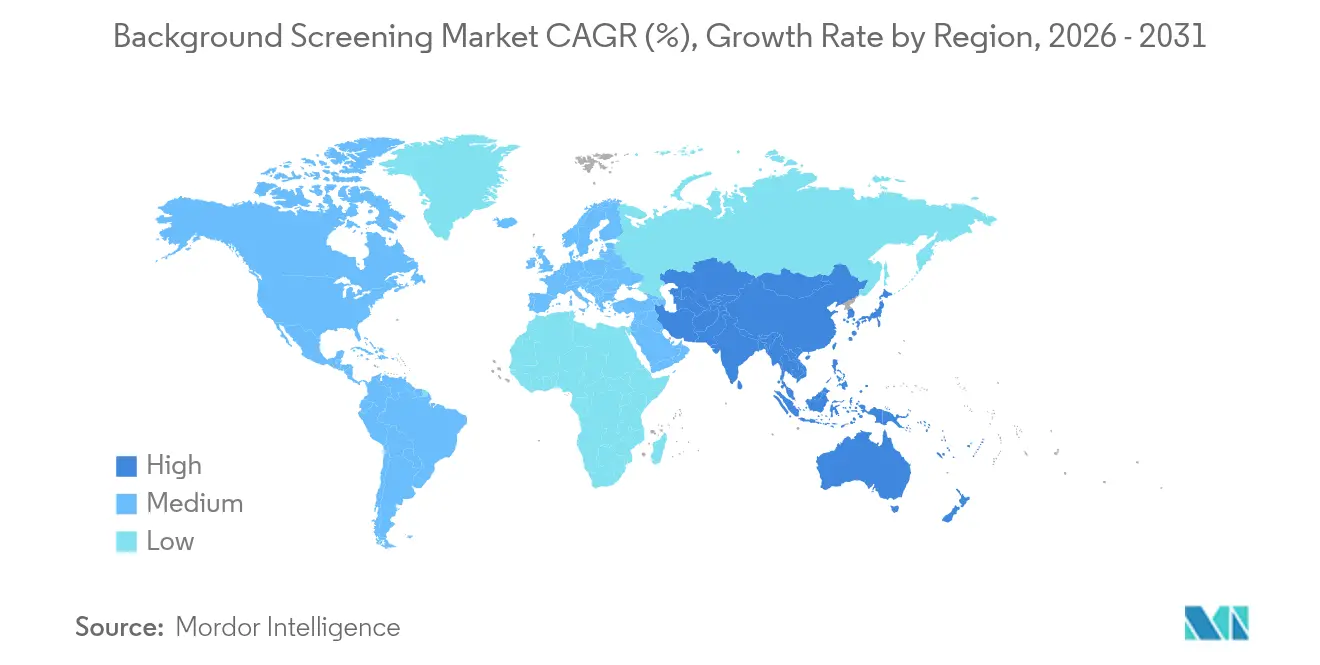

- Regional comparison shows North America accounting for 43.60% of the background screening market share in 2025, with Asia Pacific pacing growth at 12.30% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Background Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gig-economy growth boosting high-frequency re-screenings in North America | +2.1% | North America, spill-over to Asia-Pacific | Medium term (2-4 years) |

| EU whistle-blower directive accelerating criminal and credit checks across Europe | +1.8% | Europe, regulatory influence on global standards | Short term (≤ 2 years) |

| ASEAN cross-border hiring fuelling multilingual verifications | +1.5% | ASEAN core, expansion to broader Asia-Pacific | Medium term (2-4 years) |

| AI-driven continuous monitoring reducing post-hire risk for healthcare providers | +1.3% | Global, with early adoption in North America and EU | Long term (≥ 4 years) |

| Blockchain credential wallets enabling instant education verification | +0.9% | Global, pilot programs in developed markets | Long term (≥ 4 years) |

| Data-localization mandates spurring regional data-centre investments | +1.2% | MEA, Asia-Pacific, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gig-economy growth boosting high-frequency re-screenings in North America

Gig platforms embed monthly automated checks that cover county criminal records and sex-offender registries, enabling real-time risk decisions for drivers and delivery personnel.[1]Checkr, “Continuous Crim, Ongoing Background Checks,” checkr.com Continuous protocols improve customer confidence for on-demand services, reduce liability exposure, and extend into healthcare staffing, where rotating clinicians require perpetual credential validation. Vendors leverage API-driven workflows that integrate with scheduling apps, ensuring compliance without added friction. As gig-work penetration rises, this driver elevates the addressable background screening market and accelerates platform revenue tied to recurring transactions

EU whistle-blower directive accelerating criminal and credit checks across Europe

The 2023/24 directive compels companies to protect whistle-blowers, prompting deeper vetting for finance, compliance, and audit roles. Parallel GDPR obligations demand strict consent controls, spurring demand for specialized European-hosted solutions that reconcile thorough checks with data minimization principles.[2]Morrison Foerster, “Shielding Your Company: Best Practices for Background Checks,” mofo.com Financial services institutions lead adoption as they overlay whistle-blower safeguards onto existing AML frameworks. Multinationals then export these elevated standards to global subsidiaries, amplifying the driver’s influence beyond Europe.

ASEAN cross-border hiring fueling multilingual verifications

Singapore’s COMPASS framework introduces skills-based eligibility, requiring authentication of foreign education, employment, and criminal records across 10+ languages. [3]HireRight, “Adapting to Change: Building a Futureproof Background Screening Strategy,” hireright.com Providers respond by building regional hubs, deploying OCR tuned to country-specific document formats, and partnering with local data sources in Thailand, Malaysia, and Indonesia. The capability gap among legacy vendors creates white-space for specialists and lifts the background screening market as intra-ASEAN labor mobility accelerates.

Blockchain credential wallets enabling instant education verification

Pilot programs allow universities to issue tamper-proof digital diplomas stored in candidate-controlled wallets. Employers can confirm authenticity in seconds, slashing verification turnaround times. Early adopters in the United States, Europe, and Australia validate feasibility; broader rollout hinges on interoperability standards. While incremental today, blockchain wallets promise structural efficiency gains that broaden the background screening market over the long haul.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented judiciary data inflating TAT and cost | –1.4% | LATAM core; multinational impact | Medium term (2-4 years) |

| Stringent GDPR consent rules limiting depth of checks | –0.8% | Europe; global spill-over | Short term (≤2 years) |

| False positives in algorithmic name-matching | –0.6% | MEA and Asia-Pacific markets | Medium term (2-4 years) |

| Rising applicant-fraud sophistication vs legacy tech | –1.1% | Global; higher in digital-first markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented judiciary data in LATAM inflating TAT and cost

Brazil’s courts trial AI for docket backlogs, yet screening firms still face inconsistent digitization, manual record retrieval, and language barriers that yield 50-65% completion rates versus 85-90% in developed regions. Providers must hire local agents, extend service-level agreements, and budget higher fees, suppressing profitability and slowing client adoption.

Stringent GDPR consent rules limiting depth of EU checks

Explicit consent, purpose limitation, and data-minimization clauses restrict permissible queries, trimming accessible criminal and credit data. Multinationals adjust by narrowing screening scopes, which tempers revenue growth in the European slice of the background screening market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screening Type: Employment verification dominance with criminal check surge

Employment verification generated the largest revenue, accounting for 62.18% of background screening market share in 2025. The driver stems from increasingly mobile career paths that necessitate rigorous, multi-jurisdiction employment history confirmation. Conversely, criminal background checks post the fastest 11.78% CAGR, reflecting heightened security mandates across gig-economy, financial services, and healthcare roles. Integrated platforms now bundle education, credit, and drug testing to lower client onboarding friction. AI-assisted adjudication engines flag only materially relevant offenses, aligning with “clean-slate” law compliance. The combined functionality enlarges the addressable background screening market and spurs recurrent revenue models anchored in continuous monitoring.

Emerging adoption of blockchain-verified diplomas compresses turnaround times for education checks, redirecting provider focus toward data analytics that interpret credential relevance. Credit and financial checks apply alternative data such as utility-payment histories, improving inclusion for under-banked applicants within ASEAN and MEA. Drug and health testing shifts from pre-hire snapshots to recurring assessments tied to safety-sensitive scheduling, further expanding the background screening market size at the segment level.

By Deployment: Cloud solutions accelerate digital transformation

Cloud captured 71.05% of background screening market size in 2025 and retains top-line momentum with a 11.95% CAGR to 2031. SaaS-based workflow engines deliver API connectivity into HRIS, ATS, and payroll platforms, enabling same-day program rollouts for distributed teams. Configurable compliance templates simplify regional rule administration, a capability valued by multinationals pursuing talent arbitrage strategies.

On-premises installations persist in defense, critical infrastructure, and certain banking environments where data-sovereignty trumps speed. Even so, many organizations adopt hybrid architectures: sensitive disclosure forms reside behind corporate firewalls while standard verifications execute on accredited cloud nodes. This flexibility sustains overall background screening market demand across diverse regulatory settings.

By Industry Vertical: IT sector leadership challenged by gig-platform growth

IT and telecom contributed 27.45% of 2025 global revenue, driven by cybersecurity compliance and privileged-access risk. Yet gig-platforms and shared mobility post the leading 12.05% CAGR through 2031 as continuous criminal and motor-vehicle record checks become standard for rideshare and delivery workers. BFSI shows notable expansion amid Know-Your-Employee (KYE) mandates: background check discrepancies in India’s BFSI segment rose 18.1% year-on-year, prompting broader vendor engagement. Healthcare intensifies use of sanctions and license monitoring, accelerated by the New Jersey statute referenced earlier.

Government, defense, and education settings evolve policy frameworks—California’s AB2534 tightens teacher verification rules. Manufacturing and energy sectors align drug-testing frequencies with changing cannabis legislation, feeding incremental revenue into the background screening market.

By Organization Size: SME growth outpaces enterprise expansion

Enterprises with >5,000 staff continued to command 67.20% of 2025 revenue, yet SME demand expands fastest at 12.34% CAGR on the back of affordable, subscription-priced bundles. HireRight’s April 2025 acquisition of ClearChecks exemplifies the strategic push into simplified, SME-oriented product lines. Integrated onboarding suites that include background screening as a pre-configured module help smaller firms meet client and regulatory expectations without heavy IT lift, broadening total background screening market penetration.

Geography Analysis

North America generated 43.60% of 2025 revenue, anchored by FCRA obligations, state clean-slate laws, and healthcare staffing expansions. The FDIC’s revised Fair Hiring in Banking Act (effective October 2024) further extends mandatory vetting for covered positions. State-level privacy statutes in Oregon, Texas, and Florida prompt platform updates that blend consent flows with candidate experience. Cannabis law divergence pushes employers toward nuanced drug-testing policies supported by consultative screening providers.

Asia Pacific records the highest 12.30% CAGR, fueled by digital-first governmental programs and intra-ASEAN labor mobility. Singapore’s COMPASS mandates trigger skills-centric verifications; India’s Digital Personal Data Protection Act introduces cross-border data-transfer obligations; and Australia’s SOCI Act tightens vendor vetting for critical-infrastructure work. Providers that invest in in-country data nodes and language-aware algorithms capitalize on widening talent flows and grow their regional background screening market share. Europe exhibits moderate expansion constrained by GDPR consent complexity, though high-value industries—including financial services—drive specialist demand. In the Middle East, the UAE and Saudi Arabia embrace data-protection frameworks aligned with GDPR but combine them with aggressive economic diversification agendas, boosting screening volumes for expatriate roles. Latin America’s fragmented judiciary landscape hampers growth; nevertheless, modernization initiatives in Brazil and Mexico create pockets of opportunity for regional specialists that grasp nuanced compliance regimes.

Competitive Landscape

Acquisition-led consolidation reshapes competitive dynamics. First Advantage’s USD 2.2 billion purchase of Sterling Check in October 2024 created a USD 1.5 billion pro-forma entity poised to unlock USD 50-70 million in annual synergies for investors.. The deal expands global reach, reinforces AI R&D funding, and deepens vertical specialization. Private equity accelerates the trend: General Atlantic and Stone Point Capital’s USD 1.7 billion take-private of HireRight (July 2024) injects fresh capital for platform modernization and bolt-on deals.

Checkr’s acquisition of Truework brings income and employment verification in-house, facilitating an end-to-end data ecosystem that boosts upsell capacity among gig-platform clients. Accurate Background’s June 2024 purchase of Orange Tree further consolidates mid-market share while adding healthcare expertise. Competitive differentiation increasingly centers

Background Screening Industry Leaders

HireRight Holdings Corp.

First Advantage Corp.

Sterling Check Corp.

Checkr Inc.

Accurate Background LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Certn partnered with RemotePass to streamline global team onboarding, integrating background screening into employment lifecycle management.

- April 2025: HireRight acquired ClearChecks to extend simplified screening packages for SMEs, targeting high-growth lower-mid-market customers.

- February 2025: First Advantage projected 2025 revenue of USD 1.5–1.6 billion after Sterling integration, citing USD 60–70 million synergy capture.

- January 2025: Ernst & Young launched VerifyEmployment, enabling employers to self-manage income verification while protecting data privacy.

Global Background Screening Market Report Scope

A background screening is the process of using third-parties (usually professional background screening providers) to properly vet candidates for career opportunities. Sources may include public records, law enforcement, credit bureaus and previous employers.

The background screening market is segmented by type (employment screening, tenant screening, criminal background checks, education verification, other types), by deployment (cloud, on-premises), by end-user (IT and telecom, healthcare, education, government, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Employment Screening |

| Criminal Background Checks |

| Education and Credential Verification |

| Credit and Financial Checks |

| Drug and Health Testing |

| Tenant and Property Screening |

| Cloud |

| On-Premises |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Government and Defense |

| Education |

| Manufacturing and Energy |

| Gig-platforms and Shared Mobility |

| Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Screening Type | Employment Screening | ||

| Criminal Background Checks | |||

| Education and Credential Verification | |||

| Credit and Financial Checks | |||

| Drug and Health Testing | |||

| Tenant and Property Screening | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| By Industry Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Education | |||

| Manufacturing and Energy | |||

| Gig-platforms and Shared Mobility | |||

| By Organization Size | Large Enterprises | ||

| Small and Mid-sized Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Nordics (Denmark, Sweden, Norway, Finland) | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected growth rate for the background screening market to 2031?

The market is forecast to grow at an 11.58% CAGR, reaching USD 13.88 billion by 2031.

Which screening type is expanding most quickly?

Criminal background checks lead with a 11.78% CAGR due to stronger security mandates across industries.

Why are SMEs adopting screening services faster than large enterprises?

Subscription-based cloud platforms lower cost and complexity, giving SMEs access to enterprise-grade verification at a 12.34% CAGR growth pace.

How do data-localization laws influence provider strategy?

Vendors invest in regional data centers to comply with sovereignty rules in MEA and APAC, using local infrastructure as a competitive differentiator.

Page last updated on: