Market Overview

| Study Period | 2019 - 2030 |

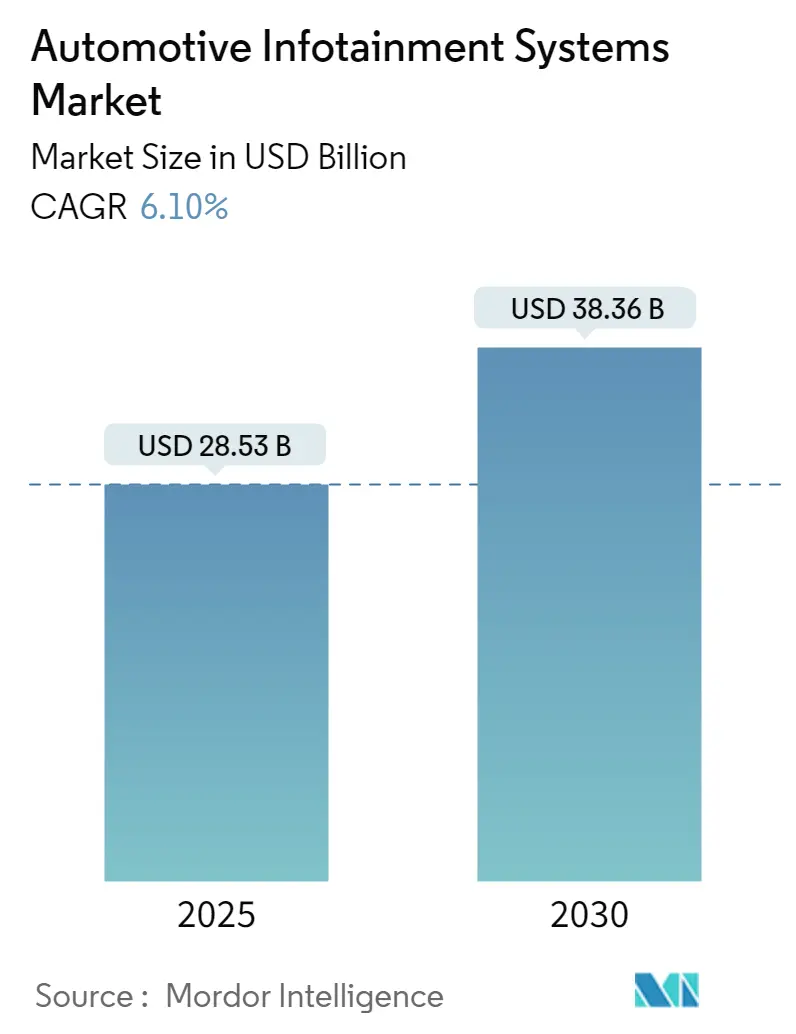

| Market Size (2025) | USD 28.53 Billion |

| Market Size (2030) | USD 38.36 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Infotainment Systems Market Analysis by Mordor Intelligence

The global automotive infotainment systems market reached USD 28.53 billion in 2025 and is projected to expand to USD 38.36 billion by 2030, registering a compound annual CAGR of 6.10% during the forecast period. This growth trajectory reflects the automotive industry's fundamental shift toward software-defined vehicles, where infotainment systems serve as the primary interface between drivers and increasingly complex vehicle architectures. The market's expansion is underpinned by mandatory safety regulations, particularly the EU's General Safety Regulation II, effective July 2024, which requires advanced driver assistance systems integration with infotainment platforms, such as Continental Automotive.[1]"GSR II elevates vehicle standards from July 2024", General Safety Regulation II, www.continental-automotive.com. The market's evolution reflects a broader transformation where infotainment systems transition from entertainment-centric platforms to mission-critical vehicle operating interfaces. NITI Aayog projects semiconductor costs per vehicle will double to USD 1,200 by 2030, with infotainment systems accounting for a substantial portion of this increase as vehicles integrate artificial intelligence, machine learning, and cloud-native architectures.

Key Report Takeaways

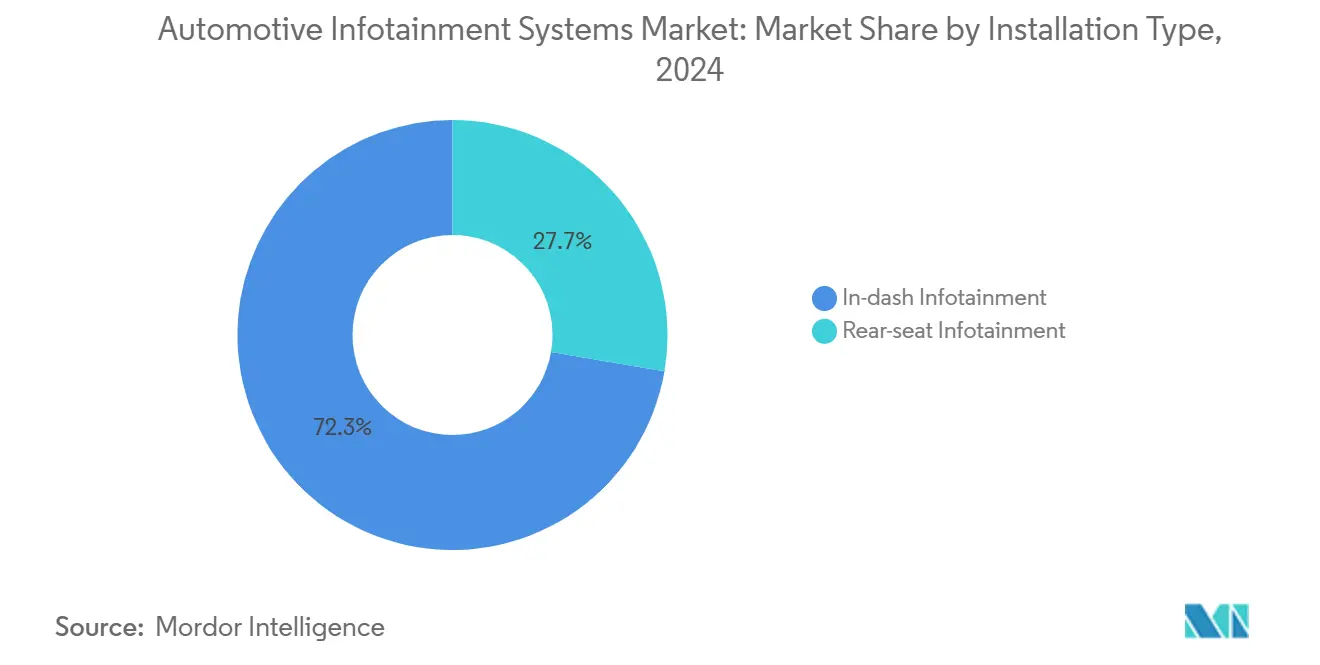

- By installation type, in-dash units accounted for 72.32% of the automotive infotainment systems market share in 2024, whereas rear-seat entertainment is poised to expand at an 11.81% CAGR through 2030.

- By vehicle type, passenger cars held 79.34% revenue in 2024; light commercial vehicle is expanding at 11.34% CAGR by 2030.

- By component type, head units and domain controllers captured 41.33% of 2024 revenue, yet operating-system software and apps will register the highest 15.92% CAGR.

- By propulsion type, battery-electric vehicles will post a 24.21% CAGR, outpacing internal-combustion and hybrid formats however accounting for 67.56% in 2024.

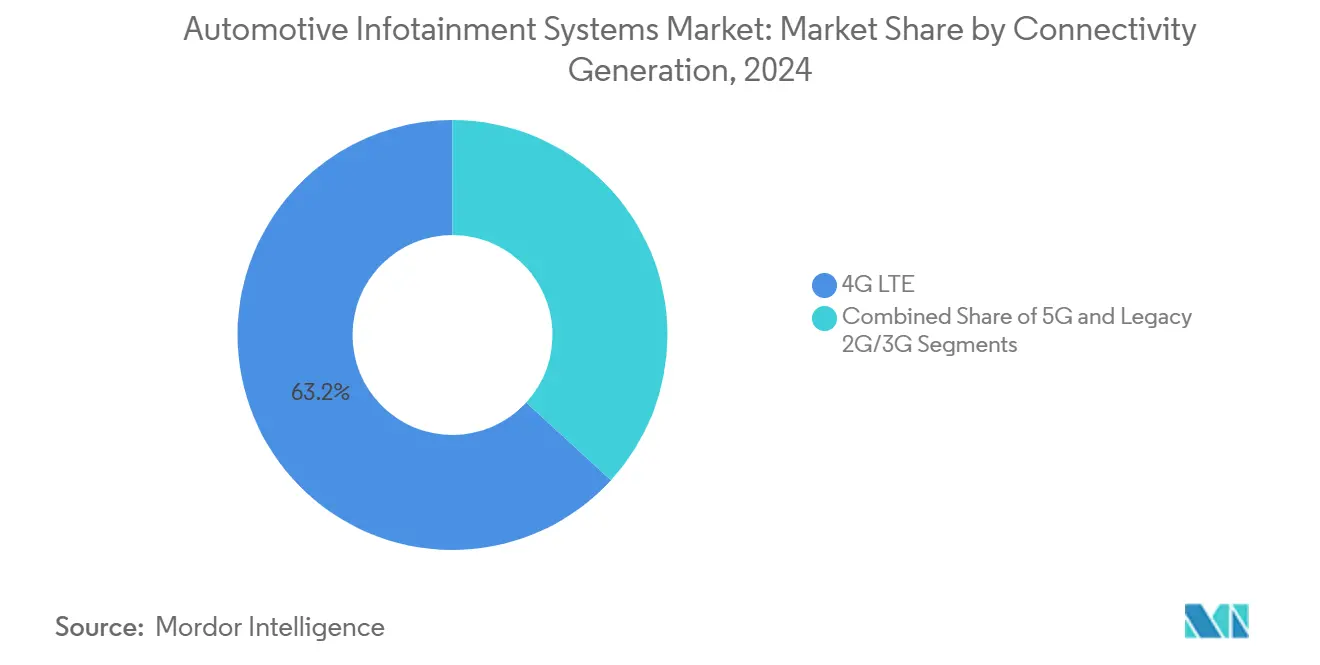

- By connectivity generation, 5 G-enabled platforms are projected to grow at 19.43% CAGR, compared with a dominant but slowing 63.23% share for 4G LTE in 2024.

- By operating system, Android Automotive OS is set to grow 18.23% annually, while Linux-based stacks retain a 35.12% revenue share.

- By sales channel, OEM accounts for 88.12% market share in 2024, whereas aftermarket accelerate at 9.73% CAGR through 2030.

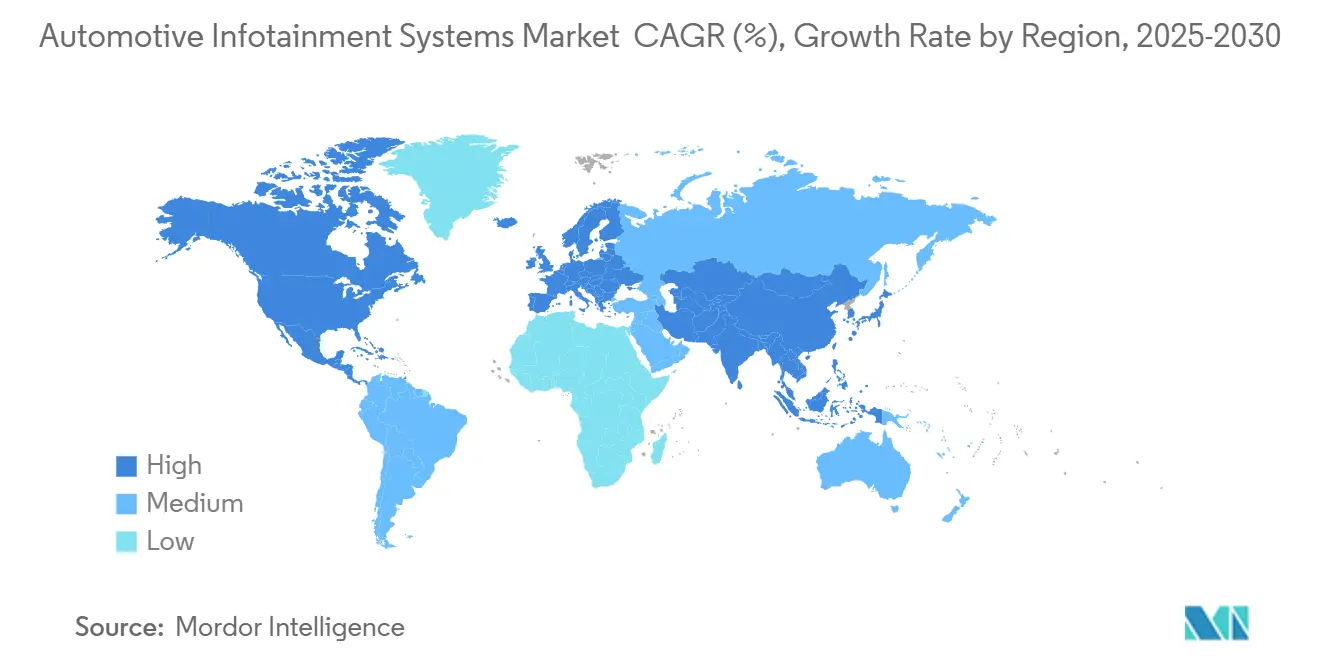

- By geography, Asia-Pacific led with a 39.23% share in 2024; South America is forecast to log a region-leading 9.31% CAGR to 2030.

Global Automotive Infotainment Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of ADAS-Centric HMI | +1.8% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Consumer Demand for Connected Services | +1.5% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Shift Toward Software-Defined Vehicles | +1.2% | Global, spearheaded by premium OEMs | Long term (≥ 4 years) |

| In-Car E-commerce/App-Store Monetisation | +0.8% | North America and EU core markets | Medium term (2-4 years) |

| Mandatory eCall & Data-Logging Regulations | +0.6% | EU mandatory, expanding to emerging markets | Short term (≤ 2 years) |

| Cloud-Native Updates Enabling Feature-on-Demand | +0.4% | Global, premium segments leading adoption | Long term (≥ 4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Integration of ADAS-Centric HMI into Infotainment Head Units

The convergence of Advanced Driver Assistance Systems with human-machine interfaces represents a paradigm shift that extends beyond traditional safety applications to create unified vehicle control architectures. Continental's Smart Cockpit High-Performance Computer supports up to 3 displays and five cameras while integrating Google Cloud's generative AI for intuitive voice interaction, enabling conversational navigation and seamless in-car control. HARMAN's collaboration with HL Klemove demonstrates how ADAS integration creates unified solutions for automakers, where driver monitoring systems and collision avoidance features share processing resources with entertainment functions. This integration reduces system complexity while enabling automakers to differentiate through software-defined experiences rather than hardware proliferation. The EU's mandatory implementation of intelligent speed assistance and driver drowsiness warnings from July 2024 accelerates this convergence. OEMs seek cost-effective solutions that combine regulatory compliance with enhanced user experiences.[2]"Mandatory drivers assistance systems expected to help save over 25,000 lives by 2038", European Commission, single-market-economy.ec.europa.eu.Bosch's cockpit integration platform exemplifies this trend by enabling seamless integration of various functionalities within a single vehicle cockpit architecture.

Consumer Demand for Connected Services & 5G Roll-out

The automotive industry's 5G deployment accelerates beyond mere connectivity upgrades to enable fundamentally new business models centered on real-time data monetization and edge computing applications. Lear Corporation estimates the automotive 5G market will grow from USD 2 billion in 2025 to USD 5 billion by 2030, driven by vehicle-to-everything communication capabilities that transform infotainment systems into comprehensive mobility platforms. HARMAN's 5G-enabled TBOT technology anticipates connectivity needs for streaming and gaming applications while optimizing data usage across varying connectivity zones, demonstrating how intelligent software can maximize 5G's potential. It has been estimated that over 90% of vehicles sold by 2030 will feature connectivity capabilities, with consumers willing to switch brands for superior connected experiences, particularly in battery-electric vehicle segments. The convergence of 5G with artificial intelligence enables predictive maintenance and personalized content delivery, creating subscription revenue opportunities that could generate USD 1,600 per vehicle annually. General Motors' partnership with AT&T for 5G deployment across U.S.-built vehicles exemplifies how traditional automakers position connectivity as a core differentiator rather than an optional feature.

Shift toward Software-Defined Vehicles & Digital Cockpits

Software-defined vehicle architectures fundamentally alter infotainment system development by decoupling software innovation from hardware refresh cycles, enabling continuous feature enhancement through over-the-air updates. BMW's Remote Software Upgrades have delivered over 50 new features since 2019, demonstrating how software-centric approaches extend vehicle lifecycles while creating ongoing customer engagement opportunities. HARMAN's OTA 12.0 release supports over 40 global vehicle manufacturers with enhanced cybersecurity measures and distributed orchestration capabilities, addressing the shift toward centralized architectures that accommodate larger software images. The transition enables automakers to implement features-on-demand business models, where consumers can activate premium functionalities through subscription services, creating recurring revenue streams beyond traditional vehicle sales. Sony Honda Mobility's AFEELA project exemplifies this transformation by positioning the vehicle as a smartphone-on-wheels, where entertainment and services generate revenue streams comparable to traditional automotive sales. Marelli's Digital Twin technology enables simultaneous feature development and testing, facilitating rapid innovation cycles that traditional hardware-centric approaches cannot match.

In-Car E-commerce / App-Store Monetization

The emergence of in-vehicle commerce platforms transforms infotainment systems from cost centers into revenue-generating assets. Juniper Research projects in-vehicle payment spending to reach USD 86 billion in 2025. HARMAN's Ignite Store provides white-label app distribution capabilities on Android Automotive OS, enabling OEMs to control branding while monetizing third-party content through integrated payment systems. Porsche Consulting identifies three distinct monetization categories: functions-on-demand for software upgrades, vehicle-related payments for fueling and charging, and non-vehicle payments for shopping and entertainment, with projections of 600 million connected cars generating USD 537 billion in transactions by 2030. Stellantis' integration of pop-up advertisements into Jeep infotainment systems represents a controversial but potentially lucrative approach to monetizing in-vehicle attention, targeting a significant leap in annual software revenue. MAVI.IO's OnMyWay platform demonstrates practical implementation by enabling parking payments and ordering food directly through vehicle dashboards, with recent USD 3 million funding highlighting investor confidence in this emerging sector.

Restraints Impact Analysis

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Sensitivity in Entry-Level Models | -1.1% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Cyber-Security & Liability Risks | -0.9% | Global, with stricter enforcement in EU and North America | Medium term (2-4 years) |

| Automotive SoC Supply-Chain Volatility | -0.7% | Global, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| Right-to-Repair & Data-Ownership Legislation | -0.3% | EU and North America regulatory focus | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cost Sensitivity in Entry-Level Models

Entry-level vehicle segments face mounting pressure to integrate advanced infotainment capabilities while maintaining price competitiveness, creating a fundamental tension between consumer expectations and manufacturing economics. NXP Semiconductors' entry infotainment portfolio, including i.MX6UL processors and TDF8541 power amplifiers, specifically targets cost-conscious applications where basic connectivity and audio functionality must be delivered at minimal expense. The challenge intensifies as semiconductor costs per vehicle are projected to double to USD 1,200 by 2030, with infotainment systems representing a significant portion of this increase. Indian market dynamics illustrate this tension, where premium variants account for 40% of sales in certain segments. Yet, price sensitivity remains paramount for volume segments where basic infotainment features must be carefully balanced against cost constraints. BYD's CNY 100 billion investments in smart driving technology specifically target entry-level model accessibility, aiming to democratize advanced features while maintaining competitive pricing. This cost pressure forces OEMs to make strategic trade-offs between feature richness and affordability, potentially limiting market penetration in price-sensitive segments.

Cyber-security & Liability Risks

Automotive cybersecurity threats have escalated dramatically, with infotainment systems accounting for 15% of reported cyber incidents in 2023, while 90% are linked to embedded software vulnerabilities. The VicOne Automotive Cybersecurity Report documents a 225% increase in cyberattacks from 2018 to 2021, with connected vehicle vulnerabilities surging 321% in 2021 alone. Pioneer's DMH-WT7600NEX infotainment system exemplifies these risks, where researchers demonstrated how zero-day vulnerabilities could transform aftermarket units into surveillance tools, accessing GPS locations and call logs. The EU's ISO/SAE 21434 cybersecurity standard and UN ECE R155/R156 regulations mandate comprehensive cybersecurity risk management throughout vehicle lifecycles, creating compliance costs that particularly burden smaller manufacturers. Software-defined vehicles amplify these risks as malicious apps can compromise vehicle security by stealing personal information or potentially immobilizing vehicles. This necessitates robust security-by-design approaches and regular software updates. The potential for USD 505 billion in financial losses by 2024 from automotive data breaches underscores the industry's liability exposure.

Segment Analysis

By Installation Type: In-Dash Dominance Drives Integration

In-dash configurations held 72.32% of 2024 shipments, illustrating their grip on the automotive infotainment systems market. BMW’s forthcoming Panoramic iDrive melds a 48-inch curved OLED with 3D head-up overlays, demonstrating how central displays now orchestrate HVAC, navigation, and entertainment without discrete buttons. Tesla’s single-screen Model Y cockpit offers another illustration of hardware minimalism where software menus replace physical knobs. The rear-seat entertainment category, meanwhile, is projected to register an 11.81% CAGR as autonomous features free passengers from active driving. Luxury brands deploy multi-display ceiling mounts and seat-back arrays that stream 4K content, creating a captive platform for subscription revenue. HARMAN’s SeatSonic transduces audio through seat frames, enhancing immersion without raising cabin decibel levels. Growing ride-hailing fleets add further demand: passengers increasingly expect video-on-demand during commutes, pushing operators to retrofit entertainment screens even in mid-tier sedans.

Passenger-centric interactions are reshaping interface logic. Haptic feedback, contextual lighting, and camera-based gesture control converge on the in-dash stack, turning it into a command center for vehicle domains beyond entertainment. Rear-seat modules now link directly to cloud profiles so every user can resume playlists or video progress across trips. Automakers experimenting with subscription tiers often debut pay-per-month gaming bundles on rear displays to test consumer appetite before pushing features to the driver’s screen. Emerging regulatory talk on driver distraction could also tilt design, favoring heads-up projection over touchscreens. These dynamics reinforce the automotive infotainment systems market as a playground where UX design and monetization strategy intersect.

By Vehicle Type: Passenger Cars Lead While Commercial Segments Accelerate

Passenger cars owned 79.34% of global revenue in 2024 as buyers consider the cabin an extension of their digital lifestyle. Electric powertrains intensify the need for range-optimized routing and battery analytics, driving BEV infotainment installations. Light commercial vehicle is expanding at 11.34% CAGR by 2030, long dominated by telematics, now layer infotainment apps for fatigue monitoring, digital tachographs, and haul documentation. Ford Pro, for instance, logs around 600,000 paid software subscriptions across its U.S. fleet, turning dashboards into enterprise SaaS endpoints. Fleet operators prize uptime and simple over-the-air patches that avoid depot visits. Consequently, the market size of commercial vehicles' automotive infotainment systems is projected to reach USD 6.4 billion by 2030, capturing fresh revenue otherwise shielded by price sensitivity.

Ride-sharing and last-mile logistics further widen the addressable scope. Dashboards that auto-populate waybills or proof-of-delivery photos cut administrative overhead. Camera-enabled ADAS integrated into infotainment helps insurers by providing crash forensics and lowering premiums. Meanwhile, premium sedans are differentiated through multichannel audio, immersive ambient lighting, and concierge services that are bookable straight from the screen. As software maturity grows, vehicle type distinctions blur: code modules written for premium passenger cars get repackaged for light trucks with minimal change. That reuse philosophy accelerates feature spread and enhances economies of scale for the automotive infotainment systems market.

By Component: Operating Systems Drive Software Value

Head units and domain controllers secured 41.33% revenue in 2024 because every feature—from rear-view camera stitching to voice AI—relies on computational horsepower. Yet the software tier is scaling faster: operating-system and app revenue is slated for a 15.92% CAGR, underscoring the industry pivot from steel to code. Qualcomm’s Snapdragon Cockpit Gen 4 integrates an on-die NPU capable of 8 TOPS, allowing cabin personalization and driver-state analytics without extra chips. Texas Instruments’ AM275x-Q1 microcontrollers quadruple DSP throughput so cost-conscious OEMs can add spatial audio without high-end SoCs. Displays are simultaneously evolving—micro-LED panels deliver better luminance with lower power draw, enabling slim door-mounted touchscreens. Antenna modules face a switch from diversity 4G to massive-MIMO 5G arrays, lifting the bill-of-materials value per vehicle. Altogether, these shifts reinforce software as the multiplier, transforming the automotive infotainment systems market into a layered stack where value accretes at the OS and application tier.

Supplier strategies mirror that reality. Continental now ships Telechips-based boards bundled with Android distribution, selling turnkey flexibility rather than bare metal. Tier-2 firmware houses offer over-the-air diagnostics and storefront SDKs, enabling carmakers to launch paid feature add-ons long after the initial sale. For investors, recurring software margin beats once-off hardware markup, a critical pivot as raw-material prices stay volatile. Ultimately, the automotive infotainment systems market share of pure-play software vendors is rising, even though hardware still anchors system cost.

By Propulsion Type: Electric Vehicles Reshape Requirements

Internal-combustion formats held a 67.56% share in 2024, yet battery-electric derivatives multiply module demand: high-resolution range maps, charger locators, and thermal-management dashboards are all infotainment-driven. The automotive infotainment systems market size tied to BEVs is expected to escalate at 24.21% CAGR, propelled by regulatory ZEV quotas and consumer range anxiety. Hybrid vehicles create their niche for energy-flow visualizations, requiring dual-source powertrain graphics that traditional clusters cannot easily convey. Real-time battery analytics also offer upsell potential: subscription-based degradation reports can save fleet owners thousands in residual-value forecasting, embedding new annuity streams.

With propulsion electrified, HVAC, and battery conditioning claim a larger chunk of cabin energy, so UX teams must present consumption in intuitive widgets that encourage eco-driving. Automakers integrate charging-station booking directly in head units, bypassing smartphones and keeping customers inside brand ecosystems. OTA upgrades now include firmware tweaks that boost charging curves, delivering tangible range gains and reinforcing perceived value. These capabilities position the automotive infotainment systems market as the nervous system of electrification, turning kilowatt-hours into a data-rich service domain.

By Connectivity Generation: 5G Transformation Accelerates

Although 4G LTE still powered 63.23% of units sold in 2024, bandwidth ceilings limit augmented-reality navigation and cloud gaming. 5G modules shipping from 2025 onward can process V2X alerts with 20 ms latency, letting vehicles exchange sensor data down the road. The category is forecast to grow at 19.43% CAGR, making it the fastest hardware sub-segment within the broader automotive infotainment systems market. Qualcomm-HARMAN collaborations place millimeter-wave and sub-6 GHz radios on single boards, cutting integration time while supporting fallback to LTE when necessary.

As network carriers sunset 3 G, OEMs need upgrade paths for older fleets, spurring a mini boom in retrofit telematics control units. Over-the-air map streaming becomes practical at 5G speeds, opening doors for real-time hazard overlays. Furthermore, edge-computing alliances with data-center operators allow local rendering of HD maps, slashing in-vehicle compute needs. Looking forward, 6 G-readiness discussions already inform antenna design, proving that connectivity roadmaps now drive cockpit architecture in the automotive infotainment systems market.

Note: Segment shares of all individual segments available upon report purchase

By Operating System: Android Automotive Gains Against Linux

Thanks to open-source flexibility, Linux distributions represented 35.12% revenue in 2024. Yet Android Automotive OS is projected at 18.23% CAGR, riding Google’s ecosystem lock-in and a deep pool of third-party developers. Volvo, Polestar, and Renault already ship native Play Store access, while Ford’s Lincoln Digital Experience runs dual stacks to give users Android and Apple mirroring concurrently. OEMs weigh the short time-to-market benefit against potential data-sovereignty concerns. BlackBerry QNX retains a stronghold in niches where deterministic performance, brake control gateways, or secure gateways preclude open-source.

Implementation quality is not uniform: Rivian’s snappy UX contrasts with other marques hampered by lag or missing features, proving that code optimization skills still differentiate brands. Proprietary RTOS options survive mainly in commercial and off-road segments where ruggedness trumps app variety. Over time, support costs and developer familiarity may accelerate consolidation, nudging more manufacturers toward Google’s orbit and raising the Android Automotive share of the overall automotive infotainment systems market.

By Sales Channel: OEM Integration Dominates

Factory-installed units comprised 88.12% of shipments in 2024, testimony to the value of deep integration and warranty alignment. However, the aftermarket clocks a healthy 9.73% CAGR as owners of older vehicles seek modern amenities. Companies such as White Automotive now supply retrofit kits restoring Apple CarPlay on GM EVs that ship without it, revealing pent-up demand when OEM decisions clash with user preference. Still, modern CAN-FD and Ethernet architectures complicate third-party installs; improper coding can trigger fault lights or disable safety aides.

Aftermarket brands also face stricter cyber assessments. The Pioneer zero-day example spurred calls for mandatory penetration-testing certificates. Some suppliers answer by bundling 12-month security update subscriptions with each head unit. Meanwhile, OEMs increasingly treat post-sale software as their turf: features-on-demand and app-store models reduce the value gap that once favored retail head units. Across both channels, data ownership and over-the-air update rights remain hot legal topics, shaping future slices of the automotive infotainment systems market.

Geography Analysis

Asia-Pacific’s 39% foothold owes much to China’s aggressive smart-cockpit race, with BYD earmarking CNY 100 billion for ADAS and infotainment R&D to support 5.5 million EV sales by 2025. Japanese automakers—Toyota, Nissan, Honda—are pooling resources for generative AI and in-house semiconductors, ensuring supply resilience for future cockpit platforms. India’s share of premium trims has climbed to 40%, pushing suppliers like HARMAN India to expand Bengaluru R&D for localization of voice assistants and regional language UX.

North America adopts a “connected-first” mindset. The U.S. surge of 5 G-equipped models, spurred by AT&T-GM collaboration, cuts update time and unlocks tiered data plans that generate recurring revenue. Meanwhile, bipartisan Right-to-Repair bills could compel OEMs to publish diagnostic APIs, influencing how infotainment security keys are shared with independents. Europe focuses on data governance: the EU Data Act in 2025 mandates user control of in-vehicle data and obliges carmakers to allow third-party service access. eCall migration to 4G/5G and the 2024 Right-to-Repair Directive also shape cockpit design for maintainability and backward compatibility.

South America currently represents a smaller absolute market but the highest CAGR. Brazil’s ‘Mover’ program links tax incentives to local-content rules, pushing OEMs to source infotainment ECUs domestically. Audiovisual investment exceeding USD 5 billion provides display and sound-processing supply chains that can serve automotive demand. Consumer expectations mirror smartphone penetration: connectivity, app stores, and contactless payments are now considered base-level features. However, currency volatility and high import duties require cost-down engineering, often achieved through SoC consolidation. These forces collectively maintain geographic diversity in the automotive infotainment systems market while signaling strong upside for flexible, software-centric suppliers.

Competitive Landscape

Established Tier-1s such as HARMAN, Bosch, and Continental still dominate OEM sourcing lists, yet collectively control well under half of global revenue—evidence of moderate fragmentation. HARMAN leverages its Ignite platform to bundle telematics, cybersecurity, and an app store, reducing complexity for carmakers while monetizing post-sale services. Bosch exploits cross-domain know-how to integrate cockpit control with ADAS functions on a shared SoC, slashing wiring and footprint. Continental uses Google Cloud for voice AI, differentiating around natural-language UX.

New-age suppliers such as ECARX and ND Industrial challenge incumbents by offering turnkey digital cockpits on subscription, shifting capital expense into operating cost. Snapdragon Cockpit Gen 4 places Qualcomm deeper into the software value chain, pairing silicon with AI frameworks and cloud toolchains. Nvidia’s Drive IX contributes GPU acceleration for multi-display rendering, luring premium brands that crave high-frame-rate 3D graphics. Cerence and SoundHound race to embed generative AI voice at the edge, forging alliances with Mercedes-Benz and Lucid for multi-language assistants.

Cybersecurity and OTA capability now set the entry bar; smaller suppliers partner with firewall specialists like VicOne to clear OEM audits. Migration to 5G further raises complexity, encouraging ecosystem partnerships rather than strict vertical integration. As a result, competition revolves around platform breadth and updating agility rather than isolated hardware specs. Investors value recurring app-store revenue more than unit margins, prodding legacy Tier-1s to acquire niche software houses. The dynamic yields a balanced yet fiercely innovative automotive infotainment systems market.

Automotive Infotainment Systems Industry Leaders

-

Denso Corporation

-

Harman International

-

Aisin Corporation

-

Pioneer Corporation

-

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Qualcomm and Amazon announced a technology collaboration to enhance in-vehicle experiences using Snapdragon Cockpit Platform and Amazon's AI services, enabling automakers to deliver innovative in-car experiences while reducing development time and costs through virtual development environments.

- January 2025: Mercedes-Benz and Google Cloud expanded their partnership to enhance MBUX Virtual Assistant with AI-powered conversational capabilities, debuting in the new Mercedes-Benz CLA with Automotive AI Agent built on Google's Gemini models for natural-language navigation queries.

- October 2024: Renault and Cerence expanded their partnership to integrate generative AI into Renault's in-car companion Reno, debuting in the Renault 5 E-Tech electric vehicle with Cerence Chat Pro, an automotive-grade large language model for human-like interactions

Global Automotive Infotainment Systems Market Report Scope

Automotive infotainment is an in-vehicle device that provides entertainment and information to the driver and passengers. The system includes integrated audio/video (A/V) interfaces, touchscreens, keypads, etc., for offering navigational services, hand-free phone connections, vehicle voice control, parking assistance, climate control, two-way communication tools, access to the internet, and other security services. These features help increase the operational efficiency of vehicles and improve safety and driver experience.

The Automotive Infotainment Systems Market is Segmented by Installation Type (In-dash Infotainment and Rear Seat Infotainment), Vehicle Type (Passenger Cars and Commercial Vehicles), and Geography (North America (United States, Canada, and Rest of North America), Europe (Germany, United Kingdom, France, Italy, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Rest of Asia Pacific), and Rest of the World(Brazil, South Africa, and Other Countries)). The report offers the market size and forecasts in value (USD billion) for all the above segments.

| By Installation Type | In-dash Infotainment | ||

| Rear-seat Infotainment | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium and Heavy Commercial Vehicles | |||

| By Component | Display / Touch-screen Module | ||

| Head Unit / Domain Controller | |||

| Operating-System Software & Apps | |||

| Connectivity ICs & Antenna Modules | |||

| By Propulsion Type | Internal-Combustion Engine Vehicles | ||

| Hybrid Electric Vehicles | |||

| Battery Electric Vehicles | |||

| By Connectivity Generation | 4G LTE | ||

| 5G | |||

| Legacy 2G/3G | |||

| By Operating System | Linux-Based (AAOS, AGL, etc.) | ||

| QNX | |||

| Android Automotive OS | |||

| Others (Proprietary, RTOS) | |||

| By Sales Channel | OEM-Installed | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Turkey | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

By Installation Type

| In-dash Infotainment |

| Rear-seat Infotainment |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Component

| Display / Touch-screen Module |

| Head Unit / Domain Controller |

| Operating-System Software & Apps |

| Connectivity ICs & Antenna Modules |

By Propulsion Type

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

By Connectivity Generation

| 4G LTE |

| 5G |

| Legacy 2G/3G |

By Operating System

| Linux-Based (AAOS, AGL, etc.) |

| QNX |

| Android Automotive OS |

| Others (Proprietary, RTOS) |

By Sales Channel

| OEM-Installed |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth projection of the automotive infotainment systems market?

The global automotive infotainment systems market reached USD 28.53 billion in 2025 and is projected to expand to USD 38.36 billion by 2030, registering a compound annual growth rate of 6.10% during the forecast period.

Which vehicle propulsion type shows the highest growth potential in infotainment systems?

Battery electric vehicles demonstrate the highest growth at 24.20% CAGR (2025-2030), driven by their inherent dependency on sophisticated infotainment systems for energy management, charging optimization, and range anxiety mitigation.

Which region dominates the automotive infotainment systems market?

Asia-Pacific commands the largest regional share at 39% in 2024, driven by China's aggressive smart vehicle development, Japan's collaborative software initiatives, and India's premiumization trends favoring advanced infotainment features.

Which connectivity generation is expected to grow fastest in automotive infotainment?

5G connectivity exhibits exceptional growth at 19.40% CAGR (2025-2030), enabling ultra-reliable low-latency communications essential for advanced driver assistance systems and real-time content streaming applications.

Page last updated on: June 23, 2025