Automotive Inside Rearview Mirrors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

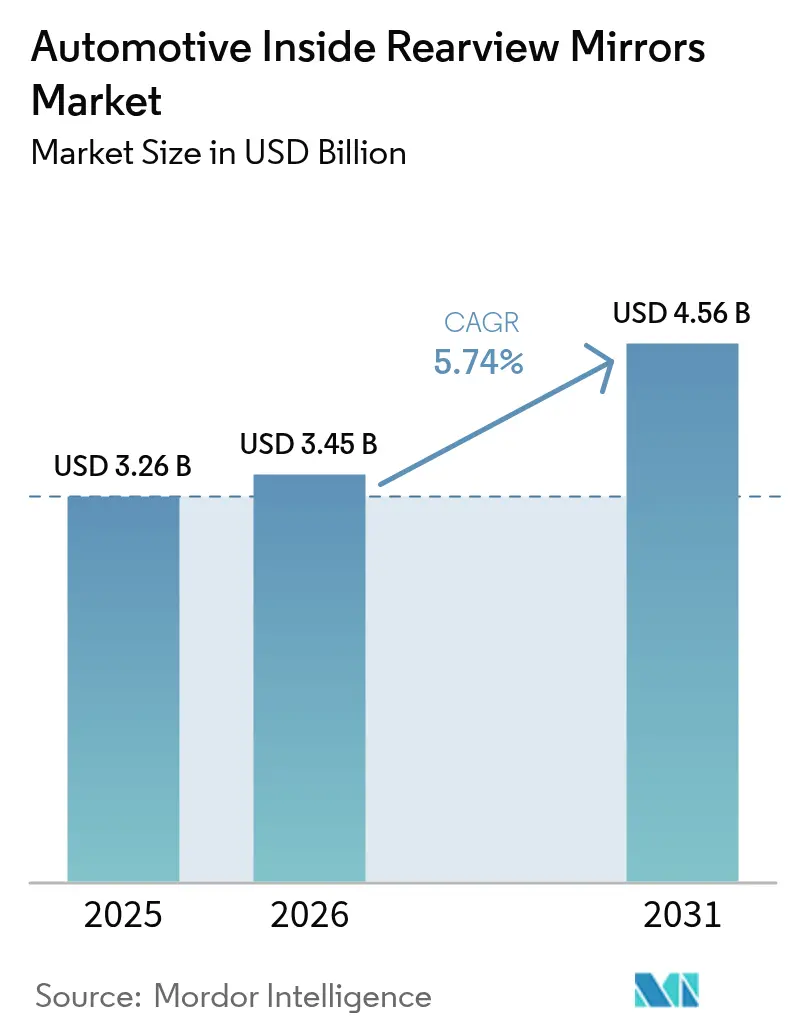

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.56 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

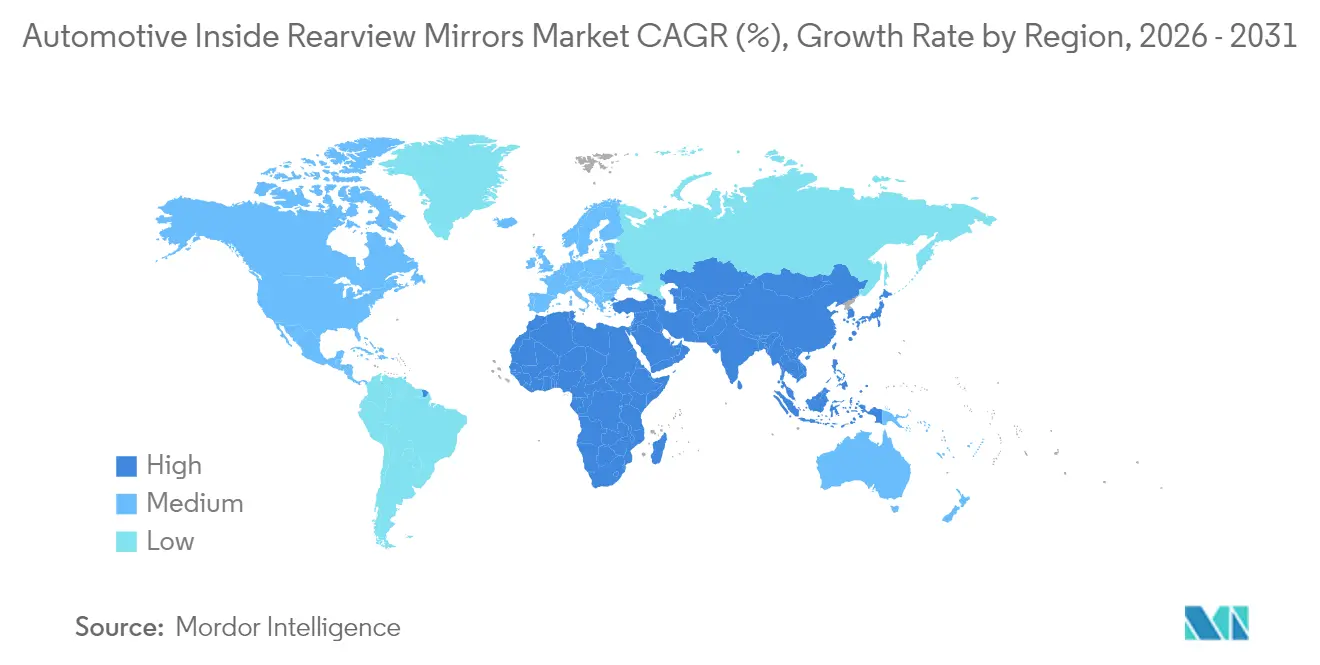

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Inside Rearview Mirrors Market Analysis by Mordor Intelligence

The automotive inside rearview mirrors market size is expected to grow from USD 3.26 billion in 2025 to USD 3.45 billion in 2026 and is forecast to reach USD 4.56 billion by 2031 at 5.74% CAGR over 2026-2031. This growth is underpinned by rising vehicle safety requirements, integration of ADAS functions into the mirror module, and the steady recovery of global light-vehicle production.

Inside rearview mirrors have shifted from being a simple reflective surface to becoming a critical part of the in-cabin safety architecture. Inside mirrors now frequently host camera-based digital displays, auto-dimming functions, and integrated driver monitoring systems. These enhancements help reduce glare, support wider and clearer fields of view, and enable new safety features such as lane departure alerts, collision warnings, and occupant monitoring.[1]“Digital Rearview Systems and Camera Monitoring Systems”, UNECE, unece.org

Regulatory momentum reinforces this transition. Safety agencies such as NHTSA and IIHS highlight blind-spot collisions and back-over accidents as key causes of injuries, prompting OEMs to adopt smarter mirrors and, in some cases, camera-based “digital rearview” solutions that supplement or replace traditional glass. Parallel trends in electrification and autonomous driving also support the market: EV platforms favor streamlined, lightweight, and aerodynamic mirror systems, while higher levels of automation require additional camera and sensor integration at or near the mirror.

Key Report Takeaways

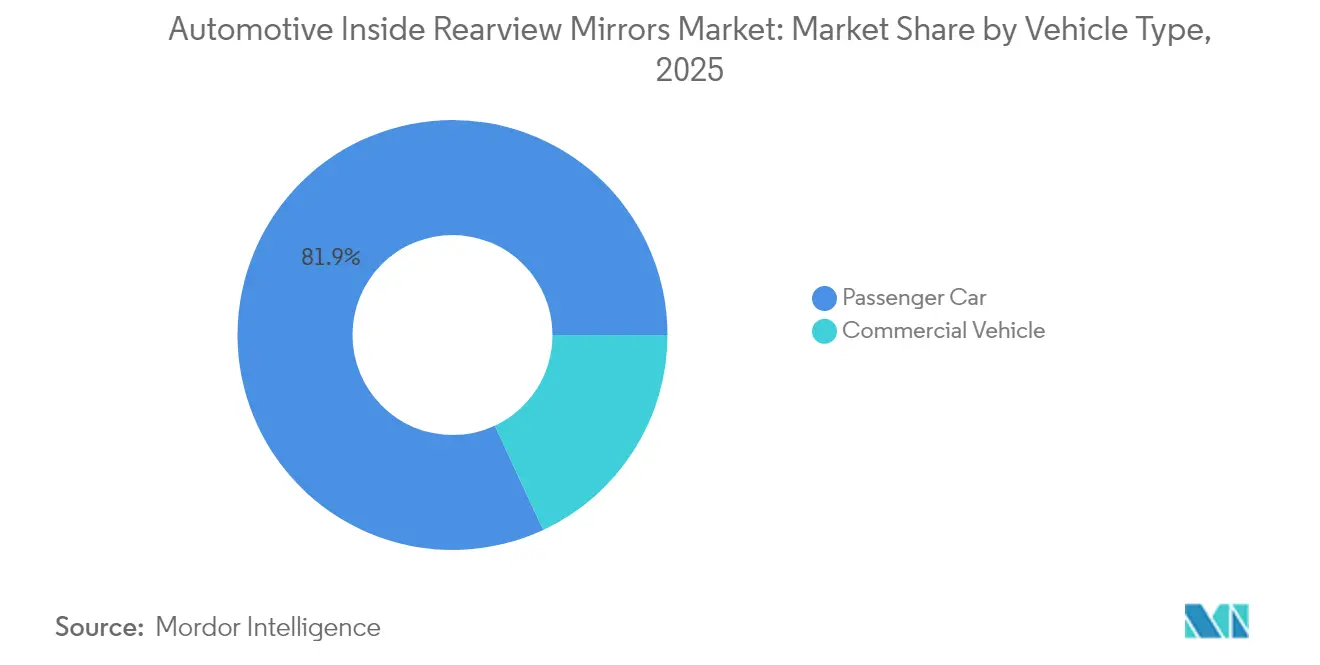

- By vehicle type, passenger cars account for about 81.94% of the automotive inside rearview mirrors market in 2025 and are projected to grow at roughly 6.18% over 2026-2031.

- By powertrain type, ICE vehicles hold close to 84.92% share in 2025, while electric vehicles are forecast to expand at around 20.95% CAGR over 2026-2031.

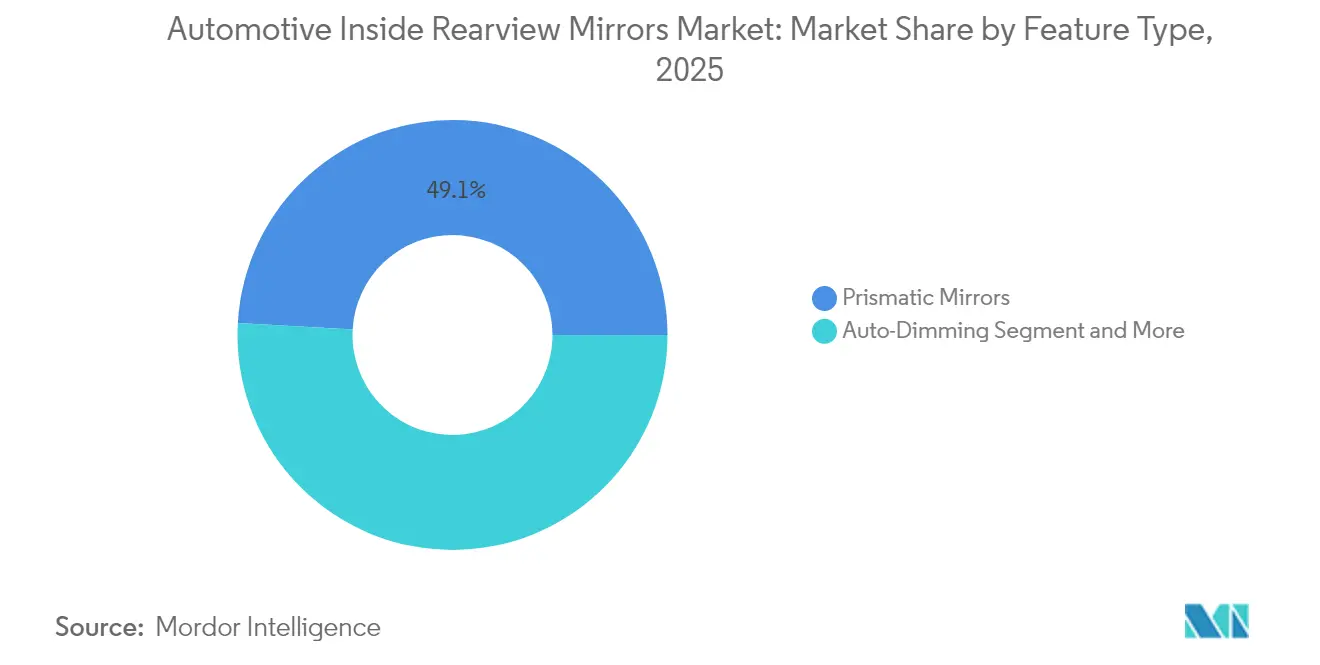

- By feature type, prismatic mirrors command roughly 49.12% share in 2025; blind-spot indicator mirrors form the fastest-growing feature cluster at about 11.74% CAGR to 2031.

- By sales channel, OEM fitment accounts for approximately 85.14% of the market value in 2025 and is expected to grow at nearly 6.06% through 2031, outpacing the aftermarket in absolute value gains.

- By geography, Asia-Pacific is both the largest and fastest-growing regional market, accounting for 41.05% of global automotive inside rearview mirrors revenues in 2025 and projected to grow at a 6.63% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Inside Rearview Mirrors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter safety & rear-visibility regulations | +1.7% | Global, strongest in Europe, North America, Japan, South Korea | Long term (≥ 4 years) |

| Adoption of ADAS & smart mirror modules | +1.5% | North America, Europe, China, South Korea | Medium term (2–4 years) |

| Premium vehicle mix & feature upgrades in mass segments | +1.1% | Global, led by US, China, Western Europe | Medium term (2–4 years) |

| Electrification & EV interior re-architecture | +1.0% | Europe, China, North America, advanced Asian EV markets | Long term (≥ 4 years) |

| Fleet & commercial-vehicle safety programs | +0.8% | North America, Europe, urban Asia (Japan, India, ASEAN metros) | Medium term (2–4 years) |

| Vehicle production growth in emerging markets | +0.6% | Asia-Pacific (India, ASEAN), Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Safety & Rear-Visibility Regulations

Regulators worldwide continue to tighten rear visibility, blind-spot, and crash-avoidance requirements, which directly lifts demand for better-performing rearview mirrors. New car assessment programs and road-safety agencies increasingly link star ratings or compliance labels to visibility performance, glare reduction, and driver awareness systems. This pushes OEMs to upgrade mirrors from basic prismatic designs to units with wider fields of view, improved anti-glare functionality, and integrated warning indicators.

In parallel, commercial-vehicle rules for buses, coaches, and trucks mandate defined mirror coverage zones and, in some regions, supplementary camera systems. Even when cameras are added, a certified interior mirror or digital mirror display is usually still required, reinforcing the mirror module as a non-negotiable safety component. Because these regulations evolve slowly but ratchet upward, they create a long-term structural pull on mirror content and quality across all major automotive regions.

Adoption of ADAS & Smart Mirror Modules

Advanced driver-assistance systems (ADAS) are increasingly being routed through or displayed in the inside rear-view mirror module. Auto-dimming, blind-spot indicators, lane-departure alerts, and camera streaming from rear or surround-view systems are now frequently anchored in the mirror housing. This design choice centralizes critical information in the driver’s natural line of sight, without increasing dashboard clutter.

As more mass-market vehicles add ADAS bundles, the mirror becomes a logical integration node for sensors, cameras, and displays. Suppliers respond by offering smart mirror platforms with modular add-ons: electrochromic glass, embedded LEDs, microphones for voice assistants, and even driver-monitoring cameras. This trend turns the mirror from a low-margin commodity into a higher-value electronics hub, lifting average selling prices and deepening supplier–OEM partnerships.[2]“New Car Assessment Program Final Decision | ADAS”, National Highway Traffic Safety Administration, nhtsa.gov

Premium Vehicle Mix & Feature Upgrades in Mass Segments

Global sales are skewing toward SUVs, crossovers, and better-equipped trim levels, which typically specify more sophisticated interior mirrors. Higher rooflines, wider pillars, and thicker rear headrests in these body styles increase reliance on optimized mirrors or digital rearview systems to maintain adequate rear visibility. Premium brands have long used auto-dimming and frameless mirrors as differentiation points; now these features are steadily cascading into upper mid-range and even mainstream models.

At the same time, competitive pressure in volume segments pushes OEMs to bundle comfort and safety features, such as auto-dimming, integrated compass/temperature displays, or embedded garage-door openers, into mid-level trims. These feature upgrades occur even in markets with tight price sensitivity, as consumers increasingly expect “premium-like” cabins. The result is a gradual uplift in content per mirror across the global passenger-car parc, not just at the luxury end.

Electrification & EV Interior Re-Architecture

Electric vehicles provide a catalyst for re-thinking cabin layouts and visibility solutions, and the rearview mirror benefits directly from this re-architecture. EV platforms often feature higher tailgates, thicker C-pillars, and distinct rear glazing for aerodynamic efficiency, all of which can compromise traditional rearward visibility and necessitate enhanced mirror or camera-mirror solutions. Digital mirrors that can switch between optical reflection and camera feed become especially attractive in EVs, where consumers are already primed for high-tech interiors.

Moreover, EVs frequently launch with advanced driver-monitoring and ADAS suites as standard or near-standard equipment. Locating cameras and infrared emitters in or around the inside mirror simplifies sensor placement and calibration while preserving dashboard design freedom. This tight integration means each incremental increase in EV penetration disproportionately expands demand for high-spec mirror modules compared with basic ICE vehicles. Over the long term, as EV share grows, this driver meaningfully boosts both volumes and value per unit in the inside rearview mirrors market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced mirrors in price-sensitive segments | –1.3% | Emerging markets in Asia, Latin America, Africa | Short–medium term (≤4 years) |

| Semiconductor & electronics supply volatility | –1.0% | Global, with acute impact in Europe, North America, East Asia | Medium term (2–4 years) |

| OEM cost-down pressure and mirror commoditization | –0.8% | Global, especially mass-market passenger-car programs | Long term (≥ 4 years) |

| Regulatory and design uncertainty around pure camera-mirror systems | –0.7% | Europe, Japan, selected North American and Chinese OEMs | Medium–long term (≥3 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Mirrors in Price-Sensitive Segments

Auto-dimming, camera-integrated, and sensor-rich mirrors significantly increase bill-of-materials cost versus traditional prismatic units. In mature markets, this is absorbed into higher trim prices, but in emerging economies, where entry-level cars and basic commercial vehicles dominate, OEMs face strong resistance to passing these costs to consumers. As a result, many models in India, Southeast Asia, Africa, and Latin America still ship with basic mirrors, and smart features are limited to premium variants or optional packs with low take-rates.

This cost barrier is especially acute when combined with rising electronics prices and currency volatility. Smaller OEMs and regional brands may delay upgrading mirror specifications to avoid margin erosion, even when regulations permit more advanced solutions. Consequently, the adoption curve for smart mirrors flattens in low- and mid-income markets, muting global growth that would otherwise be supported by safety and technology trends.

Semiconductor & Electronics Supply Volatility

Advanced inside rear-view mirrors increasingly depend on semiconductors, image sensors, microcontrollers, and specialized driver ICs. Periodic shortages or price spikes in these components can delay production schedules, force design simplifications, or push OEMs to prioritize chip allocation toward higher-margin systems such as infotainment and powertrain control. Mirror programs, often seen as secondary electronics, can experience launch delays or temporary feature de-contenting when supply is tight.

Even when components are available, long lead times and sharp price movements complicate planning for tier-1 suppliers, who typically operate on fixed-price, multi-year contracts with automakers. This squeezes margins and discourages aggressive rollout of new smart-mirror platforms, particularly in volatile regions. In aggregate, supply-chain unpredictability subtly suppresses the effective CAGR of the inside rearview mirrors market by constraining how quickly advanced electronic features can be deployed at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Anchor Demand

Passenger cars dominate the automotive inside rearview mirrors market, with around 81.94% share in 2025. High global production volumes of hatchbacks, sedans, SUVs, and crossovers underpin this dominance, alongside increasingly stringent occupant-safety norms that make advanced interior mirrors standard or near-standard on many trims. Auto-dimming, integrated displays, and embedded sensors are now frequently specified in mid-range and premium passenger vehicles, lifting mirror content per vehicle. The rise of compact SUVs and crossovers with higher beltlines and rear head restraints has also increased reliance on optimized mirror designs and digital mirrors for rearward visibility.

Commercial vehicles form a smaller but strategically important segment, particularly for safety-critical applications. Trucks and buses require specialized inside mirrors, often paired with complex exterior mirror sets and camera systems to manage extended blind spots. Fleet operators and regulators push for enhanced rear visibility in school buses, coaches, and long-haul trucks, incentivizing OEMs to integrate digital rearview modules and driver monitoring into fleet-spec cabs. Over the forecast period, commercial vehicles are expected to grow steadily as governments tighten safety rules for professional drivers and as logistics and passenger transport fleets upgrade to more advanced mirror systems.

By Powertrain Type: ICE Still Dominant, EVs Scale Rapidly

Vehicles with internal combustion engines (ICE) continue to represent roughly 84.92% of inside rearview mirror demand in 2025, reflecting the large global in-use fleet and ongoing ICE vehicle sales in emerging markets. Inside rearview mirror specifications for ICE vehicles are being upgraded as OEMs respond to new safety regulations and competitive benchmarks, adding auto-dimming, compass/temperature displays, and basic ADAS alerts into the mirror housing. This keeps the ICE segment structurally important for mirror suppliers even as EV growth accelerates.

The electric vehicle (EV) segment, though smaller today, is forecast to grow at an impressive 20.95% CAGR through 2031 in the inside rearview mirrors market. EV architectures often incorporate camera-based mirror systems and integrated driver monitoring as standard features, increasing the electronics and software content per mirror. As OEMs redesign cabins around large central displays and digital cockpits, the inside rearview mirror becomes a logical location for ADAS sensors, driver monitoring cameras, and streaming-video displays. This makes EVs an outsized driver of advanced mirror technology adoption, with premium electric models frequently debuting new digital mirror configurations that later trickle down into higher-volume ICE platforms.

By Feature Type: Prismatic Mirrors Lead, Smart Features Take Off

Prismatic mirrors remain the workhorse of the industry, holding roughly 49.12% share of the automotive inside rearview mirrors market in 2025. Their relatively low cost, proven durability, and simple yet effective anti-glare performance keep them widely used in entry-level and mid-range vehicles across all regions. For many volume OEMs, prismatic mirrors provide a baseline safety function at minimal incremental cost, ensuring full compliance with visibility regulations even in cost-sensitive segments.

At the same time, blind-spot indicator mirrors form the fastest-growing feature cluster, with an expected growth rate of about 11.74% CAGR through 2031, supported by tighter crash-avoidance standards and growing consumer awareness of lane-change accidents. Auto-dimming mirrors and smart mirrors with integrated displays and cameras are gaining traction in premium and upper mid-range vehicles, where glare reduction, camera streaming, and on-glass graphics (compass, temperature, alerts) deliver clear perceived value. These advanced feature sets translate into higher ASPs for suppliers and encourage tier-1 manufacturers to invest in electrochromic materials, compact displays, and camera integration technologies that can eventually scale into higher-volume segments.

By Sales Channel: OEM Fitment Dominates, Aftermarket Enables Upgrades

The OEM channel commands roughly 85.14% of global automotive inside rearview mirror revenues in 2025, and is also tracking the highest growth trajectory at around 6.06% through 2031. This dominance stems from the fact that rear-view mirrors are safety-critical components, tightly integrated into vehicle design, ADAS sensor placement, and homologation. Automakers increasingly specify customized mirror modules, including camera, sensor, and display integration, during vehicle development, locking in long-term supply agreements with major mirror manufacturers. As regulatory requirements evolve and ADAS penetration rises, OEMs continue to expand the scope of features built into factory-fitted mirrors, further reinforcing this channel’s importance.

The aftermarket plays a complementary role, focusing on replacement mirrors for collision damage as well as technology upgrades for older vehicles. Owners of legacy vehicles increasingly retrofit auto-dimming mirrors, dash-cam integrated mirrors, and mirrors with built-in parking or reverse-camera displays. Aftermarket suppliers target regions with large, ageing vehicle fleets and less stringent homologation barriers, offering plug-and-play mirror upgrades through accessory channels and online platforms. While absolute growth is slower than in the OEM channel, the aftermarket remains significant due to persistent replacement demand and consumer interest in adding modern safety features without purchasing a new vehicle.

Geography Analysis

Asia-Pacific is the clear demand hub for automotive inside rearview mirrors, accounting for an estimated 41.05% of global market value in 2025 and growing at about 6.63% CAGR over 2026-2031. This reflects the region’s dominance in vehicle production, with China, Japan, India, and South Korea together contributing the largest share of global light-vehicle output and new registrations. High volumes of passenger cars, rising SUV and crossover sales, and accelerating EV adoption all translate into strong OEM fitment of both conventional and smart IRVMs. As local brands move up the value ladder, mid-range and premium trims increasingly adopt auto-dimming and feature-rich mirrors, further lifting content per vehicle in Asia-Pacific.

North America and Europe remain substantial but comparatively slower-growing markets, driven by stringent safety regulations and high ADAS penetration, while the Rest of the World (Latin America, Middle East & Africa) offers smaller but steadily expanding pockets of demand tied to vehicle parc growth and gradual safety upgrades. However, neither region matches Asia-Pacific’s combination of scale and growth: OEM programs in China and India alone can shift global demand for advanced mirrors when they migrate a feature from optional to standard. Over the forecast period, this dynamic keeps Asia-Pacific both the largest regional market and the fastest-growing geography, making it the strategic focal point for mirror suppliers’ capacity expansion, localization, and co-development programs with global and regional automakers.

Regulatory Landscape

Rear visibility and indirect vision requirements are anchored by major rulebooks that shape inside rearview mirror design and homologation globally. In the United States, NHTSA regulates rear visibility performance through FMVSS No. 111 (49 CFR 571.111), which sets requirements for rearview mirrors across passenger cars, multipurpose vehicles, trucks, and buses, including field-of-view and mounting provisions.

Outside the US, UNECE Regulation No. 46 governs devices for indirect vision and their installation, including Class I interior mirrors and the inclusion of camera-monitor systems within the indirect vision framework. The parallel existence of FMVSS 111 and UNECE R46 keeps suppliers focused on region-specific compliance paths, particularly when camera-based and hybrid optical-digital solutions must be validated against different technical provisions and approval processes.

Value Chain Analysis

The value chain is tiered, with material and sub-component suppliers feeding Tier 1 mirror system integrators that design, validate, and assemble complete inside mirror modules for OEM fitment. Upstream inputs include glass substrates and coatings (including electrochromic stacks for auto-dimming), plastics for housings and mounts, and electronics such as image sensors, microcontrollers, LEDs/IR components, and display panels for full-display or digital mirrors. Tier 1 suppliers such as Gentex, Magna, and Ficosa typically manage system engineering, functional safety integration, and vehicle-program validation, then deliver sequenced modules to OEM assembly plants through just-in-time logistics.

As mirrors take on more ADAS-adjacent functions (camera video, driver/occupant monitoring, warning indicators), the chain has shifted toward higher electronics and software content. This increases reliance on semiconductor and sensor availability and extends validation cycles for new vision systems. Manufacturing remains concentrated in Asia, and electronics sourcing adds exposure to supply volatility, which has driven suppliers toward more vertical integration of subassemblies (camera/display integration, behind-the-glass architectures) and process automation in mirror plants to control cost, quality, and throughput for OEM programs.

Competitive Landscape

The automotive inside rearview mirrors market is moderately consolidated, with a handful of global tier-1 suppliers capturing a large share of OEM contracts. Key players include Gentex Corporation, Magna International, Samvardhana Motherson Reflectec, Ficosa International, and Murakami Corporation, alongside several regional specialists. These companies invest heavily in R&D to develop electrochromic (auto-dimming) mirrors, blind-spot indicator modules, camera-integrated digital mirrors, and driver monitoring solutions embedded in the mirror housing.

Strategic priorities focus on technology differentiation, manufacturing scale, and long-term OEM partnerships. Suppliers are expanding production footprints in Asia-Pacific, adopting advanced manufacturing practices (automation, digital twins, AI-enabled quality control), and pursuing joint ventures or acquisitions to secure electronics and software capabilities. As the boundary between mirrors, cameras, and in-cabin sensing systems blurs, the most competitive vendors are those able to deliver integrated, software-enabled mirror modules that meet evolving safety regulations while remaining cost-competitive across both ICE and EV platforms.

Automotive Inside Rearview Mirrors Industry Leaders

Gentex Corporation

Magna International, Inc.

Samvardhana Motherson Reflectec

Ficosa International SA

Murakami Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary opportunity is the migration of the inside mirror from a discrete reflective component into an in-cabin sensing and display hub as OEMs expand ADAS and occupant-protection content without adding cockpit clutter. Supplier actions reflect this shift: Magna secured a program for a mirror-integrated driver and occupant monitoring system using a behind-the-glass camera architecture, and Gentex has been advancing full-display mirror capability with multi-mode views that support broader use cases (reverse assist, blind-spot-related views, and cargo-bed monitoring for pickups).

Standardization and enabling technologies are also opening space for camera and digital mirror architectures. UNECE Regulation No. 46 already provides a pathway for camera-monitor systems within indirect vision, while SAE published J3155_202604 to define camera monitor system test protocols and performance requirements for US road vehicles, supporting more consistent engineering targets across programs. On the component side, production-ready high-speed video connectivity building blocks, such as MIPI A-PHY enabled e-mirror demonstrations by Valens Semiconductor with Sakae Riken Kogyo, point to momentum toward higher data-rate, higher-resolution video mirrors that can help suppliers scale digital mirror modules across more vehicle segments as cost and validation barriers ease.

Recent Industry Developments

- May 2026: Magna International Inc. was awarded a driver and occupant monitoring system program with a European OEM, using a behind-the-glass camera architecture integrated into the mirror module. The award reinforces the inside mirror as a preferred packaging location for DMS/OMS hardware because it consolidates sensing with minimal visible cockpit changes and supports OEM safety-feature roadmaps across platforms.

- November 2025: Gentex Corporation announced the GNTX-R Series, a slim-profile carbon fiber automatic-dimming rearview mirror aimed at custom-vehicle and aftermarket applications, with availability planned via Ringbrothers in Q1 2026. The launch broadens Gentex participation beyond OEM fitment by targeting premium retrofit demand where styling and compact packaging can command higher price points.

- April 2024: Gentex announced that Polestar 4 would use its digital rearview mirror system in place of a traditional rear window, relying on a rear camera and an in-mirror HD display. This vehicle integration provided a high-visibility reference program for camera-based rearward vision in passenger cars and strengthened the case for digital mirrors where rearward sightlines are constrained by design.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of inside rearview mirrors installed inside vehicles, including standard prismatic units and feature-added mirrors used to improve driver visibility and comfort. We treat the market as the mirror module sold through OEM fitment and replacement demand, across major vehicle producing regions.

Scope exclusions: The totals exclude outside rearview mirrors, general camera-only ADAS hardware, and in-cabin displays that are not sold as part of an inside mirror module.

Segmentation Overview

- By Vehicle Type

- Passenger Car

- Commercial Vehicle

- By Powertrain Type

- ICE

- Electric

- By Feature Type

- Auto-Dimming

- Prismatic

- Blind spot indicator

- Other Smart / Digital Mirrors

- By Sales Channel Type

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Rest of Europe

- Asia Pacific

- India

- China

- Japan

- South Korea

- Rest of Asia-Pacific

- Rest of the World

- Brazil

- United Arab Emirates

- Other Countries

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean demand context for inside rearview mirrors by linking mirror fitment needs to vehicle production and parc signals. We referenced public vehicle production statistics and registrations from sources such as OICA and national transport agencies, followed by trade and customs summaries from portals such as UN Comtrade where mirror-related flows help sanity check regional supply movement.

To keep feature adoption realistic, we also reviewed safety and visibility related guidance and regulations from sources such as NHTSA and UNECE, and we used peer-reviewed papers and patent filings to understand how fast auto-dimming and camera-based mirror functions are diffusing into mid-priced vehicles. Company annual reports, investor presentations, and reputable press were used to confirm product mix language and capacity expansion timelines, and a paid company financials and intelligence subscription helped standardize revenue and footprint data across suppliers. The sources listed here are illustrative only, and many other public documents were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary discussions were used to pressure-test the desk assumptions on OEM take rates, feature mix shifts, and typical price bands by vehicle class, and then we adjusted the model only when multiple respondents pointed in the same direction. We spoke with a mix of mirror suppliers, vehicle program stakeholders, aftermarket channel participants, and independent engineers across APAC, EMEA, and the Americas so regional production patterns and specification differences could be reflected in one consistent view.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 44% |

| Mid tier: 49% | Functional/Unit leaders: 30% | EMEA: 32% |

| Smaller Players: 16% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

The core build uses top-down and bottom-up logic in a practical order, where the starting point is the vehicle production base by region and vehicle type, which is then translated into mirror demand using fitment assumptions and replacement cycles. After that, value is reconstructed using a blended pricing curve that reflects mirror type mix and the pace of feature adoption, and then it is converted into USD using consistent annual average exchange rates.

To keep the model grounded, we track inputs that are observable and explainable, such as light-vehicle and commercial-vehicle production levels, penetration of auto-dimming and camera-integrated mirrors, the share of OEM versus aftermarket demand, and the pace of electric vehicle platform launches that often pull higher feature content. We also watch regional regulation and safety-related specification changes, because those shifts can move standard content in mirrors faster than consumer preference alone. The totals are corroborated through selective supplier roll-ups (sampled revenue exposure to inside mirrors and implied volumes), and gaps are handled by using proxy adoption rates from comparable vehicle classes and then rechecking those proxies in interviews.

For forecasting, we use scenario analysis supported by a simple multivariate regression layer that links mirror value growth to vehicle production, feature take rates, and expected price progression for key mirror types. Final year-by-year movements are only accepted when they align with expert expectations on platform refresh cycles and sourcing timing, since mirror content usually changes at new model launches rather than smoothly every quarter.

Data Validation & Update Cycle

Validation is done through multiple checks so the output does not drift away from real-world signals. We compare modeled mirror volumes against vehicle build totals, review implied average selling prices against interview ranges, and then re-open assumptions if a region shows an unexplained step change that does not match production, trade, or program timing.

Before sign-off, the model and the written story go through an internal review where key tables are recalculated and variances are questioned until they have a clear explanation. The report is refreshed annually, and interim updates are triggered when material events occur, such as a major platform award shift, a regulation-led spec change, or a sharp production reset in a large vehicle market. Right before delivery, we do a final scan of the newest public indicators so clients receive the most current view available at the time.

Mordor Intelligence's Automotive Inside Rearview Mirrors Market Size Versus Other Published Estimates

Published market values for inside rearview mirrors can differ even when the topic label looks the same, because firms do not always treat product scope, channel coverage, and pricing logic in the same way. Differences also show up when base years vary, currency conversions are done using different timing, and when refresh cycles lag behind fast feature mix changes.

Some external estimates fold adjacent interior vision hardware and broader visibility systems into the same total, which can inflate the number beyond mirror-only revenue. In Mordor Intelligence, the value is counted only for inside rearview mirror modules sold through OEM and aftermarket channels, and it is kept separate from outside mirrors and non-mirror in-cabin displays, with pricing tied to feature mix rather than a single blended ASP.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.45 B (2026) | |

| Industry Publisher A | USD 3.69 B (2025) | Uses a different base year and a longer horizon, and the feature mix and pricing progression are typically treated more uniformly, which can shift the near-term value upward versus a launch-timed mix curve. |

| Analytics Firm B | USD 8.30 B (2024) | Likely aggregates wider visibility system revenue beyond inside mirror modules, and the published figure appears to be built at a higher category level without clear separation of adjacent interior components. |

The spread in the table is mainly explained by scope and year alignment, followed by how feature adoption is translated into pricing. When the market is kept to inside mirror modules and the value is rebuilt from vehicle builds, take rates, and a visible price curve, the result is easier to trace and repeat across regions and update cycles.

Key Questions Answered in the Report

What is the current size of the automotive inside rearview mirrors market?

The market is estimated at about USD 3.45 billion in 2026, with projections indicating it could reach roughly USD 4.56 billion by 2031, reflecting a CAGR of 5.74% over 2026-2031.

What factors are driving growth in this market?

Key growth drivers include stricter safety and rear-visibility regulations, rising adoption of ADAS and smart mirror modules, growing EV production, and premiumization of vehicle interiors across major markets.

Who are the major players in the automotive inside rearview mirrors market?

Major players include Gentex Corporation, Magna International Inc., Samvardhana Motherson Reflectec, Ficosa International S.A., and Murakami Corporation, which together command a significant share of global OEM supply.

Which region is expected to grow the fastest?

Asia-Pacific is both the largest and the fastest-growing region, supported by high vehicle production in China, Japan, India, and South Korea and rapid adoption of advanced safety technologies.

How are digital and camera-based mirrors impacting the market?

In 2025, the Asia Pacific accounts for the largest market share in Automotive Inside Rearview Mirrors (IRVM) Market.

Page last updated on: