Automatic High Beam Control Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 2.02 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

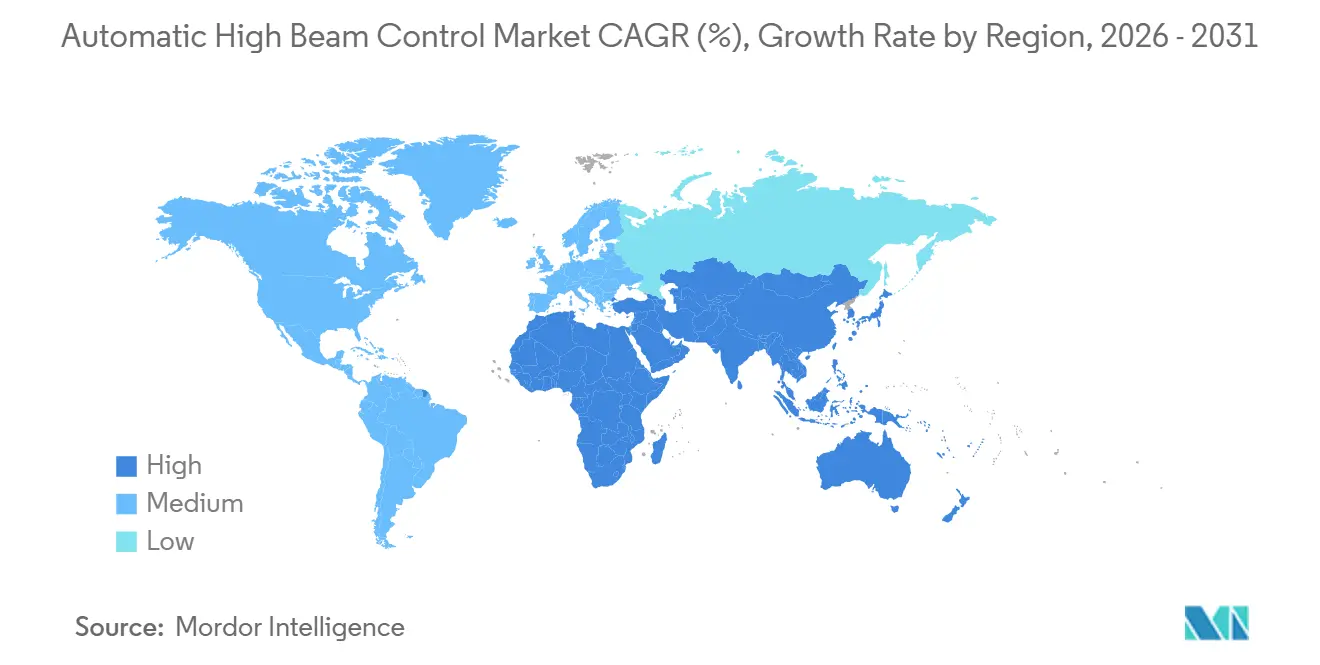

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

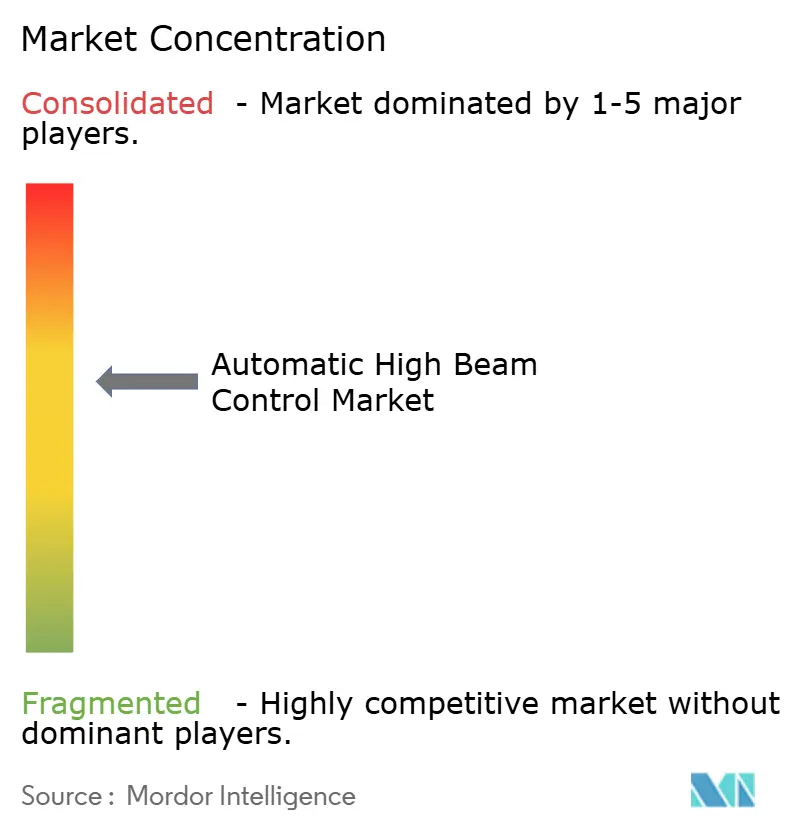

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automatic High Beam Control Market Analysis by Mordor Intelligence

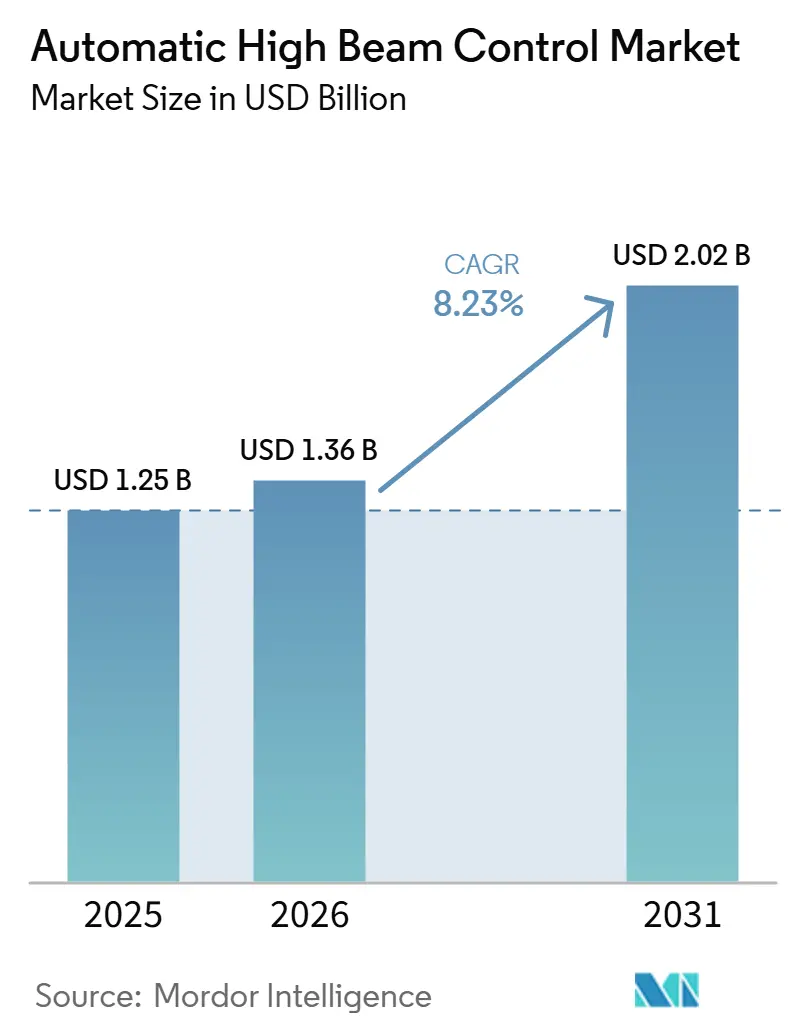

The Automatic High Beam Control Market size reached USD 1.25 billion in 2025, USD 1.36 billion in 2026, and is expected to reach USD 2.02 billion by 2031, growing at a CAGR of 8.23% from 2026 to 2031. That expansion reflects regulatory green lights, falling LED matrix prices, and insurers’ growing recognition of crash-reduction benefits. Camera-based products dominate sales today because they leverage cameras already required for other ADAS features. Yet, sensor-fusion modules are gaining momentum as automakers chase reliable nighttime performance in rain and fog. Passenger cars lead adoption, but commercial fleets are discovering measurable insurance savings that improve the total cost of ownership, nudging the technology into trucks and buses. Asia-Pacific remains the largest regional base due to China’s scale in electric vehicles and Japan’s lighting expertise. At the same time, the Middle East and Africa will post the fastest growth as local assembly plants and safety standards converge on global norms. Competitive intensity is rising as suppliers bundle software, sensors, and optics into vertically integrated packages that promise over-the-air upgrades and new recurring-revenue streams.

Key Report Takeaways

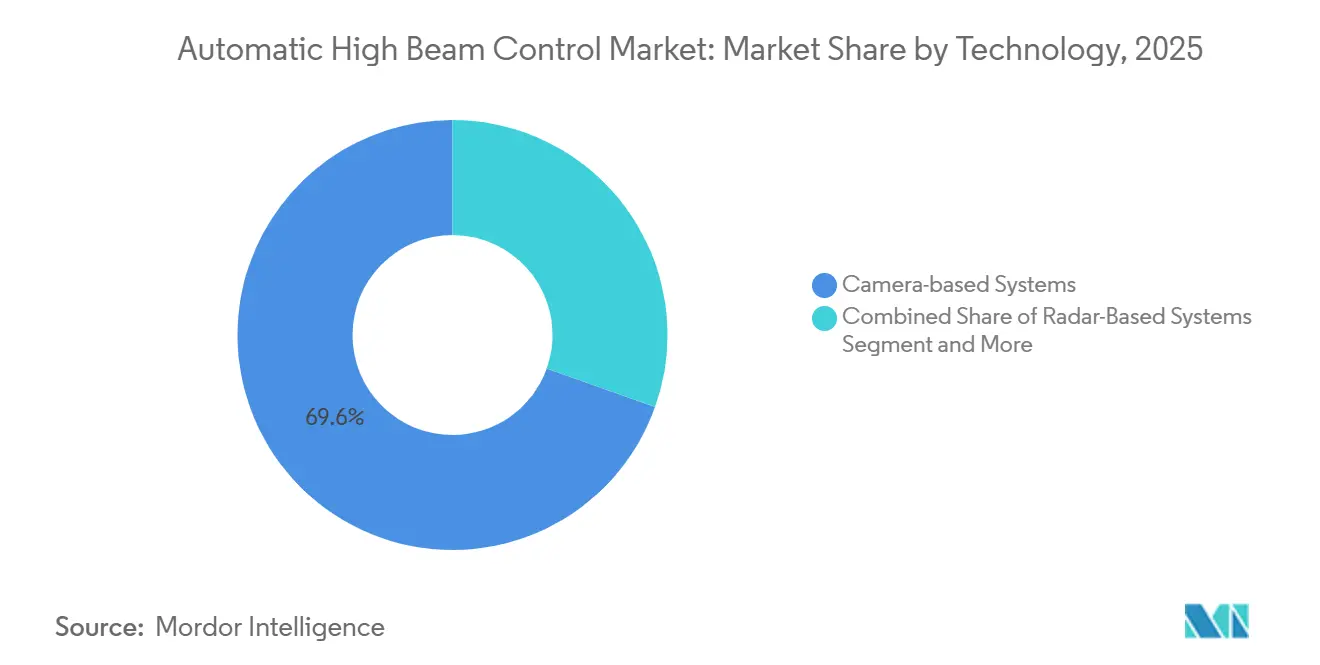

- By technology, camera-based systems held 69.57% of the automatic high beam control market share in 2025; sensor-fusion modules are projected to expand at an 11.57% CAGR during the forecast period (2026-2031).

- By vehicle type, passenger cars commanded a 64.46% share of the automatic high beam control market in 2025 and are forecast to record the fastest CAGR of 10.29% during the forecast period (2026-2031).

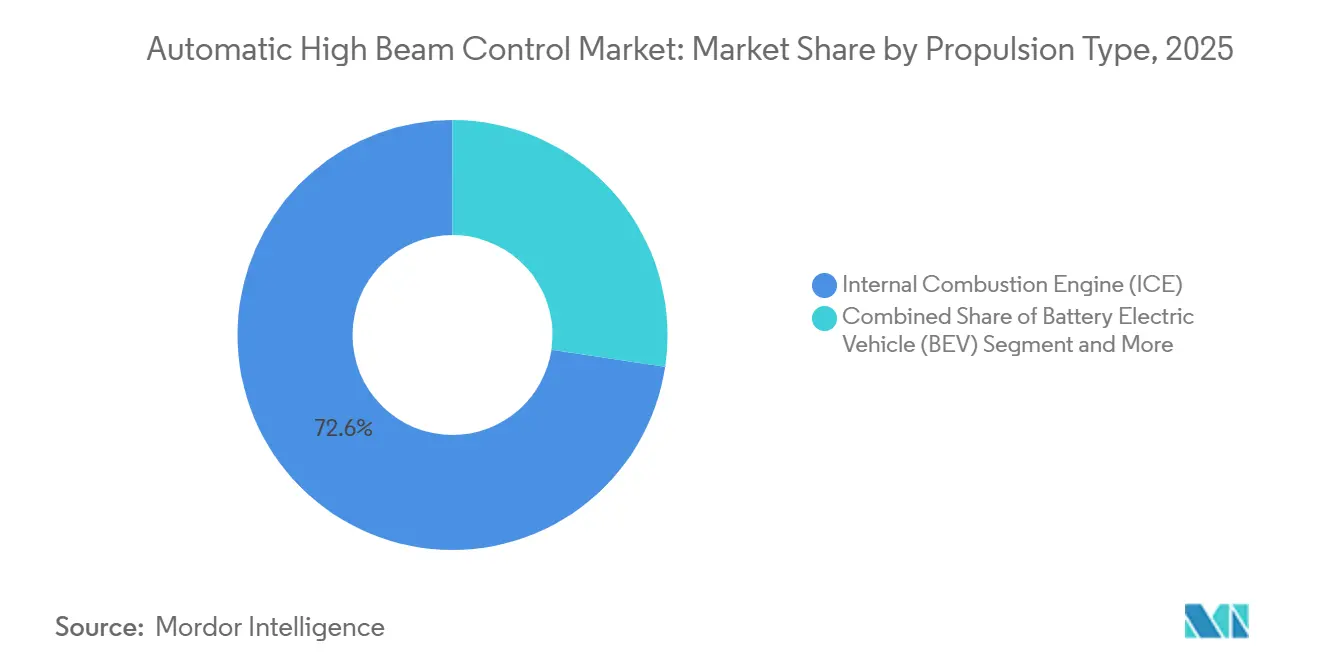

- By propulsion, Internal Combustion Engine (ICE) platforms accounted for 72.64% share of the automatic high beam control market in 2025. In contrast, the Battery Electric Vehicle (BEV) segment is expected to climb at a 16.13% CAGR during the forecast period (2026-2031).

- By distribution channel, Original Equipment Manufacturer (OEMs) fitment dominated with 91.06% revenue share of the automatic high beam control market in 2025; the aftermarket is predicted to grow at 9.90% CAGR during the forecast period (2026-2031).

- By geography, Asia-Pacific captured 46.04% of the automatic high beam control market share in 2025; the Middle East and Africa are set to accelerate at an 8.59% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automatic High Beam Control Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandates Allowing Adaptive Driving Beam | +2.1% | North America, global spill-over to harmonized markets | Medium term (2-4 years) |

| LED Matrix Cost Decline | +1.8% | Global, with strongest impact in cost-sensitive APAC markets | Short term (≤ 2 years) |

| PARTS Data | +1.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| OTA-Upgradable Lighting Software | +1.2% | North America and EU premium segments, expanding to APAC | Long term (≥ 4 years) |

| Insurance and Safety-Rating Incentives | +1.0% | North America and EU mature markets | Medium term (2-4 years) |

| Regional NCAP Lighting Protocols | +0.6% | South America, ASEAN, expanding to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates Allowing Adaptive Driving Beam in the United States

The National Highway Traffic Safety Administration cleared adaptive driving beams in September 2022, removing a decade-long roadblock. Automakers can now standardize the function across global programs, benefiting from shared tooling and software. Night-time high-beam usage remains low; IIHS found that only 18% of drivers engage manual beams, so automated glare-free high beams address a proven safety gap. Model-year refresh cycles align with the ruling, helping OEMs incorporate the feature without mid-cycle cost penalties. Follow-on updates to state inspection codes are reinforcing demand in dealership showrooms.[1]“Federal Motor Vehicle Safety Standards; Lamps, Reflective Devices, and Associated Equipment,” National Highway Traffic Safety Administration, nhtsa.gov

LED Matrix Cost Decline Enabling Mass-Market AHB Integration

In Asia-Pacific markets, where cost efficiency is paramount, recent enhancements in wafer yields and the integration of driver components have slashed the costs of matrix LED packages. This shift is paving the way for automatic high beam control to become a standard feature in mid-range vehicles. Suppliers are rolling out scalable modular optics that cater to diverse zone configurations. This innovation allows automakers to offer differentiated trim levels with distinct lighting features. Furthermore, as LED assembly operations relocate closer to China's primary automotive manufacturing hubs, they stand to benefit from reduced logistics challenges and diminished currency exposure, heralding further cost reductions.

United States Embraces Advanced Headlights, Setting Stage for Global Standardization

In the United States, insurance incentives are increasingly favoring vehicles with advanced headlight systems, leading to their widespread adoption in new models. Recognizing this pivotal shift, automakers are pushing to standardize headlamp architectures across major global markets, including North America, Europe, and Asia. This harmonization not only amplifies economies of scale, especially for automatic high-beam control systems, but also helps offset software validation costs. While luxury brands were the early adopters, mainstream manufacturers are now following suit to stay competitive in showrooms.

OTA-Upgradable Lighting Software Tiers Creating New Revenue Pools

Software-defined vehicle architectures enable automotive lighting suppliers to implement over-the-air upgradable functionality, creating recurring revenue opportunities beyond traditional hardware sales. Tier-1 suppliers embed higher-resolution DMDs and unlock pixel groups as customers pay. Beyond revenue, OTA keeps regulatory signatures current, useful as UNECE cybersecurity rules tighten. Premium buyers are initial adopters, yet as whole-vehicle architectures migrate to centralized compute, mid-segment cars will follow suit.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Glint and Heavy-Rain Performance Gaps | -1.4% | Global, particularly challenging in tropical and high-precipitation regions | Medium term (2-4 years) |

| Headlamp ECU (UN R155) Cost | -1.1% | Europe, expanding globally through regulatory harmonization | Short term (≤ 2 years) |

| Driver Disengagement | -0.8% | Global, with higher impact in markets with mixed lighting infrastructure | Medium term (2-4 years) |

| Low Consumer Awareness | -0.5% | MEA, South America, parts of APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Camera Glint and Heavy-Rain Performance Gaps Limit Regulatory Acceptance

Camera-based automatic high beam systems experience performance degradation in challenging weather conditions, particularly during heavy rainfall and when facing direct sunlight or reflective surfaces that cause sensor glint. Regulators in tropical markets hesitate to approve tech that may fail during seasonal monsoons. Testing cycles grow longer, delaying launches and driving interest in radar-vision fusion. OEMs weigh the extra bill of materials against warranty-claim risk, slowing take rate on entry models even as halo cars showcase the feature.

Cyber-Hardening Costs for Headlamp ECU (UN R155) Pressure Tier-1 Margins

UN Regulation R155 cybersecurity requirements mandate comprehensive cyber-hardening measures for automotive electronic control units, including headlamp ECUs that control automatic high-beam systems. Many lighting suppliers grapple with tight profit margins, restricting their research and development resources. This financial strain could push some smaller tier-2 firms out of the automatic high beam control segment, leading to market consolidation. However, this also heightens the risk of OEMs relying heavily on single-source suppliers. Furthermore, as cybersecurity requirements evolve, they are lengthening product development timelines. Suppliers now need to validate digital security measures in addition to traditional functional and safety tests. These complexities not only delay the rollout of next-generation lighting technologies but also intensify the pressure on engineering teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Sensor Fusion Advances Reliability

Camera modules accounted for 69.57% of the automatic high beam control market share in 2025, favored for reusing forward-facing ADAS cameras, which limit incremental costs. The automatic high beam control market size tied to sensor-fusion designs is projected to expand at an 11.57% CAGR during the forecast period (2026-2031) as radar and, later, short-range LiDAR add redundancy in fog and heavy rain. Automakers increasingly integrate fusion within domain controllers, trimming wiring weight and enabling higher pixel counts for glare-free precision. As scalability improves, the segment is expected to put pressure on standalone camera solutions, especially in commercial vehicles operating in variable weather conditions.

Sensor-fusion modules push the performance envelope by blending multi-spectral inputs, yielding smoother beam cutoffs and fewer false negatives. Suppliers demonstrate algorithms that maintain target recognition at 40 lux backscatter, a threshold that cameras struggle to meet on their own. Open-source perception stacks shorten time-to-proof, and licensing models mean even mid-tier brands can access advanced fusion without owning the full stack. By decade’s end, pure camera dominance is likely to recede in favor of budget cars, similar to the trajectory seen with basic forward-collision warning systems.

By Vehicle Type: Passenger Cars Sustain Broad Leadership

Passenger cars held a commanding 64.46% market share in the automatic high beam control market in 2025 and are expected to post the fastest 10.29% CAGR during the forecast period (2026-2031). Carmakers have moved the feature from high-end trims into standard equipment on many mass-market models, so shoppers now view glare-free high beams as routine safety gear rather than a luxury add-on. Falling LED matrix prices and clearer regulations encourage that shift, while safety-focused marketing helps buyers justify the small extra cost. Light commercial vans rank second because fleet managers report fewer nighttime collisions and lower insurance bills when the systems are fitted. Medium and heavy trucks adopt the technology mainly on long-haul routes where hours of darkness raise crash risk, so payback looks more convincing.

Several forces will keep the passenger-car lead intact. Component costs are still easing, letting automakers add beam-assist without nudging showroom prices out of reach. Regulators in major markets now count advanced headlights toward safety ratings, pushing the feature up the options list. Consumer awareness also matters; word of mouth and insurer discounts reinforce demand each time a driver experiences clearer night vision with no oncoming glare. Buses and coaches primarily add the function to premium lines, where passenger safety and liability are top of mind, but tight public budgets slow broader rollouts. Taken together, these trends echo the rapid rise of airbags and electronic stability control: once buyers and regulators agree on the benefits, industry-wide adoption follows in short order.

By Propulsion Type: BEVs Accelerate Feature Diffusion

Internal Combustion Engine (ICE) cars still accounted for 72.64% of the revenue in the automatic high beam control market in 2025. Yet, the Battery Electric Vehicle (BEV) segment is expected to grow at a 16.13% CAGR during the forecast period (2026-2031), as penetration reshapes the feature mix, with electric architectures supplying ample 48-V power and zonal Ethernet bandwidth. The automatic high-beam control market share for BEVs is growing quickly because lighting serves as both a styling signature and an energy-efficiency play. Manufacturers highlight the technology in EV launch campaigns, pairing pixel headlights with welcome animations that reinforce premium perception.

In China, automatic high beam control is swiftly emerging as a standard feature in new electric vehicle models. This trend underscores its growing significance, placing it on par with established lighting technologies, such as LED daytime running lights. While plug-in hybrids, sharing similar electrical platforms, are also adopting this feature, their uptake is somewhat tempered, primarily due to cost considerations. Electric-first vehicle designs offer greater flexibility, particularly in the front fascia, enabling larger lighting components and improved thermal management. In light of this, suppliers are redesigning lamp assemblies to cater to both internal combustion and electric models. This strategy not only streamlines inventory but also distributes development costs more evenly. With advancements in battery design that have led to more compact batteries, headlamp designers are seizing the opportunity to use grille space for advanced optics. This evolution positions lighting modules not just as signature brand elements but also as avenues for potential service-driven revenue.

By Distribution Channel: OEM Remains Dominant, Aftermarket Rises in Fleets

Original equipment manufacturers (OEMs) accounted for 91.06% of the automatic high beam control market in 2025 because the function requires ECU coding and calibration that are intertwined with vehicle CAN networks. Nonetheless, the retrofit business now mirrors the path of rear cameras: niche at first, but poised for compound growth as regulatory gaps close. Fleet managers retrofit older vans to meet corporate safety key performance indicators, using sensor pods that piggyback on existing windshields and communicate with stand-alone lamp drivers.

The aftermarket segment is expected to grow at a 9.90% CAGR during the forecast period (2026-2031), as suppliers partner with body shops for turnkey kits that complete in under two hours, a threshold often cited by fleet maintenance planners. Consolidation shapes channel dynamics. Large tier-1 suppliers divest halogen bulbs and refocus on LED modules, leaving aftermarket specialists to scoop up lamp units. This realignment means customers buying replacement parts see automatic high beam control as the default, not the option. Regional distributors report a significant year-on-year rise in inquiries for retrofit beam-assist since mid-2024, underscoring latent demand tucked inside the global parc.

Geography Analysis

Asia-Pacific delivered 46.04% of the automatic high beam control market share in 2025, propelled by China’s battery-electric boom and Japan’s lighting supply chain depth. Domestic EV makers such as NIO and BYD standardize beam assist to meet NCAP protocols and differentiate their dashboards. Japanese tier-1s Koito and Stanley funnel matrix modules to both local and export programs, reinforcing regional leadership. South Korea aligns its semiconductor prowess with optical know-how, bringing integrated LED driver ASICs in-house for Hyundai and Kia platforms. India, while cost-sensitive, benefits from rising awareness of safety ratings as Bharat NCAP comes online, setting the stage for wider penetration after 2027.

Europe maintains a high installed base, though growth is moderating as the region faces economic headwinds. UNECE headlamp rules harmonize requirements across 27 member states, simplifying supplier validation. Luxury segments, especially German marques, continue to push pixel densities upward, making the continent a proving ground for high-resolution adaptive lamps. Eastern Europe’s contract assemblers adopt identical lighting harnesses, broadening reach without separate homologation costs. Energy-price fluctuations remain a minor drag but are partly offset by the OEM push to sell profitable technology bundles with every new EV.

North America follows closely, expanding at a 6.27% CAGR through 2031, with the 2022 NHTSA rule change catalyzing demand. Pickup trucks and large SUVs gain the most because their high eye-point exacerbates glare concerns, making adaptive beams an easy marketing win. Canada’s harsh winters validate performance claims in low-contrast snow, and United States insurers already offer premium discounts for IIHS “good” headlight ratings. Mexico leverages USMCA content rules to establish lamp-module export bases, reinforcing the continental supply web. Middle East and Africa, though smaller in absolute value, experiences the swiftest 8.59% CAGR as Gulf-state luxury imports and South African assembly clusters converge on global safety feature sets.

Competitive Landscape

The automatic high beam control market exhibits moderate concentration, leaving meaningful room for niche entrants. Koito Manufacturing leads, bolstered by mid-range LED matrices supplied to compact cars worldwide. HELLA and Valeo leverage electronics depth to pitch whole-system solutions that span optics, camera, and software stacks. Merger activity remains brisk. FORVIA’s 2022 acquisition of HELLA combined Faurecia’s cockpit-integration skills with HELLA’s lighting pedigree, creating scale for centralized ECU architectures[2]“Group Profile,” FORVIA, forvia.com.

Tier-2 specialists try to protect turf through patents on thermal management and pixel drivers, yet rising software content favors those who can finance algorithm development. Financial resilience is a growing separator. Marelli’s Chapter 11 filing in June 2025 illustrates balance-sheet fragility. OEMs hedge by dual-sourcing optics and drivers, but that raises validation costs. Larger groups with cash to fund cybersecurity compliance gain sales chatter advantage when pitching to procurement teams wary of supply disruptions.

Technology competition pivots from lumens to lines of code. Premium carmakers want beam patterns that integrate with navigation and V2X cues and demand real-time over-the-air updates. Suppliers invest in ADAS-grade chips that can segment 20,000 pixels per lamp without adding thermal burden. Strategically, patents around adaptive algorithms and optical coupling now matter as much as stamping dies once did, signaling a shift toward a more software-weighted race.

Automatic High Beam Control Industry Leaders

Koito Manufacturing

HELLA GmbH and Co. KGaA

Valeo SA

Stanley Electric

Marelli Automotive Lighting

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Toyota confirmed the Hyryder facelift will add Level 2 ADAS that includes auto high beam.

- August 2025: Hyundai announced the next-generation Venue will offer six standard airbags and Level 2 ADAS with high-beam assist.

- July 2025: Kia India unveiled an EV ecosystem ahead of the Carens Clavis EV launch and signaled inclusion of high-beam assist in the Level 2 ADAS suite.

- March 2025: Lexus India opened bookings for the LX 500d featuring Automatic High Beam and Adaptive High Beam System lighting.

Global Automatic High Beam Control Market Report Scope

The automatic high beam control market is segmented by technology, vehicle type, propulsion type, distribution channel, and geography. By technology, the market is segmented into camera-based systems, radar-based systems, LiDAR-based systems, and sensor fusion modules. By vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCVs), medium and heavy commercial vehicles (MHCVs), and buses and coaches. By propulsion type, the market is segmented into internal combustion engine (ICE), battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV), hybrid electric vehicle (HEV), and fuel cell electric vehicle (FCEV). By distribution channel, the market is segmented into OEM and aftermarket, and by geography, the market is segmented into North America, South America, Europe, Asia Pacific, and the Middle East and Africa.

The market forecasts are provided in terms of value (USD).

| Camera-Based Systems |

| Radar-Based Systems |

| LiDAR-Based Systems |

| Sensor Fusion Modules |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

| Buses and Coaches |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Camera-Based Systems | |

| Radar-Based Systems | ||

| LiDAR-Based Systems | ||

| Sensor Fusion Modules | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium and Heavy Commercial Vehicles (MHCVs) | ||

| Buses and Coaches | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the automatic high beam control space in 2026?

The automatic high beam control market is valued at USD 1.36 billion in 2026.

How fast is automatic high beam control expected to expand through 2031?

The automatic high beam control market revenue is projected to rise at an 8.23% CAGR from 2026-2031.

Which vehicle category shows the highest uptake of automatic high beam control?

Passenger cars hold 64.46% share and are also set to grow the quickest at a 10.29% CAGR.

Which region currently contributes the largest share to automatic high beam control sales?

Asia-Pacific accounts for 46.04% of global revenue due to strong EV production and advanced lighting supply chains.

Which technology sub-segment is recording the fastest growth rate?

Sensor-fusion modules are forecast to expand at an 11.57% CAGR, outpacing camera-only solutions.

Page last updated on: