Aluminum Caps And Closures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.65 Billion |

| Market Size (2031) | USD 9.02 Billion |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

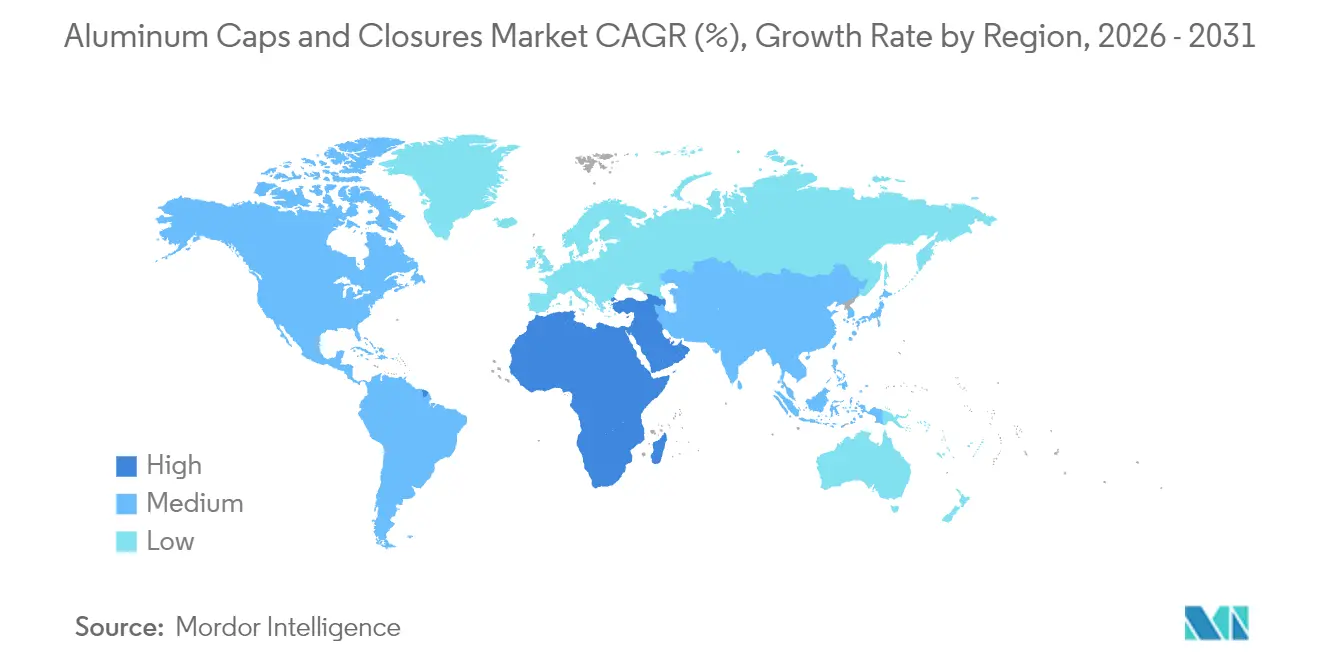

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

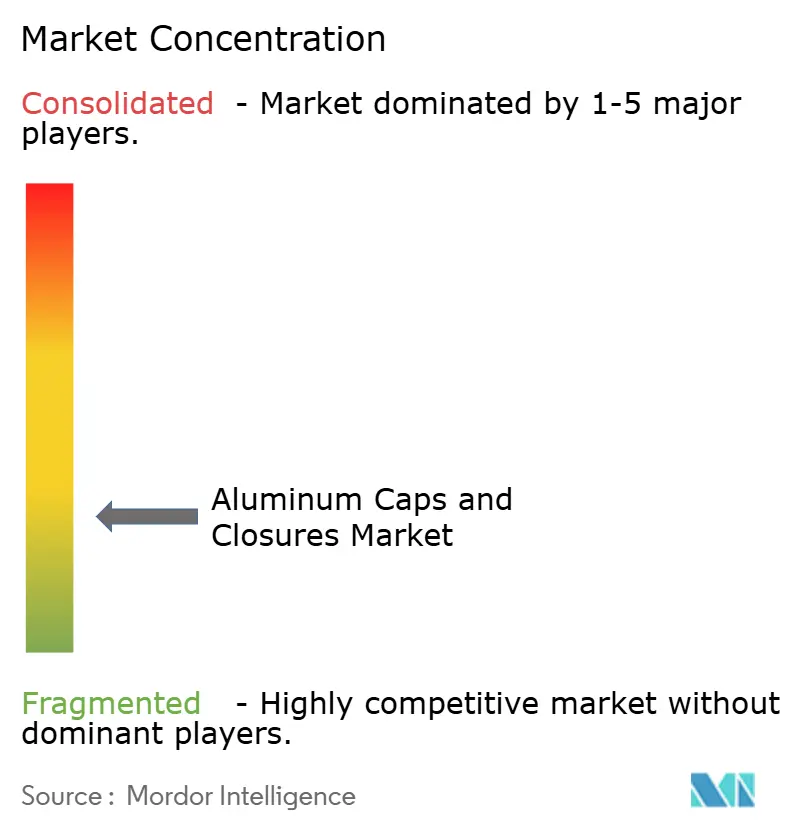

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Caps And Closures Market Analysis by Mordor Intelligence

The aluminium caps and closures market size is expected to grow from USD 7.40 billion in 2025 to USD 7.65 billion in 2026 and is forecast to reach USD 9.02 billion by 2031 at 3.34% CAGR over 2026-2031. Demand growth is paced, not explosive, because penetration in core beverage segments is mature; however, upgrades in premium spirits, biologics packaging, and EU sustainability rules continue to open profitable niches. Mandatory tethered-cap regulations in Europe, recycled-aluminium incentives in China, and a shift toward premium ready-to-drink offerings in North America are prompting brand owners to redesign closures with higher functional and aesthetic value. Volatility in London Metal Exchange (LME) pricing tightens converter margins, yet the push for infinitely recyclable materials still tilts preference toward aluminium over cork, steel, or plastic[1]Source: London Metal Exchange, “LME Aluminium,” lme.com . Regional cost advantages particularly additional recycled capacity in Asia-Pacific are helping offset raw-material swings while keeping premium segments insulated from low-cost PET alternatives.

Key Report Takeaways

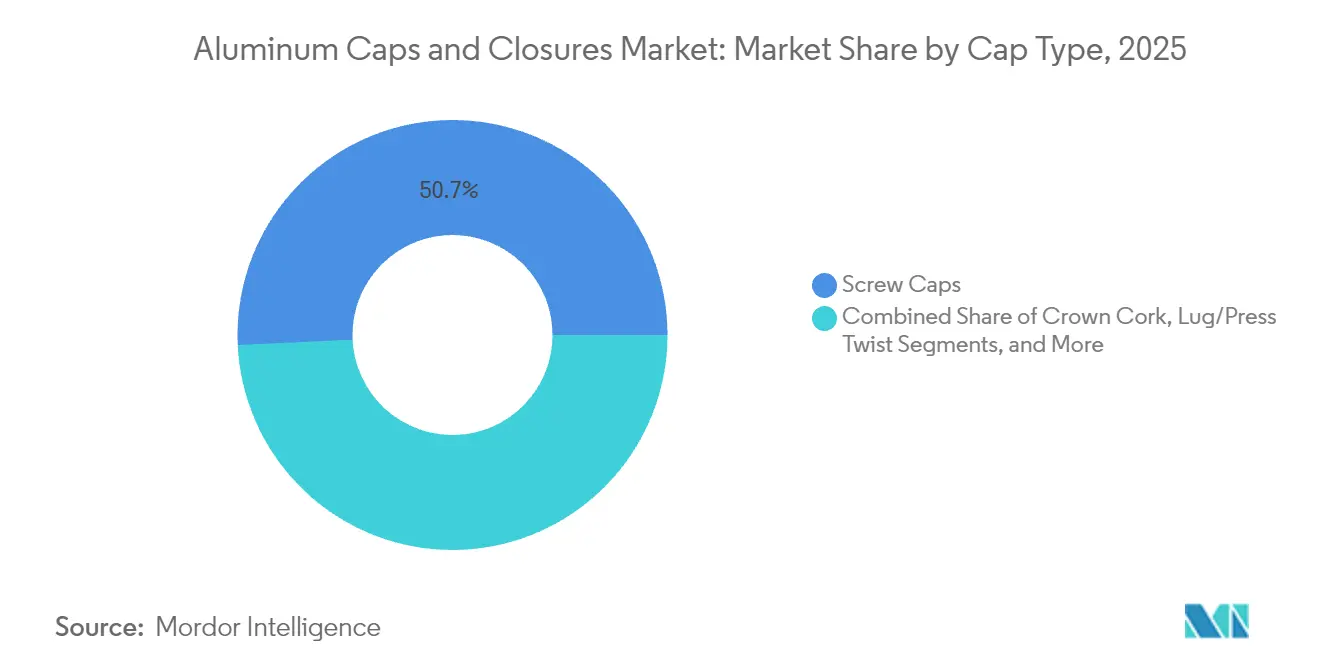

- By cap type, screw caps led with 50.74% of the aluminium caps and closures market share in 2025.

- By application, the beverage segment accounted for 46.02% of the aluminium caps and closures market size in 2025.

- By cap type, screw caps led with 50.74% of the aluminium caps and closures market share in 2025.

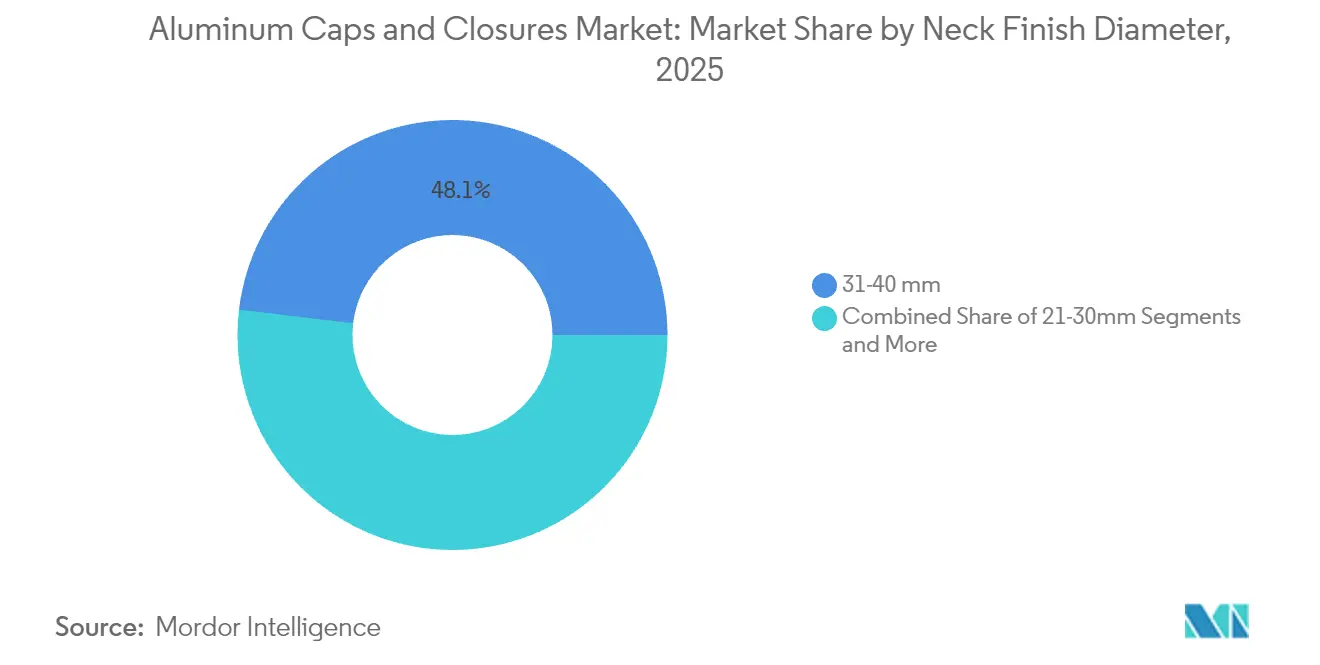

- By Neck Finish Diameter, 31-40 mm captured 48.12% of the aluminium caps and closures market size in 2025.

- By geography, Asia-Pacific held 40.20% revenue share of the aluminium caps and closures market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Caps And Closures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of premium RTD-cocktail aluminium bottling in North America | +0.8% | North America, spill-over to Europe | Medium term (2-4 years) |

| Mandatory transition to tethered caps in EU beverage packaging | +0.6% | Europe, potential global adoption | Short term (≤ 2 years) |

| Beverage-grade recycled aluminium capacity expansions in China | +0.5% | APAC core, global supply chain benefits | Long term (≥ 4 years) |

| Pharma shift to flip-off tear-down aluminium seals for biologics | +0.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Craft spirits’ migration from cork to aluminium ROPP in Europe | +0.3% | Europe, North America adoption | Long term (≥ 4 years) |

| E-commerce leakage-testing protocols driving lug-cap adoption in India | +0.2% | India, emerging APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of Premium RTD-Cocktail Aluminium Bottling in North America

Premium ready-to-drink cocktail brands introduced aluminium bottles throughout 2024 to signal upscale positioning while retaining recyclability. Several brands recorded 40–60% price premiums versus conventional cans, indicating consumers value tactile rigidity and re-close functionality. The barrier performance of aluminium protects botanical extracts from UV light and oxygen, supporting shelf life for spirit-based formulations. Brand collaborations with environmental non-profits reinforce sustainable credentials, creating a marketing halo that smaller steel or PET formats cannot match. The phenomenon is spilling into European travel-retail channels where single-serve spirits require tamper-evident yet elegant closures.

Mandatory Transition to Tethered Caps in EU Beverage Packaging (Directive 2019/904)

Since July 2024, EU beverage bottles must feature tethered closures, sparking redesign activity across carbonated soft drink and water segments.Early consumer pushback against plastic tethered systems led premium water and juice brands to adopt aluminium screw-top variants with integrated hinge mechanisms. Because aluminium is infinitely recyclable and easily detached in material-recovery facilities, brand owners meet both tethered-cap rules and forthcoming 90% metal-collection targets. Multinationals are harmonizing pack formats across non-EU markets to avoid line-change complexity, magnifying near-term demand for value-added aluminium closures.[2]Source: European Parliament, “Parliamentary Question | Tethered Bottle Caps,” europarl.europa.eu

Beverage-Grade Recycled Aluminium Capacity Expansions in China

China’s January 2025 tariff removal on imported recycled aluminium, paired with a policy exempting recycled content from the country’s 45 million-tonne primary cap, is shifting cost curves globally. Domestic mills quote beverage-grade coil at price points 8–12% below primary aluminium, enabling competitive exports of closure stock into Europe and the Americas. Western flat-rolled suppliers answered by announcing alliances aimed at 100% recycled beverage can sheet. While imports alleviate supply tightness, they also deepen scrutiny of traceability systems, accelerating blockchain pilots that certify post-consumer content.

Pharma Shift to Flip-Off Tear-Down Aluminium Seals for Biologics

Cold-chain breakage rates for mRNA vaccines highlighted weaknesses in rubber and plastic closure systems. Regulatory guidance in 2024 emphasized verified container closure integrity for parenterals stored at -20 °C or below, elevating aluminium tear-down seals to the default standard for new biologic drug applications. Contract development and manufacturing organizations retrofitted filling lines with ISO 15378-qualified sealers, creating high switching costs that favor incumbent suppliers. As biologics accelerate from 48% of FDA approvals in 2024 to a projected majority before 2030, aluminium closure demand in pharmaceutical contexts expands in tandem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile LME aluminium prices compressing converter margins | -0.7% | Global, acute in price-sensitive segments | Short term (≤ 2 years) |

| Brand-owner switch to PET tethered caps in carbonated soft drinks | -0.4% | Europe, potential global adoption | Medium term (2-4 years) |

| Tin-free steel crown-cork substitution in Mexican beer | -0.3% | Mexico, Latin America expansion | Long term (≥ 4 years) |

| Limited food-grade recycling streams in Middle East | -0.2% | Middle East, North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile LME Aluminium Prices Compressing Converter Margins

Aluminium ingot reached USD 2,662 per ton in February 2025, swinging more than 15% within six months and squeezing converters that sell on long-term fixed contracts. Smaller closure firms without hedging programs face eroded margins, making them attractive acquisition targets for multinationals with advanced risk-management desks. Russian export uncertainty, elevated European smelting power costs, and new US container duties all amplify volatility. To stabilize supply, leading converters raise recycled content and explore alloy recipes with higher scrap tolerance, an approach aligned with carbon-reduction pledges yet requiring capital spend on upgraded annealing furnaces.

Brand-Owner Switch to PET Tethered Caps in Carbonated Soft Drinks

Global soft-drink majors opted for PET tethered closures across mainstream SKUs to comply with EU rules at the lowest unit cost. Because these beverages operate on razor-thin per-serving margins, aluminium cannot always match PET economics. Closure makers catering to carbonated categories therefore reposition aluminium as a premium upgrade reserved for flagship products where visual impact and “plastic-free” messaging justify price differentials. The bifurcation underscores the need for solution selling rather than volume chasing in price-sensitive channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cap Type: Easy-Open Innovation Drives Growth

Screw caps retained dominance with 50.74% share in 2025 as they span beverages, condiments, and pharmaceuticals. That share equals USD 3.75 billion of the aluminium caps and closures market size in 2025, reflecting their proven sealing reliability. Easy-open ends, while smaller, are gaining fastest at a 6.38% CAGR through 2031 as consumers gravitate toward convenience features in canned coffee and ready meals. Continuous-thread ROPP variants secure traction in craft spirits because they reconcile tamper evidence with luxury visual cues. Crown corks hold relevance in traditional beer packaging, yet their growth is modest given the migration toward full-body slim cans. Lug, press-twist, and specialized flip-off designs serve tamper-sensitive food and pharma uses, illustrating the segmentation’s shift from generalist to application-specific solutions.

Investment is flowing into die-cutting and scoring technologies that create safer, finger-friendly easy-open tabs, unlocking new mass channels like senior-nutrition beverages. Closure makers are also integrating laser-etched QR codes for trace-and-trace compliance without compromising decoration space. These embellishments carry higher unit economics, cushioning margins when raw-material costs rise. In contrast, standard screw-cap formats face commoditization, pressing manufacturers to differentiate through liner chemistry improvements that extend shelf life in aggressive-pH drinks.

By Application: Pharmaceutical Biologics Accelerate Demand

Beverages commanded 46.02% share in 2025, equivalent to USD 3.41 billion of the aluminium caps and closures market. The segment covers still water, carbonated drinks, beer, wine, and premium spirits, each with nuanced closure needs. Premium alcohol producers elevate aluminium as a branding canvas, whereas carbonated soft-drink fillers chase lowest cost compliance to EU tethering. Pharmaceutical demand is expanding at a 6.76% CAGR, adding USD 284 million incremental value by 2031. Growth rests on biologic drug launches that specify flip-off tear-down seals to ensure sterile integrity. Food applications remain steady, propelled by gourmet oils and sauces pursuing metal lug caps for smooth pour control. Personal-care brands leverage aluminium’s recyclability story to displace mixed-material lids, evidenced by high-profile deodorant launches in recyclable aluminium aerosols.

Cross-sector learning accelerates innovation: beverage can suppliers partner with personal-care companies to adapt internal varnishes for lotion compatibility, broadening addressable markets. Industrial chemical closures, though niche, benefit from aluminium’s corrosion resistance when combined with specialty liners. The versatility across end-uses supports balanced portfolio exposure, hedging against cyclical dips in any one sector.

By Neck Finish Diameter: Mid-Range Dominance Reflects Versatility

Closures sized 31-40 mm captured 48.12% of revenue in 2025, translating to USD 3.56 billion of the aluminium caps and closures market size. They fit standard wine, premium water, and spirit bottles, making them the workhorse of the industry. The 21-30 mm segment is set to expand at 5.52% CAGR as craft beverage brands and functional water players adopt slender bottle profiles to signal modernity. Sub-20 mm diameters cater to ampoules, vials, and single-dose nutraceutical shots where dosing accuracy is vital. Large diameters above 40 mm address wide-mouth condiments, sports-nutrition powders, and household chemicals areas with steady if unspectacular growth.

Manufacturers are investing in adjustable forming lines to shift swiftly between neck-finish sizes, lowering inventory risk. Lightweighting initiatives focus on mid-range diameters where demand density justifies tooling upgrades, yielding 5-8% material savings per closure without compromising performance. Such gains are instrumental in buffering LME volatility and meeting corporate emissions targets.

By Distribution Channels: Direct Sales Maintain Technical Advantage

Direct engagement delivered 78.10% of 2025 revenue because closure development often intertwines with filler-line geometry, liner selection, and artwork integration. Major suppliers embed engineers within customer sites, creating sticky relationships and multi-year tooling amortization structures. Indirect channels distributors and e-commerce portals grow at 4.21% CAGR, supplying regional craft brewers and SME food packers seeking smaller order quantities. Digital configurators now allow small buyers to specify liner compound, print colors, and embossing online, compressing design-to-delivery cycles to under four weeks.

In emerging markets, distributors leverage local language support and regulatory guidance, filling a knowledge gap for brands new to food-contact and child-resistant norms. Meanwhile, global procurement teams of multinational FMCGs still favor direct contracts to secure capacity during demand spikes. The coexistence of high-touch technical collaboration and quick-turn commodity distribution underscores the dual-speed nature of the aluminium caps and closures industry.

Geography Analysis

Asia-Pacific anchored 40.20% of global revenue in 2025, driven by China’s prolific beverage output and India’s packaged-goods expansion. Cost competitiveness improved after November 2024 when China abolished tariffs on imported recycled aluminium, enabling mills to supply coil at discounts versus primary metal. Japan and South Korea added a layer of technological sophistication, exporting closure presses and vision-inspection systems regionally. Southeast Asian demand benefitted from urbanization and Western quick-service restaurant chains insisting on tamper-proof lids, stimulating local cap conversion lines. India’s standards upgrade mandating QR traceability for edible-oil packs nudged value share toward premium lug caps, attracting foreign joint ventures.

The Middle East and Africa represent the fastest-growing territory, forecast at 6.89% CAGR through 2031. Beverage investments in Nigeria and Kenya, plus desalinated bottled-water capacity in the Gulf, underpin volume. However, limited circular-economy infrastructure tempers aluminium caps and closures market penetration. Egypt’s move to establish a dedicated food-grade recycling mill marks progress, yet widespread adoption awaits proof of economically viable collection streams. South Africa’s established aluminium smelter base and port connectivity create export opportunities into landlocked neighbors.

Europe, though mature, remains pivotal because regulation steers global specifications. The July 2024 tethered-cap deadline forced fillers to redesign PET and aluminium containers simultaneously, generating engineering consulting revenue for closure specialists. Germany’s mechanical-engineering cluster pioneered continuous-thread screw-top machines capable of 600 cpm with integrated torque monitoring, raising performance benchmarks. Italy’s design houses customized embossing and color-shift inks for premium spirits, preserving perceived luxury even as closures migrate from cork to aluminium for sustainability reasons.

North America’s market rides consumer migration to craft beverages and ready-to-drink cocktails packaged in resealable aluminium bottles. US tariff barriers imposed in April 2025 boosted domestic can-stock production, indirectly supporting closure coil producers by tightening local supply and encouraging reshoring. Mexico, a major beer exporter, toggles between aluminium and steel closure options to balance cost and supply risk, yet aluminium retains a foothold in premium bottle lines destined for European customers. South America, led by Brazil, invests in new beverage can lines that include in-house closure modules, shortening lead times.

Competitive Landscape

The aluminium caps and closures market exhibits low concentration. Crown Holdings, Silgan, and Guala Closures dominate high-volume contracts for global beverage brands, leveraging economies of scale and vertically integrated coil sourcing. Crown reported 24% beverage-can segment income growth in Q1 2025, attributing performance to robust demand in Brazil and Europe as well as productivity gains in newly automated lines. Silgan’s EUR 838 million acquisition of Weener Packaging in January 2025 expanded its specialty-closure footprint, particularly in European personal-care markets, while adding design centers that cross-pollinate aesthetics across sectors.

Competitive intensity is escalating as can-sheet producers push downstream into closures to secure margin capture. Amcor’s April 2025 all-stock merger with Berry Global integrated films, dispensing systems, and metal-closure know-how, creating a one-stop packaging supplier with USD 650 million synergy targets. Regional challengers in Asia-Pacific and Latin America differentiate through shorter lead times and proximity to low-cost scrap pools, attracting second-tier beverage fillers. Intellectual-property filings reveal a surge in tethered-aluminium classifications and child-resistant reseal mechanisms, signaling technological races beyond simple diameter or threading changes.

Digitalization of quality control camera-based seal inspection linked to factory analytics has become table stakes for winning pharmaceutical and premium-spirit contracts. Established players deploy inline X-ray porosity scanners and real-time torque analytics, translating into lower recall risk for customers. Sustainability credentials also weigh heavily: Novelis’ 3x30 initiative targets 75% recycled content by 2030, positioning the company favorably for brand owners with net-zero pledges. Smaller firms unable to document recycled content or energy intensity face procurement exclusion from top clients, nudging the sector toward gradual consolidation.

Aluminum Caps And Closures Industry Leaders

Amcor Plc

O.Berk Company

Reynolds Packaging Group Ltd

Pelliconi & C. SpA

Nippon Closures Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The United States imposed 25% tariffs on imported canned beer and empty aluminium cans, increasing packaging costs for companies such as Constellation Brands.

- January 2025: China reduced import tariffs on recycled aluminium to zero, effective 1 January 2025, supporting domestic carbon-neutrality objectives.

- January 2025: Silgan Holdings completed its EUR 838 million acquisition of Weener Packaging, expanding its Dispensing and Specialty Closures network.

- July 2024: EU Directive 2019/904 requiring tethered caps on beverage bottles came into force, spurring aluminium-closure innovation.

Global Aluminum Caps And Closures Market Report Scope

The report on the aluminum caps and closures market studies the various segments that manufacture different types of aluminum caps and closures with applications in various end-user segments. It also analyzes the demand-supply pattern of aluminum cap stock or rolled sheets pertaining to geographies. The different applications of aluminum caps and closures are in sectors like beverages, foods, pharmaceuticals, cosmetics, and other end-users, such as paints, coatings, and chemicals.

| Screw Caps |

| Crown Cork |

| Lug / Press-Twist |

| Easy-Open End |

| Roll-On Pilfer Proof (ROPP) |

| Others (Flip-Off, Tear-Down) |

| Beverages | Alcoholic Beverages |

| Non-Alcoholic Beverages | |

| Food | |

| Pharmaceutical | |

| Cosmetics and Personal Care | |

| Industrial and Household Chemicals |

| Less than and Equal to 20 mm |

| 21-30 mm |

| 31-40 mm |

| More than 40 mm |

| Direct Sales Channels |

| Indirect Sales Channels |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| United Kingdom | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Cap Type | Screw Caps | ||

| Crown Cork | |||

| Lug / Press-Twist | |||

| Easy-Open End | |||

| Roll-On Pilfer Proof (ROPP) | |||

| Others (Flip-Off, Tear-Down) | |||

| By Application | Beverages | Alcoholic Beverages | |

| Non-Alcoholic Beverages | |||

| Food | |||

| Pharmaceutical | |||

| Cosmetics and Personal Care | |||

| Industrial and Household Chemicals | |||

| By Neck Finish Diameter | Less than and Equal to 20 mm | ||

| 21-30 mm | |||

| 31-40 mm | |||

| More than 40 mm | |||

| By Distribution Channels | Direct Sales Channels | ||

| Indirect Sales Channels | |||

| By Region | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| Italy | |||

| United Kingdom | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the aluminium caps and closures market?

The market was valued at USD 7.65 billion in 2026 and is projected to reach USD 9.02 billion by 2031 at a 3.34% CAGR.

Which cap type holds the largest share?

Screw caps commanded 50.74% of global revenue in 2025, reflecting their versatility across beverage, food, and pharmaceutical products.

Why are aluminium closures gaining traction in pharmaceuticals?

Flip-off and tear-down aluminium seals meet stringent container-closure integrity requirements for biologics, supporting 6.76% CAGR growth in the pharmaceutical segment.

How will EU tethered-cap regulations influence the market?

Directive 2019/904 accelerates adoption of innovative aluminium tethered designs, particularly for premium beverages, and is adding +0.58% to projected market CAGR.

Which region will grow fastest through 2031?

The Middle East and Africa are forecast to expand at 6.89% CAGR due to rising beverage production and modernization of packaging formats.

How are raw-material price swings affecting suppliers?

Volatile LME aluminium pricing pressures margins, encouraging converters to boost recycled content and hedge metal exposure through long-term coil contracts.

Page last updated on: