Australia Insulin Delivery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

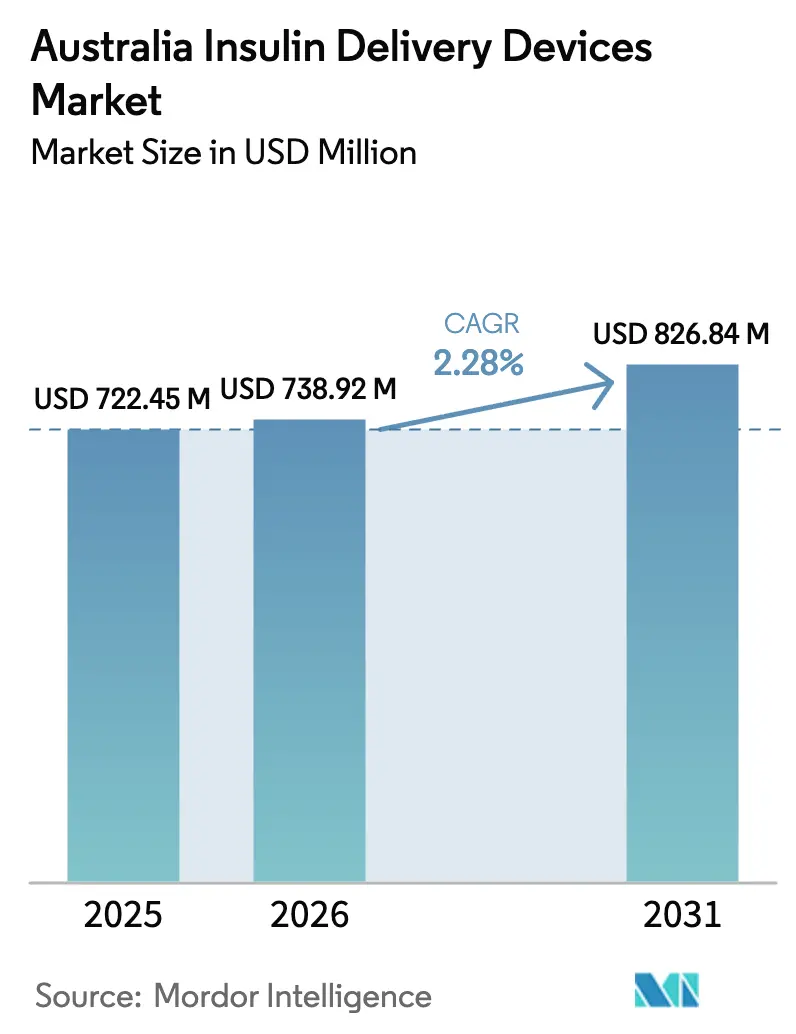

| Base Year Market Size (2025) | USD 722.45 Million |

| Market Size (2026) | USD 738.92 Million |

| Market Size (2031) | USD 826.84 Million |

| Growth Rate (2026 - 2031) | 2.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Insulin Delivery Devices Market Analysis by Mordor Intelligence

Australia insulin delivery devices market size in 2026 is estimated at USD 738.92 million, growing from 2025 value of USD 722.45 million with 2031 projections showing USD 826.84 million, growing at 2.28% CAGR over 2026-2031. This tempered growth reflects an industry moving from rapid expansion to measured maturation, balancing an expanding diabetes population with competitive pressure from GLP-1 therapies that can defer insulin use[1]Australian Bureau of Statistics, “National Health Survey 2024,” abs.gov.au. Persistent diabetes prevalence, wider reimbursement of advanced devices under the National Diabetes Services Scheme (NDSS), and continuous glucose monitoring (CGM) integration keep demand resilient even as some type 2 patients delay insulin initiation. Manufacturers focus on hardware–software ecosystems that automate dosing decisions, opening premium-priced niches and longer lifetime revenue per user. Consumables growth outpaces hardware because every new pump placement locks in years of infusion-set and sensor sales. At the same time, telehealth infrastructure built during the pandemic now supports remote pump programming, improving rural access and reducing the clinical overhead tied to device initiation.

Key Report Takeaways

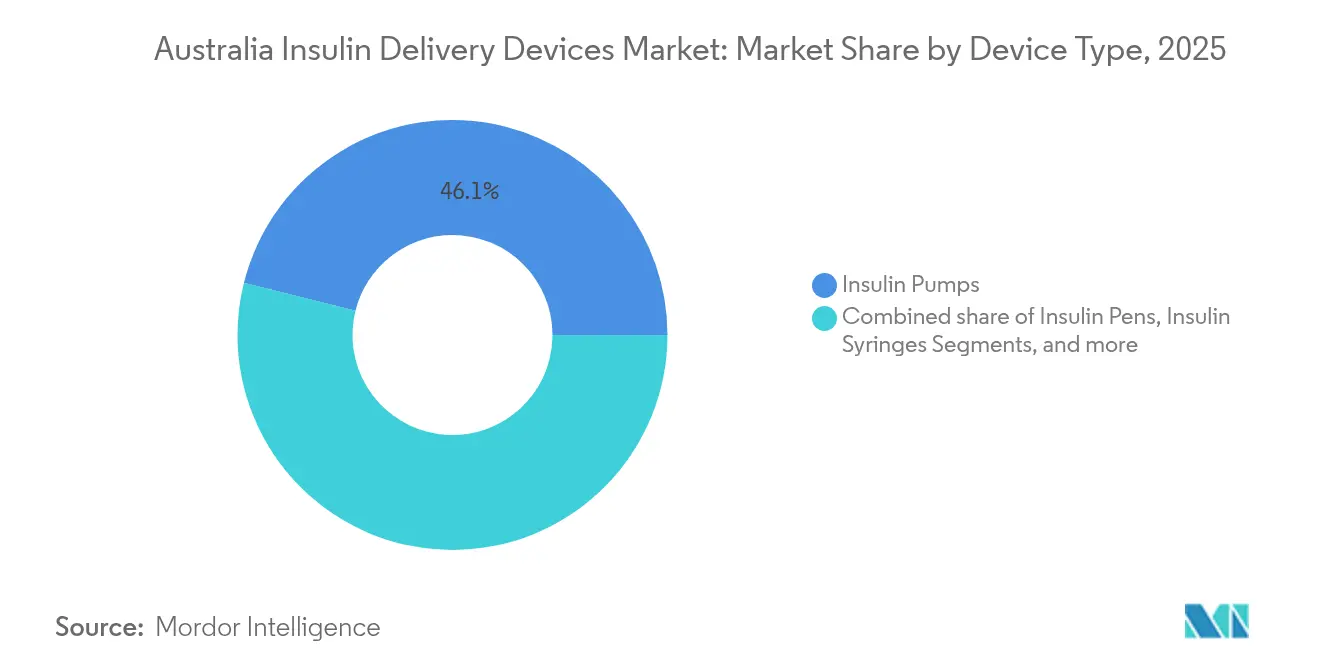

- By device type, insulin pumps captured 46.10% of the Australia insulin delivery devices market share in 2025, while smart patch pumps are forecast to grow at a 5.39% CAGR to 2031.

- By component, delivery devices accounted for 63.05% of the Australia insulin delivery devices market size in 2025; consumables are projected to rise at a 5.62% CAGR through 2031.

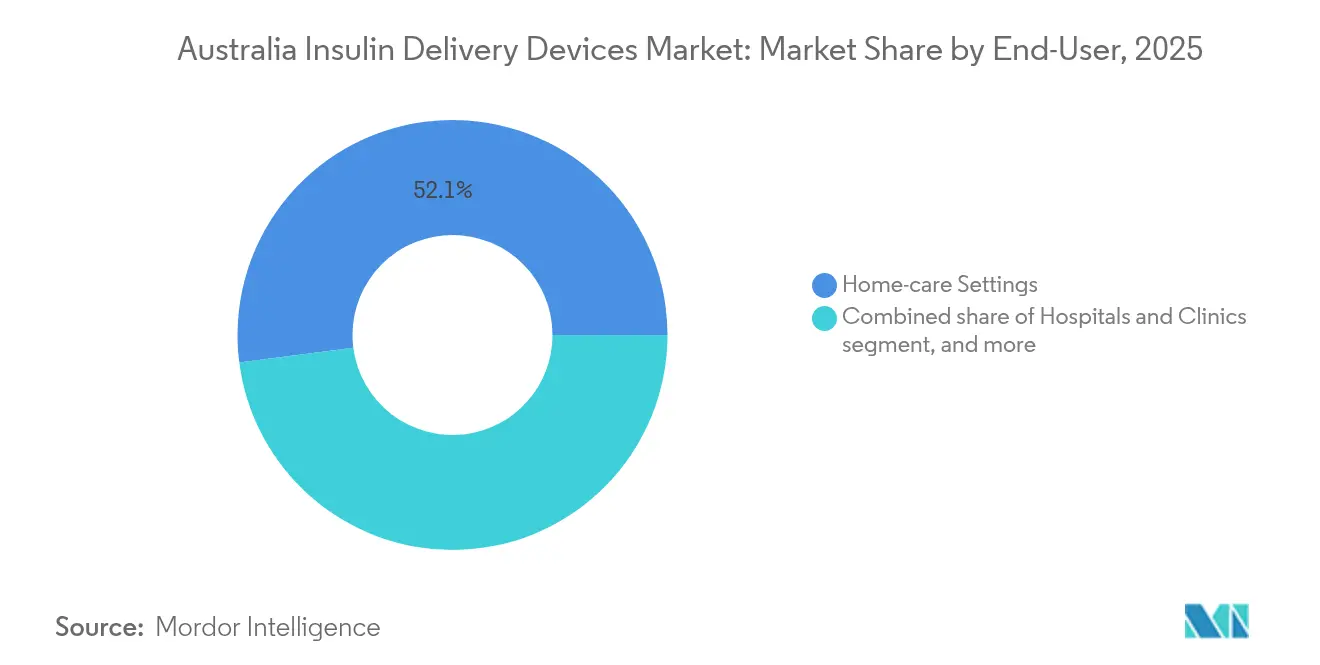

- By end-user, home-care settings represented 52.05% of the Australia insulin delivery devices market in 2025 and are advancing at a 6.08% CAGR to 2031.

- By distribution channel, retail pharmacies led with 41.05% share in 2025, whereas online pharmacies record the highest projected CAGR at 4.33% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Insulin Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes in Australia | +0.8% | National, higher concentration in urban areas | Long term (≥ 4 years) |

| NDSS & private-insurance pump subsidies | +0.6% | National, stronger effect in metropolitan hubs | Medium term (2-4 years) |

| CGM-enabled closed-loop system integration | +0.5% | National | Medium term (2-4 years) |

| Ageing & obesity-driven demand growth | +0.4% | National, pronounced in regional communities | Long term (≥ 4 years) |

| Telehealth-enabled remote pump programming | +0.3% | National, with greatest benefit in rural areas | Short term (≤ 2 years) |

| GLP-1 side-effect rebound to basal insulin therapy | +0.2% | National, concentrated in private healthcare | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Of Diabetes In Australia

Official surveys show 6.6% of Australian adults live with diabetes, yet University of Sydney researchers estimate the real number is 35% higher, lifting the patient pool above 2 million. The gap stems from under-registration in the NDSS, indicating latent demand that comes into the commercial funnel as detection improves. Urban clusters match the supplier network of major pump distributors, easing after-sales support. Earlier onset among younger cohorts extends lifetime therapy duration, which heightens interest in tech-forward pumps, pens, and connected wearables that fit digital lifestyles.

Expansion Of NDSS & Private Insurance Subsidies For Pumps

Since March 2025 the NDSS has subsidised Dexcom G7 and, from April 2025, Abbott FreeStyle Libre 2 Plus sensors, lowering out-of-pocket costs for hybrid closed-loop therapy[2]National Diabetes Services Scheme, “Product and Subsidy Updates 2024–25,” ndss.com.au. Private insurers follow suit: Insulet’s OmnipodPromise covers waiting periods so members can transition immediately to Omnipod 5. Medtronic runs “Bridging the Gap,” supplying MiniMed 780G during insurance onboarding. Combined public-private funding dismantles cost barriers for roughly 18,000 Australians judged clinically eligible for automated insulin delivery systems[3]Australian Government Department of Health, “Type 1 Diabetes Clinical Research Network Funding Announcement,” health.gov.au.

Integration Of CGM-Enabled Closed-Loop Systems

Meta-analyses of nearly 14,000 European users show hybrid closed-loop therapy delivers 64% time-in-range versus 52% for open-loop care, while cutting severe hypoglycaemia rates. Australia benefits from near-simultaneous global launches: MiniMed 780G offers the highest published time-in-range among seven commercial systems, Omnipod 5 arrived in March 2025 with Dexcom G6/G7 compatibility, and Tandem’s t:slim X2 now reads Abbott Libre 2 Plus data. Convergence reduces multi-device complexity, raising uptake among both newly diagnosed and long-term users.

Ageing & Obesity-Driven Demand Growth

Diabetes was Australia’s sixth-leading cause of death in 2023, a burden amplified by population ageing and youth obesity. Older patients value automation that lightens daily disease management, while tech-savvy younger users push for smartphone-integrated dose capture such as NovoPen 6’s automatic logging feature. Telehealth closes rural service gaps, letting clinicians fine-tune settings remotely, which is critical as regional obesity rates outpace metropolitan averages and drive fresh insulin starts.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & consumable costs of advanced devices | -0.7% | National, heavier burden in regional areas | Medium term (2-4 years) |

| Rapid uptake of GLP-1 weight-loss drugs reducing insulin demand | -0.5% | National, strongest in urban private care | Medium term (2-4 years) |

| Patchy reimbursement for consumables outside NDSS | -0.4% | National, varies by private insurer | Medium term (2-4 years) |

| Supply-chain vulnerability for single-use consumables | -0.3% | National, influenced by import dependence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront & Consumable Costs Of Advanced Devices

Even after NDSS discounts, annual consumable spend for a pump user—infusion sets, reservoirs, sensors—can exceed USD 1,000, a notable outlay for middle-income households. Supply interruptions, such as the April 2024 withdrawal of particular Medtronic infusion sets, intensify cost by forcing brand switches or emergency purchases. Insurance coverage varies: some funds now cap Ozempic rebates and tightly manage device benefits, creating postcode-dependent access.

Rapid Uptake Of GLP-1 Weight-Loss Drugs Reducing Insulin Demand

GLP-1 agonists like Ozempic diminish HbA1c and aid weight loss, delaying insulin initiation for many type 2 patients. Analysts project the global GLP-1 segment could reach USD 150 billion by 2032, siphoning growth from traditional insulin delivery channels. As the Therapeutic Goods Administration reviews Wegovy for cardiovascular indications, broader prescribing could further suppress basal-insulin starts, trimming potential pump conversions[4]Therapeutic Goods Administration, “Consultation on GLP-1 Compounding Exemptions,” tga.gov.au.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Pumps Lead Despite Patch Innovation

Insulin pumps captured a 46.10% slice of the Australia insulin delivery devices market in 2025, a dominance rooted in proven glycaemic benefits and expanding reimbursement. MiniMed 780G users achieve superior time-in-range, reinforcing trust in tubed pumps. Yet patch pumps are the growth engine, set for a 5.39% CAGR through 2031 as Omnipod 5 and emerging tubeless rivals lower insertion anxiety and simplify wear. As a result, patch platforms are poised to lift their share of the Australia insulin delivery devices market size for type 1 cohorts between 2026 and 2031.

Smart pens remain essential for cost-sensitive type 2 patients. NovoPen 6 and similar devices log doses automatically, supporting tele-review without adding pump-level expense. Syringes and jet injectors continue a slow decline because consumers migrate toward simpler, connected options. Embecta’s coming patch pump for type 2 users and Sequel’s modular twiist system hint at a bifurcated future: premium closed-loops for intensive users and pared-down wearables for the broader population.

By Component: Delivery Devices Dominate Revenue Streams

Hardware generated 63.05% of revenue in 2025, underpinned by multi-thousand-dollar pump placements that anchor therapy for 4–5 years. Consumables follow a razor-and-blade model and post the steeper 5.62% CAGR as every pump user consumes infusion sets every 2–3 days and CGM sensors every 10 days. Because each active user represents annuity-style revenue, boosting the installed base enlarges lifetime value even if hardware ASPs flatten.

Supply security is critical. The April 2024 exit of certain Medtronic infusion sets highlighted vulnerability and encouraged wider stocking of alternate brands through NDSS logistics. Extended-wear sets now promise up to 7 days use, improving convenience but also trimming raw unit volumes. Nonetheless, sensor adoption attached to pumps is rising rapidly enough to sustain consumables momentum, cementing half of future Australia insulin delivery devices market size growth in recurring supplies.

By End-User: Home-Care Settings Drive Market Expansion

Home-care represented 52.05% of 2025 revenue and is tracking a 6.08% CAGR to 2031 as technology enables safe self-management. Telehealth sessions covered under Medicare let clinicians adjust basal rates or deliver bolus coaching without clinic visits, a benefit keenly felt in remote regions. Hospital initiation persists for new pump starts, but once configured, most users transition to community follow-up.

Covid-era digital tools now underpin routine education: Medtronic’s Smart MDI cloud dashboard and Tandem’s mobile bolus app give providers real-time data feeds, shifting labour from in-person to virtual care. This structural change anchors the Australia insulin delivery devices market as a patient-centred, service-rich domain that both improves outcomes and unlocks broader geographic penetration.

By Distribution Channel: Retail Dominance Faces Digital Disruption

Retail pharmacies held 41.05% share in 2025 thanks to their advisory role and established reimbursement workflows. Yet online platforms are scaling at a 4.33% CAGR as repeat pod or sensor orders move to subscription models. Tandem’s 2025 plan to sell pumps directly through pharmacies blurs channel lines and demands pharmacist upskilling.

Meanwhile, direct-to-consumer web stores tie into tele-consults, making device renewals seamless. Hybrid pathways will likely prevail, where initial prescription flows through endocrinologists and hospital pharmacies, but consumable replenishment migrates online. This omnichannel shift keeps the Australia insulin delivery devices market accessible even in territories lacking brick-and-mortar capacity.

Geography Analysis

Australia’s patchwork of densely populated coasts and sparsely settled interiors shapes device uptake. Urban centres, Sydney, Melbourne, Brisbane, house the bulk of endocrinologists and pump training clinics, which accelerates hybrid closed-loop adoption among city dwellers. Regional diabetes rates run lower on a percentage basis yet remain material in absolute numbers; combined with fewer specialists, this drives reliance on tele-enabled pumps and smart pens that clinicians can program remotely. NDSS reimbursement rules apply nationwide, but practical access still hinges on freight logistics and local pharmacy inventories.

The Australian Government’s USD 50.1 million support for the Type 1 Diabetes Clinical Research Network clusters most trial activity around metropolitan research hospitals, reinforcing a city-centric innovation loop. Conversely, rural communities benefit when device suppliers fold training into virtual care packages, limiting travel burdens. Novel oral-insulin work emerging from the University of Sydney could, if successful, further democratise access by removing insertion requirements altogether.

CGM-pump ecosystems that store data in the cloud compress distance; clinicians fine-tune parameters anywhere an internet connection exists. This tele-support capacity helps the Australia insulin delivery devices market maintain penetration even in low-density areas where shipping consumables can take days and in-person endocrinology visits are quarterly at best. Continual government investment in rural broadband promises to buttress long-run uptake across all postcodes.

Competitive Landscape

Global diabetes technology leaders Medtronic, Insulet, and Tandem anchor the domestic field, together generating more than 55% of sales in 2024. Medtronic leans on algorithmic leadership; MiniMed 780G plus Simplera CGM delivered 12.4% segment revenue growth in Q2 FY25 by driving time-in-range gains. Insulet’s tubeless design recorded 22% revenue expansion in 2024 and landed in Australia in March 2025, intensifying competition for pump upgrades. Tandem booked USD 940.2 million in 2024, up 26%, and differentiated through an open-sensor stance integrating both Dexcom and Abbott data streams.

Emerging challengers address white-space segments. Embecta filed an FDA submission for a disposable patch pump tailored to type 2 patients, historically underserved by premium closed-loop systems. Sequel Med Tech’s modular twiist uses Tidepool Loop software and interchangeable parts to cut upgrade friction while accepting multiple CGM brands. Local biotech EndoAxiom pursues oral insulin that could sidestep injection devices entirely, backed by a USD 5 million Proto Axiom investment.

Big-tech firms hold glucose-sensing patents that foreshadow deeper convergence: Samsung and Apple each filed smartwatch CGM applications, setting up potential alliances with pump vendors. Competitive edge is shifting from pure hardware features to full-stack ecosystems—connectivity, data analytics, and reimbursement programs that smooth patient onboarding. Firms that orchestrate open platforms around insurance pipelines and telehealth services are best placed to capture incremental Australia insulin delivery devices market share as growth decelerates into maturity.

Australia Insulin Delivery Devices Industry Leaders

Insulet Corporation

Ypsomed

Novo Nordisk A/S

Medtronic

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Insulet launched Omnipod 5 in Australia via AMSL Diabetes, marking the first tubeless automated insulin delivery system compatible with Dexcom G6/G7 and Libre 2 Plus.

- March 2024: Sequel Med Tech paired its twiist pump with Abbott Libre 3 Plus, broadening sensor choice for modular closed-loop therapy.

- February 2025: The Australian Government allocated USD 50.1 million to the Type 1 Diabetes Clinical Research Network to accelerate prevention and cure programs.

- November 2024: Medtronic gained FDA clearance for an upgraded InPen app, paving the way for a Smart MDI suite combining Simplera CGM with dose-calculation software.

- June 2024: Proto Axiom invested USD 5 million in University of Sydney spin-out EndoAxiom to develop oral insulin formulations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Australian insulin delivery devices market as revenue earned in-country from newly sold insulin pumps (tethered and patch), insulin pens (disposable, reusable and smart), pen needles, jet injectors, and insulin syringes that administer therapeutic insulin at home or in clinical settings. Values are captured at ex-factory level before any retail mark-ups.

Scope exclusion: stand-alone continuous glucose monitors and all insulin drug sales sit outside this computation.

Segmentation Overview

- By Device Type

- Insulin Pumps

- Patch Pumps

- Traditional Pumps

- Insulin Pens

- Reusable Pens

- Disposable Pens

- Insulin Syringes

- Insulin Jet Injectors

- Smart Insulin Delivery Wearables

- Insulin Pumps

- By Component

- Delivery Devices

- Consumables (Reservoirs, Cartridges, Infusion Sets, Needles)

- By End-User

- Hospitals & Clinics

- Home-care Settings

- Ambulatory Surgical Centres

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists across three states, hospital buyers, certified pump educators, and leaders of diabetes consumer groups. Their guidance sharpened uptake ratios, average selling prices, and the early traction of smart wearables, filling gaps left by public data.

Desk Research

We began by mining Australian Institute of Health and Welfare diabetes datasets, ABS prevalence micro-sets, NDSS subsidy volumes, and Therapeutic Goods Administration device registers. Those official numbers were blended with Diabetes Australia position papers, peer-reviewed work in Diabetes Care, respected press coverage, and listed-company filings to anchor prices and unit swings. Paid portals such as D&B Hoovers for supplier revenue and Dow Jones Factiva for deal flow helped us flag anomalies that required follow-up. The sources mentioned are illustrative only, and many others informed our desk work.

Second, we tracked policy moves, import statistics, private insurance reimbursements, and tender notices that influence volume or price trends. This continuous scan ensured the model reflects real-time shifts rather than static snapshots.

Market-Sizing & Forecasting

We apply a top-down prevalence-to-treated cohort build. Australia's diabetics are narrowed to insulin users, which are then split by device type using NDSS claim ratios and import audits. Select bottom-up checks, sampled ASP multiplied by annual units, keep totals grounded. Key variables modeled include pump penetration, pen-needle pack price, GLP-1 substitution pressure, subsidy ceilings, and replacement cycles, with a multivariate regression projecting every driver to the forecast period. The single mention of top-down and bottom-up highlights how results are cross-checked.

Data Validation & Update Cycle

Outputs clear three internal review layers before a senior analyst sign-off. We refresh the file yearly and issue interim flashes whenever technology or policy shifts materially.

Why Mordor's Australia Insulin Delivery Devices Baseline Figures Stand Firm

Published estimates often diverge because some studies fold drug revenue into devices, others drop consumables, and many freeze exchange rates.

By locking scope, refreshing each year, and validating assumptions with frontline experts, Mordor Intelligence offers buyers a balanced, transparent baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 722.45 M (2025) | Mordor Intelligence | - |

| USD 250 M (2023) | Regional Consultancy A | Counts pen needles only, ignores pumps and pens |

| USD 180 M (2028) | Global Consultancy B | Models smart pumps only, uses aggressive currency parity |

The contrast shows that once full device breadth and current pricing are applied, our baseline remains the most dependable foundation for planning.

Key Questions Answered in the Report

What is the current value of the Australia insulin delivery devices market?

The market stands at USD 738.92 million in 2026 and is projected to reach USD 826.84 million by 2031 at a 2.28% CAGR.

Which device category holds the largest share?

Conventional and hybrid insulin pumps lead with 46.10% of 2025 revenue, driven by broad clinical adoption and subsidy support.

How fast are patch pumps growing in Australia?

Smart, tubeless patch pumps are registering a 5.39% CAGR to 2031, making them the fastest-expanding device sub-segment.

Why are consumables such a key revenue stream?

Every new pump user needs infusion sets and CGM sensors on a near-weekly cycle, pushing consumables to a 5.62% CAGR even as hardware growth plateaus.

How are GLP-1 drugs affecting insulin device demand?

GLP-1 therapies delay insulin starts for some type 2 patients, subtracting roughly 0.5 percentage points from the market CAGR, yet insulin remains indispensable for type 1 cases and many long-term type 2 users.

What role does telehealth play in rural device adoption?

Cloud-linked pumps and smart pens allow endocrinologists to adjust settings remotely, enabling safe home use and expanding access in regions that lack specialist clinics.

Page last updated on: