Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

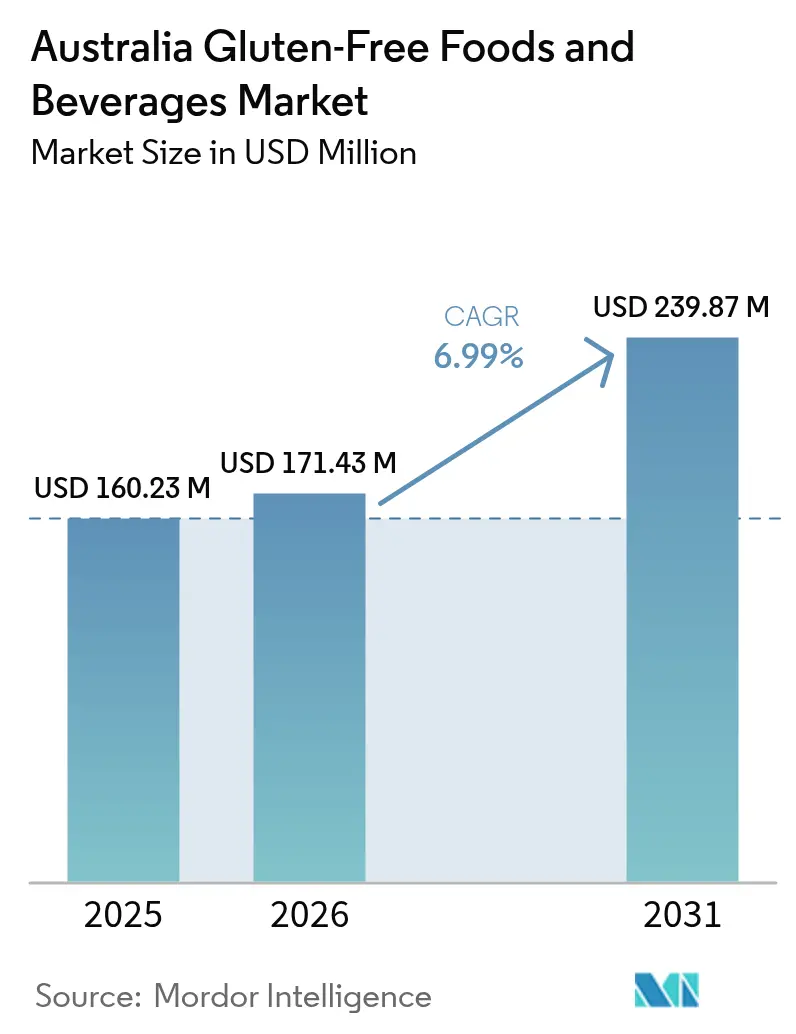

| Base Year Market Size (2025) | USD 160.23 Million |

| Market Size (2026) | USD 171.43 Million |

| Market Size (2031) | USD 239.87 Million |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

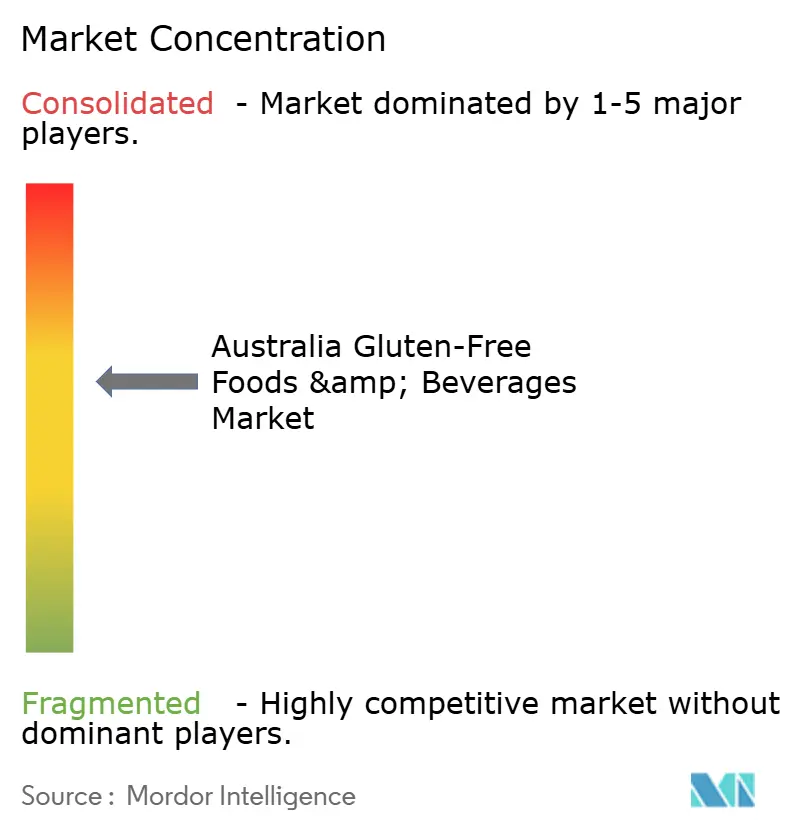

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Gluten-Free Foods And Beverages Market Analysis by Mordor Intelligence

The Australian gluten-free foods and beverages market size in 2026 is estimated at USD 171.43 million, growing from 2025 value of USD 160.23 million with 2031 projections showing USD 239.87 million, growing at 6.99% CAGR over 2026-2031. This growth stems from increasing health awareness, higher diagnosis rates of celiac disease and gluten intolerance, and a growing consumer segment choosing gluten-free diets for health and wellness reasons. Product innovation focuses on improving taste, texture, and nutritional value, enhancing the appeal of gluten-free options. Manufacturers utilize both local and international ingredients, building on Australia's expertise in plant-based materials and strict food safety standards to create premium products with added benefits such as fiber, protein, and probiotics. Consumer education and marketing initiatives have expanded the market beyond medical necessity to include health-conscious consumers. The market's expansion into regional areas and e-commerce platforms has improved product accessibility. While the industry faces challenges, including higher production costs and supply chain issues, continued advances in ingredients, packaging technology, and regulatory compliance support its growth and market position.

Key Report Takeaways

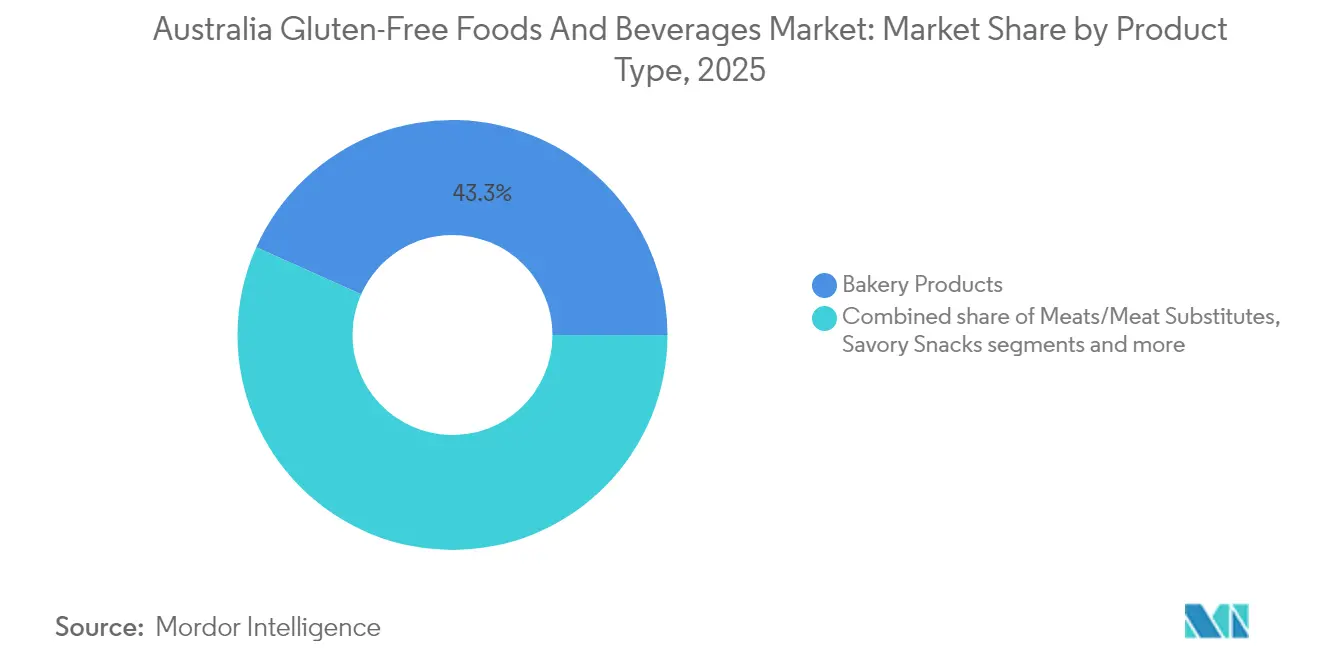

- By product type, bakery products led with 43.30% revenue share in 2025, while beverages are projected to expand at an 7.96% CAGR through 2031, underscoring a pivot toward functional drinks that complement core meal occasions.

- By packaging type, plastic packaging held 50.62% share of the Australian gluten-free foods and beverages market size in 2025 and is advancing at a 7.58% CAGR through 2031 as recyclability upgrades offset sustainability pushback.

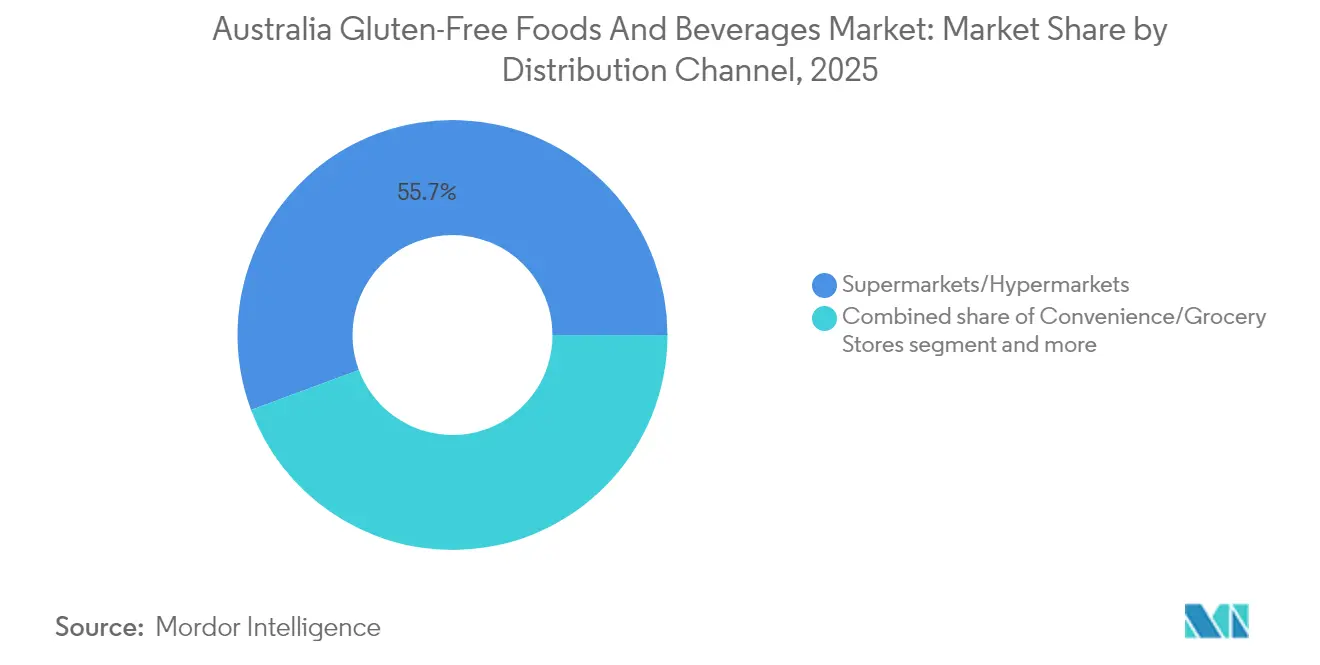

- By distribution channel, supermarkets and hypermarkets accounted for 55.68% share of the Australian gluten-free foods and beverages market size in 2025, while online retail stores are registering the fastest expansion with a 8.74% CAGR to 2031, boosted by pandemic-era digital habits.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Gluten-Free Foods And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of celiac disease and gluten intolerance | +1.8% | National, with higher concentrations in urban centers | Medium term (2-4 years) |

| Expansion in product innovation | +1.2% | National, led by NSW and Victoria manufacturing hubs | Short term (≤ 2 years) |

| Health consciousness and wellness trends | +1.0% | National, with premium segments in major cities | Long term (≥ 4 years) |

| Enhanced labelling regulations and certification schemes | +0.8% | National, FSANZ compliance requirements | Medium term (2-4 years) |

| Clean label and ingredient transparency trends | +0.7% | National, consumer-driven demand | Long term (≥ 4 years) |

| Expansion into mainstream food categories | +0.9% | National, retail channel expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Celiac Disease and Gluten Intolerance

The increasing prevalence of celiac disease and gluten intolerance drives growth in the Australian gluten-free foods and beverages market. Celiac disease, an autoimmune disorder triggered by gluten consumption, remains underdiagnosed in Australia. According to Coeliac Australia, during Coeliac Awareness Week 2025, approximately 80% of Australians with celiac disease are undiagnosed [1]Source: Coeliac Australia, "Coeliac Australia – Coeliac Awareness Week 2025", https://coeliac.org.au. This high rate of underdiagnosis indicates many individuals experiencing symptoms are either unaware of their condition or seeking diagnosis, leading to increased demand for gluten-free products. As strict gluten avoidance is the only effective treatment for celiac disease, the consumption of gluten-free foods and beverages continues to rise. Additionally, non-celiac gluten sensitivity expands the consumer base for gluten-free products. The growing recognition of gluten-related disorders has prompted manufacturers and retailers to expand their gluten-free product offerings and improve availability to meet the needs of patients and health-conscious consumers.

Expansion in Product Innovation

The Australian gluten-free foods and beverages market is experiencing growth due to significant product innovation. Manufacturers are increasing their research and development investments to enhance the quality, taste, texture, and nutritional value of gluten-free products. These improvements address traditional consumer concerns about the dryness and density of gluten-free alternatives. The incorporation of alternative flours, including almond, coconut, quinoa, and sorghum, has resulted in more nutritious and palatable products. Modern food processing technologies enable the production of gluten-free baked goods, snacks, and pasta that closely resemble traditional gluten-containing products, increasing consumer acceptance. The University of Adelaide's research on Australian Plantago demonstrates the country's innovation capabilities in gluten-free ingredients. This research aims to replace imported psyllium husk, a common binding agent in gluten-free products. The development of Australian Plantago reduces import dependence while creating intellectual property advantages by utilizing domestic agricultural resources. This initiative showcases Australia's scientific and manufacturing capabilities in developing proprietary gluten-free formulations using local ingredients.

Health Consciousness and Wellness Trends

Health consciousness and wellness trends drive the growth of Australia's gluten-free foods and beverages market. Consumer attitudes toward food are shifting from basic sustenance to proactive health management, with increased focus on preventive nutrition, clean-label ingredients, and functional food consumption. Individuals seek foods that align with current health research, using dietary choices to enhance immunity, improve digestion, and reduce the risk of chronic conditions. Demographic changes, particularly the growing proportion of older Australians, strengthen these health-focused consumption patterns. According to the Australian Bureau of Statistics, as of 2024, people aged 55 years and over represent 26% of Australia's population, compared to 34% in certain regions [2]Source: Australian Bureau of Statistics, "Regional population by age and sex", www.abs.gov.au. This aging population seeks specialized dietary products that support disease prevention, chronic condition management, and overall health. Their demand extends beyond gluten avoidance to holistic nutrition solutions that address age-related needs, including digestive comfort, cardiovascular health, and bone density. In response, food and beverage manufacturers are developing gluten-free products that offer broader functional benefits by incorporating ingredients and formulations that support health and longevity.

Enhanced Labelling Regulations and Certification Schemes

Labelling regulations and certification schemes drive growth and consumer trust in the Australian gluten-free foods and beverages market. Strict labelling requirements enhance transparency and safety, minimizing the risk of gluten exposure for individuals with celiac disease or gluten intolerance. As gluten-free diets become more common, consumers require accurate information about ingredients and manufacturing processes. Certification schemes and labelling standards help consumers make informed decisions while strengthening the credibility of compliant brands. Food Standards Australia New Zealand stipulates that foods labeled gluten-free must not contain detectable gluten, while products with low gluten claims must contain less than 200 parts per million of gluten. These standards exceed many international requirements, ensuring higher safety levels for sensitive individuals. The regulations require all potential allergens, including gluten-containing grains, to be displayed in bold font and clearly listed on packaging for easy consumer identification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of gluten-free products | -1.5% | National, with greater impact on price-sensitive segments | Short term (≤ 2 years) |

| Supply chain constraints for gluten-free raw materials | -1.2% | National, with regional variations in ingredient availability | Medium term (2-4 years) |

| Competition from alternative diets | -0.8% | Urban centers, health-conscious demographics | Long term (≥ 4 years) |

| Taste and texture challenges | -0.7% | National, consumer acceptance barriers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Gluten-Free Products

The high cost of gluten-free products remains a significant constraint in the Australian gluten-free foods and beverages market. The price difference stems from multiple factors, including the cost of specialized raw ingredients, strict quality control measures to prevent cross-contamination, and lower production volumes compared to traditional wheat-based products. Manufacturers must invest in separate production facilities, implement thorough cleaning protocols, obtain third-party certifications, and manage higher ingredient import costs. These costs particularly affect consumers in rural and remote areas, where limited product availability and additional shipping expenses increase retail prices. Small and medium-sized manufacturers struggle with profitability due to increasing costs in ingredients, insurance, employee training, compliance requirements, and inventory waste management. Despite growing demand, consumers express concerns about the high prices of gluten-free products. The industry continues to focus on supply chain optimization, production scaling, and ingredient innovation to reduce costs and improve accessibility for Australian consumers who require or prefer gluten-free options.

Supply Chain Constraints for Gluten-Free Raw Materials

Supply chain constraints for gluten-free raw materials limit the growth of the Australian gluten-free foods and beverages market. The production of certified gluten-free foods requires strict segregation of raw materials throughout the supply chain to prevent cross-contamination, making the process logistically complex and expensive. Manufacturers face challenges in sourcing adequate quantities of gluten-free grains such as rice, corn, sorghum, buckwheat, quinoa, and millet due to seasonal harvest variations, limited domestic cultivation, and dependence on imports for specialty ingredients like psyllium husk and specific gluten-free flours. The situation is further complicated by increasing global demand for gluten-free ingredients, international trade disruptions, and weather-related impacts on crop yields. The industry requires close coordination between manufacturers, certified growers, and specialized logistics providers to maintain allergen-safe handling protocols throughout the process. Small and emerging brands particularly struggle to secure consistent supplies of high-quality, locally grown gluten-free raw materials, leading to increased reliance on global markets with higher transportation costs and geopolitical risks. These supply chain difficulties result in higher retail prices and occasional product shortages for consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Segment 1

The bakery products segment dominates the Australian gluten-free foods and beverages market with a 43.30% market share in 2025. This dominance stems from the fundamental role of baked goods in daily diets, particularly for consumers with celiac disease or gluten intolerance. The segment continues to grow through product innovation, as demonstrated by the March 2024 partnership between The Hallway and Sydney-based Wholegreen Bakery. Their launch of the Cardboard Cake, a coeliac-approved bakery product containing butterscotch, coffee, cocoa powder, pastry, caramel, and brown rice flour, represents the industry's commitment to developing gluten-free options that maintain taste and texture quality.

While bakery products lead the market, the beverages segment is experiencing the fastest growth, with a projected CAGR of 7.96% through 2031. This growth reflects increasing consumer demand for gluten-free beverages among health-conscious individuals who seek safe options beyond traditional food items. The segment's expansion indicates a shift in consumer preferences, as gluten-free considerations extend to daily beverage choices. Savory snacks present growth opportunities as manufacturers develop gluten-free alternatives to conventional products using alternative grain technologies and innovative flavoring methods. The sauces, dressings, and seasonings category offers potential for high margins with simpler manufacturing processes, though it requires careful selection of gluten-free thickeners and flavor enhancers.

By Packaging Type: Sustainability Pressures Challenge Plastic Leadership

The plastic packaging segment holds a 50.62% market share in the Australian gluten-free foods and beverages market in 2025. This dominance stems from plastic's functional advantages in preserving gluten-free products. These products require specific protection against texture degradation and moisture-related issues, which plastic packaging effectively provides through superior moisture barrier properties and shelf stability. The cost-efficiency of plastic packaging compared to alternatives enables manufacturers to maintain competitive pricing while meeting quality standards. These characteristics are essential in the gluten-free market segment, where consumers demand product integrity and protection from gluten contamination.

Paper packaging is experiencing rapid growth in the gluten-free food and beverages packaging market, with a projected CAGR of 7.58% through 2031. This growth reflects increasing demand for sustainable packaging alternatives. Consumer environmental awareness and stricter regulations on plastic waste reduction have prompted brands to adopt paper-based solutions that offer biodegradability and recyclability. Innovations in paper and paperboard packaging provide enhanced protective features while meeting consumer preferences for environmentally responsible options. The growth of paper packaging demonstrates the market's evolution toward diverse and sustainable packaging solutions while maintaining necessary product protection standards.

By Distribution Channel: Online Growth Challenges Traditional Retail Dominance

Supermarkets and hypermarkets hold a 55.68% market share in the Australian gluten-free foods and beverages market in 2025. Their market dominance stems from extensive reach, well-established distribution networks, and comprehensive consumer accessibility. Major chains like Coles and Woolworths offer strategically positioned dedicated sections for gluten-free products, significantly enhancing the shopping experience. These retailers strengthen their market position through exceptional convenience and deep-rooted consumer trust, while systematically expanding their gluten-free product range to serve both medical requirements and evolving lifestyle choices.

Online retail stores represent the fastest-growing distribution channel for gluten-free foods and beverages in Australia, with a projected CAGR of 8.74% through 2031. This growth trajectory is underpinned by Australia's high internet penetration rate, which stood at 97.1% in 2023 according to the International Telecommunication Union (ITU) . This near-universal internet access facilitates widespread consumer adoption of online shopping, allowing easy access to a diverse range of gluten-free products that may not always be available in traditional retail outlets. Advanced digital marketing strategies and increasing social media influence significantly boost consumer awareness of gluten-free options, accelerating online sales growth. The powerful combination of robust digital infrastructure and rapidly evolving consumer preferences firmly establishes online retail as a transformative market growth driver.

Geography Analysis

Australia's gluten-free foods and beverages market concentrates primarily in New South Wales and Victoria's urban centers. These states dominate consumption due to their high population density, higher disposable incomes, and increased health awareness among consumers. Sydney and Melbourne serve as key innovation centers for premium gluten-free products. The multicultural populations in these cities, with their diverse dietary needs, increase the demand for specialized gluten-free options. The well-developed retail infrastructure in these regions enables broad product availability and consumer awareness.

Queensland's market expansion stems from its population growth and tourism industry. The state's health-focused resorts and hospitality sector drive gluten-free food demand as dietary requirements become essential for visitors. Regional areas across Australia face distribution limitations due to lower population density and fewer specialty retail outlets. The Northern Territory and Tasmania, while smaller markets, maintain their position through health tourism and premium product offerings.

Western Australia's position as the world's largest sweet lupin producer strengthens its role in gluten-free ingredient supply for domestic manufacturing and exports. South Australia contributes through its established food manufacturing base and research in plant-based ingredients, supporting product development and commercialization.

Competitive Landscape

The Australian gluten-free foods and beverages market has a moderately fragmented structure, comprising multinational corporations, domestic specialists, and niche players. The Sanitarium Health and Wellbeing Company, General Mills, Inc., and Arnott's Group dominate traditional categories like bakery, snacks, and beverages. New market entrants focus on premium products and specific consumer segments, including organic, plant-based, and gluten-free offerings with functional benefits. This market structure promotes innovation and product diversity, allowing smaller companies to establish specialized niches while pushing established manufacturers to update their product lines.

Technology adoption serves as a competitive advantage in the Australian gluten-free market. Manufacturers use precision agriculture technologies to source high-quality gluten-free ingredients efficiently while maintaining strict standards. Advanced packaging technologies improve product shelf life and safety, particularly important for maintaining the texture and freshness of gluten-free items. Digital marketing platforms enable direct consumer communication and education about gluten-free products and lifestyles. These digital channels support product discovery and provide transparent information to consumers, creating opportunities for brand growth and customer retention.

Export market development offers significant opportunities for Australian manufacturers, supported by the country's strong food safety standards and access to unique gluten-free ingredients like lupin and quinoa. Australian producers can expand into international markets with premium, clean-label products marketed as safe and nutritious alternatives. The combination of quality ingredients, established food safety practices, and innovative products provides competitive advantages in both domestic and international markets, supporting market expansion.

Australia Gluten-Free Foods And Beverages Industry Leaders

-

The Sanitarium Health and Wellbeing Company

-

General Mills, Inc.

-

Dr. Schar AG

-

Arnott's Group

-

Bob’s Red Mill Natural Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Well & Good's Bakery launched two types of allergy-friendly bread rolls at Woolworths. The rolls are soft, tasty, and free from gluten, soy, nuts, dairy, and eggs.

- May 2025: Simply Wize introduced gluten-free churros to the market. The product serves as a snack or dessert option and can be paired with chocolate or caramel sauce.

- March 2025: Arnott's introduced a gluten-free product range, featuring Gluten-Free Jatz and Gluten-Free Barbecue Shapes. The products are manufactured in Australia using a gluten-free flour blend comprising maize, tapioca, rice, sorghum, and soy.

- October 2024: Warburtons expanded its product portfolio in Australia by introducing gluten-free bakery items at Coles supermarkets nationwide. The new range includes Tiger Bloomer Loaf, Super Soft Brioche Sliced Rolls, Super Soft White Sliced Rolls, and Crumpets.

Australia Gluten-Free Foods And Beverages Market Report Scope

Gluten is a protein found in wheat, barley, rye, and triticale. Gluten-free food and beverage products exclude gluten.

The Australian gluten-free foods and beverages market is segmented by product type and distribution channel. By product type, the market is segmented into bakery products, pizzas and pasta, cereals and snack food, meat and meat products, beverages, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. The report offers market size and forecasts for the Australian gluten-free foods and beverages market in value (USD million) for all the above segments.

By Product Type

| Bakery Products |

| Meats/Meat Substitutes |

| Dairy/Dairy Substitutes |

| Savory Snacks |

| Beverages |

| Sauces, Dressings, and Seasonings |

| Other Product Types |

By Packaging Type

| Paper |

| Plastic |

| Metal |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Bakery Products |

| Meats/Meat Substitutes | |

| Dairy/Dairy Substitutes | |

| Savory Snacks | |

| Beverages | |

| Sauces, Dressings, and Seasonings | |

| Other Product Types | |

| By Packaging Type | Paper |

| Plastic | |

| Metal | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Australia gluten free foods beverages market in 2026?

It is valued at USD 171.43 million and is forecast to rise to USD 239.87 million by 2031.

What drives demand beyond diagnosed celiac patients?

Broader wellness adoption, personalized nutrition apps, and preventive health trends expand consumption to non-celiac shoppers.

Which product line is growing the fastest?

Beverages, especially plant-based milks and functional drinks, are advancing at an 7.96% CAGR through 2031.

How significant is online retail for gluten-free products?

Online sales are rising at a 8.74% CAGR as consumers embrace digital grocery and subscription services.

Page last updated on: