Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

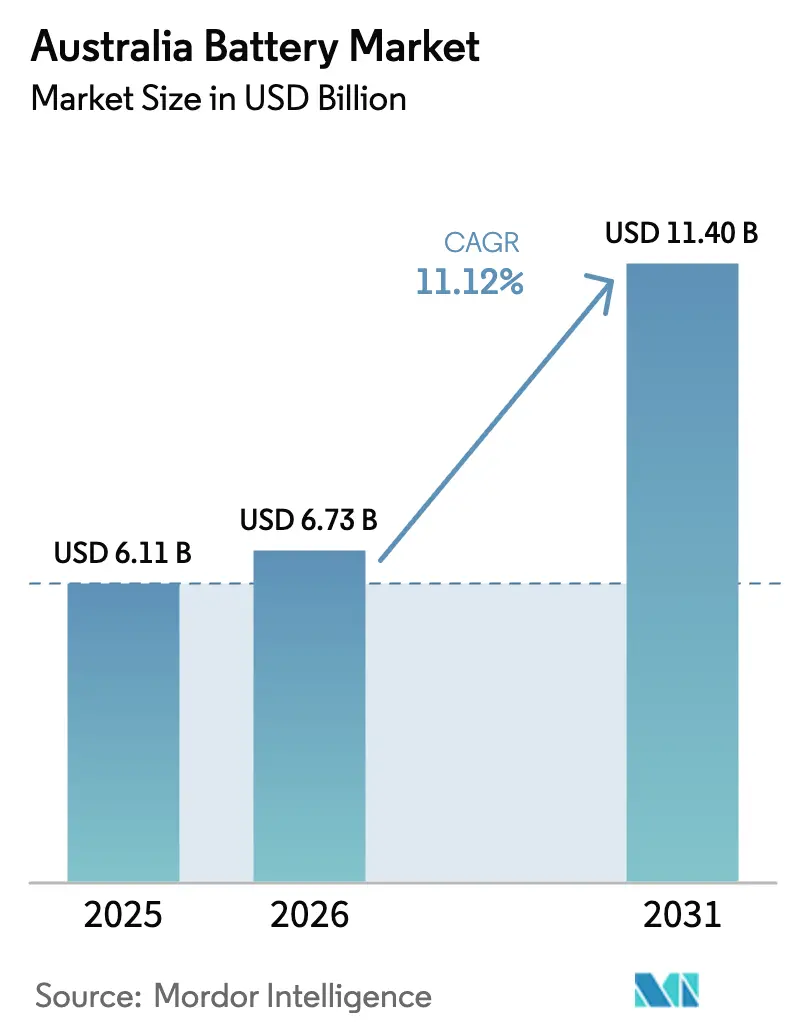

| Base Year Market Size (2025) | USD 6.11 Billion |

| Market Size (2026) | USD 6.73 Billion |

| Market Size (2031) | USD 11.40 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Battery Market Analysis by Mordor Intelligence

The Australia Battery Market size is expected to grow from USD 6.11 billion in 2025 to USD 6.73 billion in 2026 and is forecast to reach USD 11.40 billion by 2031 at 11.12% CAGR over 2026-2031.

This trajectory highlights a nationwide transition from fossil-fuel dependence toward electrified transport and renewable-driven power systems, supported by falling lithium-ion pack prices, an AUD 2 billion critical-minerals finance facility, and aggressive state procurement of large-scale batteries. Federal fuel-efficiency standards are pushing vehicle makers to accelerate electric-vehicle (EV) rollouts, which is lifting demand for high-cycle secondary cells, while coal-plant retirement schedules in New South Wales (NSW) and Victoria have moved utilities to tender multi-gigawatt storage arrays. Local assembly ambitions are growing around lithium-iron-phosphate packs as policymakers seek to capture more value domestically, yet upstream material gaps still expose integrators to import risks. Defence orders for submarine and guided-weapon batteries add a strategic layer that prioritizes sovereign capability, nudging suppliers to locate facilities near naval precincts. Together, these vectors narrow payback periods for storage projects, expand addressable use cases, and intensify competition across the Australian battery market.

Key Report Takeaways

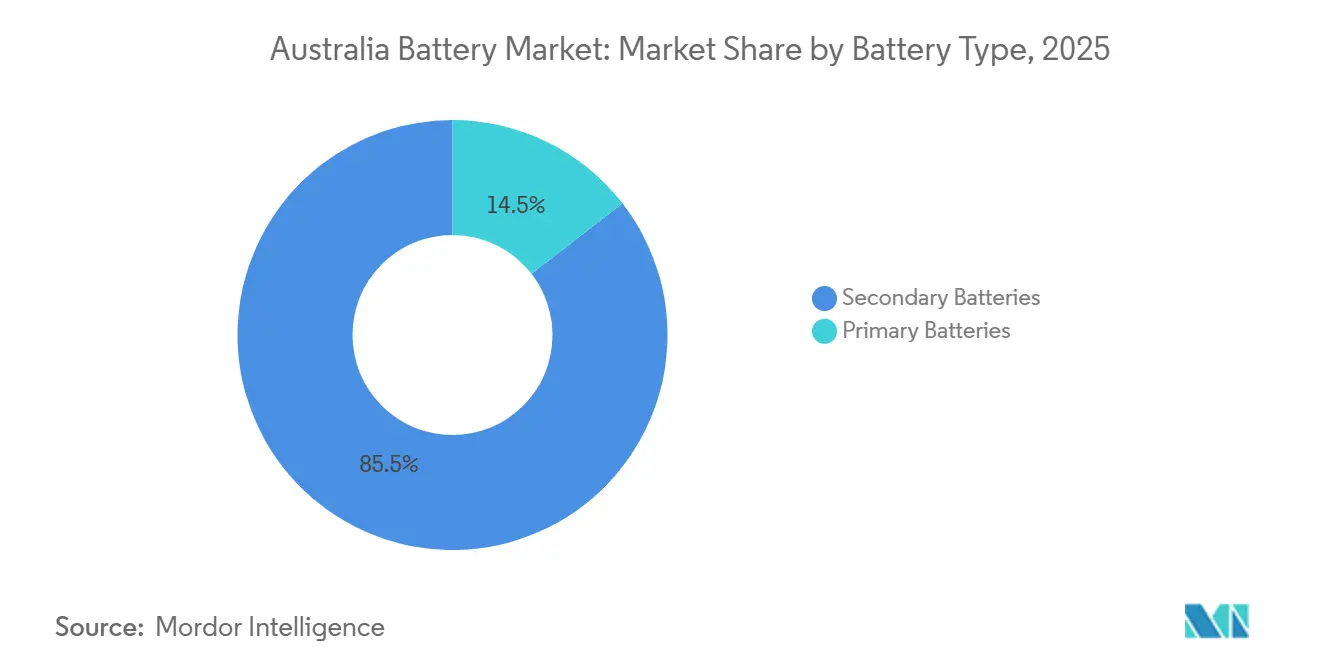

- By battery type, secondary batteries held 85.5% of the Australian battery market share in 2025, and they are set to expand at a 12.8% CAGR to 2031.

- By technology, lead-acid commanded 41.9% of the Australian battery market share in 2025, whereas lithium-ion is forecast to post the fastest 19.5% CAGR through 2031.

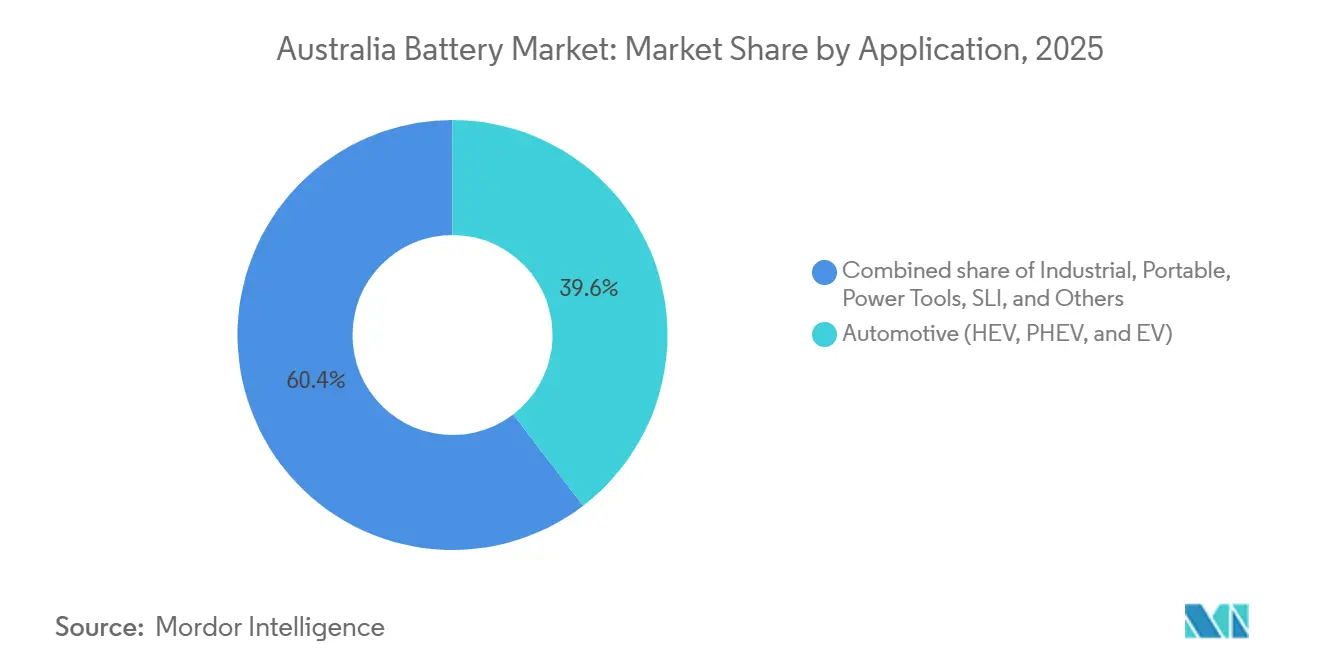

- By application, automotive batteries led with 39.6% share in 2025, while industrial applications are poised to register a 17.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV adoption catalysed by Federal Fuel Efficiency Standards | +2.3% | National, with early concentration in NSW, VIC metropolitan areas | Medium term (2-4 years) |

| Rapid renewable-plus-storage tenders from states (NSW, SA, VIC) | +2.8% | NSW, SA, VIC leading; QLD emerging | Short term (≤ 2 years) |

| Accelerated phase-out of coal-fired power stations drives grid-scale storage | +2.1% | NSW (Eraring, Liddell), VIC (Loy Yang A, Yallourn), QLD (Callide, Tarong) | Long term (≥ 4 years) |

| Falling lithium-ion battery pack prices (< USD 100/kWh threshold) | +1.9% | National, with spillover to industrial and residential segments | Short term (≤ 2 years) |

| Australian Government's AUD 2 billion Critical Minerals Facility spurs local battery value chain | +1.2% | National, with clusters in WA (lithium), QLD (refining), NSW (manufacturing) | Long term (≥ 4 years) |

| Defence push for sovereign submarine & guided-weapons battery systems | +0.6% | SA (Osborne Naval Shipyard), WA (Henderson), NSW (defence precincts) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging EV Adoption Catalyzed by Federal Fuel-Efficiency Standards

Federal fleet-average CO₂ limits that took effect in 2025 are compelling vehicle brands to raise EV allocations to Australia or face penalty payments. National light-duty EV registrations climbed 35% year on year to 87,000 units in 2025, led by models such as Tesla Model Y and BYD Atto 3.[1]Federal Chamber of Automotive Industries, “Electric Vehicle Sales Data 2025,” fcai.com.au Fleet operators, including rental agencies and ride-hail platforms, have accelerated orders to lock in depreciation schedules, and battery demand is rising for nickel-manganese-cobalt and lithium-iron-phosphate chemistries sized between 60 kWh and 75 kWh. Charging-infrastructure expansion lags vehicle uptake, yet the regulatory certainty has enabled multi-year offtake agreements between global cell makers and domestic pack assemblers. As a result, EV-related orders account for the largest single pull on high-energy-density cells within the Australian battery market.

Rapid Renewable-Plus-Storage Tenders from States (NSW, SA, VIC)

States awarded 4.2 GW of combined renewable-generation and storage contracts in 2025, triple 2023 volume.[2]Australian Energy Market Operator, “Integrated System Plan 2024,” aemo.com.au Flagship projects include the 2 GW Waratah Super Battery in NSW and the 450 MW Geelong Big Battery expansion in Victoria, each backed by 15-year capacity-payment schemes that derisk financing.[3]New South Wales Government, “Waratah Super Battery Project,” nsw.gov.au South Australia’s grid-forming inverter pilots at Hornsdale are showing batteries can supply voltage and frequency reference without thermal plant support.[4]South Australian Government, “Hornsdale Grid-Forming Trials,” sa.gov.au The compressed build schedules are stretching module supply chains, encouraging developers to source from domestic integrators to avoid shipping delays and import duties.

Accelerated Phase-Out of Coal-Fired Stations Drives Grid-Scale Storage

The planned exit of 6.5 GW of coal capacity by 2035 (Eraring in 2027, Yallourn in 2028, and Loy Yang A in 2035) is forcing network planners to procure fast-response batteries to replace synchronous inertia. Queensland’s SuperGrid Blueprint allocates AUD 62 billion (USD 41 billion) to transmission and 3 GW of long-duration storage, signaling a multi-year build cycle. Developers favor retired coal sites that already have transmission links, saving years of grid-connection lead time. The storage mix is diverging between one-hour lithium-ion systems for frequency regulation and four-to-eight-hour flow batteries for evening-peak firming.

Falling Lithium-Ion Battery Pack Prices Below USD 100/kWh

BloombergNEF’s 2024 survey placed average pack pricing at USD 97/kWh, an 18% drop from 2023 and the lowest level on record. Residential installers responded with a 22% jump in battery attachment to rooftop solar in 2025, and commercial buyers cut payback periods to under five years in demand-charge management projects. Although cost declines are slowing as raw-material prices floor, pricing under USD 100/kWh has widened economic viability for a broad spectrum of Australia battery market applications.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented domestic battery manufacturing ecosystem | -1.4% | National, with acute gaps in NSW, VIC assembly capacity | Medium term (2-4 years) |

| Supply-chain bottlenecks for anode/precursor materials | -1.1% | National, with import dependency on China, Japan for graphite, electrolyte salts | Short term (≤ 2 years) |

| Lagging end-of-life recycling & take-back logistics | -0.7% | National, with pilot facilities in VIC, SA only | Long term (≥ 4 years) |

| Distribution-network hosting-capacity limits for behind-the-meter storage | -0.9% | Urban NSW, VIC, QLD distribution feeders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Domestic Battery Manufacturing Ecosystem

Australia hosts fewer than a dozen sub-gigawatt-hour assembly plants, none at a scale rivaling Asian gigafactories. Redflow’s voluntary administration in 2025 exposed the capital intensity of local integration without anchor orders. Energy Renaissance’s Tomago facility will reach 1.5 GWh of pack output by 2027, yet it still imports finished cells, capturing only one-fifth of the bill-of-materials value. State subsidies remain fragmented, preventing economies of scale in workforce training and shared R&D. Until coordinated national support emerges, integrators face higher working-capital needs and currency risk, which moderates growth across the Australian battery market.

Supply-Chain Bottlenecks for Anode and Precursor Materials

Synthetic graphite, electrolyte salts, and nickel sulfate are heavily sourced from China and Japan, creating single-country concentration risk. In 2025, 61% of Australian spodumene exports left the country without conversion, forgoing a four-to-six-times value uplift. High-temperature furnaces and renewable-power requirements have slowed domestic synthetic-graphite ventures, and permitting timelines stretch four-plus years. Shipment delays in 2024 postponed grid-battery commissioning by up to 12 weeks, prompting developers to diversify toward suppliers in Mozambique and South Korea, though contracted volumes cover less than 10% of aggregate demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Dominance Reflects Electrification Shift

Secondary batteries accounted for 85.5% of 2025 revenue and are expanding at a 12.8% CAGR, underscoring how electrification in transport, grid services, and households is redefining the Australian battery market size. Primary cells maintained a 14.5% niche in low-drain devices, but extended-producer-responsibility rules under consideration in Victoria and South Australia threaten margins. Residential adoption of Tesla Powerwall 3 exceeded 6,000 units in its first quarter on the market, and installation momentum is spreading to the SonnenCore and LG ESS lines, amplifying volume growth. At the industrial end, grid-storage integrators favor secondary chemistries for multi-cycle resilience, while remote sensors and military hardware keep single-use cells relevant.

Margin pressure is building as lithium-ion costs fall; integrators have seen gross margins slide from 25% to 18% since 2024, prompting deeper vertical integration. Energy Renaissance plans to pair assembly with end-of-life disassembly, targeting 92% lithium, cobalt, and nickel recovery. Primary battery producers face higher landfill fees and tightening mercury limits, nudging clients toward rechargeable alternatives. Long-cycle chemistries such as lithium-metal and solid-state are under pilot evaluation, and their commercialization could introduce higher-density options suitable for aviation and maritime by 2028, reshaping the competitive order inside the Australian battery market.

By Technology: Lithium-Ion Disruption Amid Lead-Acid Incumbency

Lead-acid held 41.9% of 2025 revenue thanks to a mature recycling system that recovers 98% of lead content, insulating producers from raw-material swings. Telecom operators and warehouse-equipment fleets still specify lead-acid where cost and legacy infrastructure outweigh weight penalties. Lithium-ion, however, is advancing at a 19.5% CAGR, driven by EVs, residential solar-plus-storage, and grid-scale arrays. Nickel-metal-hydride keeps a foothold in hybrid vehicles, while nickel-cadmium persists in aviation emergency lighting but faces phase-out pressure.

Solid-state prototypes are edging toward 500 Wh/kg energy density, with QuantumScape reporting 1,000 cycles at 80% retention, yet yields remain too low for volume production. Flow batteries, led by vanadium-redox and zinc-bromine chemistries, offer long-duration discharge and near-unlimited cycles, suiting evening-peak firming despite capital costs that still sit double lithium-ion levels. The technology contest is pushing lead-acid recyclers to diversify into lithium recovery while lithium-ion suppliers race to drop pack prices below USD 80/kWh, a figure that would unlock total-cost parity for industrial motive power in the Australian battery market.

By Application: Industrial Surge Outpaces Automotive Leadership

Automotive batteries represented 39.6% of 2025 revenue as EV and hybrid sales increased, yet industrial usage, including telecom towers, data centers, and grid storage, is forecast to grow faster at 17.2% CAGR through 2031. Telstra installed 2,400 lithium-ion tower systems in 2025, doubling average backup duration to eight hours, and data-center operators such as NextDC now specify lithium-ion UPS with 95% round-trip efficiency. Utility-scale projects reached 1.8 GWh of installed capacity in 2025, with another 6.5 GWh under construction, creating a robust pipeline that supports high-energy cell demand and expands the Australian battery market size for stationary deployments.

Chemistry selection diverges by mobility needs: nickel-manganese-cobalt for long-range EVs, lithium-iron-phosphate for value-oriented models, and nickel-cobalt-aluminum for performance segments. Fleet operators value eight-year warranties and residual guarantees, while commercial-vehicle electrification is catching up as state procurement mandates clarify order volumes. Portable-electronics batteries face mature smartphone demand, but growth persists in wearables, drones, and e-bikes. Altogether, the application mix continues to tilt toward segments with higher cycle counts and longer operating lives, reinforcing top-line resilience for the Australian battery market.

Geography Analysis

Eastern seaboard states dominate deployments. NSW led grid-storage additions in 2025 with the 2 GW Waratah Super Battery and a 700 MW expansion at Eraring, collectively supplying 3.2 GWh of firming capacity scheduled for completion by 2027. Victoria’s renewable-energy zones attracted AUD 8.3 billion (USD 5.5 billion) of investment in 2025, anchored by the Geelong Big Battery, and the state requires that half of new renewable capacity include co-located storage to receive network-connection priority.

South Australia operates the Hornsdale Power Reserve, which became the first large battery to deliver grid-forming capability after a 212 MW expansion in 2025. Queensland’s AUD 62 billion SuperGrid program targets 22 GW of renewables and 3 GW of long-duration storage by 2035, with near-term focus on a north-south transmission corridor that will rely on 1.5 GW of intermediate batteries. Western Australia’s isolated grid is installing solar-battery microgrids to replace rural feeders, recording 200 systems in 2025, while Tasmania leverages hydro reservoirs for pumped storage to export firming via the Marinus Link.

Distribution-network constraints limit behind-the-meter adoption in urban areas. Ausgrid and Powercor have rolled out dynamic operating envelopes that adjust export limits in real time, enabling more rooftop solar batteries without costly feeder upgrades. The Northern Territory and Australian Capital Territory pursue 100% renewable goals by 2030, so their storage spend outweighs load size, exemplified by the 35 MW Darwin-Katherine battery and the 250 MW Big Canberra Battery. Differing state connection codes, tariff structures, and safety standards inflate compliance costs, slowing technology diffusion but also creating consultancy and software niches within the Australian battery industry.

Competitive Landscape

The Australian battery market remains moderately fragmented, with no firm controlling more than 15% of total revenue. Global cell giants LG Energy Solution, CATL, and Panasonic supply most modules, while domestic integrators such as Energy Renaissance and Battery Energy Power Solutions focus on pack assembly and balance-of-plant engineering. Tesla’s vertical stack, with cells from Nevada and Megapack assembly and operation at Hornsdale, shows the advantage of scale, yet its premium positioning leaves room for cost-focused rivals.

Strategic moves in 2025 illustrate rising intensity. LG Energy Solution allocated AUD 200 million to expand its Sydney module plant to 2 GWh by 2028. Fluence Energy secured an AUD 1.4 billion EPC contract for the 2 GW Waratah project, deepening utility-scale credentials. Envirostream opened Victoria’s first 3,000-ton-per-year lithium-ion recycling line, while MGA Thermal raised AUD 10 million to commercialize aluminum-silicon heat-storage blocks. Chinese entrants BYD and EVE Energy have begun direct distribution, undercutting incumbent module pricing by up to 20% and prompting consolidation among sub-scale local assemblers.

Despite growing domestic ambition, supply-chain gaps in cathode, anode, and electrolyte production make full vertical integration elusive. The AUD 2 billion Critical Minerals Facility is easing financing hurdles, yet equity co-investment requirements slow uptake. Defence procurement brings a niche but high-margin demand stream, with PMB Defence winning multi-year contracts to supply lithium-polymer packs for guided-weapon programs. As circular-economy regulations tighten, companies able to tie upstream supply with end-of-life recovery are set to gain share in the next growth phase of the Australian battery market.

Australia Battery Industry Leaders

-

Century Yuasa Batteries Pty Ltd

-

Enersys Australia Pty Ltd

-

Sonnen Australia Pty Limited

-

R & J Batteries Pty Ltd.

-

PMB Defence

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: LG Energy Solution Australia committed AUD 200 million to expand its Sydney module facility to 2 GWh of annual capacity by 2028.

- August 2025: Energy Renaissance secured AUD 50 million from the Critical Minerals Facility to lift Tomago pack output to 1.5 GWh by 2027 with integrated recycling.

- August 2025: Stanwell awarded Fluence a AUD 1.4 billion EPC contract for the 2 GW Waratah Super Battery in NSW, slated for service in 2027.

- April 2025: MGA Thermal closed an AUD 10 million Series B to scale aluminum-silicon heat-storage blocks, piloting a 5 MWh system at a Queensland smelter.

Australia Battery Market Report Scope

A battery is a source of electric power consisting of one or more electrochemical cells with external connections for powering electrical devices. It mainly provides backup power during a power outage. The Australian battery market report includes:

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Australia battery market?

The Australia battery market size stood at USD 6.73 billion in 2026 and is projected to reach USD 11.40 billion by 2031.

Which battery segment is growing fastest in Australia?

Lithium-ion technology is expanding the fastest, advancing at a 19.5% CAGR on the back of grid-scale storage and electric-vehicle uptake.

How are state tenders influencing battery demand?

Combined renewable-plus-storage tenders totaling 4.2 GW in 2025 have locked in 15-year revenue contracts, accelerating utility-scale battery installations.

What is the main constraint on local battery manufacturing?

Fragmented, sub-scale assembly plants and limited cathode, anode, and electrolyte production keep Australia reliant on imported components.

How low have lithium-ion battery pack prices fallen?

Average pack prices dipped below the USD 100/kWh threshold in late 2024, widening the economic case for both EVs and stationary storage.

Which state leads in grid-scale battery capacity?

New South Wales leads, underpinned by the 2 GW Waratah Super Battery and multiple expansions at existing generation sites.

Page last updated on: