Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

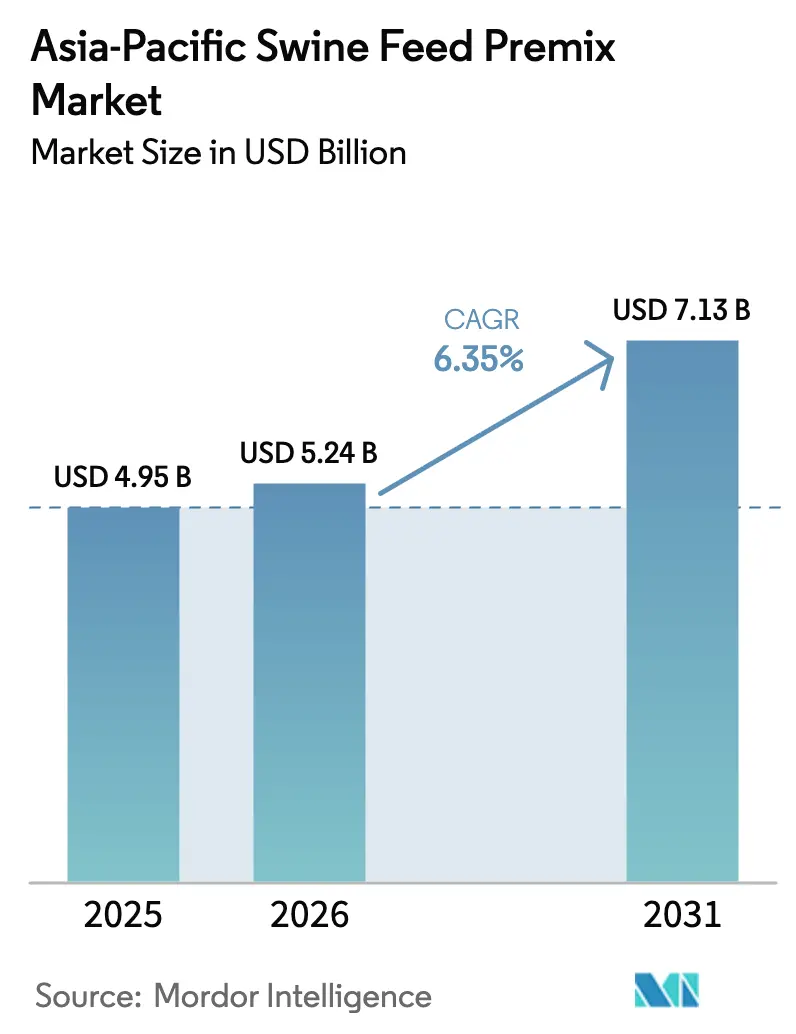

| Base Year Market Size (2025) | USD 4.95 Billion |

| Market Size (2026) | USD 5.24 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

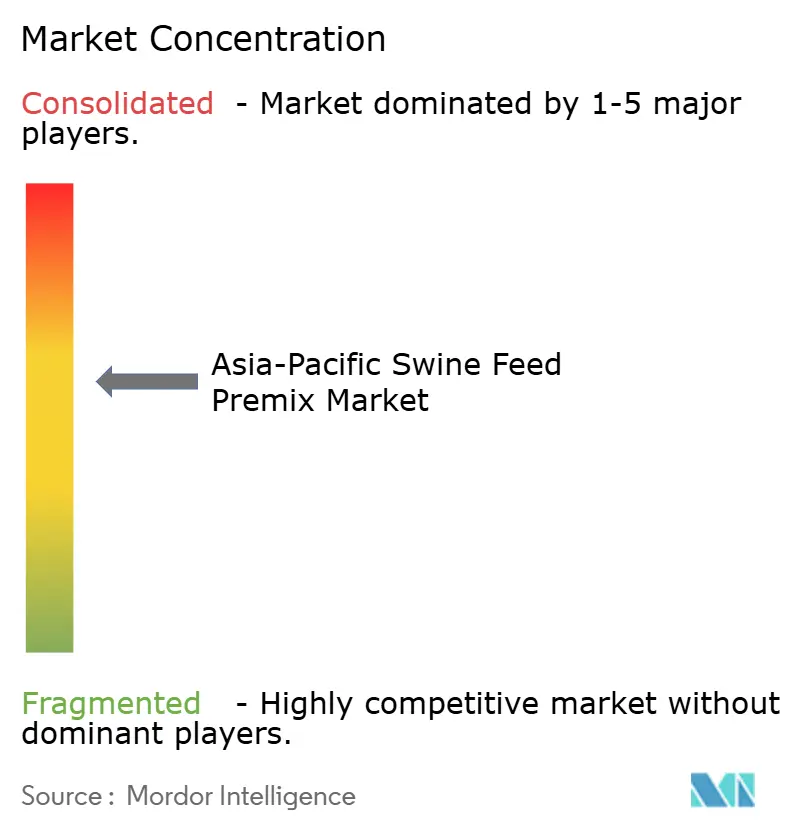

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Swine Feed Premix Market Analysis by Mordor Intelligence

The Asia-Pacific swine feed premix market size is projected to expand from USD 4.95 billion in 2025 and USD 5.24 billion in 2026, to USD 7.13 billion by 2031, registering a CAGR of 6.35% between 2026 to 2031. Demand is rising as producers rebuild herds after African Swine Fever, comply with antibiotic-free regulations, and shift from backyard to commercial operations in China, Vietnam, and Thailand. Enzyme premixes that replace banned growth promoters, automated liquid-dosing installations, and clean-label pork programs are reinforcing adoption. Although the Asia-Pacific swine premix market experienced a 15% margin compression in early 2025 due to global shortages of vitamins A and E, capacity restorations at BASF SE and Zhejiang Medicine Co., Ltd., stabilized pricing by late 2025. This stabilization allowed the market to utilize precision nutrition software, supporting projected growth.

Key Report Takeaways

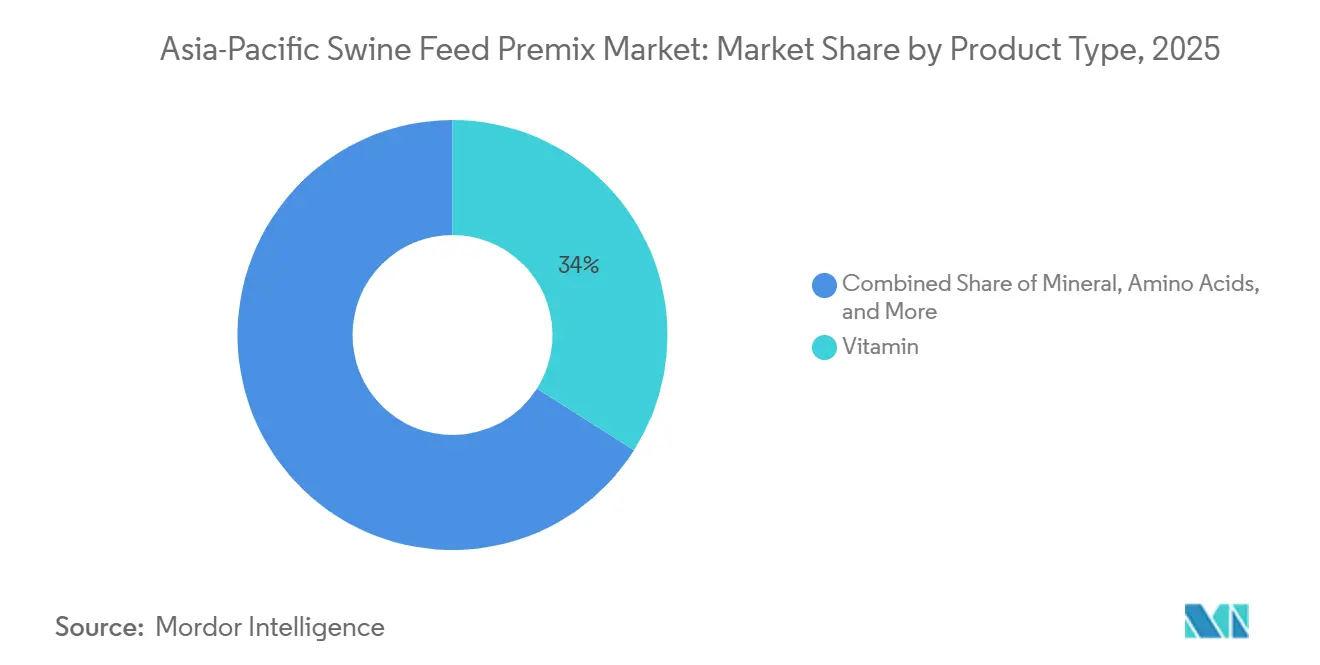

- By product type, vitamins led with 34% of the Asia-Pacific swine feed premix market share in 2025, and enzymes are projected to post the fastest 8.9% CAGR through 2031.

- By form, dry premixes accounted for 71.5% of the Asia Pacific swine feed premix market share in 2025, whereas liquid formats are advancing at a 7.6% CAGR, driven by rising automated dosing.

- By functionality, growth promotion accounted for 40.2% of the Asia Pacific swine feed premix market size in 2025, while immunity enhancement is forecast to expand at a 9.4% CAGR during 2026-2031.

- By ingredient source, natural formulations accounted for 58.8% of the Asia Pacific swine feed premix market size in 2025 demand and are growing at a 7.8% CAGR, outpacing synthetic alternatives.

- By purchaser type, commercial integrators accounted for 56.9% of the Asia Pacific swine feed market size in 2025, while cooperative feed mills are anticiapted to have the highest 8.2% CAGR through 2031.

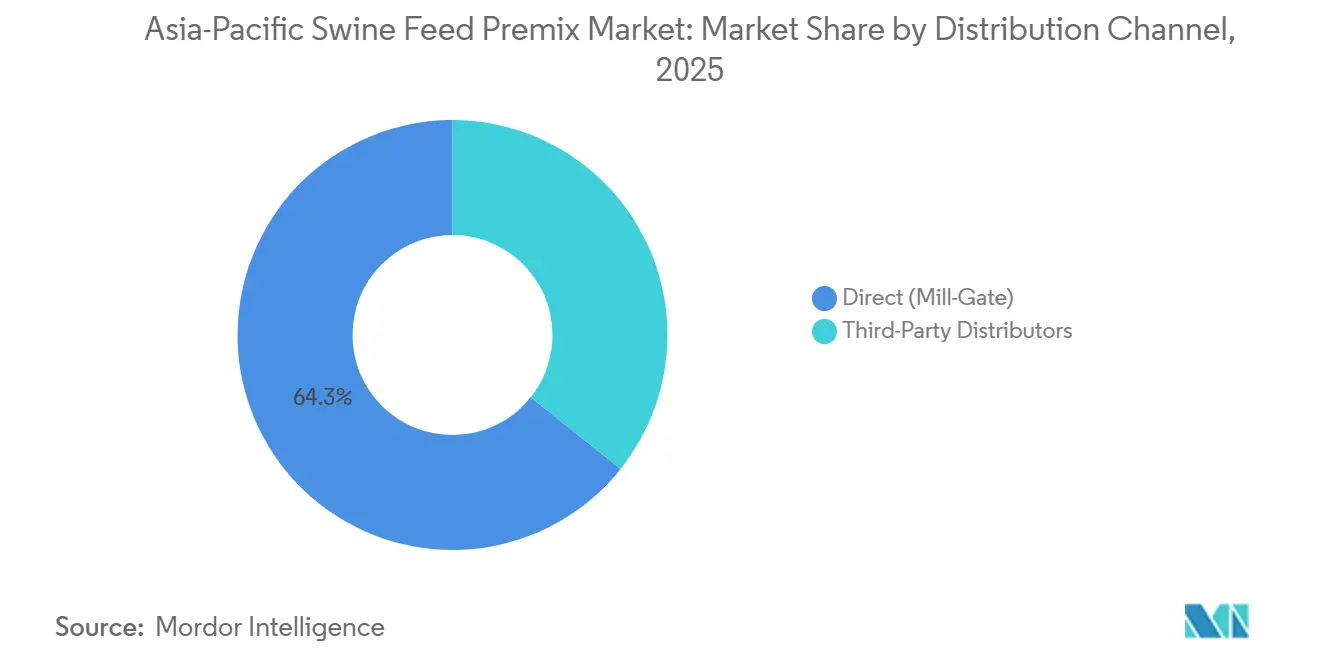

- By distribution channel, third-party distributors grew at an 8.5% CAGR, while direct (mill-gate) supply accounted for 64.3% of 2025 sales of the Asia-Pacific swine feed premix market.

- By geography, China led the Asia-Pacific swine feed premix market with 54.3% share in 2025, while Vietnam is projected to post the fastest 8.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Swine Feed Premix Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| African Swine Fever (ASF)-driven biosecurity protocols elevating fortified premix demand | +1.2% | China, Vietnam, Philippines, Thailand, and Indonesia | Medium term (2–4 years) |

| Government mandates for antibiotic-free pork accelerating functional additives | +1.4% | China, Vietnam, and Thailand | Long term (≥ 4 years) |

| Rising pork consumption among emerging middle class expanding commercial feed penetration | +1.1% | India, Indonesia, and Philippines | Long term (≥ 4 years) |

| Expansion of integrator-owned mega-farms consolidating premix procurement | +0.9% | China, Vietnam, and Thailand | Medium term (2–4 years) |

| Adoption of precision-nutrition micro-dosing systems improving feed efficiency | +0.7% | China, Japan, South Korea, and Australia | Medium term (2–4 years) |

| Digitized on-farm dispensers reducing labor needs and dosing errors | +0.5% | Japan, South Korea, Australia, China, and Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

African Swine Fever (ASF)-Driven Biosecurity Protocols Elevating Fortified Premix Demand

African Swine Fever devastated China's hog industry, cutting the sow herd and prompting a shift to industrialized biosecurity standards [1]Source: United States Department of Agriculture Foreign Agricultural Service, “Livestock and Poultry: World Markets and Trade,” fas.usda.gov. Integrators now raise vitamin A, D, E, zinc, and selenium inclusion rates to strengthen immunity in densely stocked facilities. Herd rebuilding in Dong Nai and Long An drove Vietnam's demand for high-protein premix and specialized feeds in 2025, raising compound feed production to 22.12 million metric tons. The Philippines required enhanced nutrition on farms in African Swine Fever (ASF)-affected areas in 2024, triggering immediate demand spikes. The modernization of livestock systems in Southeast Asia is anticipated to drive growth in the Asia-Pacific swine feed market, with specialized premix and additive segments leading the way, driven by a focus on biosecurity and feed efficiency through 2028.

Government Mandates for Antibiotic-Free Pork Accelerating Functional Additives

China banned antibiotic growth promoters in feed from July 2020, prompting increased use of enzymes, probiotics, and organic acids that boosted feed conversion by up to 5% for leading integrators. Following 2024 pilot programs in key livestock provinces, Vietnam plans to ban growth-promoting antibiotics by 2026, boosting demand for enzyme cocktails and probiotics as alternatives to Colistin and Zinc Bacitracin. Thailand’s export-oriented farms need Good Manufacturing Practice Plus certification that forbids antibiotic promoters, pushing natural growth-promoting premixes. Though compliance raised formulation costs by 8-10% in 2024-2025, integrators regained profitability through improved nutrient digestibility. The shift toward antibiotic-free feed is anticipated to boost the Asia-Pacific swine feed premix market, as producers in China and Southeast Asia focus on nutritional additives for gut health.

Rising Pork Consumption Among Emerging Middle Class Expanding Commercial Feed Penetration

India's per capita pork consumption is low at 0.24 kg, with nearly 50% of demand concentrated in the Northeast states of Assam, Nagaland, and Meghalaya, where meat availability rose significantly in the 2024-25 cycle [2]Source: Indian Council of Agricultural Research, “Livestock Production Trends,” icar.gov.in. Indonesia's pork consumption is projected to reach 0.40 kg per capita by 2026, supported by a USD 1.2 billion government plan to build 30 feed mills and secure the livestock supply chain. Metro Manila and Central Luzon together captured around 60% of incremental Philippine pork demand from 2020-2025, catalyzing a shift from backyard to commercial farming. Growing income enables farms to purchase standardized premixes rather than raw additives.

Digitized On-Farm Dispensers Reducing Labor Needs and Dosing Errors

In October 2025, CJ CheilJedang Corp. (CJ Corp.) sold its livestock and feed subsidiary, CJ Feed & Care, to Royal De Heus for 1.2 trillion won (USD 854 million) after modernizing its contract farm networks with digital farm management systems and IoT-enabled dispensers. This initiative resulted in a 20% reduction in labor and a 3% improvement in feed conversion, showcasing the effectiveness of its vertical integration model. Japan’s Zen-Noh cooperative tied blockchain-linked dispenser data to premium retail traceability claims. Adoption concentrates in markets where hourly wages exceed USD 15 [3]Source: International Labour Organization, “Wages and Working Conditions Database,” ilo.org. The technology advancement further boosts regional growth through 2027, tapering as penetration saturates early-adopter farms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile vitamin A and E prices compressing formulator margins | -0.8% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Strict Chinese ban on antibiotic growth promoters raising formulation cost | -0.6% | China, Vietnam, Thailand | Medium term (2–4 years) |

| El Niño-driven grain shortfalls disrupting supply chains | -0.5% | Vietnam, Thailand, Philippines, Indonesia | Short term (≤ 2 years) |

| Consumer skepticism toward synthetic additives steering demand to natural | -0.3% | Japan, South Korea, Australia, Urban China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Vitamin A and E Prices Compressing Formulator Margins

In July 2024, a fire at BASF SE's Ludwigshafen plant disrupted a significant portion of global precursor capacity, causing vitamin A prices to more than double by the end of the year. Supply levels returned to normal only after production resumed in April 2025. Concurrently, Zhejiang Medicine temporarily closed its Shaoxing site for environmental upgrades, leading to a 38% increase in vitamin E prices. By late 2025, multi-year low hog prices in China (below ¥11/kg) severely impacted margins, prompting swine feed premix manufacturers to delay additive purchases until 2026 while negotiating price reductions of up to 50% on vitamins. Similarly, Indian buyers postponed orders to mitigate volatility in raw material prices. Global additive prices are anticipated to stabilize fully by early 2027 as swine cycles return to normal patterns.

Strict Chinese Ban on Antibiotic Growth Promoters Raising Formulation Cost

In accordance with the Ministry of Agriculture and Rural Affairs (MARA)'s antibiotic-free mandate, Chinese feed producers have substituted colistin and zinc bacitracin with multi-enzyme and probiotic blends. This initially increased costs by 8–10%, but these were later mitigated by enhanced feed efficiency and improved animal health. Early adopters experienced a 2–3% reduction in daily gain during feed formulation refinement. Following the January 2026 ban on preventive antibiotics, Vietnamese livestock exporters have faced margin pressures due to investments in expensive probiotics and specialized feed required to meet residue-free standards for export markets such as Japan and South Korea. However, declining enzyme costs and advancements in formulation efficiency are anticipated to alleviate these challenges in the future.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enzymes Gain Momentum While Vitamins Remain Core

Vitamins secured 34% of the Asia-Pacific swine feed premix market share in 2025, as regulations mandate the use of fat-soluble vitamins for optimal growth and fertility. Enzymes, however, are projected to expand at an 8.9% CAGR through 2031, the fastest among product types, as phytase and xylanase blends recapture feed efficiency lost after antibiotic bans. Amino acids and minerals together meet a significant portion of the demand and remain indispensable for lean tissue deposition and immune support. Antibiotics accounted for a limited market share, limited to prescription therapy in China and Vietnam.

Minerals are further anticipated to follow the growth of Enzymes, owing to their natural positioning. Suppliers bundle enzymes with probiotics in single-dose sachets to ease handling and align with precision dosing systems. China’s GB 13078 hygiene code lengthens approval cycles for new actives, favoring multinational firms that operate advanced labs. These dynamics keep the Asia-Pacific swine feed premix market competitive and innovation-rich.

By Form: Dry Dominates but Liquid Surges in Automated Sites

Dry premixes occupied 71.5 % of the Asia Pacific swine feed premix market size during 2025, owing to the cooperative mills and family farms that rely on conventional batch mixers. In contrast, liquid products are forecast to post a 7.6% CAGR through 2031, benefiting from automated injection systems that reduce labor by 15-20% and tighten dosing to within 1% tolerance. The Asia-Pacific swine feed premix market for liquid formulations is experiencing rapid growth, driven by growing adoption among Japanese and South Korean integrators, who are leading rollouts, citing labor cost savings.

The adoption persists in India and Indonesia, where dispensers cost USD 50,000-80,000 per unit and require temperature-controlled storage. Leasing models are emerging to ease funding hurdles. Suppliers also use concentrated liquid additives that reduce freight weight by up to 40%, improving landed economics. As wage inflation spreads, the liquid share should rise across the Asia-Pacific swine feed premix industry.

By Functionality: Immunity Enhancement Accelerates Post-African Swine Fever (ASF)

Growth promotion retained 40.2% of the Asia Pacific swine feed premix market size in 2025, as producers still target rapid weight gain and efficient feed conversion. Immunity enhancement is projected to grow at a 9.4% CAGR through 2031, making it the fastest-growing functionality segment as African Swine Fever (ASF) recovery drives higher levels of vitamin C, E, selenium, and zinc. Feed conversion efficiency premixes held significant demand, leveraging phytase and xylanase to trim feed costs by 3-5%. Reproductive performance blends covered further hold a prominent share, addressing sow fertility and piglet viability.

China’s Ministry of Agriculture mandates fortified rations in African Swine Fever (ASF)-designated zones, boosting immunity-focused product lines. Vietnam’s imports of immunity premix rose 23 % year-on-year through September 2025 as integrators rebuilt sow numbers. Suppliers now offer micro-pack sachets that combine vitamins and trace minerals in targeted ratios. This design syncs with dispenser platforms and strengthens biosecurity compliance.

By Ingredient Source: Natural Formulations Outpace Synthetic Counterparts

Natural premixes accounted for 58.8% of the Asia Pacific swine feed premix market size in 2025, driven by retailer and consumer preferences for antibiotic-free and additive-light pork in markets such as Japan, South Korea, Australia, and urban China. The natural segment is advancing at a 7.8% CAGR through 2031, making it the fastest-growing segment in the Asia-Pacific swine feed premix market. Meanwhile, synthetic premixes continue to hold a significant share due to their ability to provide standardized potency at a lower cost, particularly in India, Indonesia, and the Philippines. Retailer programs are now heavily focused on natural-origin content, prompting integrators to incorporate plant-derived vitamins and chelated minerals into their formulations.

Fermentation-based vitamins from CJ CheilJedang Corp. (CJ Corp.) are narrowing the natural price premium to single digits. DSM-Firmenich AG commercialized algae-derived vitamin D in the Asia Pacific in 2025, further diversifying supply. These pull factors underpin long-run growth.

By Purchaser Type: Cooperative Feed Mills Emerge as Fastest-Growing Buyers

Commercial integrators commanded 56.9% of 2025 volume, leveraging direct mill-gate contracts that secure 8-12% price concessions and technical support bundles. Cooperative feed mills are projected to post the highest 8.2% CAGR through 2031 because smallholders in Indonesia, the Philippines, and India are consolidating into buying groups that match integrator purchasing power. Independent family farms retained a significant share, mainly in Thailand and Vietnam, where ownership fragmentation persists. Cooperatives now pool credit and logistics to buy fortified premixes at near-integrator prices.

Indonesia’s cooperative membership rose 18% over 2024-2025, elevating premix adoption by 14% among member farms. Philippine cooperatives receive state credit lines that underwrite inventory for 60 days, softening cash flow strain. Suppliers design discounted technical packages for cooperatives, cementing loyalty. As consolidation progresses, the Asia-Pacific swine feed premix industry will see a flatter buyer hierarchy.

By Distribution Channel: Third-Party Distributors Gain Where Infrastructure Lags

Direct mill-gate supply dominated with a 64.3% share in 2025 because large integrators own transport fleets or locate feed mills on-site. Third-party distributors are growing at an 8.5% CAGR through 2031, the fastest among channels, because they bridge logistics and credit gaps in India, Indonesia, and the Philippines. In 2025, India’s agricultural distributor network utilized a more than 50% increase in logistics supply and standard 30-60-day payment terms to boost premix adoption.

Third-party agents are increasingly combining technical advice with mobile app ordering, enhancing customer retention. Integrated players, however, continue to favor direct channels for biosecurity management and cost efficiency. Despite this, the Asia-Pacific swine feed premix market depends on distributors to access fragmented regions. This reliance is expected to continue until infrastructure developments, such as road and cold-chain projects, address existing structural challenges.

Geography Analysis

China accounted for 54.3% of the Asia-Pacific swine feed premix demand in 2025 as large-scale farms enhanced rations to improve resilience against African Swine Fever (ASF). Vietnam is projected to grow at the fastest rate, with an 8.1% CAGR through 2031, driven by foreign-funded mega-mills in Dong Nai and Long An that incorporate high-spec premixes. The adoption of precision nutrition software and automated liquid dosing systems is expanding rapidly in both countries, increasing the complexity of feed specifications. Together, China and Vietnam are projected to represent approximately two-thirds of the Asia-Pacific swine feed premix market during the forecast period.

Thailand, Indonesia, and the Philippines collectively hold a significant share of the Asia-Pacific swine feed premix market in terms of 2025 volume. Thailand benefits from export-oriented antibiotic-free certification programs that necessitate the use of natural premixes. Indonesia is projected to achieve a strong CAGR, reflecting increased pork consumption among Balinese and Papuan middle-class consumers. The Philippines is supported by urbanization and cooperative consolidation, which help standardize feed formulations.

Japan, South Korea, Australia, and New Zealand collectively hold a moderate share of the Asia-Pacific swine feed premix market and are projected to exhibit steady annual growth. These countries emphasize labor-saving dispenser technologies and traceability to cater to premium retail channels. India accounts for a smaller share, with growth driven by dietary changes in the northeastern region. Emerging markets such as Laos and Cambodia are anticipated to develop as road networks and cold-chain infrastructure improve. These diverse growth patterns are anticipated to further diversify the geographic revenue base of the Asia-Pacific swine feed premix market.

Competitive Landscape

The Asia-Pacific swine feed premix market exhibited moderate concentration in 2025, with the top five companies, such as Charoen Pokphand Group Co., Ltd., Cargill, Incorporated, Guangdong Haid Group Co., Ltd., New Hope Liuhe Co., Ltd. (New Hope Group), and SHV Holdings N.V. (Nutreco), accounting for a significant share of the market value. Charoen Pokphand Group and Cargill emerged as the two largest suppliers, collectively accounting for slightly more than one-third of regional turnover. These companies leverage captive premix plants and extensive contract-farm networks. Their vertical integration ensures access to raw materials and reduces distributor margins, enabling aggressive pricing strategies combined with technical services. Both firms have invested in automated manufacturing lines equipped with liquid injection technology, significantly reducing labor costs and improving accuracy, further strengthening their operational advantage.

In the Asia-Pacific region, companies such as Beijing Dabeinong Technology Group Co., Ltd., Tongwei Co., Ltd., and Guangdong Haid Group Co., Ltd. utilize localized formulations and on-farm advisory teams to capture market share from multinational competitors. Bluestar Adisseo Company (Sinochem Holdings) operates a methionine complex in Nanjing, which helps stabilize its premix margins against fluctuations in amino acid prices.

From 2026 onward, competition in the Asia-Pacific swine feed premix market will revolve around sustainability scoring, carbon labeling, and premium natural formulations. Suppliers integrating precision software with ingredient production will achieve cost reductions and enhanced nutrient accuracy. Expansion into regions such as India’s northeast and Indonesia’s outer islands will depend on forming distributor alliances and utilizing micro-finance solutions. These developments will gradually elevate the industry toward higher value-added segments without leading to monopolistic conditions.

Asia-Pacific Swine Feed Premix Industry Leaders

Charoen Pokphand Group Co., Ltd.

Cargill, Incorporated

Guangdong Haid Group Co., Ltd.

New Hope Liuhe Co., Ltd. (New Hope Group)

SHV Holdings N.V. (Nutreco)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DSM-Firmenich AG finalized the divestiture of its stake in the Feed Enzymes Alliance to Novonesis for EUR 1.5 billion (USD 1.65 billion), unlocking cash for core nutrition and health investments while consolidating Novonesis’ position in global feed enzymes.

- January 2025: Godrej Agrovet introduced “Pride Hog,” a stage-wise pig feed range that includes Starter, Grower, and Finisher variants formulated to boost immunity and growth among the 9-million-head Indian herd, with a launch roundtable in Guwahati addressing African Swine Fever prevention.

- September 2024: Japfa Vietnam opened a new feed plant in Huong Canh, Vinh Phuc province, designed to serve swine producers across northern Vietnam with modern bulk-handling and macro-dosing systems, thereby increasing the company's installed capacity for its integrated operations.

Asia-Pacific Swine Feed Premix Market Report Scope

A feed premix is a concentrated mixture of essential nutrients, additives, and supplements that are incorporated into animal feed to enhance its nutritional value and ensure optimal animal health, growth, and productivity. The Asia Pacific feed premix market segmentation by Product Type (Vitamin Premix, Mineral Premix, Amino Acid Premix, Antibiotic Premix, and More), by Form (Dry and Liquid), by Functionality (Growth Promotion, and More), by Ingredient Source (Natural and Synthetic). Additionally, the report presents a detailed analysis of the market by Geography (China, India, Japan, South Korea, Vietnam, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Vitamins |

| Minerals |

| Amino Acids |

| Antibiotics |

| Enzymes |

| Other Types (Probiotics, Essential Oils) |

By Form

| Dry |

| Liquid |

By Functionality

| Growth Promotion |

| Immunity Enhancement |

| Reproductive Performance |

| Feed Conversion Efficiency |

By Ingredient Source

| Natural |

| Synthetic |

By Purchaser Type

| Commercial Integrators |

| Cooperative Feed Mills |

| Independent Family Farms |

By Distribution Channel

| Direct (Mill-Gate) |

| Third-Party Distributors |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Vietnam |

| Thailand |

| Philippines |

| Indonesia |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Vitamins |

| Minerals | |

| Amino Acids | |

| Antibiotics | |

| Enzymes | |

| Other Types (Probiotics, Essential Oils) | |

| By Form | Dry |

| Liquid | |

| By Functionality | Growth Promotion |

| Immunity Enhancement | |

| Reproductive Performance | |

| Feed Conversion Efficiency | |

| By Ingredient Source | Natural |

| Synthetic | |

| By Purchaser Type | Commercial Integrators |

| Cooperative Feed Mills | |

| Independent Family Farms | |

| By Distribution Channel | Direct (Mill-Gate) |

| Third-Party Distributors | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Thailand | |

| Philippines | |

| Indonesia | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected value of Asia-Pacific premix demand in 2025?

The Asia-Pacific swine feed premix market size is estimated at USD 4.95 billion in 2025.

Which country will expand the fastest by 2031?

Vietnam is forecast to grow at an 8.1% CAGR through 2031, driven by new foreign-funded mega-mills.

Which segment shows the highest growth rate?

Enzymes are leading with an 8.9% CAGR through 2031, as they replace banned antibiotic growth promoters.

Why are liquid premixes gaining importance?

Automated injection systems in large integrator facilities reduce labor and dosing errors, driving a 7.6% CAGR through 2031, for liquid formats.

How concentrated is supplier power in the region?

The top five companies account for a significant share of the 2025 Asia Pacific swine feed market size, giving the market a moderate concentration.

Page last updated on: