Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

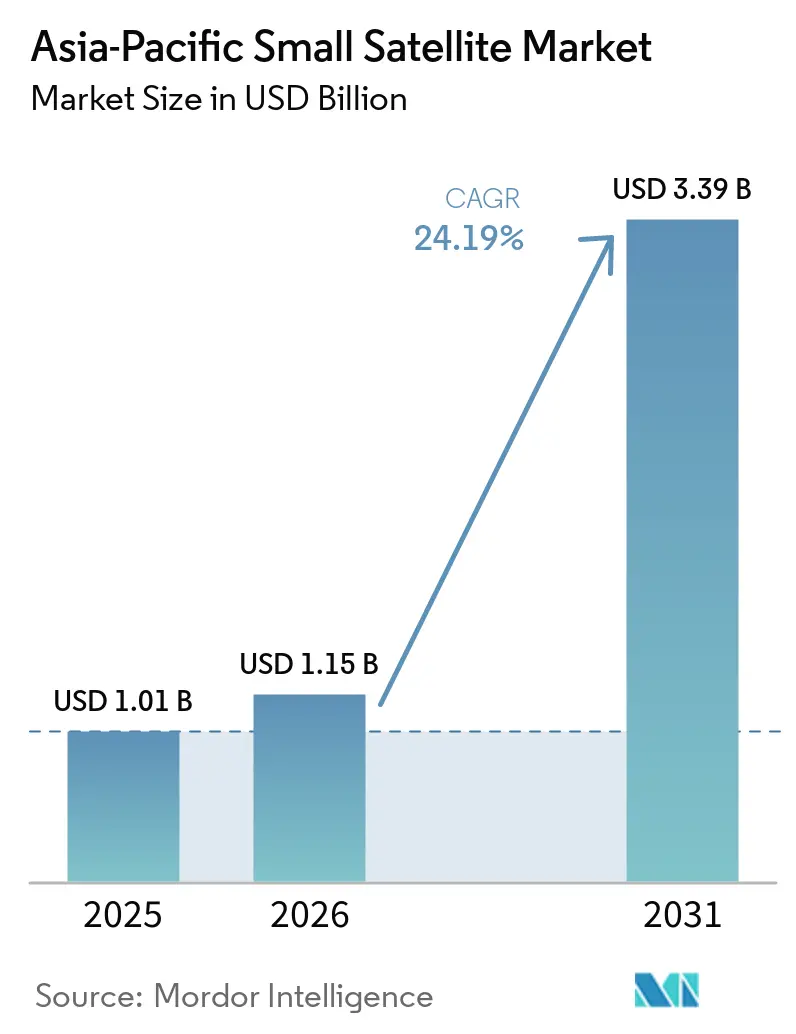

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 24.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Small Satellite Market Analysis by Mordor Intelligence

The Asia-Pacific small satellite market size is projected to grow from USD 1.01 billion in 2025 to USD 1.15 billion in 2026 and is forecast to reach USD 3.39 billion by 2031 at 24.19% CAGR over 2026-2031. The Asia-Pacific small satellite market is expanding rapidly as sovereign constellation programs move from planning to deployment and public-private procurement models open a broader path for commercial participation. Demand is also rising as military and civil agencies treat satellite capacity as operational infrastructure rather than as a support tool used only for selected missions. Commercial buyers are adding to that demand by seeking higher revisit rates, better imaging performance, and faster data delivery for analytics-led use cases. Manufacturing scale is improving across the region as launch activity increases and component sourcing becomes more organized around repeat production runs. The main pressure points for the Asia-Pacific small satellite market remain access to orbital slots, spectrum coordination, and compliance with debris-related regulations, which are increasing execution risk and operating costs for smaller operators.

Key Report Takeaways

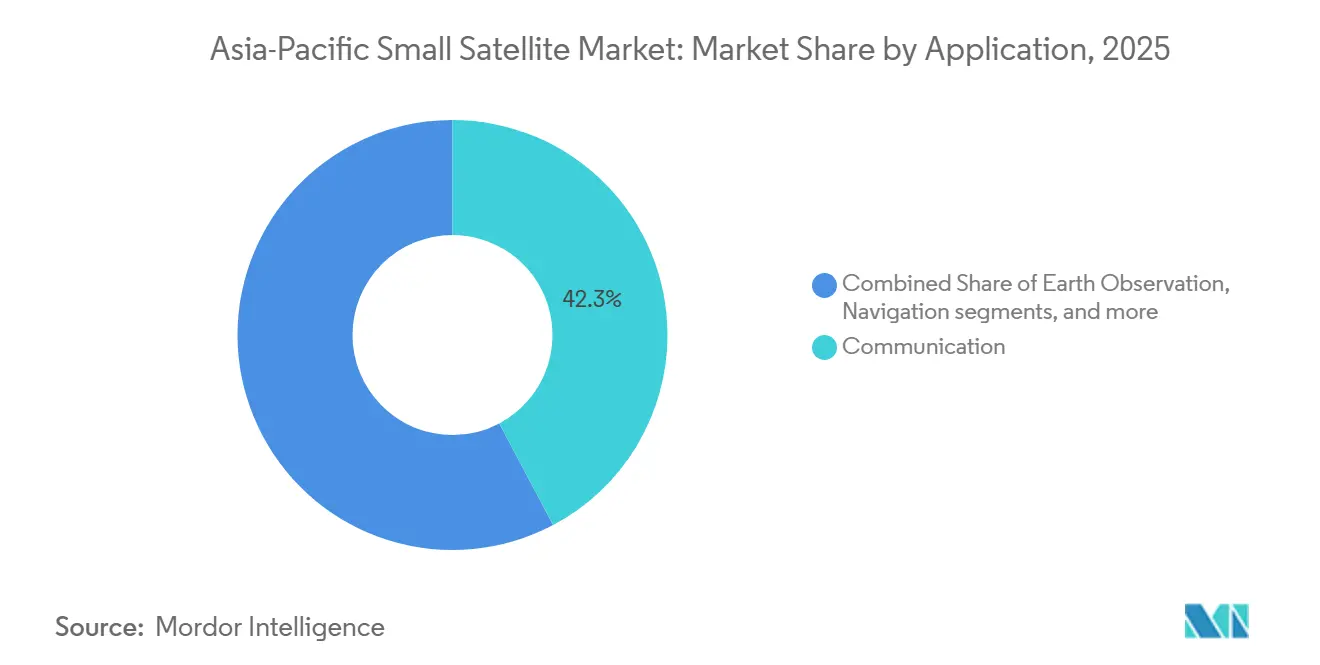

- By application, communication accounted for 42.25% of revenue in 2025, while Earth observation is projected to expand at a 25.78% CAGR through 2031.

- By orbit, LEO accounted for 51.75% of revenue in 2025, while MEO is forecast to grow at 25.83% CAGR through 2031.

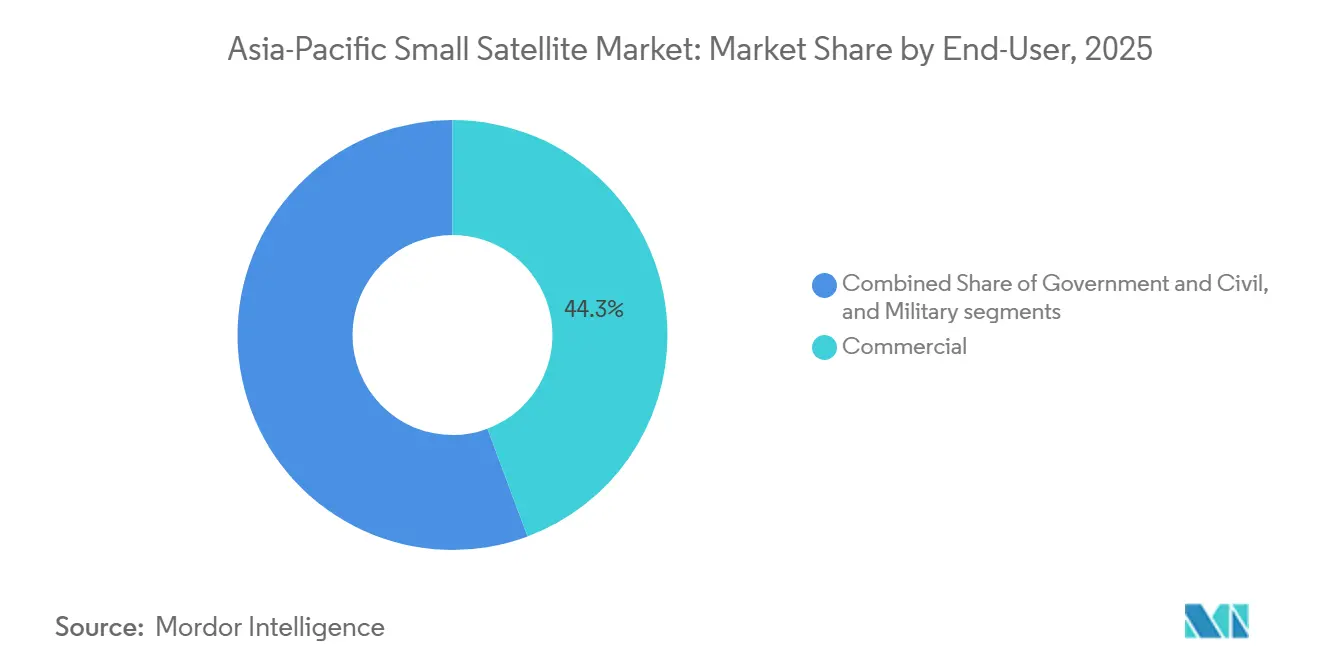

- By end-user, the commercial segment captured 44.32% of revenue in 2025, while government and civil is forecast to advance at a 25.95% CAGR through 2031.

- By satellite mass, minisatellites represented 46.69% of revenue in 2025, while microsatellites are expected to grow at 25.58% CAGR through 2031.

- By geography, China accounted for 68.77% of revenue in 2025, while India is forecast to grow at a 26.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Small Satellite Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid expansion of mega-constellation programs across Asia-Pacific | 5.50% | China, with spillover to ASEAN and India | Short term (≤ 2 years) |

| Increasing investments in government-led space initiatives | 5.00% | India, Japan, South Korea, Australia | Medium term (2-4 years) |

| Declining launch costs driven by regional small-lift providers | 4.00% | India, China, South Korea, Rest of Asia-Pacific | Medium term (2-4 years) |

| Growing demand for real-time Earth-observation analytics | 3.50% | Regional, with early gains in India, Japan, and China | Medium term (2-4 years) |

| Rising adoption of CubeSat-based IoT connectivity networks | 2.50% | China, core ASEAN markets, and South Asia | Short term (≤ 2 years) and Medium term (2-4 years) |

| Increasing integration of optical relay systems with 5G NTN infrastructure | 2.00% | Japan, South Korea, Singapore, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Mega-Constellation Programs Across Asia-Pacific

China's launch cadence has entered a new scale phase, reshaping the Asia-Pacific small satellite market. The country recorded 92 orbital launches in 2025 and is targeting as many as 140 launches in 2026, with Guowang and Qianfan expected to use 70 or more of those missions.[1]SpaceNews Staff, “China Conducts Pair of Long March Launches for Thousand Sails and Guowang Megaconstellations,” SpaceNews, spacenews.com By April 2026, Guowang had 168 operational satellites against a 13,000-satellite ITU-filed target, while Qianfan had 126 satellites in orbit against a 15,000-satellite approved plan. That scale is pushing the regional supply chain toward higher output in components, integration work, and launch services. It is also lowering unit costs faster than standalone commercial demand would have, improving hardware access for buyers across the Asia-Pacific small satellite market, even when procurement policy still leans toward local sourcing.

Increasing Investments in Government-Led Space Initiatives

Government spending is rising across the region, but the more important shift is that procurement models are becoming more open to private execution in the Asia-Pacific small satellite market. India's Department of Space received INR 13,705.6 crore (USD 1.62 billion) in the FY2026-27 Union Budget, above the revised FY2025-26 level of INR 12,448.6 crore (USD 1.30 billion), and capital expenditure also moved higher.[2]Staff Reporter, “Union Budget 2026, Government Allocates Rs 13,705 Crore for Department of Space,” The Economic Times, economictimes.indiatimes.com South Korea's 2026 space budget reached KRW 1.2 trillion (USD 790 million) and included satellite information utilization across 42 projects in 13 ministries.[3]DongA Science Staff, “South Korea Boosts Lunar Lander Development with 1.16 Trillion Won Space Budget,” DongA Science, dongascience.com These budget decisions are supporting mixed execution models in which private firms build spacecraft, supply payloads, and deliver data services under public mandates. That improves revenue visibility, reduces early commercialization risk, and strengthens domestic manufacturing capacity across the Asia-Pacific small satellite market.

Declining Launch Costs Driven by Regional Small-Lift Providers

The reduction in launch costs has emerged as a significant driver of growth in the Asia-Pacific small satellite market. This trend is attributed to the rise of regional small launch operators and advancements in launch technology. Historically, satellite deployment was an expensive process requiring substantial investments in large, dedicated rockets, limiting access to governments and major organizations. However, regional space firms and government agencies in countries such as China, India, Japan, South Korea, and Australia are now investing in cost-efficient launch platforms tailored for small satellites. The adoption of rideshare missions, where multiple satellites share a single rocket to reduce costs, has further enhanced affordability and accessibility for startups, research institutions, and commercial entities. These cost-effective launch solutions enable more frequent satellite deployments for applications such as remote sensing, communication services, IoT connectivity, scientific research, and defense.

Growing Demand for Real-Time Earth Observation Analytics

Demand in the Asia-Pacific small satellite market is moving from image collection alone toward faster interpretation and decision-ready geospatial output. In January 2026, Pixxel led a consortium that signed an INR 1,200 crore (USD 142 million) agreement with IN-SPACe to build India's first privately led national Earth observation constellation of 12 satellites under a public-private partnership structure.[4]Pixxel Team, “Pixxel-Led Consortium Signs Agreement with IN-SPACe to Build India’s National EO Constellation,” Pixxel, pixxel.space The program spans optical, multispectral, SAR, and hyperspectral payloads, indicating that buyers want broader sensing capability from a single constellation. Pixxel also partnered with Sarvam AI to build an orbital data center satellite targeted for launch by Q4 2026, which shows how analytics functions are moving closer to the spacecraft. As this model spreads, the Asia-Pacific small satellite market should capture a larger share of value at the operator level rather than only in downstream software and imagery resale.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing spectrum allocation congestion across LEO bands | -2.50% | Global, with acute effects on APAC new entrants in Ku and Ka bands | Short term (≤ 2 years) |

| Rising costs of orbital debris mitigation compliance | -1.50% | Global, with disproportionate effects on smaller APAC operators | Medium term (2-4 years) |

| Export control restrictions on advanced satellite technologies and components | -1.50% | India, South Korea, and ASEAN, with less impact on China | Medium term (2-4 years) |

| Limited availability of on-orbit servicing infrastructure in Asia-Pacific | -1.00% | APAC-wide, especially India and ASEAN | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Spectrum Allocation Congestion Across LEO Bands

Spectrum access is becoming one of the clearest structural constraints on the Asia-Pacific small satellite market. In December 2025, China filed ITU paperwork for 2 additional satellite networks, each comprising 96,714 satellites, bringing potential new Chinese filings to nearly 200,000 satellites. A 2025 analysis published in ScienceDirect found that rapid expansion of LEO constellations is exposing major limitations in the ITU coordination model, with the Ku and Ka bands already facing increasing interference. Smaller operators, therefore, face longer filing cycles, more complex coordination work, and a greater risk that early movers secure high-value slots. That combination can delay deployment plans and reduce commercial flexibility across the Asia-Pacific small satellite market.

Rising Costs of Orbital Debris Mitigation Compliance

Debris mitigation is becoming a direct cost item in the Asia-Pacific small satellite market rather than a secondary policy issue. Operators seeking access to the U.S. market must meet the FCC's 5-year deorbit rule, which can require additional propellant, drag devices, or external support arrangements that increase mass and cost burdens on low-cost spacecraft. NASA's 2024 cost-benefit analysis found that just-in-time collision avoidance technologies could return 100 to 300 times their cost through reduced collision risk. Asia-Pacific operators still have limited regional access to commercial in-orbit servicing and dedicated debris support infrastructure. That leaves smaller developers with a heavier compliance load and makes scale a stronger competitive advantage across the Asia-Pacific small satellite market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Earth Observation Closing the Gap on Communication

Communication accounted for 42.25% of the Asia-Pacific small satellite market share in 2025, while Earth observation is projected to expand at 25.78% CAGR through 2031. Communication remains the largest application because mega-constellation deployment, IoT-focused networks, and data relay needs continue to drive the broadest current demand. Earth observation is growing faster because regional buyers now want more than periodic imagery and are shifting spending toward systems that can support faster analysis and more continuous monitoring, changing how operators design payload mixes, revisit strategies, and downstream services across the Asia-Pacific small satellite market.

The Earth observation opportunity is being reinforced by public programs that seek sovereign sensing capability rather than outsourced access alone. Pixxel's 2026 agreement with IN-SPACe combines optical, multispectral, SAR, and hyperspectral systems into a single national constellation, pointing to broader procurement goals than just imaging coverage. Navigation demand is also rising as countries look to supplement or localize positioning and timing capacity for civilian and strategic uses. Space observation and other applications remain smaller, but they still matter for scientific missions, academic programs, and early-stage technology demonstration within the Asia-Pacific small satellite industry.

By Orbit: LEO as the Platform of Choice, MEO Gaining Strategic Relevance

LEO accounted for 51.75% of revenue in the Asia-Pacific small satellite market in 2025, making it the primary deployment layer for current communication, Earth observation, and IoT missions. Its lead reflects lower launch energy needs, shorter signal latency, and a stronger fit with constellation architectures that require frequent revisit or continuous network growth. MEO is forecast to grow at a 25.83% CAGR through 2031 as operators seek navigation augmentation and medium-latency services that sit between LEO and GEO. GEO still serves selected broadcast and VSAT use cases, but competitive pressure from higher-throughput LEO satellite systems is increasing. Japan's NICT achieved the world's first demonstration of 2 Tbit/s free-space optical communication in December 2025, using small-satellite-mountable terminals, supporting the case for multi-orbit optical relay systems that can improve data transfer across regional networks as the Asia-Pacific small satellite market matures. Even with that progress, continuous-zone coverage requirements will keep part of the demand anchored in GEO and in mixed-orbit architectures across the Asia-Pacific small satellite industry.

By End-User: Government and Military Procurement Reshaping the Demand Mix

Commercial users accounted for 44.32% of the Asia-Pacific small satellite market in 2025, while government and civil demand are projected to grow at a 25.95% CAGR through 2031. Commercial demand remains broad because Chinese constellation operators, analytics firms, and enterprise buyers still account for a large share of current spacecraft deployments and data consumption.

Military and government demand is growing faster as satellite systems become increasingly important for surveillance, maritime awareness, border monitoring, and resilient communications. This shift is raising demand for higher-specification payloads, stronger system reliability, and longer program continuity across the Asia-Pacific small satellite market. India's 2026 Pixxel-led Earth observation program shows how government procurement is being structured around private execution rather than only state-led delivery. Government and civil customers also provide a steadier contract base because they are more willing to fund indigenous capability development over multiple years. Dual-use mission design is becoming more common, enabling one spacecraft to support civilian imaging, environmental monitoring, and defense surveillance simultaneously. That change is increasing system complexity and favoring integrators with deeper engineering, compliance, and execution capability across the Asia-Pacific small satellite market.

By Satellite Mass: Minisatellites Lead as Microsatellites Reach Manufacturing Scale

Minisatellites held 46.69% of revenue in 2025 in the Asia-Pacific small satellite market, while microsatellites are expected to expand at 25.58% CAGR through 2031. Minisatellites still lead because many government and high-capability commercial programs prefer larger platforms that can support heavier payloads and broader mission sets. Microsatellites are growing faster because they offer a better balance of payload flexibility, constellation economics, and manufacturing repeatability for new operators. The result is a more active middle layer of spacecraft design that bridges low-cost experimentation and full-scale national programs in the Asia-Pacific small satellite market. Dhruva Space's Project Garud is designed around a standardized 500 kg-class platform and a production target of 500 to 600 satellites per year, which shows how scale economics are reshaping platform strategy.

Femtosatellites, picosatellites, and nanosatellites still play a role in technology demonstrations and selective IoT missions, even though their revenue contribution remains small. More standardized production in the 10 kg to 100 kg range is lowering cost and schedule barriers for constellation entrants. That makes microsatellites a practical first step for operators who want to validate capability before moving into heavier fleet investment in the Asia-Pacific small satellite market.

Geography Analysis

China accounted for 68.77% of revenue in the Asia-Pacific small satellite market in 2025, making it the clear center of regional demand, manufacturing, and launch activity. Its lead is driven by state-directed constellation programs, especially Guowang and Qianfan, with ITU-filed or approved plans totaling 28,000 satellites. China recorded 92 orbital launches in 2025 and is targeting as many as 140 in 2026, with Guowang and Qianfan expected to account for 70 or more missions. In December 2025, China also filed ITU paperwork for 2 additional networks of 96,714 satellites each, reinforcing its push to secure orbital and spectrum access ahead of future regulatory changes. This combination of launch cadence, policy support, and industrial depth gives China a structural lead in the Asia-Pacific small satellite market.

India is the fastest-growing geography, with 26.85% CAGR projected through 2031 in the Asia-Pacific small satellite market. The country's FY2026-27 budget allocated INR 13,705.6 crore (USD 1.62 billion) to the Department of Space. Pixxel's January 2026 agreement with IN-SPACe to build a 12-satellite national Earth observation constellation is giving India a visible template for private participation in publicly backed infrastructure programs. The 2025 removal of customs duties on satellite components and launch vehicle goods also lowered procurement barriers for domestic operators and supports manufacturing buildout.

Japan and South Korea form the region's second tier of investment, combining industrial maturity with rising strategic and commercial demand in the Asia-Pacific small satellite market. South Korea's 2026 space budget reached KRW 1.2 trillion (USD 790 million) and supports the fifth Nuri launch, lunar lander work, and AI-based satellite information services across 42 government projects. Japan is advancing in higher-value niches through work in optical communications and Earth observation, including NICT's free-space optical demonstration and Axelspace's planned GRUS-3 deployment. Australia and the rest of the region remain smaller in value. Still, they matter as test beds for CubeSat programs, startup ecosystems, institutional buildout, and new LEO satellite service models across the Asia-Pacific small satellite market.

Competitive Landscape

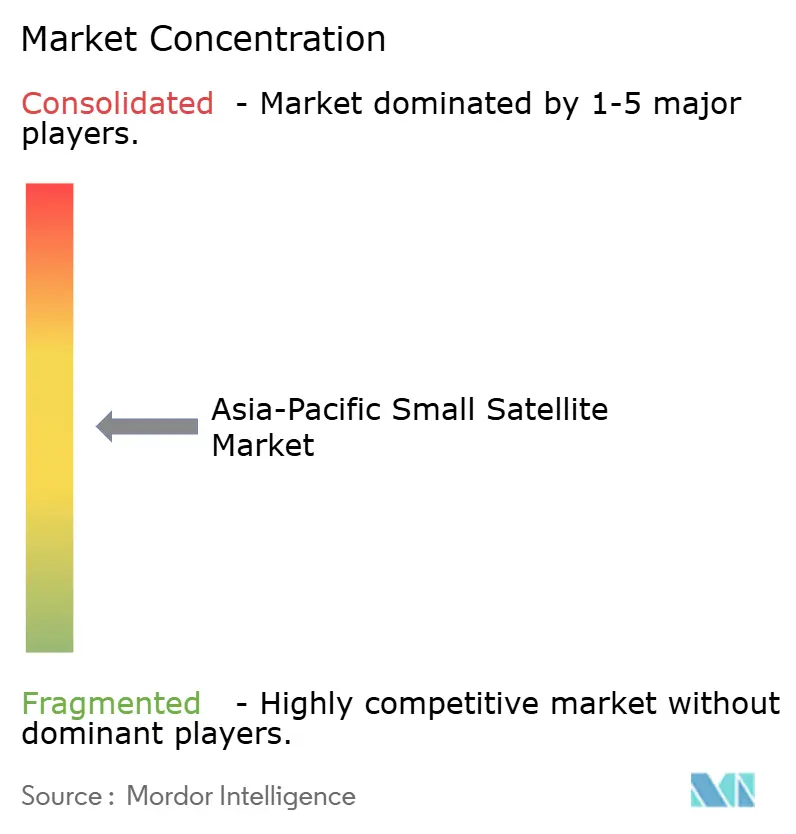

The Asia-Pacific small satellite market is moderately fragmented across 3 broad competitive tiers. Chinese state-backed entities, including CASC and CGST, lead by aggregate output because they benefit from captive launch schedules, large domestic constellation programs, and policy-backed scale. Japanese and Korean companies such as Axelspace, Satrec Initiative, and NEC compete through dual-use engineering depth, payload capability, and long-standing government relationships. Indian firms such as Pixxel and Dhruva Space are gaining ground quickly as public-private procurement creates clearer order visibility and faster commercialization pathways. The ISRO provides cost-effective launch services, advanced satellite development capabilities, and support for commercial and international space missions, shaping the Asia-Pacific small satellite market beyond price alone, as launch access, integration capability, delivery speed, and compliance readiness now matter just as much.

Strategic positioning in the Asia-Pacific small satellite market is increasingly built around vertical integration, manufacturing services, and space-terrestrial convergence. NEC completed payload design in March 2026 for an optical communication technology demonstration satellite planned for FY2027, signaling a push into inter-satellite links and high-capacity data transfer. Kongsberg KSAT and NanoAvionics also formed a 2026 partnership combining small satellite platforms with a global ground station network, pointing to rising demand for integrated mission services. Technology differentiation is becoming sharper in hyperspectral imaging, optical inter-satellite links, SAR deployment speed, and 5G non-terrestrial network integration across the Asia-Pacific small satellite market.

At the same time, no regional operator currently offers commercially established in-orbit refueling or life-extension services, leaving a clear gap as disposal expectations and debris rules tighten. Buyers are also placing greater weight on transparent testing, program execution discipline, and credible deorbit planning when evaluating vendors. This combination of fragmentation and rising compliance pressure favors companies that can pair specialized technology with dependable delivery and long-term support in the Asia-Pacific small satellite market.

Asia-Pacific Small Satellite Industry Leaders

Chang Guang Satellite Technology Co. Ltd.

China Aerospace Science and Technology Corporation

Indian Space Research Organisation

NEC Space Technologies, Ltd.

Axelspace Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Dhruva Space received an INR 105 crore (USD 12.4 million) grant from India's Research, Development, and Innovation Fund for Project Garud, targeting a standardized 500 kg-class satellite platform designed for high-volume deployment at production rates of 500 to 600 satellites per year.

- May 2026: Axelspace announced the simultaneous launch of 7 GRUS-3 Earth observation microsatellites after July 2026 aboard SpaceX's Transporter-17 rideshare from Vandenberg Space Force Base, with Nikon telescopes targeting 2.2-meter resolution at daily revisit frequency.

- April 2026: China conducted 2 Long March launches in the month, adding 18 Qianfan satellites and 5 Guowang satellites, respectively, maintaining China's trajectory toward 400 Guowang satellites in orbit by 2027 and supporting the national target of 140 launches in 2026.

- March 2026: NEC Corporation completed the design of payload equipment for a small optical communication technology demonstration satellite covering inter-satellite optical links, high-speed routing, and millimeter-wave band communications, with launch scheduled for FY2027.

Asia-Pacific Small Satellite Market Report Scope

Small satellites are those satellites weighing under 500 kg. The small satellite market report excludes sounding rockets, high-altitude balloon platforms, and purely experimental payloads.

The Asia-Pacific small satellite market is segmented by application, orbit, end-user, satellite mass, and geography. By application, the market is segmented into communication, Earth observation, navigation, space observation, and others. By orbit, the market is segmented into low Earth orbit (LEO), medium Earth orbit (MEO), and geostationary orbit (GEO). By end-user, the market is segmented into commercial, government and civil, and military. By satellite mass, the market is segmented into femtosatellites, picosatellites, nanosatellites, microsatellites, and minisatellites. The report also covers the market sizes and forecasts for the Asia-Pacific small satellite market in five countries across the region. For each segment, the market size is provided in terms of value (USD).

By Application

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

By Orbit

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

By End-User

| Commercial |

| Government and Civil |

| Military |

By Satellite Mass

| Femtosatellites |

| Picosatellites |

| Nanosatellites |

| Microsatellites |

| Minisatellites |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others | |

| By Orbit | Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) | |

| Geostationary Orbit (GEO) | |

| By End-User | Commercial |

| Government and Civil | |

| Military | |

| By Satellite Mass | Femtosatellites |

| Picosatellites | |

| Nanosatellites | |

| Microsatellites | |

| Minisatellites | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.