Asia-Pacific Military Satellite Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 23.07 Billion |

| Market Size (2030) | USD 37.58 Billion |

| Growth Rate (2025 - 2030) | 10.25% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Military Satellite Market Analysis by Mordor Intelligence

The Asia-Pacific Military Satellite Market size is estimated at 23.07 billion USD in 2025, and is expected to reach 37.58 billion USD by 2030, growing at a CAGR of 10.25% during the forecast period (2025-2030).

The Asia-Pacific military satellite industry is experiencing transformative growth driven by substantial government investments in space technology and infrastructure. China has emerged as a leading force in the region's space sector, with a significant space budget allocation of USD 10.2 billion in 2022, followed by Japan at USD 4.2 billion and India at USD 1.96 billion. This increased funding has enabled the development of sophisticated military space systems and ground infrastructure, fostering innovation across the entire space value chain. The strategic importance of defense space capabilities has led to the establishment of dedicated space agencies and research centers, promoting collaboration between government entities and private sector participants.

A notable trend in the market is the evolution towards dual-use satellites that serve both military and civilian purposes, optimizing resource utilization and cost-effectiveness. This is exemplified by recent developments such as India's ISRO's delivery of the GSAT 7B military-grade multiband satellite, with an investment of INR 4,635 crore, designed to provide both strategic communications and civilian applications. The integration of commercial technologies with military satellite requirements has created new opportunities for industry participants, while also addressing the growing demand for reliable and secure satellite communications.

The market is witnessing a significant emphasis on Earth observation and reconnaissance capabilities, with countries rapidly expanding their satellite constellations. In 2022, China demonstrated this trend by launching a series of 27 classified military Earth observation satellites, highlighting the growing importance of space-based intelligence gathering. The continued deployment of advanced imaging satellites, such as the March 2023 launch of the Gaofen satellite, reflects the region's commitment to enhancing its space-based surveillance and monitoring capabilities.

The industry landscape is being reshaped by increasing commercial participation and international collaboration in military space programs. Between 2017 and 2022, approximately 146 satellites were manufactured and launched for various military and government applications in the region, indicating the scale of space activities. This has led to the emergence of specialized satellite manufacturers, launch service providers, and technology companies that support military space technology missions. The growing ecosystem of commercial space companies is introducing innovative technologies and cost-effective solutions, while maintaining the high reliability and security standards required for military applications.

Asia-Pacific Military Satellite Market Trends and Insights

Increasing demand for satellite miniaturization globally

- Miniature satellites leverage advances in computation, miniaturized electronics, and packaging to produce sophisticated mission capabilities. Microsatellites can share the ride to space with other missions and offer a considerable reduction in launch costs. The demand from Asia-Pacific is primarily driven by China, Japan, South Korea, and India, which manufacture the largest number of small satellites each year. Though the launches from the country have decreased over the last three years, a huge potential lies in the country’s industry, and the ongoing investments in the startups and the nano and microsatellite development projects are expected to boost the revenue growth of the region. Between 2017 and 2022, more than 50 nano and microsatellites were placed into orbit by various players in the region.

- For instance, in November 2021, China successfully launched a new remote-sensing satellite, Yaogan-35A, into space from the Xichang Satellite Launch Center. Yaogan-35A is an intelligence, surveillance, and reconnaissance (ISR) satellite. The Yaogan-35A series of satellites are built by the Small Satellite Centre at the China Academy of Science (CAS). It is speculated that these satellites are signals or electronic intelligence (SIGINT/ELINT) gathering systems that will collect and geolocate radio emissions from ships and are part of the Chinese maritime domain awareness mission.

,-Number-of-Launches,-Asia-Pacific,-2017---2022.svg)

Investment opportunities in the global satellite manufacturing market

- Considering the increase in space-related activities in Asia-Pacific, satellite manufacturers are enhancing their satellite production capabilities to tap into the rapidly emerging market potential. The prominent countries in Asia-Pacific that pose a robust space infrastructure are China, India, Japan, and South Korea. China National Space Administration (CNSA) announced space exploration priorities for the 2021-2025 period, including enhancing national civil space infrastructure and ground facilities. As a part of this plan, the Chinese government established China Satellite Network Group Co. Ltd for the development of a 13,000-satellite constellation for satellite internet.

- In 2022, according to the draft budget of Japan, the space budget of the country was over USD 1.4 billion, which included investment for space activities of 11 government ministries, such as the development of the H3 rocket, Engineering Test Satellite-9, and the nation’s Information Gathering Satellite (IGS) program. India has become a global leader in third-party launch services and has several ongoing R&D programs for new launch platforms. The proposed budget for India's space programs for FY22 was USD 1.83 billion.

- South Korea's space program has seen slow progress as other countries are reluctant to transfer core technologies. In 2022, the Ministry of Science and ICT announced a space budget of USD 619 million for manufacturing satellites, rockets, and other key space equipment. Many Southeast Asian countries have started investing in space technology. As of March 2021, the Indonesian government secured USD 545 million to continue the fabrication of the very high throughput satellite (SATRIA), using a public-private partnership (PPP) scheme, for launch in 2023.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Small satellites are poised to create demand in the market

Segment Analysis: Satellite Mass

Above 1000kg Segment in Asia-Pacific Military Satellite Market

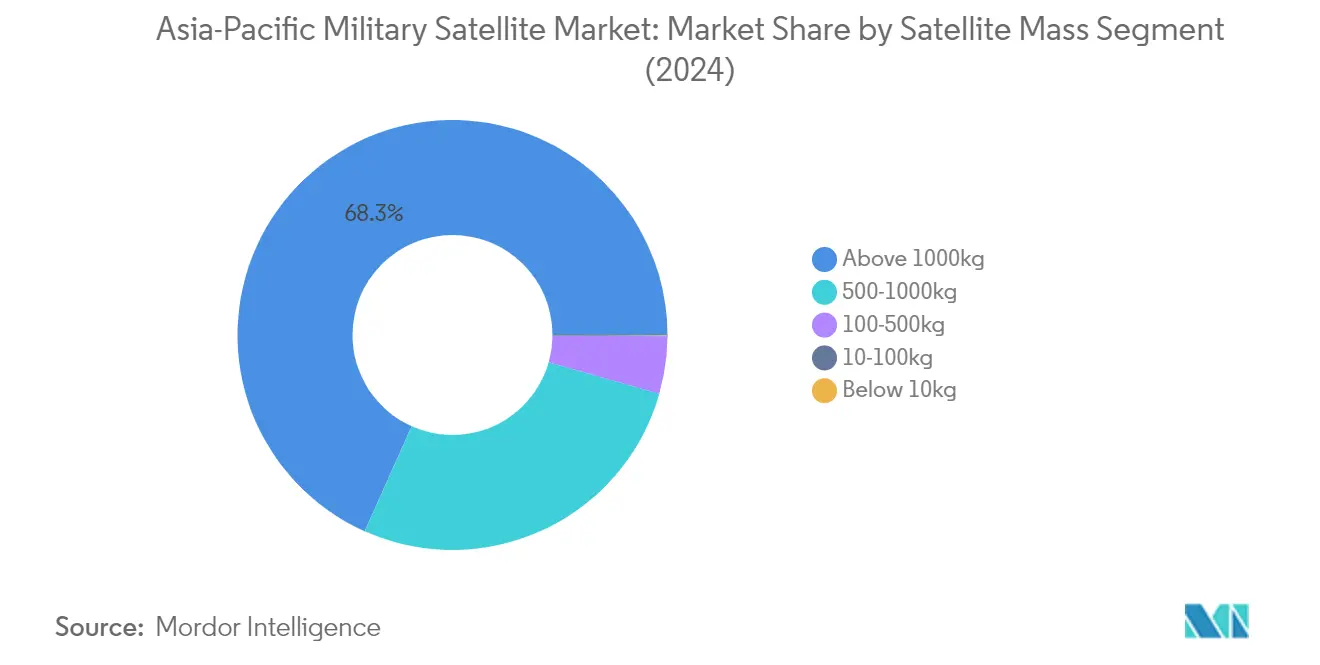

The above 1000kg satellite segment dominates the Asia-Pacific military satellite market, commanding approximately 68% market share in 2024. These large satellites are primarily designed for operational purposes with extended lifetimes ranging between 5 and 10 years, making them crucial for military applications. They are extensively used to carry larger remote sensing payloads and larger antennas for communication purposes. These operational satellites incorporate redundancy for all major subsystems to support random failures and extend lifespan, making them highly reliable for military operations. Countries like China, Japan, and India are significantly investing in large military surveillance satellite systems that serve dual purposes - military and civilian applications. The segment's dominance is further strengthened by the increasing deployment of advanced communication satellites, navigation systems, and surveillance platforms by major military powers in the region.

10-100kg Segment in Asia-Pacific Military Satellite Market

The 10-100kg satellite segment is experiencing remarkable growth in the Asia-Pacific military satellite market, projected to expand at approximately 30% during 2024-2029. This rapid growth is driven by the increasing adoption of microsatellites for specific military missions, particularly due to their cost-effectiveness and operational flexibility. These satellites are designed for medium-duration applications of up to two years and feature redundancy for critical subsystems like bus management units. The development of anti-satellite capabilities by Asia-Pacific countries has further accelerated the demand for smaller satellites weighing less than 100 kg, as they are more difficult to target and can operate in constellations to match the capabilities of larger satellites. The segment's growth is also supported by their lower manufacturing costs and ease of mass production, making them an attractive option for military space programs.

Remaining Segments in Satellite Mass

The remaining segments in the satellite mass category include 500-1000kg (medium satellites), 100-500kg (mini satellites), and below 10kg (nanosatellites) segments. Medium satellites are crucial for navigation and global positioning applications, while mini satellites compete with large satellites in many applications through their miniaturized but redundant electronics. The nanosatellite segment, though smaller in market share, is gaining importance for specialized military missions and technology demonstration purposes. These segments collectively contribute to the diverse requirements of military space operations, offering different capabilities based on specific mission requirements, orbital parameters, and payload configurations. The variety in satellite mass categories enables military organizations to maintain a comprehensive space-based capability portfolio, from high-resolution imaging to tactical communications.

Segment Analysis: Orbit Class

LEO Segment in Asia-Pacific Military Satellite Market

Low Earth Orbit (LEO) dominates the Asia-Pacific military satellite market, commanding approximately 85% of the market share in 2024. The segment's prominence is driven by the increasing demand for satellite-based applications such as Earth observation, remote sensing, and communication services. China's significant focus on enhancing its space capabilities and rising expenditure in the space sector has been a major contributor to this segment's dominance. The Chinese government's substantial investment of approximately USD 10.3 billion in space programs has strengthened the LEO segment's position. Military organizations in the region are increasingly deploying LEO satellites for intelligence, surveillance, and reconnaissance (ISR) missions, leveraging their advantages of lower latency and higher resolution imaging capabilities.

GEO Segment in Asia-Pacific Military Satellite Market

The Geostationary Earth Orbit (GEO) segment is projected to be the fastest-growing segment in the Asia-Pacific military satellite market, with an expected growth rate of approximately 15% during 2024-2029. This growth is primarily driven by the increasing demand for reliable, long-range communication systems and broadcasting services for military applications. Several countries in the region, including China, Japan, and India, are actively investing in GEO satellite technology to enhance their military communication capabilities and ensure continuous coverage over specific geographical areas. The segment's growth is further supported by technological advancements in satellite communication systems and the increasing need for secure, high-bandwidth communication channels for military operations.

Remaining Segments in Orbit Class

The Medium Earth Orbit (MEO) segment plays a crucial role in the Asia-Pacific military satellite market, particularly in navigation and positioning applications. MEO satellites serve as vital components in global navigation satellite systems, providing essential services for military operations and strategic planning. These satellites operate at an optimal altitude that balances coverage area with signal strength, making them particularly effective for navigation and timing applications. The MEO segment continues to evolve with technological advancements and increasing integration with other orbit-based systems, contributing to the overall robustness of military satellite infrastructure in the region.

Segment Analysis: Satellite Subsystem

Propulsion Hardware and Propellant Segment in Asia-Pacific Military Satellite Market

The propulsion hardware and propellant segment dominates the Asia-Pacific military reconnaissance satellite market, commanding approximately 79% of the total market share in 2024. This substantial market leadership is primarily driven by the increasing demand for advanced propulsion systems that enable military satellites to maneuver and maintain their orbits effectively. The segment's prominence is further reinforced by the growing emphasis on developing high-efficiency electric propulsion systems, advanced chemical propulsion systems, and hybrid propulsion technologies specifically tailored for military applications. Several countries in the region, particularly China, are actively investing in constellation projects that require sophisticated propulsion systems for orbit maintenance and collision avoidance. The segment's growth is also supported by the increasing focus on reducing space debris through better propulsion control and the rising demand for longer operational lifespans of military satellites.

Satellite Bus & Subsystems Segment in Asia-Pacific Military Satellite Market

The satellite bus and subsystems segment is experiencing remarkable growth, projected to expand at approximately 20% annually from 2024 to 2029. This accelerated growth is driven by the increasing sophistication of military satellite missions requiring advanced bus architectures and subsystems. The segment's expansion is supported by technological advancements in satellite bus design, enabling enhanced payload capacity, improved power management, and better thermal control systems. Military organizations across the Asia-Pacific region are increasingly demanding customized satellite buses that can accommodate multiple payloads while ensuring optimal performance in harsh space environments. The growth is further fueled by the development of standardized bus platforms that reduce manufacturing time and costs while maintaining high reliability standards. The segment is also benefiting from increased investments in research and development activities focused on improving satellite bus efficiency and durability.

Remaining Segments in Satellite Subsystem

The solar array and power hardware segment, along with the structures, harness, and mechanisms segment, play crucial roles in the overall military satellite ecosystem. Solar array and power hardware components are essential for ensuring continuous and reliable power supply to satellite operations, with manufacturers focusing on developing more efficient and durable solar cells and power management systems. The structures, harness, and mechanisms segment provides the fundamental physical framework and interconnection systems that ensure satellite integrity and functionality throughout its operational lifetime. Both segments are witnessing technological advancements in materials science and manufacturing processes, contributing to the development of lighter, more durable, and more efficient satellite components. These segments are particularly important in supporting the increasing demands for longer satellite lifespans and improved reliability in military applications.

Segment Analysis: Application

Earth Observation Segment in Asia-Pacific Military Satellite Market

Earth observation satellites have emerged as the dominant segment in the Asia-Pacific military surveillance satellite market, commanding approximately 82% of the market share in 2024. This significant market position is driven by the increasing demand for advanced surveillance and reconnaissance capabilities among military forces in the region. These satellites are extensively utilized for applications including territorial surveillance, urban planning, land confirmation, road network design, crop yield estimation, and disaster prevention and mitigation. The segment's dominance is further reinforced by major regional powers like China and India continuously expanding their earth observation satellite constellations for military purposes. These satellites are equipped with sophisticated imaging capabilities, including high-resolution optical sensors and synthetic aperture radar (SAR) systems, enabling them to provide detailed imagery and data crucial for military intelligence and strategic planning.

Navigation Segment in Asia-Pacific Military Satellite Market

The navigation segment is experiencing remarkable growth in the Asia-Pacific military satellite market, projected to expand at approximately 30% annually from 2024 to 2029. This exceptional growth is primarily driven by increasing investments in military navigation systems and the growing emphasis on precise positioning capabilities for defense operations. The segment's rapid expansion is supported by technological advancements in satellite navigation systems, particularly in ultra-high frequency (UHF), C-band, and Ku-band capabilities. Regional powers are actively developing and deploying their own satellite navigation constellations to reduce dependency on foreign systems and enhance their military capabilities. These navigation satellites are becoming increasingly crucial for providing secure, real-time communication links between land-based facilities, surface ships, submarines, and aircraft, contributing to enhanced military operational efficiency and strategic advantages.

Remaining Segments in Application

The remaining segments in the Asia-Pacific military satellite market include communication, space observation, and other specialized applications. The communication segment plays a vital role in providing secure and reliable communication channels for military operations, supporting everything from tactical communications to strategic command and control systems. Space observation satellites contribute to space situational awareness and monitoring of space-based assets, though their deployment is more limited compared to other segments. The 'Others' category encompasses various specialized applications such as signal intelligence gathering, technology demonstration, and educational purposes. These segments collectively contribute to the comprehensive space-based capabilities of military forces in the region, though their market impact is relatively smaller compared to the earth observation and navigation segments.

Asia-Pacific Military Satellite Market Geography Segment Analysis

Military Satellite Market in China

China dominates the Asia-Pacific military satellite market, commanding approximately 95% of the regional market share in 2024. The country's supremacy in the sector is primarily driven by the China Aerospace Science and Technology Corporation (CASC), which serves as the government's major supplier of Earth observation, communication, and reconnaissance satellites. China's robust space infrastructure and continued investment in military satellite technology have established it as a cornerstone of regional space capabilities. The country has demonstrated particular strength in developing and deploying various satellite types, from large geostationary platforms to smaller tactical satellites. China's commitment to enhancing its space capabilities is evident through its comprehensive satellite programs, including the Yaogan series for military reconnaissance and the BeiDou navigation system for strategic positioning capabilities. The nation's focus on self-reliance in space technology has resulted in the development of sophisticated manufacturing capabilities and launch facilities. Furthermore, China's integration of commercial space companies into its military satellite ecosystem has created a dynamic and innovative environment for technological advancement.

Military Satellite Market in South Korea

South Korea's military satellite market is projected to grow at an impressive rate of approximately 30% during 2024-2029, marking it as one of the most dynamic markets in the region. The country's aggressive push into space technology is driven by its comprehensive space development strategy and increasing defense modernization initiatives. South Korea has made significant strides in developing its indigenous satellite capabilities, particularly focusing on advanced military communication satellites and reconnaissance satellites. The nation's space program has evolved from being primarily dependent on international partnerships to developing sophisticated in-house capabilities. The country's investment in military satellite technology is part of a broader strategy to enhance its defense capabilities and achieve greater strategic autonomy. South Korea's emphasis on developing both geostationary and low-earth orbit satellites demonstrates its commitment to establishing a comprehensive space presence. The nation has also fostered a robust ecosystem of domestic companies and research institutions, creating a strong foundation for sustained growth in the military satellite sector. Additionally, South Korea's focus on developing dual-use technologies has enabled efficient resource utilization while maintaining military capabilities.

Military Satellite Market in India

India's military satellite market has emerged as a significant force in the Asia-Pacific region, driven by the Indian Space Research Organisation's (ISRO) comprehensive capabilities in satellite manufacturing and launch services. The country's approach to military satellite development combines indigenous innovation with strategic international partnerships, creating a robust ecosystem for space technology advancement. India's focus on developing dual-use satellites has enabled it to maximize resource utilization while maintaining strategic capabilities. The nation's satellite program encompasses a wide range of applications, from communication and navigation to Earth observation and electronic intelligence gathering. India's emphasis on developing sophisticated C4ISR systems has driven the demand for advanced military communication satellites. The country's strategic location and growing regional influence have necessitated the development of comprehensive space-based military capabilities. Furthermore, India's push towards self-reliance in defense technology has catalyzed domestic innovation in the military satellite sector, leading to the development of advanced indigenous platforms and technologies.

Military Satellite Market in Japan

Japan's military satellite market represents a sophisticated blend of technological innovation and strategic capability development. The country's approach to military satellite development is characterized by its focus on high-quality, reliable systems, particularly in the areas of reconnaissance and communication. Japan's satellite program benefits from the expertise of major industrial players like Mitsubishi Heavy Industries, which brings decades of experience in aerospace technology. The country's emphasis on developing dual-use technologies has enabled efficient resource utilization while maintaining robust military capabilities. Japan's satellite program is notable for its focus on advanced Earth observation and communication systems, which serve both civilian and military purposes. The nation's strategic partnership with international allies has enhanced its access to advanced technologies and expertise. Japan's commitment to space situational awareness has driven investments in sophisticated satellite tracking and monitoring capabilities. Additionally, the country's focus on developing resilient space infrastructure has resulted in the creation of robust satellite systems capable of operating in challenging conditions.

Military Satellite Market in Other Countries

The military satellite by country market in other Asia-Pacific countries, including Australia, Singapore, New Zealand, and emerging Southeast Asian nations, represents a diverse landscape of capabilities and ambitions. These countries are increasingly recognizing the strategic importance of space-based assets and are developing their satellite capabilities accordingly. While some nations focus on developing indigenous capabilities, others opt for international partnerships to access advanced satellite technologies. The regulatory frameworks in these countries are evolving to support the growth of their space sectors while ensuring compliance with international standards. These nations are particularly interested in developing capabilities in areas such as maritime surveillance, border security, and disaster monitoring. The emergence of commercial space companies in these markets is creating new opportunities for innovation and growth. Additionally, regional cooperation initiatives are enabling smaller nations to participate in space activities through shared resources and expertise. The increasing accessibility of small satellite technologies has enabled these countries to develop targeted capabilities aligned with their specific defense requirements.

Competitive Landscape

Top Companies in Asia-Pacific Military Satellite Market

The competitive landscape is dominated by major aerospace and defense companies with established capabilities in military satellite manufacturing and space technologies. Companies are focusing on developing advanced satellite systems with enhanced capabilities in Earth observation, communication, and reconnaissance applications. Strategic partnerships and collaborations with government agencies and military organizations have become crucial for market expansion. Product innovation efforts are centered around developing smaller, more efficient satellites with improved propulsion systems and payload capabilities. Companies are also emphasizing operational agility through automated manufacturing processes and integrated supply chains. The industry has witnessed increased investment in research and development of new satellite technologies, particularly in areas such as miniaturization, artificial intelligence integration, and enhanced communication systems.

State-Owned Enterprises Lead Market Development Trends

The Asia-Pacific defense satellite market is characterized by a strong presence of state-owned enterprises and government-backed organizations, particularly in countries like China and India. These organizations benefit from substantial government support, established infrastructure, and preferential access to military contracts. The market structure shows high consolidation among a few major players, with China Aerospace Science and Technology Corporation (CASC) holding a dominant position. The industry has limited private sector participation due to high entry barriers, complex regulatory requirements, and the strategic nature of military satellite technology.

The market demonstrates a trend toward vertical integration, with major players maintaining control over various aspects of satellite manufacturing, launch services, and ground operations. Merger and acquisition activities are limited due to government restrictions and national security considerations. Instead, companies focus on forming strategic alliances and joint ventures to enhance technological capabilities and expand market reach. Local players in various countries are gradually building capabilities through technology transfer agreements and collaborative projects with established international players.

Innovation and Collaboration Drive Future Growth

Success in the military satellite market increasingly depends on the ability to offer comprehensive solutions that integrate multiple capabilities, from Earth observation to secure communications. Companies need to focus on developing cost-effective manufacturing processes while maintaining high reliability and performance standards. Building strong relationships with government agencies and military organizations remains crucial, as does the ability to adapt to evolving security requirements and technological standards. Investments in research and development, particularly in areas such as artificial intelligence, quantum communications, and advanced materials, will be essential for maintaining a competitive advantage.

Market contenders can gain ground by focusing on specialized niche applications or developing innovative solutions for specific military requirements. The increasing emphasis on space-based military capabilities across Asia-Pacific countries presents opportunities for new entrants with unique technological offerings. However, companies must navigate complex regulatory environments and security requirements while building credibility with military customers. Success will also depend on the ability to establish reliable supply chains and maintain high-quality standards while managing costs effectively. The risk of substitution remains low due to the critical nature of satellite technology in modern military operations, but companies must continue to innovate to maintain their market positions.

Asia-Pacific Military Satellite Industry Leaders

Airbus SE

China Aerospace Science and Technology Corporation (CASC)

Innovative Solutions in Space BV

Mitsubishi Heavy Industries

Thales

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2023: Mitsubishi Electric was given a contract by JAXA, the Ministry of Environment, and the National Institute of Environmental Studies, Japan, to build the Greenhouse Gases Observing Satellite-2 (GOSAT-2). The satellite was launched from the Tanegashima Space Center in southern Japan.

- September 2023: The Royal Thai Air Force awarded Innovative Solutions In Space a contract to build its next satellite mission based on an ISISpace 6U CubeSat.

- February 2023: Mitsubishi Electric was given a contract by Cabinet Satellite Intelligence Center (CSIC) to build a reconnaissance satellite named IGS Optical 7. The satellite was launched from the Tanegashima Space Center in southern Japan.

Asia-Pacific Military Satellite Market Report Scope

10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. GEO, LEO, MEO are covered as segments by Orbit Class. Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms are covered as segments by Satellite Subsystem. Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application.| 10-100kg |

| 100-500kg |

| 500-1000kg |

| Below 10 Kg |

| above 1000kg |

| GEO |

| LEO |

| MEO |

| Propulsion Hardware and Propellant |

| Satellite Bus & Subsystems |

| Solar Array & Power Hardware |

| Structures, Harness & Mechanisms |

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Satellite Mass | 10-100kg |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg | |

| Orbit Class | GEO |

| LEO | |

| MEO | |

| Satellite Subsystem | Propulsion Hardware and Propellant |

| Satellite Bus & Subsystems | |

| Solar Array & Power Hardware | |

| Structures, Harness & Mechanisms | |

| Application | Communication |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- Category - North America Space Propulsion Market

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.