Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

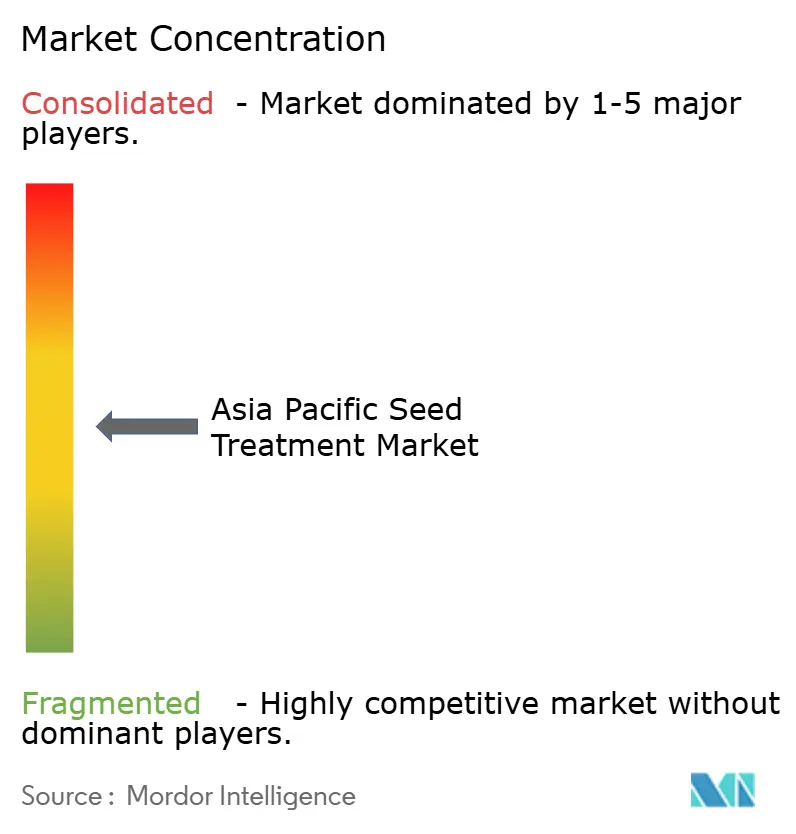

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Seed Treatment Market Analysis by Mordor Intelligence

The Asia Pacific seed treatment market size was valued at USD 1.64 billion in 2025 and estimated to grow from USD 1.71 billion in 2026 to reach USD 2.11 billion by 2031, at a CAGR of 4.26% during the forecast period (2026-2031). The acceleration is anchored in government mandates that push comprehensive seed coverage, rising resistance among major pest complexes, and the steady intake of combination formulations that couple insecticidal and fungicidal modes of action. Low-dose systemic coatings, utilizing active ingredients such as thiamethoxam and clothianidin at 30-50% reduced rates compared to foliar applications, provide season-long protection while reducing total pesticide load per hectare by up to 60%. Strategic alliances among multinational manufacturers and local formulators advance the technology pipeline, while digital analytics embedded into crop protection prescriptions create upselling potential.

Key Report Takeaways

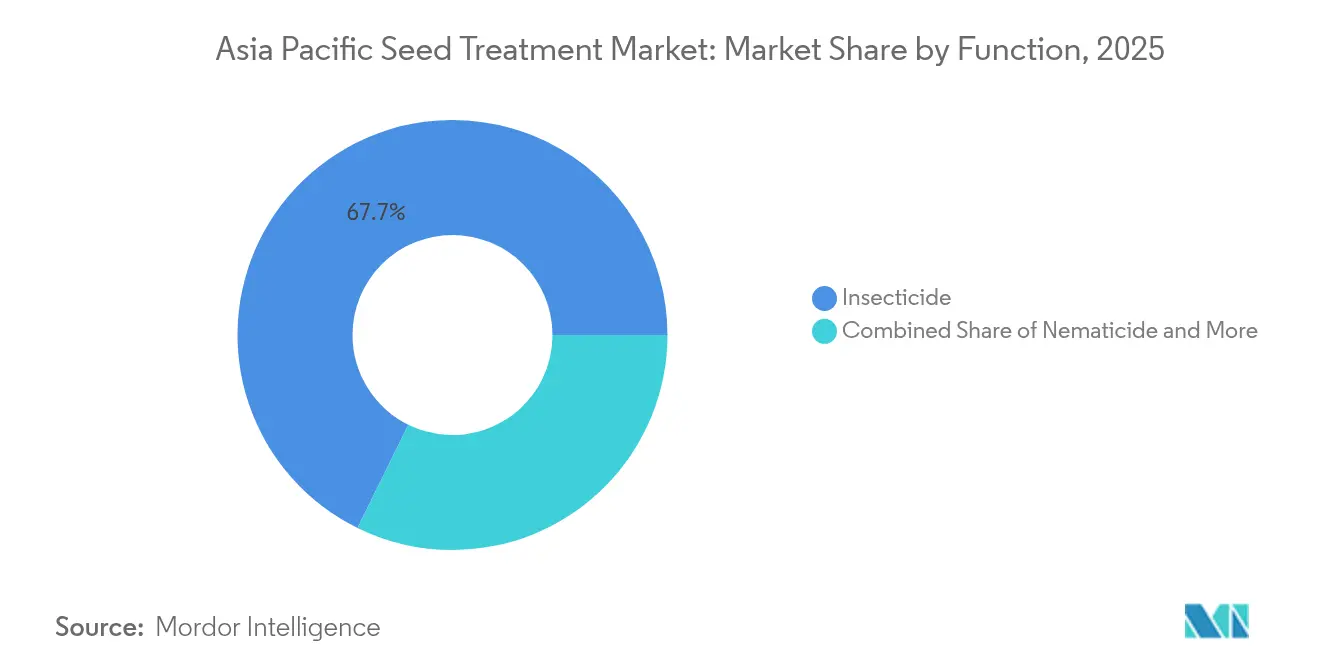

- By function, insecticide treatments led with 67.72% Asia Pacific seed treatment market share in 2025, and they are advancing at a 4.37% CAGR through 2031.

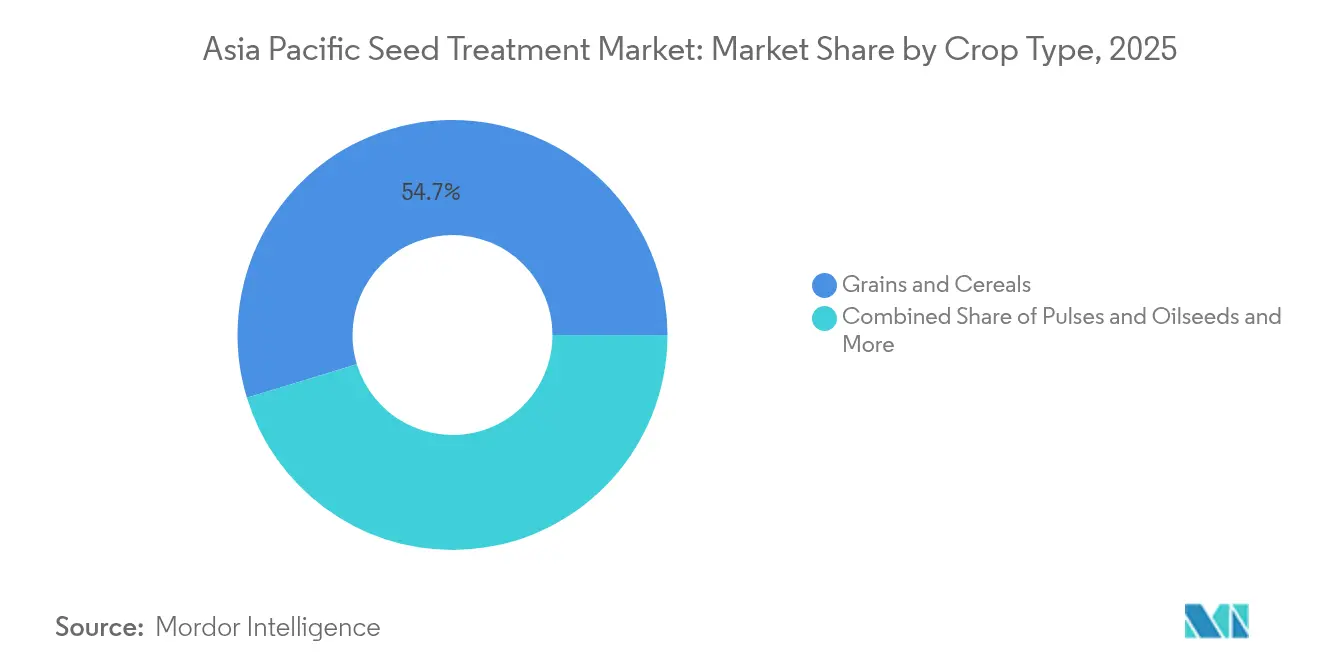

- By crop type, grains and cereals accounted for 54.72% of the Asia Pacific seed treatment market size in 2025, while fruits and vegetables are forecast to expand at a 4.38% CAGR in the same period.

- By geography, China commanded 29.05% revenue share of the Asia Pacific seed treatment market in 2025, while recording the fastest regional CAGR at 5.21% to 2031.

- The five largest suppliers, Syngenta Group, BASF, UPL, Corteva Agriscience, and Bayer, held 56.35% in the Asia Pacific seed treatment market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying pest resistance pressures on high-value horticulture | +0.8% | Southeast Asia and India | Medium term (2-4 years) |

| Government push for 100 % seed-treatment coverage in India's Kharif season | +0.6% | India and South Asia | Short term (≤ 2 years) |

| Rise of combination insecticide-fungicide formulations tailored to tropical climates | +0.7% | Thailand, Vietnam, and Indonesia | Medium term (2-4 years) |

| Rapid adoption of low-dose systemic insecticide seed coatings to manage pyrethroid-resistant pests | +0.9% | Asia-Pacific-wide | Medium term (2-4 years) |

| Precision planting equipment adoption enabling higher-margin seed-applied inputs | +0.5% | China and Australia | Long term (≥ 4 years) |

| Corporate pacts to embed digital analytics in seed-care prescriptions | +0.4% | Japan, Australia, and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying pest resistance pressures on high-value horticulture

Escalating resistance among key insects in tomato, pepper, and melon crops forces growers to demand multi-mode seed protection packages. Studies in Thailand and Vietnam record a 40% rise in pyrethroid resistance since 2022. Combination seed treatments that merge synthetic actives gain favor, cutting early-season loss by 18% and supporting premium crop pricing in export markets. Government extension services now bundle resistance-management guidelines with subsidized seed kits. Manufacturers capitalize by fast-tracking novel chemistries into the Asia Pacific seed treatment market, thereby strengthening brand differentiation.

Government push for 100 % seed-treatment coverage in India's Kharif season

India’s agriculture ministry earmarked INR 192 billion (USD 2.3 billion) to convert all subsidized Kharif seed supplies to treated status by 2026.[1]Source: Ministry of Agriculture and Farmers Welfare, “Seed Treatment Policy Initiative,” agricoop.nic.in The program spans rice, cotton, and sugarcane, representing 65% of India’s Kharif acreage. Pilot districts in Punjab delivered 23% yield gains and 31% pest-loss reductions. Mandatory seed certification now embeds treatment compliance, elevating baseline demand across the Asia Pacific seed treatment market. Implementation hurdles, skill gaps among rural agents, and inconsistent cold-chain links spur private firms to co-invest in last-mile logistics.

Rise of combination insecticide-fungicide formulations tailored to tropical climates

High humidity and monsoon volatility accelerate pathogen and pest cycles. Syngenta invested significantly in Singapore to tailor dual-active films that remain stable under high temperatures. Similar investments by BASF in Malaysia have shortened registration timelines under ASEAN mutual recognition pacts, thereby boosting the adoption of combination products in Southeast Asia. Growers appreciate the simplified one-pass coating and notable cost savings per hectare, cementing the Asia Pacific seed treatment market’s tilt toward premium tropical formulations.

Rapid Adoption of Low-Dose Systemic Insecticide Seed Coatings to Manage Pyrethroid-Resistant Pests

The proliferation of pyrethroid-resistant pest populations across the Asia Pacific is driving accelerated adoption of low-dose systemic insecticide seed coatings, which deliver targeted protection while minimizing environmental exposure and preserving beneficial insect populations. This technology shift addresses the critical challenge of pyrethroid resistance in key pests such as bollworm in cotton and aphids in vegetable crops, where traditional foliar applications have lost efficacy due to widespread resistance development. Low-dose systemic coatings, utilizing active ingredients such as thiamethoxam and clothianidin at 30-50% reduced rates compared to foliar applications, provide season-long protection while reducing total pesticide load per hectare by up to 60%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented smallholder base restricting per-hectare spend | -0.9% | India and Southeast Asia | Short term (≤ 2 years) |

| Regulatory withdrawal of neonicotinoids in Japan and Australia | -0.6% | Japan and Australia | Medium term (2-4 years) |

| Cold-chain gaps shortening microbial coating shelf-life | -0.4% | Tropical rural zones | Medium term (2-4 years) |

| Volatile active-ingredient prices for cypermethrin and abamectin | -0.7% | Region-wide price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented smallholder base limiting per-hectare spend

Average farm sizes remain under 2 hectares across much of Asia, capping disposable income for seed treatments at under 3% of total input cost.[2]Source: Food and Agriculture Organization, “Asia Pacific Smallholder Farm Structure 2024,” fao.org Cooperative purchasing schemes and microfinance lines address the affordability gap, but administrative frictions and repayment risk slow penetration. Firms pilot pay-at-harvest models, yet scale remains elusive. Consequently, the Asia Pacific seed treatment market experiences uneven uptake, particularly in remote districts with limited market access.

Regulatory withdrawal of selected neonicotinoids in Japan and Australia

Japan’s phased ban on clothianidin and thiamethoxam seed uses, coupled with Australia’s ongoing review, forces reformulation across 17 flagship brands.[3]Source: Australian Pesticides and Veterinary Medicines Authority, “Neonicotinoid Review Update,” apvma.gov.au Replacement chemistries cost up to 32% more and require additional validation trials, eroding short-term margins. Distributors brace for supply gaps in early 2026. These changes temper near-term growth for the Asia Pacific seed treatment market until compliant alternatives scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides consolidate leadership through diversified chemistry

Insecticide treatments commanded 67.72% market share in 2025 while maintaining the fastest growth trajectory at 4.37% CAGR through 2031, reflecting both the persistent pest pressures across Asia Pacific's diverse agricultural systems and the segment's rapid technological evolution in response to resistance challenges. The segment's dominance is increasingly driven by innovation in low-dose systemic coatings that address widespread pyrethroid resistance, with manufacturers developing precision application technologies that reduce active ingredient usage by 30-50% while maintaining season-long efficacy. This technological shift is particularly pronounced in cotton and vegetable production systems, where traditional foliar applications have lost effectiveness, creating premium market opportunities for companies that can deliver resistance management solutions through seed-applied technologies.

Fungicide treatments capture the second-largest functional segment, driven by monsoon-related disease pressures in rice production systems and the increasing prevalence of fungal pathogens in high-value horticultural crops across Southeast Asia's humid tropical climates. The fungicide segment benefits from combination formulations that integrate multiple modes of action, addressing both early-season soil-borne diseases and emerging foliar pathogens that threaten crop establishment and yield potential. Nematicide applications represent a specialized but growing segment, particularly in high-value crops such as tomatoes and ornamental plants where soil-borne nematodes cause significant economic losses, with market expansion driven by improved application technologies and enhanced active ingredient stability in tropical soil conditions Applied Soil . Regulatory compliance frameworks, particularly ISO 14001 environmental management standards and national pesticide registration requirements, are influencing product development across all functional segments toward lower-impact formulations that maintain efficacy while reducing environmental footprint and meeting export market requirements.

By Crop Type: Grains dominate volume while fruits register the quickest uptick

Grains and cereals dominated with 54.72% market share in 2025, reflecting the region's rice-wheat production systems that require comprehensive seed protection against diverse pest complexes, while fruits and vegetables emerged as the fastest-growing segment at 4.38% CAGR, driven by export market expansion and premium quality requirements. The grains segment benefits from government support programs and mechanized application systems that enable cost-effective seed treatment deployment across large acreages. Commercial crops, including cotton and sugarcane, maintain steady growth supported by integrated pest management adoption, while pulses and oilseeds represent emerging opportunities as dietary preferences shift toward protein-rich crops.

Historical analysis reveals grains and cereals maintained 6.2% CAGR from 2020-2024, compared to the forecasted 3.96% growth through 2031, indicating market maturation in traditional crops while fruits and vegetables accelerate from 3.8% historical growth to 4.38% projected expansion. The fruits and vegetables segment's acceleration reflects increasing consumer quality expectations and export market compliance requirements, with seed treatments becoming essential for meeting international phytosanitary standards. Turf and ornamental applications, while smaller in volume, command premium pricing due to aesthetic quality requirements and specialized formulation needs. Regulatory frameworks such as GLOBALG.A.P. certification are driving seed treatment adoption in export-oriented fruit and vegetable production, creating sustainable growth opportunities for specialized formulations.

Geography Analysis

China captured 29.05% market share in 2025 while posting the highest growth rate of 5.21% CAGR through 2031, reflecting the country's agricultural modernization initiatives and scale advantages in seed treatment deployment across its 165 million hectares of cultivated land. China's market leadership reflects both scale and sophistication, with the country's agricultural modernization program driving adoption of precision seed treatment technologies and digital application monitoring systems across large-scale farming operations. The government's commitment to food security and sustainable agriculture has resulted in increased investment in seed treatment infrastructure, with state-owned enterprises partnering with international companies to develop locally-adapted formulations. Regional growth patterns show accelerating adoption in northeastern provinces where mechanized farming enables efficient seed treatment deployment, while southern regions focus on specialty crop applications that command premium pricing.

India's market expansion is driven by the convergence of government policy support and increasing farmer awareness of seed treatment benefits, with the Pradhan Mantri Fasal Bima Yojana crop insurance program incentivizing comprehensive crop protection practices, including seed treatments. The country's diverse agro-climatic zones create opportunities for specialized formulations, from rice-focused treatments in eastern states to cotton and sugarcane applications in western regions. Historical growth of 3.9% CAGR (2020-2024) is accelerating to projected 4.59% through 2031, supported by increasing mechanization and corporate farming initiatives that enable more sophisticated seed treatment protocols.

Southeast Asian markets demonstrate the highest growth potential, with Thailand, Vietnam, and Indonesia leading regional expansion through export-oriented agriculture and technology adoption initiatives. Thailand's Board of Investment has approved USD 1.2 billion in agricultural technology investments, including seed treatment facilities, while Vietnam's agricultural modernization program targets 40% increase in seed treatment coverage by 2027. Australia and Japan represent mature markets characterized by premium product adoption and stringent regulatory compliance, with both countries implementing advanced resistance management protocols that drive demand for innovative seed treatment solutions. Regulatory frameworks such as Australia's APVMA registration system and Japan's Food Safety Commission standards ensure high product quality while creating barriers to entry that benefit established players with comprehensive regulatory expertise.

Competitive Landscape

The Asia Pacific seed treatment market exhibits moderate concentration with the top five players controlling approximately 57% market share, creating a competitive environment that balances established multinational presence with opportunities for regional specialists. Market dynamics favor companies with comprehensive product portfolios and strong regulatory capabilities, as the complexity of navigating diverse national registration requirements creates significant barriers to entry for smaller players.

Strategic differentiation increasingly centers on chemical solutions and precision application technologies, with leading companies investing heavily in R&D partnerships and local manufacturing capabilities to serve diverse regional needs. Competition intensity has escalated through strategic partnerships and technology licensing agreements, exemplified by Syngenta's collaboration with Intrinsyx Bio for endophyte-based formulations and BASF's alliance with Chinese partners for localized product development.

White-space opportunities exist in chemical seed treatments and precision application systems, where established players face competition from specialized biotechnology companies and agricultural technology startups that can move quickly to address emerging market needs. Technology deployment for competitive advantage includes digital application monitoring, predictive analytics for pest pressure forecasting, and customized formulation development that addresses specific regional pest complexes and regulatory requirements. Regulatory compliance frameworks, particularly adherence to ISO 9001 quality management standards and national pesticide registration requirements, serve as both competitive differentiators and market entry barriers that consolidate market share among well-resourced players.

Asia Pacific Seed Treatment Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Syngenta Group

UPL Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: UPL, through Advanta Seeds International Mauritius, acquired Wuhan Advanta Seeds Company Limited in China. This strategic move marks UPL’s entry into the Chinese seed market and strengthens its presence in Asia. The move enhances UPL’s capabilities in seed treatment and distribution, supporting its growth in the Asia-Pacific seed market.

- May 2025: BASF’s agriculture unit plans to expand into Asia and the global seed market as it prepares for a public listing. The move aims to tap into high-growth regions and strengthen its position in crop protection and seed treatment technologies.

- March 2025: Syngenta Australia introduced VICTRATO, a seed treatment for wheat and barley designed to combat Fusarium crown rot, a disease responsible for substantial yield losses. Utilizing TYMIRIUM technology, it safeguards roots and shoots from early-stage infections. Following more than 300 trials conducted across Australia, VICTRATO provides growers with enhanced crop health, improved grain quality, and greater assurance when planting in high-risk areas.

Asia Pacific Seed Treatment Market Report Scope

Fungicide, Insecticide, Nematicide are covered as segments by Function. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type. Australia, China, India, Indonesia, Japan, Myanmar, Pakistan, Philippines, Thailand, Vietnam are covered as segments by Country.Function

| Fungicide |

| Insecticide |

| Nematicide |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Myanmar |

| Pakistan |

| Philippines |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Function | Fungicide |

| Insecticide | |

| Nematicide | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Myanmar | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Market Definition

- Function - Insecticides, fungicides, and nematicides are the crop protection chemicals used to treat seeds or seedlings.

- Application Mode - Seed treatment is a method of applying crop protection chemicals to the seeds before sowing or the seedlings before transplanting to the main field.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms