Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

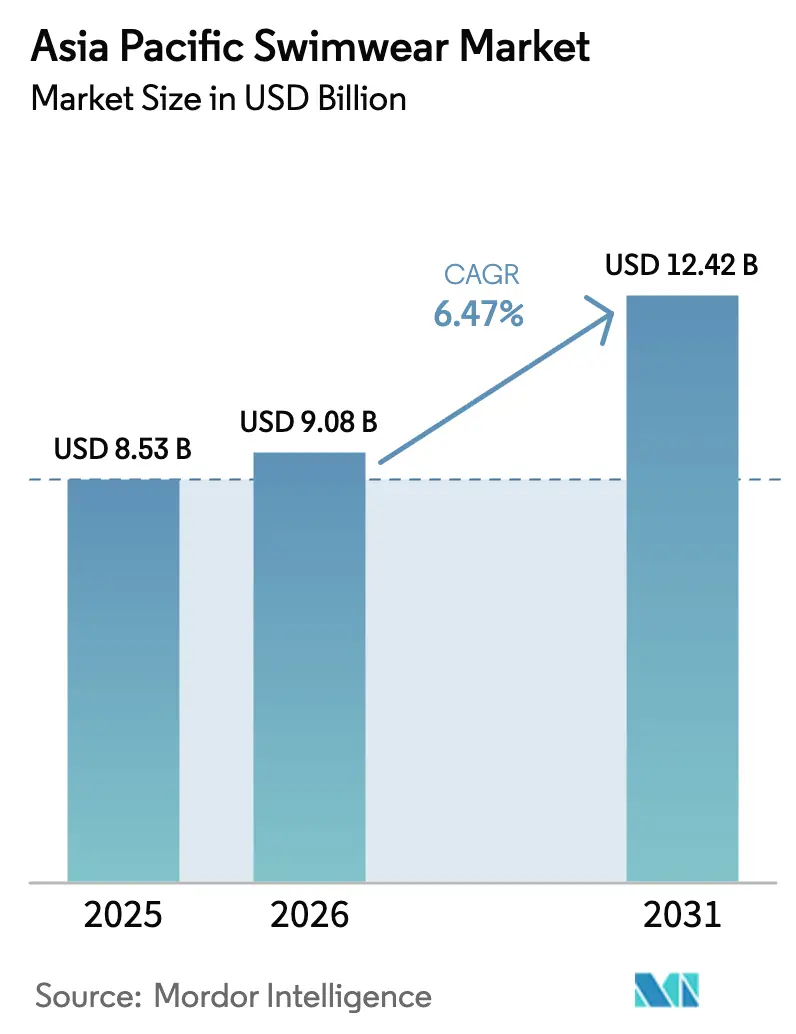

| Base Year Market Size (2025) | USD 8.53 Billion |

| Market Size (2026) | USD 9.08 Billion |

| Market Size (2031) | USD 12.42 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Swimwear Market Analysis by Mordor Intelligence

Asia-Pacific swimwear market size in 2026 is estimated at USD 9.08 billion, growing from 2025 value of USD 8.53 billion with 2031 projections showing USD 12.42 billion, growing at 6.47% CAGR over 2026-2031. This growth is driven by heightened health awareness, a resurgence in regional tourism, and rapid fabric innovations, shifting consumer desires from mere coverage to performance-oriented gear. For example, as reported by Thailand's Ministry of Digital Economy and Society in November 2024, Phuket welcomed around 124,500 visitors from Russia, while over 55,000 hailed from India. Other notable arrivals came from China, Germany, and Australia[1]Source: Ministry of Digital Economy and Society (Thailand), "Inbound All Borders Monthly Overview Statistic Overall, 2024", travellink.go.th. Premium brands are tapping into Korean pop culture, forging partnerships with athletes, and employing digital storytelling to engage younger consumers. These shoppers increasingly view swimwear as essential activewear, not just seasonal attire. In January 2025, the Queensland government invested USD 108 million in the Swan Active Ellenbrook project, a world-class aquatic center. This expansion boosts pool capacity and drives demand for chlorine-resistant suits. The rise of online retail, especially through platforms like TikTok Shop, is reshaping the sales landscape, turning influencer content into direct sales and challenging the long-standing dominance of hypermarkets. Furthermore, as major export markets emphasize sustainability and consumers lean towards eco-friendly choices, suppliers are pivoting to recycled fibers and biodegradable polyamides, even at premium price points.

Key Report Takeaways

- By product type, women’s swimwear led with 42.02% revenue share in 2025, and accessories are projected to advance at a 7.57% CAGR through 2031.

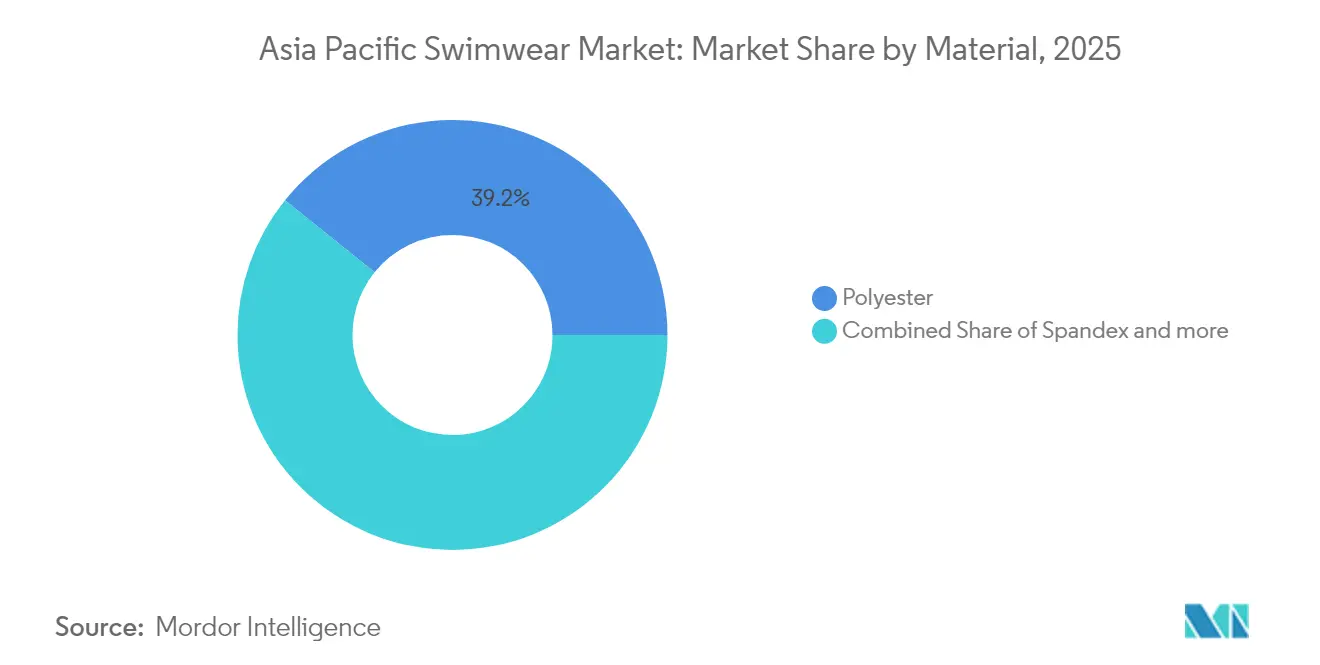

- By material, polyester accounted for 39.22% of the Asia-Pacific swimwear market share in 2025, while spandex is expected to expand at an 7.97% CAGR to 2031.

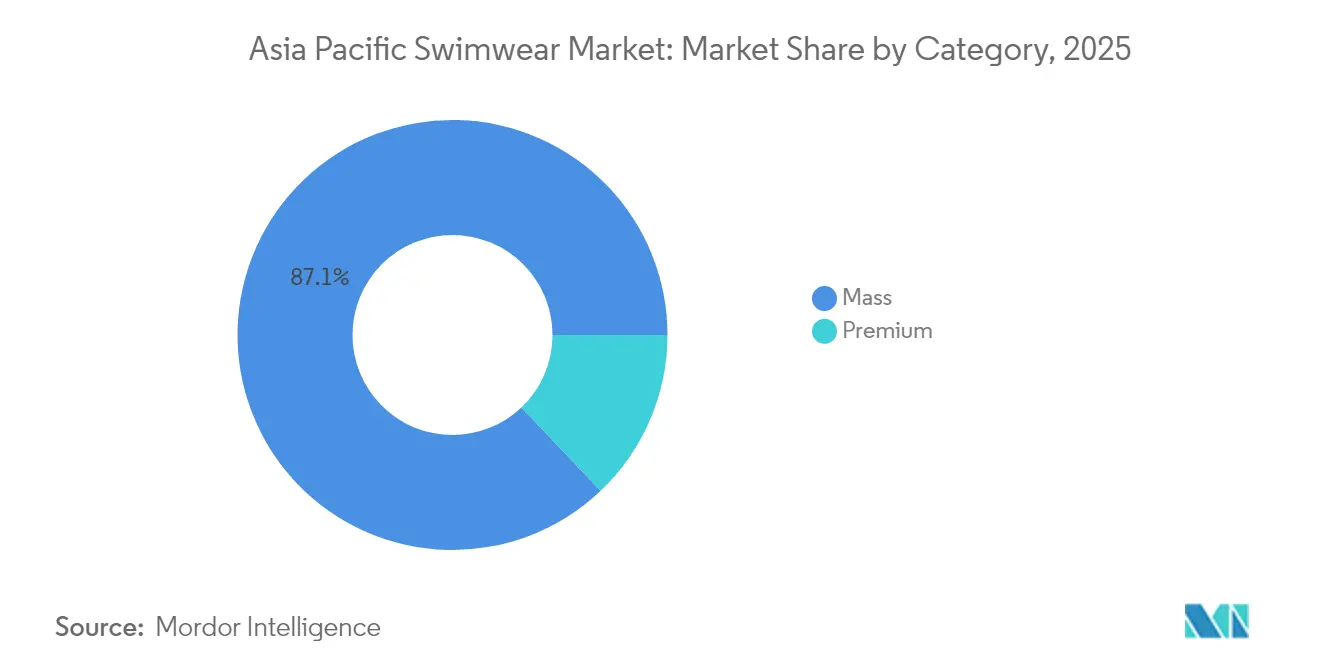

- By category, the mass segment captured 87.10% of the Asia-Pacific swimwear market size in 2025, while premium products are projected to grow at a 7.72% CAGR through 2031.

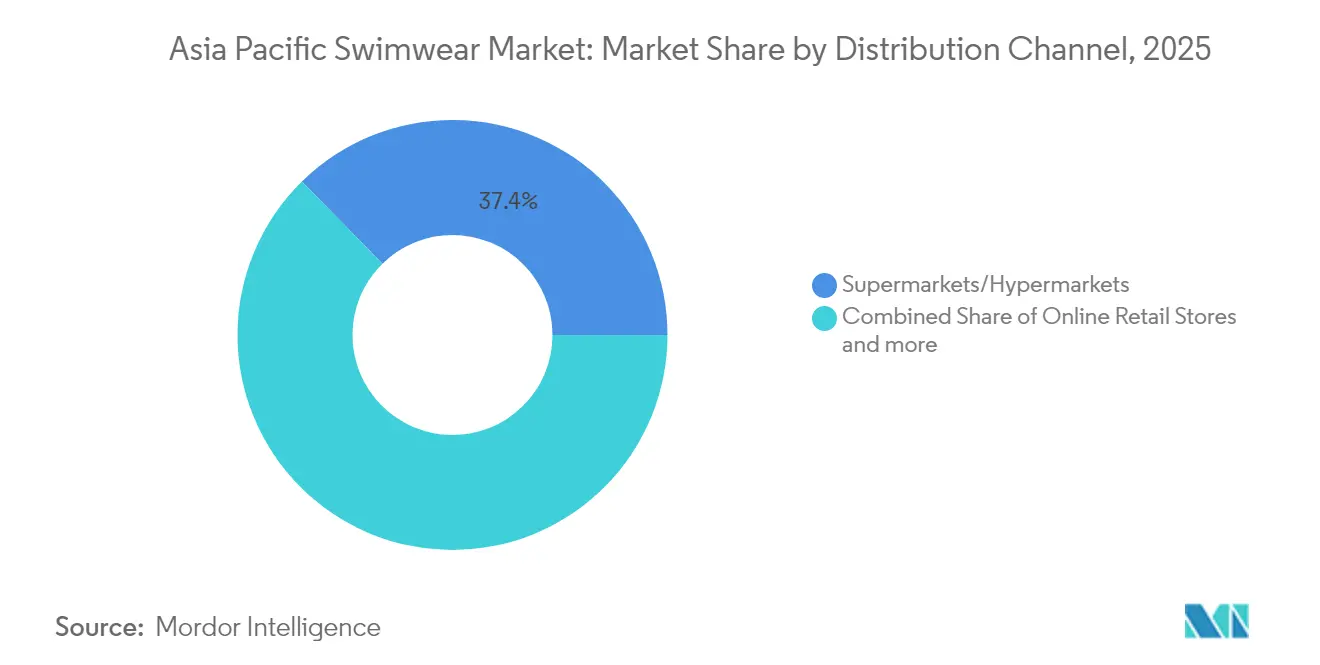

- By distribution channel, supermarkets and hypermarkets held a 37.35% share in 2025, and online retail is forecast to grow at an 8.55% CAGR up to 2031.

- By geography, China commanded a 32.16% share in 2025, and India recorded the fastest growth rate of 7.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Swimwear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and fitness trends | +1.1% | Global, with the strongest impact in China, Singapore, and South Korea | Medium term (2-4 years) |

| Growth of tourism and leisure activities | +0.8% | Thailand, Singapore, Australia, Indonesia | Short term (≤ 2 years) |

| Technological advancements in fabric | +1.2% | Global, led by Japan and South Korea's innovation hubs | Long term (≥ 4 years) |

| Rise of athleisure and multifunctional swimwear | +0.9% | China, Australia, Singapore | Medium term (2-4 years) |

| Expansion of aquatic facilities | +0.7% | Australia, Singapore, China | Long term (≥ 4 years) |

| Increased focus on sustainability | +0.6% | Australia, Japan, South Korea, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Fitness Trends

Across the region, government-led wellness initiatives are fueling a growing demand for performance-oriented swimwear, moving beyond mere recreational use. In 2025, Singapore's Health Promotion Board bolstered workplace wellness programs, co-funding up to SGD 65 per session for physical activities, contingent on a minimum of 15 participants. This move directly champions the adoption of a corporate fitness culture. Such institutional backing aligns with a broader behavioral shift: Singapore's populace is increasingly engaging in regular sports, underscoring a momentum towards active living. Data from the Singapore Department of Statistics reveal a notable increase in sports bookings: in 2023, football field reservations reached approximately 34,550, while tennis courts saw bookings of around 205,700[2].Source: Singapore Department of Statistics, "Singapore Department of Statistics", tablebuilder.singstat.gov.sg This trend isn't limited to individual pursuits; community-driven activities are on the rise. China's vibrant marathon scene is not only spotlighting the demand for moisture-wicking fabrics but also setting new benchmarks for swimwear materials. In China, premium sportswear brands are experiencing growth rates that surpass those of general apparel, underscoring a consumer trend: a willingness to invest in specialized, activity-centric apparel. This discerning, health-focused consumer demographic is reshaping perceptions of swimwear, viewing it increasingly as essential performance gear. As a result, there's a heightened demand for advanced features like chlorine resistance, UV protection, and quick-dry technologies.

Growth of Tourism and Leisure Activities

As the Asia-Pacific's tourism rebounds, key destination markets see a surge in swimwear demand, bolstered by infrastructure investments that hint at sustained growth. Thailand, aiming for 35.99 million foreign tourist arrivals by 2025, nearly back to pre-pandemic levels, is introducing a THB 300 (USD 8.20) tourism fee. This fee aims to bolster attraction development and enhance safety infrastructure. Meanwhile, the 2025 World Aquatics Championships in Singapore underscore the lasting impact of major sporting events on tourism. With 40,000 international visitors projected, the event is expected to generate an additional SGD 60 million in tourism receipts, according to the Ministry of Culture, Community and Youth[3]Source: Ministry of Culture, Community and Youth, "Temporary facility, tourism receipts and sponsorships for the World Aquatics Championships 2025", mccy.gov.sg. The championships necessitated the construction of temporary facilities, boasting a water capacity of 2.06 million gallons. This not only underscores the event's scale but also highlights the dual benefit: an immediate uptick in swimwear demand and the long-term utility of such facilities. As regional tourism trends shift towards experiential and wellness-centric travel, swimwear purchases are increasingly seen as integral to the travel experience, rather than mere pre-trip shopping. This evolution paves the way for premium, multifunctional swimwear that seamlessly blends performance with lifestyle appeal.

Technological Advancements in Fabric

Breakthrough technologies are simultaneously enhancing durability, sustainability, and functionality in swimwear, setting new performance standards. In April 2025, Speedo unveiled a biodegradable apparel line, featuring a Carbon Neutral knit polyamide that decomposes in sanitary landfills within three years. This line also boasts the Stretch Wet 80+ technology, ensuring UV 80+ protection even when the fabric is stretched and wet. LYCRA's lastingFIT technology showcases fiber-level innovation, allowing swimwear to last up to ten times longer than those with unprotected spandex, thanks to enhanced resistance to chlorine, UV rays, and chemicals. In June 2023, Arena partnered with The Woolmark Company to launch the Tech Wool capsule collection of swimsuits. These suits, crafted from a blend of Merino wool and technological fibers, are ultralight, breathable, and biodegradable, yet resistant to saltwater and chlorine. These advancements cater to consumers seeking versatile performance while upholding sustainability standards. The blend of enhanced performance and environmental stewardship is giving rise to new market categories, where technical excellence commands a premium price, particularly in environmentally conscious markets such as Australia and Japan.

Rise of Athleisure and Multifunctional Swimwear

As consumers increasingly seek lifestyle-integrated apparel, swimwear is evolving from its traditional role as a poolside accessory to become versatile garments suitable for various activities. Lululemon is strategically expanding across Europe, the Middle East, Africa, Asia-Pacific, and Mainland China regions, focusing on direct-to-consumer investments and brand activations. Their goal is to tap into the rising demand for apparel that seamlessly transitions between different environments. This shift highlights a broader consumer trend favoring multifunctional products, which command higher price points due to their versatility, rather than being optimized for single-use applications. Arena, traditionally a swimwear brand, is broadening its horizons. Their foray into beachwear, outerwear, bags, and mini-dresses highlights a strategy to engage consumers year-round. The growing influence of athleisure is paving the way for swimwear designs that blend fashion-forward aesthetics with technical performance. This fusion resonates especially with younger consumers, who see activewear as an extension of their identity. Platforms like TikTok Shop, which raked in a whopping USD 15 billion GMV through influencer-led content, are emerging as prime venues. They spotlight multifunctional swimwear in diverse lifestyle scenarios, moving beyond just athletic contexts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -0.9% | China, India, Vietnam, Thailand | Short term (≤ 2 years) |

| Proliferation of counterfeit products | -0.5% | Southeast Asia, China | Medium term (2-4 years) |

| Environmental concerns and sustainability costs | -0.4% | Global, strongest in Australia, Japan, South Korea | Long term (≥ 4 years) |

| Intense market competition and fragmentation | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility

Price instability in spandex and polyester is squeezing margins and complicating inventory management, hampering market growth due to supply chain disruptions and limited ability to pass on costs. China's spandex sector is grappling with a persistent oversupply, despite annual capacity expansion. While demand growth is pushing prices for the mainstream 40D spandex, this oversupply leads to instability. Producers are contemplating production cuts to better manage inventories. Meanwhile, feedstock costs for 1,4-Butanediol (BDO) and Polytetramethylene Ether Glycol (PTMEG), although at multi-year lows, are under downward pressure, raising concerns about potential supply disruptions. In the polyester filament yarn market, a notable shift is observed: inventory levels have plummeted from 20 days to just one week, and operating rates are exceeding 90%. This suggests a tighter balance between supply and demand, yet it's a balance that could easily tip with any changes in demand. Given the ongoing challenges of overcapacity, the spandex market's recovery appears sluggish. This unpredictability in input costs poses challenges for swimwear manufacturers, who depend on a consistent elastane content for optimal performance. As raw material prices fluctuate, manufacturers face a crossroads: either compress margins by maintaining fixed retail prices or risk demand destruction through price hikes. Both choices limit the potential for market expansion.

Proliferation of Counterfeit Products

Cross-border counterfeit trade networks are exploiting e-commerce platforms and weak enforcement mechanisms, flooding Asia-Pacific markets with low-quality imitations. These imitations not only undermine brand value but also jeopardize consumer safety. China stands out as the primary source of global counterfeit goods, accounting for roughly 75% of the total. Notably, counterfeit exports from China to Southeast Asia are estimated at a staggering USD 35 billion. This trade is bolstered by sophisticated supply chains and infrastructure, making it challenging to replicate elsewhere. In April 2024, a police raid in Shanghai targeted the cross-border platform Pandabuy. Authorities uncovered a vast network spanning 20 cities in China, employing 2,200 individuals. This operation boasted over 100,000 square meters of warehouse space and had processed more than 50 million counterfeit items since 2021. In 2023 alone, the network generated revenues of RMB 39.6 billion, as reported by Managing Intellectual Property. Southeast Asian e-commerce platforms are increasingly becoming conduits for cross-border sellers, leveraging Chinese fulfillment centers. Meanwhile, local drop-shippers are sourcing directly from China. This dynamic complicates detection and enforcement efforts. The rise of counterfeit swimwear in the market not only sows confusion but also diminishes legitimate brand sales. Furthermore, these counterfeit products pose safety risks, as they may be made from substandard materials lacking essential features like UV protection or chlorine resistance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Women's Dominance Drives Accessories Innovation

In 2025, women's swimwear holds a dominant 42.02% market share in the Asia-Pacific region, driven by demographic purchasing habits and higher average selling prices resulting from product complexity. The accessories segment is projected to grow at a 7.57% CAGR through 2031, driven by multifunctional innovations such as UV-protective cover-ups, waterproof fitness trackers, and customizable modular swimwear. Men's swimwear continues to grow steadily, focusing on performance-driven designs for competitive swimming and water sports, while benefiting from the athleisure trend that blends swim trunks with casual shorts. Kids' swimwear experiences consistent growth, driven by demographic trends and an increase in swimming program participation, with safety features such as built-in flotation and bright, visibility-enhancing colors becoming standard.

Arena's lifestyle expansion showcases how performance brands are capitalizing on accessories growth by incorporating beachwear collections, including bags, outerwear, and mini-dresses, which complement their swimwear offerings. Women's swimwear benefits from fashion-forward designs and seasonal refreshes, encouraging multiple purchases annually, while accessories provide year-round revenue, reducing seasonal dependency. Accessories innovation focuses on tech integration, with waterproof cases, UV-monitoring devices, and performance-tracking wearables creating new market intersections. The segment's growth reflects consumer preference for holistic swim ecosystems over standalone products, offering opportunities for brands with cohesive collections across product types.

By Material Type: Polyester Stability Amid Spandex Innovation

In 2025, polyester leads with a 39.22% market share, thanks to its durability and scalable manufacturing, which balance cost optimization and performance. Spandex is expected to grow at the fastest rate, with an 7.97% CAGR through 2031, driven by advancements in chlorine resistance, UV protection, stretch recovery, and the integration of recycled content. Nylon dominates premium segments, such as women's fashion swimwear, where its superior hand feel and drape justify the higher costs. Emerging bio-based and recycled materials are gaining market share through innovations in sustainability and performance, challenging traditional materials.

LYCRA's lastingFIT technology enhances swimwear longevity, lasting up to 10 times longer than standard spandex by improving resistance to chlorine, UV exposure, and washing. Speedo's biodegradable polyamide addresses environmental concerns while maintaining performance, with garments decomposing within three years when disposed of properly. China's spandex oversupply, characterized by capacity growth outpacing demand and historic low prices, enables manufacturers to incorporate higher spandex content into mid-market products while remaining competitive. Material selection reflects brand strategies, with premium brands focusing on technical performance and sustainability, while mass-market products prioritize cost efficiency. Rising performance demands and environmental responsibility drive material innovation toward superior technical and eco-friendly solutions.

By Category: Mass Market Scale Enables Premium Growth

In 2025, the mass category commands a dominant 87.10% market share, laying the groundwork for efficient supply chains and retail distribution. Meanwhile, the premium segment, which is projected to grow at a 7.72% CAGR through 2031, highlights a rising consumer trend: a willingness to invest in differentiated products. The mass market prioritizes accessibility and basic functionality, distributing widely through supermarkets and hypermarkets. This approach caters to price-sensitive consumers who value cost over advanced features. Conversely, the premium segment's growth is driven by demographic shifts: a rising disposable income, heightened health consciousness, and a trend among younger consumers. These younger shoppers are increasingly viewing swimwear as a lifestyle statement, rather than just functional attire.

China's premium sportswear market is growing at a rate nearly nine times that of the general apparel market, underscoring a regional appetite for premium, activity-specific products, including swimwear. Lululemon's impressive 45% growth in China, with net sales nearing USD 1 billion for fiscal year 2023, showcases the potential for premium brands. Their success stems from community-driven marketing and direct-to-consumer strategies, sidestepping traditional retail markups. As consumers recognize performance benefits and cultivate brand loyalty, the shift from mass to premium becomes evident. Premium brands are now emphasizing technical innovation, sustainability, and experiential retail to validate their price points. In response, mass market players are enhancing features and design, blurring the lines between traditional categories.

By Distribution Channel, the Digital Transformation Reshapes Retail

In 2025, traditional supermarkets and hypermarkets command a 37.35% market share, leveraging convenience, impulse buying, and prominent seasonal displays. However, they face competition from online retail stores, which are expanding at a robust 8.55% CAGR, projected to continue through 2031. This surge in online channels underscores a broader e-commerce trend, bolstered by advanced product visualization technologies and direct-to-consumer strategies that sidestep traditional retail margins. Specialty stores, with their expert fitting services and curated premium brands, remain vital, especially in the performance swimwear category, where a perfect fit is crucial. Meanwhile, other channels, such as resort retail and pop-up concepts, adeptly tap into tourism-driven demand and seasonal buying habits.

Southeast Asia's e-commerce surge underscores the digital channel's promise, with prominent players such as Shopee, while TikTok Shop, through its innovative blend of content creation and direct purchasing, boasts a GMV of USD 15 billion. Amazon Singapore emerges as a pivotal regional hub, facilitating cross-border distribution of swimwear. Their 'fulfillment by Amazon' service streamlines logistics for international brands. As online purchasing gains traction, brands are channeling investments into digital marketing, influencer collaborations, and virtual try-on tech, mirroring in-store fitting experiences. Social commerce platforms elevate the game for swimwear brands, allowing them to present products in relatable lifestyle scenarios, thanks to user-generated content and influencer partnerships. This approach crafts a more immersive shopping experience, outshining traditional e-commerce catalogs. The evolving distribution landscape favors brands adept at omnichannel strategies, balancing a physical retail presence with robust digital consumer engagement.

Geography Analysis

The Asia-Pacific region represents the dominant and most rapidly expanding market for swimwear globally. In 2025, China seized a commanding 32.16% share of the Asia-Pacific swimwear market, driven by robust domestic demand, a burgeoning middle class, and a crackdown on counterfeits that increasingly favors genuine brands. While fluctuations in raw material prices and intellectual property violations pose challenges, government-led fitness initiatives and upgraded facilities bolster volume growth. The Chinese market is characterized by an increasing interest in water sports and fashion-forward, high-quality one-piece suits, heavily influenced by online retail and social media trends. India, riding the wave of swift urbanization and a youthful populace, boasts the region's fastest growth at an 7.88% CAGR. This momentum is further propelled by Decathlon's ambitious commitment to ramp up local sourcing to USD 3 billion by 2030. With production-linked incentives for technical textiles and the "Make in India" initiative, India emerges not just as a consumer giant but also as a budding export nexus, effectively diversifying the regional supply chain.

The markets in Japan, Australia, and New Zealand are mature and health-conscious, with a strong emphasis on functional fabrics offering UV protection and chlorine resistance, aligning with sun-safety mandates and high rates of water activity participation. South Korea exhibits a similar interest in high-tech, fashionable, and functional wear. Southeast Asia benefits significantly from year-round tourism, with key markets such as Thailand, Singapore, and Indonesia experiencing high demand during holiday seasons. A large youth population and changing cultural attitudes are driving demand for modern styles beyond traditional modest swimwear, with government initiatives like 'Make in India' supporting local manufacturing. Overall, the regional landscape is characterized by a blend of established markets that focus on quality and functionality, and emerging markets driven by rapid lifestyle changes and economic growth.

Completing the growth tapestry are Australia, Japan, Thailand, Singapore, Indonesia, South Korea, and New Zealand. Japan leans towards high-tech fabrics and eco-friendly credentials, Thailand enjoys a resurgence thanks to resort tourism, Singapore reaps benefits from prestigious aquatic events, and Australia leads in regional facility investments. Together, these nations fortify the Asia-Pacific swimwear market against localized economic upheavals, rewarding brands that adeptly adjust their offerings to align with local climates, cultures, and regulatory landscapes.

Competitive Landscape

The Asia-Pacific swimwear market is a dynamic and competitive landscape, characterized by a mix of global giants, regional specialists, and emerging digital-first brands. Key players include multinational corporations such as Adidas AG, Nike Inc., Pentland Group (including Speedo), Arena Italia S.p.A., and Boardriders (parent company of Rip Curl and Billabong), alongside regional and local brands like Seafolly Australia, Wacoal Holdings, and Zivame. Strategies for market growth are multi-pronged, with a strong focus on technological advancements in fabrics, such as UV protection (UPF 80+) and chlorine resistance, to cater to performance-oriented consumers and sun-safety mandates in countries like Australia. Responding to growing consumer ecological consciousness, brands are increasingly adopting eco-friendly materials, such as recycled yarns and biodegradable polyamides, and implementing sustainable production practices. For example, in April 2025, Speedo unveiled a new biodegradable apparel line to appeal to the ethically minded consumer.

Companies are bridging the gap between performance wear and fashion by launching trendy designs, inclusive sizing, and multifunctional swimwear that aligns with the growing athleisure trend. This approach appeals to a wider demographic, particularly women, who hold the largest market share. Brands are also focusing on an omnichannel approach, leveraging traditional supermarkets and hypermarkets while heavily investing in online retail and social commerce platforms, which are the fastest-growing distribution channels in the region. Major players are engaging in mergers, acquisitions, and partnerships to expand their product ranges and market reach. For instance, a collaboration between Arena and The Woolmark Company in June 2023 focused on lightweight, biodegradable swimsuits.

This strategic agility, combining innovation with sustainable practices and targeted distribution, is essential for maintaining a competitive edge in this rapidly evolving market. By addressing consumer demands for functionality, sustainability, and style, brands are positioning themselves to capitalize on the region's growth potential. The Asia-Pacific swimwear market continues to evolve, driven by a blend of technological advancements, eco-conscious initiatives, and a focus on meeting diverse consumer preferences.

Asia Pacific Swimwear Industry Leaders

-

Adidas AG

-

Nike Inc

-

Pentland Group

-

Arena S.p.A.

-

TYR Sport Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Speedo launched the Eco Fastskin collection, which represented a significant move towards sustainability in the performance swimwear market. The line was asserted to be crafted entirely from 100% recycled nylon and polyester, making it an eco-conscious alternative for competitive swimmers and fitness enthusiasts. The collection maintains the high-performance standards for which Speedo is known, offering exceptional durability and a sleek, hydrodynamic fit.

- July 2025: Lululemon opened its first-ever retail-meets-wellness concept store in Southeast Asia, located in Singapore’s Takashimaya Shopping Centre. The store featured an integrated wellness offering through a partnership with a local movement studio. This innovative approach allows customers to not only shop for Lululemon's product lines, including swimwear, but also participate in adjacent yoga and Pilates classes.

- January 2025: H&M launched a major size-inclusive swimwear campaign, which featured a new collection of adaptive swimwear designs. The launch was aimed at creating more accessible and body-positive options for a wider range of customers. The collection included a variety of styles, from bikinis to one-pieces, catering to different body types and needs.

- May 2024: SHEIN collaborated with influencer and TV personality Lele Pons and launched an exclusive swimwear collection. The collection featured a wide variety of on-trend, affordably priced pieces, including vibrant bikinis, stylish one-pieces, and resort wear. The designs were inspired by Pons' personal style, with key elements including marbled patterns, mesh cutouts, and neon crochet.

Asia Pacific Swimwear Market Report Scope

Swimwear is an outfit worn along with accessories while performing swimming. The outfit allows the consumer to swim with ease and comfort. The Asia-Pacific swimwear market (henceforth referred to as the market studied) is segmented by product type, distribution channel, and geography. By product type, the market is segmented into women's swimwear, men's swimwear, goggles, and caps. Based on the distribution channel, the market studied is segmented into offline stores and online stores. By geography, it is segmented into China, India, Japan, Australia, and the rest of Asia-Pacific. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Women's Swimwear |

| Men's Swimwear |

| Kids' Swimwear |

| Accessories |

By Material Type

| Nylon |

| Polyester |

| Spandex |

| Other Fabric Types |

By Category

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Women's Swimwear |

| Men's Swimwear | |

| Kids' Swimwear | |

| Accessories | |

| By Material Type | Nylon |

| Polyester | |

| Spandex | |

| Other Fabric Types | |

| By Category | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific swimwear market in 2026?

The market stands at USD 9.08 billion in 2026 and is projected to reach USD 12.42 billion by 2031.

What is the forecast CAGR for Asia-Pacific swimwear through 2031?

A compound annual growth rate of 6.47% is expected from 2026 to 2031.

Which product category grows fastest within the Asia-Pacific swimwear?

Accessories, including UV-protective cover-ups and waterproof wearables, are growing at a 7.57% CAGR.

Which country is the fastest-growing swimwear market in the region?

India leads with an 7.88% CAGR through 2031, driven by urbanization and policy support.

How are online channels impacting swimwear sales?

Online retail advances at an 8.55% CAGR, powered by social commerce platforms that blend influencer content and one-click purchasing.

Which material innovation offers the longest suit life?

LYCRA lastingFIT fiber provides suits up to ten times more resistant to chlorine and UV than traditional spandex blends.

Page last updated on: