Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

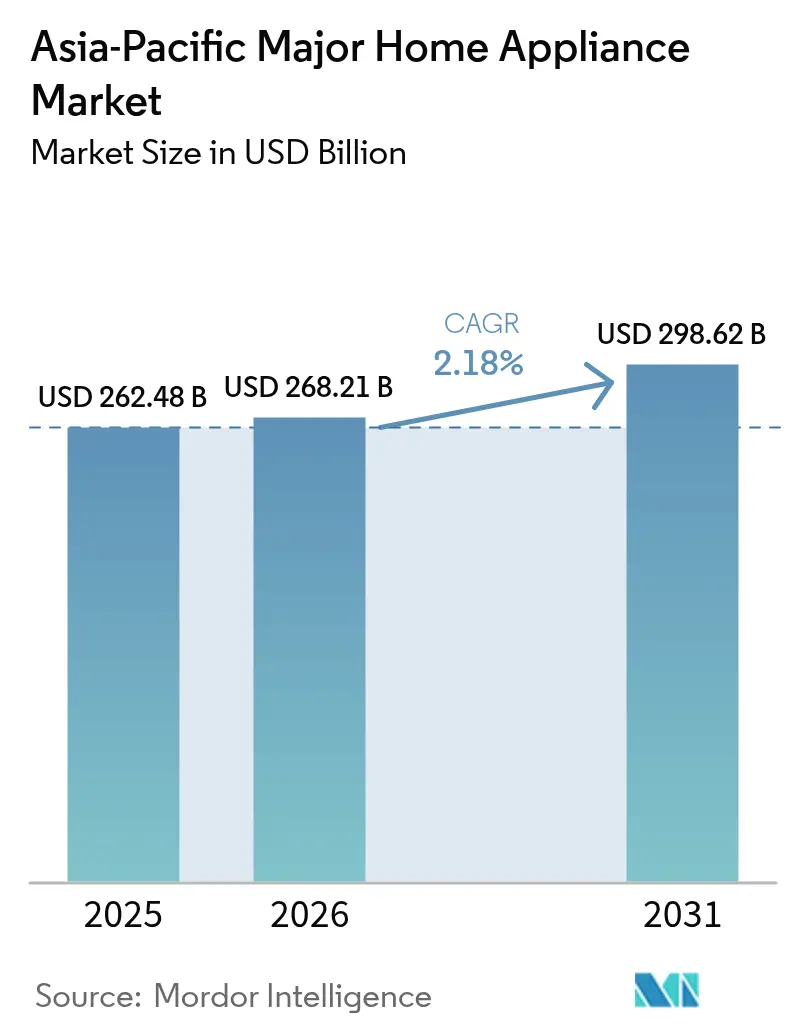

| Base Year Market Size (2025) | USD 262.48 Billion |

| Market Size (2026) | USD 268.21 Billion |

| Market Size (2031) | USD 298.62 Billion |

| Growth Rate (2026 - 2031) | 2.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Major Home Appliance Market Analysis by Mordor Intelligence

The Asia-Pacific major home appliance market size is expected to grow from USD 262.48 billion in 2025 to USD 268.21 billion in 2026 and is forecast to reach USD 298.62 billion by 2031 at 2.18% CAGR over 2026-2031. The shift from volume-led expansion toward value-oriented premiumization shapes this trajectory as producers embed smart connectivity, AI, and energy-saving technologies into core product lines while navigating competitive pressure from Chinese OEMs and dynamic consumer preferences across diverse economies [1]China Daily, “Home appliance makers eye bigger global reach,” chinadaily.com.cn. In . In mature markets such as Japan and South Korea, replacement demand for high-end SKUs dominates, whereas first-time purchases anchored in rising disposable incomes and rapid urbanization propel growth in Indonesia, Vietnam, and the Philippines. Government trade-in subsidies, buy-now-pay-later (BNPL) schemes, and expanding last-mile logistics collectively protect baseline demand despite raw-material cost volatility. Strategic moves by leading manufacturers include cross-border localization of production to sidestep tariffs and shorten lead times, as well as ecosystem partnerships that integrate appliances with home-energy management platforms.

Key Report Takeaways

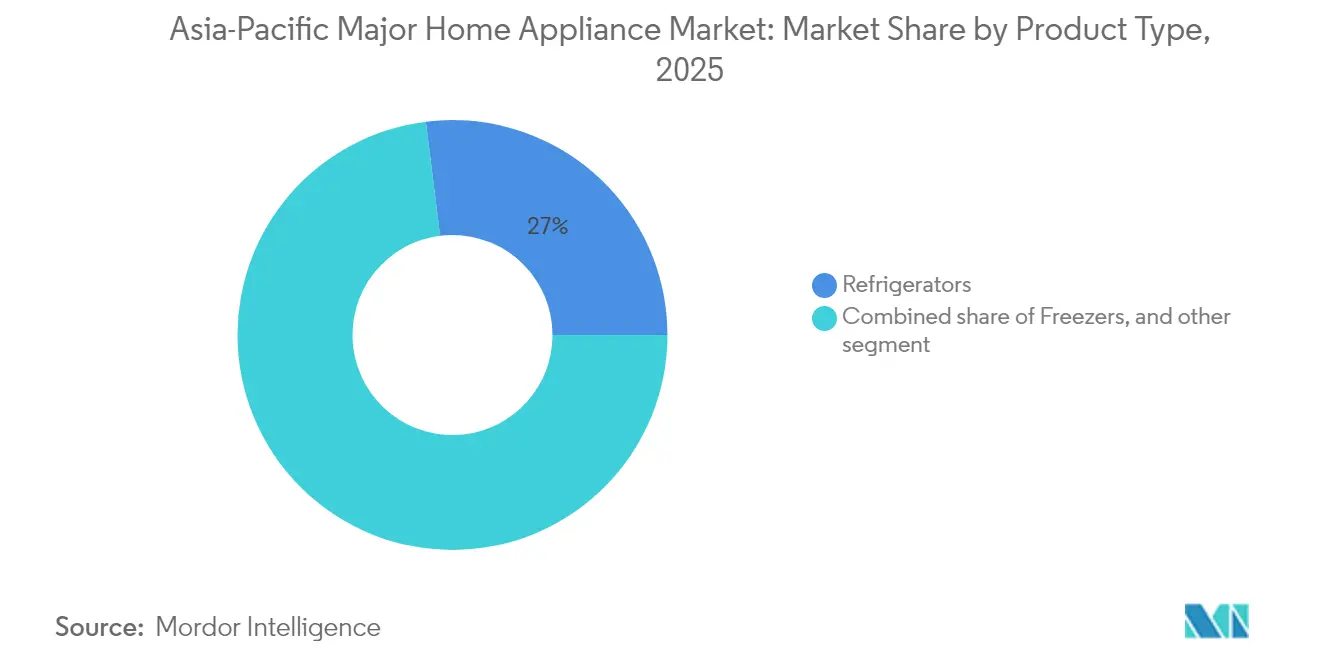

- By product type, refrigerators led with 26.98% of Asia-Pacific major home appliance market share in 2025, while smart refrigerators posted the fastest 14.75% CAGR through 2031.

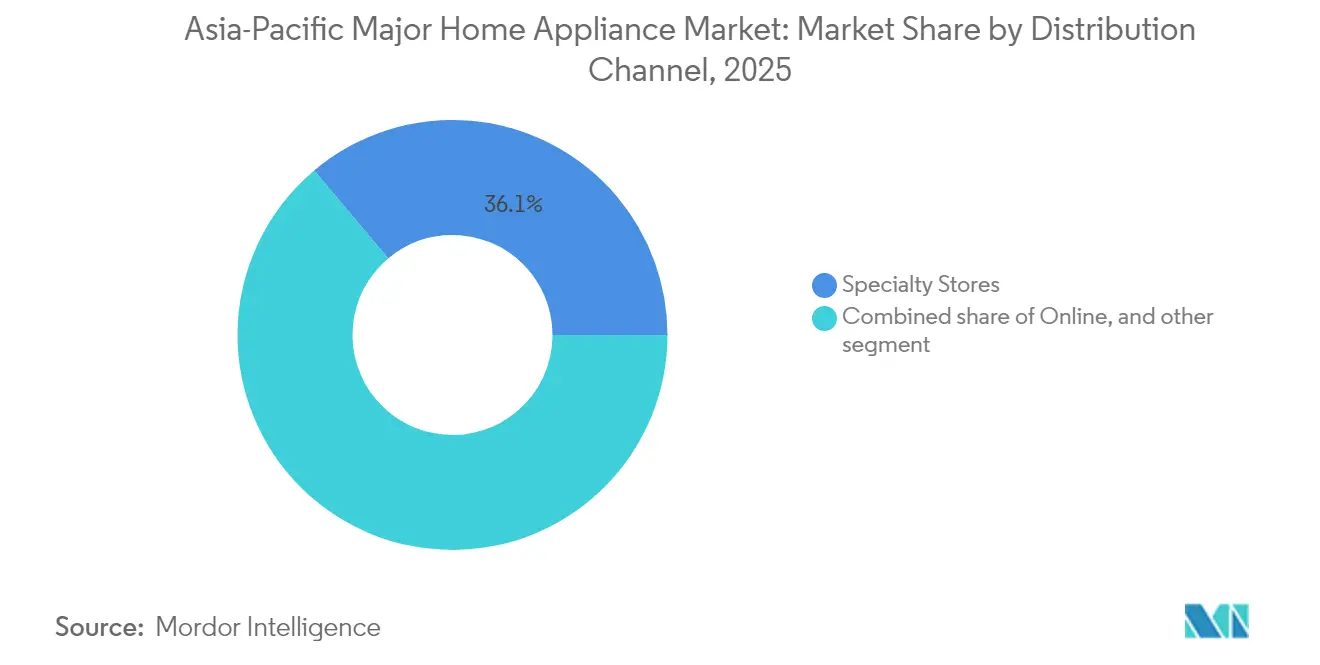

- By distribution channel, specialty stores captured 36.12% of Asia-Pacific major home appliance market share in 2025; e-commerce recorded the strongest 18.92% CAGR through 2031.

- By technology, smart connected appliances accounted for a 32.85% share of the Asia-Pacific major home appliance market size in 2025 and are advancing at a 15.11% CAGR through 2031.

- By geography, China commanded 43.02% share of the Asia-Pacific major home appliance market in 2025, whereas Southeast Asia is projected to expand at a 15.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Major Home Appliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & rapid urbanisation | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Explosive growth of e-commerce & last-mile logistics | +0.8% | Global, strongest in ASEAN | Short term (≤ 2 years) |

| Mandatory energy-efficiency rebate & trade-in schemes | +0.6% | China, India, Singapore | Short term (≤ 2 years) |

| Cross-border localisation of Chinese OEM manufacturing | +0.4% | ASEAN, India, Mexico | Medium term (2-4 years) |

| BNPL & embedded-finance-powered affordability | +0.3% | Southeast Asia, India | Short term (≤ 2 years) |

| Uptake of premium built-in / modular kitchen concepts | +0.2% | Urban China, India, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Rapid Urbanisation

Middle-income households across Indonesia and Vietnam grew sharply in 2024 and are projected to exceed 415 million by 2030, driving first-time appliance purchases and accelerating replacement cycles. Urban migration concentrates demand in tier-2 cities where real-estate developers bundle built-in kitchens with residential projects, spurring multi-appliance adoption. Retailers leverage BNPL platforms to convert latent demand into sales by lowering upfront price barriers. Correlation between urbanization velocity and appliance penetration remains strongest in cities where infrastructure outpaces income, creating near-term surges once credit access improves. For manufacturers, aligning product portfolios with aspirational yet affordable SKUs helps balance volume and margin goals.

Explosive Growth of E-Commerce & Last-Mile Logistics

Enhanced logistics networks and omnichannel strategies pushed digital transactions to a 19.84% CAGR for the Asia-Pacific major home appliance market. Regional platforms introduced augmented-reality showrooms that reduce the need for physical touchpoints in high-consideration categories like refrigerators and washers. Cross-border marketplaces allow Chinese brands to reach underserved rural customers, but aggressive discounting compresses margins. Partnerships with third-party logistics players shorten delivery windows to under 48 hours in key ASEAN metro areas, strengthening consumer confidence. Integrated after-sales services and instant refunds further narrow the experiential gap with brick-and-mortar outlets.

Mandatory Energy-Efficiency Rebate & Trade-In Schemes

China’s national trade-in subsidies lifted large-appliance retail sales by 24.8% year-over-year in Q4 2024 [2]Shanghai Metals Market, “[SMM Hot Topic] Home Appliance Sales Hit a Record High in 2024,” metal.com. . Singapore’s tighter energy labeling rules raised minimum standards, prompting a shift to inverter compressors and heat-pump dryers. These programs induce demand spikes that compel manufacturers to refine production planning and inventory allocation. Retailers synchronize promotional calendars with subsidy windows to maximize sell-through, though sudden surges challenge logistics capacity. Over time, stricter efficiency norms elevate average selling prices and catalyze product innovation.

BNPL & Embedded-Finance-Powered Affordability

Fintech partnerships with banks like ACLEDA in Cambodia democratize appliance ownership by converting lump-sum purchases into micro-installments, expanding addressable markets among Gen-Z and rural customers [3]The Straits Times, “Energy-saving standards for certain home appliances raised,” straitstimes.com. . Embedded finance at the point of sale reduces friction, raising acceptance rates even for premium SKUs. Manufacturers gain data-driven insights into repayment behavior, enabling tailored marketing and upsell opportunities. While credit risk requires vigilant monitoring, early evidence suggests default rates remain within acceptable limits due to strong employer-linked deductions and digital KYC protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material & freight costs | -0.9% | Global, acute in import-dependent markets | Short term (≤ 2 years) |

| Margin pressure from low-cost regional OEMs | -0.7% | ASEAN core, India | Medium term (2-4 years) |

| Grid-instability & high tariffs curbing energy-hungry SKUs | -0.4% | India, Indonesia, Philippines | Long term (≥ 4 years) |

| Remote-area logistics & reverse-logistics costs | -0.3% | Rural ASEAN, India tier-3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material & Freight Costs

Steel and copper price volatility compressed manufacturer margins throughout 2024, with galvanized sheet demand from home appliances experiencing mixed performance despite overall production growth exceeding 10%. Raw material cost inflation forces manufacturers to implement dynamic pricing strategies, though consumer price sensitivity limits pass-through effectiveness in competitive segments. Supply chain disruptions from geopolitical tensions and port congestion create inventory management challenges, particularly for companies operating just-in-time production models across multiple geographic markets.

Margin Pressure from Low-Cost Regional OEMs

Aggressive pricing from ASEAN-based manufacturers intensifies competitive pressure in commodity appliance segments, forcing established players to accelerate premium product development and service differentiation strategies. Korean manufacturers like Panasonic adopted private-label production for retailers to maintain volume while preserving brand positioning. This margin compression accelerates industry consolidation as smaller players struggle to maintain profitability amid rising marketing and R&D investment requirements for smart appliance development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigerators Drive Smart Integration

Refrigerators captured 26.98 of % Asia-Pacific major home appliance market share in 2025 and continue to anchor connected-home ecosystems through embedded sensors, cameras, and AI-driven food management software. The premium smart-refrigerator segment is forecast to deliver a 14.75% CAGR, reinforcing the Asia-Pacific major home appliance market trajectory toward higher ASPs. Washing machines held an 17.82% stake as inverter motors and water-saving cycles resonate with urban dwellers. Air conditioners contributed 15.34%, benefiting from rising heat-wave frequency but tempered by energy-tariff sensitivities. Dishwashers and freezers remain niche yet are gaining acceptance in high-density urban apartments as lifestyles evolve.

The convergence of IoT with refrigeration repositions the appliance as a household command center capable of choreographing other devices via voice assistants or smartphone apps. Manufacturers deploy predictive maintenance analytics that flag compressor issues before failures, curbing service costs. Built-in French-door models integrated into modular kitchens enlarge design-driven appeal, while compact top-mount units meet small-space constraints. Competitive intensity is elevated, yet differentiated software ecosystems and proprietary AI algorithms help preserve margins for market leaders.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Specialty stores accounted for a 36.12% share, leveraging hands-on demonstrations and bundled installation to maintain relevance. E-commerce, however, is set to outpace all channels at a 18.92% CAGR, powered by same-day delivery promises and wide product assortments. Multi-brand retailers command 29.18% of the Asia-Pacific major home appliance market, relying on comparative shopping formats and value-added services. Exclusive brand outlets claimed 28.07% through curated customer experiences and loyalty programs.

South Korea’s rental model illustrates channel innovation: the aggregate rental services sector is projected to hit KRW 100 trillion (USD 75.3 billion) by 2025, with 34.5% of large-appliance shoppers opting for subscriptions. Direct-to-consumer portals backed by OEMs use live-stream selling and AR visualization to replicate in-store engagement online. The Asia-Pacific major home appliance market size for online channels is poised to rise further as payment gateways mature and reverse-logistics efficiencies improve.

By Technology: Smart Connectivity Accelerates Adoption

Smart connected appliances held a 32.85% share in 2025 and are expected to expand at a 15.11% CAGR through 2031, well above the broader Asia-Pacific major home appliance market CAGR. These devices sync with AI hubs such as LG ThinQ ON to learn usage patterns and coordinate operations, enabling up to 23% energy savings according to field trials. Conventional appliances, retaining a 67.15% share, remain favored for entry-level price points and perceived reliability. However, commoditization of Wi-Fi modules and voice control is eroding the price gap, encouraging faster mid-tier diffusion.

Energy-efficient technologies comprise 38% of total units sold, aided by government rebates. Inverter compressors, heat-pump dryers, and R-32 refrigerants are becoming baseline specs. Early adopters of predictive-maintenance algorithms unlock subscription service revenues and extend product lifecycles by dispatching technicians preemptively. Data privacy regulation compliance emerges as a differentiator as governments scrutinize cross-border data flows from connected devices.

Geography Analysis

China retained a 43.02% of the Asia-Pacific major home appliance market share in 2025, underpinned by domestic brand dominance and integrated supply chains, yet saturation is slowing unit growth. The Asia-Pacific major home appliance market size in China is moving toward replacement-driven cycles, emphasizing smart upgrades and high-efficiency SKUs. Southeast Asia, propelled by urbanization and youthful demographics, is the fastest-growing sub-region at a forecast 15.82% CAGR. India followed with a 15.42% share in 2025, benefitting from production incentives and a widening middle-class, while Japan sustained a 14.05% slice despite an aging population through premiumization and frequent replacement.

Australia and South Korea contribute smaller proportions but demonstrate high per-capita spend and advanced adoption of connected-home ecosystems. Retail expansion by groups such as Harvey Norman signals confidence in Southeast Asia’s long-run demand. Meanwhile, Chinese OEMs are leveraging ASEAN production bases to secure tariff-free access to the Regional Comprehensive Economic Partnership (RCEP) bloc, shortening delivery cycles and tailoring products to tropical climates.

India features a dichotomy of price-sensitive rural customers and premium-oriented urban consumers. LG planned an INR 5,000 crore (USD 600–610 million) manufacturing complex in Andhra Pradesh to tap local sourcing incentives. Urban smart-energy platforms that integrate solar rooftops and time-of-use tariffs catalyze the adoption of AI-enabled appliances capable of dynamic load shifting. However, intermittent grid quality and high GST rates on large appliances constrain penetration in lower-income segments, sustaining latent demand for future conversion.

Competitive Landscape

The Asia-Pacific major home appliance market is becoming moderately concentrated as leading brands strengthen their positions through innovation and regional strategies. Haier Smart Home is expanding its presence with a multi-brand approach, including premium lines like CASARTE, supported by a global R&D network. Midea Group has prioritized international expansion, establishing Thailand as a key production hub outside China. LG Electronics continues to build consumer lock-in through its ThinQ AI platform, seamlessly connecting HVAC, kitchen, and laundry appliances. Meanwhile, Samsung emphasizes product design and has expanded its heat-pump dryer offerings to suit various Asian climates, while Panasonic focuses on energy efficiency and product reliability, integrating appliances with home energy storage systems.

Strategic approaches vary by country, with Chinese manufacturers focusing on geographic diversification to mitigate trade risks, Korean firms deepening their AI and software capabilities, and Japanese companies highlighting energy efficiency and high-quality after-sales support. Subscription-based appliance services, which gained popularity in South Korea, are spreading across Southeast Asia, offering recurring revenue opportunities and deeper customer relationships. There is also growing interest in retrofit smart modules that enable basic connectivity in older appliances, catering to price-sensitive consumers. In markets like Japan and South Korea, aging populations are driving demand for user-friendly appliances such as microwaves and washer-dryers with ergonomic designs. These trends are shaping both product development and go-to-market strategies across the region.

The competition is intensifying as companies ramp up patent filings related to AI and sensor technologies. Many manufacturers are collaborating with semiconductor firms to co-develop components that improve energy efficiency and enhance data security. Sustainability is also becoming a key purchasing factor, particularly among institutional buyers, prompting brands to use recycled materials and adopt low-emission logistics solutions. As a result, competitive advantage is shifting beyond pricing to include system integration, responsive service networks, and environmental performance. The future of the market will be shaped by how effectively brands align technological innovation with evolving consumer and regulatory expectations.

Asia-Pacific Major Home Appliance Industry Leaders

Haier Smart Home

Midea Group

LG Electronics

Samsung Electronics

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Midea Group designated Thailand its largest overseas manufacturing hub, operating seven plants to bolster Asia-Pacific leadership.

- March 2025: ACLEDA Bank and Daikin launched BNPL financing for Cambodian consumers.

- January 2025: Toshiba Lifestyle allocated USD 207 million to expand Thai production of refrigerators, washers, and air conditioners.

- November 2024: Samsung and LG launched premium all-in-one washer-dryers in South Korea, with LG's Signature model priced at KRW 6.9 million (USD 5,180) and Samsung's Bespoke AI Combo featuring heat-pump drying technology

Asia-Pacific Major Home Appliance Market Report Scope

A complete background analysis of Asia-Pacific Home Appliances market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview is covered in the report.

By Product Type

| Refrigerators |

| Freezers |

| Dishwashing Machines |

| Washing Machines |

| Ovens |

| Air Conditioners |

| Other Major Products (Electric Hobs, Ranges, etc.) |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Technology

| Smart Connected Major Appliances |

| Conventional Major Appliances |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) |

| Rest of Asia-Pacific |

| By Product Type | Refrigerators |

| Freezers | |

| Dishwashing Machines | |

| Washing Machines | |

| Ovens | |

| Air Conditioners | |

| Other Major Products (Electric Hobs, Ranges, etc.) | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Technology | Smart Connected Major Appliances |

| Conventional Major Appliances | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific major home appliance market in 2026?

The market is valued at USD 268.21 billion in 2026 with a forecast CAGR of 2.18% through 2031.

Which product category holds the largest share in Asia-Pacific home appliances?

Refrigerators lead with 26.98% share, supported by rapid uptake of smart, energy-efficient models.

Which region within Asia-Pacific is expected to grow quickest for home appliances?

Southeast Asia is projected to expand at a 15.82% CAGR through 2031, driven by urbanization and rising incomes.

What is the outlook for smart connected appliances?

Smart devices already command a 32.85% share and are accelerating at a 15.11% CAGR as AI ecosystems mature across the region.

How are financing innovations influencing appliance demand?

BNPL and embedded-finance platforms lower upfront costs, broadening access among younger and rural consumers while enabling OEMs to capture service-driven revenue streams.

Page last updated on: