Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

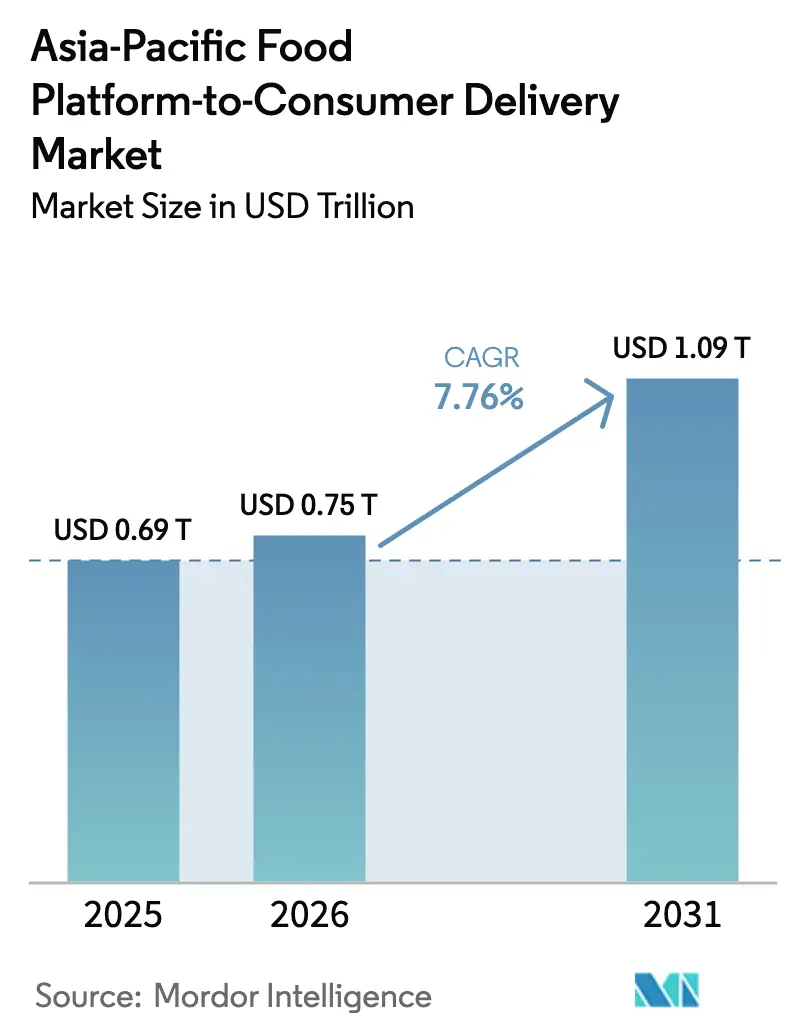

| Base Year Market Size (2025) | USD 0.69 Trillion |

| Market Size (2026) | USD 0.75 Trillion |

| Market Size (2031) | USD 1.09 Trillion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Food Platform-to-Consumer Delivery Market Analysis by Mordor Intelligence

The Asia-Pacific Food Platform-to-Consumer Delivery Market size is expected to grow from USD 0.69 trillion in 2025 to USD 0.75 trillion in 2026 and is forecast to reach USD 1.09 trillion by 2031 at a 7.76% CAGR over 2026-2031. Infrastructure investments in dark-kitchen grids, rapid 4G and 5G rollouts, and super-app bundling are reshaping access to prepared meals for 2.3 billion regional consumers. Express fulfillment promises under 30 minutes have migrated from premium novelty to baseline expectation, while social-commerce tie-ins convert entertainment streams into high-velocity transactions at marginal marketing cost. Competitive tactics continue to revolve around subsidy-funded user acquisition, yet leading operators are pivoting to vertical integration and autonomous logistics to protect margins. Regulators are simultaneously raising the cost floor through gig-worker protections, data localization mandates, and single-use plastic bans, forcing a reassessment of long-standing growth assumptions.

Key Report Takeaways

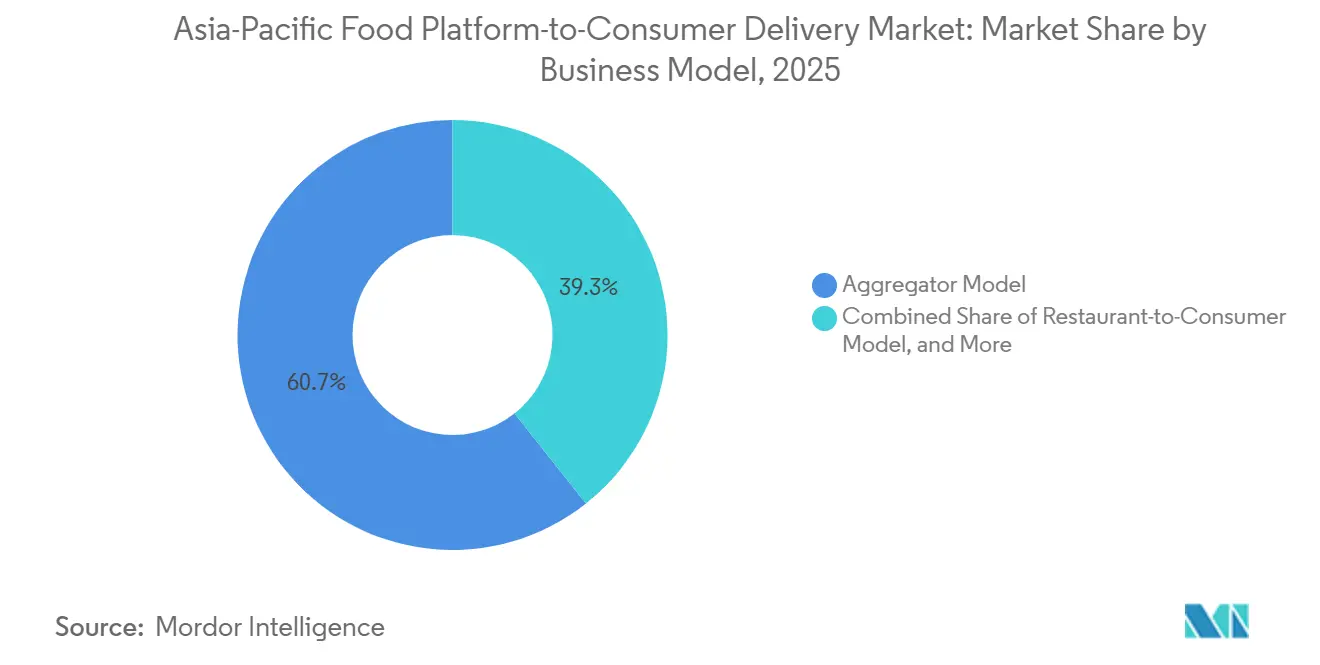

- By business model, the aggregator format led with 60.66% revenue share in 2025; hybrid and cloud-kitchen-owned platforms are advancing at a 9.40% CAGR to 2031.

- By geography, China captured 54.48% of the Asia-Pacific food platform-to-consumer delivery market share in 2025, while Indonesia is projected to expand at an 8.10% CAGR through 2031.

- By order platform, mobile apps accounted for 82.55% of orders in 2025 and are rising at an 8.80% CAGR to 2031.

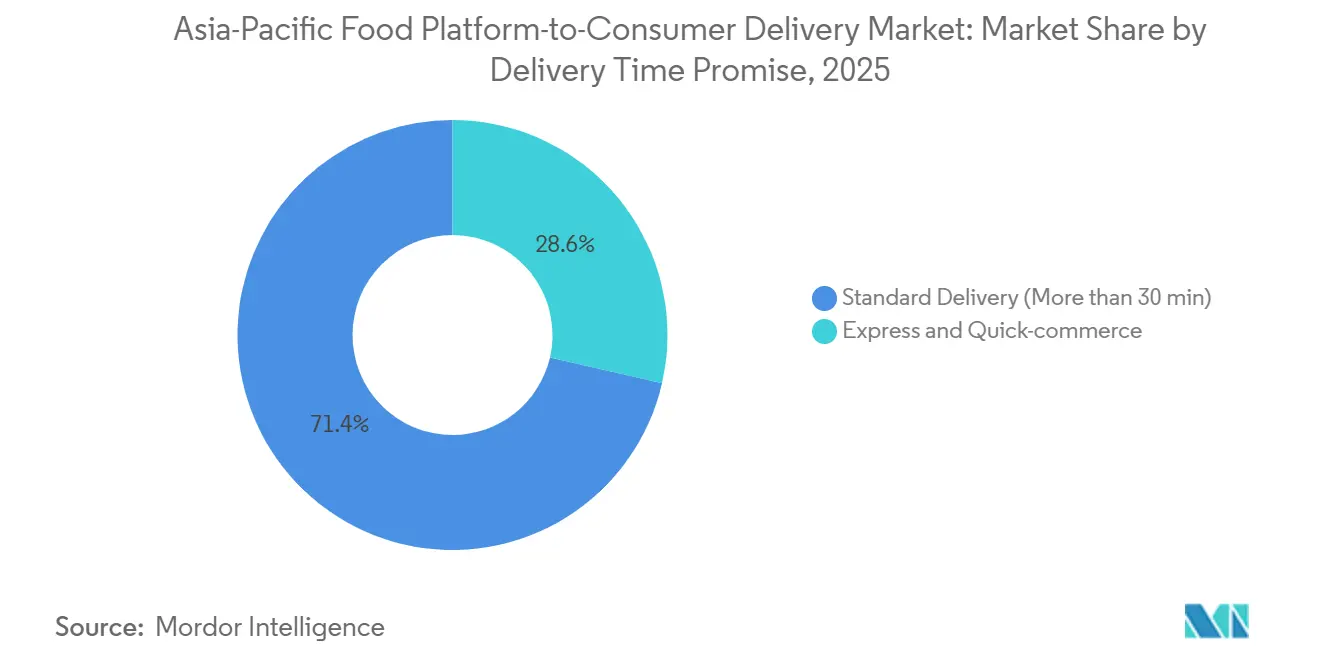

- By delivery time promise, express fulfillment represented 28.6% of orders in 2025 and is growing at an 8.6% CAGR, outpacing standard delivery.

- By consumer segment, household users held 71.05% volume share in 2025; the student segment is registering the fastest 8.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Food Platform-to-Consumer Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dark-kitchen networks enabling Less than 30-min fulfillment | +2.8% | India, Indonesia, China Tier-2 and Tier-3 cities | Medium term (2-4 years) |

| Social-commerce gifting of food orders during live-stream events | +1.9% | China, South Korea, Southeast Asia | Short term (≤ 2 years) |

| Explosive smartphone penetration in Tier-2 and Tier-3 APAC cities | +1.6% | India, Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Discount-driven user acquisition battles among super-apps | +1.2% | Most APAC markets, especially India and Indonesia | Short term (≤ 2 years) |

| Affordability of 4G/5G data plans | +1.40% | India, Indonesia, Vietnam, Philippines | Long term (≥ 4 years) |

| Rapid urban millennial lifestyle shifts | +1.70% | China, India, South Korea, Singapore | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Dark-Kitchen Networks Enabling Less than 30-Minute Fulfillment

Cloud kitchens have matured into the infrastructure spine that makes sub-30-minute delivery financially viable. Rebel Foods operates 450 facilities and secured USD 210 million from KKR in 2024 to expand into Indonesia and the Middle East, signaling institutional belief in asset-light networks that sit closer to demand. Hangry raised USD 10.5 million to seed secondary Indonesian cities where traditional restaurant density is thin, demonstrating the arbitrage opportunity in underserved locales. In China, Meituan has rolled out 500 autonomous vehicles completing 20 orders daily each, trimming last-mile cost by 30%. By decoupling production from dining space, dark kitchens let platforms reposition supply dynamically, compress delivery radii, and meet rising service levels without relying on partner compliance. The model resonates strongest in Tier-2 and Tier-3 clusters where smartphone uptake is surging but brick-and-mortar options lag.

Social-Commerce Gifting of Food Orders During Live-Stream Events

Live-stream retail generated USD 807 billion GMV in China during 2024, with food and beverage ranking second by volume. Ele.me’s 2025 integration with Taobao Live allowed influencers to drop discount codes mid-broadcast, spiking new-user additions by 40% during campaign windows.[1]Alibaba Group, “Taobao Live Merchant Tools Update 2025,” alibaba.com South Korea’s Baemin mirrored the feature through Naver Live, letting hosts curate meal bundles redeemable in a single click. Social gifting turns entertainment into frictionless checkout, moving marketing dollars from paid search toward influencer ecosystems that deliver higher conversion at lower cost. Because viewers treat vouchers as experiential gifts, average order values trend 12-15% above platform means, reinforcing the tactic’s profitability.

Explosive Smartphone Penetration in Tier-2 and Tier-3 APAC Cities

Smartphone ownership in India’s Tier-2 and Tier-3 cities reached 68% in 2025, up from 52% two years earlier, fueled by sub-USD 150 handsets and cheaper data. Indonesia hit 71% penetration in secondary municipalities,[2]Telecom Regulatory Authority of India, “The Indian Telecom Services Performance Indicators October-December 2025,” trai.gov.in aided by subsidized 4G expansion. Swiggy disclosed that 38% of Q3 FY25 gross order value came from these hinterland zones, up 10 percentage points in two years. Zomato tracked a 22% year-over-year order-frequency jump in Tier-2 locales once delivery times fell below 40 minutes. The interplay of affordable devices, reliable coverage, and expanding dark-kitchen grids is widening the total addressable base faster outside megacities, tilting platform growth strategies toward new regional catchments.

Discount-Driven User Acquisition Battles Among Super-Apps

Super-apps deploy food delivery as the on-ramp to higher-margin fintech and mobility services. Grab’s delivery segment produced USD 664 million revenue in Q3 2024 yet remained loss-making, while its financial unit posted USD 93 million operating profit, underscoring deliberate cross-subsidization. GoTo booked Q3 2024 GMV of USD 3.9 billion but reported an USD 87 million operating loss after offering 50% discounts to defend Indonesian share. Meituan’s sales and marketing line grew 18% year-over-year even as order growth plateaued, revealing low switching costs and fragile loyalty. Competitive parity forces perpetual subsidies, and no incumbent can unilaterally retreat without ceding volume. The cycle erodes unit margins, prompting a search for alternative revenue levers such as proprietary kitchens and logistics automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising rider-wage regulation and social-security costs | -1.4% | Singapore, Malaysia, India, China | Medium term (2-4 years) |

| Thin unit economics amid subsidy wars | -1.1% | Regionwide, most acute in India and Indonesia | Short term (≤ 2 years) |

| Stricter data-localization and privacy rules | -0.6% | China, India, Indonesia, Vietnam | Long term (≥ 4 years) |

| ESG pressure on single-use packaging | -0.5% | Singapore, Japan, Australia, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Rider-Wage Regulation and Social-Security Costs

Mandatory gig-worker protections are resetting labor economics. Malaysia’s 2025 Gig Workers Bill obliges platforms to fund provident and social-security accounts, adding MYR 200-300 (USD 45-67) monthly per active rider. Singapore’s Platform Workers Act requires work-injury coverage and representation rights, inflating per-order cost by 8-10%. India’s phased Social Security Code enables states to classify gig couriers as employees, creating compliance uncertainty.[3]Government of India Ministry of Labour and Employment, “Social Security Code Implementation Status,” labour.gov.in In China, provincial enforcement of 2023 guidelines compels platforms to guarantee minimum wages and accident insurance. Operators thus face a margin squeeze: absorb the expense, pass it to restaurants, or risk demand elasticity by raising consumer fees.

Thin Unit Economics Amid Subsidy Wars

Despite scale, profitability remains scarce. Swiggy’s Q2 FY26 loss widened to Rs 1,092 crore (USD 130 million) even as gross order value rose 15%. Delivery Hero recorded EUR 2.9 billion revenue in Q3 2024 but still posted an adjusted EBITDA loss of EUR 47 million (USD 50 million). Meituan’s core local-commerce margin slipped to 20.6% as it boosted rider pay and restaurant incentives. Growing order frequency fails to offset escalating marketing and compliance charges, implying structural fragility in commission-centric economics. Platforms are countering by pivoting into quick commerce and grocery, yet those verticals demand fresh warehousing and dark-store spend, prolonging the break-even horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Vertical Integration Gains Ground

Hybrid and cloud-kitchen-owned formats are expanding at a 9.40% CAGR through 2031, nearly triple the growth rate of the Asia-Pacific food platform-to-consumer delivery market. The aggregator structure still held 60.66% share in 2025, powered by incumbents such as Meituan, Zomato, and GrabFood, yet its dominance is slipping as operators chase restaurant-level margins once obscured by commissions. Rebel Foods’ USD 210 million raise from KKR highlighted investor conviction that owned kitchens can scale across borders faster than marketplace listings. Zomato’s take rate fell from 22% in FY23 to 19% in FY25 after chains demanded lower fees, illustrating shrinking pricing power. Platforms are responding by blending aggregation with proprietary supply, rerouting peak-hour demand to in-house brands, and using algorithmic load balancing to protect service-level agreements.

The Asia-Pacific food platform-to-consumer delivery market now prioritizes inventory control over homepage traffic. Swiggy Access runs 80 kitchens across 15 cities, filling demand voids where restaurant density is low. Meituan’s autonomous van fleet further compresses last-mile cost, letting the company sustain promotional pricing without sacrificing contribution margin. Restaurant-to-consumer fleets from Domino’s and KFC, which jointly held roughly 15% market share in 2025, affirm that direct channels can coexist with marketplace reach when data ownership is strategic. The hybrid blueprint therefore balances discovery scale with cost visibility, creating a defensible path to profitability.

By Order Platform: Mobile Apps Dominate and Accelerate

Mobile applications captured 82.55% of the order share in 2025 and are growing at an 8.80% CAGR. Super-app designs that weave food delivery into payments, grocery, and ride-hailing extend session length and raise cross-sell probability. Grab recorded a 28% lift in multi-service usage when users ordered meals, while GoTo’s 2024 tie-up with TikTok Shop embeds GoFood carts into short-video streams that 120 million Indonesians view daily. The Asia-Pacific food platform-to-consumer delivery market for mobile orders is projected to surpass USD 900 billion by 2031, underscoring the channel’s centrality.

Website and desktop flows, once critical for corporate catering, slipped to 13% share in 2025 as mobile-first behavior mainstreamed. Conversational interfaces account for only 3% due to inconsistent voice recognition in regional dialects. Zomato’s WhatsApp ordering experiment targets the 200 million Indian users without dedicated food apps, reflecting a fringe play to nudge digital migration. Meituan’s predictive menu engine, which boosted order frequency by 14%, indicates that mobile supremacy now rests on data-driven personalization rather than raw convenience.

By Delivery Time Promise: Express Fulfillment Reshapes Expectations

Express and quick-commerce propositions promising sub-30-minute arrival are advancing at an 8.6% CAGR, making them the fastest rising sub-segment across the Asia-Pacific food platform-to-consumer delivery market. Standard windows still command 71% share but are eroding as consumers grow accustomed to instant gratification provided by nearby dark kitchens. Swiggy Instamart and Zomato Blinkit provide 10-minute delivery for prepared meals in dense neighborhoods, while BigBasket plans to replicate the model through its 400 dark stores.

The trade-off rests in higher rider density and kitchen throughput. Meituan cut average delivery time from 38 to 32 minutes year over year, yet per-order labor expense climbed 12% due to surge bonuses. Reliance Industries will enter quick-commerce via JioMart targeting 15-minute fulfillment in 20 Indian cities, illustrating how conglomerates view speed as the key disruptor. Consequently, platforms must weigh capital expenditure in micro-fulfillment hubs against potential cannibalization of slower, yet higher-margin, standard deliveries.

By Consumer Segment: Students Drive Incremental Growth

Households contributed 71% of 2025 volume, reflecting deep penetration among family diners, but growth is moderating as saturation nears in metros. Students, in contrast, are expanding at an 8.50% CAGR and delivering outsized order frequency despite lower ticket sizes. GrabStudent offers 30% discounts after 10 p.m. and on-campus pickup, lifting student order counts 45% in Malaysia. GoFood’s pay-later feature reduced Indonesian student cart abandonment by 22%, proving that installment terms can unlock constrained wallets.

Office and corporate demand, holding 18% share in 2025, benefits from companies outsourcing cafeteria programs to improve flexibility. Zomato for Enterprise already supplies 12% of company revenue, and Swiggy Corporate pushes average order value 35% above individual spend. Yet the Asia-Pacific food platform-to-consumer delivery market share gain among students signals that lifetime value accrues by embedding habits early, making youth-centric promotions a strategic imperative.

Geography Analysis

China dominated with 54.48% Asia-Pacific food platform-to-consumer delivery market share in 2025, but growth is slowing as urban penetration exceeds 85%. Meituan and Ele.me now push into Tier-3 cities and rural counties where smartphone coverage improved to 68%. Meituan’s 360,000 drone deliveries in Shenzhen demonstrate logistics trials that can lower rural last-mile cost by 30%. Data-localization rules under the 2025 Personal Information Protection Law raise compliance overhead for foreign entrants, bolstering domestic incumbents.

Indonesia claims the region’s fastest growth. GoFood’s TikTok integration merges social feeds with food ordering, enabling impulse conversion inside entertainment sessions. GrabFood commands 54% share yet faces aggressive discounting from ShopeeFood, which cross-leverages e-commerce wallets. Smartphone take-up in secondary Indonesian cities climbed to 71% under state-backed 4G subsidies, widening the consumer funnel. Concurrently, BPOM heightened kitchen hygiene requirements in 2024, compelling platforms to verify supplier certifications before onboarding.

India, Japan, South Korea, Australia, and the broader Southeast Asia bloc collectively made up more than 40% of the 2025 value. India is the second-largest market, with Zomato achieving first-time profitability via Blinkit quick commerce and Swiggy raising USD 1.2 billion for dark-kitchen expansion. Japan’s landscape remains fragmented as Uber Eats and Demae-can defend their share under tight delivery-fee caps. South Korea’s Baemin holds 60% share yet contends with Coupang Eats’ logistics edge. In Australia, Deliveroo’s 2022 exit left DoorDash, Uber Eats, and Menulog to battle in a stagnant growth setting where profitability remains elusive.

Competitive Landscape

Moderate concentration characterizes the Asia-Pacific food platform-to-consumer delivery market, with the top five players, Meituan, Ele.me, GrabFood, Zomato, and Swiggy, controlling roughly 65% of GMV in 2025. Each enjoys dominance only in its home territory, leading to a patchwork of localized oligopolies. Competitive intensity is heightened by subsidy loops, rapid feature imitation, and super-app leverage that treats meals as customer-acquisition hooks for higher-margin services. Meituan’s autonomous vehicles and drone sorties slash last-mile cost and defend urban share against Douyin’s nascent delivery service. Zomato’s Blinkit pivot underscores the sector-wide move toward inventory ownership and quicker cycles.

Disruptors are emerging at ecosystem edges. Douyin and TikTok Shop infuse shoppable video with one-tap meal vouchers, achieving conversion rates traditional apps struggle to match. Reliance Industries plans a quick-commerce rollout through JioMart in 20 Indian metros by 2026, backed by USD 500 million capex. Platforms converge on three imperatives: bundle more services to boost lifetime value, invest in dark kitchens for supply assurance, and deploy AI personalization to drive frequency. A prisoner’s-dilemma landscape persists, however, where relaxing discounts risks instant share loss, prolonging thin margins despite scale.

Asia-Pacific Food Platform-to-Consumer Delivery Industry Leaders

Meituan Inc.

ELEME Inc (Alibaba)

Grab Holdings Inc.

Delivery Hero SE

Foodpanda GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Swiggy raised Rs 10,000 crore (USD 1.2 billion) via qualified institutional placement to fund quick-commerce growth in Tier-2 Indian cities.

- December 2024: GoTo merged with TikTok Shop Indonesia, embedding GoFood ordering inside TikTok’s video feed.

- November 2024: Swiggy completed its IPO, raising Rs 11,327 crore (USD 1.3 billion) at a Rs 87,000 crore valuation.

- October 2024: Meituan reported RMB 93.6 billion (USD 13.2 billion) revenue and deployed 500 autonomous delivery vans across 10 Chinese cities.

Asia-Pacific Food Platform-to-Consumer Delivery Market Report Scope

Food Platform-to-Consumer Delivery market cover revenues of an online business that acts as an intermediary between consumers and multiple food facilities to submit food orders from a consumer to a participating food facility and to arrange for the delivery of the order from the food facility to the consumer. A food platform to consumer delivery model is a business model where the customers can get their favorite food by making an order via their smartphones or computers.

The Asia-Pacific Food Platform-to-Consumer Delivery Market Report is Segmented by Business Model (Aggregator Model, Restaurant-to-Consumer Model, Hybrid/Cloud-Kitchen-Owned), Order Platform (Mobile App, Website/Desktop, Conversational), Delivery Time Promise (Standard Delivery, Express/Q-Commerce), Consumer Segment (Household Users, Office/Corporate, Students), and Geography (China, India, Japan, South Korea, Australia, SEA, and Others). The Market Forecasts are Provided in Terms of Value (USD).

By Business Model

| Aggregator Model |

| Restaurant-to-Consumer Model |

| Hybrid / Cloud-Kitchen-Owned |

By Order Platform

| Mobile App |

| Website / Desktop |

| Conversational (Chatbot / Call) |

By Delivery Time Promise

| Standard Delivery (Above 30 min) |

| Express / Q-Commerce (≤30 min) |

By Consumer Segment

| Household Users |

| Office / Corporate |

| Students |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| South East Asia |

| Rest of the Asia-Pacific |

| By Business Model | Aggregator Model |

| Restaurant-to-Consumer Model | |

| Hybrid / Cloud-Kitchen-Owned | |

| By Order Platform | Mobile App |

| Website / Desktop | |

| Conversational (Chatbot / Call) | |

| By Delivery Time Promise | Standard Delivery (Above 30 min) |

| Express / Q-Commerce (≤30 min) | |

| By Consumer Segment | Household Users |

| Office / Corporate | |

| Students | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South East Asia | |

| Rest of the Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific food platform-to-consumer delivery market market in 2026?

The Asia-Pacific food platform-to-consumer delivery market size reached USD 0.75 trillion in 2026.

What growth rate is forecast for the sector through 2031?

The market is projected to expand at a 7.76% CAGR between 2026 and 2031.

Which geography is growing fastest?

Indonesia is advancing at an 8.10% CAGR, the highest among major regional economies.

Which delivery promise segment is expanding most quickly?

Express and quick-commerce orders under 30 minutes are growing at an 8.6% CAGR.

Why are platforms investing in dark kitchens?

Owned kitchens place inventory closer to demand, lower real estate dependency, and enable sub-30-minute fulfillment.

What key regulation is raising costs for gig-economy platforms?

New social-security mandates such as Singapore’s Platform Workers Act and Malaysia’s Gig Workers Bill are lifting per-order labor expenses.

Page last updated on: