Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

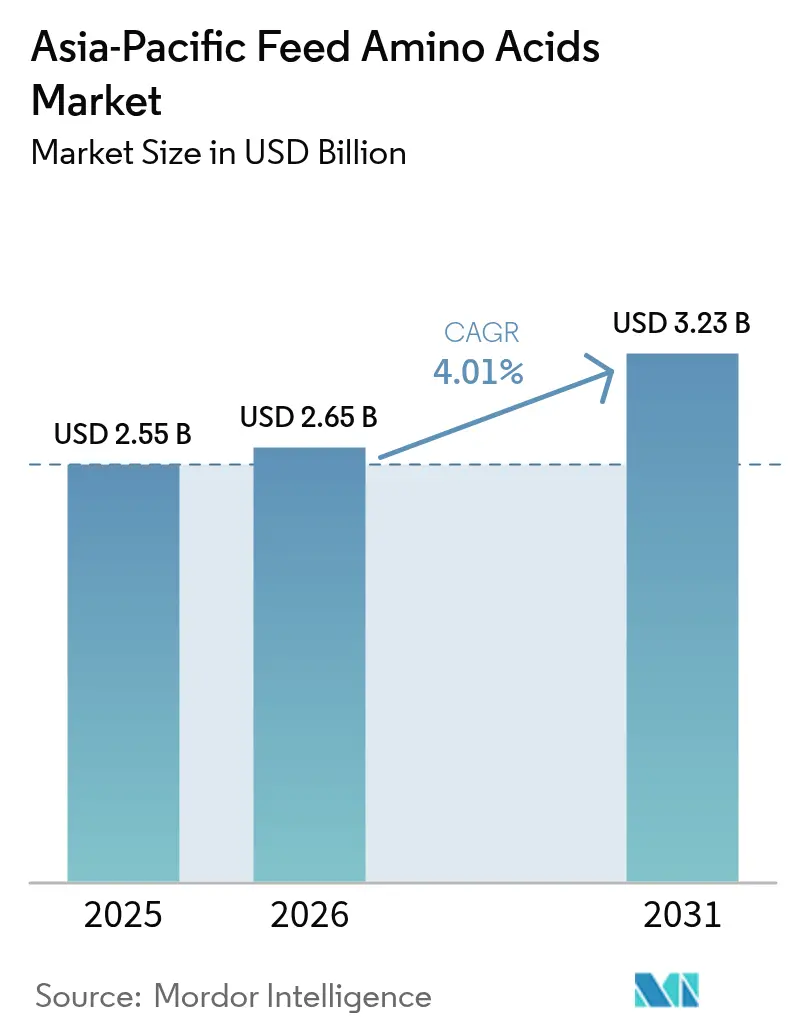

| Base Year Market Size (2025) | USD 2.55 Billion |

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

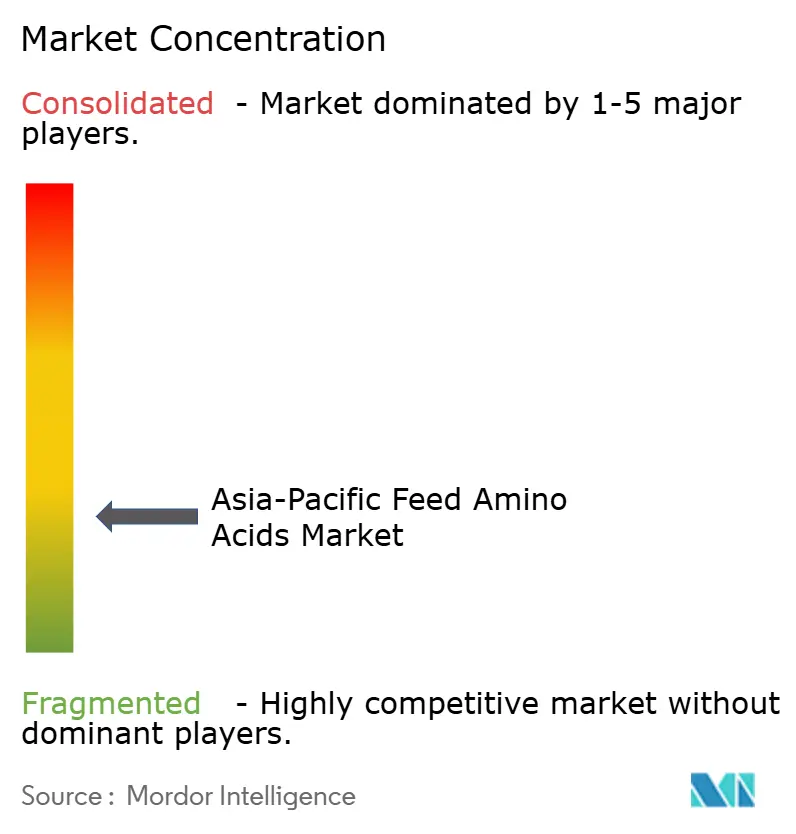

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Feed Amino Acids Market Analysis by Mordor Intelligence

The Asia-Pacific feed amino acids market size is expected to grow from USD 2.55 billion in 2025 to USD 2.65 billion in 2026 and is forecast to reach USD 3.23 billion by 2031 at 4.01% CAGR over 2026-2031. Sustained population growth, rising disposable incomes, and steady urbanization continue to lift per-capita meat and seafood intake, compelling feed manufacturers to fine-tune protein conversion efficiency with crystalline amino acids. Precision formulation software, wider domestic manufacturing capacity, and supportive environmental policies are converging to anchor a favorable demand outlook. At the same time, capacity rationalization among leading suppliers following CJ Group’s planned bio-division divestiture is likely to recalibrate competitive behavior and temper excessive price swings. Ongoing investments in fermentation efficiency and functional amino acid research continue to expand applications in aquaculture, poultry, and high-yield dairy operations.

Key Report Takeaways

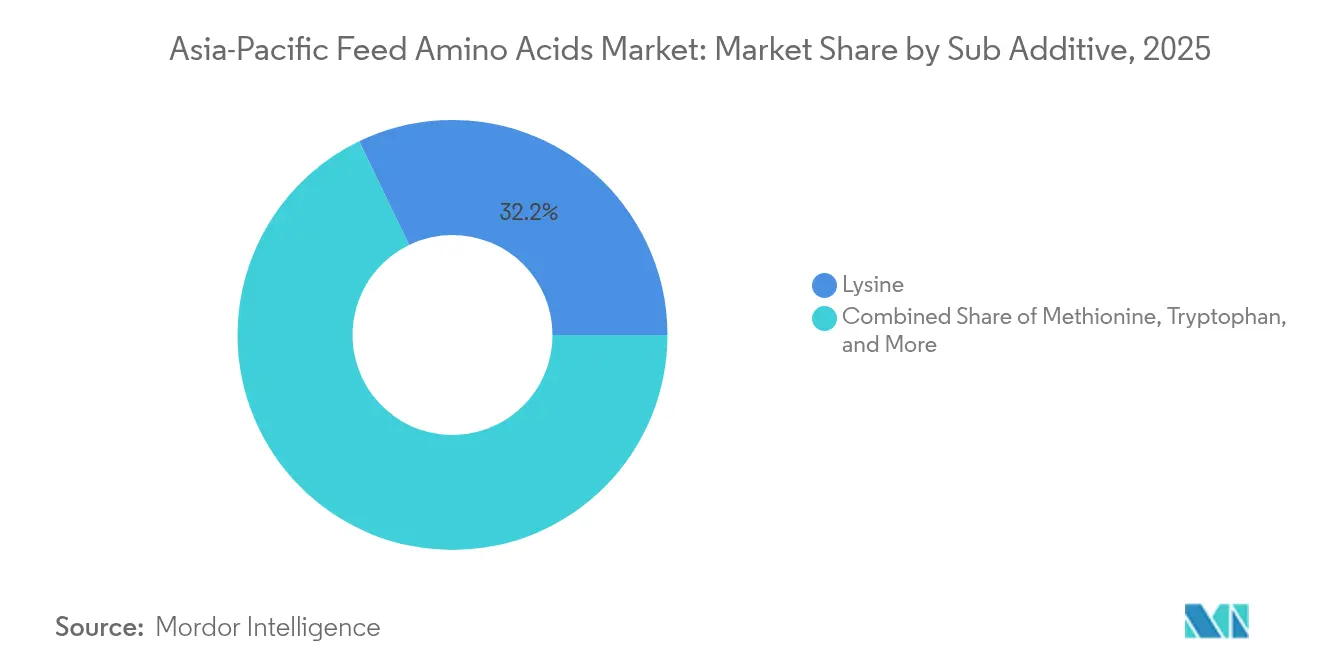

- By sub-additive, lysine captured 32.15% of the Asia-Pacific feed amino acids market share in 2025, while methionine is projected to expand at a 4.24% CAGR through 2031.

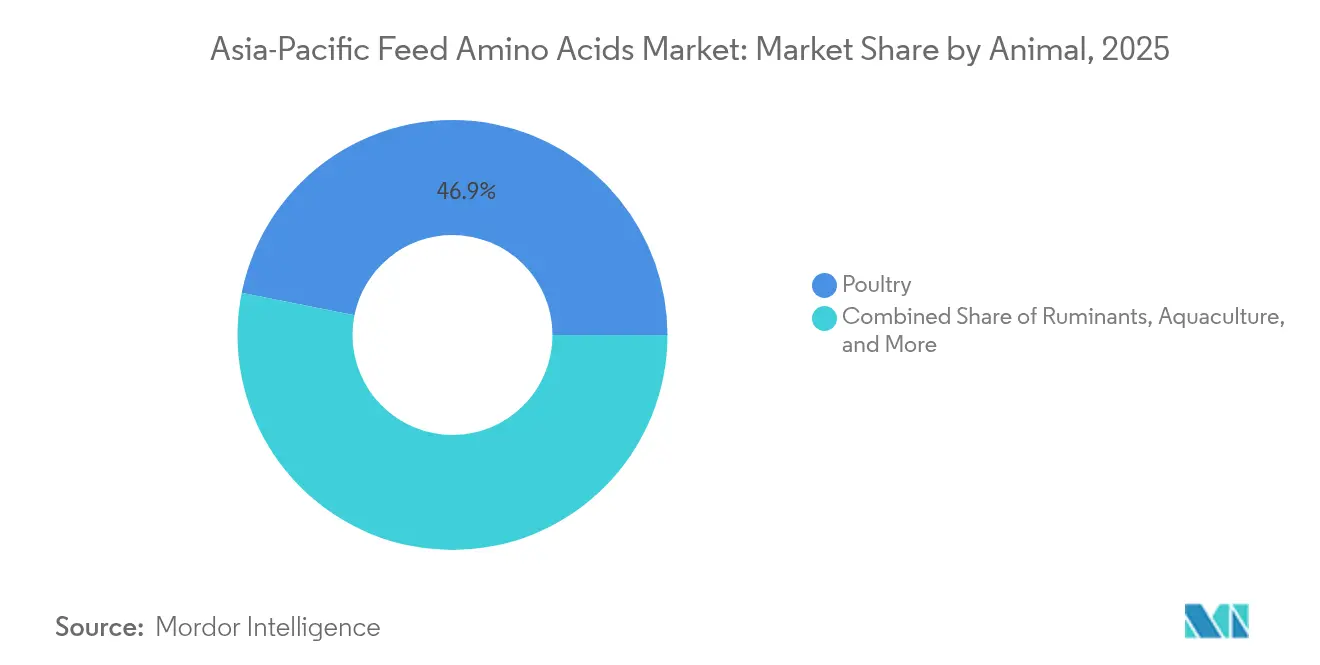

- By animal, poultry accounted for 46.85% of the Asia-Pacific feed amino acids market size in 2025, and the same segment is positioned for the fastest 4.58% CAGR to 2031.

- By geography, China accounted for a 32.30% revenue share in 2025, while Thailand is projected to register the highest CAGR of 4.82% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Feed Amino Acids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising poultry and swine meat production | +1.2% | China, Thailand, Vietnam, and Indonesia | Medium term (2-4 years) |

| Rapid expansion of aquaculture output and specialized aqua-feed plants | +0.8% | China, Vietnam, Thailand, and Indonesia | Long term (≥ 4 years) |

| Regulatory push for low-crude-protein diets to cut nitrogen emissions | +0.6% | China, Japan, and South Korea | Long term (≥ 4 years) |

| Large domestic amino-acid capacity additions improve cost access | +0.5% | China, India, and Thailand | Short term (≤ 2 years) |

| Precision nutrition tools accelerate the adoption of minor Amino Acids | +0.4% | Japan, South Korea, and Australia | Medium term (2-4 years) |

| Heat-stress mitigation diets in tropical Asia require higher functional Amino Acids | +0.3% | Thailand, Indonesia, Philippines, and Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Poultry and Swine Meat Production

Escalating demand for affordable animal protein positions poultry and swine as structural growth pillars for the Asia-Pacific feed amino acids market. The United States Department of Agriculture (USDA) projects gross domestic product expansion at 4–6% across major Southeast Asian countries, translating into dietary shifts toward white and red meat[1]Source: U.S. Department of Agriculture, “International Long-Term Projections Report,” usda.gov. With modern broiler lines capable of reaching 2 kg body weight in under 35 days, any marginal amino acid deficiency directly erodes feed-to-gain ratios and profit margins. National development plans in Vietnam and Indonesia target double-digit annual output gains, compelling integrators to embed higher lysine and threonine levels to support muscle deposition and carcass yield. Swine producers rebuilding herds after African Swine Fever outbreaks rely on precision amino acid supplementation to accelerate weight recovery while curbing nitrogen excretion penalties.

Rapid Expansion of Aquaculture Output and Specialized Aqua-Feed Plants

Asia-Pacific contributes roughly 90% of the global aquaculture harvest, and the sector’s feed volume now grows faster than terrestrial livestock. Species such as shrimp and high-value marine fish possess distinct amino acid profiles that mandate tailored formulations. The Chinese Ministry of Agriculture confirmed a 14% year-on-year surge in specialty aqua-feed output during 2025, far outstripping land-animal feed growth[2]Source: Ministry of Agriculture and Rural Affairs of the People’s Republic of China, “2025 National Feed Industry Statistics Bulletin,” moa.gov.cn. Shrimp diets, for instance, demand elevated methionine and taurine to support osmoregulation under intensive farming. Functional amino acids like tryptophan and arginine also enhance stress resilience and immunity in recirculating aquaculture systems.

Regulatory Push for Low-Crude-Protein Diets to Cut Nitrogen Emissions

China’s agricultural ecology codes enforce area-specific nitrogen caps, obliging producers to slash crude protein by 2–3 percentage points and offset with crystalline amino acids. Pilot projects registered under the national carbon-trading scheme documented 15–20% lower nitrogen excretion without performance loss when lysine, methionine, and threonine ratios were balanced precisely[3]Source: Ajinomoto Co. Inc., “AjiPro-L Environmental Assessment,” ajinomoto.com. Similar frameworks are rolling out in Japan and South Korea as part of net-zero roadmaps. Dairy farms adopting rumen-protected lysine (AjiPro-L) report up to 1 metric ton CO₂-e emission reduction per cow annually.

Large Domestic Amino-Acid Capacity Additions Improve Cost Access

Incremental nameplate capacity has come online in Hebei, Shandong, and Gujarat, aided by low-cost fermentation substrates and wastewater recycling technology. CJ Group’s assets, Evonik’s fully restored Singapore methionine plant, and Meihua Holdings’ corn-steep-liquor integration collectively shrink import reliance and freight exposure. Immediate freight savings and swifter order cycles widen usage among small and medium feed mills. The capacity surge also dilutes the risk of abrupt supply shocks, fostering more stable growth trajectories across the Asia-Pacific feed amino acids market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn/soy price volatility raises input costs for fermentation feedstocks | -0.4% | China, Thailand, and Vietnam | Short term (≤ 2 years) |

| Anti-dumping duties on exports create regional price spikes | -0.3% | China and Japan | Medium term (2-4 years) |

| High sulfate load in lysine-sulfate limits inclusion in ruminant premixes | -0.2% | Australia, India, and China | Long term (≥ 4 years) |

| Dust and endotoxin exposure at handling sites increases compliance costs | -0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corn/Soy Price Volatility Raises Input Costs for Fermentation Feedstocks

Fermentation economics hinge on stable dextrose and soy peptone prices. Climate-induced crop failures and competing biofuel mandates led to a jump in average corn futures during 2024, squeezing producer margins and forcing sporadic list-price hikes across the Asia-Pacific feed amino acids market. Smaller plants with spot-market procurement face the greatest exposure, promoting further consolidation into vertically integrated conglomerates. Substitution elasticity with lower-protein meals narrows when amino acid premiums inflate.

Anti-Dumping Duties on Exports Create Regional Price Spikes

The June 2025 United States investigation into Chinese L-lysine imports triggered precautionary stockpiling among Asian countries buyers and introduced new administrative hurdles for exporters. Subsequent safeguard petitions filed by Philippine authorities on imported methionine add another layer of uncertainty. Disparate duty rulings distort intra-regional price parity and complicate distributor inventory planning, collectively subtracting some points from CAGR potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Additive: Lysine Leads While Methionine Accelerates

Lysine retained a dominant 32.15% revenue share within the Asia-Pacific feed amino acids market in 2025 on the strength of corn-soy-based swine and poultry rations. The segment’s entrenched position stems from its role as the first limiting amino acid in prevalent basal diets, ensuring consistent baseline demand even when relative prices fluctuate. Despite this, methionine’s 4.24% CAGR forecast underscores shifting nutritional priorities. Rapid aquaculture scale-up and heat-stress abatement strategies in tropical broiler complexes require higher methionine densities to sustain oxidative balance and feather development. Evonik’s newly upgraded Singapore facility enhances regional methionine availability, compressing freight and lead times and thus amplifying uptake.

Threonine and tryptophan usage gains momentum through precision feeding tools that capture marginal performance lifts, particularly during disease-challenge windows. Specialty amino acids such as valine and isoleucine, once viewed as niche, now benefit from algorithm-driven least-cost formulations that validate their cost-to-benefit parity. Parallel advances in continuous fermentation and membrane filtration shorten cycle time, lowering the barrier to entry for regional newcomers.

By Animal: Poultry Dominates and Grow Fastest

Poultry commanded 46.85% of the Asia-Pacific feed amino acids market share in 2025, and the same segment is positioned for the fastest 4.58% CAGR to 2031, reflecting its unmatched feed conversion efficiency and swift production cycles. Modern genetics require precise essential amino acid ratios. Suboptimal levels of methionine or threonine can reduce daily gains by over 3% within a single flock rotation. Consequently, integrators allocate dedicated budget lines for crystalline amino acids to safeguard profitability. Layer segments increasingly fine-tune tryptophan dosages to stabilize egg mass under heat load, extending adoption beyond broilers.

Ruminant applications face technical constraints due to rumen degradation of amino acids, though protected forms like Ajinomoto's AjiPro-L demonstrate solutions for dairy and beef cattle operations. Swine operations continue steady amino acid adoption, driven by genetic improvements and intensive production systems requiring optimized nutrition programs. The segment evolution reflects broader trends toward precision animal nutrition and sustainable protein production systems.

Geography Analysis

China is projected to account for 32.30% of the value share in the Asia-Pacific feed amino acids market in 2025, maintaining its position as the central market in the region. High livestock inventories, government-mandated nitrogen caps, and formidable domestic manufacturing depth create a virtuous demand-supply feedback loop. The Ministry of Ecology and Environment’s green-livestock standards stipulate stepwise crude protein reductions, ensuring long-term demand for crystalline balancing. On the supply side, integrated corn-processing complexes in Hebei and Jilin sustain low unit costs, protecting domestic players from external price shocks. Yet bilateral trade disputes, especially the United States' antidumping probes against lysine, inject volatility into export channels, nudging producers toward diversification within Asian countries.

Thailand posts the swiftest trajectory, set to log a 4.82% CAGR through 2031. Government incentives for value-added poultry exports and large-scale shrimp-farm recovery underpin feed expansion. Newly commissioned amino acid formulators along the Eastern Economic Corridor shorten delivery cycles to feed mills clustered near coastal aquaculture hubs. Methionine already commands 30.8% of the local amino acid value pool, illustrating sophisticated diet architectures oriented toward heat-tolerance and export quality standards.

Japan and South Korea represent mature yet innovation-rich arenas. Stringent feed-additive registration under the Act on Safety Assurance and Quality Improvement of Feeds ensures premium product positioning. Carbon-credit pilots bundling rumen-protected lysine with verified emission reductions attract dairy cooperatives seeking Scope 3 decarbonization pathways.

Competitive Landscape

The Asia-Pacific feed amino acids market exhibits a fragmented structure. The major players/companies include Adisseo, Ajinomoto Co., Inc., SHV (Nutreco NV), Evonik Industries AG, and Archer Daniels Midland Co., supplemented by region-specific challengers. CJ Group’s exit plan for its bio division, priced at KRW 4.21 trillion (USD 3.16 billion), will likely realign share allocations once the deal concludes. Potential bidders cite the unit’s 11-country footprint and 1.2 million metric tons capacity as unparalleled scale advantages. Evonik’s completion of debottlenecking at its Singapore DL-methionine complex reinstates annual output, reinforcing its Asia-Pacific supply resilience. Ajinomoto leverages differentiated portfolios such as rumen-protected lysine and functional peptides, complemented by carbon-credit partnerships with dairy processors to craft a premium narrative.

Regional producers intensify innovation efforts. Beijing Shougang Technology’s steel-gas-fed single-cell protein project scales circular-economy credentials, whereas an Indian start-up in Gujarat pioneers continuous fermentation powered by solar-integrated bioreactors to slash energy intensity. Distributors like Nutreco and Prinova integrate formulation consultancy and on-farm monitoring sensors, seeking to lock in customer loyalty beyond commodity transactions. Regulatory scrutiny, especially over heavy-metal impurities and endotoxin benchmarks, raises entry barriers, indirectly favoring incumbents with established quality systems.

Competitive tactics now extend into sustainability certification, traceability platforms, and local-language technical helplines. Multinational companies are establishing regional application centers, as demonstrated by FrieslandCampina Ingredients' planned 2025 hub in Singapore, which will provide customized trial diets and efficient troubleshooting services. These moves shift the basis of competition from unit cost alone to holistic solution delivery, reinforcing customer stickiness and raising the strategic stakes in the Asia-Pacific feed amino acids market.

Asia-Pacific Feed Amino Acids Industry Leaders

Adisseo

Ajinomoto Co., Inc.

Evonik Industries AG

SHV (Nutreco NV)

Archer Daniels Midland Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The United States initiated antidumping investigations on L-lysine imports from China, potentially affecting trade flows and pricing dynamics across Asia-Pacific amino acid markets. This follows similar trade measures affecting other amino acids and demonstrates escalating trade tensions impacting the sector.

- September 2024: SK Pharmteco announced a USD 260 million investment to build a peptide and low-molecular-weight drug production facility in Sejong City, South Korea, featuring eight production lines and dedicated R&D capabilities. The facility will commence operations in late 2026 and create approximately 300 jobs, targeting growing demand for peptide-based therapies composed of amino acids.

- August 2024: Evonik has fully restored DL-methionine production at its Singapore facility and reported robust sales in the Animal Nutrition division across Asia. Additionally, the product carbon footprint of DL-methionine produced in Singapore has been reduced by 6%.

Asia-Pacific Feed Amino Acids Market Report Scope

Lysine, Methionine, Threonine, Tryptophan are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Australia, China, India, Indonesia, Japan, Philippines, South Korea, Thailand, Vietnam are covered as segments by Country.Additive

| By Sub Additive | Lysine |

| Methionine | |

| Threonine | |

| Tryptophan | |

| Other Amino Acids |

Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

Geography

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Philippines |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| Additive | By Sub Additive | Lysine | |

| Methionine | |||

| Threonine | |||

| Tryptophan | |||

| Other Amino Acids | |||

| Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| Geography | Australia | ||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Philippines | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms