Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

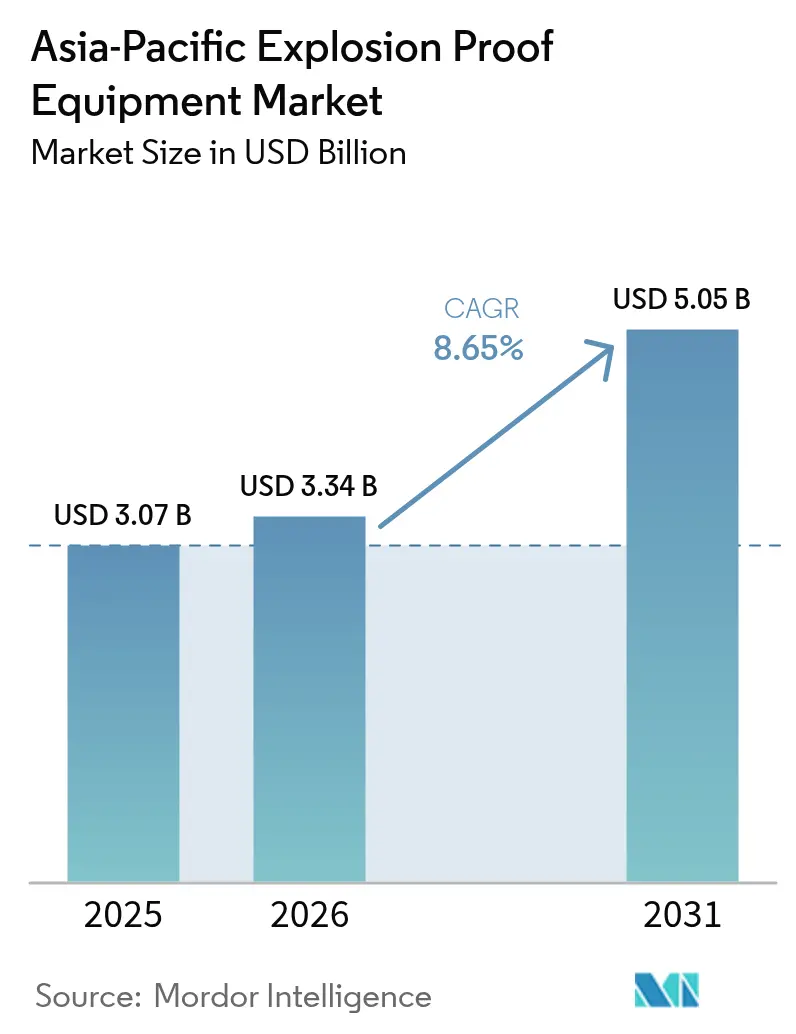

| Base Year Market Size (2025) | USD 3.07 Billion |

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 5.05 Billion |

| Growth Rate (2026 - 2031) | 8.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Explosion Proof Equipment Market Analysis by Mordor Intelligence

The Asia-Pacific explosion-proof equipment market size is expected to grow from USD 3.07 billion in 2025 to USD 3.34 billion in 2026 and is forecast to reach USD 5.05 billion by 2031 at 8.65% CAGR over 2026-2031. Heightened regulatory scrutiny, accelerating industrial automation, and rapid pharmaceutical capacity additions underpin this expansion. China’s manufacturing dominance and India’s large-scale greenfield projects provide a strong demand base, while oil and gas modernization, mining electrification, and food-grade safety mandates broaden the customer pool. Technology advances—especially intrinsic safety, pressurization, and Ethernet-APL connectivity—are reshaping buyer preferences, shifting value from purely mechanical flameproof designs toward digitally enabled, predictive-maintenance-ready solutions. Competitive intensity is moderate as global incumbents transition from hardware-centric to integrated digital offerings, while rising Chinese suppliers leverage cost advantages and local certifications to scale regionally. Supply chain cost spikes in copper and rare-earth magnets, coupled with shortages of IECEx-certified technicians, have tempered profit margins but not derailed long-term growth momentum.

Key Report Takeaways

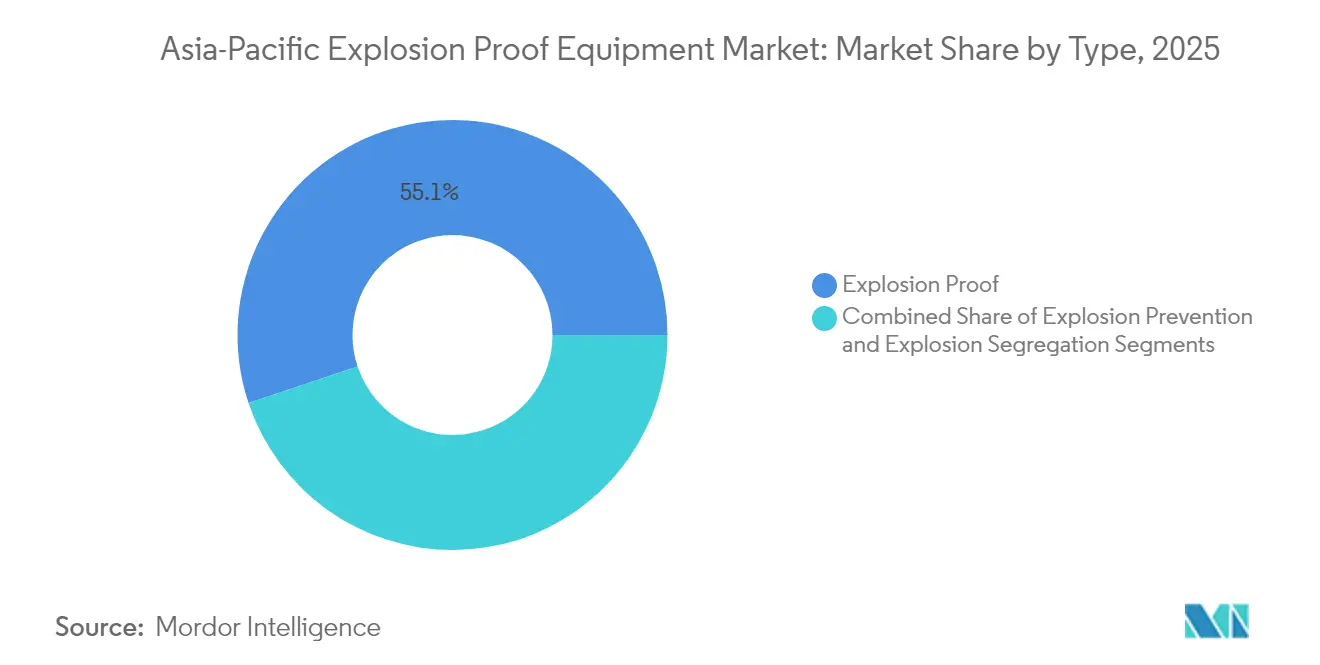

- By type, explosion-proof designs led with a 55.12% share of the Asia-Pacific explosion-proof equipment market in 2025, while prevention methods are projected to expand at a 10.05% CAGR through 2031.

- By zone, Zone 1 installations accounted for 33.45% of the Asia-Pacific explosion-proof equipment market size in 2025; Zone 20 applications are forecasted to grow at a 11.35% CAGR through 2031.

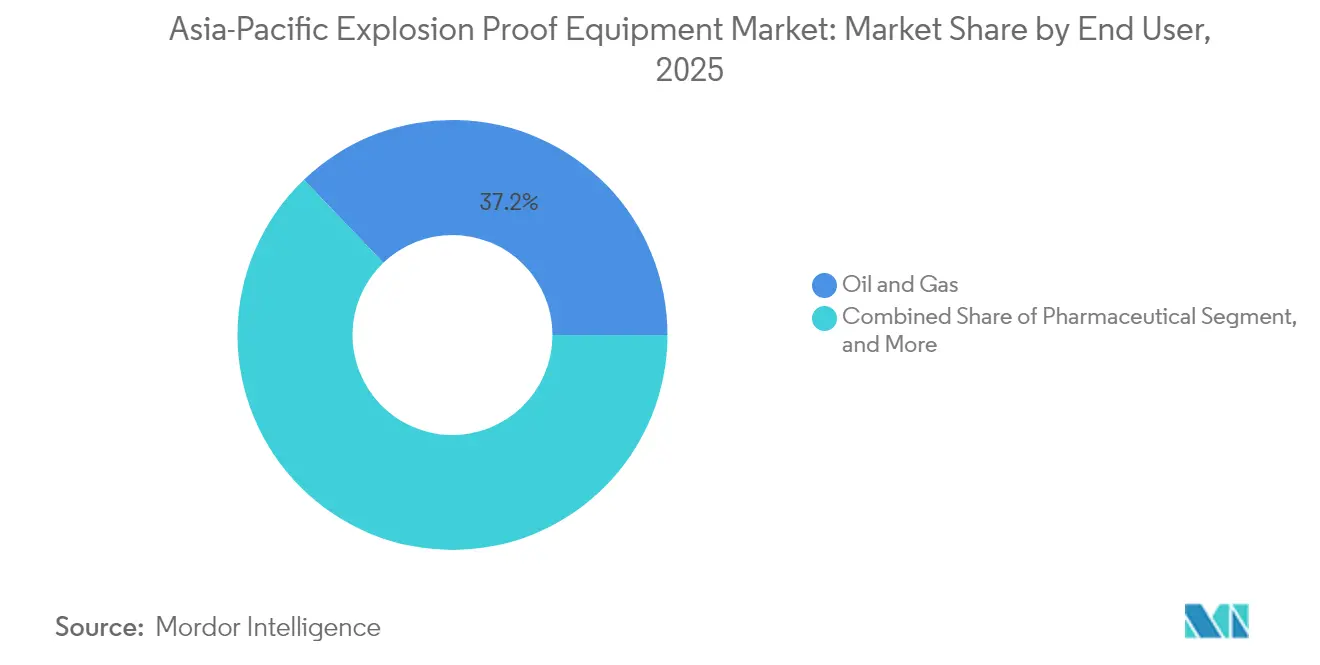

- By end user, the oil and gas sector accounted for 37.15% of revenue of the Asia-Pacific explosion-proof equipment market in 2025, whereas the pharmaceuticals sector is expected to register the fastest growth of 11.02% CAGR through 2031.

- By system, motors and drives held a 29.65% share of the Asia-Pacific explosion-proof equipment market size in 2025; however, automation and control systems are expected to rise at a 10.86% CAGR over the outlook period.

- By country, China dominated the Asia-Pacific explosion-proof equipment market, with a 38.05% revenue share in 2025. In contrast, India is poised to grow at a 10.92% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Explosion Proof Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter regulatory enforcement across hazardous zones (ATEX/IECEx, IEC 60079 series, China GB-3836 upgrade) | +2.1% | Global, with strongest impact in China, India, Southeast Asia | Medium term (2-4 years) |

| Rising oil, gas and mining capacity expansions in emerging Asian economies | +1.8% | Asia Pacific core, particularly Indonesia, Vietnam, Australia | Long term (≥ 4 years) |

| Accelerating shift toward explosion-proof LED lighting and smart sensors | +1.4% | Global, with early adoption in Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Rapid industrial automation driving demand for intrinsically-safe control systems | +1.6% | China, India, Thailand manufacturing hubs | Medium term (2-4 years) |

| Localisation of certification labs reducing approval lead-times | +0.9% | National, with gains in major industrial centers | Short term (≤ 2 years) |

| Booming Asia-Pacific pharmaceutical manufacturing clusters needing GMP-compliant Ex equipment | +1.2% | India, China, Singapore pharmaceutical corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Regulatory Enforcement Across Hazardous Zones

ATEX and IECEx compliance have expanded from a narrow focus on oil and gas to a broader mandate encompassing pharmaceuticals, food processing, and battery materials. China’s GB-3836 upgrade in 2024 imposed higher protection levels for Zone 0 and Zone 20, prompting widespread retrofits.[1]GB Standards Committee, “GB 3836 Explosive Atmospheres,” China National Standards, gb688.cn India’s PESO regime tightened import approvals, accelerating replacement cycles for legacy gear. Australia and New Zealand have aligned the ANZEx with IECEx, easing multi-country certifications for multinationals. The convergence reduces engineering complexity, enabling regional product platforms that lower development costs and accelerate time-to-market. As plants seek recertification of equipment installed before 2020, the Asia-Pacific explosion-proof equipment market records sizable repeat orders.

Rising Oil, Gas and Mining Capacity Expansions in Emerging Asian Economies

Indonesia’s Pertamina has earmarked USD 20 billion for upstream projects through 2030, necessitating robust flameproof motors, pressurized analyzer shelters, and Ex p ventilation skids.[2]Pertamina Corporate Strategy, “Upstream Investment Program 2024-2030,” Pertamina, pertamina.com Vietnam’s Long Son petrochemical hub and Australia’s critical minerals rush add large Zone 1 and Zone 20 footprints, respectively. Extended supply lines in offshore rigs and remote mines amplify the need for low-maintenance, condition-monitored Ex lighting and drives. Projects often bundle multi-system packages, such as motors, controls, cameras, and gas detectors, which boosts average order values and deepens vendor lock-in.

Accelerating Shift Toward Explosion-Proof LED Lighting and Smart Sensors

Energy policies and carbon targets prompt end users to switch from fluorescent fixtures, which consume 70% more power, to LED variants offering 100,000-hour lifespans. Integrated vibration, temperature, and gas sensors inside Ex luminaires feed data to cloud dashboards via LoRaWAN, cutting unscheduled downtime. Japanese and South Korean firms are pioneering explosion-proof IoT gateways that normalize multi-protocol sensor streams and push analytics to enterprise platforms, opening up service-revenue avenues. Payback periods of under two years fuel rapid capex sign-offs even for mid-sized factories.

Rapid Industrial Automation Driving Demand for Intrinsically-Safe Control Systems

Industry 4.0 projects in China, India, and Thailand require Ethernet-APL-ready PLCs inside Ex d enclosures that maintain high data rates without compromising safety. Pharmaceutical continuous-manufacturing lines necessitate dual compliance with IEC 60079 and GMP validation, which increases documentation complexity, favoring vendors offering digital twin models linked to certification files. In chemical export zones, government subsidies for smart factories offset 20-30% of automation capex, accelerating order volumes. As control logic shifts to edge devices, sales of compact Ex i I/O modules outpace traditional barrier boards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and installation cost of explosion-proof equipment | -1.3% | Global, particularly affecting smaller enterprises in emerging markets | Long term (≥ 4 years) |

| Shortage of certified Ex installation and maintenance talent | -0.9% | Asia Pacific emerging markets, rural industrial locations | Medium term (2-4 years) |

| Proliferation of counterfeit/non-certified devices eroding buyer confidence | -0.7% | China, India, Southeast Asian markets | Short term (≤ 2 years) |

| Volatile copper and rare-earth magnet prices inflating motor costs | -0.8% | Global supply chain impact, affecting all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Installation Cost of Explosion-Proof Equipment

Explosion-proof motors, drives, and control panels cost 150–300% more than their general-purpose equivalents. Additionally, certified installation, rigid metallic conduit, and pressurization hardware increase project budgets by an extra 40–60%.[3]ABB Motion, “Explosion-Proof Motors and Drives,” ABB, abb.com SMEs in emerging economies often defer upgrades until inspectors issue notices, causing demand spikes rather than steady growth. Currency swings against the USD raise import bills, especially for sensor and chipset components sourced from the U.S. and Europe. Financing gaps remain acute despite government credit lines, as the uptake among cash-constrained processors slows.

Shortage of Certified Ex Installation and Maintenance Talent

Fewer than 15,000 IECEx CoPC-qualified technicians serve the entire Asia-Pacific region, with most concentrated in metropolitan areas. Projects in hinterlands face multi-week delays as contractors fly in qualified personnel, inflating labor costs by 25–40%. Maintenance backlogs jeopardize equipment uptime, prompting some operators to run uncertified repairs that void warranties and regulatory approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Prevention Methods Gain Traction

Explosion-proof enclosures retained 55.12% of the Asia-Pacific explosion-proof equipment market share in 2025, driven by entrenched oil and gas usage. Still, intrinsic safety and pressurization drive a vigorous 10.05% CAGR through 2031, lifting their contribution to the Asia-Pacific explosion-proof equipment market size, particularly in data-intensive control rooms and sensor networks. Manufacturers exploit semiconductor miniaturization to embed higher power levels into Ex i circuits without exceeding thermal limits, broadening applicability to valve actuators and small motors. Pressurization systems are gaining ground in analyzer houses that handle multiple gas streams; centralized air-purge skids protect several cabinets simultaneously, reducing lifecycle costs compared to per-device enclosures. Encapsulation and powder-fill solutions carve out niches in high-voltage drives and precision instruments, prized for their contamination-free design, especially in clean-room pharmaceuticals.

Second-generation prevention solutions integrate micro-controllers that log pressure, temperature, and purge cycles, transmitting diagnostics to SCADA platforms. Firmware updates enable remote calibration, eliminating the need for site visits and ensuring audit readiness. Service models shift from parts replacement to outcome-based contracts guaranteeing leak-rate thresholds. Competitors are exploring additive-manufactured housings that optimize airflow and reduce weight by up to 25%, thereby lowering crane and footing costs during installation.

By Zone: Zone 1 Dominates While Zone 20 Shows Promise

Zone 1 retained 33.45% revenue as operators prioritized equipment for areas with frequent gas-vapor presence, sustaining steady retrofits in mature refineries. Conversely, dust-heavy Zone 20 posts the market’s fastest 11.35% CAGR, propelled by tablet coating, flour milling, and battery-materials grinding lines that redefine hazardous-area priorities. Several lithium-processing plants in Australia specify hybrid Ex t/Ex p protection for ball mills, which has spurred innovations in dual-rating designs. Equipment makers develop universal mounting kits compliant with both IEC 60079-31 (dust) and 60079-2 (pressurization), enabling single-SKU stocking across varied plant zones.

Zone 0 remains a specialist zone, limited to constant-exposure environments, such as storage tank interiors. New ultrasonic thickness sensors rated Ex ia allow in-service tank-roof inspections, reducing hot-work permits and downtime. Zone 2 retains widespread appeal where intermittent risk suffices; OEMs focus on cost-optimized enclosures that balance compliance and price to counter grey-market imports.

By End User: Pharmaceuticals Accelerate Past Traditional Leaders

Oil and gas sustained 37.15% revenue in 2025, but green-field capex is tilting toward LNG regasification and refinery petrochemicals, which require advanced control room pressurization and flameproof diesel generators. Pharmaceuticals stride ahead at an 11.02% CAGR, lifting their slice of the Asia-Pacific explosion-proof equipment market size through 2031. Batch-to-continuous manufacturing migration and solvent-rich environments necessitate the broad adoption of stainless-steel, easy-clean Ex devices that can withstand 24/7 operation and rigorous validation. Regulatory audits now extend to auxiliary systems, such as HVAC and weight-check stations, thereby widening the scope of equipment per site.

Mining contributes a steady volume, especially for flameproof longwall shearers and intrinsically safe communication nodes in coal and hard rock mining scenes. Food processors upgrade bucket elevators and silo aeration systems with dust-ignition-proof gear, driven by insurance premium discounts tied to IECEx compliance. Growth in fine chemicals and bio-based materials fuels demand for Ex reactors and spray dryers, adding another layer of opportunity for multidisciplinary vendors.

By System: Automation Leads Digital Transformation

Motors and drives accounted for 29.65% of 2025 revenue, yet face margin pressure due to copper cost volatility. OEMs respond by embedding temperature and vibration sensors into motor windings, enabling predictive analytics via cloud dashboards. Permanent-magnet synchronous motors with IP66 flameproof housings reduce energy consumption by 8–12%, justifying the higher upfront cost in continuous processes. Automation and control systems outpace all others at an 10.86% CAGR, propelled by Ethernet-APL adoption that extends 10 Mbit/s data rates into Zone 0 intrinsically safe loops.

Surveillance and monitoring lines incorporate 4K day-night cameras inside Ex d housings with AI edge chips that flag unsafe behaviors, reducing operator exposure. Advanced gas-detection arrays integrate laser dispersion and electrochemical technologies, providing ppm-level accuracy for hydrogen and ammonia detection. Power supply modules utilize conformal coatings and encapsulation to meet the requirements of high-humidity, tropical installations in Southeast Asia. Lighting systems benefit from LED price declines and universal-input drivers that accept 100–277 VAC, thereby simplifying regional inventory management.

Geography Analysis

China maintained a commanding 38.05% share of the Asia-Pacific explosion-proof equipment market in 2025, driven by its vast petrochemical, mining, and pharmaceutical clusters. Harmonization of GB-3836 with IECEx lowers export friction, enabling domestic suppliers such as Warom to win overseas contracts. Provincial subsidies cover up to 15% of capex for safety upgrades in chemical parks, stimulating bulk orders for Ex motors and IoT sensors. Carbon-neutrality goals trigger investment in Ex equipment for hydrogen electrolyzers and battery-recycling centers.

India is the growth pacesetter with an 10.92% CAGR through 2031. Pharmaceutical mega-parks in Telangana and Gujarat require comprehensive GMP documentation packages, favoring global brands with validated device libraries. PESO’s stricter import checks are spurring localized assembly under the Make-in-India initiative, with foreign OEMs forming joint ventures to shorten lead times. Coal and iron-ore mechanization projects in Jharkhand and Odisha require flameproof conveyors and intrinsically safe signaling networks, broadening vendor portfolios beyond process industries.

Japan and South Korea retain mature, high-specification niches in semiconductor chemicals and offshore wind power, emphasizing explosion-proof systems with digital twins for remote islands. Australia’s critical minerals boom drives demand for transportable, pressurized substations and wireless Ex sensors that can withstand abrasive dust and 50 °C ambient temperatures. Across Southeast Asia, Indonesia, Vietnam, and Thailand are accelerating industrial estate expansions; local governments are coupling FDI incentives with mandatory IECEx compliance, thereby expanding the addressable demand for mid-tier suppliers.

Competitive Landscape

The Asia-Pacific explosion-proof equipment market is moderately fragmented, with the top five players collectively holding roughly 35–40% of the revenue, leaving space for regional challengers. European and U.S. majors retain leadership in automation, analytics, and high-throughput drives, but Chinese vendors dominate the low-to-mid-end market for lighting, junction boxes, and cable glands through aggressive pricing and rapid GB/IECEx dual approvals. Digital differentiation now outweighs metal thickness: suppliers embed cloud gateways, edge AI, and blockchain-verified certification files, commanding 10–20% price premiums despite material cost inflation.

Strategic moves underscore this pivot. ABB rolled out Ethernet-APL-enabled variable frequency drives with SIL2 safety layers, targeting solvent recovery towers and continuous API production lines. Pepperl+Fuchs partnered with WANTAI to create 5G intrinsically safe routers for underground mines, merging explosion protection with ultra-low-latency communication. Eaton boosted Thai motor capacity by 25%, hedging against single-country supply risk while leveraging ASEAN free-trade benefits.

Patent filings related to explosion-proof IoT devices surged 340% between 2022 and 2024, signaling an intensification of the arms race for wireless sensor networks, power-harvesting circuits, and AI-assisted safety analytics. M&A activity concentrates on niche specialists: larger vendors acquire firmware houses and analytics start-ups to shorten time-to-solution and broaden recurring-revenue pools. Meanwhile, counterfeit clampdown initiatives utilize QR-code tracking, but grey markets persist, prompting brand owners to shift from part to module sales, where tampering is more difficult.

Asia-Pacific Explosion Proof Equipment Industry Leaders

ABB Ltd.

Eaton Corporation plc

R. Stahl AG

Pepperl+Fuchs SE

Warom Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Siemens announced a USD 25 million investment to establish a new explosion-proof automation systems manufacturing facility in Pune, India, targeting the growing pharmaceutical and chemical sectors. The facility will focus on the development of intrinsically safe control systems and smart sensor production, with an expected operational capacity by Q2 2026.

- September 2025: ABB has completed the acquisition of Jiangsu Explosion-Proof Electric, a Chinese manufacturer of explosion-proof motors, for USD 180 million, expanding its presence in the Asia-Pacific market and adding specialized mining equipment capabilities. The acquisition includes three manufacturing facilities, strengthening ABB's position in Zone 20-22 dust explosion protection applications.

- September 2025: Pepperl+Fuchs launched its next-generation Ethernet-APL explosion-proof communication systems in Singapore, featuring integrated cybersecurity protocols and 5G connectivity for hazardous area applications. The product line targets pharmaceutical and petrochemical facilities requiring high-speed data transmission with intrinsic safety certification.

- August 2025: Warom Technology invested USD 30 million in expanding its Zhejiang manufacturing complex, adding 50,000 square meters of production space dedicated to smart explosion-proof lighting systems. The expansion includes automated assembly lines and testing facilities for LED-based explosion-proof fixtures with IoT capabilities.

- August 2025: Honeywell has established a strategic partnership with the Indian pharmaceutical giant Cipla to develop GMP-compliant, explosion-proof equipment specifically for continuous manufacturing processes. The collaboration involves a joint R&D investment of USD 15 million over three years.

- July 2025: Eaton opened its largest Asia-Pacific explosion-proof equipment testing center in Bangkok, Thailand, providing comprehensive IECEx, ATEX, and local certification services. The USD 12 million facility reduces regional certification timelines by 40% and supports the expansion of the Southeast Asian market.

Asia-Pacific Explosion Proof Equipment Market Report Scope

An explosion-proof equipment is an explosion or flameproof equipment that is sealed and rugged, so that it does not ignite a dangerous atmosphere in spite of any flames or explosions within. The market is defined by the revenue accrued by the adoption of various types of explosion-proof equipment across end users in the Asia-Pacific region.

The market is segmented by type (explosion proof, explosion prevention, and explosion segregation), zone (zone 0, zone 20, zone 1, zone 21, zone 2, and zone 22), end user (pharmaceutical, chemical and petrochemical, energy and power, mining, food processing, oil and gas, and other end users), system (power supply system, material handling, motor, automation system, surveillance system, and other systems), and country (China, India, Japan, and the Rest of Asia-Pacific). The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Type

| Explosion Proof (Flameproof/Ex d) |

| Explosion Prevention (Intrinsic Safety/Ex i, Pressurisation/Ex p) |

| Explosion Segregation (Encapsulation/Ex m, Powder-filling/Ex q) |

By Zone

| Zone 0 |

| Zone 1 |

| Zone 2 |

| Zone 20 |

| Zone 21 |

| Zone 22 |

By End User

| Oil and Gas |

| Chemical and Petrochemical |

| Energy and Power |

| Mining |

| Pharmaceutical |

| Food Processing |

| Other End Users |

By System

| Power Supply Systems (Transformers, Switchgear) |

| Material Handling (Hoists, Conveyors) |

| Motors and Drives |

| Automation and Control Systems (PLC, SCADA) |

| Surveillance and Monitoring (Cameras, Gas Detectors) |

| Lighting Systems (LED, Fluorescent) |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Rest of Asia Pacific |

| By Type | Explosion Proof (Flameproof/Ex d) |

| Explosion Prevention (Intrinsic Safety/Ex i, Pressurisation/Ex p) | |

| Explosion Segregation (Encapsulation/Ex m, Powder-filling/Ex q) | |

| By Zone | Zone 0 |

| Zone 1 | |

| Zone 2 | |

| Zone 20 | |

| Zone 21 | |

| Zone 22 | |

| By End User | Oil and Gas |

| Chemical and Petrochemical | |

| Energy and Power | |

| Mining | |

| Pharmaceutical | |

| Food Processing | |

| Other End Users | |

| By System | Power Supply Systems (Transformers, Switchgear) |

| Material Handling (Hoists, Conveyors) | |

| Motors and Drives | |

| Automation and Control Systems (PLC, SCADA) | |

| Surveillance and Monitoring (Cameras, Gas Detectors) | |

| Lighting Systems (LED, Fluorescent) | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific explosion proof equipment market by 2031?

The market is expected to reach USD 5.05 billion by 2031, expanding at a 8.65% CAGR.

Which segment is growing fastest within the region?

Automation and control systems are forecast to rise at an 10.86% CAGR, driven by Industry 4.0 adoption.

Why is pharmaceutical manufacturing boosting demand for explosion-proof equipment?

Solvent-rich processes and GMP validation mandates require Ex-rated motors, controls, and sensors that ensure both safety and hygiene compliance.

How do evolving regulations influence purchasing decisions?

Stricter ATEX, IECEx, GB-3836, and PESO rules force operators to replace or upgrade legacy equipment, driving steady, compliance-led orders.

Which country offers the biggest growth runway after China?

India is set to record an 10.92% CAGR through 2031, backed by pharma clusters, oil and gas infrastructure, and mining modernization.

How are vendors differentiating their offerings?

Suppliers integrate IoT sensors, Ethernet-APL connectivity, and cloud analytics into traditional flameproof or intrinsic-safety hardware to deliver predictive-maintenance and compliance documentation services.

Page last updated on: